Business Finance: Cost Calculation and Investment Appraisal Techniques

Added on 2023-06-11

23 Pages5384 Words394 Views

BUSINESS FINANCE

Contents:

INTRODUCTION...........................................................................................................................3

Case Study 1:...................................................................................................................................3

Part A...............................................................................................................................................3

1.Calculation of contribution per unit:...................................................................................3

2.Calculation of breakeven point in units and breakeven sales:.............................................3

3.Calculation of margin of safety:..........................................................................................4

4.Calculation of number of units sold:...................................................................................5

5.Preparation of memo suggesting the finance manager the importance of contribution:.....5

6.Calculation of profit using marginal and absorption costing and reconciliation between

them:.......................................................................................................................................6

Part B...............................................................................................................................................8

1.Importance of Standard Costing and Variance Analysis:....................................................8

2.Calculation of material and labour variance along with comment on them:.......................8

3.Preparation of budget for controlling the operations:........................................................10

CONCLUTION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Case Study 2:.................................................................................................................................14

INTRODUCTION.........................................................................................................................14

Part A.............................................................................................................................................14

1.Payback period:.................................................................................................................14

2.Net present value:..............................................................................................................15

3.Internal rate of return:........................................................................................................16

4.Advice regarding suitability of the project:.......................................................................18

Part B.............................................................................................................................................18

1.Risk assessment of Omega limited using accounting ratios:.............................................18

2.Identification and explanation on non-finance performance indicators:...........................20

3.Impact of pricing policy on the performance of the business:..........................................20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION...........................................................................................................................3

Case Study 1:...................................................................................................................................3

Part A...............................................................................................................................................3

1.Calculation of contribution per unit:...................................................................................3

2.Calculation of breakeven point in units and breakeven sales:.............................................3

3.Calculation of margin of safety:..........................................................................................4

4.Calculation of number of units sold:...................................................................................5

5.Preparation of memo suggesting the finance manager the importance of contribution:.....5

6.Calculation of profit using marginal and absorption costing and reconciliation between

them:.......................................................................................................................................6

Part B...............................................................................................................................................8

1.Importance of Standard Costing and Variance Analysis:....................................................8

2.Calculation of material and labour variance along with comment on them:.......................8

3.Preparation of budget for controlling the operations:........................................................10

CONCLUTION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Case Study 2:.................................................................................................................................14

INTRODUCTION.........................................................................................................................14

Part A.............................................................................................................................................14

1.Payback period:.................................................................................................................14

2.Net present value:..............................................................................................................15

3.Internal rate of return:........................................................................................................16

4.Advice regarding suitability of the project:.......................................................................18

Part B.............................................................................................................................................18

1.Risk assessment of Omega limited using accounting ratios:.............................................18

2.Identification and explanation on non-finance performance indicators:...........................20

3.Impact of pricing policy on the performance of the business:..........................................20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION

Business finance simply means managing the finance of the organisation in an effective

manner so the funds of the business can’t be misused. It is important for the company to hire

smart personnel in the finance department having sufficient knowledge of funds and their

treatment so that effective utilisation can be carried out. This report consists of two different case

study relating to cost calculation and investment appraisal techniques to judge the viability of the

project. (Al Dahdah, 2022).

Case Study 1:

Part A

1.Calculation of contribution per unit:

It can also be defined as profit on the sales of one unit and after subtracting all variable

expenses the amount is come is called as contribution. This detail is helpful to identify the

minimum possible price at which to sell the good.

Contribution per unit = sales per unit – variable cost per unit

= £120 – £50

= £70 per unit

Now, it can show that the sales per unit is £120 and variable expense is £50 per unit and the

contribution of the Lobelia Ltd company is £70 per unit.

2.Calculation of breakeven point in units and breakeven sales:

This is the most important concept to measure that weights the expenses of a new

company, goods and service against the unit of the selling price to identify the point at which it

will break even. Basically, it is the stage of sales where a total of fixed cost and variable cost is

equals to total sales revenue. On the other it can also say that the break- even point is a stage

where the business neither create a profit nor a loss. In simple words break- even point is an

amount of revenue that cover whole fixed and variable expenses. If company having a lower

sale, then it will show the low performance in break-even point. But if the revenue of the

company is high then break-even point, then it creates profit but after considering all expenses

(Álvarez‐Herránz, Lagos, and Balsalobre‐Lorente, 2018).

Simplification of Break- even point:

Business finance simply means managing the finance of the organisation in an effective

manner so the funds of the business can’t be misused. It is important for the company to hire

smart personnel in the finance department having sufficient knowledge of funds and their

treatment so that effective utilisation can be carried out. This report consists of two different case

study relating to cost calculation and investment appraisal techniques to judge the viability of the

project. (Al Dahdah, 2022).

Case Study 1:

Part A

1.Calculation of contribution per unit:

It can also be defined as profit on the sales of one unit and after subtracting all variable

expenses the amount is come is called as contribution. This detail is helpful to identify the

minimum possible price at which to sell the good.

Contribution per unit = sales per unit – variable cost per unit

= £120 – £50

= £70 per unit

Now, it can show that the sales per unit is £120 and variable expense is £50 per unit and the

contribution of the Lobelia Ltd company is £70 per unit.

2.Calculation of breakeven point in units and breakeven sales:

This is the most important concept to measure that weights the expenses of a new

company, goods and service against the unit of the selling price to identify the point at which it

will break even. Basically, it is the stage of sales where a total of fixed cost and variable cost is

equals to total sales revenue. On the other it can also say that the break- even point is a stage

where the business neither create a profit nor a loss. In simple words break- even point is an

amount of revenue that cover whole fixed and variable expenses. If company having a lower

sale, then it will show the low performance in break-even point. But if the revenue of the

company is high then break-even point, then it creates profit but after considering all expenses

(Álvarez‐Herránz, Lagos, and Balsalobre‐Lorente, 2018).

Simplification of Break- even point:

Break-even point is a calculation of sustenance and the lesser the quantity of break-even, the

good it is for the business.

Here is formula to calculate break-even point and Break-even sales:

Break-even point

= Fixed cost / (sales per unit – variable cost per unit)

Break-even point

= £700000 / (£120 - £50)

= £700000 / £70

= £10000 units

It clearly shows that the above formula shows the calculation of break-even point in this fixed

per unit cost is divide by the contribution per unit and the value of fixed cost is given £700000

and Contribution per unit is calculated in above point is £70.

Break- even sales in %

= Fixed cost / Contribution margin

Break- even sales

= £700000 / £2800000 *100

= 25 %

From the above calculation it clearly shows that the break-even sales is 25 % and if it calculate in

units then its show the same unit of breakeven point that is £70.

3.Calculation of margin of safety:

In this concept of margin of safety, it shows the difference between the both current sales

level and the break-even sales. It shows the stage of safety that the business appreciates before

occurring losses means decline below the break-even stage (Benton, 2022).

Clarification of Margin of safety:

It calculates the risk of the company and if margin of safety is higher than its good for the

business.

Here is formula to calculate margin of safety:

Margin of safety (MOS)

= Budgeted sales – Break-even point / budgeted sales * 100

= £40000 units - £10000 units / £40000 units *100

= £30000 units / £40000 units *100

good it is for the business.

Here is formula to calculate break-even point and Break-even sales:

Break-even point

= Fixed cost / (sales per unit – variable cost per unit)

Break-even point

= £700000 / (£120 - £50)

= £700000 / £70

= £10000 units

It clearly shows that the above formula shows the calculation of break-even point in this fixed

per unit cost is divide by the contribution per unit and the value of fixed cost is given £700000

and Contribution per unit is calculated in above point is £70.

Break- even sales in %

= Fixed cost / Contribution margin

Break- even sales

= £700000 / £2800000 *100

= 25 %

From the above calculation it clearly shows that the break-even sales is 25 % and if it calculate in

units then its show the same unit of breakeven point that is £70.

3.Calculation of margin of safety:

In this concept of margin of safety, it shows the difference between the both current sales

level and the break-even sales. It shows the stage of safety that the business appreciates before

occurring losses means decline below the break-even stage (Benton, 2022).

Clarification of Margin of safety:

It calculates the risk of the company and if margin of safety is higher than its good for the

business.

Here is formula to calculate margin of safety:

Margin of safety (MOS)

= Budgeted sales – Break-even point / budgeted sales * 100

= £40000 units - £10000 units / £40000 units *100

= £30000 units / £40000 units *100

= 75%

The above calculation show margin of safety is 75% and the budgeted sales of the company is

already given £40000 but the break-even point is calculated in above point that is £10000.

4.Calculation of number of units sold:

This concept is asked to calculate how much unit sold is needed to gain £700000 in a year

that means they want required sales unit. Here is one formula to calculate the desired profit of the

firm:

Required sales units

= fixed cost + target profit / Contribution margin per unit

= £700000 + £700000 / £70 units

= £1400000 / £70 units

= £20000 units

In the above formulation of required sales unit, it states that company need to sold £20000 units

want to earn a profit of £700000.

5.Preparation of memo suggesting the finance manager the importance of contribution:

Importance of contribution

It assists the company to know the contribution of different company lines and or

different goods and services. It also helps to know the strength and weakness of the company or

the product also. It used to measure the profit into the business after selling the goods and

services (Busch, Domeij, and Madera, 2022).

Suggestion how contribution margin helps to take business decisions:

contribution margin is a strong decision making and budgeting tools that management

accounting objective and superior utilize to take decision making procedure. Here are some uses

of contribution margin for the business decision making: Fixed minimum sale price its best

technique to target selling price it will cover both fixed and variable expenses, It permit to draw a

profit volume chart to know the position of the business that the company will be in a profitable

situation or not because of the chart it easy to understand the profit position (Clifton, 2018).

How contribution affects margin of safety

In the above formula of break-even point show that the fixed cost / contribution margin means if

contribution margin is high or less then it affects the value of break-even point and because of

The above calculation show margin of safety is 75% and the budgeted sales of the company is

already given £40000 but the break-even point is calculated in above point that is £10000.

4.Calculation of number of units sold:

This concept is asked to calculate how much unit sold is needed to gain £700000 in a year

that means they want required sales unit. Here is one formula to calculate the desired profit of the

firm:

Required sales units

= fixed cost + target profit / Contribution margin per unit

= £700000 + £700000 / £70 units

= £1400000 / £70 units

= £20000 units

In the above formulation of required sales unit, it states that company need to sold £20000 units

want to earn a profit of £700000.

5.Preparation of memo suggesting the finance manager the importance of contribution:

Importance of contribution

It assists the company to know the contribution of different company lines and or

different goods and services. It also helps to know the strength and weakness of the company or

the product also. It used to measure the profit into the business after selling the goods and

services (Busch, Domeij, and Madera, 2022).

Suggestion how contribution margin helps to take business decisions:

contribution margin is a strong decision making and budgeting tools that management

accounting objective and superior utilize to take decision making procedure. Here are some uses

of contribution margin for the business decision making: Fixed minimum sale price its best

technique to target selling price it will cover both fixed and variable expenses, It permit to draw a

profit volume chart to know the position of the business that the company will be in a profitable

situation or not because of the chart it easy to understand the profit position (Clifton, 2018).

How contribution affects margin of safety

In the above formula of break-even point show that the fixed cost / contribution margin means if

contribution margin is high or less then it affects the value of break-even point and because of

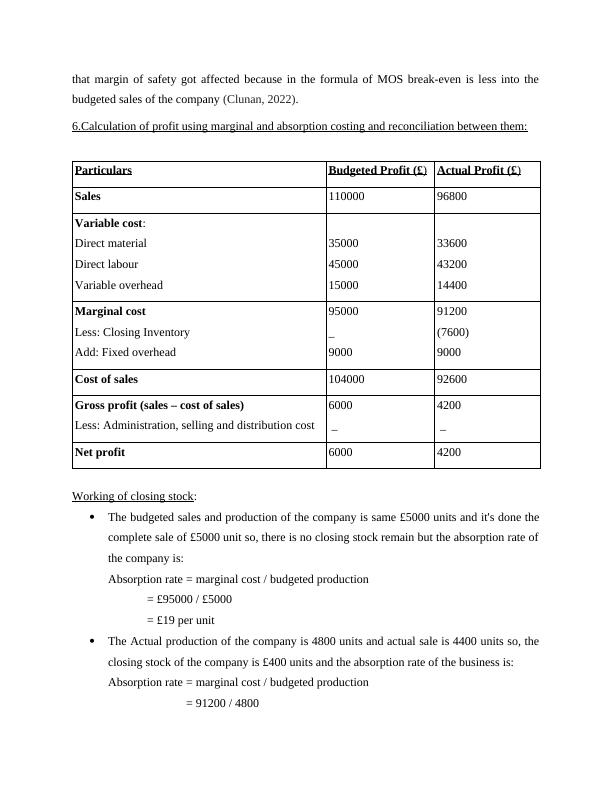

that margin of safety got affected because in the formula of MOS break-even is less into the

budgeted sales of the company (Clunan, 2022).

6.Calculation of profit using marginal and absorption costing and reconciliation between them:

Particulars Budgeted Profit (£) Actual Profit (£)

Sales 110000 96800

Variable cost:

Direct material

Direct labour

Variable overhead

35000

45000

15000

33600

43200

14400

Marginal cost

Less: Closing Inventory

Add: Fixed overhead

95000

_

9000

91200

(7600)

9000

Cost of sales 104000 92600

Gross profit (sales – cost of sales)

Less: Administration, selling and distribution cost

6000

_

4200

_

Net profit 6000 4200

Working of closing stock:

The budgeted sales and production of the company is same £5000 units and it's done the

complete sale of £5000 unit so, there is no closing stock remain but the absorption rate of

the company is:

Absorption rate = marginal cost / budgeted production

= £95000 / £5000

= £19 per unit

The Actual production of the company is 4800 units and actual sale is 4400 units so, the

closing stock of the company is £400 units and the absorption rate of the business is:

Absorption rate = marginal cost / budgeted production

= 91200 / 4800

budgeted sales of the company (Clunan, 2022).

6.Calculation of profit using marginal and absorption costing and reconciliation between them:

Particulars Budgeted Profit (£) Actual Profit (£)

Sales 110000 96800

Variable cost:

Direct material

Direct labour

Variable overhead

35000

45000

15000

33600

43200

14400

Marginal cost

Less: Closing Inventory

Add: Fixed overhead

95000

_

9000

91200

(7600)

9000

Cost of sales 104000 92600

Gross profit (sales – cost of sales)

Less: Administration, selling and distribution cost

6000

_

4200

_

Net profit 6000 4200

Working of closing stock:

The budgeted sales and production of the company is same £5000 units and it's done the

complete sale of £5000 unit so, there is no closing stock remain but the absorption rate of

the company is:

Absorption rate = marginal cost / budgeted production

= £95000 / £5000

= £19 per unit

The Actual production of the company is 4800 units and actual sale is 4400 units so, the

closing stock of the company is £400 units and the absorption rate of the business is:

Absorption rate = marginal cost / budgeted production

= 91200 / 4800

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Corporate Finance: Cost Estimating and Investment Assessment Methodologieslg...

|11

|2681

|456

Business Finance: Cost Estimation and Investment Assessment Approacheslg...

|12

|2814

|301

Standard Costing System and Variance Analysis in Business Financelg...

|12

|3208

|189

Business Finance Case Study 1: Contribution, Break Even, Margin of Safety, Profit, Costing Methods, Variance Analysis, Budgetinglg...

|12

|2611

|161

Business Finance: Calculation of Break-Even Point, Margins, and Profitlg...

|12

|2690

|257

Business Financelg...

|23

|5468

|265