Business Finance: Financial Analysis of Rio Tinto Limited Report

VerifiedAdded on 2023/02/01

|17

|4241

|40

Report

AI Summary

This report provides a comprehensive financial analysis of Rio Tinto Limited, a major player in the materials and metals sector. The analysis includes the calculation and interpretation of various financial ratios, such as profitability and efficiency ratios, to assess the company's performance. The report examines the company's profitability position by analyzing net profit margin, return on assets, return on equity, and return on capital employed. Furthermore, the report assesses the efficiency position using working capital ratio, asset turnover ratio, and accounts receivable turnover. The report also compares Rio Tinto's share price movements with the All Ordinaries Index. The capital structure of Rio Tinto is also evaluated. The analysis aims to provide insights for institutional investors, evaluating the company's financial health and investment potential. The report concludes with recommendations based on the financial analysis.

Running head: BUSINESS FINANCE

Business finance

Name of the Student

Name of the University

Author Note

Business finance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

Abstract:

The current paper discusses about several financials of the company for assessing the overall

finance performance. For this purpose, one of the companies from materials sector of

Australia has been chosen named Rio Tinto which is the leading suppliers of material and

metals all over the world. Evaluation of the financial performance is done by using several

financial tools such as ratio analysis, computation of WACC and cost of equity using

constant divided growth model and analyzing the share price movements in relation to the

ordinaries index. Moreover, the capital structure of Rio Tinto is also evaluated by analyzing

the change in total value of capital along with changes in the proportion of equity and debt.

The overall report prepared is analyzed for helping the institutional investors to make

investment decisions.

Abstract:

The current paper discusses about several financials of the company for assessing the overall

finance performance. For this purpose, one of the companies from materials sector of

Australia has been chosen named Rio Tinto which is the leading suppliers of material and

metals all over the world. Evaluation of the financial performance is done by using several

financial tools such as ratio analysis, computation of WACC and cost of equity using

constant divided growth model and analyzing the share price movements in relation to the

ordinaries index. Moreover, the capital structure of Rio Tinto is also evaluated by analyzing

the change in total value of capital along with changes in the proportion of equity and debt.

The overall report prepared is analyzed for helping the institutional investors to make

investment decisions.

BUSINESS FINANCE

Table of Contents

I. Introduction:............................................................................................................................3

II. FINANCIAL ANALYSIS OF RIO TINTO LIMITED........................................................4

2.1 Description of company.......................................................................................................4

2.2 Calculation and analysis of financial ratios.........................................................................5

Analysis of profitability position:..............................................................................................5

Analysis of efficiency position:.................................................................................................7

2.3 Graphs and comparison of share price movements..............................................................9

2.4 Calculation of cost of equity..............................................................................................11

2.5 Identify the capital structure...............................................................................................11

III. CONCLUSION..................................................................................................................14

IV. RECOMMENDATIONS:..................................................................................................14

Table of Contents

I. Introduction:............................................................................................................................3

II. FINANCIAL ANALYSIS OF RIO TINTO LIMITED........................................................4

2.1 Description of company.......................................................................................................4

2.2 Calculation and analysis of financial ratios.........................................................................5

Analysis of profitability position:..............................................................................................5

Analysis of efficiency position:.................................................................................................7

2.3 Graphs and comparison of share price movements..............................................................9

2.4 Calculation of cost of equity..............................................................................................11

2.5 Identify the capital structure...............................................................................................11

III. CONCLUSION..................................................................................................................14

IV. RECOMMENDATIONS:..................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

I. Introduction:

The objective of the report is to demonstrate an understanding of the overall

performance of chosen company from the stock exchange of Australia. Financial analysis of

the selected company has been done by the computation of various profitability and

efficiency ratios that depicts the efficiency and profitability position of company. In addition

to this, the current paper intends to assess the capital structure and determine the influence of

cost of capital on the capital structure of the firm. The share price of Rio Tinto is compared

against the movement of price of all ordinaries index. From the analysis of the different

ratios, it has been found that the company is efficiency in utilizing their assets to generate

income and their profitability position has also improved. Nevertheless, there seems to be

fluctuation in the price of share, the share price is following an upward trend in the current

year encouraging investors to invest in the company shares.

II. FINANCIAL ANALYSIS OF RIO TINTO LIMITED

2.1 Description of company

Rio Tinto is one of the largest metal and mining companies operating in the world

having significant operations in refining particularly for iron ore and refining bauxite. The

organization is engaged in supplying minerals and metals that assist world in growing with

some of the major products comprising of copper, aluminum, industrial minerals, diamond,

gold, and uranium and iron ore. The strong representation of company is in North America

and Australia and has significant business in Europe, Asia, South America and Africa. Some

of the best and largest quality mines and operations of the world has been developed by the

company (Riotinto.com 2019). For finding the potential new sources of metals and minerals,

some of the most advanced exploration technologies are used by the business. Each potential

operation of business is assessed with a focus on potential risk and return and long term value

I. Introduction:

The objective of the report is to demonstrate an understanding of the overall

performance of chosen company from the stock exchange of Australia. Financial analysis of

the selected company has been done by the computation of various profitability and

efficiency ratios that depicts the efficiency and profitability position of company. In addition

to this, the current paper intends to assess the capital structure and determine the influence of

cost of capital on the capital structure of the firm. The share price of Rio Tinto is compared

against the movement of price of all ordinaries index. From the analysis of the different

ratios, it has been found that the company is efficiency in utilizing their assets to generate

income and their profitability position has also improved. Nevertheless, there seems to be

fluctuation in the price of share, the share price is following an upward trend in the current

year encouraging investors to invest in the company shares.

II. FINANCIAL ANALYSIS OF RIO TINTO LIMITED

2.1 Description of company

Rio Tinto is one of the largest metal and mining companies operating in the world

having significant operations in refining particularly for iron ore and refining bauxite. The

organization is engaged in supplying minerals and metals that assist world in growing with

some of the major products comprising of copper, aluminum, industrial minerals, diamond,

gold, and uranium and iron ore. The strong representation of company is in North America

and Australia and has significant business in Europe, Asia, South America and Africa. Some

of the best and largest quality mines and operations of the world has been developed by the

company (Riotinto.com 2019). For finding the potential new sources of metals and minerals,

some of the most advanced exploration technologies are used by the business. Each potential

operation of business is assessed with a focus on potential risk and return and long term value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

and sustainability. The minerals and metals of company are used in vast array of products and

the product line is managed by ensuring that they align with the needs of customers and

markets. The organization follows the strategy of creating superior values for shareholders by

maximizing the allocation of capital and cash from the world class assets. The strategy of

group that helps in gaining comparative advantage is focusing on demand led business and

low cost of operations. The product group grows and creates the global market for the

products to deliver value through its strategies of integrated marketing. Some of the strategic

advantage enjoyed by the company includes proximity to key Asian markets, strong presence

in key markets, and low cost position with Pilbara cash unit costing US $ 13.4 tone and high

margin at 68% for EBITDA margin (Riotinto.com 2019). Furthermore, the company is

industry leader in creating responsible mining, supply chain management, innovation and

technology.

2.2 Calculation and analysis of financial ratios

The operating efficiency and profitability position of Rio Tinto is evaluated by the

computation of several ratios such as asset turnover, accounts receivable turnover, working

capital ratio, return on assets, return on capital employed and return on equity.

Analysis of profitability position:

Profitability ratio analysis helps in evaluating the return generated by company on its

investment in inventories or some other assets which helps in depicting how well the

company generates profits on their operations. The ability of company to generate operational

profits from their assets is evaluated using ratios such as net profit ratio, return on equity,

return on capital employed and return on total assets (Berger et al. 2018).

and sustainability. The minerals and metals of company are used in vast array of products and

the product line is managed by ensuring that they align with the needs of customers and

markets. The organization follows the strategy of creating superior values for shareholders by

maximizing the allocation of capital and cash from the world class assets. The strategy of

group that helps in gaining comparative advantage is focusing on demand led business and

low cost of operations. The product group grows and creates the global market for the

products to deliver value through its strategies of integrated marketing. Some of the strategic

advantage enjoyed by the company includes proximity to key Asian markets, strong presence

in key markets, and low cost position with Pilbara cash unit costing US $ 13.4 tone and high

margin at 68% for EBITDA margin (Riotinto.com 2019). Furthermore, the company is

industry leader in creating responsible mining, supply chain management, innovation and

technology.

2.2 Calculation and analysis of financial ratios

The operating efficiency and profitability position of Rio Tinto is evaluated by the

computation of several ratios such as asset turnover, accounts receivable turnover, working

capital ratio, return on assets, return on capital employed and return on equity.

Analysis of profitability position:

Profitability ratio analysis helps in evaluating the return generated by company on its

investment in inventories or some other assets which helps in depicting how well the

company generates profits on their operations. The ability of company to generate operational

profits from their assets is evaluated using ratios such as net profit ratio, return on equity,

return on capital employed and return on total assets (Berger et al. 2018).

BUSINESS FINANCE

Net profit ratio Return on Total

Assets Return on

Equity Return on

capital

employed

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.35

0.09

0.20

0.17

0.44

0.15

0.32

0.22 2017

2018

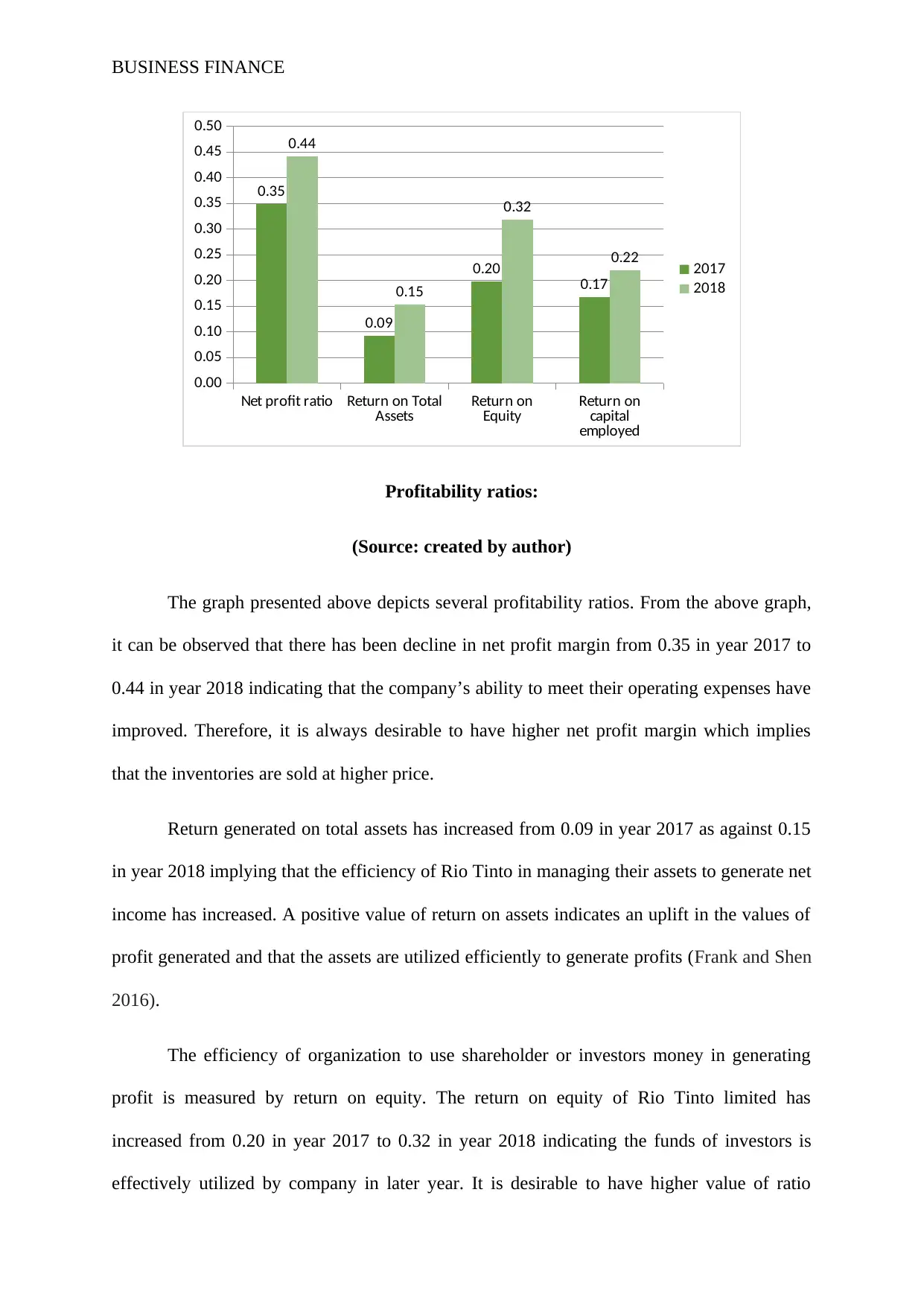

Profitability ratios:

(Source: created by author)

The graph presented above depicts several profitability ratios. From the above graph,

it can be observed that there has been decline in net profit margin from 0.35 in year 2017 to

0.44 in year 2018 indicating that the company’s ability to meet their operating expenses have

improved. Therefore, it is always desirable to have higher net profit margin which implies

that the inventories are sold at higher price.

Return generated on total assets has increased from 0.09 in year 2017 as against 0.15

in year 2018 implying that the efficiency of Rio Tinto in managing their assets to generate net

income has increased. A positive value of return on assets indicates an uplift in the values of

profit generated and that the assets are utilized efficiently to generate profits (Frank and Shen

2016).

The efficiency of organization to use shareholder or investors money in generating

profit is measured by return on equity. The return on equity of Rio Tinto limited has

increased from 0.20 in year 2017 to 0.32 in year 2018 indicating the funds of investors is

effectively utilized by company in later year. It is desirable to have higher value of ratio

Net profit ratio Return on Total

Assets Return on

Equity Return on

capital

employed

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.35

0.09

0.20

0.17

0.44

0.15

0.32

0.22 2017

2018

Profitability ratios:

(Source: created by author)

The graph presented above depicts several profitability ratios. From the above graph,

it can be observed that there has been decline in net profit margin from 0.35 in year 2017 to

0.44 in year 2018 indicating that the company’s ability to meet their operating expenses have

improved. Therefore, it is always desirable to have higher net profit margin which implies

that the inventories are sold at higher price.

Return generated on total assets has increased from 0.09 in year 2017 as against 0.15

in year 2018 implying that the efficiency of Rio Tinto in managing their assets to generate net

income has increased. A positive value of return on assets indicates an uplift in the values of

profit generated and that the assets are utilized efficiently to generate profits (Frank and Shen

2016).

The efficiency of organization to use shareholder or investors money in generating

profit is measured by return on equity. The return on equity of Rio Tinto limited has

increased from 0.20 in year 2017 to 0.32 in year 2018 indicating the funds of investors is

effectively utilized by company in later year. It is desirable to have higher value of ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

compared to lower value as it implies that company is generating higher profit because of

efficiently utilizing the investor’s fund.

The ability of company to generate profits by employing each dollar of capital

employed is measured by computing return on capital employed ratio. It can be seen that

return on capital employed of Rio Tinto has increased from 0.17 in year 2017 compared to

0.22 in year 2018. This increase in ratio is considered favorable because it indicates that with

each dollar of capital employed, there is more dollars of profits generated (Song et al. 2018).

Therefore, from the analysis of all the profitability ratios, it can be inferred that

profitability position of Rio Tinto has improved in the current year of analysis as the

company is performing well to achieve increased level of profits from their operations.

Hence, the company is making enough operational profits from the investment in assets

which is considered attractive for investors to make investment in the company (Gitman et al.

2015).

Analysis of efficiency position:

Efficiency ratios help in evaluating the efficiency of companies in utilizing their

assets to generate income and the management uses this ratio for improving the profitability

from operations to investors and creditors (Belo et al. 2015). Some of the profitability ratios

that have been computed for the analysis purpose includes working capital ratio, asset

turnover ratio and accounts receivable turnover.

compared to lower value as it implies that company is generating higher profit because of

efficiently utilizing the investor’s fund.

The ability of company to generate profits by employing each dollar of capital

employed is measured by computing return on capital employed ratio. It can be seen that

return on capital employed of Rio Tinto has increased from 0.17 in year 2017 compared to

0.22 in year 2018. This increase in ratio is considered favorable because it indicates that with

each dollar of capital employed, there is more dollars of profits generated (Song et al. 2018).

Therefore, from the analysis of all the profitability ratios, it can be inferred that

profitability position of Rio Tinto has improved in the current year of analysis as the

company is performing well to achieve increased level of profits from their operations.

Hence, the company is making enough operational profits from the investment in assets

which is considered attractive for investors to make investment in the company (Gitman et al.

2015).

Analysis of efficiency position:

Efficiency ratios help in evaluating the efficiency of companies in utilizing their

assets to generate income and the management uses this ratio for improving the profitability

from operations to investors and creditors (Belo et al. 2015). Some of the profitability ratios

that have been computed for the analysis purpose includes working capital ratio, asset

turnover ratio and accounts receivable turnover.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

Working capital ratio Asset turnover ratio Accounts receivable

turnover

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

1.66

0.29

7.83

1.91

0.29

7.95

2017

2018

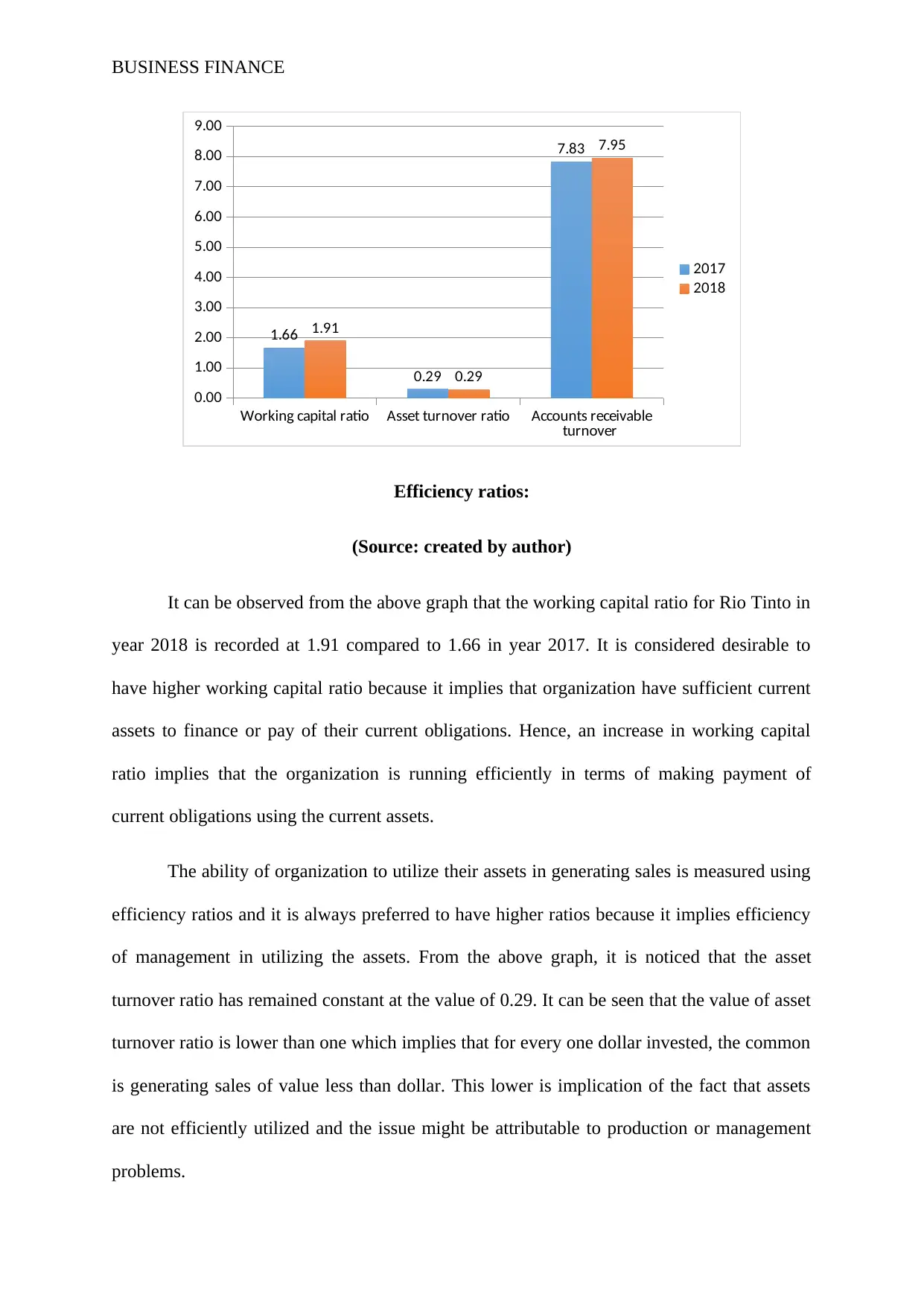

Efficiency ratios:

(Source: created by author)

It can be observed from the above graph that the working capital ratio for Rio Tinto in

year 2018 is recorded at 1.91 compared to 1.66 in year 2017. It is considered desirable to

have higher working capital ratio because it implies that organization have sufficient current

assets to finance or pay of their current obligations. Hence, an increase in working capital

ratio implies that the organization is running efficiently in terms of making payment of

current obligations using the current assets.

The ability of organization to utilize their assets in generating sales is measured using

efficiency ratios and it is always preferred to have higher ratios because it implies efficiency

of management in utilizing the assets. From the above graph, it is noticed that the asset

turnover ratio has remained constant at the value of 0.29. It can be seen that the value of asset

turnover ratio is lower than one which implies that for every one dollar invested, the common

is generating sales of value less than dollar. This lower is implication of the fact that assets

are not efficiently utilized and the issue might be attributable to production or management

problems.

Working capital ratio Asset turnover ratio Accounts receivable

turnover

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

1.66

0.29

7.83

1.91

0.29

7.95

2017

2018

Efficiency ratios:

(Source: created by author)

It can be observed from the above graph that the working capital ratio for Rio Tinto in

year 2018 is recorded at 1.91 compared to 1.66 in year 2017. It is considered desirable to

have higher working capital ratio because it implies that organization have sufficient current

assets to finance or pay of their current obligations. Hence, an increase in working capital

ratio implies that the organization is running efficiently in terms of making payment of

current obligations using the current assets.

The ability of organization to utilize their assets in generating sales is measured using

efficiency ratios and it is always preferred to have higher ratios because it implies efficiency

of management in utilizing the assets. From the above graph, it is noticed that the asset

turnover ratio has remained constant at the value of 0.29. It can be seen that the value of asset

turnover ratio is lower than one which implies that for every one dollar invested, the common

is generating sales of value less than dollar. This lower is implication of the fact that assets

are not efficiently utilized and the issue might be attributable to production or management

problems.

BUSINESS FINANCE

Accounts receivable turnover measures the efficiency of the company regarding the

number of times account receivable is converted into cash. In other words, the efficiency of

company in collecting its credit sales from customers is measured with this ratio. Accounts

receivable turnover for Rio Tinto is computed at 7.83 in year 2017 and the value increased to

7.95 in year 2018. This increase in ratio is preferable as it implies that there is frequent

collection of cash from the credit sales made to customers and such cash helps in meeting the

obligations such as payment of bills and other obligations.

From the analysis of the figures related to efficiency ratios, it is inferred that the

overall efficiency position of Rio Tinto has improved in recent years and the company is

efficient with the resources and is conclusive of the fact that assets are utilized appropriate to

generate income.

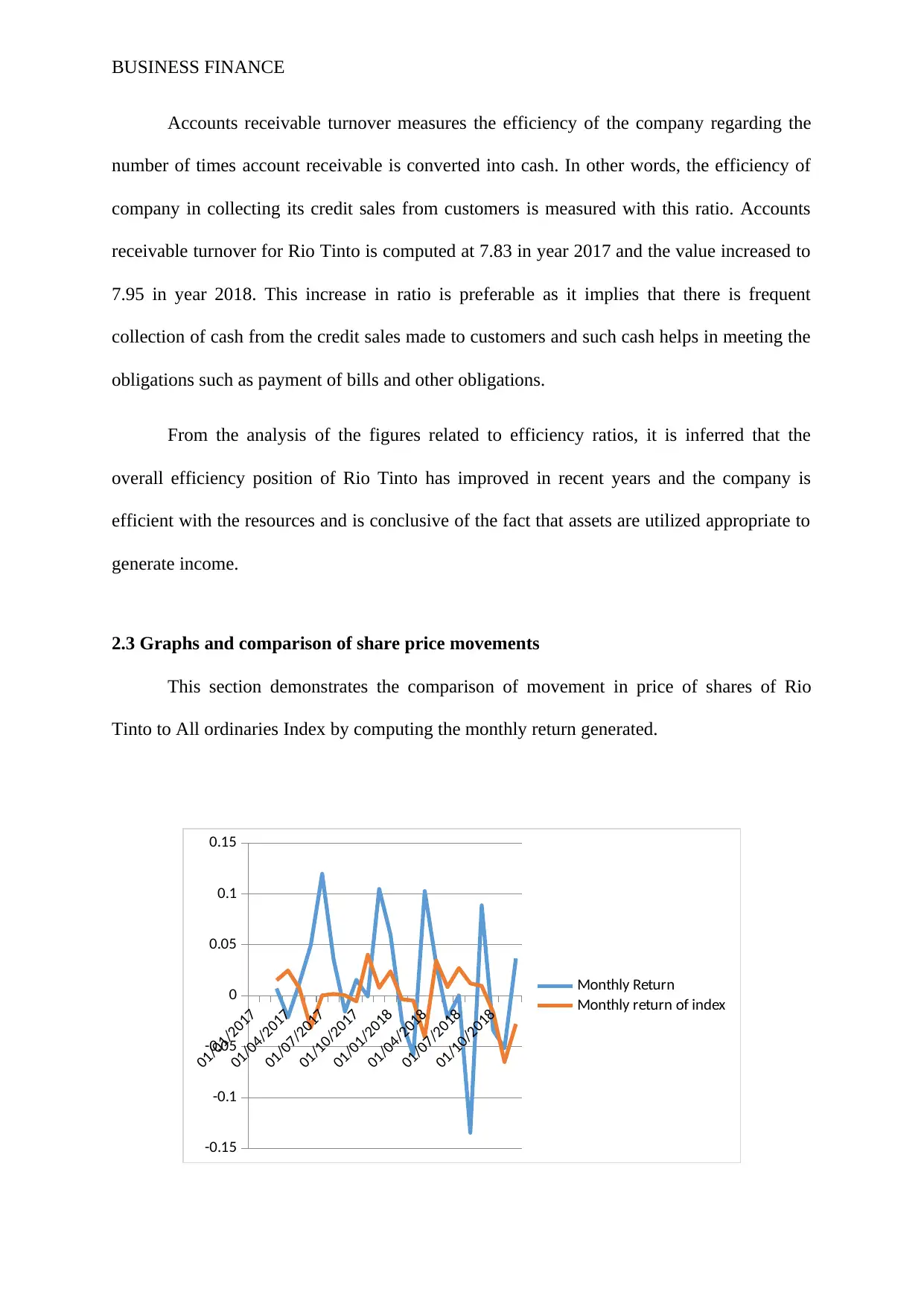

2.3 Graphs and comparison of share price movements

This section demonstrates the comparison of movement in price of shares of Rio

Tinto to All ordinaries Index by computing the monthly return generated.

01/01/2017

01/04/2017

01/07/2017

01/10/2017

01/01/2018

01/04/2018

01/07/2018

01/10/2018

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Monthly Return

Monthly return of index

Accounts receivable turnover measures the efficiency of the company regarding the

number of times account receivable is converted into cash. In other words, the efficiency of

company in collecting its credit sales from customers is measured with this ratio. Accounts

receivable turnover for Rio Tinto is computed at 7.83 in year 2017 and the value increased to

7.95 in year 2018. This increase in ratio is preferable as it implies that there is frequent

collection of cash from the credit sales made to customers and such cash helps in meeting the

obligations such as payment of bills and other obligations.

From the analysis of the figures related to efficiency ratios, it is inferred that the

overall efficiency position of Rio Tinto has improved in recent years and the company is

efficient with the resources and is conclusive of the fact that assets are utilized appropriate to

generate income.

2.3 Graphs and comparison of share price movements

This section demonstrates the comparison of movement in price of shares of Rio

Tinto to All ordinaries Index by computing the monthly return generated.

01/01/2017

01/04/2017

01/07/2017

01/10/2017

01/01/2018

01/04/2018

01/07/2018

01/10/2018

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Monthly Return

Monthly return of index

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

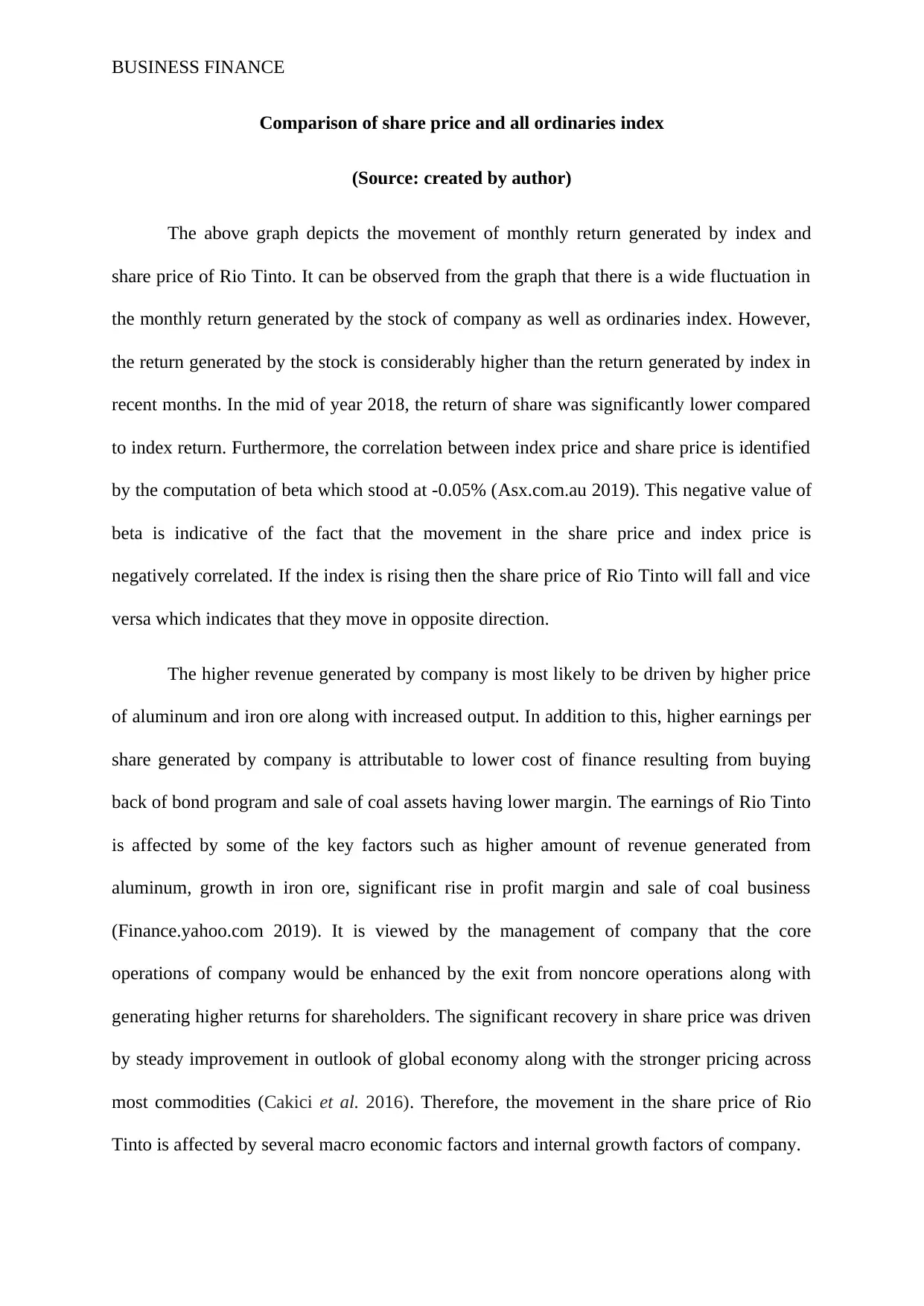

Comparison of share price and all ordinaries index

(Source: created by author)

The above graph depicts the movement of monthly return generated by index and

share price of Rio Tinto. It can be observed from the graph that there is a wide fluctuation in

the monthly return generated by the stock of company as well as ordinaries index. However,

the return generated by the stock is considerably higher than the return generated by index in

recent months. In the mid of year 2018, the return of share was significantly lower compared

to index return. Furthermore, the correlation between index price and share price is identified

by the computation of beta which stood at -0.05% (Asx.com.au 2019). This negative value of

beta is indicative of the fact that the movement in the share price and index price is

negatively correlated. If the index is rising then the share price of Rio Tinto will fall and vice

versa which indicates that they move in opposite direction.

The higher revenue generated by company is most likely to be driven by higher price

of aluminum and iron ore along with increased output. In addition to this, higher earnings per

share generated by company is attributable to lower cost of finance resulting from buying

back of bond program and sale of coal assets having lower margin. The earnings of Rio Tinto

is affected by some of the key factors such as higher amount of revenue generated from

aluminum, growth in iron ore, significant rise in profit margin and sale of coal business

(Finance.yahoo.com 2019). It is viewed by the management of company that the core

operations of company would be enhanced by the exit from noncore operations along with

generating higher returns for shareholders. The significant recovery in share price was driven

by steady improvement in outlook of global economy along with the stronger pricing across

most commodities (Cakici et al. 2016). Therefore, the movement in the share price of Rio

Tinto is affected by several macro economic factors and internal growth factors of company.

Comparison of share price and all ordinaries index

(Source: created by author)

The above graph depicts the movement of monthly return generated by index and

share price of Rio Tinto. It can be observed from the graph that there is a wide fluctuation in

the monthly return generated by the stock of company as well as ordinaries index. However,

the return generated by the stock is considerably higher than the return generated by index in

recent months. In the mid of year 2018, the return of share was significantly lower compared

to index return. Furthermore, the correlation between index price and share price is identified

by the computation of beta which stood at -0.05% (Asx.com.au 2019). This negative value of

beta is indicative of the fact that the movement in the share price and index price is

negatively correlated. If the index is rising then the share price of Rio Tinto will fall and vice

versa which indicates that they move in opposite direction.

The higher revenue generated by company is most likely to be driven by higher price

of aluminum and iron ore along with increased output. In addition to this, higher earnings per

share generated by company is attributable to lower cost of finance resulting from buying

back of bond program and sale of coal assets having lower margin. The earnings of Rio Tinto

is affected by some of the key factors such as higher amount of revenue generated from

aluminum, growth in iron ore, significant rise in profit margin and sale of coal business

(Finance.yahoo.com 2019). It is viewed by the management of company that the core

operations of company would be enhanced by the exit from noncore operations along with

generating higher returns for shareholders. The significant recovery in share price was driven

by steady improvement in outlook of global economy along with the stronger pricing across

most commodities (Cakici et al. 2016). Therefore, the movement in the share price of Rio

Tinto is affected by several macro economic factors and internal growth factors of company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

2.4 Calculation of cost of equity

The dividend growth model is used for computing the cost of equity which is the

return generated by the investment made in equity. Such model takes into account the

assumption that the dividend paid by company grows at constant rate. The market cost of

equity and the value of equity of firms are linked by modeling the expected future value of

dividends that would be received by shareholders (Boyer et al. 2017). The growth model

makes use of following formula for computing the cost of equity.

Cost of equity= (Annual dividend paid in the next year/ Current price of stock) + growth rate

of dividend

Constant growth rate of dividend= 4%

Current price of stock= 45.003

Annual dividend paid= $ 5.3 billion

Cost of equity= (5.3/45.003) + 4%= 0.11776*100+4= 15.776%

Therefore, the required rate of return generated on equity investment of Rio Tinto is

15.776%.

2.5 Identify the capital structure

The capital structure of organization is how the organization finances their growth and

operations by using different sources of funds. It is desirable for organization to have optimal

capital structure that there should be proper and appropriate proportion of equity and debt in

the capital structure which indicates that the firm has best combination of debt and equity

(Adam et al. 2017). In other words, the proportion of equity and debt that results in lowest

WACC (weighted average cost of capital) gives the optimal capital structure.

2.4 Calculation of cost of equity

The dividend growth model is used for computing the cost of equity which is the

return generated by the investment made in equity. Such model takes into account the

assumption that the dividend paid by company grows at constant rate. The market cost of

equity and the value of equity of firms are linked by modeling the expected future value of

dividends that would be received by shareholders (Boyer et al. 2017). The growth model

makes use of following formula for computing the cost of equity.

Cost of equity= (Annual dividend paid in the next year/ Current price of stock) + growth rate

of dividend

Constant growth rate of dividend= 4%

Current price of stock= 45.003

Annual dividend paid= $ 5.3 billion

Cost of equity= (5.3/45.003) + 4%= 0.11776*100+4= 15.776%

Therefore, the required rate of return generated on equity investment of Rio Tinto is

15.776%.

2.5 Identify the capital structure

The capital structure of organization is how the organization finances their growth and

operations by using different sources of funds. It is desirable for organization to have optimal

capital structure that there should be proper and appropriate proportion of equity and debt in

the capital structure which indicates that the firm has best combination of debt and equity

(Adam et al. 2017). In other words, the proportion of equity and debt that results in lowest

WACC (weighted average cost of capital) gives the optimal capital structure.

BUSINESS FINANCE

The weighted average cost of capital is computed by the organization for determining

the level of risk so that the cost of capital is lower than the expected return on capital. In this

section, it is required to compute the weighted average cost of capital of Rio Tinto for which

the required rate of return on preference shares and required rate of return on industrial debt

is given. The formula for computing the weighted average cost of capital is given below:

WACC= (E/V * Re) + ((D/V*Kd)* (1-T))

Where E is the market value of firm’s equity

D is the market value of firm’s debt and V denotes the total value of capital.

D/V is the weightage of debt to total capital and E/V is the weightage of equity to total

capital.

Kd is the debt cost and Re is the equity cost

T is the rate of tax

In the computation of WACC, it is seen that the company does not have any

preference shares and hence no required rate of return on preference share is taken into

account while computing the cost of capital (Brusov et al. 2017).

Therefore, WACC= (51115/66263*16%) + (15148/66263*5%)*(1-30%) = 16%.

From the computation of WACC, it can be seen that the value of WACC is

approximately same as the cost of equity.

The change in structure of capital of Rio Tinto is presented in the table below which

shows the change in value of debt and equity in relation to the total amount of capital. The

weight of debt and equity is also computed.

The weighted average cost of capital is computed by the organization for determining

the level of risk so that the cost of capital is lower than the expected return on capital. In this

section, it is required to compute the weighted average cost of capital of Rio Tinto for which

the required rate of return on preference shares and required rate of return on industrial debt

is given. The formula for computing the weighted average cost of capital is given below:

WACC= (E/V * Re) + ((D/V*Kd)* (1-T))

Where E is the market value of firm’s equity

D is the market value of firm’s debt and V denotes the total value of capital.

D/V is the weightage of debt to total capital and E/V is the weightage of equity to total

capital.

Kd is the debt cost and Re is the equity cost

T is the rate of tax

In the computation of WACC, it is seen that the company does not have any

preference shares and hence no required rate of return on preference share is taken into

account while computing the cost of capital (Brusov et al. 2017).

Therefore, WACC= (51115/66263*16%) + (15148/66263*5%)*(1-30%) = 16%.

From the computation of WACC, it can be seen that the value of WACC is

approximately same as the cost of equity.

The change in structure of capital of Rio Tinto is presented in the table below which

shows the change in value of debt and equity in relation to the total amount of capital. The

weight of debt and equity is also computed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.