Business Law Assignment: Income Tax and Capital Gains Analysis

VerifiedAdded on 2021/05/31

|8

|1393

|29

Homework Assignment

AI Summary

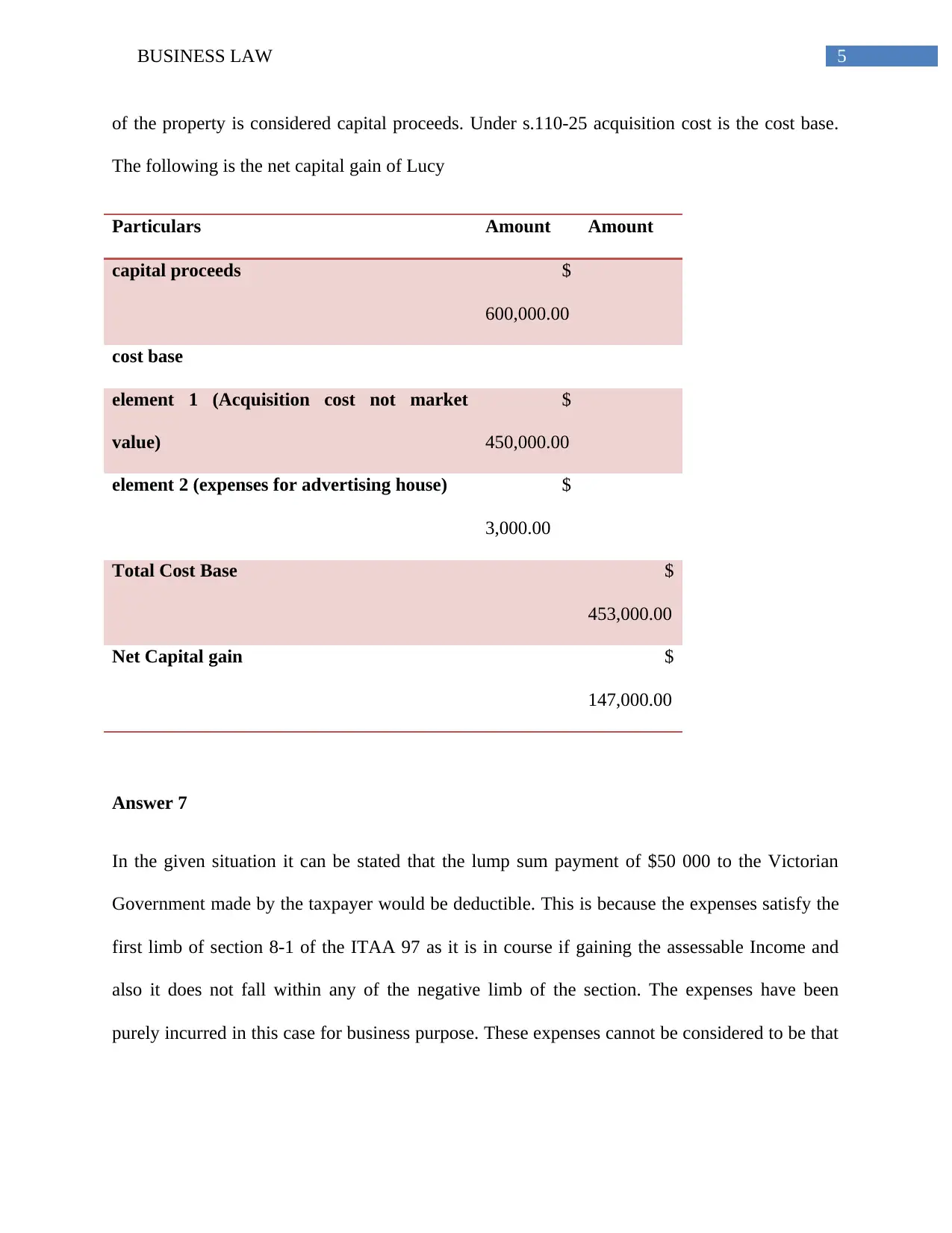

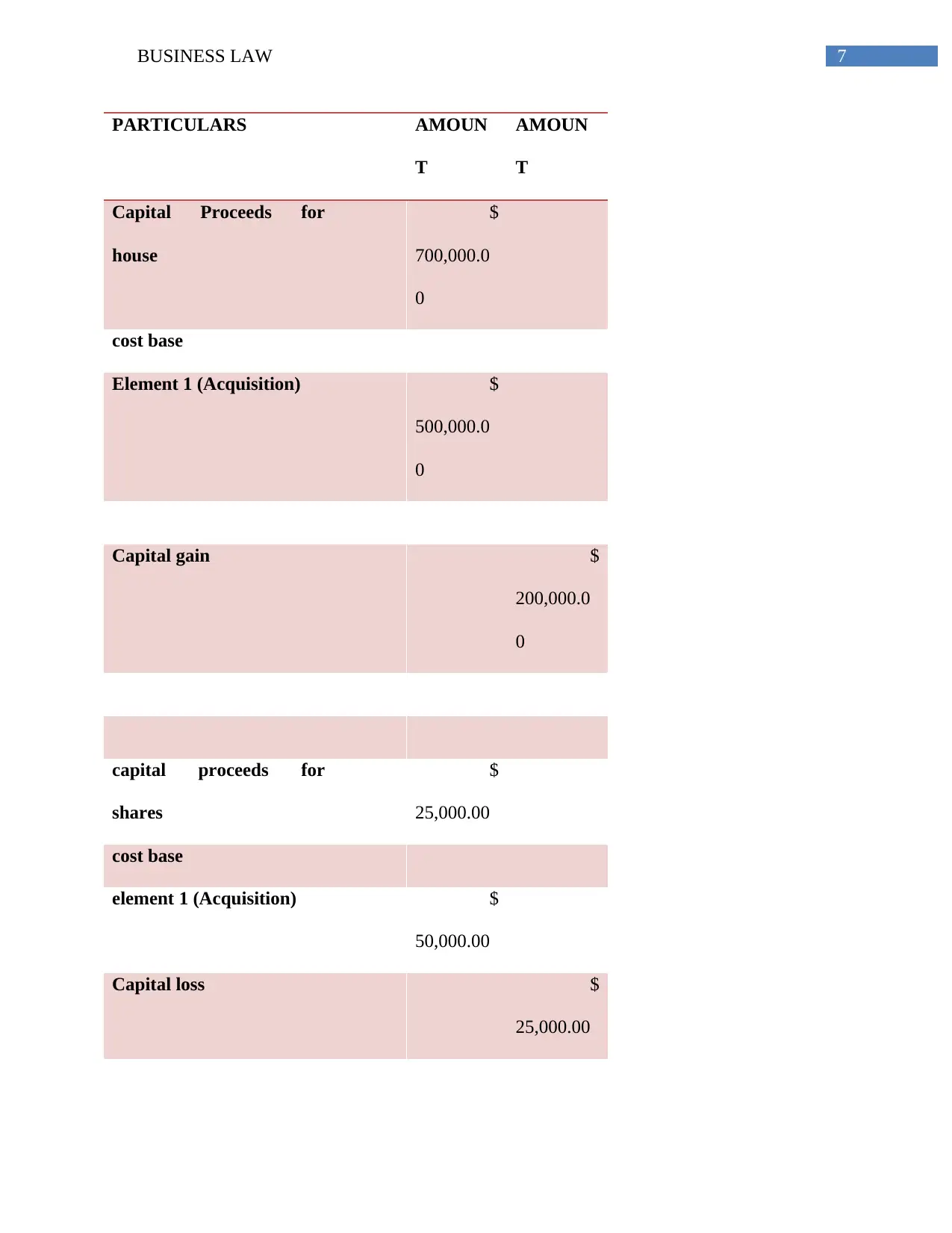

This business law assignment provides detailed answers to ten questions related to Australian income tax and capital gains tax. The assignment covers various aspects of the Income Tax Assessment Act 1997, including deductible expenses, cost base calculations, capital gains, and depreciation methods. The solutions analyze scenarios involving legal fees, property repairs, capital proceeds, declining asset depreciation, golf club memberships, and lump-sum payments to the government. Additionally, it addresses capital gains from property sales, insurance proceeds, and the treatment of internet costs, mortgage interest, and accountant fees, providing a comprehensive analysis of tax-related concepts and calculations. The assignment concludes with the calculation of net capital gains and losses, demonstrating how capital gains and losses are offset.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.