UK Tax Policy and Analysis

VerifiedAdded on 2020/02/14

|15

|4528

|319

AI Summary

This assignment delves into various aspects of UK tax policy. It requires students to research and analyze current income tax rates, personal allowances, and the impact of taxation on business investment. The task also involves examining the effectiveness of tax incentives for innovation and exploring the relationship between taxation and technology-based small firms in the UK. Students are expected to utilize a range of resources including academic journals, government publications, and online databases.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business and

Personal

taxation

1

Personal

taxation

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Part 1 Tax situation for the two companies for the year ended 31 March 2015..............................3

Identification of capital gains arising on the transfer of the chargeable asset from Brownleas

plc to Retro Ltd............................................................................................................................3

Explanation of consideration of two companies as a group for the purpose of group relief.......4

Available option of tax relief to the Retro Ltd regarding tax adjustment of tax losses...............5

Capital allowance treatment for the purchase of each asset........................................................5

Part 2 Evaluation of tax considerations in respect of the proposed methods...................................7

Selection of suitable business structure ......................................................................................7

Conclusion.....................................................................................................................................10

Appendices.....................................................................................................................................11

Calculations of capital allowances.............................................................................................11

Tax adjusted trading profits.......................................................................................................12

Gross value of the foreign income of Brownleas plc................................................................12

Total taxable profits ..................................................................................................................12

Total taxable profits ..................................................................................................................13

References......................................................................................................................................14

2

Introduction......................................................................................................................................3

Part 1 Tax situation for the two companies for the year ended 31 March 2015..............................3

Identification of capital gains arising on the transfer of the chargeable asset from Brownleas

plc to Retro Ltd............................................................................................................................3

Explanation of consideration of two companies as a group for the purpose of group relief.......4

Available option of tax relief to the Retro Ltd regarding tax adjustment of tax losses...............5

Capital allowance treatment for the purchase of each asset........................................................5

Part 2 Evaluation of tax considerations in respect of the proposed methods...................................7

Selection of suitable business structure ......................................................................................7

Conclusion.....................................................................................................................................10

Appendices.....................................................................................................................................11

Calculations of capital allowances.............................................................................................11

Tax adjusted trading profits.......................................................................................................12

Gross value of the foreign income of Brownleas plc................................................................12

Total taxable profits ..................................................................................................................12

Total taxable profits ..................................................................................................................13

References......................................................................................................................................14

2

INTRODUCTION

Companies operating in UK are required to pay taxation charges on the chargeable profits

in accordance with the described provisions by the HMRC. Companies are entitled for making

claim of the taxation benefits in order to make reduction in their tax obligations. For this aspect,

management of companies are required to do suitable tax planning (Becker and Fuest, 2011).

Present business report is focused on the computation of taxable profits and tax planning of

Brownleas plc and Retro Ltd by considering their financial figures of 31st March 2015. For this

aspect, description of tax benefits will be provided available to the company by considering the

situational facts. This description will be supported by the tax provisions that are stated by the

HMRC.

PART 1 TAX SITUATION FOR THE TWO COMPANIES FOR THE YEAR

ENDED 31 MARCH 2015

1. Identification of capital gains arising on the transfer of the chargeable asset from Brownleas

plc to Retro Ltd

Capital gain tax can be defined as a profit that is made by a person on the transfer of

property, shares or other investment (Citron, 2001). Provisions for capital gain tax is charged in

the following situations:

Give away the chargeable asset

Transfer of chargeable asset by one person to another

Acceptance of something in against of chargeable asset

Receipt of compensation for the destruction or loss of an asset such as receipt of amount

of insurance claim.

Transfer of chargeable assets from Brownleas plc to Retro Ltd is covered in second

option. By considering the provided information, it can be noticed that Brownleas plc holds 85%

interest in Retro SA. Due to this aspect, provisions of capital group, company will be applied in

this case. Description of this provision is as follows:

Rules of group relief

In accordance with the provisions of UK taxation, transfer of chargeable assets between

capital group companies will not be considered for the purpose of any gain or loss. In addition to

3

Companies operating in UK are required to pay taxation charges on the chargeable profits

in accordance with the described provisions by the HMRC. Companies are entitled for making

claim of the taxation benefits in order to make reduction in their tax obligations. For this aspect,

management of companies are required to do suitable tax planning (Becker and Fuest, 2011).

Present business report is focused on the computation of taxable profits and tax planning of

Brownleas plc and Retro Ltd by considering their financial figures of 31st March 2015. For this

aspect, description of tax benefits will be provided available to the company by considering the

situational facts. This description will be supported by the tax provisions that are stated by the

HMRC.

PART 1 TAX SITUATION FOR THE TWO COMPANIES FOR THE YEAR

ENDED 31 MARCH 2015

1. Identification of capital gains arising on the transfer of the chargeable asset from Brownleas

plc to Retro Ltd

Capital gain tax can be defined as a profit that is made by a person on the transfer of

property, shares or other investment (Citron, 2001). Provisions for capital gain tax is charged in

the following situations:

Give away the chargeable asset

Transfer of chargeable asset by one person to another

Acceptance of something in against of chargeable asset

Receipt of compensation for the destruction or loss of an asset such as receipt of amount

of insurance claim.

Transfer of chargeable assets from Brownleas plc to Retro Ltd is covered in second

option. By considering the provided information, it can be noticed that Brownleas plc holds 85%

interest in Retro SA. Due to this aspect, provisions of capital group, company will be applied in

this case. Description of this provision is as follows:

Rules of group relief

In accordance with the provisions of UK taxation, transfer of chargeable assets between

capital group companies will not be considered for the purpose of any gain or loss. In addition to

3

this, such transfer must not be considered for the purpose of tax planning opportunity (Dowell,

2013). Reason of this provision is that there is no requirement of transfer of asset for the purpose

of the realization of allowable loss or chargeable gain on an external sale in a particular group

company. In addition to this, profit or loss such transaction will be recorded in the particular

group at the time of final elimination (Garrett and Mitchell, 2001). Provision of group relief is

applied in situation where there is transfer of chargeable assets between the management of a

group of companies for the purpose of accomplishment of commercial transactions. For example,

a particular asset or an entire trade is transferred by one company to another without raising any

provisions of chargeable gain.

By considering this aspect, it can be said that no capital gain tax will be charged on the

transaction of transferring chargeable assets from Brownleas plc to Retro Ltd.

2. Explanation of consideration of two companies as a group for the purpose of group relief

The two companies are considered as a group for the purpose of transferring chargeable

assets in order to make claim of relief in the taxation. With this relief they are able to make

reduction in their overall tax as loss of one company is compensated with the profit of another

company. In accordance with the provisions of UK taxation, a UK resident company is in

position to make claim of group relief in order to take benefit of set off of trading losses of a non

UK subsidiary however but resident of European Economic Area (EEA).

Tax consolidation is permitted by the UK in situation where companies in a group are not

considered as a single entity for the purpose of tax computation. Major benefit of this provision

is that tax loss of one company will be considered relievable for the tax profits of another

company (Henrekson and Sanandaji, 2011). By considering this aspect, company is in position

to surrender their losses in situation where losses of the accounting period (other than capital

gains) are higher than the taxable profits to a group member who have sufficient taxable profits

in the similar accounting period (Miller and Oats, 2012). Member Company can use these losses

to make reduction in their tax profits. Full group relief is permitted in situation where companies

have interest more than equal to the 75%.

Loss relief is usually available for the trading losses incurred by an overseas branch.

Provision stated in UK Paper F6 shows that no UK relief will be available for the trading losses

incurred by the overseas subsidiary company (Finney, 2010). In addition to this, UK capital

4

2013). Reason of this provision is that there is no requirement of transfer of asset for the purpose

of the realization of allowable loss or chargeable gain on an external sale in a particular group

company. In addition to this, profit or loss such transaction will be recorded in the particular

group at the time of final elimination (Garrett and Mitchell, 2001). Provision of group relief is

applied in situation where there is transfer of chargeable assets between the management of a

group of companies for the purpose of accomplishment of commercial transactions. For example,

a particular asset or an entire trade is transferred by one company to another without raising any

provisions of chargeable gain.

By considering this aspect, it can be said that no capital gain tax will be charged on the

transaction of transferring chargeable assets from Brownleas plc to Retro Ltd.

2. Explanation of consideration of two companies as a group for the purpose of group relief

The two companies are considered as a group for the purpose of transferring chargeable

assets in order to make claim of relief in the taxation. With this relief they are able to make

reduction in their overall tax as loss of one company is compensated with the profit of another

company. In accordance with the provisions of UK taxation, a UK resident company is in

position to make claim of group relief in order to take benefit of set off of trading losses of a non

UK subsidiary however but resident of European Economic Area (EEA).

Tax consolidation is permitted by the UK in situation where companies in a group are not

considered as a single entity for the purpose of tax computation. Major benefit of this provision

is that tax loss of one company will be considered relievable for the tax profits of another

company (Henrekson and Sanandaji, 2011). By considering this aspect, company is in position

to surrender their losses in situation where losses of the accounting period (other than capital

gains) are higher than the taxable profits to a group member who have sufficient taxable profits

in the similar accounting period (Miller and Oats, 2012). Member Company can use these losses

to make reduction in their tax profits. Full group relief is permitted in situation where companies

have interest more than equal to the 75%.

Loss relief is usually available for the trading losses incurred by an overseas branch.

Provision stated in UK Paper F6 shows that no UK relief will be available for the trading losses

incurred by the overseas subsidiary company (Finney, 2010). In addition to this, UK capital

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

allowances will be available to the parent company if capital expenditure is made by the branch

company. However, benefit of capital allowances will not be attainable by parent company if

capital expenditure are done by subsidiary company. Further, profits of the overseas branch are

liable for the UK corporation tax in the year they are occurred regardless of the fact that they are

remitted to the UK or not. Overseas branch will not be considered as associated company but

overseas subsidiary will be treated as associated company due to which tax will be reduced

accordingly.

By considering this aspect, it will be beneficial for the Brownleas plc and Retro Ltd to

consider themselves as a group for the effective tax planning of reduction of tax charges to the

government.

3. Available option of tax relief to the Retro Ltd regarding tax adjustment of tax losses

In accordance with the described provisions of group relief, Retro Ltd is in position to

make tax adjustment for the set of tax losses of the company and group members. As per this

provision, tax adjusted trading loss of £318,000 will be surrendered to the Brownleas plc for the

purpose of tax planning.

By considering the computation of total taxable profits of Brownleas plc, it can be

noticed that company is required to pay tax on £2,081,540.00. However, due to the provisions of

group relief, they are able to take benefit of loss of Retro Ltd of £199,000.00 and net taxable

profit will be £1882540. Further, company will not be required to carry their losses in next

accounting years for the adjustments as they can surrender the entire loss to the member

company in order to make overall reduction in the profits. For the computation of group relief

computation of Table 3: Computation of total taxable profits of Brownleas plc.

4. Capital allowance treatment for the purchase of each asset

Capital allowance can be defined as the amount that can be deducted by the commercial

entities of UK from the overall amount of income or corporate tax on its profits. This amount is

derived from the certain purchases or investment outlined in the provisions of Capital

Allowances Act 2001 (Tae -Uk, 2009). Applicability of capital allowance on the assets

purchased by the company:

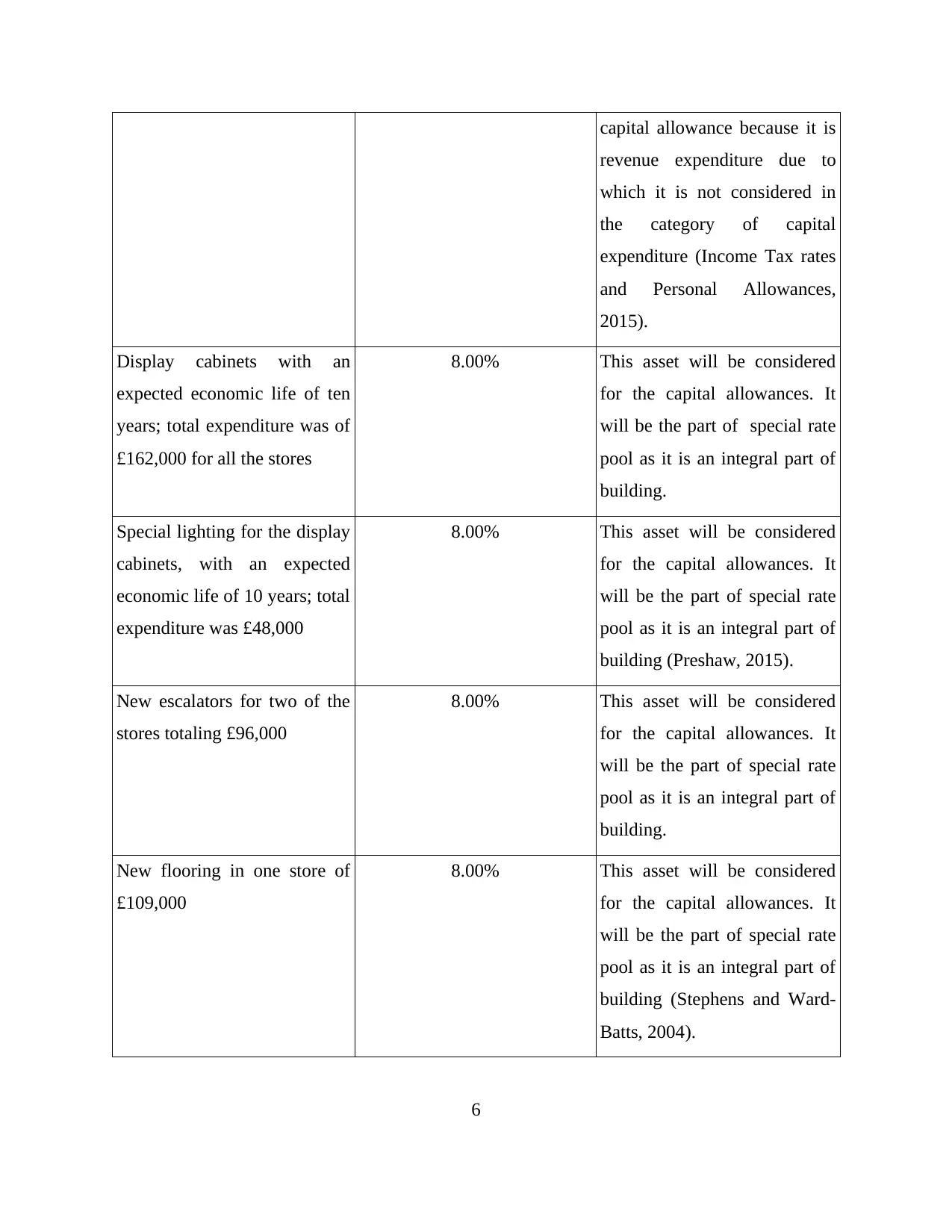

Asset Capital allowances Justification

Inventory of £400,000 - Inventory is not entitled for the

5

company. However, benefit of capital allowances will not be attainable by parent company if

capital expenditure are done by subsidiary company. Further, profits of the overseas branch are

liable for the UK corporation tax in the year they are occurred regardless of the fact that they are

remitted to the UK or not. Overseas branch will not be considered as associated company but

overseas subsidiary will be treated as associated company due to which tax will be reduced

accordingly.

By considering this aspect, it will be beneficial for the Brownleas plc and Retro Ltd to

consider themselves as a group for the effective tax planning of reduction of tax charges to the

government.

3. Available option of tax relief to the Retro Ltd regarding tax adjustment of tax losses

In accordance with the described provisions of group relief, Retro Ltd is in position to

make tax adjustment for the set of tax losses of the company and group members. As per this

provision, tax adjusted trading loss of £318,000 will be surrendered to the Brownleas plc for the

purpose of tax planning.

By considering the computation of total taxable profits of Brownleas plc, it can be

noticed that company is required to pay tax on £2,081,540.00. However, due to the provisions of

group relief, they are able to take benefit of loss of Retro Ltd of £199,000.00 and net taxable

profit will be £1882540. Further, company will not be required to carry their losses in next

accounting years for the adjustments as they can surrender the entire loss to the member

company in order to make overall reduction in the profits. For the computation of group relief

computation of Table 3: Computation of total taxable profits of Brownleas plc.

4. Capital allowance treatment for the purchase of each asset

Capital allowance can be defined as the amount that can be deducted by the commercial

entities of UK from the overall amount of income or corporate tax on its profits. This amount is

derived from the certain purchases or investment outlined in the provisions of Capital

Allowances Act 2001 (Tae -Uk, 2009). Applicability of capital allowance on the assets

purchased by the company:

Asset Capital allowances Justification

Inventory of £400,000 - Inventory is not entitled for the

5

capital allowance because it is

revenue expenditure due to

which it is not considered in

the category of capital

expenditure (Income Tax rates

and Personal Allowances,

2015).

Display cabinets with an

expected economic life of ten

years; total expenditure was of

£162,000 for all the stores

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building.

Special lighting for the display

cabinets, with an expected

economic life of 10 years; total

expenditure was £48,000

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building (Preshaw, 2015).

New escalators for two of the

stores totaling £96,000

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building.

New flooring in one store of

£109,000

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building (Stephens and Ward-

Batts, 2004).

6

revenue expenditure due to

which it is not considered in

the category of capital

expenditure (Income Tax rates

and Personal Allowances,

2015).

Display cabinets with an

expected economic life of ten

years; total expenditure was of

£162,000 for all the stores

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building.

Special lighting for the display

cabinets, with an expected

economic life of 10 years; total

expenditure was £48,000

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building (Preshaw, 2015).

New escalators for two of the

stores totaling £96,000

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building.

New flooring in one store of

£109,000

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building (Stephens and Ward-

Batts, 2004).

6

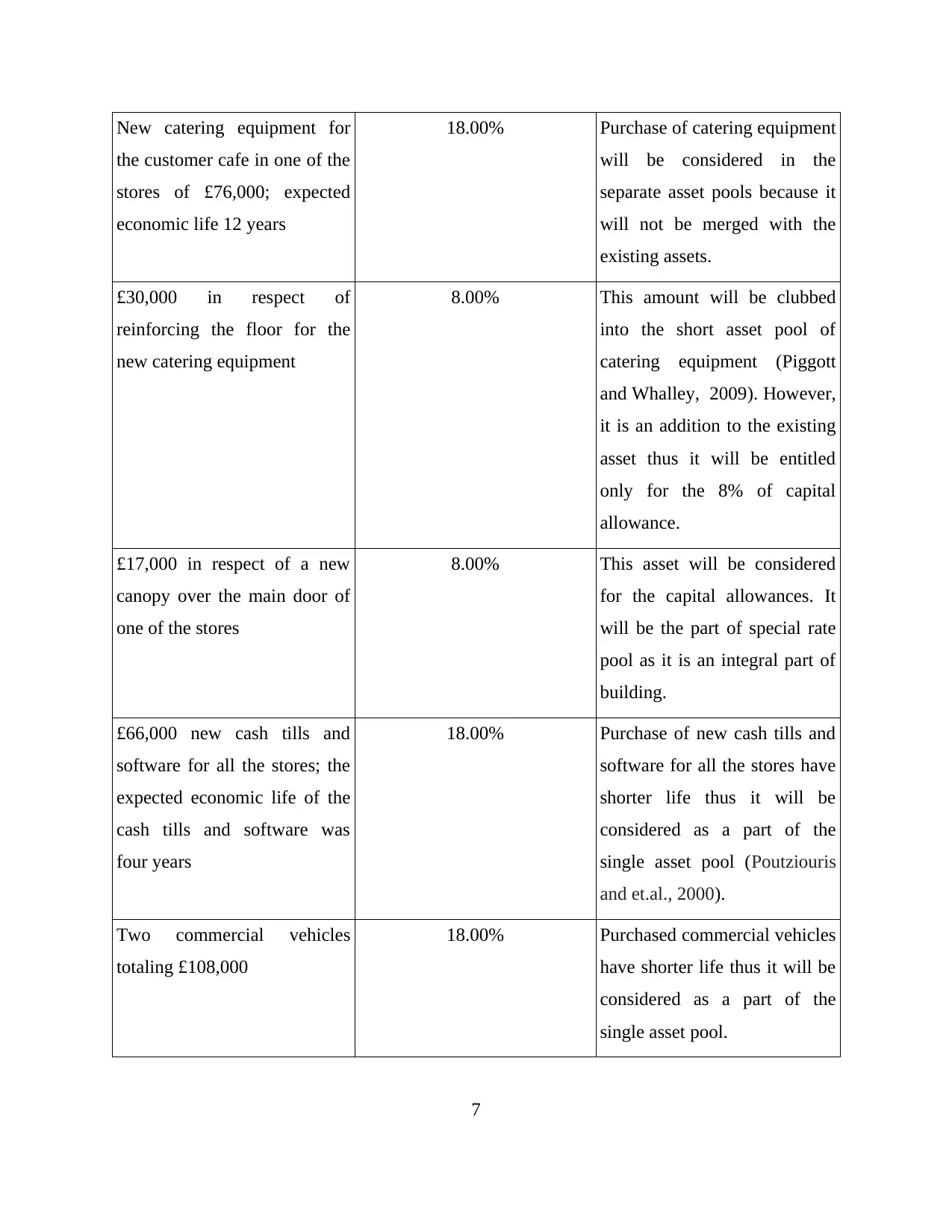

New catering equipment for

the customer cafe in one of the

stores of £76,000; expected

economic life 12 years

18.00% Purchase of catering equipment

will be considered in the

separate asset pools because it

will not be merged with the

existing assets.

£30,000 in respect of

reinforcing the floor for the

new catering equipment

8.00% This amount will be clubbed

into the short asset pool of

catering equipment (Piggott

and Whalley, 2009). However,

it is an addition to the existing

asset thus it will be entitled

only for the 8% of capital

allowance.

£17,000 in respect of a new

canopy over the main door of

one of the stores

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building.

£66,000 new cash tills and

software for all the stores; the

expected economic life of the

cash tills and software was

four years

18.00% Purchase of new cash tills and

software for all the stores have

shorter life thus it will be

considered as a part of the

single asset pool (Poutziouris

and et.al., 2000).

Two commercial vehicles

totaling £108,000

18.00% Purchased commercial vehicles

have shorter life thus it will be

considered as a part of the

single asset pool.

7

the customer cafe in one of the

stores of £76,000; expected

economic life 12 years

18.00% Purchase of catering equipment

will be considered in the

separate asset pools because it

will not be merged with the

existing assets.

£30,000 in respect of

reinforcing the floor for the

new catering equipment

8.00% This amount will be clubbed

into the short asset pool of

catering equipment (Piggott

and Whalley, 2009). However,

it is an addition to the existing

asset thus it will be entitled

only for the 8% of capital

allowance.

£17,000 in respect of a new

canopy over the main door of

one of the stores

8.00% This asset will be considered

for the capital allowances. It

will be the part of special rate

pool as it is an integral part of

building.

£66,000 new cash tills and

software for all the stores; the

expected economic life of the

cash tills and software was

four years

18.00% Purchase of new cash tills and

software for all the stores have

shorter life thus it will be

considered as a part of the

single asset pool (Poutziouris

and et.al., 2000).

Two commercial vehicles

totaling £108,000

18.00% Purchased commercial vehicles

have shorter life thus it will be

considered as a part of the

single asset pool.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

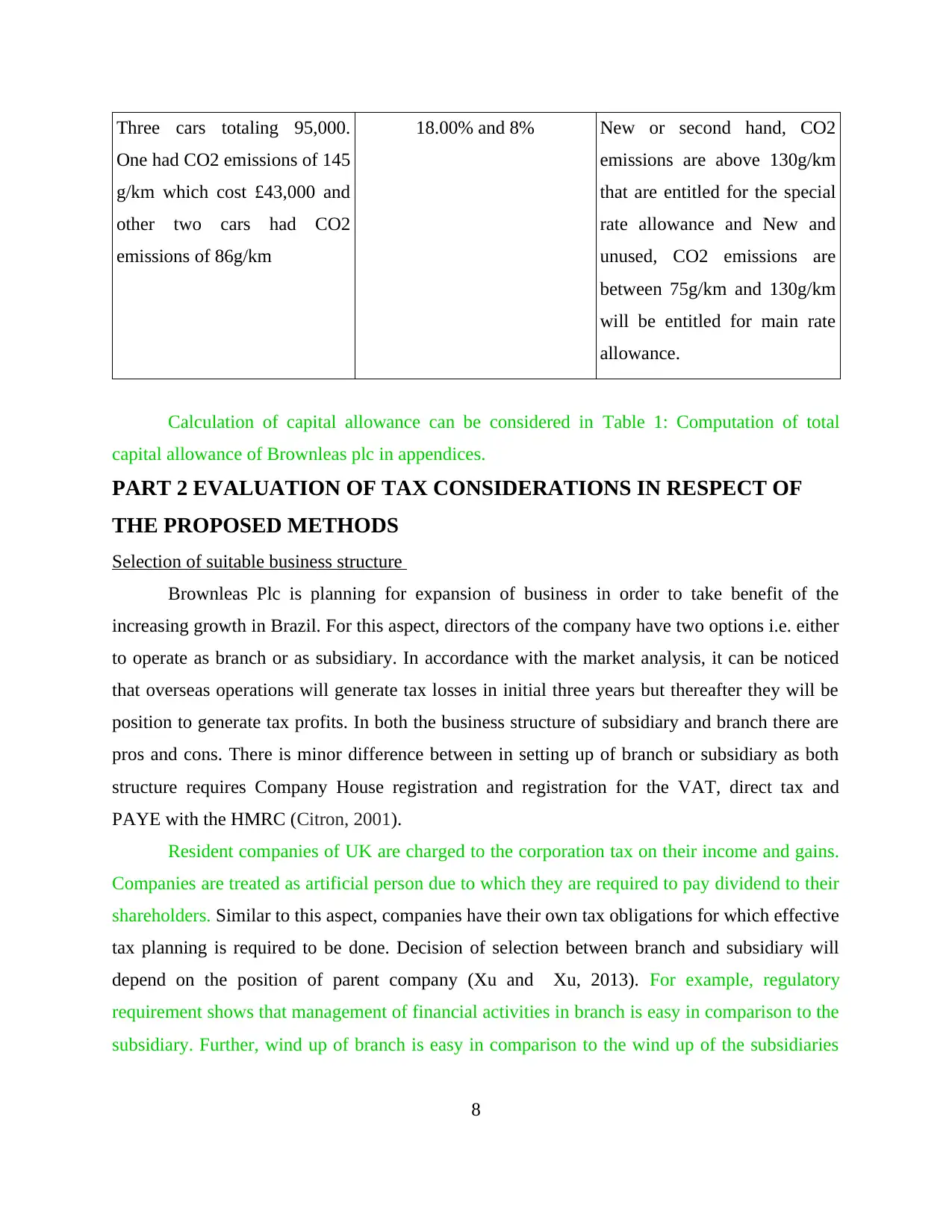

Three cars totaling 95,000.

One had CO2 emissions of 145

g/km which cost £43,000 and

other two cars had CO2

emissions of 86g/km

18.00% and 8% New or second hand, CO2

emissions are above 130g/km

that are entitled for the special

rate allowance and New and

unused, CO2 emissions are

between 75g/km and 130g/km

will be entitled for main rate

allowance.

Calculation of capital allowance can be considered in Table 1: Computation of total

capital allowance of Brownleas plc in appendices.

PART 2 EVALUATION OF TAX CONSIDERATIONS IN RESPECT OF

THE PROPOSED METHODS

Selection of suitable business structure

Brownleas Plc is planning for expansion of business in order to take benefit of the

increasing growth in Brazil. For this aspect, directors of the company have two options i.e. either

to operate as branch or as subsidiary. In accordance with the market analysis, it can be noticed

that overseas operations will generate tax losses in initial three years but thereafter they will be

position to generate tax profits. In both the business structure of subsidiary and branch there are

pros and cons. There is minor difference between in setting up of branch or subsidiary as both

structure requires Company House registration and registration for the VAT, direct tax and

PAYE with the HMRC (Citron, 2001).

Resident companies of UK are charged to the corporation tax on their income and gains.

Companies are treated as artificial person due to which they are required to pay dividend to their

shareholders. Similar to this aspect, companies have their own tax obligations for which effective

tax planning is required to be done. Decision of selection between branch and subsidiary will

depend on the position of parent company (Xu and Xu, 2013). For example, regulatory

requirement shows that management of financial activities in branch is easy in comparison to the

subsidiary. Further, wind up of branch is easy in comparison to the wind up of the subsidiaries

8

One had CO2 emissions of 145

g/km which cost £43,000 and

other two cars had CO2

emissions of 86g/km

18.00% and 8% New or second hand, CO2

emissions are above 130g/km

that are entitled for the special

rate allowance and New and

unused, CO2 emissions are

between 75g/km and 130g/km

will be entitled for main rate

allowance.

Calculation of capital allowance can be considered in Table 1: Computation of total

capital allowance of Brownleas plc in appendices.

PART 2 EVALUATION OF TAX CONSIDERATIONS IN RESPECT OF

THE PROPOSED METHODS

Selection of suitable business structure

Brownleas Plc is planning for expansion of business in order to take benefit of the

increasing growth in Brazil. For this aspect, directors of the company have two options i.e. either

to operate as branch or as subsidiary. In accordance with the market analysis, it can be noticed

that overseas operations will generate tax losses in initial three years but thereafter they will be

position to generate tax profits. In both the business structure of subsidiary and branch there are

pros and cons. There is minor difference between in setting up of branch or subsidiary as both

structure requires Company House registration and registration for the VAT, direct tax and

PAYE with the HMRC (Citron, 2001).

Resident companies of UK are charged to the corporation tax on their income and gains.

Companies are treated as artificial person due to which they are required to pay dividend to their

shareholders. Similar to this aspect, companies have their own tax obligations for which effective

tax planning is required to be done. Decision of selection between branch and subsidiary will

depend on the position of parent company (Xu and Xu, 2013). For example, regulatory

requirement shows that management of financial activities in branch is easy in comparison to the

subsidiary. Further, wind up of branch is easy in comparison to the wind up of the subsidiaries

8

for the UK companies (Terra and Wattèl, 2005). It is because, if experiment of Brownleas Plc

turns to be unsuccessful then branch will be automatically closed but subsidiary will require

formal procedure such as appointment of liquidator, striking off and winding up.

However, by considering tax position it will be suitable for the parent company to select

subsidiary for high benefits. In situation where, subsidiary is funded by the loan amount provided

by the parent company then organizations are able to take tax deduction of the interest paid to the

loan in order to make reduction in the profit (Taxation and investment in United Kingdom, 2015).

This benefit is not available in the tax accounting of the branch company as they are not entitled

to take tax deduction for that interest. Another difference between branch and subsidiary is

regarding computation of corporation tax. Branch of the company is subjected to the UK

corporation tax on the profits of the parent company. However, subsidiary company is subjected

for the corporation tax on its worldwide profits. It is because, subsidiary company has separate

legal existence from its parent company which branch is considered as part of the parent entity.

Start-up losses of branch is available to the overseas parent for the set off against home

profits for tax purposes. This aspect will be beneficial for the parent company as they can obtain

loss relief sooner in comparison to the subsidiary. It is because, losses of UK subsidiary is

required to be carried off for the set off in against of future profits as holding company cannot

use these losses for making reduction in amount of profit (Branch v Subsidiary, 2015). In

accordance with the provisions of transfer pricing in UK, parent companies are prevented from

reduction of their taxable total profits subjected to UK corporation tax. For example, holding

companies cannot sale their goods to the subsidiary company at below market price.

Applicability of the provisions on the business transactions

The transfer of goods between the companies

Management of Brownleas company will not be entitled to transfer their goods lower

than the market value if they expand their business by selecting structure of subsidiary. It

is because, restriction is imposed by the taxation policy of UK. Due to this aspect, it will

be beneficial for management to expand their business operations as branch instead

of subsidiary company. With this commercial structure, they can transfer the goods to the

branch at lower value in order to attain the tax advantage.

9

turns to be unsuccessful then branch will be automatically closed but subsidiary will require

formal procedure such as appointment of liquidator, striking off and winding up.

However, by considering tax position it will be suitable for the parent company to select

subsidiary for high benefits. In situation where, subsidiary is funded by the loan amount provided

by the parent company then organizations are able to take tax deduction of the interest paid to the

loan in order to make reduction in the profit (Taxation and investment in United Kingdom, 2015).

This benefit is not available in the tax accounting of the branch company as they are not entitled

to take tax deduction for that interest. Another difference between branch and subsidiary is

regarding computation of corporation tax. Branch of the company is subjected to the UK

corporation tax on the profits of the parent company. However, subsidiary company is subjected

for the corporation tax on its worldwide profits. It is because, subsidiary company has separate

legal existence from its parent company which branch is considered as part of the parent entity.

Start-up losses of branch is available to the overseas parent for the set off against home

profits for tax purposes. This aspect will be beneficial for the parent company as they can obtain

loss relief sooner in comparison to the subsidiary. It is because, losses of UK subsidiary is

required to be carried off for the set off in against of future profits as holding company cannot

use these losses for making reduction in amount of profit (Branch v Subsidiary, 2015). In

accordance with the provisions of transfer pricing in UK, parent companies are prevented from

reduction of their taxable total profits subjected to UK corporation tax. For example, holding

companies cannot sale their goods to the subsidiary company at below market price.

Applicability of the provisions on the business transactions

The transfer of goods between the companies

Management of Brownleas company will not be entitled to transfer their goods lower

than the market value if they expand their business by selecting structure of subsidiary. It

is because, restriction is imposed by the taxation policy of UK. Due to this aspect, it will

be beneficial for management to expand their business operations as branch instead

of subsidiary company. With this commercial structure, they can transfer the goods to the

branch at lower value in order to attain the tax advantage.

9

The provision of a loan from Brownleas plc to the overseas operations; interest will be

charges on this

In situation where business is expanded through subsidiary in Brazil then branch will be

required to pay taxes to the parent company and they can use this expenditure for the

purpose of tax deduction. It is because, both the organization have separate legal

existence and they are entitled for such tax planning. Although, this amount will be

chargeable for the parent company as a foreign income and they will be required to pay

tax on such income. However, in the case of branch, tax deduction of interest charges

cannot be taken by the subsidiary company. In this case, neither branch will be claim for

tax deduction for interest not parent company will be obliged to pay tax on the foreign

income.

The levying of a management charge from Brownleas plc to the overseas operation

In accordance with the provided information, overseas operations will be managed by the

board of directors of Brownleas plc. By considering the UK tax provisions, companies

are considered to be resident of UK if tier central management and control is exercised in

UK. The directors of the Brownleas plc are based and hold their meetings in UK. This

factor indicates that overseas branch is managed and controlled in UK thus it will have

residential status for the computation of tax. By considering this aspect transfer pricing

implications will be applied. Due to this aspect, company is required to apply arm length

prices.

Selection of suitable structure for the purpose of expansion

By considering the above described provisions, it would be beneficial for the Brownleas

plc to expand business as branch instead of using status of subsidiary. It is because, in this

structure they will be able to transfer good at lower price than market value. In addition to this,

they can take advantage of loss relief for make reduction in the tax obligation of parent company.

This benefit will not be available in the selection of subsidiary company (Piggott and Whalley,

2009). However, they will not be able to charge interest expenses for the tax deduction in the

computation of taxable profit.

By making comparative evaluation it can be noticed that benefit of loss relief is higher

than charge of interest as deductible expense. It is because, in selection of subsidiary only profit

10

charges on this

In situation where business is expanded through subsidiary in Brazil then branch will be

required to pay taxes to the parent company and they can use this expenditure for the

purpose of tax deduction. It is because, both the organization have separate legal

existence and they are entitled for such tax planning. Although, this amount will be

chargeable for the parent company as a foreign income and they will be required to pay

tax on such income. However, in the case of branch, tax deduction of interest charges

cannot be taken by the subsidiary company. In this case, neither branch will be claim for

tax deduction for interest not parent company will be obliged to pay tax on the foreign

income.

The levying of a management charge from Brownleas plc to the overseas operation

In accordance with the provided information, overseas operations will be managed by the

board of directors of Brownleas plc. By considering the UK tax provisions, companies

are considered to be resident of UK if tier central management and control is exercised in

UK. The directors of the Brownleas plc are based and hold their meetings in UK. This

factor indicates that overseas branch is managed and controlled in UK thus it will have

residential status for the computation of tax. By considering this aspect transfer pricing

implications will be applied. Due to this aspect, company is required to apply arm length

prices.

Selection of suitable structure for the purpose of expansion

By considering the above described provisions, it would be beneficial for the Brownleas

plc to expand business as branch instead of using status of subsidiary. It is because, in this

structure they will be able to transfer good at lower price than market value. In addition to this,

they can take advantage of loss relief for make reduction in the tax obligation of parent company.

This benefit will not be available in the selection of subsidiary company (Piggott and Whalley,

2009). However, they will not be able to charge interest expenses for the tax deduction in the

computation of taxable profit.

By making comparative evaluation it can be noticed that benefit of loss relief is higher

than charge of interest as deductible expense. It is because, in selection of subsidiary only profit

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

of overseas company will be reduced and the ultimate loss will be carried off for the future years.

However, in the case of branch, there is benefit to the both the companies as loss will be utilized

in the similar year and parent company will not be required to pay tax on the interest income. In

addition to this, they can also make claim for the relief from double taxation in the future years.

Established and wind up of branch is also easy in comparison to the subsidiary (Terra and

Wattèl, 2005 ). In addition to this capital allowances will also be available to the organization on

capital expenditure. Thus, evaluation through aspects of management accounting and tax

provisions recommends that management of Brownleas plc should consider the status of branch

instead of subsidiary.

CONCLUSION

In accordance with the present study, conclusion can be drawn that management of

companies are required to do proper tax planning in order to make reduction in their obligation.

For this aspect, they are required to make comparative assessment of optional tax provisions for

effective tax planning. In this manner, management of the companies will be able to retain higher

benefits for the future expansion. By considering the evaluation of second part, it would be

beneficial for company expand overseas business in form of branch for the better tax relief.

11

However, in the case of branch, there is benefit to the both the companies as loss will be utilized

in the similar year and parent company will not be required to pay tax on the interest income. In

addition to this, they can also make claim for the relief from double taxation in the future years.

Established and wind up of branch is also easy in comparison to the subsidiary (Terra and

Wattèl, 2005 ). In addition to this capital allowances will also be available to the organization on

capital expenditure. Thus, evaluation through aspects of management accounting and tax

provisions recommends that management of Brownleas plc should consider the status of branch

instead of subsidiary.

CONCLUSION

In accordance with the present study, conclusion can be drawn that management of

companies are required to do proper tax planning in order to make reduction in their obligation.

For this aspect, they are required to make comparative assessment of optional tax provisions for

effective tax planning. In this manner, management of the companies will be able to retain higher

benefits for the future expansion. By considering the evaluation of second part, it would be

beneficial for company expand overseas business in form of branch for the better tax relief.

11

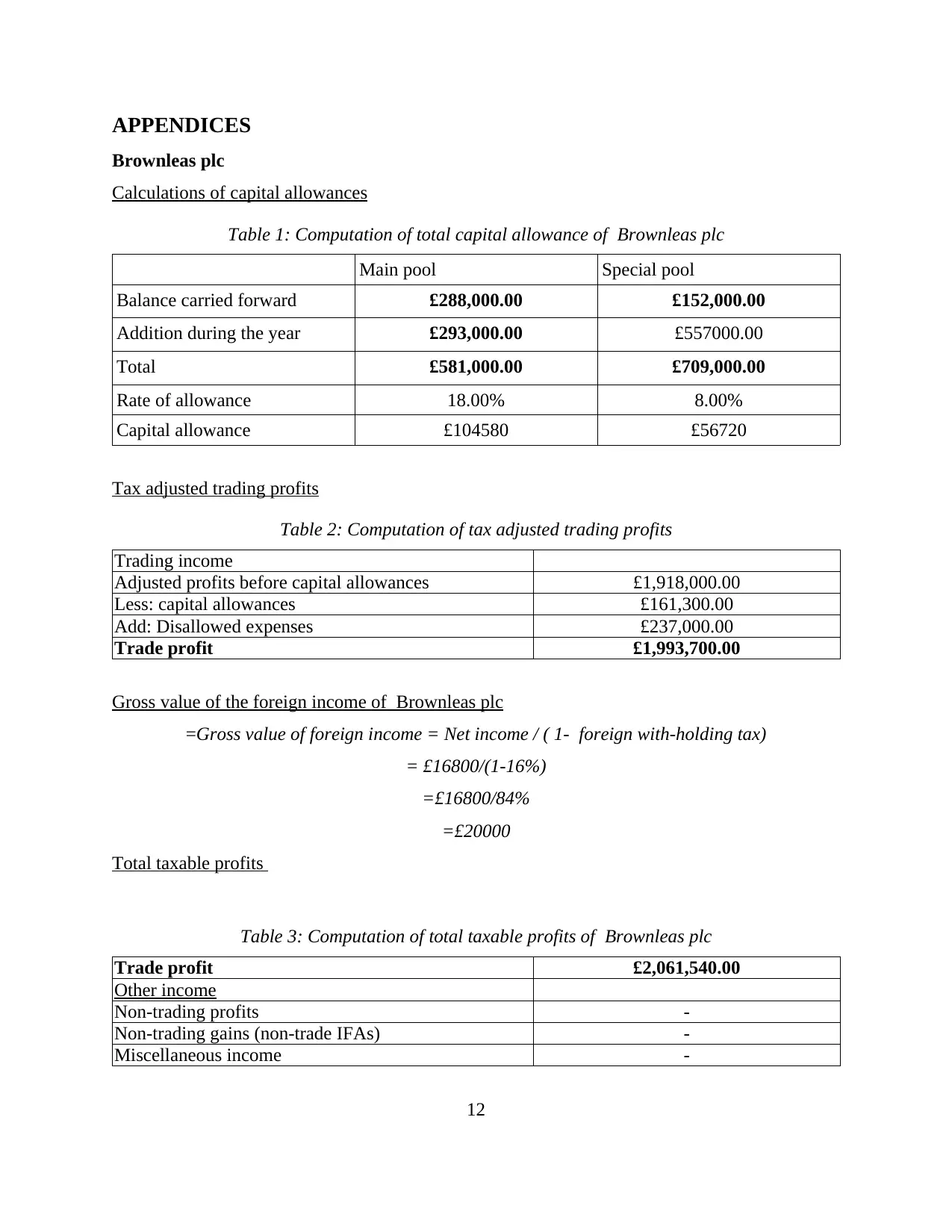

APPENDICES

Brownleas plc

Calculations of capital allowances

Table 1: Computation of total capital allowance of Brownleas plc

Main pool Special pool

Balance carried forward £288,000.00 £152,000.00

Addition during the year £293,000.00 £557000.00

Total £581,000.00 £709,000.00

Rate of allowance 18.00% 8.00%

Capital allowance £104580 £56720

Tax adjusted trading profits

Table 2: Computation of tax adjusted trading profits

Trading income

Adjusted profits before capital allowances £1,918,000.00

Less: capital allowances £161,300.00

Add: Disallowed expenses £237,000.00

Trade profit £1,993,700.00

Gross value of the foreign income of Brownleas plc

=Gross value of foreign income = Net income / ( 1- foreign with-holding tax)

= £16800/(1-16%)

=£16800/84%

=£20000

Total taxable profits

Table 3: Computation of total taxable profits of Brownleas plc

Trade profit £2,061,540.00

Other income

Non-trading profits -

Non-trading gains (non-trade IFAs) -

Miscellaneous income -

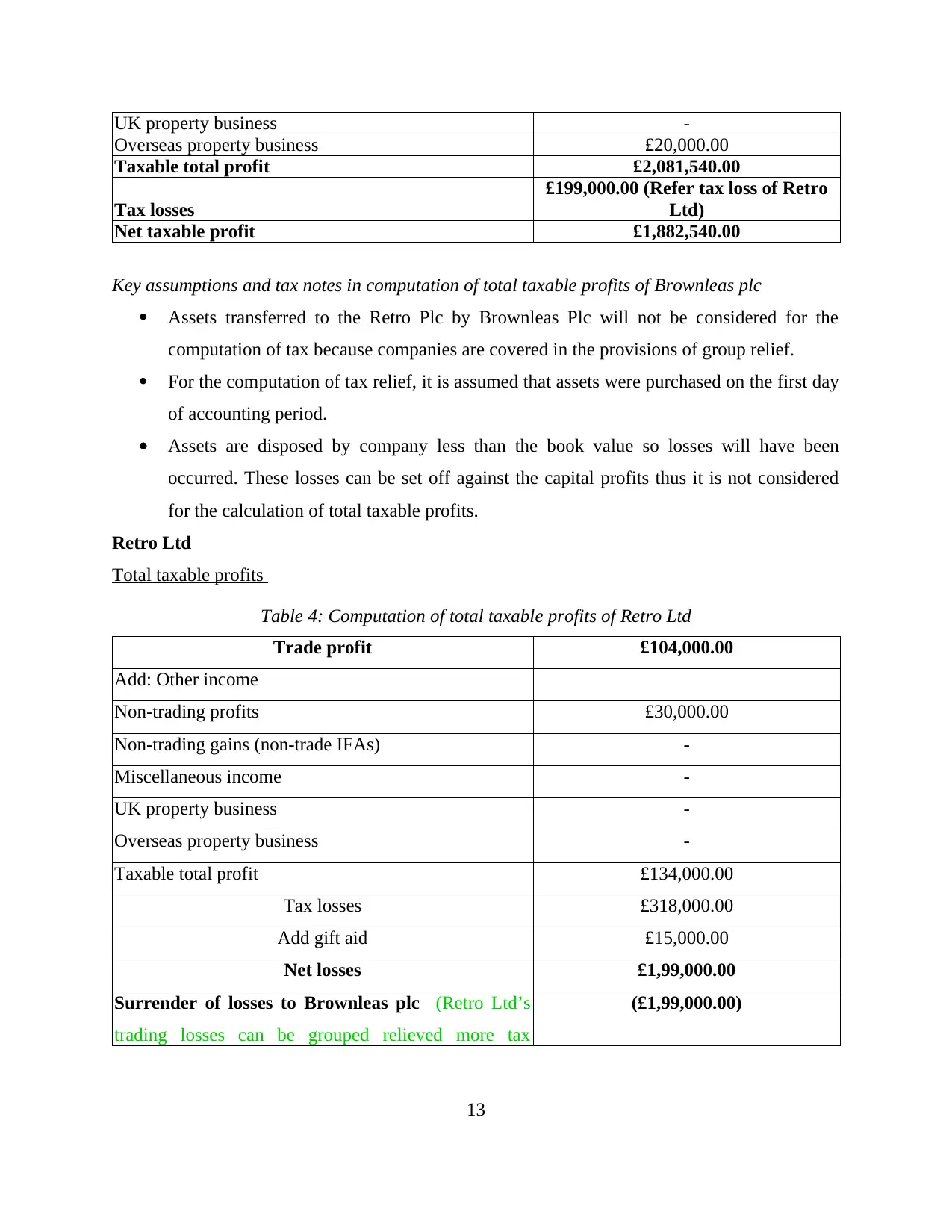

12

Brownleas plc

Calculations of capital allowances

Table 1: Computation of total capital allowance of Brownleas plc

Main pool Special pool

Balance carried forward £288,000.00 £152,000.00

Addition during the year £293,000.00 £557000.00

Total £581,000.00 £709,000.00

Rate of allowance 18.00% 8.00%

Capital allowance £104580 £56720

Tax adjusted trading profits

Table 2: Computation of tax adjusted trading profits

Trading income

Adjusted profits before capital allowances £1,918,000.00

Less: capital allowances £161,300.00

Add: Disallowed expenses £237,000.00

Trade profit £1,993,700.00

Gross value of the foreign income of Brownleas plc

=Gross value of foreign income = Net income / ( 1- foreign with-holding tax)

= £16800/(1-16%)

=£16800/84%

=£20000

Total taxable profits

Table 3: Computation of total taxable profits of Brownleas plc

Trade profit £2,061,540.00

Other income

Non-trading profits -

Non-trading gains (non-trade IFAs) -

Miscellaneous income -

12

UK property business -

Overseas property business £20,000.00

Taxable total profit £2,081,540.00

Tax losses

£199,000.00 (Refer tax loss of Retro

Ltd)

Net taxable profit £1,882,540.00

Key assumptions and tax notes in computation of total taxable profits of Brownleas plc

Assets transferred to the Retro Plc by Brownleas Plc will not be considered for the

computation of tax because companies are covered in the provisions of group relief.

For the computation of tax relief, it is assumed that assets were purchased on the first day

of accounting period.

Assets are disposed by company less than the book value so losses will have been

occurred. These losses can be set off against the capital profits thus it is not considered

for the calculation of total taxable profits.

Retro Ltd

Total taxable profits

Table 4: Computation of total taxable profits of Retro Ltd

Trade profit £104,000.00

Add: Other income

Non-trading profits £30,000.00

Non-trading gains (non-trade IFAs) -

Miscellaneous income -

UK property business -

Overseas property business -

Taxable total profit £134,000.00

Tax losses £318,000.00

Add gift aid £15,000.00

Net losses £1,99,000.00

Surrender of losses to Brownleas plc (Retro Ltd’s

trading losses can be grouped relieved more tax

(£1,99,000.00)

13

Overseas property business £20,000.00

Taxable total profit £2,081,540.00

Tax losses

£199,000.00 (Refer tax loss of Retro

Ltd)

Net taxable profit £1,882,540.00

Key assumptions and tax notes in computation of total taxable profits of Brownleas plc

Assets transferred to the Retro Plc by Brownleas Plc will not be considered for the

computation of tax because companies are covered in the provisions of group relief.

For the computation of tax relief, it is assumed that assets were purchased on the first day

of accounting period.

Assets are disposed by company less than the book value so losses will have been

occurred. These losses can be set off against the capital profits thus it is not considered

for the calculation of total taxable profits.

Retro Ltd

Total taxable profits

Table 4: Computation of total taxable profits of Retro Ltd

Trade profit £104,000.00

Add: Other income

Non-trading profits £30,000.00

Non-trading gains (non-trade IFAs) -

Miscellaneous income -

UK property business -

Overseas property business -

Taxable total profit £134,000.00

Tax losses £318,000.00

Add gift aid £15,000.00

Net losses £1,99,000.00

Surrender of losses to Brownleas plc (Retro Ltd’s

trading losses can be grouped relieved more tax

(£1,99,000.00)

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

efficiently consider calculation of tax of Brownleas

Plc)

Net losses carried forward -

14

Plc)

Net losses carried forward -

14

REFERENCES

Books and journals

Becker, J. and Fuest, C., 2011. The taxation of foreign profits—The old view, the new view and

a pragmatic view. Intereconomics. 46(2). pp. 92-97.

Citron, D. B., 2001. The valuation of deferred taxation: Evidence from the UK partial provision

approach. Journal of Business Finance & Accounting. 28(7‐8). Pp.821-852.

Dowell, S., 2013. History of Taxation and Taxes in England. Routledge.

Garrett, G. and Mitchell, D., 2001. Globalization, government spending and taxation in the

OECD. European Journal of Political Research. 39(2). Pp.145-177.

Henrekson, M. and Sanandaji, T., 2011. Entrepreneurship and the theory of taxation. Small

Business Economics. 37(2). pp. 167-185.

Miller, A. and Oats, L., 2012. Principles of international taxation. A&C Black.

Tae -Uk, M., 2009. Education and Tax. Seoultaxlawreview, 15(3). pp.137-174.

Terra, B. and Wattèl, P., 2005. European tax law. The Hague: Kluwer Law International.

Xu, E. and Xu, K., 2013. A Multilevel analysis of the effect of taxation incentives on innovation

performance. Engineering Management, IEEE Transactions on. 60(1). pp. 137-147.

Citron, D. B., 2001. The valuation of deferred taxation: Evidence from the UK partial provision

approach.Journal of Business Finance & Accounting. 28(7‐8). Pp.821-852.

Poutziouris, P. and et.al., 2000. Taxation and the performance of technology based small firms in

the UK. Small Business Economics. 14(1). Pp.11-36.

Piggott, J. and Whalley, J., 2009. UK tax policy and applied general equilibrium

analysis. Cambridge Books.

Stephens, M. and Ward-Batts, J., 2004. The impact of separate taxation on the intra-household

allocation of assets: evidence from the UK. Journal of Public Economics. 88(9). pp.1989-

2007.

Online

Income Tax rates and Personal Allowances. 2015. [Online]. Available

at:<https://www.gov.uk/income-tax-rates>. [Accessed on 5th January 2016].

Preshaw, J., 2015. Management of Taxes Sub-Committee. [Online]. Available

at:<https://www.tax.org.uk/tax-policy/remit-of-technical-committee/

ManagementofTaxes>. [Accessed on 5th January 2016].

Taxation and investment in United Kingdom, 2015. [Pdf]. Available

at:<https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

unitedkingdomguide-2015.pdf>. [Accessed on 5th January 2016].

15

Books and journals

Becker, J. and Fuest, C., 2011. The taxation of foreign profits—The old view, the new view and

a pragmatic view. Intereconomics. 46(2). pp. 92-97.

Citron, D. B., 2001. The valuation of deferred taxation: Evidence from the UK partial provision

approach. Journal of Business Finance & Accounting. 28(7‐8). Pp.821-852.

Dowell, S., 2013. History of Taxation and Taxes in England. Routledge.

Garrett, G. and Mitchell, D., 2001. Globalization, government spending and taxation in the

OECD. European Journal of Political Research. 39(2). Pp.145-177.

Henrekson, M. and Sanandaji, T., 2011. Entrepreneurship and the theory of taxation. Small

Business Economics. 37(2). pp. 167-185.

Miller, A. and Oats, L., 2012. Principles of international taxation. A&C Black.

Tae -Uk, M., 2009. Education and Tax. Seoultaxlawreview, 15(3). pp.137-174.

Terra, B. and Wattèl, P., 2005. European tax law. The Hague: Kluwer Law International.

Xu, E. and Xu, K., 2013. A Multilevel analysis of the effect of taxation incentives on innovation

performance. Engineering Management, IEEE Transactions on. 60(1). pp. 137-147.

Citron, D. B., 2001. The valuation of deferred taxation: Evidence from the UK partial provision

approach.Journal of Business Finance & Accounting. 28(7‐8). Pp.821-852.

Poutziouris, P. and et.al., 2000. Taxation and the performance of technology based small firms in

the UK. Small Business Economics. 14(1). Pp.11-36.

Piggott, J. and Whalley, J., 2009. UK tax policy and applied general equilibrium

analysis. Cambridge Books.

Stephens, M. and Ward-Batts, J., 2004. The impact of separate taxation on the intra-household

allocation of assets: evidence from the UK. Journal of Public Economics. 88(9). pp.1989-

2007.

Online

Income Tax rates and Personal Allowances. 2015. [Online]. Available

at:<https://www.gov.uk/income-tax-rates>. [Accessed on 5th January 2016].

Preshaw, J., 2015. Management of Taxes Sub-Committee. [Online]. Available

at:<https://www.tax.org.uk/tax-policy/remit-of-technical-committee/

ManagementofTaxes>. [Accessed on 5th January 2016].

Taxation and investment in United Kingdom, 2015. [Pdf]. Available

at:<https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

unitedkingdomguide-2015.pdf>. [Accessed on 5th January 2016].

15

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.