UGB225 Business Taxation: Alternative Assessment Report 2021/22

VerifiedAdded on 2023/06/17

|12

|3653

|269

Report

AI Summary

This report provides a comprehensive analysis of business taxation, starting with the calculation of tax-adjusted trading profit for Linda's business, highlighting necessary adjustments to the accounting profits. It distinguishes between employed and self-employed individuals, discussing the risks, freedoms, expenses, and benefits associated with each. The report also explores the reasons behind the increasing preference for self-employment, particularly in the context of IR35 legislation. Furthermore, it delves into six badges of trade, providing examples to illustrate their application in determining whether a business is indeed trading. Finally, the report discusses various VAT schemes available to VAT-registered businesses, offering a complete overview of key aspects of business taxation. Desklib offers a platform to access similar solved assignments and study tools.

Business Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................5

Distinction between individual who is employed and one who is self- employed.....................5

Reason for which people prefer to be self employed rather to being employed.........................6

QUESTION 3...................................................................................................................................7

Discussing six badges of trade along with example....................................................................7

Discussing the different types of VAT schemes available to the VAT registered business.......9

QUESTION 4...................................................................................................................................9

REFERENCES..............................................................................................................................12

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................5

Distinction between individual who is employed and one who is self- employed.....................5

Reason for which people prefer to be self employed rather to being employed.........................6

QUESTION 3...................................................................................................................................7

Discussing six badges of trade along with example....................................................................7

Discussing the different types of VAT schemes available to the VAT registered business.......9

QUESTION 4...................................................................................................................................9

REFERENCES..............................................................................................................................12

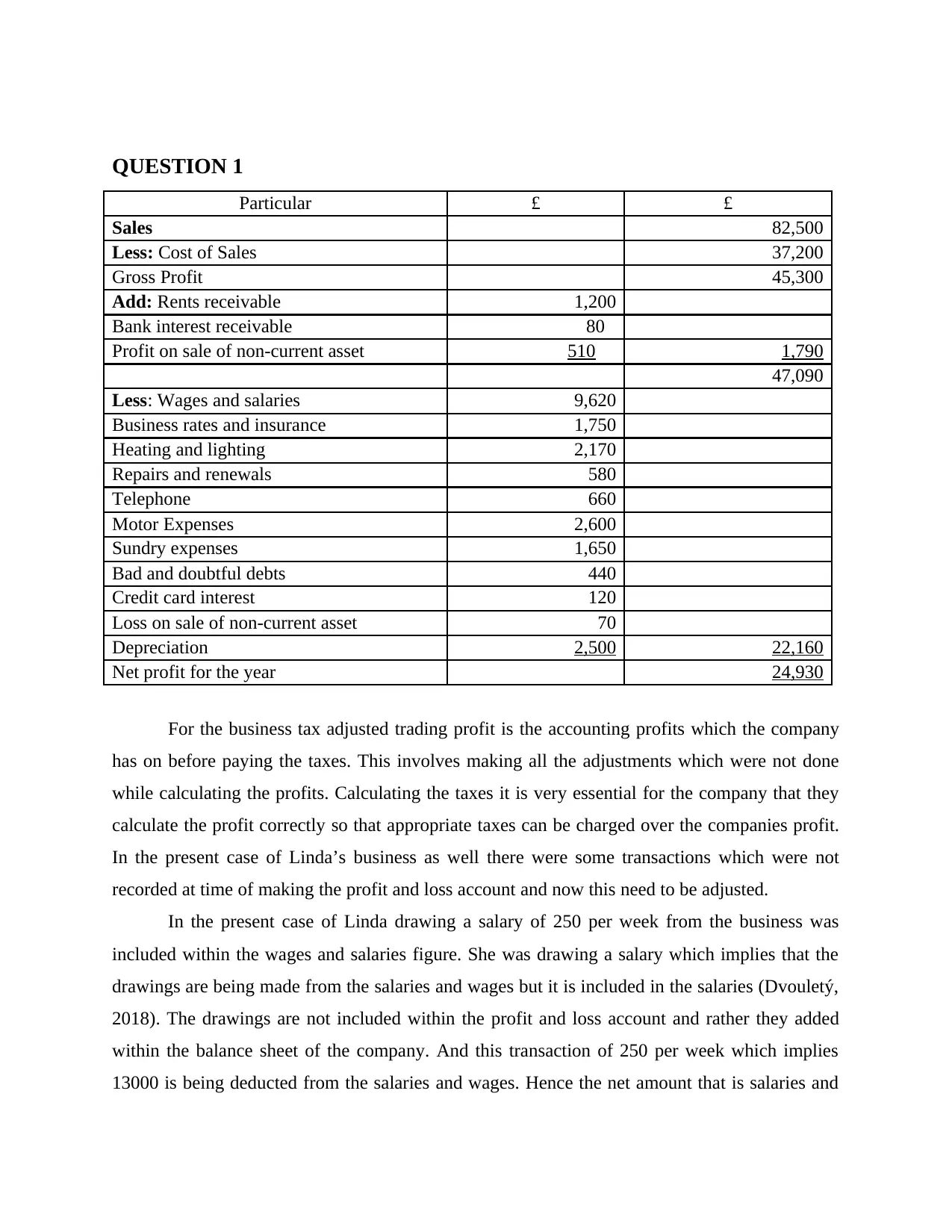

QUESTION 1

Particular £ £

Sales 82,500

Less: Cost of Sales 37,200

Gross Profit 45,300

Add: Rents receivable 1,200

Bank interest receivable 80

Profit on sale of non-current asset 510 1,790

47,090

Less: Wages and salaries 9,620

Business rates and insurance 1,750

Heating and lighting 2,170

Repairs and renewals 580

Telephone 660

Motor Expenses 2,600

Sundry expenses 1,650

Bad and doubtful debts 440

Credit card interest 120

Loss on sale of non-current asset 70

Depreciation 2,500 22,160

Net profit for the year 24,930

For the business tax adjusted trading profit is the accounting profits which the company

has on before paying the taxes. This involves making all the adjustments which were not done

while calculating the profits. Calculating the taxes it is very essential for the company that they

calculate the profit correctly so that appropriate taxes can be charged over the companies profit.

In the present case of Linda’s business as well there were some transactions which were not

recorded at time of making the profit and loss account and now this need to be adjusted.

In the present case of Linda drawing a salary of 250 per week from the business was

included within the wages and salaries figure. She was drawing a salary which implies that the

drawings are being made from the salaries and wages but it is included in the salaries (Dvouletý,

2018). The drawings are not included within the profit and loss account and rather they added

within the balance sheet of the company. And this transaction of 250 per week which implies

13000 is being deducted from the salaries and wages. Hence the net amount that is salaries and

Particular £ £

Sales 82,500

Less: Cost of Sales 37,200

Gross Profit 45,300

Add: Rents receivable 1,200

Bank interest receivable 80

Profit on sale of non-current asset 510 1,790

47,090

Less: Wages and salaries 9,620

Business rates and insurance 1,750

Heating and lighting 2,170

Repairs and renewals 580

Telephone 660

Motor Expenses 2,600

Sundry expenses 1,650

Bad and doubtful debts 440

Credit card interest 120

Loss on sale of non-current asset 70

Depreciation 2,500 22,160

Net profit for the year 24,930

For the business tax adjusted trading profit is the accounting profits which the company

has on before paying the taxes. This involves making all the adjustments which were not done

while calculating the profits. Calculating the taxes it is very essential for the company that they

calculate the profit correctly so that appropriate taxes can be charged over the companies profit.

In the present case of Linda’s business as well there were some transactions which were not

recorded at time of making the profit and loss account and now this need to be adjusted.

In the present case of Linda drawing a salary of 250 per week from the business was

included within the wages and salaries figure. She was drawing a salary which implies that the

drawings are being made from the salaries and wages but it is included in the salaries (Dvouletý,

2018). The drawings are not included within the profit and loss account and rather they added

within the balance sheet of the company. And this transaction of 250 per week which implies

13000 is being deducted from the salaries and wages. Hence the net amount that is salaries and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

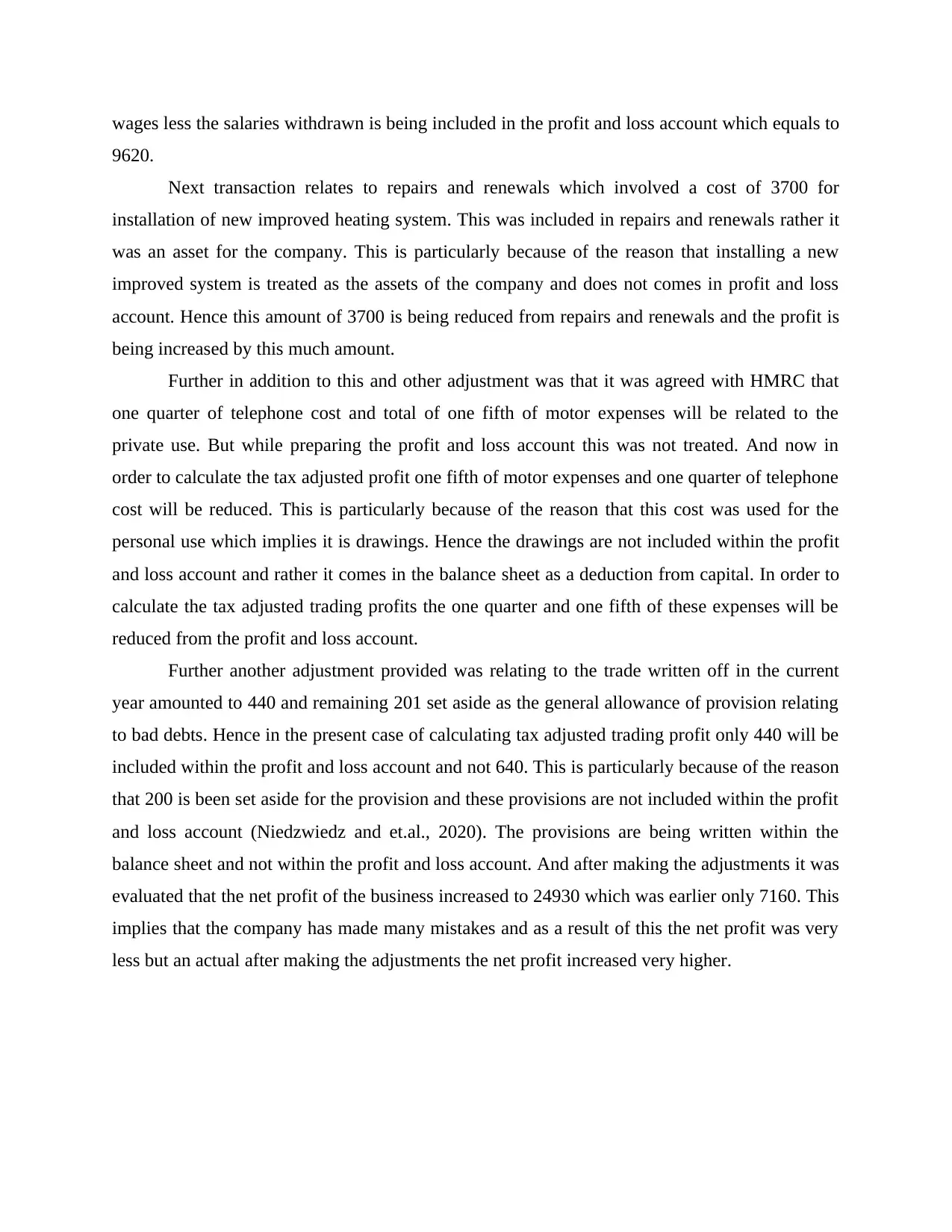

wages less the salaries withdrawn is being included in the profit and loss account which equals to

9620.

Next transaction relates to repairs and renewals which involved a cost of 3700 for

installation of new improved heating system. This was included in repairs and renewals rather it

was an asset for the company. This is particularly because of the reason that installing a new

improved system is treated as the assets of the company and does not comes in profit and loss

account. Hence this amount of 3700 is being reduced from repairs and renewals and the profit is

being increased by this much amount.

Further in addition to this and other adjustment was that it was agreed with HMRC that

one quarter of telephone cost and total of one fifth of motor expenses will be related to the

private use. But while preparing the profit and loss account this was not treated. And now in

order to calculate the tax adjusted profit one fifth of motor expenses and one quarter of telephone

cost will be reduced. This is particularly because of the reason that this cost was used for the

personal use which implies it is drawings. Hence the drawings are not included within the profit

and loss account and rather it comes in the balance sheet as a deduction from capital. In order to

calculate the tax adjusted trading profits the one quarter and one fifth of these expenses will be

reduced from the profit and loss account.

Further another adjustment provided was relating to the trade written off in the current

year amounted to 440 and remaining 201 set aside as the general allowance of provision relating

to bad debts. Hence in the present case of calculating tax adjusted trading profit only 440 will be

included within the profit and loss account and not 640. This is particularly because of the reason

that 200 is been set aside for the provision and these provisions are not included within the profit

and loss account (Niedzwiedz and et.al., 2020). The provisions are being written within the

balance sheet and not within the profit and loss account. And after making the adjustments it was

evaluated that the net profit of the business increased to 24930 which was earlier only 7160. This

implies that the company has made many mistakes and as a result of this the net profit was very

less but an actual after making the adjustments the net profit increased very higher.

9620.

Next transaction relates to repairs and renewals which involved a cost of 3700 for

installation of new improved heating system. This was included in repairs and renewals rather it

was an asset for the company. This is particularly because of the reason that installing a new

improved system is treated as the assets of the company and does not comes in profit and loss

account. Hence this amount of 3700 is being reduced from repairs and renewals and the profit is

being increased by this much amount.

Further in addition to this and other adjustment was that it was agreed with HMRC that

one quarter of telephone cost and total of one fifth of motor expenses will be related to the

private use. But while preparing the profit and loss account this was not treated. And now in

order to calculate the tax adjusted profit one fifth of motor expenses and one quarter of telephone

cost will be reduced. This is particularly because of the reason that this cost was used for the

personal use which implies it is drawings. Hence the drawings are not included within the profit

and loss account and rather it comes in the balance sheet as a deduction from capital. In order to

calculate the tax adjusted trading profits the one quarter and one fifth of these expenses will be

reduced from the profit and loss account.

Further another adjustment provided was relating to the trade written off in the current

year amounted to 440 and remaining 201 set aside as the general allowance of provision relating

to bad debts. Hence in the present case of calculating tax adjusted trading profit only 440 will be

included within the profit and loss account and not 640. This is particularly because of the reason

that 200 is been set aside for the provision and these provisions are not included within the profit

and loss account (Niedzwiedz and et.al., 2020). The provisions are being written within the

balance sheet and not within the profit and loss account. And after making the adjustments it was

evaluated that the net profit of the business increased to 24930 which was earlier only 7160. This

implies that the company has made many mistakes and as a result of this the net profit was very

less but an actual after making the adjustments the net profit increased very higher.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

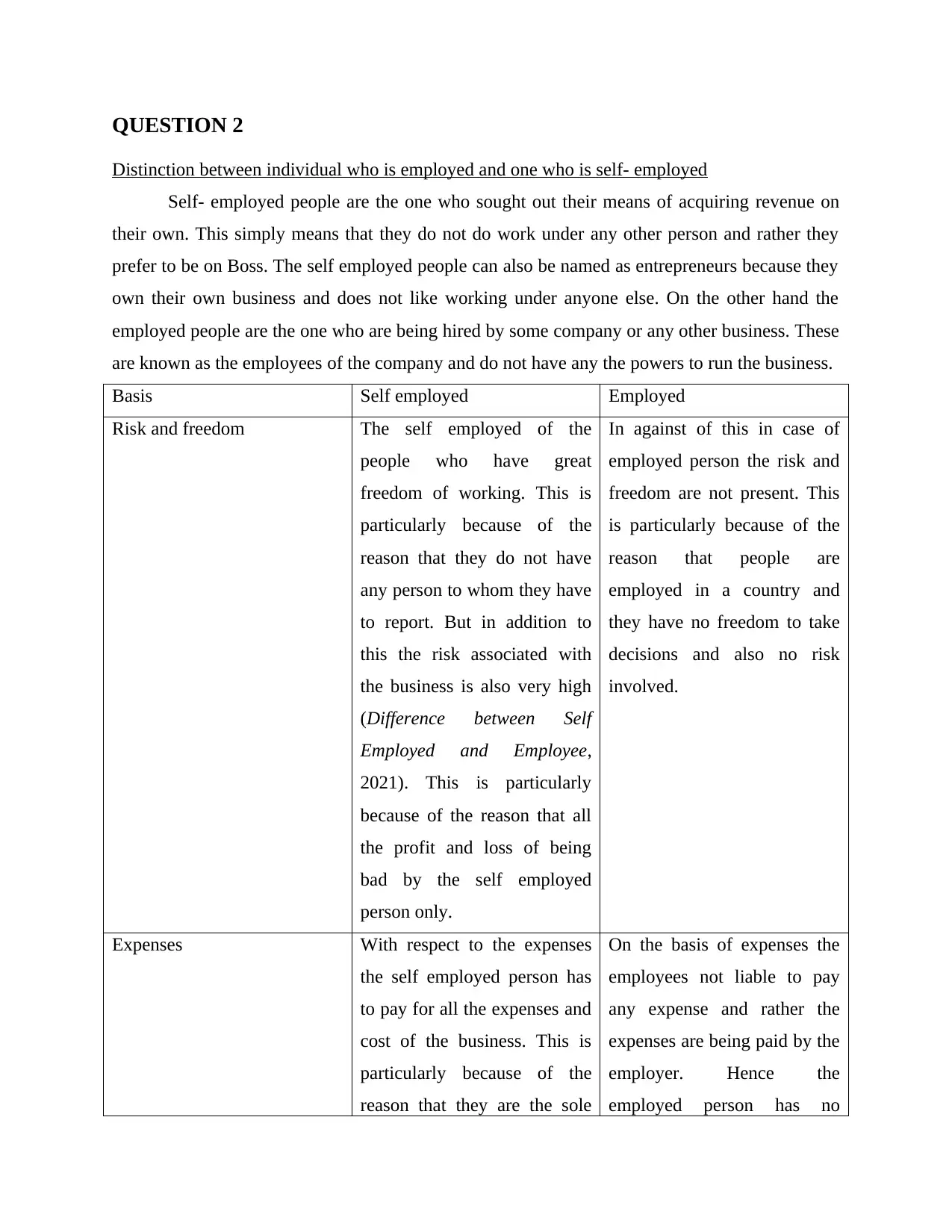

QUESTION 2

Distinction between individual who is employed and one who is self- employed

Self- employed people are the one who sought out their means of acquiring revenue on

their own. This simply means that they do not do work under any other person and rather they

prefer to be on Boss. The self employed people can also be named as entrepreneurs because they

own their own business and does not like working under anyone else. On the other hand the

employed people are the one who are being hired by some company or any other business. These

are known as the employees of the company and do not have any the powers to run the business.

Basis Self employed Employed

Risk and freedom The self employed of the

people who have great

freedom of working. This is

particularly because of the

reason that they do not have

any person to whom they have

to report. But in addition to

this the risk associated with

the business is also very high

(Difference between Self

Employed and Employee,

2021). This is particularly

because of the reason that all

the profit and loss of being

bad by the self employed

person only.

In against of this in case of

employed person the risk and

freedom are not present. This

is particularly because of the

reason that people are

employed in a country and

they have no freedom to take

decisions and also no risk

involved.

Expenses With respect to the expenses

the self employed person has

to pay for all the expenses and

cost of the business. This is

particularly because of the

reason that they are the sole

On the basis of expenses the

employees not liable to pay

any expense and rather the

expenses are being paid by the

employer. Hence the

employed person has no

Distinction between individual who is employed and one who is self- employed

Self- employed people are the one who sought out their means of acquiring revenue on

their own. This simply means that they do not do work under any other person and rather they

prefer to be on Boss. The self employed people can also be named as entrepreneurs because they

own their own business and does not like working under anyone else. On the other hand the

employed people are the one who are being hired by some company or any other business. These

are known as the employees of the company and do not have any the powers to run the business.

Basis Self employed Employed

Risk and freedom The self employed of the

people who have great

freedom of working. This is

particularly because of the

reason that they do not have

any person to whom they have

to report. But in addition to

this the risk associated with

the business is also very high

(Difference between Self

Employed and Employee,

2021). This is particularly

because of the reason that all

the profit and loss of being

bad by the self employed

person only.

In against of this in case of

employed person the risk and

freedom are not present. This

is particularly because of the

reason that people are

employed in a country and

they have no freedom to take

decisions and also no risk

involved.

Expenses With respect to the expenses

the self employed person has

to pay for all the expenses and

cost of the business. This is

particularly because of the

reason that they are the sole

On the basis of expenses the

employees not liable to pay

any expense and rather the

expenses are being paid by the

employer. Hence the

employed person has no

owner of the business and

each and every expense is

being that by that person only.

liability to pay any expenses.

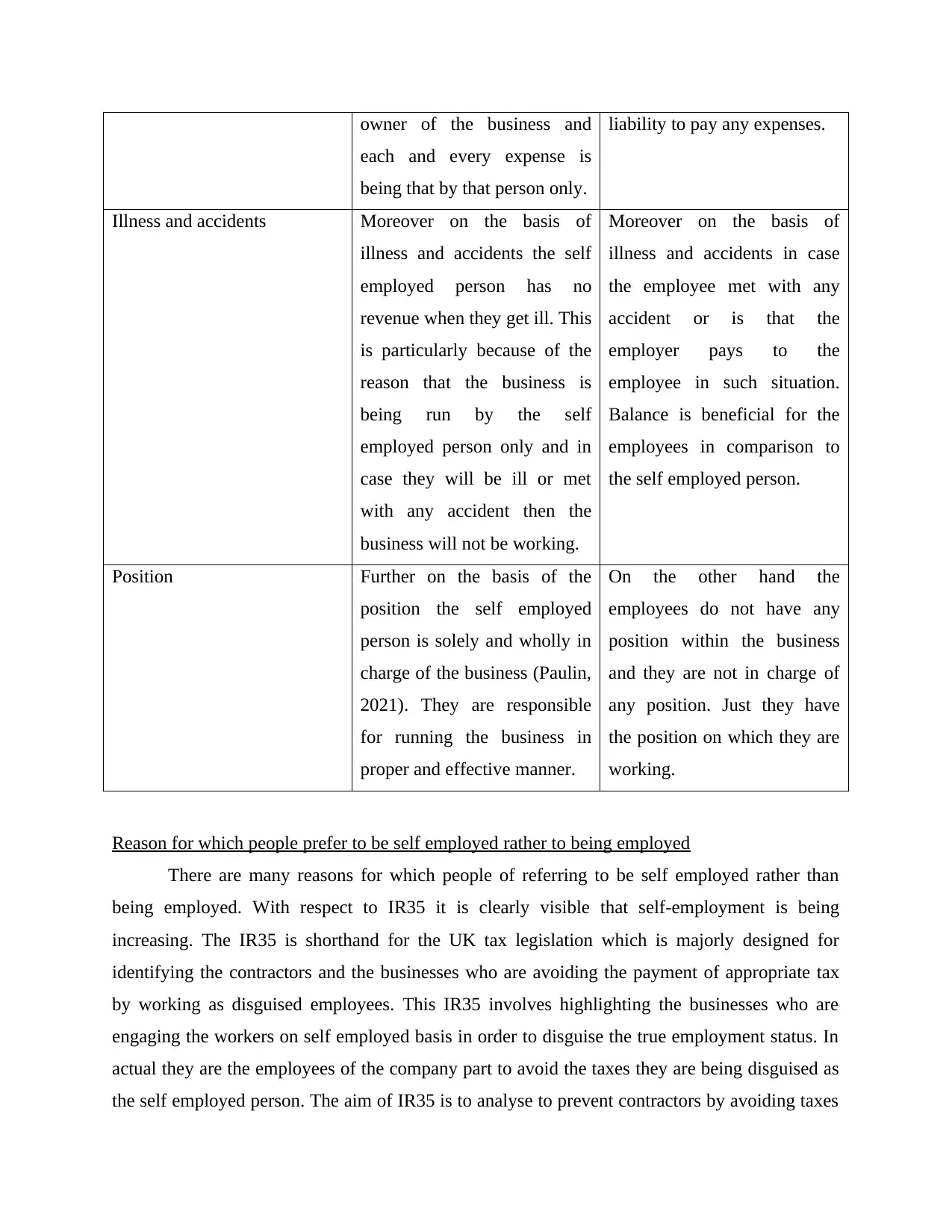

Illness and accidents Moreover on the basis of

illness and accidents the self

employed person has no

revenue when they get ill. This

is particularly because of the

reason that the business is

being run by the self

employed person only and in

case they will be ill or met

with any accident then the

business will not be working.

Moreover on the basis of

illness and accidents in case

the employee met with any

accident or is that the

employer pays to the

employee in such situation.

Balance is beneficial for the

employees in comparison to

the self employed person.

Position Further on the basis of the

position the self employed

person is solely and wholly in

charge of the business (Paulin,

2021). They are responsible

for running the business in

proper and effective manner.

On the other hand the

employees do not have any

position within the business

and they are not in charge of

any position. Just they have

the position on which they are

working.

Reason for which people prefer to be self employed rather to being employed

There are many reasons for which people of referring to be self employed rather than

being employed. With respect to IR35 it is clearly visible that self-employment is being

increasing. The IR35 is shorthand for the UK tax legislation which is majorly designed for

identifying the contractors and the businesses who are avoiding the payment of appropriate tax

by working as disguised employees. This IR35 involves highlighting the businesses who are

engaging the workers on self employed basis in order to disguise the true employment status. In

actual they are the employees of the company part to avoid the taxes they are being disguised as

the self employed person. The aim of IR35 is to analyse to prevent contractors by avoiding taxes

each and every expense is

being that by that person only.

liability to pay any expenses.

Illness and accidents Moreover on the basis of

illness and accidents the self

employed person has no

revenue when they get ill. This

is particularly because of the

reason that the business is

being run by the self

employed person only and in

case they will be ill or met

with any accident then the

business will not be working.

Moreover on the basis of

illness and accidents in case

the employee met with any

accident or is that the

employer pays to the

employee in such situation.

Balance is beneficial for the

employees in comparison to

the self employed person.

Position Further on the basis of the

position the self employed

person is solely and wholly in

charge of the business (Paulin,

2021). They are responsible

for running the business in

proper and effective manner.

On the other hand the

employees do not have any

position within the business

and they are not in charge of

any position. Just they have

the position on which they are

working.

Reason for which people prefer to be self employed rather to being employed

There are many reasons for which people of referring to be self employed rather than

being employed. With respect to IR35 it is clearly visible that self-employment is being

increasing. The IR35 is shorthand for the UK tax legislation which is majorly designed for

identifying the contractors and the businesses who are avoiding the payment of appropriate tax

by working as disguised employees. This IR35 involves highlighting the businesses who are

engaging the workers on self employed basis in order to disguise the true employment status. In

actual they are the employees of the company part to avoid the taxes they are being disguised as

the self employed person. The aim of IR35 is to analyse to prevent contractors by avoiding taxes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and National insurance by treating them as the employees for the reason of tax purpose only.

however they do not have the benefits due to employees under the employment laws like benefits

relating to sickness holiday pay maternity leaves and many other different benefits. In case the

IR35 applies then the intermediary is deemed to be the employee of the company and workers

also treated as the employees of the intermediary (Mehboob, 2020). In the situation the

customers are not affected at all. IR35 applies to the companies where in the workers or the

family control is more than 5% relating to the ordinary shares of the company. In addition to this

the work or his family must be entitled to receive more than 5% of the evidence from the

company. Along with is the work also receives or could receive the payment of benefit by the

company which are not the salary but they can be reasonably taken to represent the payments for

the service provided to the client's.

QUESTION 3

Discussing six badges of trade along with example

Trade is being defined as the venture dealing in buying and selling the goods and services

in terms of some money or other exchange medium. There are different types of the badges of

trade which needs to be followed by the company in managing its business. The HMRC that is

HM Revenue & Customs has enlisted some of the badges which need to be followed by the

business. These different types of the badges involves the following-

The first badge relates with profit seeking motive. This clearly states that the intention of

the business is to earn profits. This is generally because of the reason that the business

exist only with the purpose of earning good amount of profit. In case the company is not

earning any profit then this will effective working efficiency of the business and it will be

affected. Hence it is very necessary for the business to have a profit seeking motive in

order to get successful. For example in case a business is set up and all the transactions

taking place within the business must be on a profit only.

Another badge is the number of transactions which are taking place within the business.

This is also necessary thing to be analysed because in case the number of transactions are

low then it will be affecting the business efficiency to a great extent (Jones, 2021). Thus,

it is very crucial for the business that they have a frequent and large number of business

transactions. For instance in case of pickford V Quirke- CA 1927,13 TC 251 a business

however they do not have the benefits due to employees under the employment laws like benefits

relating to sickness holiday pay maternity leaves and many other different benefits. In case the

IR35 applies then the intermediary is deemed to be the employee of the company and workers

also treated as the employees of the intermediary (Mehboob, 2020). In the situation the

customers are not affected at all. IR35 applies to the companies where in the workers or the

family control is more than 5% relating to the ordinary shares of the company. In addition to this

the work or his family must be entitled to receive more than 5% of the evidence from the

company. Along with is the work also receives or could receive the payment of benefit by the

company which are not the salary but they can be reasonably taken to represent the payments for

the service provided to the client's.

QUESTION 3

Discussing six badges of trade along with example

Trade is being defined as the venture dealing in buying and selling the goods and services

in terms of some money or other exchange medium. There are different types of the badges of

trade which needs to be followed by the company in managing its business. The HMRC that is

HM Revenue & Customs has enlisted some of the badges which need to be followed by the

business. These different types of the badges involves the following-

The first badge relates with profit seeking motive. This clearly states that the intention of

the business is to earn profits. This is generally because of the reason that the business

exist only with the purpose of earning good amount of profit. In case the company is not

earning any profit then this will effective working efficiency of the business and it will be

affected. Hence it is very necessary for the business to have a profit seeking motive in

order to get successful. For example in case a business is set up and all the transactions

taking place within the business must be on a profit only.

Another badge is the number of transactions which are taking place within the business.

This is also necessary thing to be analysed because in case the number of transactions are

low then it will be affecting the business efficiency to a great extent (Jones, 2021). Thus,

it is very crucial for the business that they have a frequent and large number of business

transactions. For instance in case of pickford V Quirke- CA 1927,13 TC 251 a business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

purchase a cotton spinning mill and the intention was using it for trade and increasing the

number of transactions.

Along with this, another bad being used for trade is the nature of asset. This is very

essential to be insured because in case the nature of the answer is of personal use then it

will not be beneficial for the business (Sweeney, 2021). Thus it is very important and

crucial for the business to evaluate the purpose of assets and then buy it. For instance in

case of Marson V Morton Ch D 1986, 59 TC 381 ; [1986] STC 463; [1986] 1 WLR 1343

it was stated that the a land was purchased with the intention of holding it as an

investment hence no income was generated by the land. For the land was sold later

following an unsolicited offer and was treated as investment by the person and not as the

nature of trade.

In addition to the sum another badge involves the existence of similar trading transactions

and interest. This simply means that the business must have all the similar kind of

transactions and not any other kind of transaction been recorded within the books of

accounts. This is particularly because a business deals with a particular type of product

and in case there will be different transactions involving various kind of products then

this will affect business and its working. it is very necessary for the business to use this

batch as having a woman's in it within the transactions of the business. For example in

case of CIR V Fraser [1942] 24TC498 it was evaluated that the taxpayer was a

woodcutter but what a consignment of whisking bond. Subsequently he sold whisky by

an agent and made a profit. But this is not a batch of trading and due to this he was

convicted to crime. The reason underlying this fact is that by business he was a

woodcutter and dealing in whisky was not a similar trading transaction and due to this he

was convicted to crime.

Along with this another keyboard need to be taken care of at time of running the business

is changes to the asset. This is crucial badge to be analysed while doing trading. The

reason behind this fact is that in case the asset is been changed or its use then it will affect

the business to a great extent (Elliot, 2017). For example in case of Cape brandy

Syndicate V CIR- CA 1931, 12 TC 358; [1921] 2 KB 403 it was evaluated that members

of fines indicator have joined within a separate syndicate in order to purchase brandy

from South Africa. These stocks were sent to the east and the remainder was sent to

number of transactions.

Along with this, another bad being used for trade is the nature of asset. This is very

essential to be insured because in case the nature of the answer is of personal use then it

will not be beneficial for the business (Sweeney, 2021). Thus it is very important and

crucial for the business to evaluate the purpose of assets and then buy it. For instance in

case of Marson V Morton Ch D 1986, 59 TC 381 ; [1986] STC 463; [1986] 1 WLR 1343

it was stated that the a land was purchased with the intention of holding it as an

investment hence no income was generated by the land. For the land was sold later

following an unsolicited offer and was treated as investment by the person and not as the

nature of trade.

In addition to the sum another badge involves the existence of similar trading transactions

and interest. This simply means that the business must have all the similar kind of

transactions and not any other kind of transaction been recorded within the books of

accounts. This is particularly because a business deals with a particular type of product

and in case there will be different transactions involving various kind of products then

this will affect business and its working. it is very necessary for the business to use this

batch as having a woman's in it within the transactions of the business. For example in

case of CIR V Fraser [1942] 24TC498 it was evaluated that the taxpayer was a

woodcutter but what a consignment of whisking bond. Subsequently he sold whisky by

an agent and made a profit. But this is not a batch of trading and due to this he was

convicted to crime. The reason underlying this fact is that by business he was a

woodcutter and dealing in whisky was not a similar trading transaction and due to this he

was convicted to crime.

Along with this another keyboard need to be taken care of at time of running the business

is changes to the asset. This is crucial badge to be analysed while doing trading. The

reason behind this fact is that in case the asset is been changed or its use then it will affect

the business to a great extent (Elliot, 2017). For example in case of Cape brandy

Syndicate V CIR- CA 1931, 12 TC 358; [1921] 2 KB 403 it was evaluated that members

of fines indicator have joined within a separate syndicate in order to purchase brandy

from South Africa. These stocks were sent to the east and the remainder was sent to

London and this was to be blended with French brandy and sold at a profit. here in this

present case the taxpayer tried to convince that the transaction was a capital nature but it

was held as a business transaction and was assessable as a trading profit.

Along with this another kind of for trading is the sources of finance. This is very essential

to be followed as increased the finance will not be available in proper and effective

manner than this will effective working in efficiency of the business. Determining the

source of finance is very crucial for the business while doing trade (Ooi, 2021). The

finances used for purchasing the assets and also to undertake the operations of the

business. For example the finances not being available to the business then they will not

be in position to work and operate in proper and effective manner. Hence as a result of

this the business and its profitability will be affected to a great extent.

Discussing the different types of VAT schemes available to the VAT registered business

There are many different types of VAT accounting schemes available for the VAT

registered business. These entire VAT accounting schemes makes the business easier and

simplified and improve the cash flow of the business. The different types of VAT schemes

available to the VAT registered business are as follows-

Flat rate VAT accounting system scheme- this is a scheme where in it simplifies the VAT

returns. In this kind of accounting scheme the company simply calculates the VAT which is due

to HMRC as a percentage of the total turnover. This flat rate VAT accounting scheme is the

scheme instead of paying the difference between the actual VAT that is charged on sales and

VAT paid on the purchases. The person is only eligible for this VAT accounting scheme if the

estimated taxable turnover within the next year will be not more than 150000 pound (VAT

accounting schemes, 2021).

Along with this another VAT scheme for the VAT registered business is limited cost

trade off. Businesses using this VAT flat rate scheme fall within the definition of limited cost

trader. The business is coming under the limited cost trade off must pay the VAT at the enhanced

rate of 16.5%. This rule applies only if the cost of direct goods and services is less than 2% of the

turnover or is less than pound 1000 per year. Also there are many different restrictions over the

goods and services and this includes for calculation of deciding that to whether they are eligible

to stay on the lower rate or not (Scarcella, 2020).

present case the taxpayer tried to convince that the transaction was a capital nature but it

was held as a business transaction and was assessable as a trading profit.

Along with this another kind of for trading is the sources of finance. This is very essential

to be followed as increased the finance will not be available in proper and effective

manner than this will effective working in efficiency of the business. Determining the

source of finance is very crucial for the business while doing trade (Ooi, 2021). The

finances used for purchasing the assets and also to undertake the operations of the

business. For example the finances not being available to the business then they will not

be in position to work and operate in proper and effective manner. Hence as a result of

this the business and its profitability will be affected to a great extent.

Discussing the different types of VAT schemes available to the VAT registered business

There are many different types of VAT accounting schemes available for the VAT

registered business. These entire VAT accounting schemes makes the business easier and

simplified and improve the cash flow of the business. The different types of VAT schemes

available to the VAT registered business are as follows-

Flat rate VAT accounting system scheme- this is a scheme where in it simplifies the VAT

returns. In this kind of accounting scheme the company simply calculates the VAT which is due

to HMRC as a percentage of the total turnover. This flat rate VAT accounting scheme is the

scheme instead of paying the difference between the actual VAT that is charged on sales and

VAT paid on the purchases. The person is only eligible for this VAT accounting scheme if the

estimated taxable turnover within the next year will be not more than 150000 pound (VAT

accounting schemes, 2021).

Along with this another VAT scheme for the VAT registered business is limited cost

trade off. Businesses using this VAT flat rate scheme fall within the definition of limited cost

trader. The business is coming under the limited cost trade off must pay the VAT at the enhanced

rate of 16.5%. This rule applies only if the cost of direct goods and services is less than 2% of the

turnover or is less than pound 1000 per year. Also there are many different restrictions over the

goods and services and this includes for calculation of deciding that to whether they are eligible

to stay on the lower rate or not (Scarcella, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

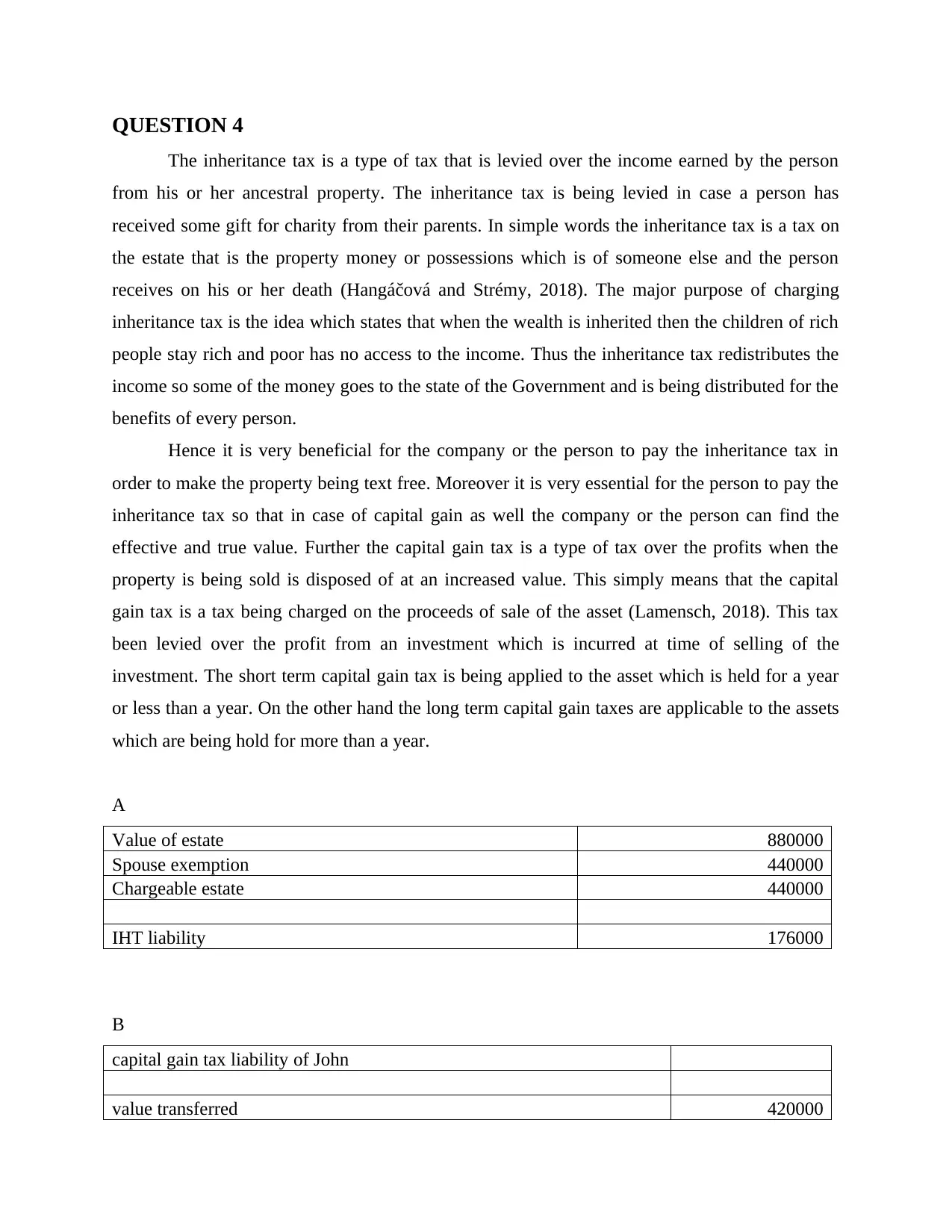

QUESTION 4

The inheritance tax is a type of tax that is levied over the income earned by the person

from his or her ancestral property. The inheritance tax is being levied in case a person has

received some gift for charity from their parents. In simple words the inheritance tax is a tax on

the estate that is the property money or possessions which is of someone else and the person

receives on his or her death (Hangáčová and Strémy, 2018). The major purpose of charging

inheritance tax is the idea which states that when the wealth is inherited then the children of rich

people stay rich and poor has no access to the income. Thus the inheritance tax redistributes the

income so some of the money goes to the state of the Government and is being distributed for the

benefits of every person.

Hence it is very beneficial for the company or the person to pay the inheritance tax in

order to make the property being text free. Moreover it is very essential for the person to pay the

inheritance tax so that in case of capital gain as well the company or the person can find the

effective and true value. Further the capital gain tax is a type of tax over the profits when the

property is being sold is disposed of at an increased value. This simply means that the capital

gain tax is a tax being charged on the proceeds of sale of the asset (Lamensch, 2018). This tax

been levied over the profit from an investment which is incurred at time of selling of the

investment. The short term capital gain tax is being applied to the asset which is held for a year

or less than a year. On the other hand the long term capital gain taxes are applicable to the assets

which are being hold for more than a year.

A

Value of estate 880000

Spouse exemption 440000

Chargeable estate 440000

IHT liability 176000

B

capital gain tax liability of John

value transferred 420000

The inheritance tax is a type of tax that is levied over the income earned by the person

from his or her ancestral property. The inheritance tax is being levied in case a person has

received some gift for charity from their parents. In simple words the inheritance tax is a tax on

the estate that is the property money or possessions which is of someone else and the person

receives on his or her death (Hangáčová and Strémy, 2018). The major purpose of charging

inheritance tax is the idea which states that when the wealth is inherited then the children of rich

people stay rich and poor has no access to the income. Thus the inheritance tax redistributes the

income so some of the money goes to the state of the Government and is being distributed for the

benefits of every person.

Hence it is very beneficial for the company or the person to pay the inheritance tax in

order to make the property being text free. Moreover it is very essential for the person to pay the

inheritance tax so that in case of capital gain as well the company or the person can find the

effective and true value. Further the capital gain tax is a type of tax over the profits when the

property is being sold is disposed of at an increased value. This simply means that the capital

gain tax is a tax being charged on the proceeds of sale of the asset (Lamensch, 2018). This tax

been levied over the profit from an investment which is incurred at time of selling of the

investment. The short term capital gain tax is being applied to the asset which is held for a year

or less than a year. On the other hand the long term capital gain taxes are applicable to the assets

which are being hold for more than a year.

A

Value of estate 880000

Spouse exemption 440000

Chargeable estate 440000

IHT liability 176000

B

capital gain tax liability of John

value transferred 420000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

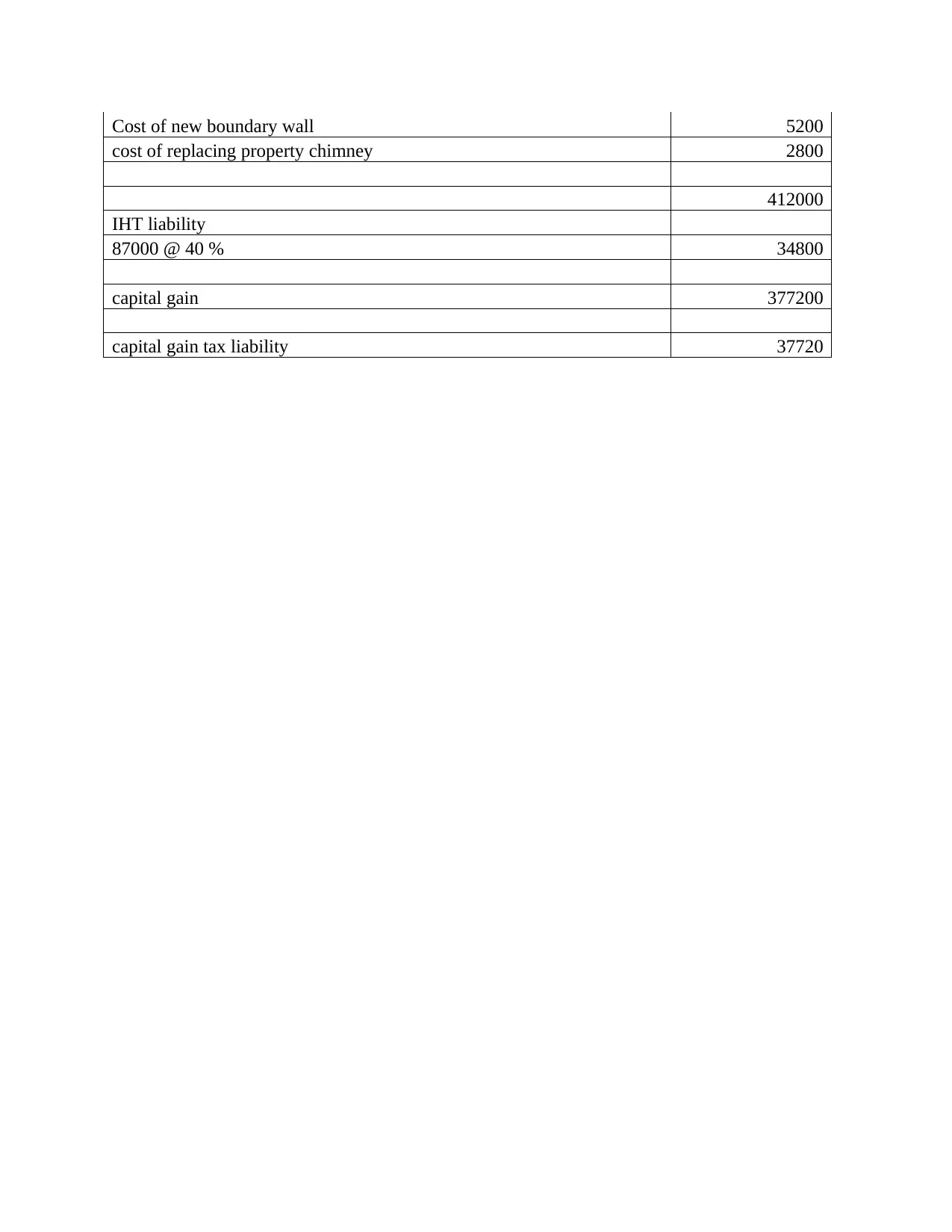

Cost of new boundary wall 5200

cost of replacing property chimney 2800

412000

IHT liability

87000 @ 40 % 34800

capital gain 377200

capital gain tax liability 37720

cost of replacing property chimney 2800

412000

IHT liability

87000 @ 40 % 34800

capital gain 377200

capital gain tax liability 37720

REFERENCES

Books and Journals

Dvouletý, O., 2018. Determinants of self-employment with and without employees: Empirical

findings from Europe. International Review of Entrepreneurship. 16(3).

Elliot, D., 2017. How IR35 legislation reforms will affect you. Practice Management. 27(5).

pp.38-39.

Hangáčová, N. and Strémy, T., 2018. Value added tax and carousel fraud schemes in the

European Union and the Slovak Republic. European Journal of Crime, Criminal Law

and Criminal Justice. 26(2). pp.132-159.

Jones, A., 2021. Improved clarity on IR35 changes proving useful for UK MNEs. International

Tax Review.

Lamensch, M., 2018. Adoption of the e-commerce VAT package: the road ahead is still a rocky

one. EC Tax Review. 27(4).

Mehboob, D., 2020. Taxpayers see long-term challenges under UK’s IR35 regime. International

Tax Review.

Niedzwiedz, C.L., and et.al., 2020. Ethnic and socioeconomic differences in SARS-CoV-2

infection: prospective cohort study using UK Biobank. BMC medicine. 18. pp.1-14.

Ooi, V., 2021. The taxation of cryptocurrency gains. Bulletin for International Taxation. 75(7).

p.1.

Paulin, M., 2021. Legal compliance with the new IR35 payroll rules. Practice

Management. 31(5). pp.34-35.

Scarcella, L., 2020. E-commerce and effective VAT/GST enforcement: Can online platforms

play a valuable role?. Computer law & security review. 36. p.105371.

Sweeney, B., 2021. Changes to IR35 and what this will mean for the vet profession. In

Practice. 43(1). pp.47-49.

Online

Difference between Self Employed and Employee. 2021. [Online]. Available through: <

http://www.differencebetween.net/miscellaneous/career-education/difference-between-

self-employed-and-employee/ >

VAT accounting schemes. 2021. [Online]. Available through: <

https://www.moneydonut.co.uk/tax/vat/vat-accounting-schemes >

Books and Journals

Dvouletý, O., 2018. Determinants of self-employment with and without employees: Empirical

findings from Europe. International Review of Entrepreneurship. 16(3).

Elliot, D., 2017. How IR35 legislation reforms will affect you. Practice Management. 27(5).

pp.38-39.

Hangáčová, N. and Strémy, T., 2018. Value added tax and carousel fraud schemes in the

European Union and the Slovak Republic. European Journal of Crime, Criminal Law

and Criminal Justice. 26(2). pp.132-159.

Jones, A., 2021. Improved clarity on IR35 changes proving useful for UK MNEs. International

Tax Review.

Lamensch, M., 2018. Adoption of the e-commerce VAT package: the road ahead is still a rocky

one. EC Tax Review. 27(4).

Mehboob, D., 2020. Taxpayers see long-term challenges under UK’s IR35 regime. International

Tax Review.

Niedzwiedz, C.L., and et.al., 2020. Ethnic and socioeconomic differences in SARS-CoV-2

infection: prospective cohort study using UK Biobank. BMC medicine. 18. pp.1-14.

Ooi, V., 2021. The taxation of cryptocurrency gains. Bulletin for International Taxation. 75(7).

p.1.

Paulin, M., 2021. Legal compliance with the new IR35 payroll rules. Practice

Management. 31(5). pp.34-35.

Scarcella, L., 2020. E-commerce and effective VAT/GST enforcement: Can online platforms

play a valuable role?. Computer law & security review. 36. p.105371.

Sweeney, B., 2021. Changes to IR35 and what this will mean for the vet profession. In

Practice. 43(1). pp.47-49.

Online

Difference between Self Employed and Employee. 2021. [Online]. Available through: <

http://www.differencebetween.net/miscellaneous/career-education/difference-between-

self-employed-and-employee/ >

VAT accounting schemes. 2021. [Online]. Available through: <

https://www.moneydonut.co.uk/tax/vat/vat-accounting-schemes >

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.