Taxation Law Report: Calculating Net Income and FBT Consequences

VerifiedAdded on 2020/10/22

|8

|2067

|177

Report

AI Summary

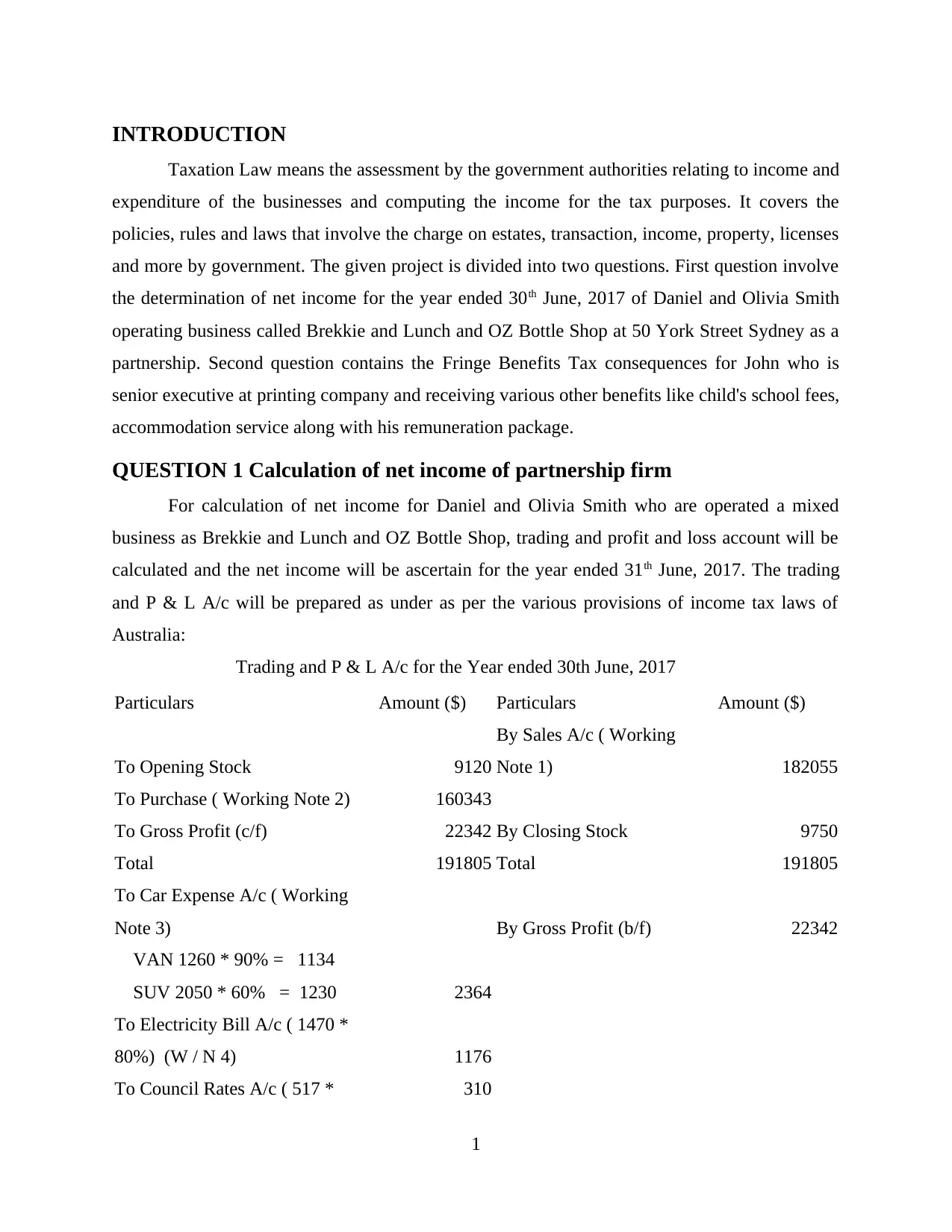

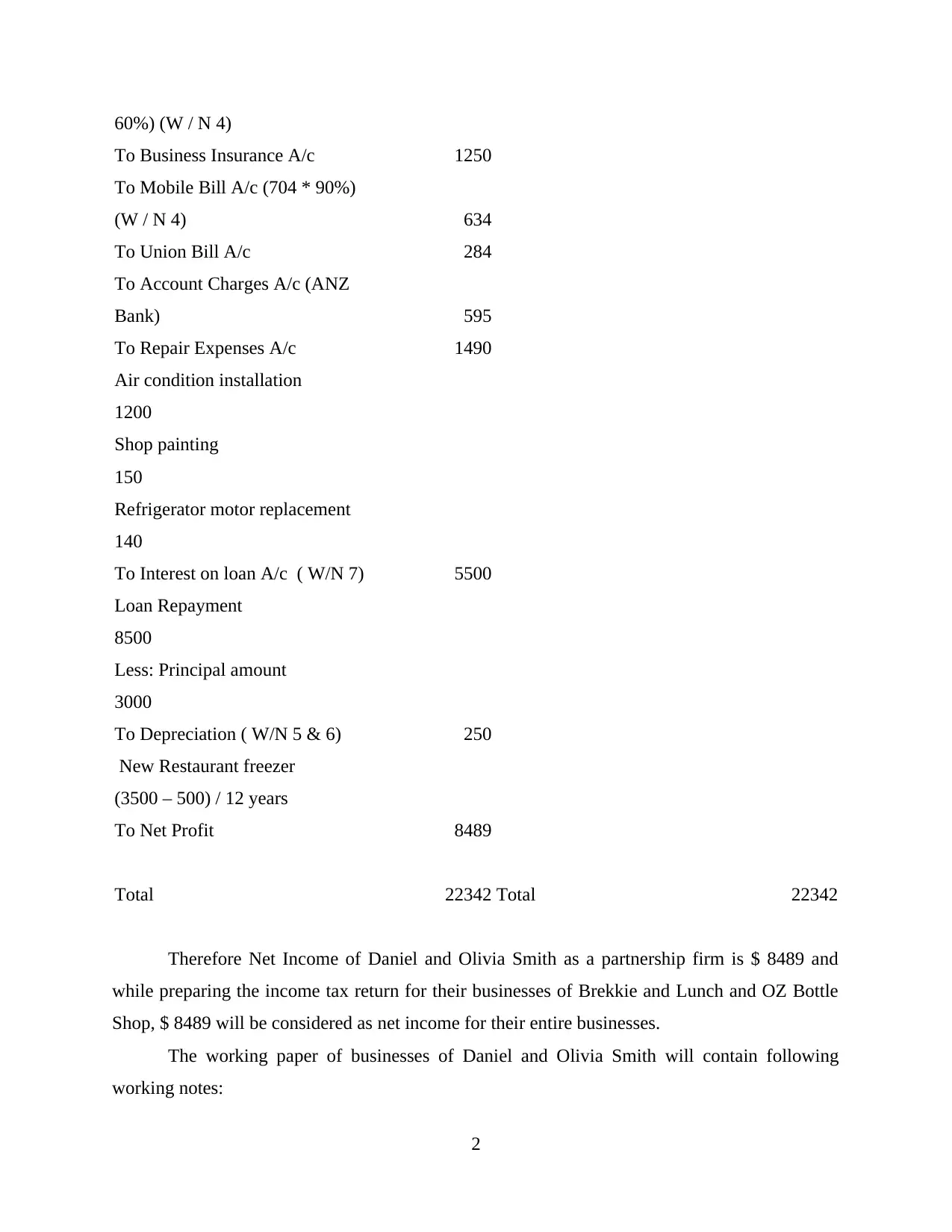

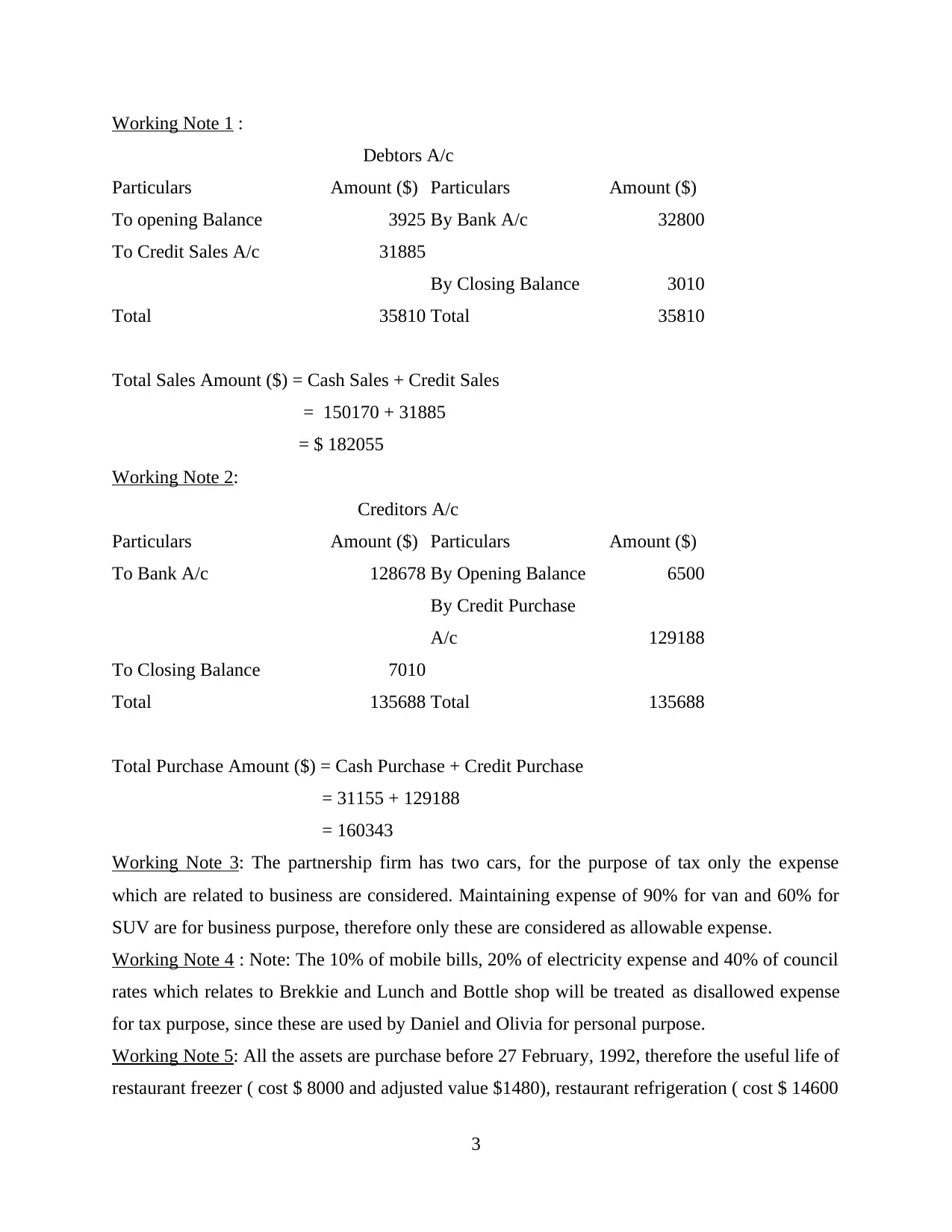

This report delves into Australian taxation law, presenting a detailed analysis of two key areas. Firstly, it calculates the net income of a partnership firm, 'Brekkie and Lunch' and 'OZ Bottle Shop,' owned by Daniel and Olivia Smith, for the year ending June 30th, 2017. The calculation involves a trading and profit and loss account, incorporating various working notes to determine sales, purchases, expenses (including car expenses, electricity, council rates, insurance, and depreciation), and ultimately, the net profit. Secondly, the report examines the fringe benefits tax (FBT) consequences for John, a senior executive receiving a remuneration package that includes child's school fees and accommodation. The analysis calculates the taxable value, grossed-up value, and FBT payable, considering the specific provisions of FBT law. The report concludes by emphasizing the importance of adhering to tax laws and regulations for effective business operations, referencing relevant academic sources.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.