HI6028 Taxation Law: Partnership Tax Return and Income Calculation

VerifiedAdded on 2023/04/23

|9

|1677

|201

Homework Assignment

AI Summary

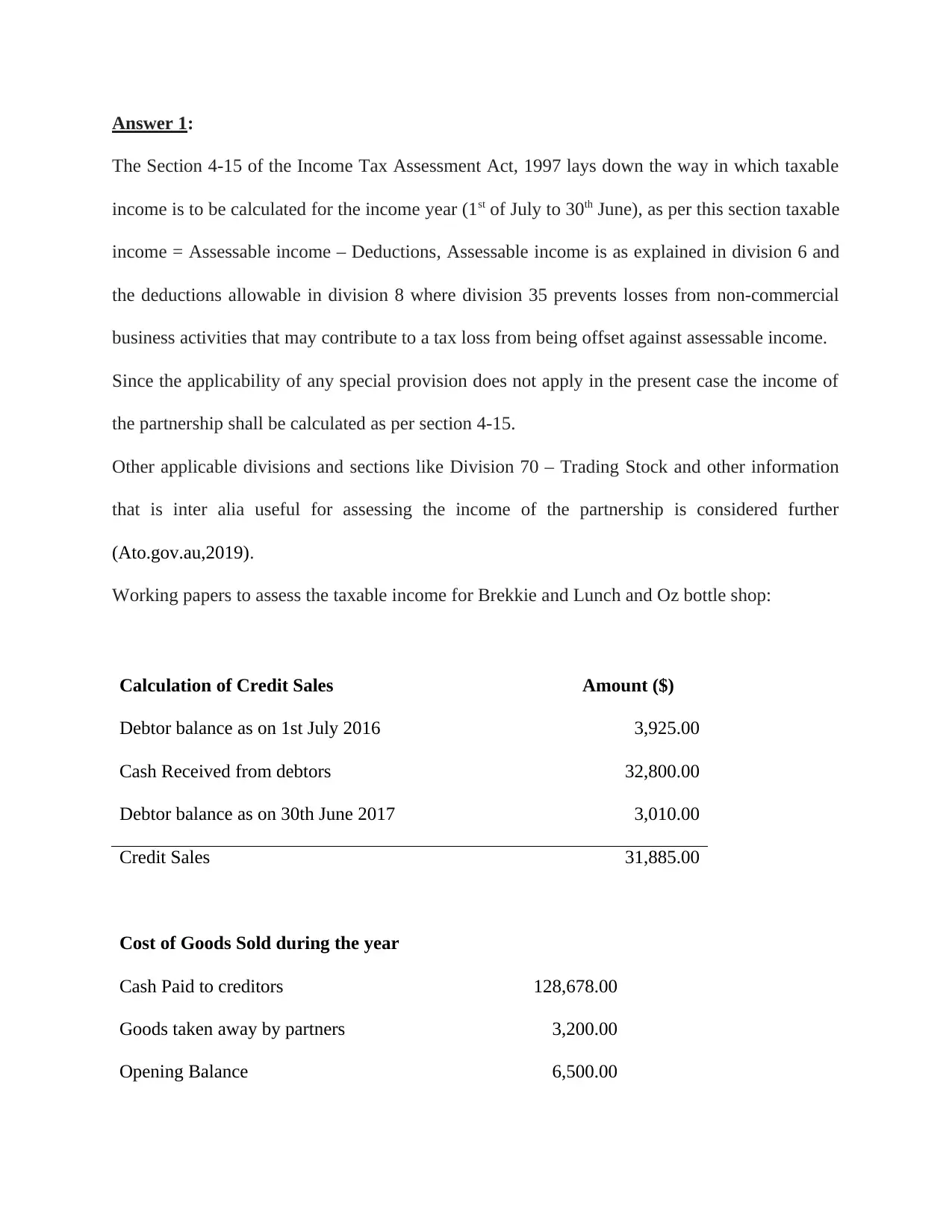

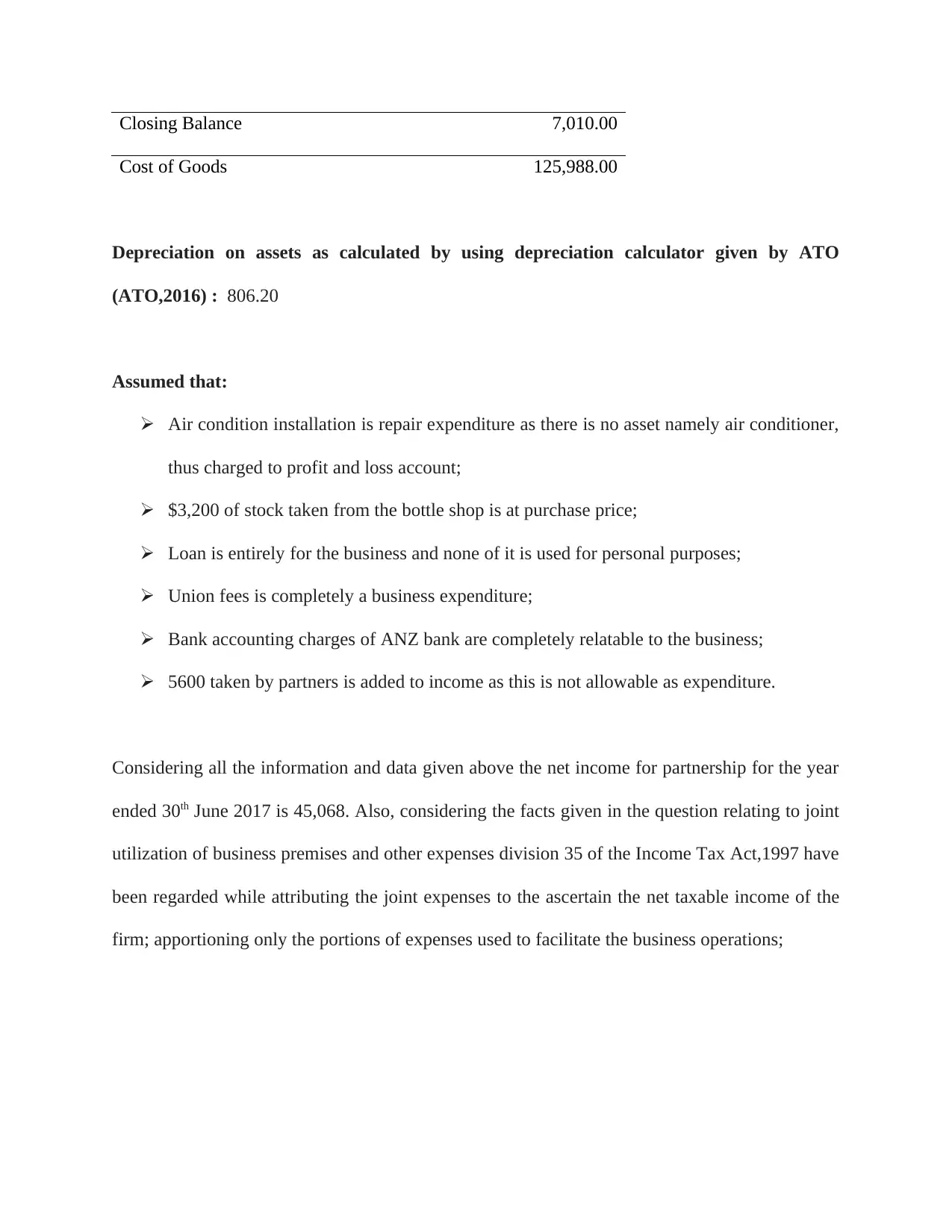

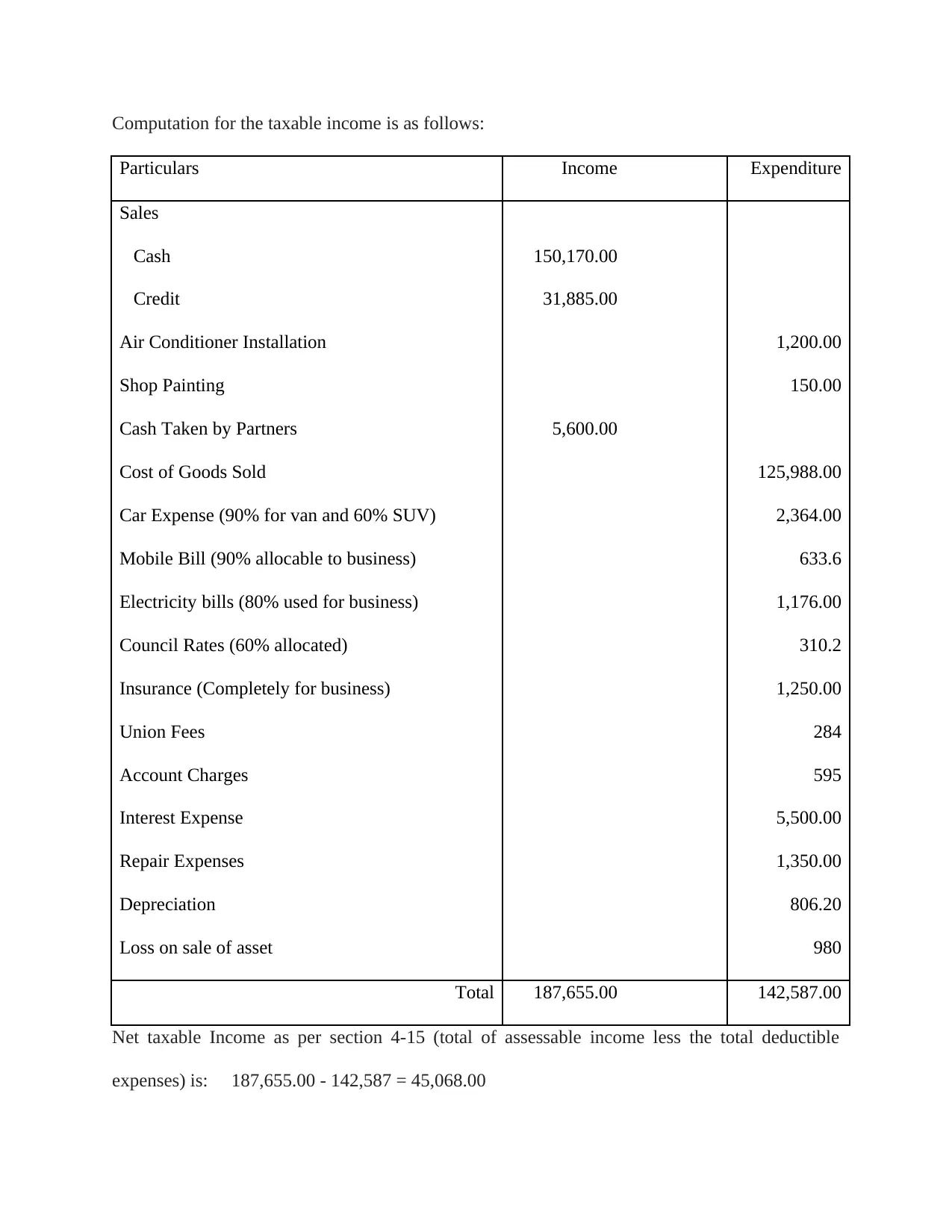

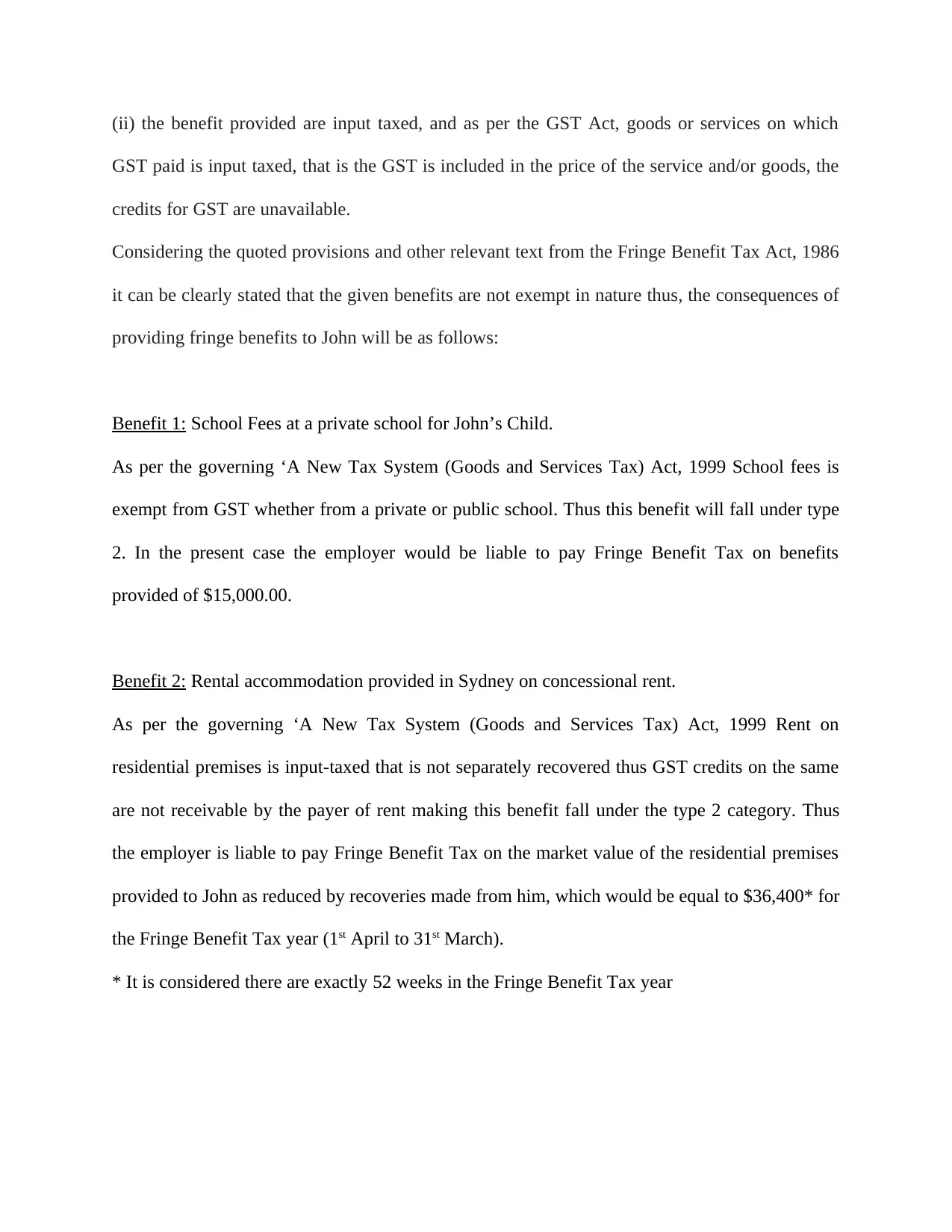

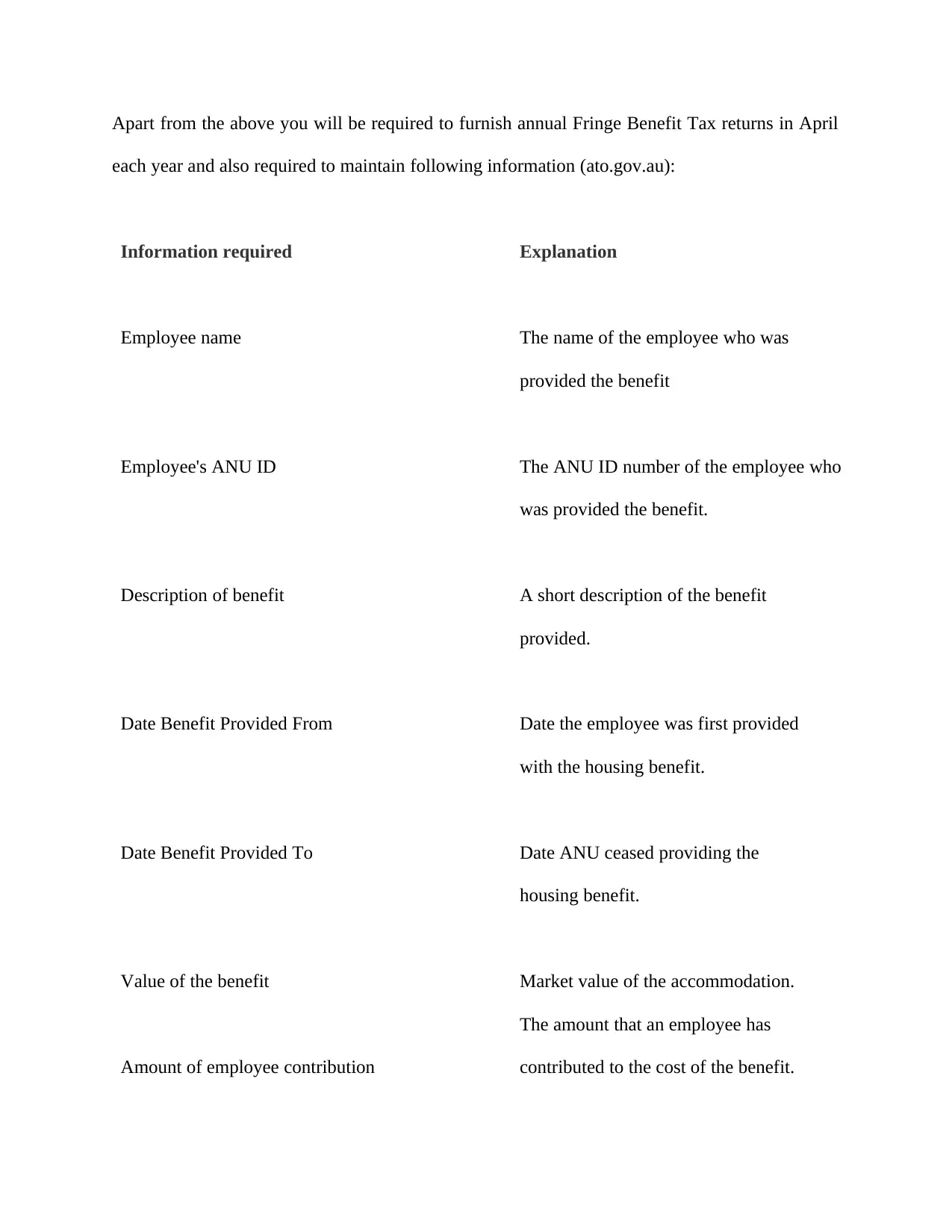

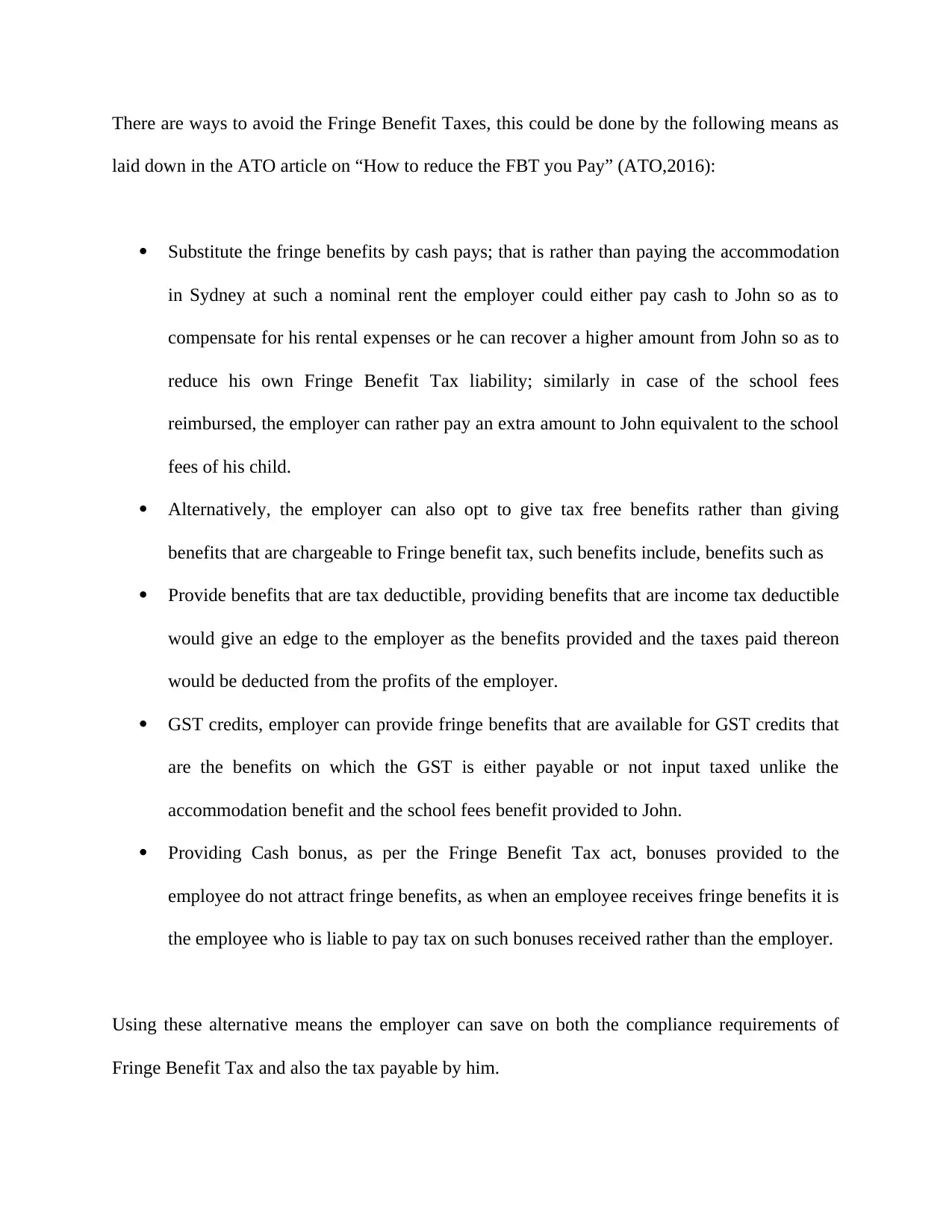

This assignment solution addresses the calculation of taxable income for a partnership, specifically Brekkie and Lunch and Oz Bottle Shop, for the 2017 tax year, in accordance with Section 4-15 of the Income Tax Assessment Act 1997. It details the calculation of credit sales, cost of goods sold, and depreciation, while also considering various business expenses and adjustments. Furthermore, the document discusses the implications of Fringe Benefits Tax (FBT) concerning benefits provided to an employee, John, including school fees and rental accommodation, and explores alternative strategies to minimize FBT liabilities. The solution references relevant sections of the Fringe Benefits Tax Act 1986 and A New Tax System (Goods and Services Tax) Act 1999, providing a comprehensive overview of the tax implications and compliance requirements.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.