Capital Budgeting and Business Valuation: FIN 505 – FALL 2018

VerifiedAdded on 2023/06/03

|8

|1607

|81

AI Summary

This article discusses capital budgeting and business valuation for FIN 505 – FALL 2018. It covers topics such as payback period, net present value, internal rate of return, cost of capital, free cash flow, terminal value, enterprise value, and share price.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

FIN 505 – FALL 2018 – Final Individual Assignment

FIN 505 – FALL 2018 – Final Individual Assignment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

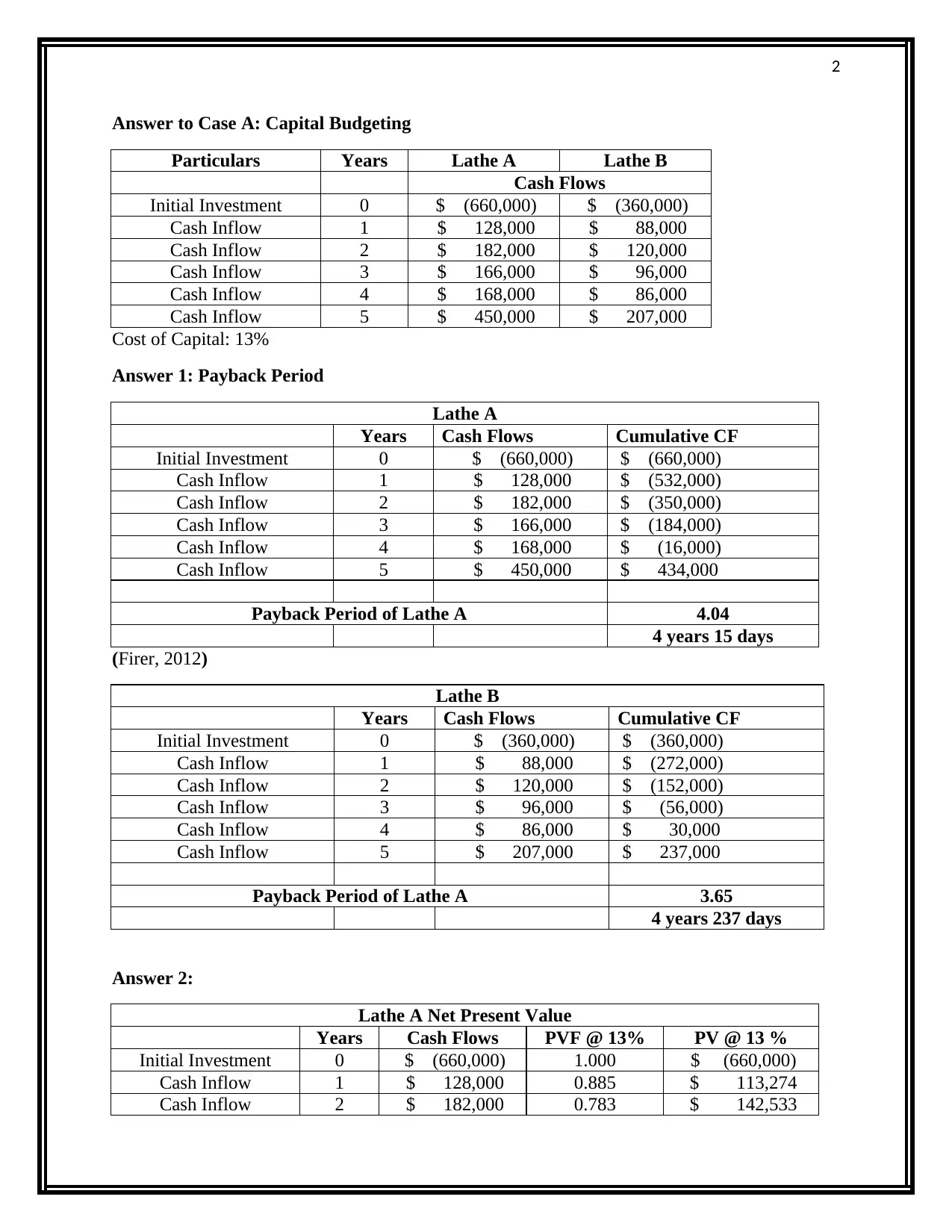

Answer to Case A: Capital Budgeting

Particulars Years Lathe A Lathe B

Cash Flows

Initial Investment 0 $ (660,000) $ (360,000)

Cash Inflow 1 $ 128,000 $ 88,000

Cash Inflow 2 $ 182,000 $ 120,000

Cash Inflow 3 $ 166,000 $ 96,000

Cash Inflow 4 $ 168,000 $ 86,000

Cash Inflow 5 $ 450,000 $ 207,000

Cost of Capital: 13%

Answer 1: Payback Period

Lathe A

Years Cash Flows Cumulative CF

Initial Investment 0 $ (660,000) $ (660,000)

Cash Inflow 1 $ 128,000 $ (532,000)

Cash Inflow 2 $ 182,000 $ (350,000)

Cash Inflow 3 $ 166,000 $ (184,000)

Cash Inflow 4 $ 168,000 $ (16,000)

Cash Inflow 5 $ 450,000 $ 434,000

Payback Period of Lathe A 4.04

4 years 15 days

(Firer, 2012)

Lathe B

Years Cash Flows Cumulative CF

Initial Investment 0 $ (360,000) $ (360,000)

Cash Inflow 1 $ 88,000 $ (272,000)

Cash Inflow 2 $ 120,000 $ (152,000)

Cash Inflow 3 $ 96,000 $ (56,000)

Cash Inflow 4 $ 86,000 $ 30,000

Cash Inflow 5 $ 207,000 $ 237,000

Payback Period of Lathe A 3.65

4 years 237 days

Answer 2:

Lathe A Net Present Value

Years Cash Flows PVF @ 13% PV @ 13 %

Initial Investment 0 $ (660,000) 1.000 $ (660,000)

Cash Inflow 1 $ 128,000 0.885 $ 113,274

Cash Inflow 2 $ 182,000 0.783 $ 142,533

Answer to Case A: Capital Budgeting

Particulars Years Lathe A Lathe B

Cash Flows

Initial Investment 0 $ (660,000) $ (360,000)

Cash Inflow 1 $ 128,000 $ 88,000

Cash Inflow 2 $ 182,000 $ 120,000

Cash Inflow 3 $ 166,000 $ 96,000

Cash Inflow 4 $ 168,000 $ 86,000

Cash Inflow 5 $ 450,000 $ 207,000

Cost of Capital: 13%

Answer 1: Payback Period

Lathe A

Years Cash Flows Cumulative CF

Initial Investment 0 $ (660,000) $ (660,000)

Cash Inflow 1 $ 128,000 $ (532,000)

Cash Inflow 2 $ 182,000 $ (350,000)

Cash Inflow 3 $ 166,000 $ (184,000)

Cash Inflow 4 $ 168,000 $ (16,000)

Cash Inflow 5 $ 450,000 $ 434,000

Payback Period of Lathe A 4.04

4 years 15 days

(Firer, 2012)

Lathe B

Years Cash Flows Cumulative CF

Initial Investment 0 $ (360,000) $ (360,000)

Cash Inflow 1 $ 88,000 $ (272,000)

Cash Inflow 2 $ 120,000 $ (152,000)

Cash Inflow 3 $ 96,000 $ (56,000)

Cash Inflow 4 $ 86,000 $ 30,000

Cash Inflow 5 $ 207,000 $ 237,000

Payback Period of Lathe A 3.65

4 years 237 days

Answer 2:

Lathe A Net Present Value

Years Cash Flows PVF @ 13% PV @ 13 %

Initial Investment 0 $ (660,000) 1.000 $ (660,000)

Cash Inflow 1 $ 128,000 0.885 $ 113,274

Cash Inflow 2 $ 182,000 0.783 $ 142,533

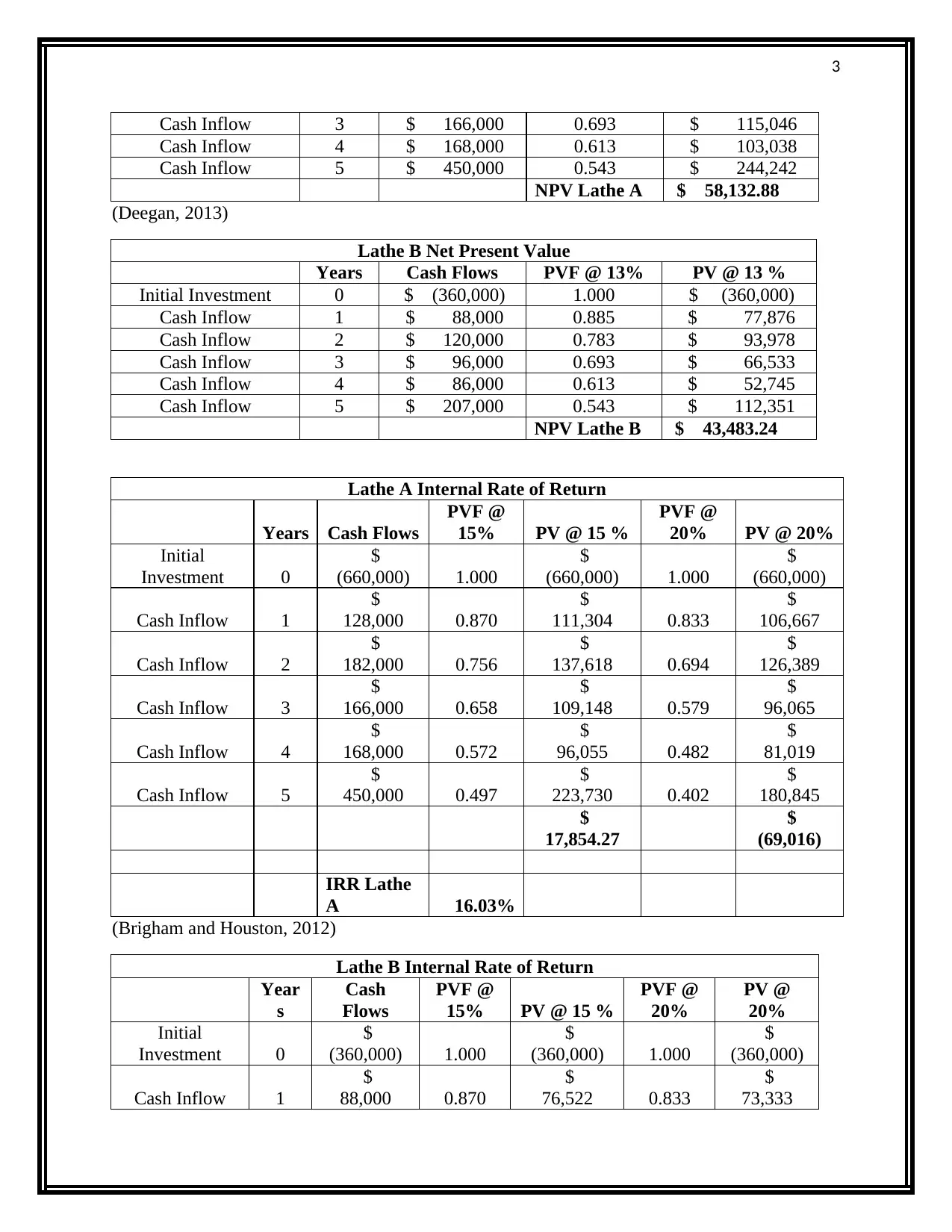

3

Cash Inflow 3 $ 166,000 0.693 $ 115,046

Cash Inflow 4 $ 168,000 0.613 $ 103,038

Cash Inflow 5 $ 450,000 0.543 $ 244,242

NPV Lathe A $ 58,132.88

(Deegan, 2013)

Lathe B Net Present Value

Years Cash Flows PVF @ 13% PV @ 13 %

Initial Investment 0 $ (360,000) 1.000 $ (360,000)

Cash Inflow 1 $ 88,000 0.885 $ 77,876

Cash Inflow 2 $ 120,000 0.783 $ 93,978

Cash Inflow 3 $ 96,000 0.693 $ 66,533

Cash Inflow 4 $ 86,000 0.613 $ 52,745

Cash Inflow 5 $ 207,000 0.543 $ 112,351

NPV Lathe B $ 43,483.24

Lathe A Internal Rate of Return

Years Cash Flows

PVF @

15% PV @ 15 %

PVF @

20% PV @ 20%

Initial

Investment 0

$

(660,000) 1.000

$

(660,000) 1.000

$

(660,000)

Cash Inflow 1

$

128,000 0.870

$

111,304 0.833

$

106,667

Cash Inflow 2

$

182,000 0.756

$

137,618 0.694

$

126,389

Cash Inflow 3

$

166,000 0.658

$

109,148 0.579

$

96,065

Cash Inflow 4

$

168,000 0.572

$

96,055 0.482

$

81,019

Cash Inflow 5

$

450,000 0.497

$

223,730 0.402

$

180,845

$

17,854.27

$

(69,016)

IRR Lathe

A 16.03%

(Brigham and Houston, 2012)

Lathe B Internal Rate of Return

Year

s

Cash

Flows

PVF @

15% PV @ 15 %

PVF @

20%

PV @

20%

Initial

Investment 0

$

(360,000) 1.000

$

(360,000) 1.000

$

(360,000)

Cash Inflow 1

$

88,000 0.870

$

76,522 0.833

$

73,333

Cash Inflow 3 $ 166,000 0.693 $ 115,046

Cash Inflow 4 $ 168,000 0.613 $ 103,038

Cash Inflow 5 $ 450,000 0.543 $ 244,242

NPV Lathe A $ 58,132.88

(Deegan, 2013)

Lathe B Net Present Value

Years Cash Flows PVF @ 13% PV @ 13 %

Initial Investment 0 $ (360,000) 1.000 $ (360,000)

Cash Inflow 1 $ 88,000 0.885 $ 77,876

Cash Inflow 2 $ 120,000 0.783 $ 93,978

Cash Inflow 3 $ 96,000 0.693 $ 66,533

Cash Inflow 4 $ 86,000 0.613 $ 52,745

Cash Inflow 5 $ 207,000 0.543 $ 112,351

NPV Lathe B $ 43,483.24

Lathe A Internal Rate of Return

Years Cash Flows

PVF @

15% PV @ 15 %

PVF @

20% PV @ 20%

Initial

Investment 0

$

(660,000) 1.000

$

(660,000) 1.000

$

(660,000)

Cash Inflow 1

$

128,000 0.870

$

111,304 0.833

$

106,667

Cash Inflow 2

$

182,000 0.756

$

137,618 0.694

$

126,389

Cash Inflow 3

$

166,000 0.658

$

109,148 0.579

$

96,065

Cash Inflow 4

$

168,000 0.572

$

96,055 0.482

$

81,019

Cash Inflow 5

$

450,000 0.497

$

223,730 0.402

$

180,845

$

17,854.27

$

(69,016)

IRR Lathe

A 16.03%

(Brigham and Houston, 2012)

Lathe B Internal Rate of Return

Year

s

Cash

Flows

PVF @

15% PV @ 15 %

PVF @

20%

PV @

20%

Initial

Investment 0

$

(360,000) 1.000

$

(360,000) 1.000

$

(360,000)

Cash Inflow 1

$

88,000 0.870

$

76,522 0.833

$

73,333

4

Cash Inflow 2

$

120,000 0.756

$

90,737 0.694

$

83,333

Cash Inflow 3

$

96,000 0.658

$

63,122 0.579

$

55,556

Cash Inflow 4

$

86,000 0.572

$

49,171 0.482

$

41,474

Cash Inflow 5

$

207,000 0.497

$

102,916 0.402

$

83,189

$

22,466.90

$

(23,115)

IRR Lathe

B 17.46%

Answer 3:

On the basis of theoretical decision it is recommended to the company to invest in such

Lathe that yield higher return and give maximum cash flow to the company. Also various factors

such as nature of investment, size, ease of operation and other relevant factors must be consider

before making taking the theoretical decision. It is recommended to the company to choose

Lathe A as it generates higher rate of return and also give maximum cash flows to the company.

On the basis of practical ground it is also suggested to select Lathe A as it has lower

payback period, higher NPV and IRR greater than cost of capital (Baker and Nofsinger, 2010).

Cash Inflow 2

$

120,000 0.756

$

90,737 0.694

$

83,333

Cash Inflow 3

$

96,000 0.658

$

63,122 0.579

$

55,556

Cash Inflow 4

$

86,000 0.572

$

49,171 0.482

$

41,474

Cash Inflow 5

$

207,000 0.497

$

102,916 0.402

$

83,189

$

22,466.90

$

(23,115)

IRR Lathe

B 17.46%

Answer 3:

On the basis of theoretical decision it is recommended to the company to invest in such

Lathe that yield higher return and give maximum cash flow to the company. Also various factors

such as nature of investment, size, ease of operation and other relevant factors must be consider

before making taking the theoretical decision. It is recommended to the company to choose

Lathe A as it generates higher rate of return and also give maximum cash flows to the company.

On the basis of practical ground it is also suggested to select Lathe A as it has lower

payback period, higher NPV and IRR greater than cost of capital (Baker and Nofsinger, 2010).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

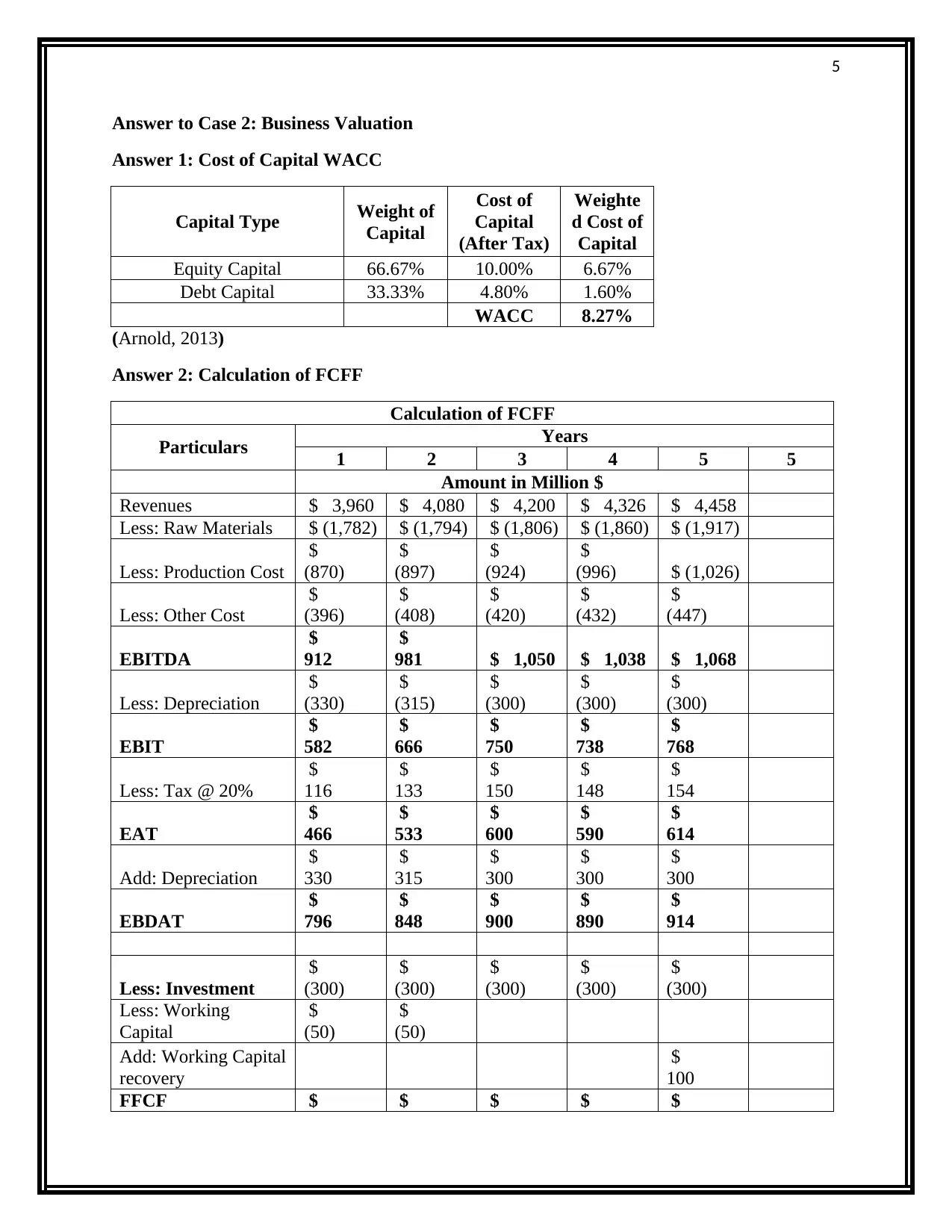

Answer to Case 2: Business Valuation

Answer 1: Cost of Capital WACC

Capital Type Weight of

Capital

Cost of

Capital

(After Tax)

Weighte

d Cost of

Capital

Equity Capital 66.67% 10.00% 6.67%

Debt Capital 33.33% 4.80% 1.60%

WACC 8.27%

(Arnold, 2013)

Answer 2: Calculation of FCFF

Calculation of FCFF

Particulars Years

1 2 3 4 5 5

Amount in Million $

Revenues $ 3,960 $ 4,080 $ 4,200 $ 4,326 $ 4,458

Less: Raw Materials $ (1,782) $ (1,794) $ (1,806) $ (1,860) $ (1,917)

Less: Production Cost

$

(870)

$

(897)

$

(924)

$

(996) $ (1,026)

Less: Other Cost

$

(396)

$

(408)

$

(420)

$

(432)

$

(447)

EBITDA

$

912

$

981 $ 1,050 $ 1,038 $ 1,068

Less: Depreciation

$

(330)

$

(315)

$

(300)

$

(300)

$

(300)

EBIT

$

582

$

666

$

750

$

738

$

768

Less: Tax @ 20%

$

116

$

133

$

150

$

148

$

154

EAT

$

466

$

533

$

600

$

590

$

614

Add: Depreciation

$

330

$

315

$

300

$

300

$

300

EBDAT

$

796

$

848

$

900

$

890

$

914

Less: Investment

$

(300)

$

(300)

$

(300)

$

(300)

$

(300)

Less: Working

Capital

$

(50)

$

(50)

Add: Working Capital

recovery

$

100

FFCF $ $ $ $ $

Answer to Case 2: Business Valuation

Answer 1: Cost of Capital WACC

Capital Type Weight of

Capital

Cost of

Capital

(After Tax)

Weighte

d Cost of

Capital

Equity Capital 66.67% 10.00% 6.67%

Debt Capital 33.33% 4.80% 1.60%

WACC 8.27%

(Arnold, 2013)

Answer 2: Calculation of FCFF

Calculation of FCFF

Particulars Years

1 2 3 4 5 5

Amount in Million $

Revenues $ 3,960 $ 4,080 $ 4,200 $ 4,326 $ 4,458

Less: Raw Materials $ (1,782) $ (1,794) $ (1,806) $ (1,860) $ (1,917)

Less: Production Cost

$

(870)

$

(897)

$

(924)

$

(996) $ (1,026)

Less: Other Cost

$

(396)

$

(408)

$

(420)

$

(432)

$

(447)

EBITDA

$

912

$

981 $ 1,050 $ 1,038 $ 1,068

Less: Depreciation

$

(330)

$

(315)

$

(300)

$

(300)

$

(300)

EBIT

$

582

$

666

$

750

$

738

$

768

Less: Tax @ 20%

$

116

$

133

$

150

$

148

$

154

EAT

$

466

$

533

$

600

$

590

$

614

Add: Depreciation

$

330

$

315

$

300

$

300

$

300

EBDAT

$

796

$

848

$

900

$

890

$

914

Less: Investment

$

(300)

$

(300)

$

(300)

$

(300)

$

(300)

Less: Working

Capital

$

(50)

$

(50)

Add: Working Capital

recovery

$

100

FFCF $ $ $ $ $

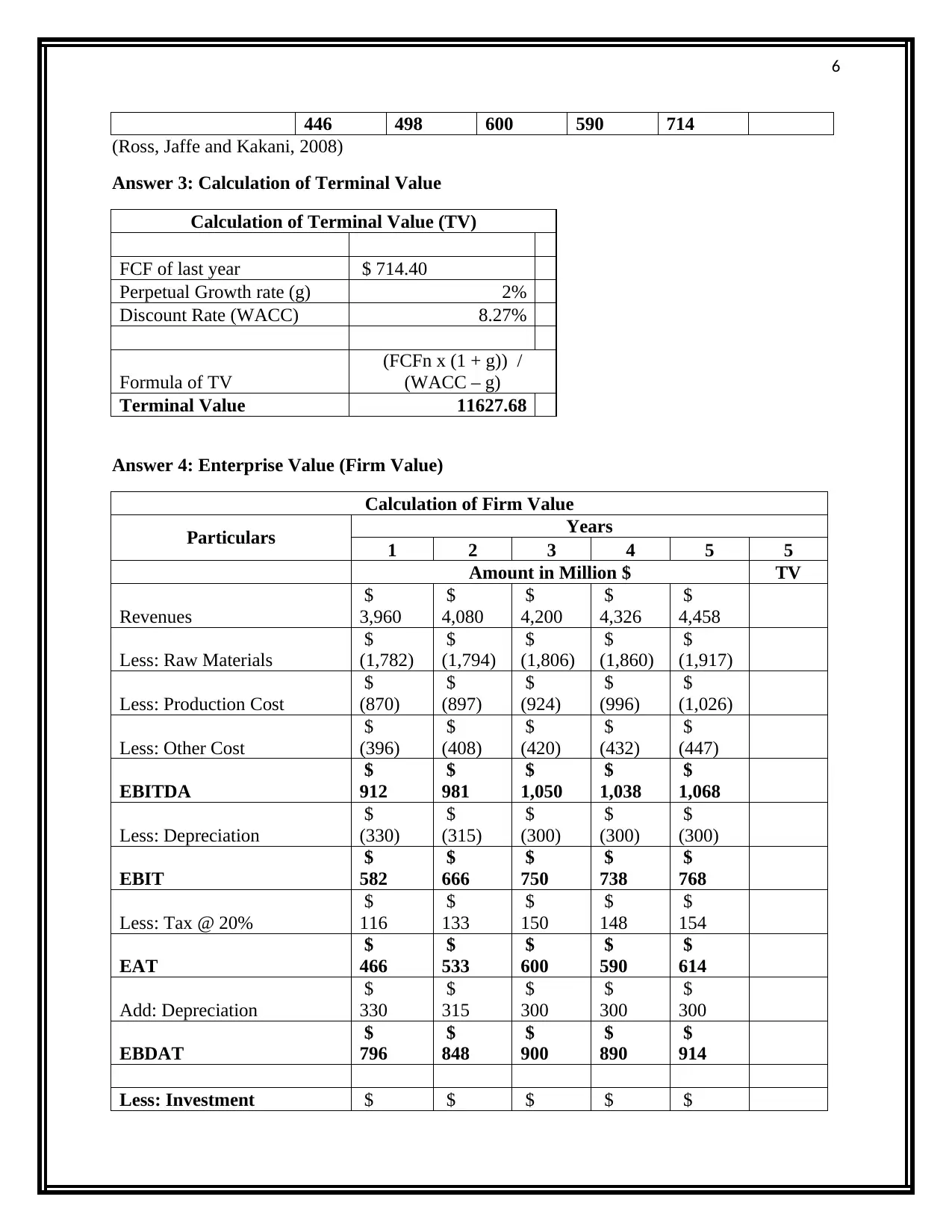

6

446 498 600 590 714

(Ross, Jaffe and Kakani, 2008)

Answer 3: Calculation of Terminal Value

Calculation of Terminal Value (TV)

FCF of last year $ 714.40

Perpetual Growth rate (g) 2%

Discount Rate (WACC) 8.27%

Formula of TV

(FCFn x (1 + g)) /

(WACC – g)

Terminal Value 11627.68

Answer 4: Enterprise Value (Firm Value)

Calculation of Firm Value

Particulars Years

1 2 3 4 5 5

Amount in Million $ TV

Revenues

$

3,960

$

4,080

$

4,200

$

4,326

$

4,458

Less: Raw Materials

$

(1,782)

$

(1,794)

$

(1,806)

$

(1,860)

$

(1,917)

Less: Production Cost

$

(870)

$

(897)

$

(924)

$

(996)

$

(1,026)

Less: Other Cost

$

(396)

$

(408)

$

(420)

$

(432)

$

(447)

EBITDA

$

912

$

981

$

1,050

$

1,038

$

1,068

Less: Depreciation

$

(330)

$

(315)

$

(300)

$

(300)

$

(300)

EBIT

$

582

$

666

$

750

$

738

$

768

Less: Tax @ 20%

$

116

$

133

$

150

$

148

$

154

EAT

$

466

$

533

$

600

$

590

$

614

Add: Depreciation

$

330

$

315

$

300

$

300

$

300

EBDAT

$

796

$

848

$

900

$

890

$

914

Less: Investment $ $ $ $ $

446 498 600 590 714

(Ross, Jaffe and Kakani, 2008)

Answer 3: Calculation of Terminal Value

Calculation of Terminal Value (TV)

FCF of last year $ 714.40

Perpetual Growth rate (g) 2%

Discount Rate (WACC) 8.27%

Formula of TV

(FCFn x (1 + g)) /

(WACC – g)

Terminal Value 11627.68

Answer 4: Enterprise Value (Firm Value)

Calculation of Firm Value

Particulars Years

1 2 3 4 5 5

Amount in Million $ TV

Revenues

$

3,960

$

4,080

$

4,200

$

4,326

$

4,458

Less: Raw Materials

$

(1,782)

$

(1,794)

$

(1,806)

$

(1,860)

$

(1,917)

Less: Production Cost

$

(870)

$

(897)

$

(924)

$

(996)

$

(1,026)

Less: Other Cost

$

(396)

$

(408)

$

(420)

$

(432)

$

(447)

EBITDA

$

912

$

981

$

1,050

$

1,038

$

1,068

Less: Depreciation

$

(330)

$

(315)

$

(300)

$

(300)

$

(300)

EBIT

$

582

$

666

$

750

$

738

$

768

Less: Tax @ 20%

$

116

$

133

$

150

$

148

$

154

EAT

$

466

$

533

$

600

$

590

$

614

Add: Depreciation

$

330

$

315

$

300

$

300

$

300

EBDAT

$

796

$

848

$

900

$

890

$

914

Less: Investment $ $ $ $ $

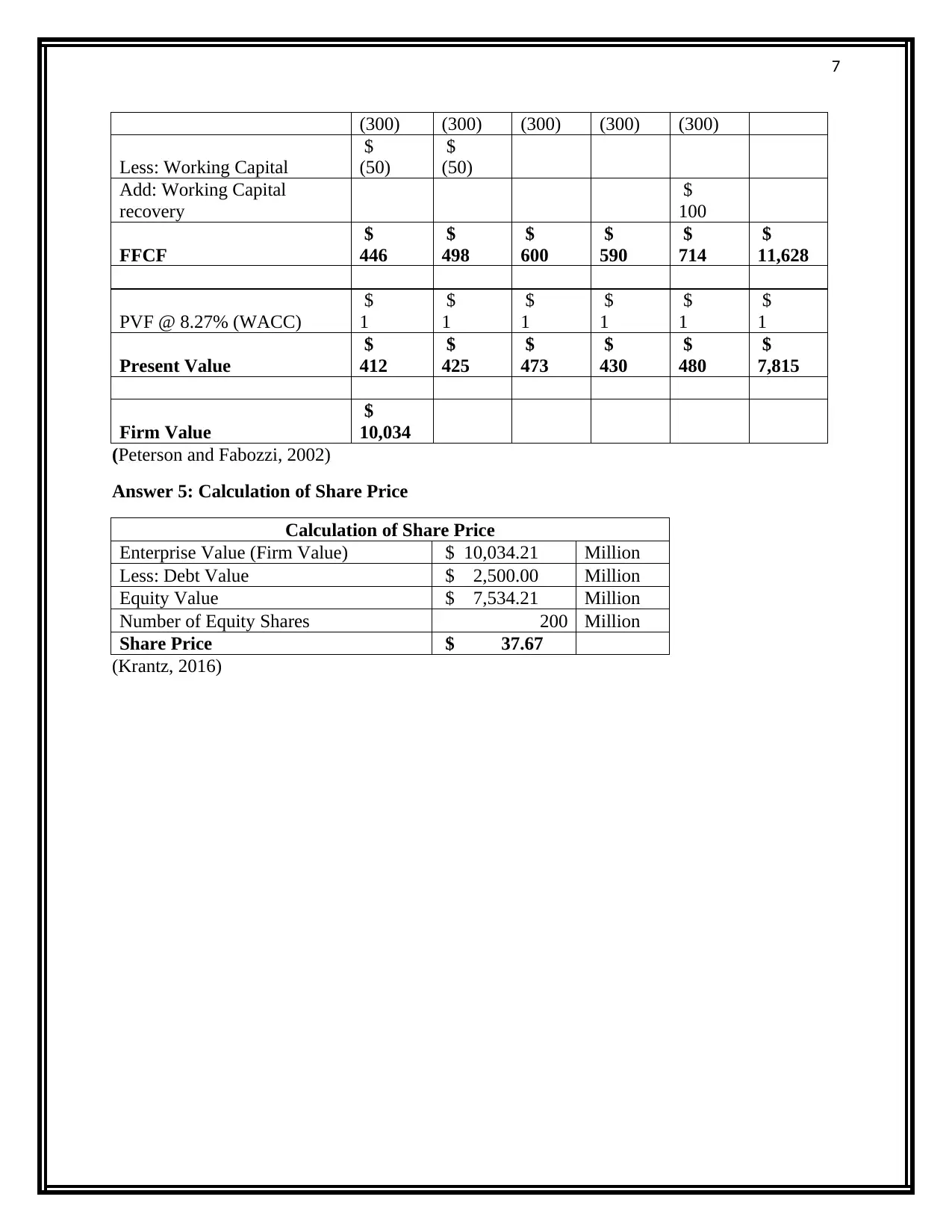

7

(300) (300) (300) (300) (300)

Less: Working Capital

$

(50)

$

(50)

Add: Working Capital

recovery

$

100

FFCF

$

446

$

498

$

600

$

590

$

714

$

11,628

PVF @ 8.27% (WACC)

$

1

$

1

$

1

$

1

$

1

$

1

Present Value

$

412

$

425

$

473

$

430

$

480

$

7,815

Firm Value

$

10,034

(Peterson and Fabozzi, 2002)

Answer 5: Calculation of Share Price

Calculation of Share Price

Enterprise Value (Firm Value) $ 10,034.21 Million

Less: Debt Value $ 2,500.00 Million

Equity Value $ 7,534.21 Million

Number of Equity Shares 200 Million

Share Price $ 37.67

(Krantz, 2016)

(300) (300) (300) (300) (300)

Less: Working Capital

$

(50)

$

(50)

Add: Working Capital

recovery

$

100

FFCF

$

446

$

498

$

600

$

590

$

714

$

11,628

PVF @ 8.27% (WACC)

$

1

$

1

$

1

$

1

$

1

$

1

Present Value

$

412

$

425

$

473

$

430

$

480

$

7,815

Firm Value

$

10,034

(Peterson and Fabozzi, 2002)

Answer 5: Calculation of Share Price

Calculation of Share Price

Enterprise Value (Firm Value) $ 10,034.21 Million

Less: Debt Value $ 2,500.00 Million

Equity Value $ 7,534.21 Million

Number of Equity Shares 200 Million

Share Price $ 37.67

(Krantz, 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

References

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Baker, H.K. and Nofsinger, J.R. 2010. Behavioral Finance: Investors, Corporations, and

Markets. John Wiley & Sons.

Brigham, F., and Houston, J. 2012. Fundamentals of financial management. Cengage Learning.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Firer, C. 2012. Fundamentals of Corporate Finance. Berkshire.McGraw-Hill.

Krantz, M. 2016. Fundamental Analysis for Dummies. John Wiley & Sons.

Peterson, P,P and Fabozzi,F,J,. 2002. Capital budgeting: theory and practice. John Wiley & sons.

Ross, A., Jaffe, J. and Kakani, R.K. 2008. Corporate Finance. Pearson.

References

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Baker, H.K. and Nofsinger, J.R. 2010. Behavioral Finance: Investors, Corporations, and

Markets. John Wiley & Sons.

Brigham, F., and Houston, J. 2012. Fundamentals of financial management. Cengage Learning.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Firer, C. 2012. Fundamentals of Corporate Finance. Berkshire.McGraw-Hill.

Krantz, M. 2016. Fundamental Analysis for Dummies. John Wiley & Sons.

Peterson, P,P and Fabozzi,F,J,. 2002. Capital budgeting: theory and practice. John Wiley & sons.

Ross, A., Jaffe, J. and Kakani, R.K. 2008. Corporate Finance. Pearson.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.