HI6028 Taxation Theory, Practice & Law T2 2018 Individual Assignment

VerifiedAdded on 2023/06/03

|13

|3249

|490

Homework Assignment

AI Summary

This document presents a comprehensive solution to the HI6028 Taxation Theory, Practice & Law assignment for T2 2018. It addresses two key questions: the calculation of capital gains tax (CGT) and fringe benefits tax (FBT). Question 1 details the provisions of CGT in Australia, including the discount method, indexation method, and other methods for calculating capital gains. It then provides detailed calculations for various assets, including land, an antique bed, an antique painting, and shares, determining both short-term and long-term capital gains, as well as net capital gains. Question 2 focuses on fringe benefits tax (FBT), explaining its provisions and how it applies to cars and loans. It outlines the statutory formula method for calculating car fringe benefits and discusses the concept of loan fringe benefits, including statutory interest rates. The document aims to provide a clear understanding of tax principles and calculations relevant to the assignment.

HI6028 Taxation Theory, Practice &

Law T2 2018 Individual Assignment

Law T2 2018 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Provisions...............................................................................................................................3

Calculations............................................................................................................................5

Question 2..................................................................................................................................5

Provisions...............................................................................................................................5

Fringe benefits tax on car...................................................................................................6

Fringe benefit on other benefits.........................................................................................7

Calculations............................................................................................................................8

Part A: Taxable FBT..........................................................................................................8

Part B: Taxable FBT..........................................................................................................9

References................................................................................................................................11

Question 1..................................................................................................................................3

Provisions...............................................................................................................................3

Calculations............................................................................................................................5

Question 2..................................................................................................................................5

Provisions...............................................................................................................................5

Fringe benefits tax on car...................................................................................................6

Fringe benefit on other benefits.........................................................................................7

Calculations............................................................................................................................8

Part A: Taxable FBT..........................................................................................................8

Part B: Taxable FBT..........................................................................................................9

References................................................................................................................................11

QUESTION 1

Provisions

In Australia 1985, Capital Gain Tax was introduced, and it applies on an asset that has

obtained after unless it is specially exempted.

In accordance with the Australian Tax Office, the difference between amount received and

cost of asset is the capital loss or a capital gain. As per assertions of Barkoczy (2016), the

individual compensates tax on capital gains is the portion of its income tax, and it is not

measured as a separate tax and it is refereed as CGT. If the asset is held not less period of 12

month than 50% of gain is first discounted for individual taxpayers and for superannuation

funds it is discounted by 33.3%.

It is required to determine capital gain or loss for each and every capital gains tax event that

takes place to assets during the year. Moreover, in case an individual has earned both capital

gain, and capital loss than an individual has to determine net capital gain or net capital loss

for the year. Furthermore, individuals, as well as small business apart from companies, could

normally discount capital gain by 50% if the asset is held for more than a year (Capital gains

tax, 2017). In addition to this, there are three methods for computing capital gain. An

individual can choose the method which gives the best result. The same implies that the

method which leads to least capital gain is applied by the assessee.

In case capital asset is sold, for example, shares, asset etc. then there will be capital gain or

loss. The same is the difference between what the cost of acquirement of the asset is and

consideration obtained when it is sold. Further, it is important to account capital gains and

losses in the income return and to reimburse tax on the capital gains. Though it is referred to

as CGT that is capital gains ,and it is the element of income tax and not a separate tax. In case

the individual had acquired capital gain on the selling of asset than the gain will be added in

the assessable income and the same might increase the tax amount to which is to be paid.

Since the tax is not withheld for capital gains, it might require finding out how much tax is to

be paid and setting aside the adequate funds in order to cover the related amount. On the

other hand, if there is a capital loss then, in that case, an individual cannot claim it against the

other income, but it could be utilised to adjust against capital gain.

Methods for calculating capital gain taxation

Provisions

In Australia 1985, Capital Gain Tax was introduced, and it applies on an asset that has

obtained after unless it is specially exempted.

In accordance with the Australian Tax Office, the difference between amount received and

cost of asset is the capital loss or a capital gain. As per assertions of Barkoczy (2016), the

individual compensates tax on capital gains is the portion of its income tax, and it is not

measured as a separate tax and it is refereed as CGT. If the asset is held not less period of 12

month than 50% of gain is first discounted for individual taxpayers and for superannuation

funds it is discounted by 33.3%.

It is required to determine capital gain or loss for each and every capital gains tax event that

takes place to assets during the year. Moreover, in case an individual has earned both capital

gain, and capital loss than an individual has to determine net capital gain or net capital loss

for the year. Furthermore, individuals, as well as small business apart from companies, could

normally discount capital gain by 50% if the asset is held for more than a year (Capital gains

tax, 2017). In addition to this, there are three methods for computing capital gain. An

individual can choose the method which gives the best result. The same implies that the

method which leads to least capital gain is applied by the assessee.

In case capital asset is sold, for example, shares, asset etc. then there will be capital gain or

loss. The same is the difference between what the cost of acquirement of the asset is and

consideration obtained when it is sold. Further, it is important to account capital gains and

losses in the income return and to reimburse tax on the capital gains. Though it is referred to

as CGT that is capital gains ,and it is the element of income tax and not a separate tax. In case

the individual had acquired capital gain on the selling of asset than the gain will be added in

the assessable income and the same might increase the tax amount to which is to be paid.

Since the tax is not withheld for capital gains, it might require finding out how much tax is to

be paid and setting aside the adequate funds in order to cover the related amount. On the

other hand, if there is a capital loss then, in that case, an individual cannot claim it against the

other income, but it could be utilised to adjust against capital gain.

Methods for calculating capital gain taxation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CGT discount method: In order to apply this method it is necessary that asset should have

been held for the period of twelve months or more. At the same time, it is not applicable to

the companies. For foreign individuals the 50% discount is deducted on capital gains which

are made subsequent to 8 may 2012. Moreover, the percentage to which capital gain could be

reduced for life insurance companies and complying super funds is 33.33%. Capital gain is

evaluated after reducing base cost from sale proceeds; further, any existing capital loss is

deducted from same and then reduced by a specified discount percentage.

Indexation method: The specified method is applied only for assets which have been acquired

before 21st September 1999 and held for a period of twelve months or more. In this method,

the value of cost base is increased through application of indexation factor which is based on

consumer price index. Thus, the specified indexation rate is applied in order to attain

deductable base cost from sale proceeds.

Other method: In accordance with the study of Woellner and et al. (2016), the specified

method is applied for assets which have been held for less than twelve months before the

CGT event. In this situation, the basic method of reducing cost base from sale proceeds is

applied in order to ascertain capital gain or capital loss.

Capital losses are in adjusted against of Capital gains, in a tax year however if amount of loss

it higher then the net capital losses are carried forward indefinitely. Nevertheless, capital

losses are not counterbalanced against other taxable income. As per the Australian Taxation

Office (ATO), CGT exempted on so many personal assets, which includes individual’s car,

residence, and mainly those assets that are taken as a personal use like example furniture.

Capital Gain Tax is also not applied on depreciating assets that are used exclusively for the

purpose of taxable, like as fitting in a rental property and business equipment (Jacob and

Jacob, 2013).

Faccio and Xu (2015) asserted that establishing the timing of CGT is also important because

the reason behind this is that it informs the individual that in which year the capital loss or

capital gain is to report and probably have an effect on how an individual computes the tax

liability. If an individual disposes of a CGT asset, then the CGT events generally occur at that

time when the individual entries in the contract for disposal. In the real state situation, for

instance, CGT event usually happens at that time when an individual enter in the contract- i.e.

the contract date, not when an individual settle.

been held for the period of twelve months or more. At the same time, it is not applicable to

the companies. For foreign individuals the 50% discount is deducted on capital gains which

are made subsequent to 8 may 2012. Moreover, the percentage to which capital gain could be

reduced for life insurance companies and complying super funds is 33.33%. Capital gain is

evaluated after reducing base cost from sale proceeds; further, any existing capital loss is

deducted from same and then reduced by a specified discount percentage.

Indexation method: The specified method is applied only for assets which have been acquired

before 21st September 1999 and held for a period of twelve months or more. In this method,

the value of cost base is increased through application of indexation factor which is based on

consumer price index. Thus, the specified indexation rate is applied in order to attain

deductable base cost from sale proceeds.

Other method: In accordance with the study of Woellner and et al. (2016), the specified

method is applied for assets which have been held for less than twelve months before the

CGT event. In this situation, the basic method of reducing cost base from sale proceeds is

applied in order to ascertain capital gain or capital loss.

Capital losses are in adjusted against of Capital gains, in a tax year however if amount of loss

it higher then the net capital losses are carried forward indefinitely. Nevertheless, capital

losses are not counterbalanced against other taxable income. As per the Australian Taxation

Office (ATO), CGT exempted on so many personal assets, which includes individual’s car,

residence, and mainly those assets that are taken as a personal use like example furniture.

Capital Gain Tax is also not applied on depreciating assets that are used exclusively for the

purpose of taxable, like as fitting in a rental property and business equipment (Jacob and

Jacob, 2013).

Faccio and Xu (2015) asserted that establishing the timing of CGT is also important because

the reason behind this is that it informs the individual that in which year the capital loss or

capital gain is to report and probably have an effect on how an individual computes the tax

liability. If an individual disposes of a CGT asset, then the CGT events generally occur at that

time when the individual entries in the contract for disposal. In the real state situation, for

instance, CGT event usually happens at that time when an individual enter in the contract- i.e.

the contract date, not when an individual settle.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

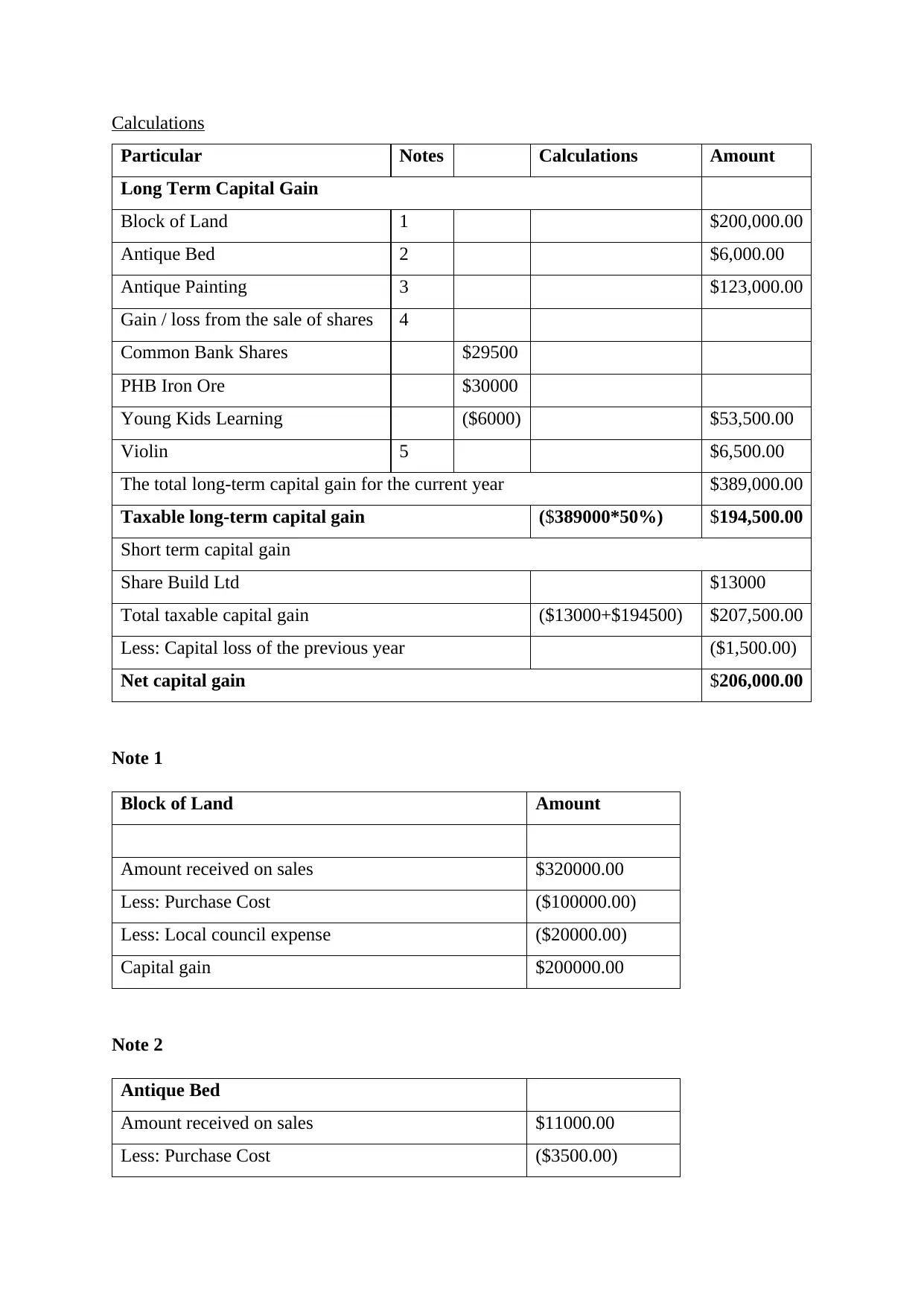

Calculations

Particular Notes Calculations Amount

Long Term Capital Gain

Block of Land 1 $200,000.00

Antique Bed 2 $6,000.00

Antique Painting 3 $123,000.00

Gain / loss from the sale of shares 4

Common Bank Shares $29500

PHB Iron Ore $30000

Young Kids Learning ($6000) $53,500.00

Violin 5 $6,500.00

The total long-term capital gain for the current year $389,000.00

Taxable long-term capital gain ($389000*50%) $194,500.00

Short term capital gain

Share Build Ltd $13000

Total taxable capital gain ($13000+$194500) $207,500.00

Less: Capital loss of the previous year ($1,500.00)

Net capital gain $206,000.00

Note 1

Block of Land Amount

Amount received on sales $320000.00

Less: Purchase Cost ($100000.00)

Less: Local council expense ($20000.00)

Capital gain $200000.00

Note 2

Antique Bed

Amount received on sales $11000.00

Less: Purchase Cost ($3500.00)

Particular Notes Calculations Amount

Long Term Capital Gain

Block of Land 1 $200,000.00

Antique Bed 2 $6,000.00

Antique Painting 3 $123,000.00

Gain / loss from the sale of shares 4

Common Bank Shares $29500

PHB Iron Ore $30000

Young Kids Learning ($6000) $53,500.00

Violin 5 $6,500.00

The total long-term capital gain for the current year $389,000.00

Taxable long-term capital gain ($389000*50%) $194,500.00

Short term capital gain

Share Build Ltd $13000

Total taxable capital gain ($13000+$194500) $207,500.00

Less: Capital loss of the previous year ($1,500.00)

Net capital gain $206,000.00

Note 1

Block of Land Amount

Amount received on sales $320000.00

Less: Purchase Cost ($100000.00)

Less: Local council expense ($20000.00)

Capital gain $200000.00

Note 2

Antique Bed

Amount received on sales $11000.00

Less: Purchase Cost ($3500.00)

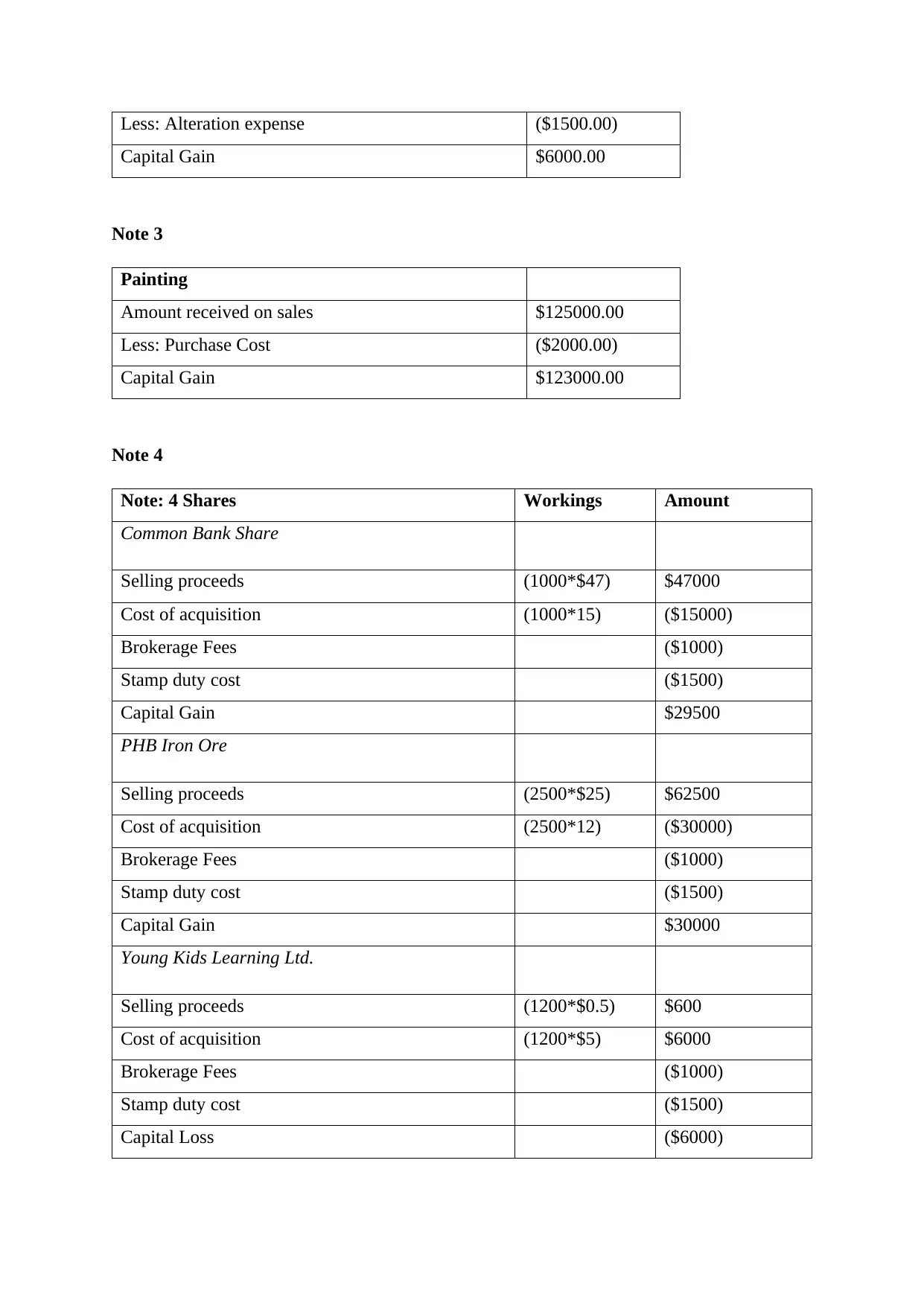

Less: Alteration expense ($1500.00)

Capital Gain $6000.00

Note 3

Painting

Amount received on sales $125000.00

Less: Purchase Cost ($2000.00)

Capital Gain $123000.00

Note 4

Note: 4 Shares Workings Amount

Common Bank Share

Selling proceeds (1000*$47) $47000

Cost of acquisition (1000*15) ($15000)

Brokerage Fees ($1000)

Stamp duty cost ($1500)

Capital Gain $29500

PHB Iron Ore

Selling proceeds (2500*$25) $62500

Cost of acquisition (2500*12) ($30000)

Brokerage Fees ($1000)

Stamp duty cost ($1500)

Capital Gain $30000

Young Kids Learning Ltd.

Selling proceeds (1200*$0.5) $600

Cost of acquisition (1200*$5) $6000

Brokerage Fees ($1000)

Stamp duty cost ($1500)

Capital Loss ($6000)

Capital Gain $6000.00

Note 3

Painting

Amount received on sales $125000.00

Less: Purchase Cost ($2000.00)

Capital Gain $123000.00

Note 4

Note: 4 Shares Workings Amount

Common Bank Share

Selling proceeds (1000*$47) $47000

Cost of acquisition (1000*15) ($15000)

Brokerage Fees ($1000)

Stamp duty cost ($1500)

Capital Gain $29500

PHB Iron Ore

Selling proceeds (2500*$25) $62500

Cost of acquisition (2500*12) ($30000)

Brokerage Fees ($1000)

Stamp duty cost ($1500)

Capital Gain $30000

Young Kids Learning Ltd.

Selling proceeds (1200*$0.5) $600

Cost of acquisition (1200*$5) $6000

Brokerage Fees ($1000)

Stamp duty cost ($1500)

Capital Loss ($6000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

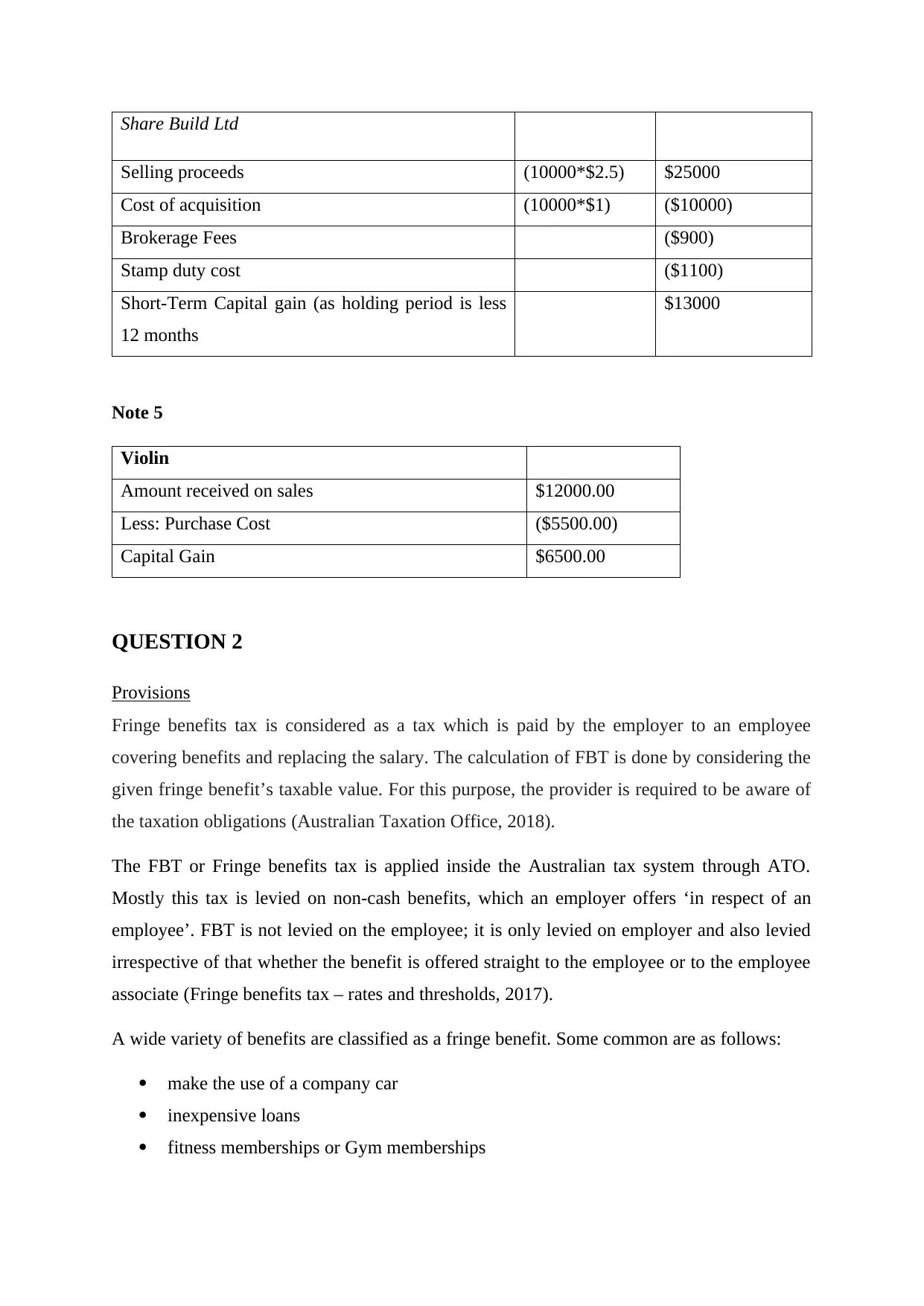

Share Build Ltd

Selling proceeds (10000*$2.5) $25000

Cost of acquisition (10000*$1) ($10000)

Brokerage Fees ($900)

Stamp duty cost ($1100)

Short-Term Capital gain (as holding period is less

12 months

$13000

Note 5

Violin

Amount received on sales $12000.00

Less: Purchase Cost ($5500.00)

Capital Gain $6500.00

QUESTION 2

Provisions

Fringe benefits tax is considered as a tax which is paid by the employer to an employee

covering benefits and replacing the salary. The calculation of FBT is done by considering the

given fringe benefit’s taxable value. For this purpose, the provider is required to be aware of

the taxation obligations (Australian Taxation Office, 2018).

The FBT or Fringe benefits tax is applied inside the Australian tax system through ATO.

Mostly this tax is levied on non-cash benefits, which an employer offers ‘in respect of an

employee’. FBT is not levied on the employee; it is only levied on employer and also levied

irrespective of that whether the benefit is offered straight to the employee or to the employee

associate (Fringe benefits tax – rates and thresholds, 2017).

A wide variety of benefits are classified as a fringe benefit. Some common are as follows:

make the use of a company car

inexpensive loans

fitness memberships or Gym memberships

Selling proceeds (10000*$2.5) $25000

Cost of acquisition (10000*$1) ($10000)

Brokerage Fees ($900)

Stamp duty cost ($1100)

Short-Term Capital gain (as holding period is less

12 months

$13000

Note 5

Violin

Amount received on sales $12000.00

Less: Purchase Cost ($5500.00)

Capital Gain $6500.00

QUESTION 2

Provisions

Fringe benefits tax is considered as a tax which is paid by the employer to an employee

covering benefits and replacing the salary. The calculation of FBT is done by considering the

given fringe benefit’s taxable value. For this purpose, the provider is required to be aware of

the taxation obligations (Australian Taxation Office, 2018).

The FBT or Fringe benefits tax is applied inside the Australian tax system through ATO.

Mostly this tax is levied on non-cash benefits, which an employer offers ‘in respect of an

employee’. FBT is not levied on the employee; it is only levied on employer and also levied

irrespective of that whether the benefit is offered straight to the employee or to the employee

associate (Fringe benefits tax – rates and thresholds, 2017).

A wide variety of benefits are classified as a fringe benefit. Some common are as follows:

make the use of a company car

inexpensive loans

fitness memberships or Gym memberships

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Entertainment expenditures such as drink, housing, foodstuff, low-priced movies

tickets,

personal health insurance

Living-away-from-home allowance (LAFHA)

assets like as construction, land, shares, bonds

school fees and the costs of childcare

The items those are required to do the job like as clothing, mobiles, all such are not included

in fringe benefits although possibly claimable.

Fringe benefits tax on car

Car fringe benefit arises in the case when the employer provides car for private use to an

employee. A car is treated as to be available for private purpose in case it is used by the

employee for a private purpose, or it was available for private use of the employee. The

taxable value of the fringe benefit of the car can be calculated by a statutory formula or

operating cost method. In the first method, the i.e. statutory method a single rate, i.e. 20% is

applied regardless of kilometre travelled (Australian Taxation Office, 2018). The rate is

applied in all situations except to the situation where a pre-existing commitment is available

to provide the car for private use. The taxable value is equal to the amount which has been

ascertained after multiplying car base value to statutory rate. Another method which is

operating cost method ascertains fringe benefit value as a percentage of total cost of operating

car during the specific year. Moreover, the percentage in this situation is evaluated on the

basis of the extent to which car has been used for private purpose. The higher the actual

private uses, the more the taxable value.

Statutory Formula Method:

The taxable value of FBT = (((Base value of car x Statutory % x no. of days in FBT year car

was applied for private use) / Total no. of days in FBT year) – employee contribution)

The statutory method is necessary to be followed in the general situation. In case the

operating cost method is to be applied for calculation of FBT than it is necessary to maintain

adequate FBT records so that information could be rechecked.

A flat statutory rate of 20% applied, in spite of the travelled distance, towards all fringe

benefits car that offers from 1 April 2014 (the same is not applied only in the case where a

pre-determined commitment exist before 7.30pm AEST on 10 May 2011 to provide a car).

tickets,

personal health insurance

Living-away-from-home allowance (LAFHA)

assets like as construction, land, shares, bonds

school fees and the costs of childcare

The items those are required to do the job like as clothing, mobiles, all such are not included

in fringe benefits although possibly claimable.

Fringe benefits tax on car

Car fringe benefit arises in the case when the employer provides car for private use to an

employee. A car is treated as to be available for private purpose in case it is used by the

employee for a private purpose, or it was available for private use of the employee. The

taxable value of the fringe benefit of the car can be calculated by a statutory formula or

operating cost method. In the first method, the i.e. statutory method a single rate, i.e. 20% is

applied regardless of kilometre travelled (Australian Taxation Office, 2018). The rate is

applied in all situations except to the situation where a pre-existing commitment is available

to provide the car for private use. The taxable value is equal to the amount which has been

ascertained after multiplying car base value to statutory rate. Another method which is

operating cost method ascertains fringe benefit value as a percentage of total cost of operating

car during the specific year. Moreover, the percentage in this situation is evaluated on the

basis of the extent to which car has been used for private purpose. The higher the actual

private uses, the more the taxable value.

Statutory Formula Method:

The taxable value of FBT = (((Base value of car x Statutory % x no. of days in FBT year car

was applied for private use) / Total no. of days in FBT year) – employee contribution)

The statutory method is necessary to be followed in the general situation. In case the

operating cost method is to be applied for calculation of FBT than it is necessary to maintain

adequate FBT records so that information could be rechecked.

A flat statutory rate of 20% applied, in spite of the travelled distance, towards all fringe

benefits car that offers from 1 April 2014 (the same is not applied only in the case where a

pre-determined commitment exist before 7.30pm AEST on 10 May 2011 to provide a car).

Fringe benefits tax on the loan

Fringe benefit relating to loan will arise in the case where a loan has been provided to an

associate or employee and interest rate charged is less than the relevant statutory interest rate.

Moreover, the loan should not be exempt (Loan and debt waiver fringe benefits, 2017).

Fringe Benefit relating to loan will be available in each year in which employee is required to

pay either whole or part of the loan. Moreover, the rate of interest is less than the statutory

rate of interest. A loan comprises advance of money, any form of financial accommodation,

payment of a certain amount which eventually leads to the rise of obligation to repay the

amount or any transaction which in substance is a form of a loan.

The statutory interest rate is determined in accordance with standard variable rate relating to

owner-occupied housing loans of significant banks. The same is published by Reserve Bank

of Australia prior to the initiation of the financial year. Moreover, the statutory interest rate

can be referred as a base for evaluation of fringe benefit value relating to the loan provided to

the employee whether at a lower rate or interest-free. Statutory benchmark interest rate for 31

March 2017is 5.65% (Division 7A – benchmark interest rate, 2018). In order to ascertain the

taxable value of fringe benefit relating to loan the interest which is actually accrued is

reduced from the interest which would have been accrued during the specified year relating to

the outstanding balance of the loan of the specified year.

Fringe benefit on other benefits

Fringe benefit taxation provision is applicable in the case specified fringe benefit during a

financial year is more than $2000 (Australian Taxation Office, 2018). Thus, an employee is

required to report the grossed value of the taxable fringe benefit provided to the employee in

the form of summary for the corresponding income year. The fringe benefit which is required

to be reported by the employer is to be presented in grossed up values with application of

lower gross up rate.

The rate at which FBT will be taxable for the year ending 31 March 2015 is 47%. Further

taxation on the same will be paid by the employer. Tax rate of 47% comprises 45% of

marginal income tax rate and 2% of the medical levy. The specified rate is applied to gross up

the value of all the benefits which are received to the employee decreased to the extent of

contribution provided by the employee. Moreover, in case some benefits are exempt from

FBT than same are charged to tax only in case they supersede the specified threshold amount.

Fringe benefit relating to loan will arise in the case where a loan has been provided to an

associate or employee and interest rate charged is less than the relevant statutory interest rate.

Moreover, the loan should not be exempt (Loan and debt waiver fringe benefits, 2017).

Fringe Benefit relating to loan will be available in each year in which employee is required to

pay either whole or part of the loan. Moreover, the rate of interest is less than the statutory

rate of interest. A loan comprises advance of money, any form of financial accommodation,

payment of a certain amount which eventually leads to the rise of obligation to repay the

amount or any transaction which in substance is a form of a loan.

The statutory interest rate is determined in accordance with standard variable rate relating to

owner-occupied housing loans of significant banks. The same is published by Reserve Bank

of Australia prior to the initiation of the financial year. Moreover, the statutory interest rate

can be referred as a base for evaluation of fringe benefit value relating to the loan provided to

the employee whether at a lower rate or interest-free. Statutory benchmark interest rate for 31

March 2017is 5.65% (Division 7A – benchmark interest rate, 2018). In order to ascertain the

taxable value of fringe benefit relating to loan the interest which is actually accrued is

reduced from the interest which would have been accrued during the specified year relating to

the outstanding balance of the loan of the specified year.

Fringe benefit on other benefits

Fringe benefit taxation provision is applicable in the case specified fringe benefit during a

financial year is more than $2000 (Australian Taxation Office, 2018). Thus, an employee is

required to report the grossed value of the taxable fringe benefit provided to the employee in

the form of summary for the corresponding income year. The fringe benefit which is required

to be reported by the employer is to be presented in grossed up values with application of

lower gross up rate.

The rate at which FBT will be taxable for the year ending 31 March 2015 is 47%. Further

taxation on the same will be paid by the employer. Tax rate of 47% comprises 45% of

marginal income tax rate and 2% of the medical levy. The specified rate is applied to gross up

the value of all the benefits which are received to the employee decreased to the extent of

contribution provided by the employee. Moreover, in case some benefits are exempt from

FBT than same are charged to tax only in case they supersede the specified threshold amount.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

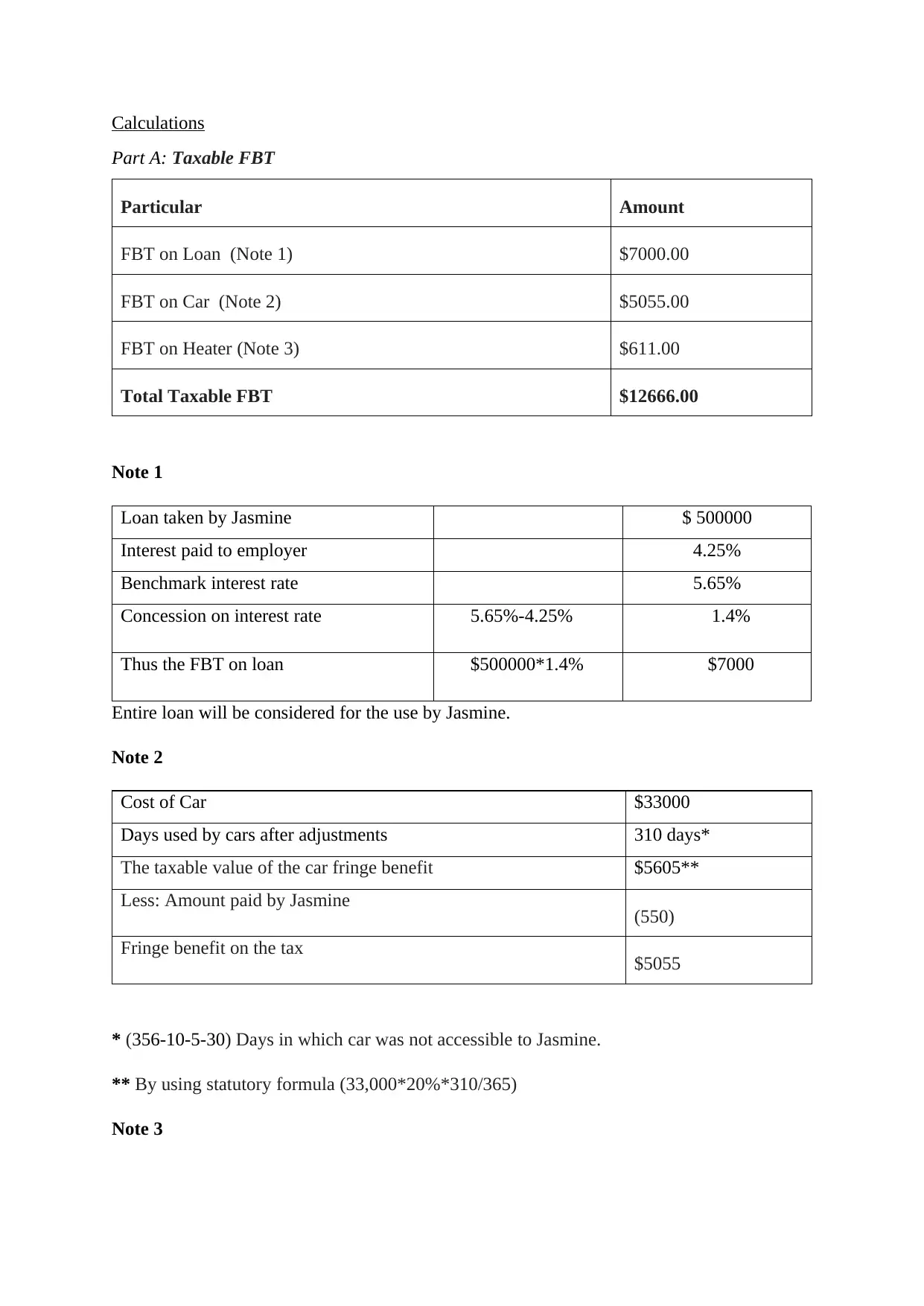

Calculations

Part A: Taxable FBT

Particular Amount

FBT on Loan (Note 1) $7000.00

FBT on Car (Note 2) $5055.00

FBT on Heater (Note 3) $611.00

Total Taxable FBT $12666.00

Note 1

Loan taken by Jasmine $ 500000

Interest paid to employer 4.25%

Benchmark interest rate 5.65%

Concession on interest rate 5.65%-4.25% 1.4%

Thus the FBT on loan $500000*1.4% $7000

Entire loan will be considered for the use by Jasmine.

Note 2

Cost of Car $33000

Days used by cars after adjustments 310 days*

The taxable value of the car fringe benefit $5605**

Less: Amount paid by Jasmine (550)

Fringe benefit on the tax $5055

* (356-10-5-30) Days in which car was not accessible to Jasmine.

** By using statutory formula (33,000*20%*310/365)

Note 3

Part A: Taxable FBT

Particular Amount

FBT on Loan (Note 1) $7000.00

FBT on Car (Note 2) $5055.00

FBT on Heater (Note 3) $611.00

Total Taxable FBT $12666.00

Note 1

Loan taken by Jasmine $ 500000

Interest paid to employer 4.25%

Benchmark interest rate 5.65%

Concession on interest rate 5.65%-4.25% 1.4%

Thus the FBT on loan $500000*1.4% $7000

Entire loan will be considered for the use by Jasmine.

Note 2

Cost of Car $33000

Days used by cars after adjustments 310 days*

The taxable value of the car fringe benefit $5605**

Less: Amount paid by Jasmine (550)

Fringe benefit on the tax $5055

* (356-10-5-30) Days in which car was not accessible to Jasmine.

** By using statutory formula (33,000*20%*310/365)

Note 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of heater $2600

Amount paid of Jasmine ($1300)

Benefit $1300

Taxable rate on FBT 47%

Taxable value on FBT (Benefit* Taxable rate on FBT) $611

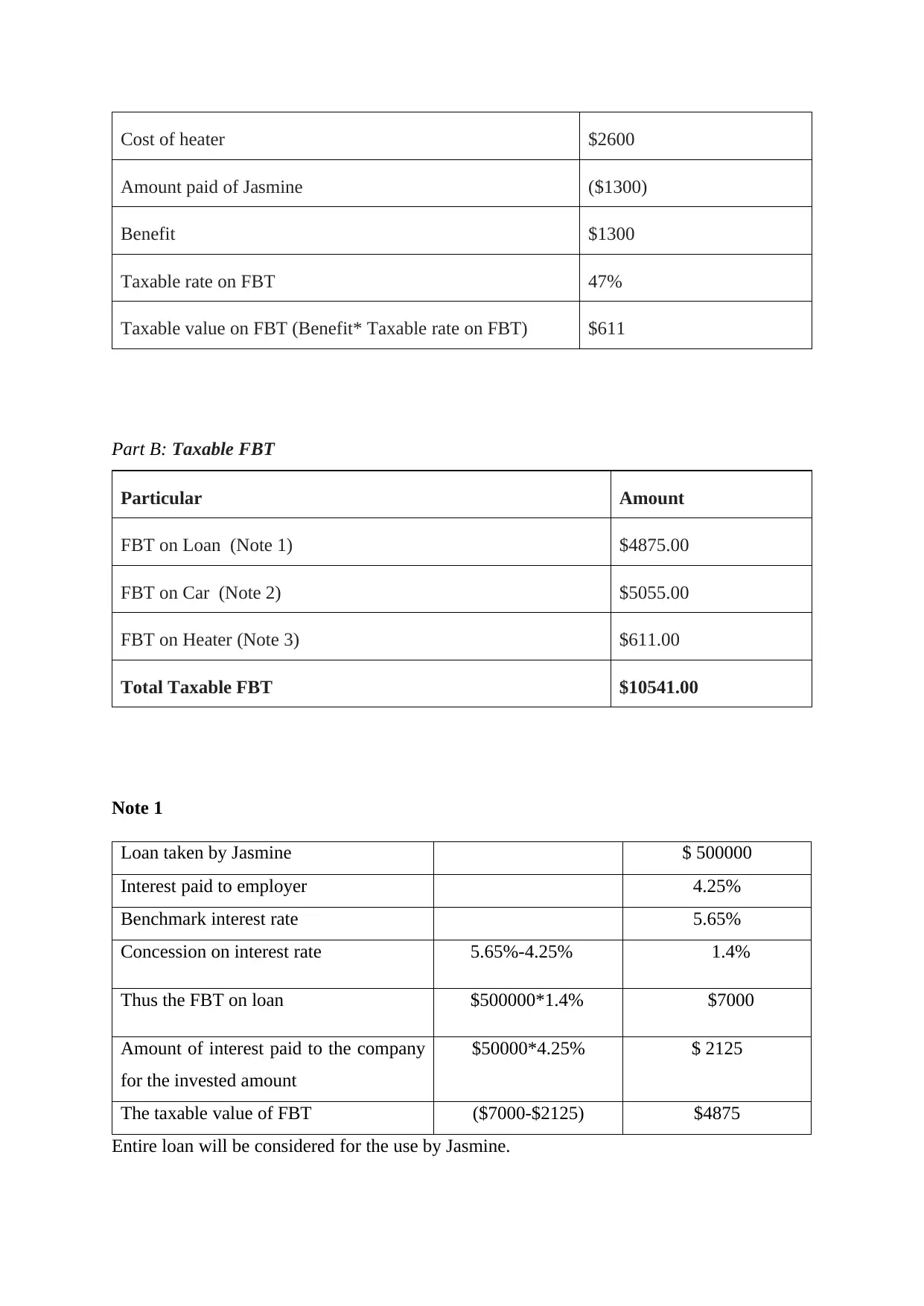

Part B: Taxable FBT

Particular Amount

FBT on Loan (Note 1) $4875.00

FBT on Car (Note 2) $5055.00

FBT on Heater (Note 3) $611.00

Total Taxable FBT $10541.00

Note 1

Loan taken by Jasmine $ 500000

Interest paid to employer 4.25%

Benchmark interest rate 5.65%

Concession on interest rate 5.65%-4.25% 1.4%

Thus the FBT on loan $500000*1.4% $7000

Amount of interest paid to the company

for the invested amount

$50000*4.25% $ 2125

The taxable value of FBT ($7000-$2125) $4875

Entire loan will be considered for the use by Jasmine.

Amount paid of Jasmine ($1300)

Benefit $1300

Taxable rate on FBT 47%

Taxable value on FBT (Benefit* Taxable rate on FBT) $611

Part B: Taxable FBT

Particular Amount

FBT on Loan (Note 1) $4875.00

FBT on Car (Note 2) $5055.00

FBT on Heater (Note 3) $611.00

Total Taxable FBT $10541.00

Note 1

Loan taken by Jasmine $ 500000

Interest paid to employer 4.25%

Benchmark interest rate 5.65%

Concession on interest rate 5.65%-4.25% 1.4%

Thus the FBT on loan $500000*1.4% $7000

Amount of interest paid to the company

for the invested amount

$50000*4.25% $ 2125

The taxable value of FBT ($7000-$2125) $4875

Entire loan will be considered for the use by Jasmine.

Note 2

Cost of Car $33000

Days used by cars after adjustments 310 days*

The taxable value of the car fringe benefit $5605**

Less: Amount paid by Jasmine (550)

Fringe benefit on the tax $5055

* (356-10-5-30) Days in which car was not accessible to Jasmine.

** By using statutory formula (33,000*20%*310/365)

Note 3

Cost of heater $2600

Amount paid of Jasmine ($1300)

Benefit $1300

Taxable rate on FBT 47%

Taxable value on FBT (Benefit* Taxable rate on FBT) $611

Cost of Car $33000

Days used by cars after adjustments 310 days*

The taxable value of the car fringe benefit $5605**

Less: Amount paid by Jasmine (550)

Fringe benefit on the tax $5055

* (356-10-5-30) Days in which car was not accessible to Jasmine.

** By using statutory formula (33,000*20%*310/365)

Note 3

Cost of heater $2600

Amount paid of Jasmine ($1300)

Benefit $1300

Taxable rate on FBT 47%

Taxable value on FBT (Benefit* Taxable rate on FBT) $611

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.