Taxation: Applying Capital Gains Tax Principles to Asset Disposals

VerifiedAdded on 2023/06/07

|13

|3103

|218

Report

AI Summary

This assignment provides a detailed analysis of Capital Gains Tax (CGT) principles and their application to various scenarios. It covers the tax implications of selling a block of land, antique beds, paintings, shares, and a violin, determining whether each is subject to CGT based on acquisition dates and personal use exemptions. Furthermore, the assignment examines Fringe Benefit Taxes (FBT) under the FBTAA 1986, addressing issues related to car benefits, expense reimbursements, and loan fringe benefits, applying relevant sections of the legislation to assess their taxability. The analysis includes references to case law and specific divisions within the FBTAA to support the conclusions.

Running head: TAXATION

Taxation

Name of the Student:

Name of the University

Author’s Note

Taxation

Name of the Student:

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION

Table of Contents

Answer to Question 1......................................................................................................................2

Part A: Block of Land..................................................................................................................2

Part B: Sale of Antique Beds.......................................................................................................3

Part C: Paintings..........................................................................................................................3

Part D: Shares..............................................................................................................................4

Part E: Violin...............................................................................................................................4

Answer to Question 2......................................................................................................................6

Requirement a..............................................................................................................................6

Issues............................................................................................................................................6

Laws.............................................................................................................................................6

Application..................................................................................................................................9

Conclusion.................................................................................................................................10

Answer to Question 2B..................................................................................................................10

Reference.......................................................................................................................................11

TAXATION

Table of Contents

Answer to Question 1......................................................................................................................2

Part A: Block of Land..................................................................................................................2

Part B: Sale of Antique Beds.......................................................................................................3

Part C: Paintings..........................................................................................................................3

Part D: Shares..............................................................................................................................4

Part E: Violin...............................................................................................................................4

Answer to Question 2......................................................................................................................6

Requirement a..............................................................................................................................6

Issues............................................................................................................................................6

Laws.............................................................................................................................................6

Application..................................................................................................................................9

Conclusion.................................................................................................................................10

Answer to Question 2B..................................................................................................................10

Reference.......................................................................................................................................11

2

TAXATION

Answer to Question 1

The main purpose of the assessment is to effectively apply the concepts and principles of

Capital Gain Taxation (CGT) which is generally applied in the event when assets which are

acquired on or before 1985. This breeds the concepts of Pre CGT and Post CGT as per the

principle of applicability. The application of CGT is shown in the case of various items which

are considered for this assessment.

Part A: Block of Land

As per the case which is provided the client has entered into an agreement to sell a plot of

vacant land for a sum pf $ 320,000. Initially the land was acquired in 2001 for a sum of $

100,000 in 2001. As per the tax guidelines, a vacant land is to be considered as a capital asset

under the ownership of the taxpayer. In case the taxpayer decides to sell the vacant land than

CGT provision will be applicable on the taxpayer. However, the applicability provisions which is

on or after 1985 is also to be considered in the case. The tax guidelines further states that the

taxpayer must maintain appropriate records of all the expenses which the tax payer has incurred

on the capital asset so that the computation of net capital gains tax is easily computed (Faccio

and Xu 2015). It is to be noted that the expenses which the taxpayer incurs on the vacant land

cannot be claimed as deduction as per CGT rulings.

In the case, the taxpayer fall under the purview of applicability as the vacant land was

acquired in 2001. The taxpayer has also incurred expenses such as sewerage, water and land tax.

When the taxpayer entered into contract for sale of the land, he attracted the provisions of CGT

event A1 which is covered under “section 104-10 (1)” and therefore, the taxpayer must show the

sum received in their computation of tax liability as per “section 102-5, ITAA 1997”.

TAXATION

Answer to Question 1

The main purpose of the assessment is to effectively apply the concepts and principles of

Capital Gain Taxation (CGT) which is generally applied in the event when assets which are

acquired on or before 1985. This breeds the concepts of Pre CGT and Post CGT as per the

principle of applicability. The application of CGT is shown in the case of various items which

are considered for this assessment.

Part A: Block of Land

As per the case which is provided the client has entered into an agreement to sell a plot of

vacant land for a sum pf $ 320,000. Initially the land was acquired in 2001 for a sum of $

100,000 in 2001. As per the tax guidelines, a vacant land is to be considered as a capital asset

under the ownership of the taxpayer. In case the taxpayer decides to sell the vacant land than

CGT provision will be applicable on the taxpayer. However, the applicability provisions which is

on or after 1985 is also to be considered in the case. The tax guidelines further states that the

taxpayer must maintain appropriate records of all the expenses which the tax payer has incurred

on the capital asset so that the computation of net capital gains tax is easily computed (Faccio

and Xu 2015). It is to be noted that the expenses which the taxpayer incurs on the vacant land

cannot be claimed as deduction as per CGT rulings.

In the case, the taxpayer fall under the purview of applicability as the vacant land was

acquired in 2001. The taxpayer has also incurred expenses such as sewerage, water and land tax.

When the taxpayer entered into contract for sale of the land, he attracted the provisions of CGT

event A1 which is covered under “section 104-10 (1)” and therefore, the taxpayer must show the

sum received in their computation of tax liability as per “section 102-5, ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION

Part B: Sale of Antique Beds

As per the scenario, the taxpayer had a antique bed which was valued recently for the

purpose of insurance and the valuation showed an amount of $ 25,000. The case further reveals

that the antique bed was stolen for which the taxpayer has received an amount of $ 11,000 as the

bed was not specifically covered in insurance deed.

The ruling for such items of collectible are covered under subdivision 108-B and the

section clearly puts out that a collectible is anything which the taxpayer or any associate can use

for the purpose of their pleasure and enjoyment (Dowd, McClelland and Muthitacharoen 2015).

The tax provisions of Section 118-10 (1), ITAA 1997 clearly covers that a collectible which has

of a value equal to or less than $ 500 will be exempted for the purpose of taxation.

In case the asset which is a capital asset in nature is damaged or destroyed then CGT

event C1 is attracted as per the provision of “section 104-25 (1)”. The receipt of the insurance

amount as shown in the case attracts CGT event C1 which needs to be considered by the

taxpayer while computing the taxable income of the taxpayer.

Part C: Paintings

As per the case which is provided in the assessment, the taxpayer acquired a painting

which had initially cost her $ 2000 on 2nd May 1985 and the same was sold for $ 1,25,000 in the

current tax year. The provisions of applicability which are set out in CGT rulings states that the

tax will be applicable on and from 20th September 1985. In such cases the assets are usually

considered to be exempt from taxation as the tax ruling was not in force at that time.

TAXATION

Part B: Sale of Antique Beds

As per the scenario, the taxpayer had a antique bed which was valued recently for the

purpose of insurance and the valuation showed an amount of $ 25,000. The case further reveals

that the antique bed was stolen for which the taxpayer has received an amount of $ 11,000 as the

bed was not specifically covered in insurance deed.

The ruling for such items of collectible are covered under subdivision 108-B and the

section clearly puts out that a collectible is anything which the taxpayer or any associate can use

for the purpose of their pleasure and enjoyment (Dowd, McClelland and Muthitacharoen 2015).

The tax provisions of Section 118-10 (1), ITAA 1997 clearly covers that a collectible which has

of a value equal to or less than $ 500 will be exempted for the purpose of taxation.

In case the asset which is a capital asset in nature is damaged or destroyed then CGT

event C1 is attracted as per the provision of “section 104-25 (1)”. The receipt of the insurance

amount as shown in the case attracts CGT event C1 which needs to be considered by the

taxpayer while computing the taxable income of the taxpayer.

Part C: Paintings

As per the case which is provided in the assessment, the taxpayer acquired a painting

which had initially cost her $ 2000 on 2nd May 1985 and the same was sold for $ 1,25,000 in the

current tax year. The provisions of applicability which are set out in CGT rulings states that the

tax will be applicable on and from 20th September 1985. In such cases the assets are usually

considered to be exempt from taxation as the tax ruling was not in force at that time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION

Thus, from the above discussion, it is clear that the painting will not be taxable and the

same will be considered to be Pre-CGT asset as the taxpayer had purchased the painting on 2nd

May 1985.

Part D: Shares

As per the case, the taxpayer has a significant holding in the shares of companies and the

shares are of different nature and denominations. The shares which are held by individual

taxpayers are considered for the purpose of charging CGT and it is to be clear that shares, public

trusts and managed funds are taken in the same way for computing taxes as in case of any other

capital asset.

The profits which are generated from shares are generally dividend income which is

considered to be part of ordinary income for the purpose of taxation. The situation which is

provided in the question clearly shows that the taxpayer has reported capital gains from the sales

of shares of PHB, Common Ltd and Build Ltd. In addition to this, the taxpayer also shows losses

which the taxpayer has incurred due to the trading in shares during the year. The taxpayer has the

option of setting off the capital losses with the capital gains during the year and any balance is to

be included in the taxable income of the taxpayer.

Part E: Violin

As per the case the taxpayer has a variety of violin collection out of which the taxpayer

sold one during the current year for $ 12,000 which has initially costed the taxpayer an amount

of $ 5,500 on 1999. The section of taxation rulings in Australia covers the personal use of assets

under section 108-C. As per section 108-20 (2), an asset which are of non-collectable nature is

identified if the asset is kept for the pleasure and enjoyment of the taxpayer when the same are

TAXATION

Thus, from the above discussion, it is clear that the painting will not be taxable and the

same will be considered to be Pre-CGT asset as the taxpayer had purchased the painting on 2nd

May 1985.

Part D: Shares

As per the case, the taxpayer has a significant holding in the shares of companies and the

shares are of different nature and denominations. The shares which are held by individual

taxpayers are considered for the purpose of charging CGT and it is to be clear that shares, public

trusts and managed funds are taken in the same way for computing taxes as in case of any other

capital asset.

The profits which are generated from shares are generally dividend income which is

considered to be part of ordinary income for the purpose of taxation. The situation which is

provided in the question clearly shows that the taxpayer has reported capital gains from the sales

of shares of PHB, Common Ltd and Build Ltd. In addition to this, the taxpayer also shows losses

which the taxpayer has incurred due to the trading in shares during the year. The taxpayer has the

option of setting off the capital losses with the capital gains during the year and any balance is to

be included in the taxable income of the taxpayer.

Part E: Violin

As per the case the taxpayer has a variety of violin collection out of which the taxpayer

sold one during the current year for $ 12,000 which has initially costed the taxpayer an amount

of $ 5,500 on 1999. The section of taxation rulings in Australia covers the personal use of assets

under section 108-C. As per section 108-20 (2), an asset which are of non-collectable nature is

identified if the asset is kept for the pleasure and enjoyment of the taxpayer when the same are

5

TAXATION

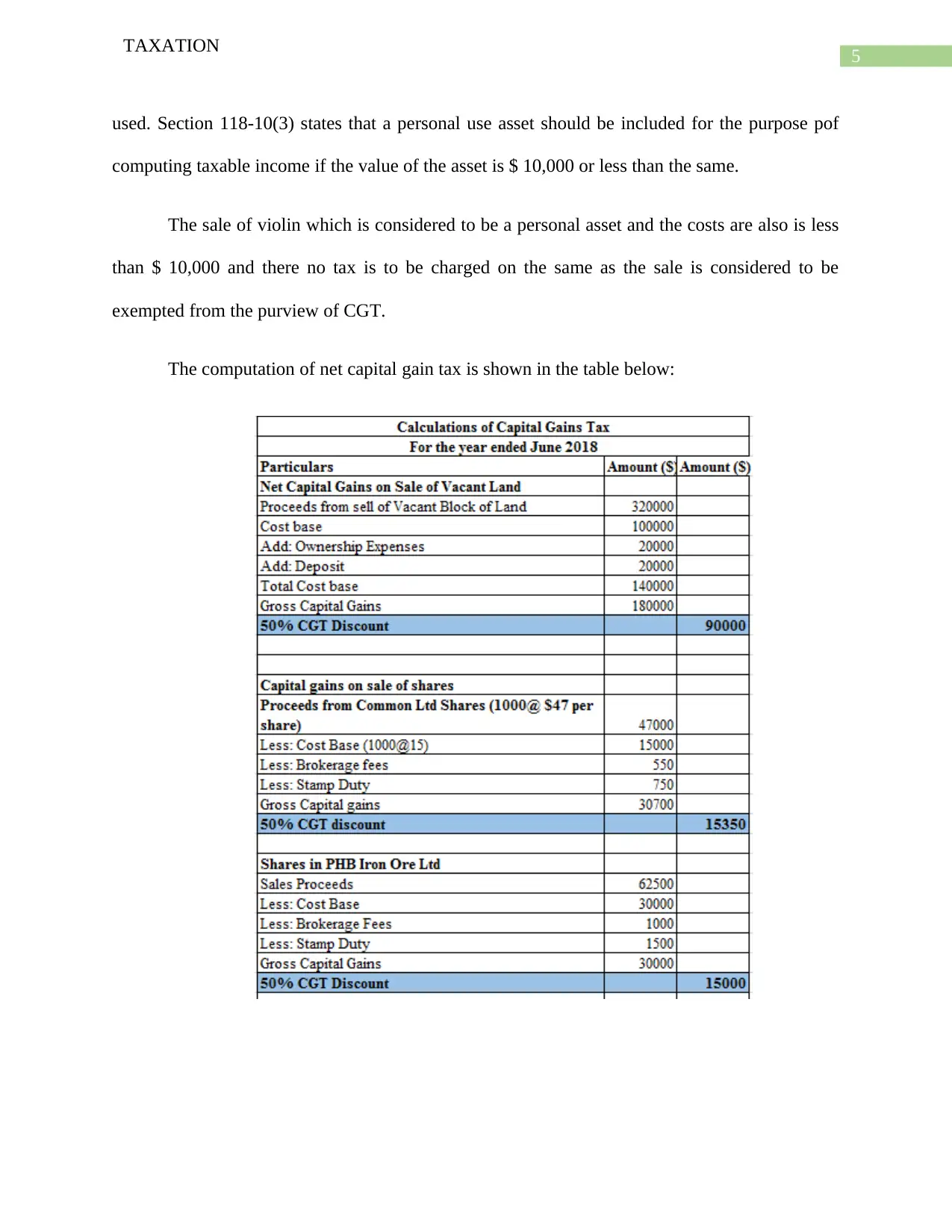

used. Section 118-10(3) states that a personal use asset should be included for the purpose pof

computing taxable income if the value of the asset is $ 10,000 or less than the same.

The sale of violin which is considered to be a personal asset and the costs are also is less

than $ 10,000 and there no tax is to be charged on the same as the sale is considered to be

exempted from the purview of CGT.

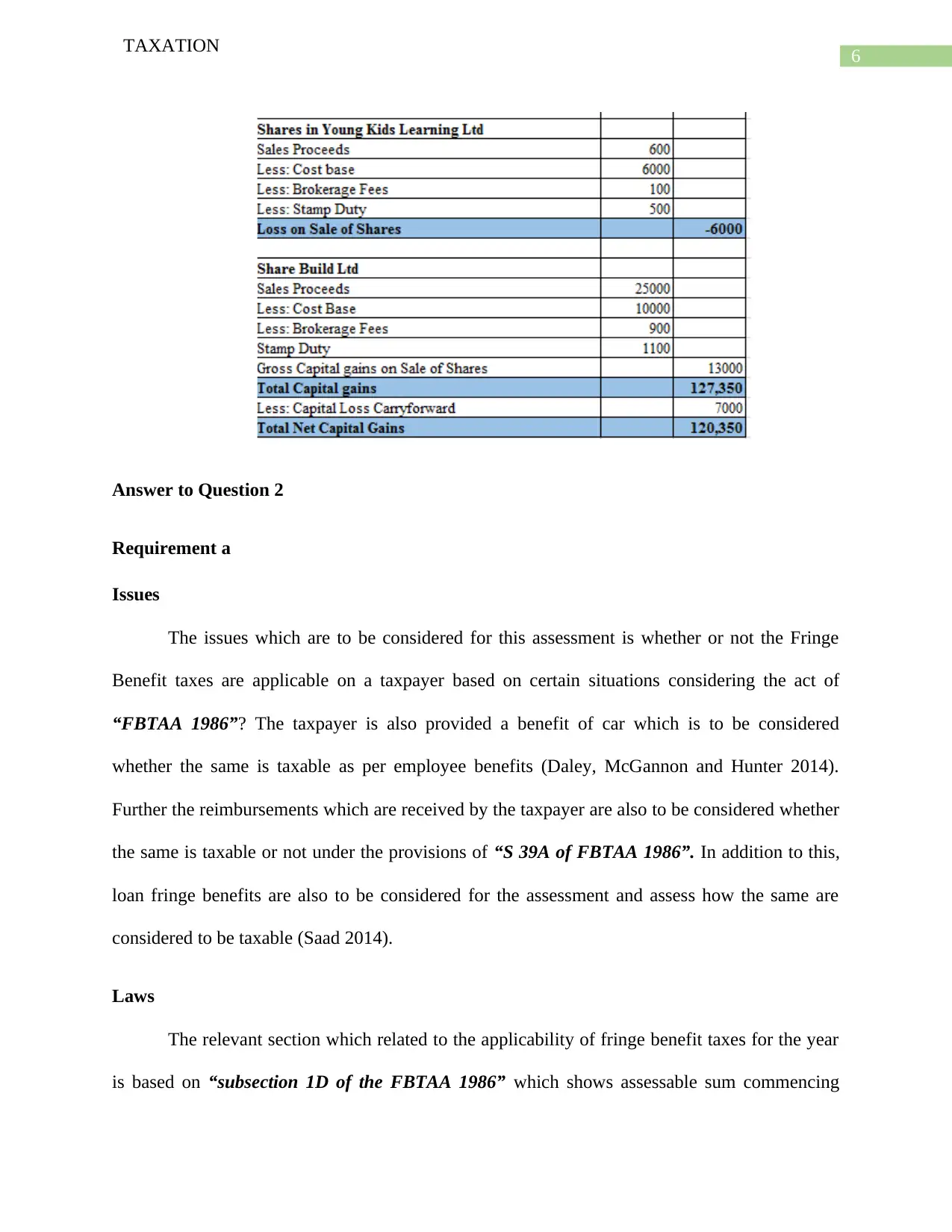

The computation of net capital gain tax is shown in the table below:

TAXATION

used. Section 118-10(3) states that a personal use asset should be included for the purpose pof

computing taxable income if the value of the asset is $ 10,000 or less than the same.

The sale of violin which is considered to be a personal asset and the costs are also is less

than $ 10,000 and there no tax is to be charged on the same as the sale is considered to be

exempted from the purview of CGT.

The computation of net capital gain tax is shown in the table below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION

Answer to Question 2

Requirement a

Issues

The issues which are to be considered for this assessment is whether or not the Fringe

Benefit taxes are applicable on a taxpayer based on certain situations considering the act of

“FBTAA 1986”? The taxpayer is also provided a benefit of car which is to be considered

whether the same is taxable as per employee benefits (Daley, McGannon and Hunter 2014).

Further the reimbursements which are received by the taxpayer are also to be considered whether

the same is taxable or not under the provisions of “S 39A of FBTAA 1986”. In addition to this,

loan fringe benefits are also to be considered for the assessment and assess how the same are

considered to be taxable (Saad 2014).

Laws

The relevant section which related to the applicability of fringe benefit taxes for the year

is based on “subsection 1D of the FBTAA 1986” which shows assessable sum commencing

TAXATION

Answer to Question 2

Requirement a

Issues

The issues which are to be considered for this assessment is whether or not the Fringe

Benefit taxes are applicable on a taxpayer based on certain situations considering the act of

“FBTAA 1986”? The taxpayer is also provided a benefit of car which is to be considered

whether the same is taxable as per employee benefits (Daley, McGannon and Hunter 2014).

Further the reimbursements which are received by the taxpayer are also to be considered whether

the same is taxable or not under the provisions of “S 39A of FBTAA 1986”. In addition to this,

loan fringe benefits are also to be considered for the assessment and assess how the same are

considered to be taxable (Saad 2014).

Laws

The relevant section which related to the applicability of fringe benefit taxes for the year

is based on “subsection 1D of the FBTAA 1986” which shows assessable sum commencing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION

from 1st April 2000. There is huge difference between benefits which normally includes some

rights or privileges and the term fringe benefits represent benefits which are provided by the

employer to the employee of the business under the terms of employment as stated in FBT

regulations (Tang and Wan 2015). In such an instance it is very essential to understand the

meaning of an employee which represent an individual who receives salaries, wages and any

benefits which the employee receives in lieu of salary and wages. It can also be stated that the

fringe benefits are received by employees of an organization just because they are employed in

an organization.

In case of fringe benefit taxes, an employer is held responsible for the taxes as the same

are provided by the employers to the employee of the business. An employer irrespective of the

situation needs to incur Fringe Benefit taxes (Evans, Lignier and Tran-Nam 2013). There are

various fringe benefit taxes which are applicable on employees based on the benefits which are

provided by the employees of the business.

A fringe benefit in relation to a car arises when a employers offers such a benefit to the

employee which can be both for personal as well as official use. This is covered under “section

7, FBTAA 1986”. As per the provisions, the car fringe benefits only arises when the same can be

used for personal use of the employee for any given day and the car is not at the work site of the

employee or residence of the employee.

The provisions which are included in “FBTAA 1986” states a car benefit is allow to an

employee for the purpose of making the travel of the employee easier from home to work place

and the same is to treated as official use of the vehicle (Le Vine, Jones and Polak 2013). In such

a case when a car is taken for extensive repairs than such will not be considered application of

TAXATION

from 1st April 2000. There is huge difference between benefits which normally includes some

rights or privileges and the term fringe benefits represent benefits which are provided by the

employer to the employee of the business under the terms of employment as stated in FBT

regulations (Tang and Wan 2015). In such an instance it is very essential to understand the

meaning of an employee which represent an individual who receives salaries, wages and any

benefits which the employee receives in lieu of salary and wages. It can also be stated that the

fringe benefits are received by employees of an organization just because they are employed in

an organization.

In case of fringe benefit taxes, an employer is held responsible for the taxes as the same

are provided by the employers to the employee of the business. An employer irrespective of the

situation needs to incur Fringe Benefit taxes (Evans, Lignier and Tran-Nam 2013). There are

various fringe benefit taxes which are applicable on employees based on the benefits which are

provided by the employees of the business.

A fringe benefit in relation to a car arises when a employers offers such a benefit to the

employee which can be both for personal as well as official use. This is covered under “section

7, FBTAA 1986”. As per the provisions, the car fringe benefits only arises when the same can be

used for personal use of the employee for any given day and the car is not at the work site of the

employee or residence of the employee.

The provisions which are included in “FBTAA 1986” states a car benefit is allow to an

employee for the purpose of making the travel of the employee easier from home to work place

and the same is to treated as official use of the vehicle (Le Vine, Jones and Polak 2013). In such

a case when a car is taken for extensive repairs than such will not be considered application of

8

TAXATION

the car for private use (Eccleston 2013). However, if the car is taken for routine servicing and

maintenance than the same will be considered to be private use of the car. As held in the case of

“Lunney v FCT (1958)” the commissioner of tax held an opinion that travelling from home to

the place of work can be considered to be personal use of the car.

“Division 5 of the FBTAA 1986” covers expense fringe benefits which are made

available to the employees of the organization. Expense fringe benefits are considered when the

employee incurs certain expenses which are then reimbursed by the employer. Similarly, such

fringe benefits can also arise when the employer pays certain expenses on behalf of the

employee. Here it is to be noted that the taxable amount for such expenses fringe benefits will be

the amount which is reimbursed or incurred by the employer.

As per “division 10A of the FBTAA 1986” car parking fringe benefits which simply

reflect the facility which is provided by the employer relating to car parking area allowed by the

employer to the employees of the business. This is basically a parking space which is provided to

the employee by the employer of the business. However, there are certain conditions which are

to be met in order for a benefit to qualify as car parking fringe benefits as per “Division 10A,

FBTAA 1986” which are listed below:

The parking space which the employee is to use is owned or leased by the employer.

The car which is provided by the employer should be parked in a radius of one kilometer

of a commercial parking and charges fees for the service.

The car should be parked for a time interval of more than four hours a day.

The benefit of car is provided in relation to the employment of the individual.

TAXATION

the car for private use (Eccleston 2013). However, if the car is taken for routine servicing and

maintenance than the same will be considered to be private use of the car. As held in the case of

“Lunney v FCT (1958)” the commissioner of tax held an opinion that travelling from home to

the place of work can be considered to be personal use of the car.

“Division 5 of the FBTAA 1986” covers expense fringe benefits which are made

available to the employees of the organization. Expense fringe benefits are considered when the

employee incurs certain expenses which are then reimbursed by the employer. Similarly, such

fringe benefits can also arise when the employer pays certain expenses on behalf of the

employee. Here it is to be noted that the taxable amount for such expenses fringe benefits will be

the amount which is reimbursed or incurred by the employer.

As per “division 10A of the FBTAA 1986” car parking fringe benefits which simply

reflect the facility which is provided by the employer relating to car parking area allowed by the

employer to the employees of the business. This is basically a parking space which is provided to

the employee by the employer of the business. However, there are certain conditions which are

to be met in order for a benefit to qualify as car parking fringe benefits as per “Division 10A,

FBTAA 1986” which are listed below:

The parking space which the employee is to use is owned or leased by the employer.

The car which is provided by the employer should be parked in a radius of one kilometer

of a commercial parking and charges fees for the service.

The car should be parked for a time interval of more than four hours a day.

The benefit of car is provided in relation to the employment of the individual.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION

The fringe benefit which is available to an employee in relation to loan wavier or debt

waiver. The loan fringe benefit occurs when the employer offers a loan to the employee at a

lower rate of interest in comparison to what is charged as a statutory interest rate (Burkhauser,

Hahn and Wilkins 2015). The loan and debt waiver fringe benefit are covered in “Division 4 of

the FBTAA 1986”

Application

The case study which is considered for this assessment is related to a business of Rapid

Heat Pty Ltd which is engaged in selling electric heaters. Jasmine is one of the employee who is

engaged in the employment with the company. Jasmine due to her job profile needs to travel a lot

and therefore the company has provided her with car benefits which can be used for official as

well as personal use. In such a circumstance, “section 7, FBTAA 1986” is applicable to the

business in such a circumstance is engaged in employment. As per the decision which was

passed in the case laws of “Lunney v FCT (1958)” the benefit of car will be classified as fringe

benefit expenses and Rapid heat Pty ltd will be liable for such expenses.

The case then shows that Jasmine utilizes the car to travel 10,000 km and has also

incurred$ 550 on repairs of the car which are reimbursed by the company. As per the situation,

the expense fringe benefit will be applicable which is covered under “division 5 of the FBTAA

1986". The amount which the business needs to incur as Fringe benefit tax is the amount which

is reimbursed to the employee.

The case further provides information that Jasmine did not use the car when she was

interstate. The car was parked at airport and another five days when the car was taken for repairs

at workstation. The provisions of “division 10A of the FBTAA 1986” clarifies that parking

TAXATION

The fringe benefit which is available to an employee in relation to loan wavier or debt

waiver. The loan fringe benefit occurs when the employer offers a loan to the employee at a

lower rate of interest in comparison to what is charged as a statutory interest rate (Burkhauser,

Hahn and Wilkins 2015). The loan and debt waiver fringe benefit are covered in “Division 4 of

the FBTAA 1986”

Application

The case study which is considered for this assessment is related to a business of Rapid

Heat Pty Ltd which is engaged in selling electric heaters. Jasmine is one of the employee who is

engaged in the employment with the company. Jasmine due to her job profile needs to travel a lot

and therefore the company has provided her with car benefits which can be used for official as

well as personal use. In such a circumstance, “section 7, FBTAA 1986” is applicable to the

business in such a circumstance is engaged in employment. As per the decision which was

passed in the case laws of “Lunney v FCT (1958)” the benefit of car will be classified as fringe

benefit expenses and Rapid heat Pty ltd will be liable for such expenses.

The case then shows that Jasmine utilizes the car to travel 10,000 km and has also

incurred$ 550 on repairs of the car which are reimbursed by the company. As per the situation,

the expense fringe benefit will be applicable which is covered under “division 5 of the FBTAA

1986". The amount which the business needs to incur as Fringe benefit tax is the amount which

is reimbursed to the employee.

The case further provides information that Jasmine did not use the car when she was

interstate. The car was parked at airport and another five days when the car was taken for repairs

at workstation. The provisions of “division 10A of the FBTAA 1986” clarifies that parking

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION

fringe benefits does not arise as the car was not parked near the premises of Rapid heat Pty

(Young and Miles 2015). In addition to this, the car was also not parked within 1 km radius from

place of work as the same was parked in airport and also in workstation for repairs (Frecknall-

Hughes and McKerchar 2013). Therefore, parking fringe benefits are not applicable to the

business. The case study also provides that the company provides Jasmine with a loan of $

500,000 which is provided with an interest of 4.25%. The interest rate is lower than statutory rate

and this results in fringe benefits relating to loans

Conclusion

As evident from the above stated discussion, Rapid Heat Pty should be applicable to loa

fringe benefit taxes during the FBT year. In addition to this, the relevant provisions also allows

Rapid Heat Pty to claim allowable deductions with respect to expenses incurred during the

course of employee’s term.

Answer to Question 2B

The provisions which are stated in “section 8-1 of the ITAA 1997” clearly indicates that

a taxpayer can claim deduction for expenses which are incurred by him in general course of

business. In the same way as per the hypothetical case, if Jasmine purchased shares with the

amount of $ 50,000 herself instead of giving a loan to her husband interest free, then she could

have claimed the deductions. However, as she gave the loan amount to her husband no deduction

will be allowed as per “section 8-1, ITAA 1997”.

TAXATION

fringe benefits does not arise as the car was not parked near the premises of Rapid heat Pty

(Young and Miles 2015). In addition to this, the car was also not parked within 1 km radius from

place of work as the same was parked in airport and also in workstation for repairs (Frecknall-

Hughes and McKerchar 2013). Therefore, parking fringe benefits are not applicable to the

business. The case study also provides that the company provides Jasmine with a loan of $

500,000 which is provided with an interest of 4.25%. The interest rate is lower than statutory rate

and this results in fringe benefits relating to loans

Conclusion

As evident from the above stated discussion, Rapid Heat Pty should be applicable to loa

fringe benefit taxes during the FBT year. In addition to this, the relevant provisions also allows

Rapid Heat Pty to claim allowable deductions with respect to expenses incurred during the

course of employee’s term.

Answer to Question 2B

The provisions which are stated in “section 8-1 of the ITAA 1997” clearly indicates that

a taxpayer can claim deduction for expenses which are incurred by him in general course of

business. In the same way as per the hypothetical case, if Jasmine purchased shares with the

amount of $ 50,000 herself instead of giving a loan to her husband interest free, then she could

have claimed the deductions. However, as she gave the loan amount to her husband no deduction

will be allowed as per “section 8-1, ITAA 1997”.

11

TAXATION

Reference

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Daley, J., McGannon, C. and Hunter, A., 2014. Budget pressures on Australian governments

2014. Grattan Institute.

Dowd, T., McClelland, R. and Muthitacharoen, A. 2015. New Evidence on the Tax Elasticity of

Capital Gains. National Tax Journal, 68(3), pp.511-544.

Eccleston, R., 2013. The tax reform agenda in Australia. Australian Journal of Public

Administration, 72(2), pp.103-113.

Evans, C., Lignier, P. and Tran-Nam, B., 2013. Tax compliance costs for the small and medium

enterprise business sector: Recent evidence from Australia. Tax Administration Research Centre

University of EXETER Discussion Paper, pp.003-13.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Frecknall-Hughes, J. and McKerchar, M., 2013. Historical perspectives on the emergence of the

tax profession: Australia and the UK. Austl. Tax F., 28, p.275.

TAXATION

Reference

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Daley, J., McGannon, C. and Hunter, A., 2014. Budget pressures on Australian governments

2014. Grattan Institute.

Dowd, T., McClelland, R. and Muthitacharoen, A. 2015. New Evidence on the Tax Elasticity of

Capital Gains. National Tax Journal, 68(3), pp.511-544.

Eccleston, R., 2013. The tax reform agenda in Australia. Australian Journal of Public

Administration, 72(2), pp.103-113.

Evans, C., Lignier, P. and Tran-Nam, B., 2013. Tax compliance costs for the small and medium

enterprise business sector: Recent evidence from Australia. Tax Administration Research Centre

University of EXETER Discussion Paper, pp.003-13.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Frecknall-Hughes, J. and McKerchar, M., 2013. Historical perspectives on the emergence of the

tax profession: Australia and the UK. Austl. Tax F., 28, p.275.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.