In-Depth Report on Capital Gains Tax and Fringe Benefits Tax

VerifiedAdded on 2023/06/07

|16

|3946

|421

Report

AI Summary

This assignment provides a detailed analysis of Australian taxation law, focusing on capital gains tax (CGT) and fringe benefits tax (FBT). It addresses various scenarios related to the sale of assets, including vacant land, antiques, paintings, shares, and personal use items like a violin, determining the CGT implications for each. The document also examines fringe benefit taxation issues, such as the provision of a car and expense reimbursements to employees, referencing relevant sections of the Fringe Benefits Tax Assessment Act 1986 (FBTAA). The analysis includes computations of net capital gains and discussions on the application of CGT discounts and exemptions. The assignment concludes by addressing issues related to expense payment fringe benefits and in-house expense payment fringe benefits under the FBTAA 1986.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Introduction:...............................................................................................................................2

Answer to question 1:.................................................................................................................2

Answer A: Block of Vacant Land:.........................................................................................2

Answer B: Sale of Antique Bed:............................................................................................3

Answer C: Painting:...............................................................................................................3

Answer D: Shares:..................................................................................................................4

Answer E: Violin:..................................................................................................................4

Answer to Question 2:................................................................................................................7

Answer to question 2 A:.............................................................................................................7

Answer A:..............................................................................................................................7

Issues:.....................................................................................................................................7

Laws:......................................................................................................................................7

Applications:..........................................................................................................................9

Conclusion:..........................................................................................................................11

Answer to 2 B:.....................................................................................................................11

References:...............................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................2

Answer to question 1:.................................................................................................................2

Answer A: Block of Vacant Land:.........................................................................................2

Answer B: Sale of Antique Bed:............................................................................................3

Answer C: Painting:...............................................................................................................3

Answer D: Shares:..................................................................................................................4

Answer E: Violin:..................................................................................................................4

Answer to Question 2:................................................................................................................7

Answer to question 2 A:.............................................................................................................7

Answer A:..............................................................................................................................7

Issues:.....................................................................................................................................7

Laws:......................................................................................................................................7

Applications:..........................................................................................................................9

Conclusion:..........................................................................................................................11

Answer to 2 B:.....................................................................................................................11

References:...............................................................................................................................12

2TAXATION LAW

Introduction:

The concept of capital gains tax is applied to the asset that are acquired or other event

taking place on or after the September 1985. Consequently, the terms of the pre-CGT and

post-CGT is commonly used to refer the assets that is purchased or events that take place

after the CGT event date (Seto 2015). The system of capital gains tax is applied on the system

on the disposal of the assets or from any other specified events.

Answer to question 1:

Answer A: Block of Vacant Land:

If an individual taxpayer has obtained the vacant land to use for the private purpose or

for the investment the land is generally regarded as the capital asset that will be subjected to

the capital gain tax when the land is sold by the taxpayer (Hoffman et al. 2014). As stated by

the Australian taxation office vacant land that is held by the taxpayer as the capital asset and

will be treated similar to any other asset for the purpose of capital gains. The taxpayer is

under the obligation of preserving the records of the date and costs for obtaining the land and

their ongoing expenses particularly the council rates and the interest on loan (Burns and

Ziliak 2017). The expenses however cannot be claimed as the income tax deductions but will

be included in the cost base of the land while computing the capital gains or capital loss when

the land is sold.

In the current case the taxpayer contracted to sell the vacant block of land for a sum of

$320,000. The taxpayer also reported outgoings on local council, water, sewerage rates and

land tax during the period of ownership of the land. The CGT event A1 happened under

“section 104-10 (1)” when the taxpayer sold the land (Stiglitz and Rosengard 2015). The

taxpayer under “section 102-5, ITAA 1997” will be required to include the net sum of capital

gains in their taxable income.

Introduction:

The concept of capital gains tax is applied to the asset that are acquired or other event

taking place on or after the September 1985. Consequently, the terms of the pre-CGT and

post-CGT is commonly used to refer the assets that is purchased or events that take place

after the CGT event date (Seto 2015). The system of capital gains tax is applied on the system

on the disposal of the assets or from any other specified events.

Answer to question 1:

Answer A: Block of Vacant Land:

If an individual taxpayer has obtained the vacant land to use for the private purpose or

for the investment the land is generally regarded as the capital asset that will be subjected to

the capital gain tax when the land is sold by the taxpayer (Hoffman et al. 2014). As stated by

the Australian taxation office vacant land that is held by the taxpayer as the capital asset and

will be treated similar to any other asset for the purpose of capital gains. The taxpayer is

under the obligation of preserving the records of the date and costs for obtaining the land and

their ongoing expenses particularly the council rates and the interest on loan (Burns and

Ziliak 2017). The expenses however cannot be claimed as the income tax deductions but will

be included in the cost base of the land while computing the capital gains or capital loss when

the land is sold.

In the current case the taxpayer contracted to sell the vacant block of land for a sum of

$320,000. The taxpayer also reported outgoings on local council, water, sewerage rates and

land tax during the period of ownership of the land. The CGT event A1 happened under

“section 104-10 (1)” when the taxpayer sold the land (Stiglitz and Rosengard 2015). The

taxpayer under “section 102-5, ITAA 1997” will be required to include the net sum of capital

gains in their taxable income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer B: Sale of Antique Bed:

Under subdivision 108-B collectable definition has been provided. Under section 108-

10 (2) a collectable is anything that is mainly used by the taxpayer and their associate for

their personal enjoyment and use (Becker, Reimer and Rust 2015). “Section 118-10 (1),

ITAA 1997” defines that collectables with the purchase value of $500 or less will be

exempted from the provision of CGT.

Present instances from the case derived suggest that the antique bed was stolen from

the premises of the taxpayer. It was later found that antique bed was not the part of the

taxpayer’s list of specified matters in the policy of insurance.

Additionally, under “section 104-25 (1)” when the asset is destroyed or damage a

CGT event C1 takes place (Auerbach and Hassett 2015). The receipt of compensation in the

current case for the stolen bed give rise to CGT event C1 since the compensation received

was for the lost asset.

Answer C: Painting:

Usually the functions of CGT operates prospectively and it is applicable if the CGT

event takes place for the assets that are purchased on after the 20-9-1985. For majority of the

CGT events, there are exceptions given the CGT asset is acquired before 20/09/2018

(Godber, Thornton and Stewart 2017). Therefore, an asset that is purchased before the CGT

event is introduced are usually held as the exempted CGT asset.

As evident in the current situation it is noticed that the painting was acquired by the

taxpayer on 2nd May 1985. The taxpayer sold the painting in the current tax year for

$125,000. As the asset was acquired before the introduction of CGT or before 20/09/1985

therefore, the asset will be considered as the pre-CGT asset that is exempted from the CGT

event.

Answer B: Sale of Antique Bed:

Under subdivision 108-B collectable definition has been provided. Under section 108-

10 (2) a collectable is anything that is mainly used by the taxpayer and their associate for

their personal enjoyment and use (Becker, Reimer and Rust 2015). “Section 118-10 (1),

ITAA 1997” defines that collectables with the purchase value of $500 or less will be

exempted from the provision of CGT.

Present instances from the case derived suggest that the antique bed was stolen from

the premises of the taxpayer. It was later found that antique bed was not the part of the

taxpayer’s list of specified matters in the policy of insurance.

Additionally, under “section 104-25 (1)” when the asset is destroyed or damage a

CGT event C1 takes place (Auerbach and Hassett 2015). The receipt of compensation in the

current case for the stolen bed give rise to CGT event C1 since the compensation received

was for the lost asset.

Answer C: Painting:

Usually the functions of CGT operates prospectively and it is applicable if the CGT

event takes place for the assets that are purchased on after the 20-9-1985. For majority of the

CGT events, there are exceptions given the CGT asset is acquired before 20/09/2018

(Godber, Thornton and Stewart 2017). Therefore, an asset that is purchased before the CGT

event is introduced are usually held as the exempted CGT asset.

As evident in the current situation it is noticed that the painting was acquired by the

taxpayer on 2nd May 1985. The taxpayer sold the painting in the current tax year for

$125,000. As the asset was acquired before the introduction of CGT or before 20/09/1985

therefore, the asset will be considered as the pre-CGT asset that is exempted from the CGT

event.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer D: Shares:

For an individual taxpayer or investors CGT is applicable to the gains that is made

from the shares or units when the CGT event takes place particular when the asset is sold

(Bronfenbrenner 2017). It is worth mentioning that the shares in the company or the units

trust together with the managed funds are considered as the same way as any other asset for

the purpose of capital gains tax.

Profits made by the taxpayer from the sale of shares are usually treated as the ordinary

income (Fairfield and Jorratt 2016). The taxpayer in the current situation reports capital gains

from shares that was held in PHB, Build Ltd and Common Ltd. In the later events the

taxpayer also reported loss from the sale upon selling the shares of young kids learning. The

taxpayer in the present situation can set-off the capital loss from the sale of young kids

learning shares against the capital gains made from the sale of PHB, Build Ltd and Common

Ltd.

Answer E: Violin:

The personal use assets are dealt under “subdivision 108-C”. The definition of

personal use asset is defined under “section 108-20 (2)” as the asset that are usually regarded

as the non-collectable asset where the assets held by the taxpayer are for the personal

enjoyment and use (Faccio and Xu 2015). These assets are boats, furniture, electrical goods

or any household items. The personal use asset does not include the land and buildings.

While section 108-30 explains that the cost of ownership of the personal use asset is not

included.

As stated under “section 118-10 (3)” the cost base of the personal asset that is less

than $10,000 or less should be ignored (Pearce and Pinto 2015). The taxpayer is only

required to keep the details of the asset that is bought for more than $10,000.

Answer D: Shares:

For an individual taxpayer or investors CGT is applicable to the gains that is made

from the shares or units when the CGT event takes place particular when the asset is sold

(Bronfenbrenner 2017). It is worth mentioning that the shares in the company or the units

trust together with the managed funds are considered as the same way as any other asset for

the purpose of capital gains tax.

Profits made by the taxpayer from the sale of shares are usually treated as the ordinary

income (Fairfield and Jorratt 2016). The taxpayer in the current situation reports capital gains

from shares that was held in PHB, Build Ltd and Common Ltd. In the later events the

taxpayer also reported loss from the sale upon selling the shares of young kids learning. The

taxpayer in the present situation can set-off the capital loss from the sale of young kids

learning shares against the capital gains made from the sale of PHB, Build Ltd and Common

Ltd.

Answer E: Violin:

The personal use assets are dealt under “subdivision 108-C”. The definition of

personal use asset is defined under “section 108-20 (2)” as the asset that are usually regarded

as the non-collectable asset where the assets held by the taxpayer are for the personal

enjoyment and use (Faccio and Xu 2015). These assets are boats, furniture, electrical goods

or any household items. The personal use asset does not include the land and buildings.

While section 108-30 explains that the cost of ownership of the personal use asset is not

included.

As stated under “section 118-10 (3)” the cost base of the personal asset that is less

than $10,000 or less should be ignored (Pearce and Pinto 2015). The taxpayer is only

required to keep the details of the asset that is bought for more than $10,000.

5TAXATION LAW

Evidence obtained from the case study explains that purchased the violin at the cost of

$5000. The violin constituted a personal use asset since it was used by asset for private

purpose only. As understood the cost of the asset was less than the stated limit of $10,000.

Therefore, the sale of violin and deriving capital gains thereon should not be ignored as it is a

personal use asset and exempted from CGT.

Below stated is the computation for the net capital gains made during the year.

Evidence obtained from the case study explains that purchased the violin at the cost of

$5000. The violin constituted a personal use asset since it was used by asset for private

purpose only. As understood the cost of the asset was less than the stated limit of $10,000.

Therefore, the sale of violin and deriving capital gains thereon should not be ignored as it is a

personal use asset and exempted from CGT.

Below stated is the computation for the net capital gains made during the year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

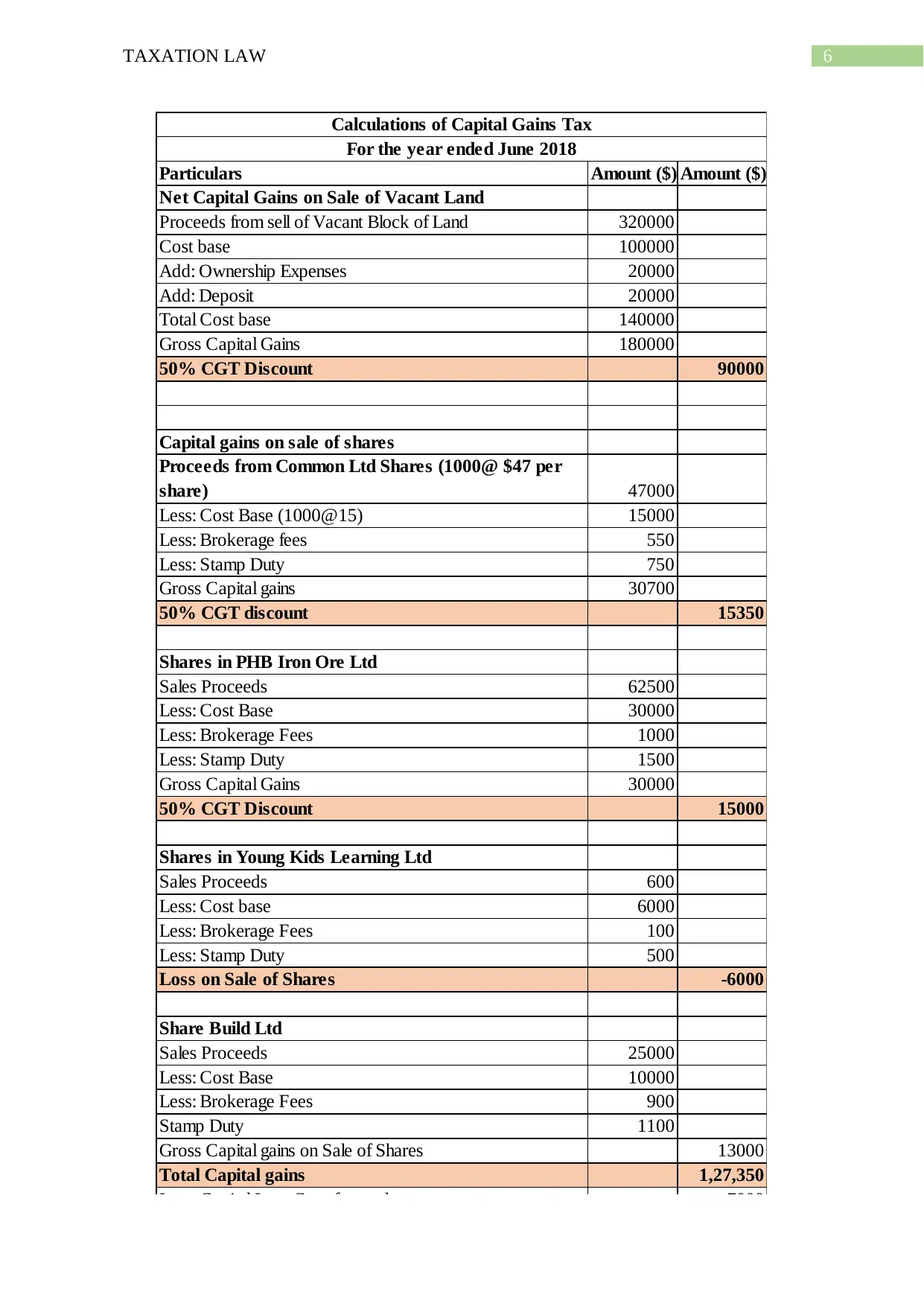

Particulars Amount ($) Amount ($)

Net Capital Gains on Sale of Vacant Land

Proceeds from sell of Vacant Block of Land 320000

Cost base 100000

Add: Ownership Expenses 20000

Add: Deposit 20000

Total Cost base 140000

Gross Capital Gains 180000

50% CGT Discount 90000

Capital gains on sale of shares

Proceeds from Common Ltd Shares (1000@ $47 per

share) 47000

Less: Cost Base (1000@15) 15000

Less: Brokerage fees 550

Less: Stamp Duty 750

Gross Capital gains 30700

50% CGT discount 15350

Shares in PHB Iron Ore Ltd

Sales Proceeds 62500

Less: Cost Base 30000

Less: Brokerage Fees 1000

Less: Stamp Duty 1500

Gross Capital Gains 30000

50% CGT Discount 15000

Shares in Young Kids Learning Ltd

Sales Proceeds 600

Less: Cost base 6000

Less: Brokerage Fees 100

Less: Stamp Duty 500

Loss on Sale of Shares -6000

Share Build Ltd

Sales Proceeds 25000

Less: Cost Base 10000

Less: Brokerage Fees 900

Stamp Duty 1100

Gross Capital gains on Sale of Shares 13000

Total Capital gains 1,27,350

Less: Capital Loss Carryforward 7000

Total Net Capital Gains 1,20,350

Calculations of Capital Gains Tax

For the year ended June 2018

Particulars Amount ($) Amount ($)

Net Capital Gains on Sale of Vacant Land

Proceeds from sell of Vacant Block of Land 320000

Cost base 100000

Add: Ownership Expenses 20000

Add: Deposit 20000

Total Cost base 140000

Gross Capital Gains 180000

50% CGT Discount 90000

Capital gains on sale of shares

Proceeds from Common Ltd Shares (1000@ $47 per

share) 47000

Less: Cost Base (1000@15) 15000

Less: Brokerage fees 550

Less: Stamp Duty 750

Gross Capital gains 30700

50% CGT discount 15350

Shares in PHB Iron Ore Ltd

Sales Proceeds 62500

Less: Cost Base 30000

Less: Brokerage Fees 1000

Less: Stamp Duty 1500

Gross Capital Gains 30000

50% CGT Discount 15000

Shares in Young Kids Learning Ltd

Sales Proceeds 600

Less: Cost base 6000

Less: Brokerage Fees 100

Less: Stamp Duty 500

Loss on Sale of Shares -6000

Share Build Ltd

Sales Proceeds 25000

Less: Cost Base 10000

Less: Brokerage Fees 900

Stamp Duty 1100

Gross Capital gains on Sale of Shares 13000

Total Capital gains 1,27,350

Less: Capital Loss Carryforward 7000

Total Net Capital Gains 1,20,350

Calculations of Capital Gains Tax

For the year ended June 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to Question 2:

Answer to question 2 A:

Answer A:

Issues:

Will the taxpayer in the current issue be subjected to fringe benefit taxation from the

events that are reported in capacity of the employee under the “FBTAA 1986”? Is the

taxpayer accountable to pay the FBT for the car provided in respect of the employment? The

issue also rotates on ascertaining that whether the reimbursement of the expenses give rise to

the FBT with respect to the “S 39A of FBTAA 1986”? Additionally, the issue also gives

explanation regarding the loan fringe benefit given to the employee under “sub division A of

FBTAA 1986”.

Laws:

With respect to the “subsection 1D of the FBTAA 1986” an employer’s fringe

benefit represents the assessable sum for the year commencing from the 1st April 2000. The

word benefit and fringe benefit possess greater meanings for the purpose of FBT (Tang and

Wan 2015). The benefits comprise of the rights, privileges and the services. As defined under

the FBT legislation, an employer providing fringe benefit to the employee with respect to the

employment constitute benefit. The benefit provided some person is because they are the

employed as employee. The employee can anyone ranging from the former employee to the

future employee. An employee is that person that will be entitled to receive the salary or the

wages or the benefits in lieu of the salary or wages.

An employer will be held responsible for the fringe benefit tax given the employer

makes any payment to the employee or the company, or the holder of office that that are

subjected to obligations of withholding or the employer provides the benefits in lieu of the

Answer to Question 2:

Answer to question 2 A:

Answer A:

Issues:

Will the taxpayer in the current issue be subjected to fringe benefit taxation from the

events that are reported in capacity of the employee under the “FBTAA 1986”? Is the

taxpayer accountable to pay the FBT for the car provided in respect of the employment? The

issue also rotates on ascertaining that whether the reimbursement of the expenses give rise to

the FBT with respect to the “S 39A of FBTAA 1986”? Additionally, the issue also gives

explanation regarding the loan fringe benefit given to the employee under “sub division A of

FBTAA 1986”.

Laws:

With respect to the “subsection 1D of the FBTAA 1986” an employer’s fringe

benefit represents the assessable sum for the year commencing from the 1st April 2000. The

word benefit and fringe benefit possess greater meanings for the purpose of FBT (Tang and

Wan 2015). The benefits comprise of the rights, privileges and the services. As defined under

the FBT legislation, an employer providing fringe benefit to the employee with respect to the

employment constitute benefit. The benefit provided some person is because they are the

employed as employee. The employee can anyone ranging from the former employee to the

future employee. An employee is that person that will be entitled to receive the salary or the

wages or the benefits in lieu of the salary or wages.

An employer will be held responsible for the fringe benefit tax given the employer

makes any payment to the employee or the company, or the holder of office that that are

subjected to obligations of withholding or the employer provides the benefits in lieu of the

8TAXATION LAW

payments. Being the employer, a person is required to pay the FBT irrespective of the

circumstances whether the employer is the sole trader, partnership, unincorporated

association or the authority of government (Hodgson and Pearce 2015). This is also

irrespective of the fact that the employer pays the FBT to the employee or any other party. It

is worth mentioning that the FBT is payable irrespective of the situation whether they are

liable to pay the other taxes particularly the income tax.

A car fringe benefit under “section 7, FBTAA 1986” includes the benefit that arises

most commonly under the circumstances where the employer makes the car that they hold

available for the employee’s private use (White and Townsend 2018). For an employer the

car they generally hold is the car they make available for employee’s usage. The employer

generally makes the car available for the employee’s personal usage when the car is really

used for the private purpose by the employer. A car fringe benefit only arises when the car is

available by the employee for their private use during any day when the car is not at the

premise of their employer or the car is garaged at the home of the employee.

The “FBTAA 1986” states the general rule that travel from and to the work place will

be treated as the private use of the vehicle. Where the car is in the workshop for the purpose

of extensive repairs it is not regarded as the private use of the employee (Pearce and Hodgson

2015). However, the car will be treated as under the private use of the employee when the car

is in the workshop for the routine services or maintenance. The commissioner of taxation in

“Lunney v FCT (1958)” provided an explanation that travelling from the home and to the

place of work give rise to the employee personal use of car.

Referring to the “Division 5 of the FBTAA 1986” an explanation relating to the

expense payment fringe benefit might originate when the employer makes any form of

reimbursement for the expenses that the employee incurs (Godber, Thornton and Stewart

payments. Being the employer, a person is required to pay the FBT irrespective of the

circumstances whether the employer is the sole trader, partnership, unincorporated

association or the authority of government (Hodgson and Pearce 2015). This is also

irrespective of the fact that the employer pays the FBT to the employee or any other party. It

is worth mentioning that the FBT is payable irrespective of the situation whether they are

liable to pay the other taxes particularly the income tax.

A car fringe benefit under “section 7, FBTAA 1986” includes the benefit that arises

most commonly under the circumstances where the employer makes the car that they hold

available for the employee’s private use (White and Townsend 2018). For an employer the

car they generally hold is the car they make available for employee’s usage. The employer

generally makes the car available for the employee’s personal usage when the car is really

used for the private purpose by the employer. A car fringe benefit only arises when the car is

available by the employee for their private use during any day when the car is not at the

premise of their employer or the car is garaged at the home of the employee.

The “FBTAA 1986” states the general rule that travel from and to the work place will

be treated as the private use of the vehicle. Where the car is in the workshop for the purpose

of extensive repairs it is not regarded as the private use of the employee (Pearce and Hodgson

2015). However, the car will be treated as under the private use of the employee when the car

is in the workshop for the routine services or maintenance. The commissioner of taxation in

“Lunney v FCT (1958)” provided an explanation that travelling from the home and to the

place of work give rise to the employee personal use of car.

Referring to the “Division 5 of the FBTAA 1986” an explanation relating to the

expense payment fringe benefit might originate when the employer makes any form of

reimbursement for the expenses that the employee incurs (Godber, Thornton and Stewart

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

2017). Alternatively, the expense fringe benefit arises when the employer pays the third party

in satisfaction of the expenditure that is occurred by the employee. In either of the cases the

expenditure might be business outgoings or the private outgoings or may be the combination

of both. The chargeable value of the expenditure fringe benefit represents the value that is

reimbursed or paid by the employer. Additionally, an in house expense payment fringe

benefit happens when the expenditure that is in incurred by the employee is reimbursed by

the employer.

Under “division 10A of the FBTAA 1986” the car parking fringe benefit happens for

each when the employer provides the employee with the space for parking car that is used by

the employee (Shields and North-Samardzic 2015). “Division 10A, FBTAA 1986” explains

that the car parking fringe benefit happens when all the below stated following conditions are

met;

a. The car is parked at the premises which the employer owns or leases

b. The car is parked inside the one kilometre area where the facilities of commercial

parking is available and charges fees for the entire day parking.

c. The car is parked for more than four hours during the day

d. The car is provided in relation to the employment of the employee

“Division 4 of the FBTAA 1986” provides explanation regarding the loan and debt

waiver fringe benefit (Seymour 2017). A loan fringe benefit happens when the employer

provides the employee with the loan and charges a very lower amount of interest rate all

through the FBT year. It is worth mentioning that the lower rate of interest is one which is

lower than the statutory rate of interest.

2017). Alternatively, the expense fringe benefit arises when the employer pays the third party

in satisfaction of the expenditure that is occurred by the employee. In either of the cases the

expenditure might be business outgoings or the private outgoings or may be the combination

of both. The chargeable value of the expenditure fringe benefit represents the value that is

reimbursed or paid by the employer. Additionally, an in house expense payment fringe

benefit happens when the expenditure that is in incurred by the employee is reimbursed by

the employer.

Under “division 10A of the FBTAA 1986” the car parking fringe benefit happens for

each when the employer provides the employee with the space for parking car that is used by

the employee (Shields and North-Samardzic 2015). “Division 10A, FBTAA 1986” explains

that the car parking fringe benefit happens when all the below stated following conditions are

met;

a. The car is parked at the premises which the employer owns or leases

b. The car is parked inside the one kilometre area where the facilities of commercial

parking is available and charges fees for the entire day parking.

c. The car is parked for more than four hours during the day

d. The car is provided in relation to the employment of the employee

“Division 4 of the FBTAA 1986” provides explanation regarding the loan and debt

waiver fringe benefit (Seymour 2017). A loan fringe benefit happens when the employer

provides the employee with the loan and charges a very lower amount of interest rate all

through the FBT year. It is worth mentioning that the lower rate of interest is one which is

lower than the statutory rate of interest.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Applications:

The case study opens up with the explanation that Jasmine is the employee of Rapid

Heat Pty Ltd that sells electric heaters. As the part of the employment, Jasmine was required

to travel a lot due to the work purpose. Rapid in such situation provided Jasmine with the car

for the work purpose. Jasmine can use also use the car for the private purpose as well. In such

a situation “section 7, FBTAA 1986” will be applied for Rapid Heat since the employer

provided the car to Jasmine for the work purpose as well as for the private purpose (Barkoczy

2016). Rapid Heat made the car available for the Jasmine personal usage as well as for the

work purpose during the course of the employment. With respect to the judgement made in

the “Lunney v FCT (1958)” the use car by Jasmine is a fringe benefit. While Rapid Heat Pty

Ltd will be liable for the fringe benefit tax for providing the car to Jasmine.

In the late part of the case it is noticed that Jasmine used the car to travel 10,000 km

and also occurred expenses of $550 on the minor repairs that is reimbursed by the Rapid-

Heat. It is worth mentioning that the employer reimbursed Jasmine with the sum of repair

expenses that was incurred for minor repairs. In such a situation under “division 5 of the

FBTAA 1986", the expense payment fringe benefit has arisen for Rapid Heat Pty Ltd (Foster

2016). This is because the employer Rapid Heat disbursed the employee with the

reimbursement for the expenses that Jasmine incurred for minor repairs on car. The

chargeable value of the expenditure fringe benefit for Rapid Heat represents the value that is

reimbursed or paid to Jasmine.

In the later events it is noticed that Jasmine did not used the car when she was

interstate and she parked the car at the airport and another five days when the car was parked

at the workstation for the purpose of scheduled repair. Referring to the “division 10A of the

FBTAA 1986” no parking fringe benefit arises for Rapid Heat Pty because the car was not

parked at the premises of the Rapid Heat Pty (Shields and North-Samardzic 2015).

Applications:

The case study opens up with the explanation that Jasmine is the employee of Rapid

Heat Pty Ltd that sells electric heaters. As the part of the employment, Jasmine was required

to travel a lot due to the work purpose. Rapid in such situation provided Jasmine with the car

for the work purpose. Jasmine can use also use the car for the private purpose as well. In such

a situation “section 7, FBTAA 1986” will be applied for Rapid Heat since the employer

provided the car to Jasmine for the work purpose as well as for the private purpose (Barkoczy

2016). Rapid Heat made the car available for the Jasmine personal usage as well as for the

work purpose during the course of the employment. With respect to the judgement made in

the “Lunney v FCT (1958)” the use car by Jasmine is a fringe benefit. While Rapid Heat Pty

Ltd will be liable for the fringe benefit tax for providing the car to Jasmine.

In the late part of the case it is noticed that Jasmine used the car to travel 10,000 km

and also occurred expenses of $550 on the minor repairs that is reimbursed by the Rapid-

Heat. It is worth mentioning that the employer reimbursed Jasmine with the sum of repair

expenses that was incurred for minor repairs. In such a situation under “division 5 of the

FBTAA 1986", the expense payment fringe benefit has arisen for Rapid Heat Pty Ltd (Foster

2016). This is because the employer Rapid Heat disbursed the employee with the

reimbursement for the expenses that Jasmine incurred for minor repairs on car. The

chargeable value of the expenditure fringe benefit for Rapid Heat represents the value that is

reimbursed or paid to Jasmine.

In the later events it is noticed that Jasmine did not used the car when she was

interstate and she parked the car at the airport and another five days when the car was parked

at the workstation for the purpose of scheduled repair. Referring to the “division 10A of the

FBTAA 1986” no parking fringe benefit arises for Rapid Heat Pty because the car was not

parked at the premises of the Rapid Heat Pty (Shields and North-Samardzic 2015).

11TAXATION LAW

Furthermore, though the car was provided to Jasmine by Rapid Heat in respect of the

employment but the car was not parked inside the one kilometre area where the facilities of

commercial parking was not available. As a result, no fringe benefit tax will be applicable for

Rapid Heat Pty Ltd in this situation.

The case study explains that Rapid Heat Pty Ltd provided Jasmine with the loan of

$500,000 at the annual interest rate of 4.25%. Therefore, in such a situation a loan fringe

benefit has arises for Rapid Heat Pty since the loan is provided in respect of the employment.

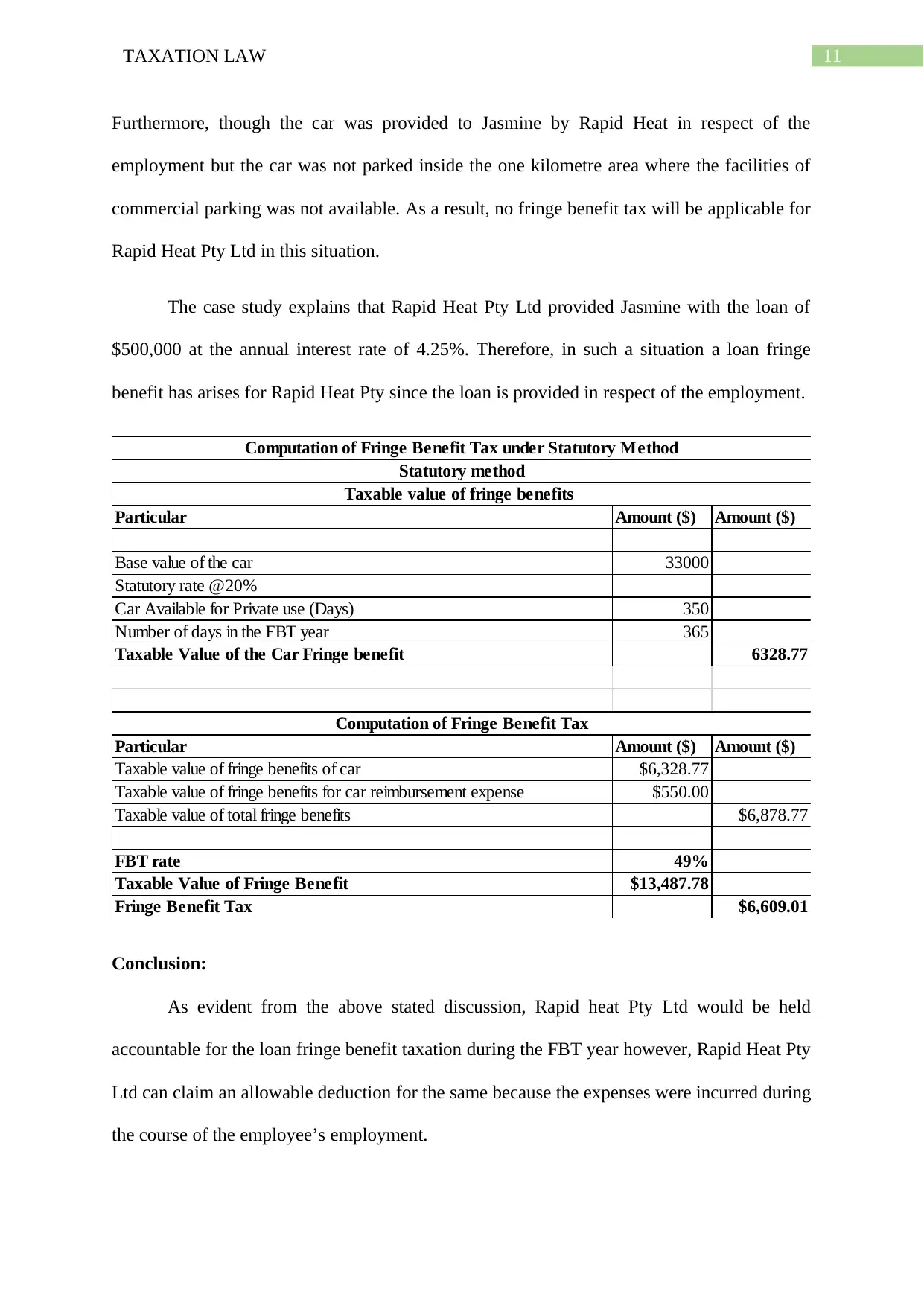

Particular Amount ($) Amount ($)

Base value of the car 33000

Statutory rate @20%

Car Available for Private use (Days) 350

Number of days in the FBT year 365

Taxable Value of the Car Fringe benefit 6328.77

Particular Amount ($) Amount ($)

Taxable value of fringe benefits of car $6,328.77

Taxable value of fringe benefits for car reimbursement expense $550.00

Taxable value of total fringe benefits $6,878.77

FBT rate 49%

Taxable Value of Fringe Benefit $13,487.78

Fringe Benefit Tax $6,609.01

Computation of Fringe Benefit Tax

Computation of Fringe Benefit Tax under Statutory Method

Statutory method

Taxable value of fringe benefits

Conclusion:

As evident from the above stated discussion, Rapid heat Pty Ltd would be held

accountable for the loan fringe benefit taxation during the FBT year however, Rapid Heat Pty

Ltd can claim an allowable deduction for the same because the expenses were incurred during

the course of the employee’s employment.

Furthermore, though the car was provided to Jasmine by Rapid Heat in respect of the

employment but the car was not parked inside the one kilometre area where the facilities of

commercial parking was not available. As a result, no fringe benefit tax will be applicable for

Rapid Heat Pty Ltd in this situation.

The case study explains that Rapid Heat Pty Ltd provided Jasmine with the loan of

$500,000 at the annual interest rate of 4.25%. Therefore, in such a situation a loan fringe

benefit has arises for Rapid Heat Pty since the loan is provided in respect of the employment.

Particular Amount ($) Amount ($)

Base value of the car 33000

Statutory rate @20%

Car Available for Private use (Days) 350

Number of days in the FBT year 365

Taxable Value of the Car Fringe benefit 6328.77

Particular Amount ($) Amount ($)

Taxable value of fringe benefits of car $6,328.77

Taxable value of fringe benefits for car reimbursement expense $550.00

Taxable value of total fringe benefits $6,878.77

FBT rate 49%

Taxable Value of Fringe Benefit $13,487.78

Fringe Benefit Tax $6,609.01

Computation of Fringe Benefit Tax

Computation of Fringe Benefit Tax under Statutory Method

Statutory method

Taxable value of fringe benefits

Conclusion:

As evident from the above stated discussion, Rapid heat Pty Ltd would be held

accountable for the loan fringe benefit taxation during the FBT year however, Rapid Heat Pty

Ltd can claim an allowable deduction for the same because the expenses were incurred during

the course of the employee’s employment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.