Sale of Land 4 Answer to Question 1: 2 Answer to Question 2: 6 Answer to E: 8 Answer to F: 8 Answer to E: 8 Answer to E: 8 Answer to F: 8 Answer to E: 8 Answer to E: 8 Answer to E: 8 Answer to E: 8 An

VerifiedAdded on 2022/08/19

|12

|2492

|14

AI Summary

LAWS OF TAXATION LAWS OF TAXATION LAWS OF TAXATION 108-10 10 LAWS OF TAXATION Name of Student Name of University Author note Word count Answer of question 1: 2 Answer A: Sale of block of land 2 Answer B: Sale of shares 4 Answer C: Sale of Stamp Collection 4 Answer D: Sale of Guitar 5 Answer to question 2: 6 Answer to A: 6 Answer to B: 6 Answer to C: 7 Answer to D: 7 Answer to E:

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: LAWS OF TAXATION

LAWS OF TAXATION

Name of Student

Name of University

Author note

Word count

LAWS OF TAXATION

Name of Student

Name of University

Author note

Word count

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1LAWS OF TAXATION

Table of Contents

Answer of question 1:................................................................................................................2

Answer A: Sale of block of land................................................................................................2

Answer B: Sale of shares...........................................................................................................4

Answer C: Sale of Stamp Collection.........................................................................................4

Answer D: Sale of Guitar...........................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to A:..............................................................................................................................6

Answer to B:..............................................................................................................................6

Answer to C:..............................................................................................................................7

Answer to D:..............................................................................................................................7

Answer to E:...............................................................................................................................8

Answer to F:...............................................................................................................................8

Answer to G:..............................................................................................................................8

Answer to H:..............................................................................................................................9

References................................................................................................................................10

Table of Contents

Answer of question 1:................................................................................................................2

Answer A: Sale of block of land................................................................................................2

Answer B: Sale of shares...........................................................................................................4

Answer C: Sale of Stamp Collection.........................................................................................4

Answer D: Sale of Guitar...........................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to A:..............................................................................................................................6

Answer to B:..............................................................................................................................6

Answer to C:..............................................................................................................................7

Answer to D:..............................................................................................................................7

Answer to E:...............................................................................................................................8

Answer to F:...............................................................................................................................8

Answer to G:..............................................................................................................................8

Answer to H:..............................................................................................................................9

References................................................................................................................................10

2LAWS OF TAXATION

Answer of question 1:

Answer A: Sale of block of land

Five elements are basically included in the cost. As mentioned under “sect-110-25

(2)” the first elements includes property paid or the money paid to obtain an asset. “Sect-110-

35” describes second element of cost which includes incidental costs which includes legal

fees, stamp duty etc. The third elements includes the cost of ownership which involve

ownership costs, land taxes, insurances and interests (McCluskey and Franzsen, 2017). As

mentioned under “sect-110-38”, the fourth element includes the cost of preservation and

capital improvement. Improvement, installation expenses and moving expenses are the

example of this type of cost. Capital improvement in maintaining the title rights of assets are

included under the fifth elements of the cost. Under “sect-110-45” includes the examples of

this cost which includes the cost which has occurred in acquisition of land by government

(O’Connell, 2017).

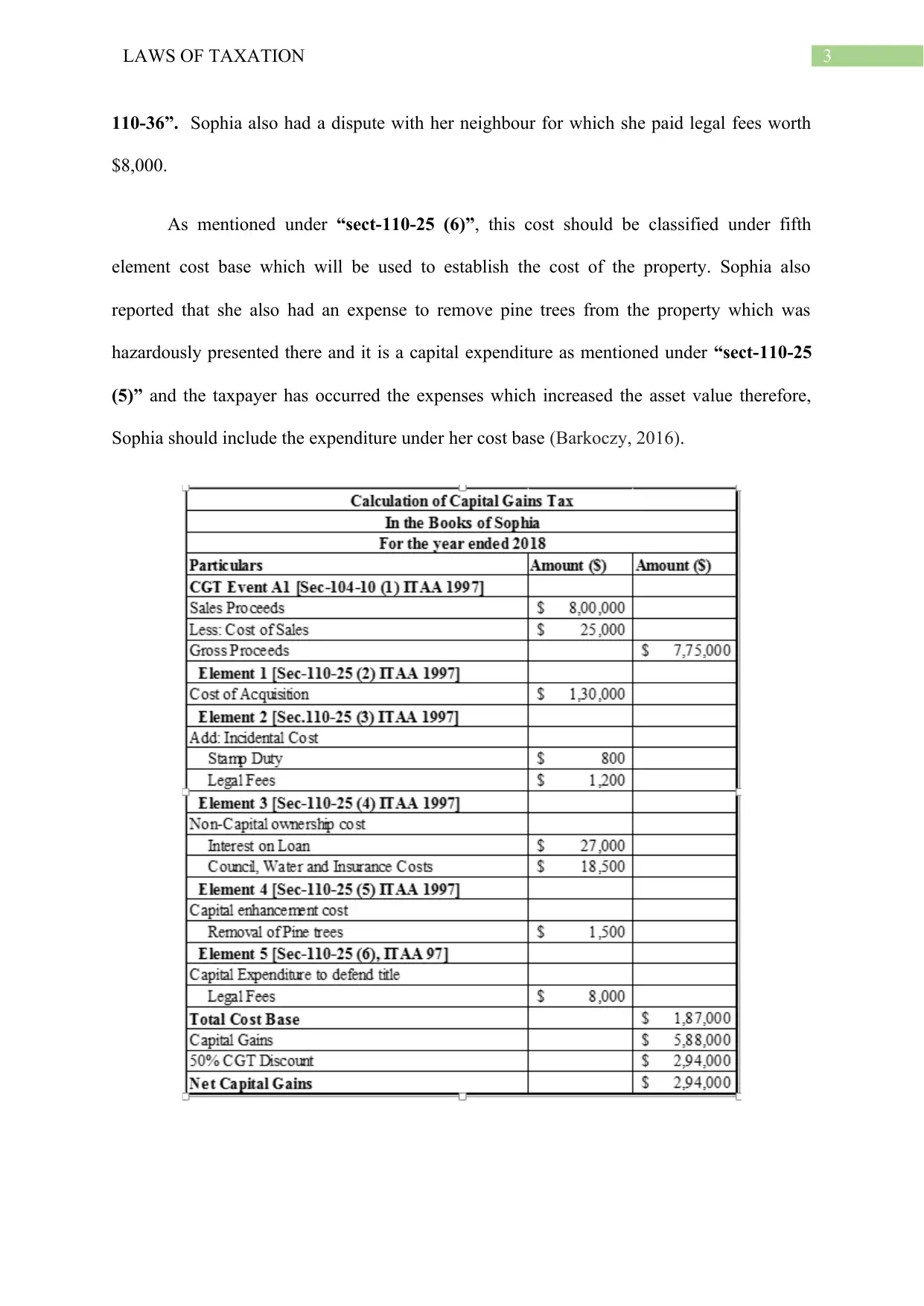

In the current situation, Sophia has reported that she sold a land for $800,000 which

she purchased for $130,000 in the year 1991. To ascertain the CGT of the land, the

acquisition cost of the asset must be understood. “Sect-110-25 (2)” describes that this

acquisition cost includes the cost of asset which is included in the purchase price paid by

Sophia on acquisition. Sophia also paid legal fees $1,200 and stamp duty for $800. “Sect-10-

35” describes that these type of cost are to be classified as incidental cost and therefore

Sophia should include the incidental amount in the cost base of the asset (Collier et.al, 2018).

Sophia also had a bank loan which she paid interest of $27,000 in order to purchase

the property. Sophia paid a water rates, council rates and insurance of $18,500 when she

owned the property. This type of expenses must be classified as property ownership cost and

hence she should add it in the cost base to calculate the net capital gains as noted under “sect-

Answer of question 1:

Answer A: Sale of block of land

Five elements are basically included in the cost. As mentioned under “sect-110-25

(2)” the first elements includes property paid or the money paid to obtain an asset. “Sect-110-

35” describes second element of cost which includes incidental costs which includes legal

fees, stamp duty etc. The third elements includes the cost of ownership which involve

ownership costs, land taxes, insurances and interests (McCluskey and Franzsen, 2017). As

mentioned under “sect-110-38”, the fourth element includes the cost of preservation and

capital improvement. Improvement, installation expenses and moving expenses are the

example of this type of cost. Capital improvement in maintaining the title rights of assets are

included under the fifth elements of the cost. Under “sect-110-45” includes the examples of

this cost which includes the cost which has occurred in acquisition of land by government

(O’Connell, 2017).

In the current situation, Sophia has reported that she sold a land for $800,000 which

she purchased for $130,000 in the year 1991. To ascertain the CGT of the land, the

acquisition cost of the asset must be understood. “Sect-110-25 (2)” describes that this

acquisition cost includes the cost of asset which is included in the purchase price paid by

Sophia on acquisition. Sophia also paid legal fees $1,200 and stamp duty for $800. “Sect-10-

35” describes that these type of cost are to be classified as incidental cost and therefore

Sophia should include the incidental amount in the cost base of the asset (Collier et.al, 2018).

Sophia also had a bank loan which she paid interest of $27,000 in order to purchase

the property. Sophia paid a water rates, council rates and insurance of $18,500 when she

owned the property. This type of expenses must be classified as property ownership cost and

hence she should add it in the cost base to calculate the net capital gains as noted under “sect-

3LAWS OF TAXATION

110-36”. Sophia also had a dispute with her neighbour for which she paid legal fees worth

$8,000.

As mentioned under “sect-110-25 (6)”, this cost should be classified under fifth

element cost base which will be used to establish the cost of the property. Sophia also

reported that she also had an expense to remove pine trees from the property which was

hazardously presented there and it is a capital expenditure as mentioned under “sect-110-25

(5)” and the taxpayer has occurred the expenses which increased the asset value therefore,

Sophia should include the expenditure under her cost base (Barkoczy, 2016).

110-36”. Sophia also had a dispute with her neighbour for which she paid legal fees worth

$8,000.

As mentioned under “sect-110-25 (6)”, this cost should be classified under fifth

element cost base which will be used to establish the cost of the property. Sophia also

reported that she also had an expense to remove pine trees from the property which was

hazardously presented there and it is a capital expenditure as mentioned under “sect-110-25

(5)” and the taxpayer has occurred the expenses which increased the asset value therefore,

Sophia should include the expenditure under her cost base (Barkoczy, 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4LAWS OF TAXATION

Answer B: Sale of shares

CGT provisions are applied to assets which is purchased following 20th September

and it is generally used to evaluate the value of asset. “Pre CGT” and “Post CGT” is used in

reference to asset purchased before or after the following date (Huizinga, Voget and Wagner,

2018).

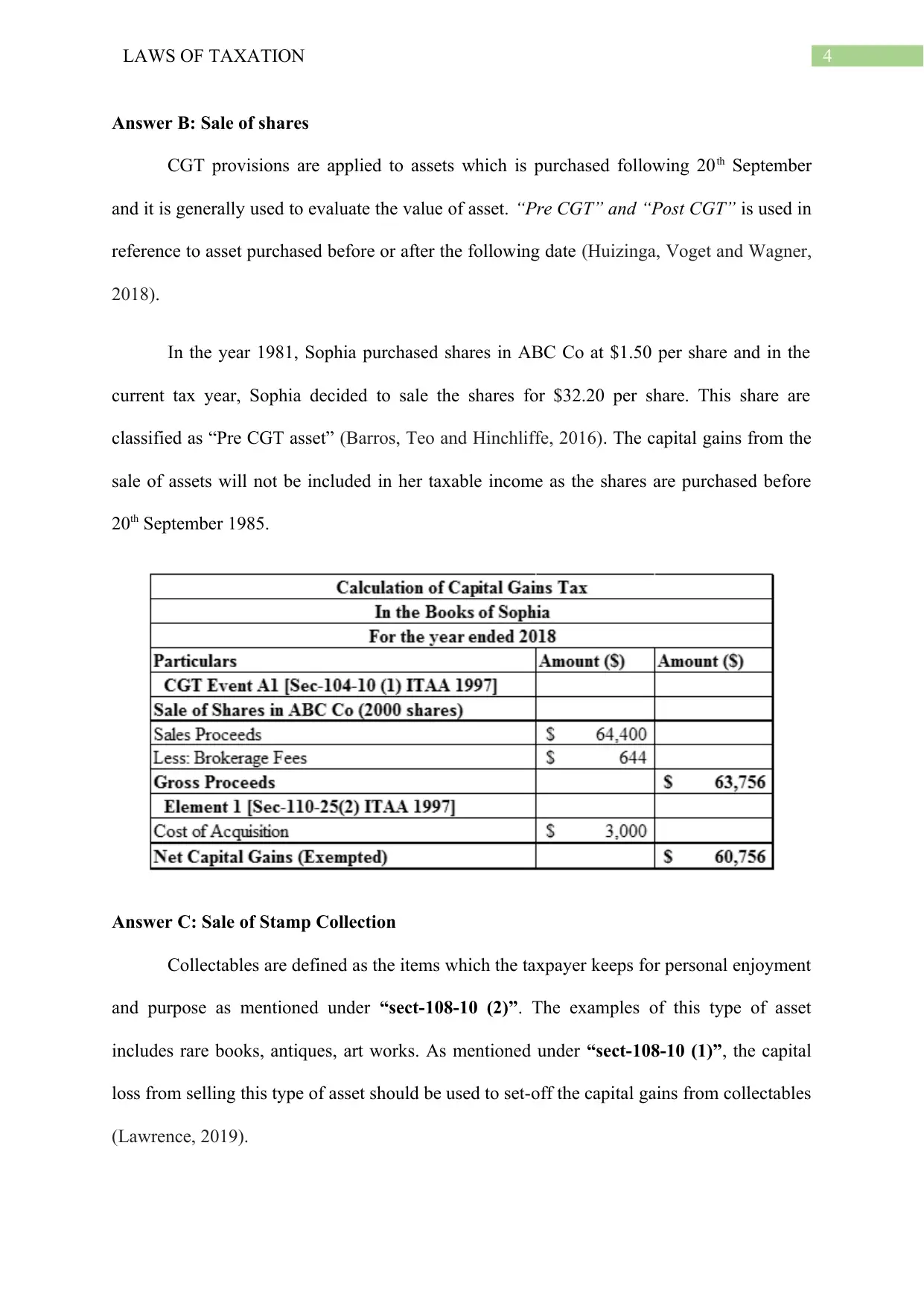

In the year 1981, Sophia purchased shares in ABC Co at $1.50 per share and in the

current tax year, Sophia decided to sale the shares for $32.20 per share. This share are

classified as “Pre CGT asset” (Barros, Teo and Hinchliffe, 2016). The capital gains from the

sale of assets will not be included in her taxable income as the shares are purchased before

20th September 1985.

Answer C: Sale of Stamp Collection

Collectables are defined as the items which the taxpayer keeps for personal enjoyment

and purpose as mentioned under “sect-108-10 (2)”. The examples of this type of asset

includes rare books, antiques, art works. As mentioned under “sect-108-10 (1)”, the capital

loss from selling this type of asset should be used to set-off the capital gains from collectables

(Lawrence, 2019).

Answer B: Sale of shares

CGT provisions are applied to assets which is purchased following 20th September

and it is generally used to evaluate the value of asset. “Pre CGT” and “Post CGT” is used in

reference to asset purchased before or after the following date (Huizinga, Voget and Wagner,

2018).

In the year 1981, Sophia purchased shares in ABC Co at $1.50 per share and in the

current tax year, Sophia decided to sale the shares for $32.20 per share. This share are

classified as “Pre CGT asset” (Barros, Teo and Hinchliffe, 2016). The capital gains from the

sale of assets will not be included in her taxable income as the shares are purchased before

20th September 1985.

Answer C: Sale of Stamp Collection

Collectables are defined as the items which the taxpayer keeps for personal enjoyment

and purpose as mentioned under “sect-108-10 (2)”. The examples of this type of asset

includes rare books, antiques, art works. As mentioned under “sect-108-10 (1)”, the capital

loss from selling this type of asset should be used to set-off the capital gains from collectables

(Lawrence, 2019).

5LAWS OF TAXATION

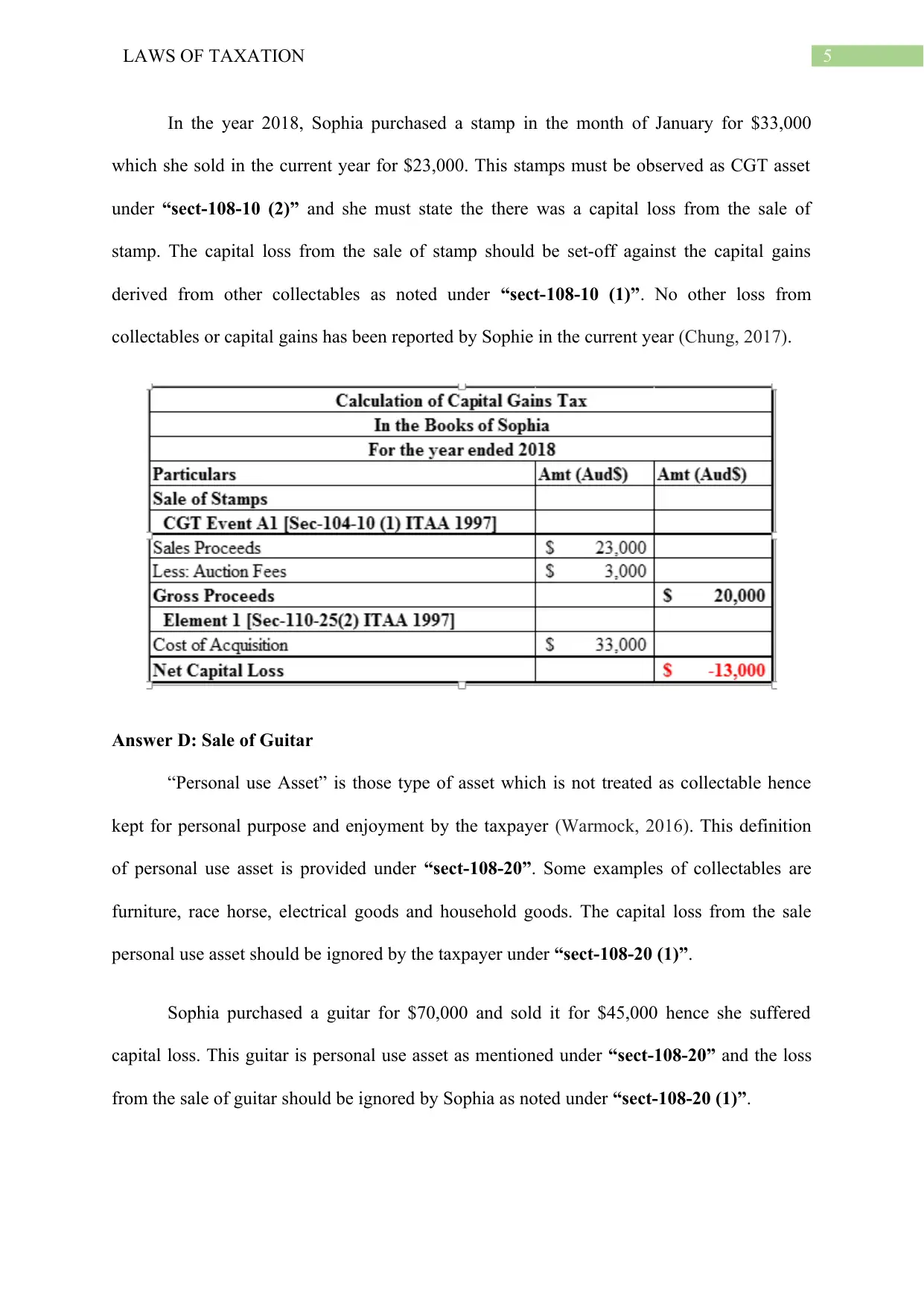

In the year 2018, Sophia purchased a stamp in the month of January for $33,000

which she sold in the current year for $23,000. This stamps must be observed as CGT asset

under “sect-108-10 (2)” and she must state the there was a capital loss from the sale of

stamp. The capital loss from the sale of stamp should be set-off against the capital gains

derived from other collectables as noted under “sect-108-10 (1)”. No other loss from

collectables or capital gains has been reported by Sophie in the current year (Chung, 2017).

Answer D: Sale of Guitar

“Personal use Asset” is those type of asset which is not treated as collectable hence

kept for personal purpose and enjoyment by the taxpayer (Warmock, 2016). This definition

of personal use asset is provided under “sect-108-20”. Some examples of collectables are

furniture, race horse, electrical goods and household goods. The capital loss from the sale

personal use asset should be ignored by the taxpayer under “sect-108-20 (1)”.

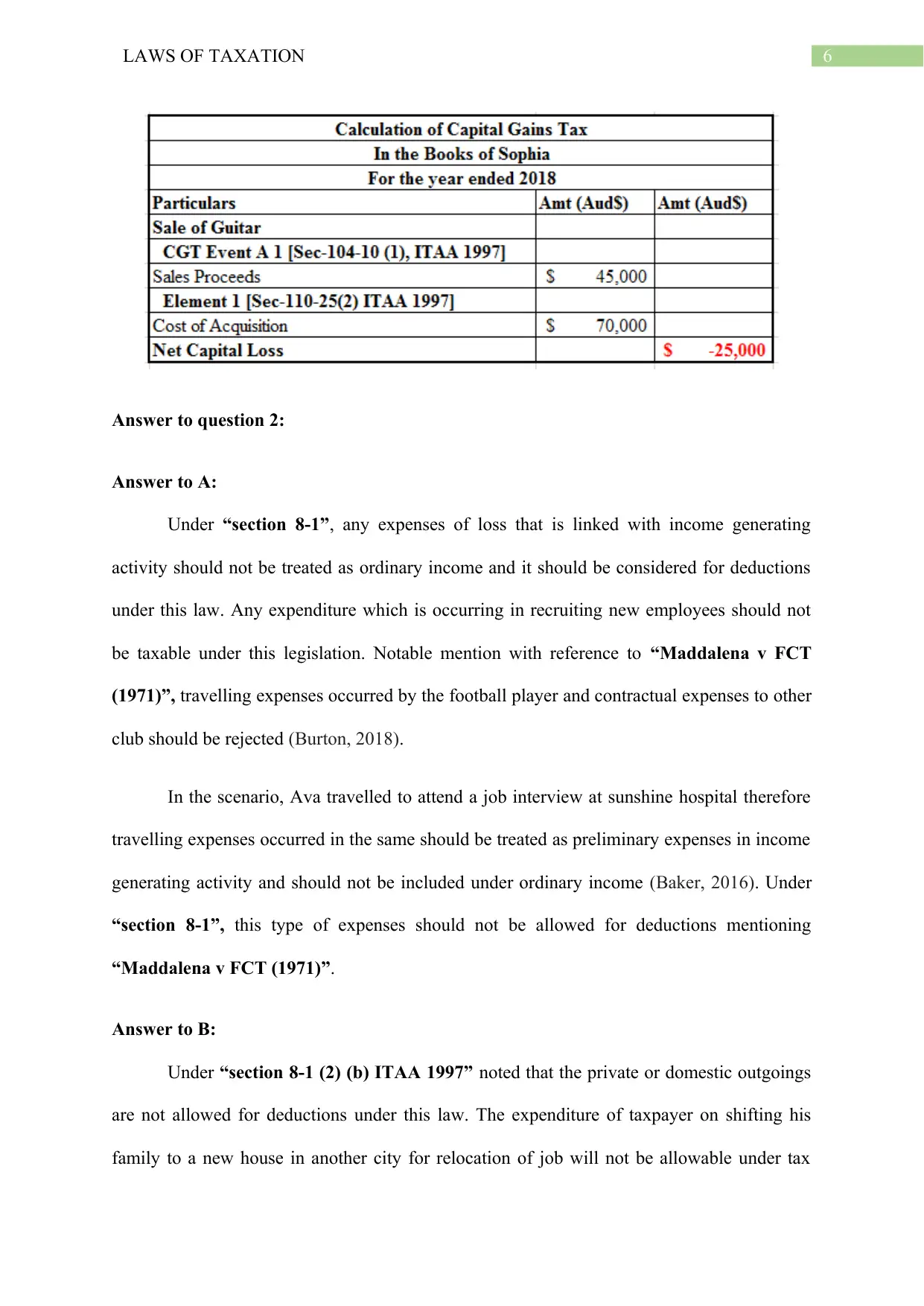

Sophia purchased a guitar for $70,000 and sold it for $45,000 hence she suffered

capital loss. This guitar is personal use asset as mentioned under “sect-108-20” and the loss

from the sale of guitar should be ignored by Sophia as noted under “sect-108-20 (1)”.

In the year 2018, Sophia purchased a stamp in the month of January for $33,000

which she sold in the current year for $23,000. This stamps must be observed as CGT asset

under “sect-108-10 (2)” and she must state the there was a capital loss from the sale of

stamp. The capital loss from the sale of stamp should be set-off against the capital gains

derived from other collectables as noted under “sect-108-10 (1)”. No other loss from

collectables or capital gains has been reported by Sophie in the current year (Chung, 2017).

Answer D: Sale of Guitar

“Personal use Asset” is those type of asset which is not treated as collectable hence

kept for personal purpose and enjoyment by the taxpayer (Warmock, 2016). This definition

of personal use asset is provided under “sect-108-20”. Some examples of collectables are

furniture, race horse, electrical goods and household goods. The capital loss from the sale

personal use asset should be ignored by the taxpayer under “sect-108-20 (1)”.

Sophia purchased a guitar for $70,000 and sold it for $45,000 hence she suffered

capital loss. This guitar is personal use asset as mentioned under “sect-108-20” and the loss

from the sale of guitar should be ignored by Sophia as noted under “sect-108-20 (1)”.

6LAWS OF TAXATION

Answer to question 2:

Answer to A:

Under “section 8-1”, any expenses of loss that is linked with income generating

activity should not be treated as ordinary income and it should be considered for deductions

under this law. Any expenditure which is occurring in recruiting new employees should not

be taxable under this legislation. Notable mention with reference to “Maddalena v FCT

(1971)”, travelling expenses occurred by the football player and contractual expenses to other

club should be rejected (Burton, 2018).

In the scenario, Ava travelled to attend a job interview at sunshine hospital therefore

travelling expenses occurred in the same should be treated as preliminary expenses in income

generating activity and should not be included under ordinary income (Baker, 2016). Under

“section 8-1”, this type of expenses should not be allowed for deductions mentioning

“Maddalena v FCT (1971)”.

Answer to B:

Under “section 8-1 (2) (b) ITAA 1997” noted that the private or domestic outgoings

are not allowed for deductions under this law. The expenditure of taxpayer on shifting his

family to a new house in another city for relocation of job will not be allowable under tax

Answer to question 2:

Answer to A:

Under “section 8-1”, any expenses of loss that is linked with income generating

activity should not be treated as ordinary income and it should be considered for deductions

under this law. Any expenditure which is occurring in recruiting new employees should not

be taxable under this legislation. Notable mention with reference to “Maddalena v FCT

(1971)”, travelling expenses occurred by the football player and contractual expenses to other

club should be rejected (Burton, 2018).

In the scenario, Ava travelled to attend a job interview at sunshine hospital therefore

travelling expenses occurred in the same should be treated as preliminary expenses in income

generating activity and should not be included under ordinary income (Baker, 2016). Under

“section 8-1”, this type of expenses should not be allowed for deductions mentioning

“Maddalena v FCT (1971)”.

Answer to B:

Under “section 8-1 (2) (b) ITAA 1997” noted that the private or domestic outgoings

are not allowed for deductions under this law. The expenditure of taxpayer on shifting his

family to a new house in another city for relocation of job will not be allowable under tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7LAWS OF TAXATION

deduction as the amounts are domestic as mentioned by the federal court in “Fullerton v

FCT (1991)”.

Ava reported to shift her house to Darwin which cost $1,800. Mentioning the

judgement of “fullerton v FCT (1991)” noted that this relocation expenses is private

arrangement and is fails to meet the positive deduction under “section 8-1 (2) (b) ITAA

1997” and it should not be permitted for deduction under this section (Brownlee, 2016).

Answer to C:

Taxpayer’s expenses for ordinary objects should not be allowed for general tax

deductions with provision under “section 8-1”. However, the taxpayer are allowed for certain

exceptions for compulsory clothing which is a specific and protective uniform. The taxpayer

are allowed for deduction relating to cost of shoes and expenses on stockings as it is

necessary that these costs should be levied by the taxpayer while working her job of flight

attendant (Woellner et.al, 2016).

Ava also paid $200 for doctor’s uniform and the expenses that is occurred towards

this amounts to specific clothing of AVA. “FCT v Mansfield (1995)” mentioned that these

expenses are allowable for tax deduction under “section 8-1 ITAA 1997”.

Answer to D:

In the current year, Ava has also occurred child care expenses for her two year old

daughter which amounts to $18,200. “Lodge v FCT (1972)” described that the claim of the

taxpayer for assessable earnings are expenses related to childcare. This should not be

included in the income generating activities of the taxpayer and therefore the outgoings will

not be treated as assessable income and there will not be any deduction under “section 8-1

ITAA 1997”.

deduction as the amounts are domestic as mentioned by the federal court in “Fullerton v

FCT (1991)”.

Ava reported to shift her house to Darwin which cost $1,800. Mentioning the

judgement of “fullerton v FCT (1991)” noted that this relocation expenses is private

arrangement and is fails to meet the positive deduction under “section 8-1 (2) (b) ITAA

1997” and it should not be permitted for deduction under this section (Brownlee, 2016).

Answer to C:

Taxpayer’s expenses for ordinary objects should not be allowed for general tax

deductions with provision under “section 8-1”. However, the taxpayer are allowed for certain

exceptions for compulsory clothing which is a specific and protective uniform. The taxpayer

are allowed for deduction relating to cost of shoes and expenses on stockings as it is

necessary that these costs should be levied by the taxpayer while working her job of flight

attendant (Woellner et.al, 2016).

Ava also paid $200 for doctor’s uniform and the expenses that is occurred towards

this amounts to specific clothing of AVA. “FCT v Mansfield (1995)” mentioned that these

expenses are allowable for tax deduction under “section 8-1 ITAA 1997”.

Answer to D:

In the current year, Ava has also occurred child care expenses for her two year old

daughter which amounts to $18,200. “Lodge v FCT (1972)” described that the claim of the

taxpayer for assessable earnings are expenses related to childcare. This should not be

included in the income generating activities of the taxpayer and therefore the outgoings will

not be treated as assessable income and there will not be any deduction under “section 8-1

ITAA 1997”.

8LAWS OF TAXATION

Answer to E:

Any expenses associated with phone rental or phone call should be allowable under

deduction if the taxpayer has evidence of the call or the call was made to the employer or

clients during the work. “Ronpibon Tin No Liability v FCT(1949)” mentioned that these

expenses related to work purpose is allowable for tax deduction should give positive limbs

noted under “section 8-1 ITAA 1997”

Ava also incurred expenses on phone call while she was away from her hospital in her

work hour to look after the patient. The cost of the phone call costs $200. As mentioned by

“Ronpibon Tin No Liability v FCT (1949)”, the expenses of phone call should be

permissible for deduction under “section 8-1 ITAA 1997”.

Answer to F:

There are certain situation where the taxpayer occurs with expenses that are related to

human being such as food, clothing or housing. This type of expenses are not allowable under

“section 8-1 ITAA 1997”. “FCT v Cooper (1991)” judged that the outgoing that is occurred

by rugby player on having food is non-deductible under positive limbs as mention under

“section 8-1 ITAA 1997”.

Ava also reported that she consumed food while working in the evening shift. Under

“section 8-1 ITAA 1997”, the food expenses is not deductible under this section as it fails to

meet the criteria of deduction. This section also stated that these expenses are outgoings and

it will not be non-deductible.

Answer to G:

Under “section 26-5 ITAA 1997” noted that fines which are imposed by the

government of Australia is non-deductible. Ava also reported a speeding fine worth $207

Answer to E:

Any expenses associated with phone rental or phone call should be allowable under

deduction if the taxpayer has evidence of the call or the call was made to the employer or

clients during the work. “Ronpibon Tin No Liability v FCT(1949)” mentioned that these

expenses related to work purpose is allowable for tax deduction should give positive limbs

noted under “section 8-1 ITAA 1997”

Ava also incurred expenses on phone call while she was away from her hospital in her

work hour to look after the patient. The cost of the phone call costs $200. As mentioned by

“Ronpibon Tin No Liability v FCT (1949)”, the expenses of phone call should be

permissible for deduction under “section 8-1 ITAA 1997”.

Answer to F:

There are certain situation where the taxpayer occurs with expenses that are related to

human being such as food, clothing or housing. This type of expenses are not allowable under

“section 8-1 ITAA 1997”. “FCT v Cooper (1991)” judged that the outgoing that is occurred

by rugby player on having food is non-deductible under positive limbs as mention under

“section 8-1 ITAA 1997”.

Ava also reported that she consumed food while working in the evening shift. Under

“section 8-1 ITAA 1997”, the food expenses is not deductible under this section as it fails to

meet the criteria of deduction. This section also stated that these expenses are outgoings and

it will not be non-deductible.

Answer to G:

Under “section 26-5 ITAA 1997” noted that fines which are imposed by the

government of Australia is non-deductible. Ava also reported a speeding fine worth $207

9LAWS OF TAXATION

while she was going for work. “Section 26-5 ITAA 1997” describes that the fines are non-

deductible to Ava.

Answer to H:

Outgoings are not allowable for deduction under “section 8-1 ITAA 1997” as it

occurred between home and place of work of taxpayer. “FCT v Lunney (1958)” mentioned

that the outgoings associated with work and travel of the taxpayer will not be permissible for

deduction as it is not generating any earnings and the outgoings are private in type (Zhu,

2019).

In the current scenario, Ava occurred travel outgoing for $330 to and from work.

Notable mention of “FCT v Lunney(1958)” described that the outgoing relating to work is

non-deductible as the deduction is private and Ava will not be provided with any taxable

deduction under “section 8-1 ITAA 1997”.

while she was going for work. “Section 26-5 ITAA 1997” describes that the fines are non-

deductible to Ava.

Answer to H:

Outgoings are not allowable for deduction under “section 8-1 ITAA 1997” as it

occurred between home and place of work of taxpayer. “FCT v Lunney (1958)” mentioned

that the outgoings associated with work and travel of the taxpayer will not be permissible for

deduction as it is not generating any earnings and the outgoings are private in type (Zhu,

2019).

In the current scenario, Ava occurred travel outgoing for $330 to and from work.

Notable mention of “FCT v Lunney(1958)” described that the outgoing relating to work is

non-deductible as the deduction is private and Ava will not be provided with any taxable

deduction under “section 8-1 ITAA 1997”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10LAWS OF TAXATION

References

Baker, D.A., 2016. The Great Tax Policy Debate: For Retention or Reform of the Preferential

Taxation of Capital Income.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barros, C., Teo, E.J. and Hinchliffe, S., 2016. Clash of the deeming provisions: Pre-CGT

concessions, tax consolidation and policy in the federal court. Austl. Tax F., 31, p.509.

Brownlee, W.E., 2016. Federal Taxation in America. Cambridge University Press.

Burton, M., 2018. Interpreting the Australian Income Tax Definition of Ordinary Income:

Ritual Incantation Or Analysis, When Examined through the Lens of Early Twentieth

Century Linguistic Philosophy. eJTR, 16, p.2.

Chung, E., 2017. The absolute beginner's guide to capital gains tax. REIQ Journal, (May

2017), p.35.

Collier, P., Glaeser, E., Venables, T., Blake, M. and Manwaring, P., 2018. Land and property

taxes for municipal finance.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Lawrence, S., 2019. Separate SMSFs for collectables. Taxation in Australia, 53(9), p.480.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

References

Baker, D.A., 2016. The Great Tax Policy Debate: For Retention or Reform of the Preferential

Taxation of Capital Income.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barros, C., Teo, E.J. and Hinchliffe, S., 2016. Clash of the deeming provisions: Pre-CGT

concessions, tax consolidation and policy in the federal court. Austl. Tax F., 31, p.509.

Brownlee, W.E., 2016. Federal Taxation in America. Cambridge University Press.

Burton, M., 2018. Interpreting the Australian Income Tax Definition of Ordinary Income:

Ritual Incantation Or Analysis, When Examined through the Lens of Early Twentieth

Century Linguistic Philosophy. eJTR, 16, p.2.

Chung, E., 2017. The absolute beginner's guide to capital gains tax. REIQ Journal, (May

2017), p.35.

Collier, P., Glaeser, E., Venables, T., Blake, M. and Manwaring, P., 2018. Land and property

taxes for municipal finance.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Lawrence, S., 2019. Separate SMSFs for collectables. Taxation in Australia, 53(9), p.480.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

11LAWS OF TAXATION

Warnock, R., 2016. MNAV test: Asset and liability issues. Taxation in Australia, 51(3),

p.133.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Zhu, L., 2019. Thoughts on the Deduction of Individual Income Tax Expenses. DEStech

Transactions on Social Science, Education and Human Science, (esem).

Warnock, R., 2016. MNAV test: Asset and liability issues. Taxation in Australia, 51(3),

p.133.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Zhu, L., 2019. Thoughts on the Deduction of Individual Income Tax Expenses. DEStech

Transactions on Social Science, Education and Human Science, (esem).

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.