Case Study on Investment Appraisal and Business Performance Analysis

VerifiedAdded on 2023/01/11

|10

|2153

|30

Case Study

AI Summary

This case study analyzes investment appraisal techniques, including Accounting Rate of Return (ARR), Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period, to evaluate the viability of a project. The analysis reveals that the ARR is 40%, the NPV is negative (-1998.4), and the IRR is 10%. The payback period is calculated at 4 years and 1 month. Furthermore, the study examines the performance of a business using various financial ratios, such as the current ratio, quick ratio, debt-equity ratio, interest coverage ratio, net profit margin, stock turnover ratio, debtors turnover ratio, and creditors turnover ratio, providing insights into the company's liquidity, solvency, and efficiency. Finally, the case study explores the importance of Key Performance Indicators (KPIs), both internal and external, in tracking and evaluating business performance, and discusses the role of pricing in influencing profitability and market share.

Case study

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

Case study..................................................................................................................................3

TASK 1......................................................................................................................................3

Computing investment appraisal............................................................................................3

TASK 2......................................................................................................................................6

Analysing performance of business.......................................................................................6

TASK 3......................................................................................................................................8

Analysing & comparing internal and the external performance measures and pricing role

on performance of business....................................................................................................8

REFERENCES.........................................................................................................................10

Case study..................................................................................................................................3

TASK 1......................................................................................................................................3

Computing investment appraisal............................................................................................3

TASK 2......................................................................................................................................6

Analysing performance of business.......................................................................................6

TASK 3......................................................................................................................................8

Analysing & comparing internal and the external performance measures and pricing role

on performance of business....................................................................................................8

REFERENCES.........................................................................................................................10

Case study

TASK 1

Computing investment appraisal

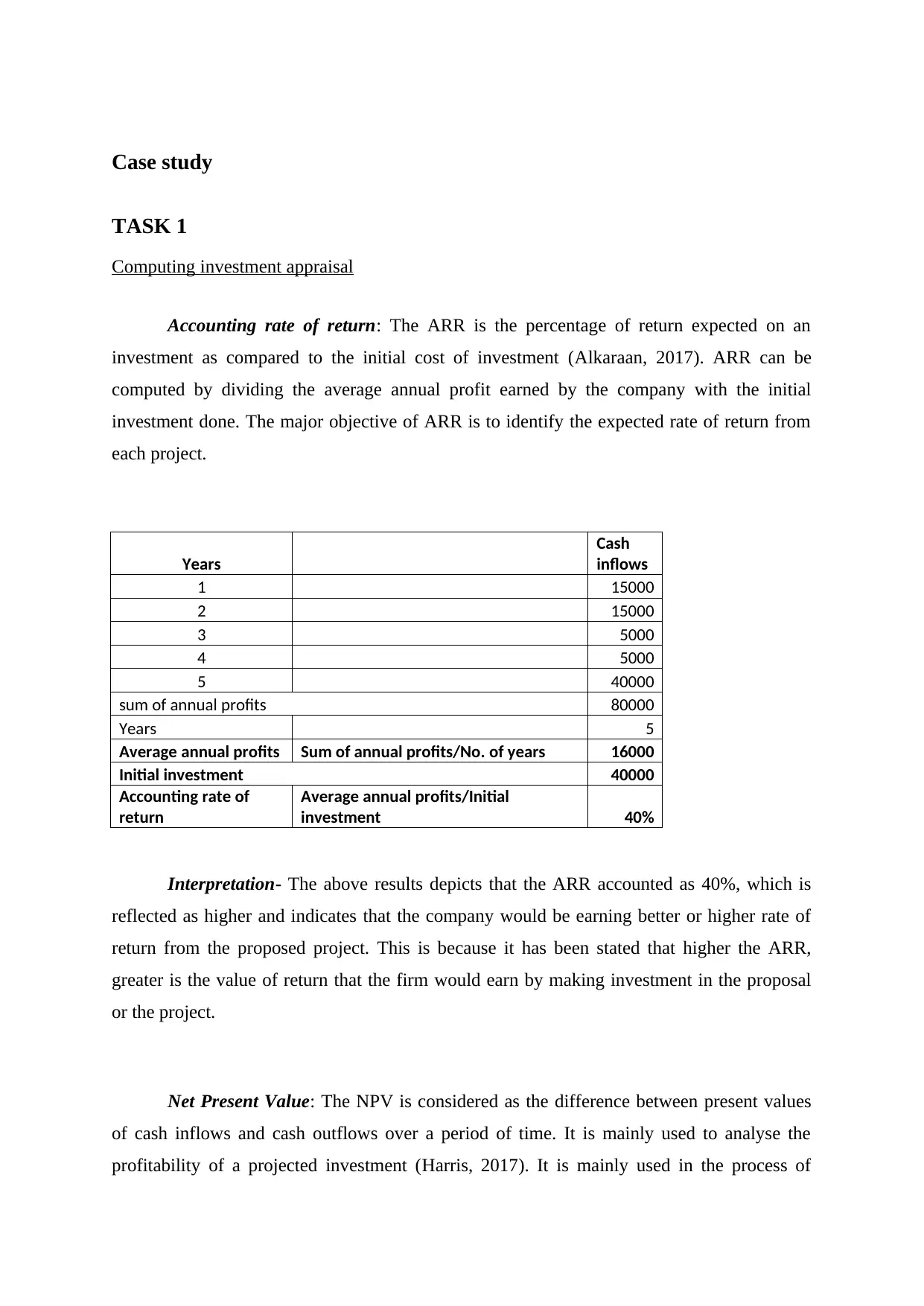

Accounting rate of return: The ARR is the percentage of return expected on an

investment as compared to the initial cost of investment (Alkaraan, 2017). ARR can be

computed by dividing the average annual profit earned by the company with the initial

investment done. The major objective of ARR is to identify the expected rate of return from

each project.

Years

Cash

inflows

1 15000

2 15000

3 5000

4 5000

5 40000

sum of annual profits 80000

Years 5

Average annual profits Sum of annual profits/No. of years 16000

Initial investment 40000

Accounting rate of

return

Average annual profits/Initial

investment 40%

Interpretation- The above results depicts that the ARR accounted as 40%, which is

reflected as higher and indicates that the company would be earning better or higher rate of

return from the proposed project. This is because it has been stated that higher the ARR,

greater is the value of return that the firm would earn by making investment in the proposal

or the project.

Net Present Value: The NPV is considered as the difference between present values

of cash inflows and cash outflows over a period of time. It is mainly used to analyse the

profitability of a projected investment (Harris, 2017). It is mainly used in the process of

TASK 1

Computing investment appraisal

Accounting rate of return: The ARR is the percentage of return expected on an

investment as compared to the initial cost of investment (Alkaraan, 2017). ARR can be

computed by dividing the average annual profit earned by the company with the initial

investment done. The major objective of ARR is to identify the expected rate of return from

each project.

Years

Cash

inflows

1 15000

2 15000

3 5000

4 5000

5 40000

sum of annual profits 80000

Years 5

Average annual profits Sum of annual profits/No. of years 16000

Initial investment 40000

Accounting rate of

return

Average annual profits/Initial

investment 40%

Interpretation- The above results depicts that the ARR accounted as 40%, which is

reflected as higher and indicates that the company would be earning better or higher rate of

return from the proposed project. This is because it has been stated that higher the ARR,

greater is the value of return that the firm would earn by making investment in the proposal

or the project.

Net Present Value: The NPV is considered as the difference between present values

of cash inflows and cash outflows over a period of time. It is mainly used to analyse the

profitability of a projected investment (Harris, 2017). It is mainly used in the process of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

capital budgeting and investment planning. If the NPV is positive, it means that the

investment will give return whereas if the NPV is negative, it is not worthwhile to invest.

Years

Net

cash

flow

Discounte

d rate

Discounte

d cash

flows

1 1500 0.87 1304.3

2 2750 0.76 2079.4

3 4000 0.66 2630.1

4 5700 0.57 3259.0

5 7500 0.50 3728.8

Sum total of discounted cash

flows 13001.6

less: Initial investment 15000

NPV -1998.4

Interpretation- The above analysis represents that further investment for buying the

new machine tend to generate loss for the firm as the value of NPV resulted as -1998.4. It has

been analyzed that positive NPV reflects that the project would be profitable; however,

negative net present value means as making investment in such project would incur losses for

the company.

Internal rate of return: The IRR concept is used in capital budgeting to calculate the

profitability aspect of potential investments. IRR is a discounted rate which makes the NPV

of all cash flows equal to zero (Jibril and Jagun, 2018). Higher the IRR, greater the amount

through which it exceeds cost of capital and more the net cash flows in the company. It is

preferred to adopt a large project with low IRR because it generates more cash flows for the

company.

Years

Net

cash

flow

0 -15000

1 1500

2 2750

3 4000

4 5700

5 7500

IRR 10%

investment will give return whereas if the NPV is negative, it is not worthwhile to invest.

Years

Net

cash

flow

Discounte

d rate

Discounte

d cash

flows

1 1500 0.87 1304.3

2 2750 0.76 2079.4

3 4000 0.66 2630.1

4 5700 0.57 3259.0

5 7500 0.50 3728.8

Sum total of discounted cash

flows 13001.6

less: Initial investment 15000

NPV -1998.4

Interpretation- The above analysis represents that further investment for buying the

new machine tend to generate loss for the firm as the value of NPV resulted as -1998.4. It has

been analyzed that positive NPV reflects that the project would be profitable; however,

negative net present value means as making investment in such project would incur losses for

the company.

Internal rate of return: The IRR concept is used in capital budgeting to calculate the

profitability aspect of potential investments. IRR is a discounted rate which makes the NPV

of all cash flows equal to zero (Jibril and Jagun, 2018). Higher the IRR, greater the amount

through which it exceeds cost of capital and more the net cash flows in the company. It is

preferred to adopt a large project with low IRR because it generates more cash flows for the

company.

Years

Net

cash

flow

0 -15000

1 1500

2 2750

3 4000

4 5700

5 7500

IRR 10%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

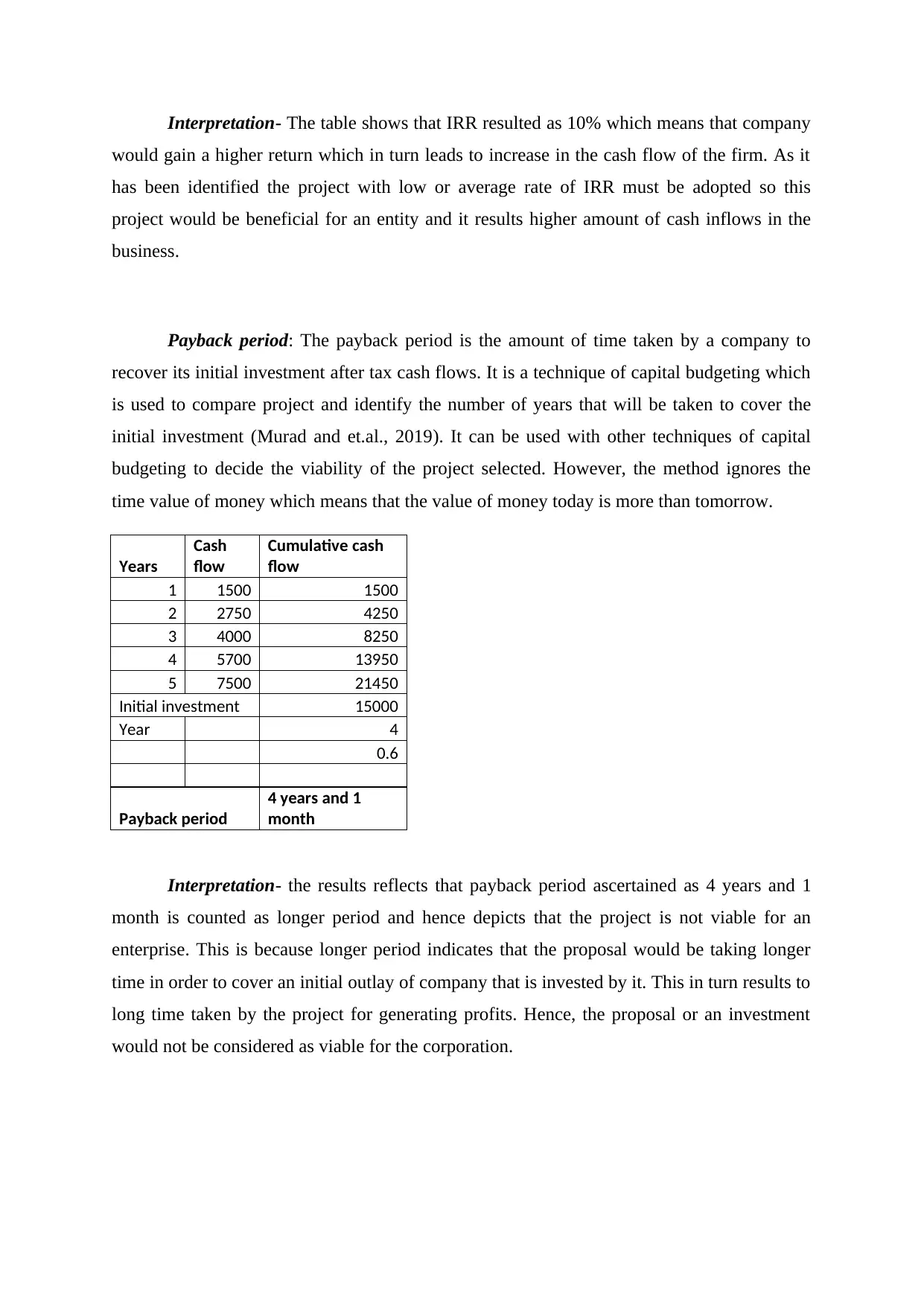

Interpretation- The table shows that IRR resulted as 10% which means that company

would gain a higher return which in turn leads to increase in the cash flow of the firm. As it

has been identified the project with low or average rate of IRR must be adopted so this

project would be beneficial for an entity and it results higher amount of cash inflows in the

business.

Payback period: The payback period is the amount of time taken by a company to

recover its initial investment after tax cash flows. It is a technique of capital budgeting which

is used to compare project and identify the number of years that will be taken to cover the

initial investment (Murad and et.al., 2019). It can be used with other techniques of capital

budgeting to decide the viability of the project selected. However, the method ignores the

time value of money which means that the value of money today is more than tomorrow.

Years

Cash

flow

Cumulative cash

flow

1 1500 1500

2 2750 4250

3 4000 8250

4 5700 13950

5 7500 21450

Initial investment 15000

Year 4

0.6

Payback period

4 years and 1

month

Interpretation- the results reflects that payback period ascertained as 4 years and 1

month is counted as longer period and hence depicts that the project is not viable for an

enterprise. This is because longer period indicates that the proposal would be taking longer

time in order to cover an initial outlay of company that is invested by it. This in turn results to

long time taken by the project for generating profits. Hence, the proposal or an investment

would not be considered as viable for the corporation.

would gain a higher return which in turn leads to increase in the cash flow of the firm. As it

has been identified the project with low or average rate of IRR must be adopted so this

project would be beneficial for an entity and it results higher amount of cash inflows in the

business.

Payback period: The payback period is the amount of time taken by a company to

recover its initial investment after tax cash flows. It is a technique of capital budgeting which

is used to compare project and identify the number of years that will be taken to cover the

initial investment (Murad and et.al., 2019). It can be used with other techniques of capital

budgeting to decide the viability of the project selected. However, the method ignores the

time value of money which means that the value of money today is more than tomorrow.

Years

Cash

flow

Cumulative cash

flow

1 1500 1500

2 2750 4250

3 4000 8250

4 5700 13950

5 7500 21450

Initial investment 15000

Year 4

0.6

Payback period

4 years and 1

month

Interpretation- the results reflects that payback period ascertained as 4 years and 1

month is counted as longer period and hence depicts that the project is not viable for an

enterprise. This is because longer period indicates that the proposal would be taking longer

time in order to cover an initial outlay of company that is invested by it. This in turn results to

long time taken by the project for generating profits. Hence, the proposal or an investment

would not be considered as viable for the corporation.

TASK 2

Analysing performance of business

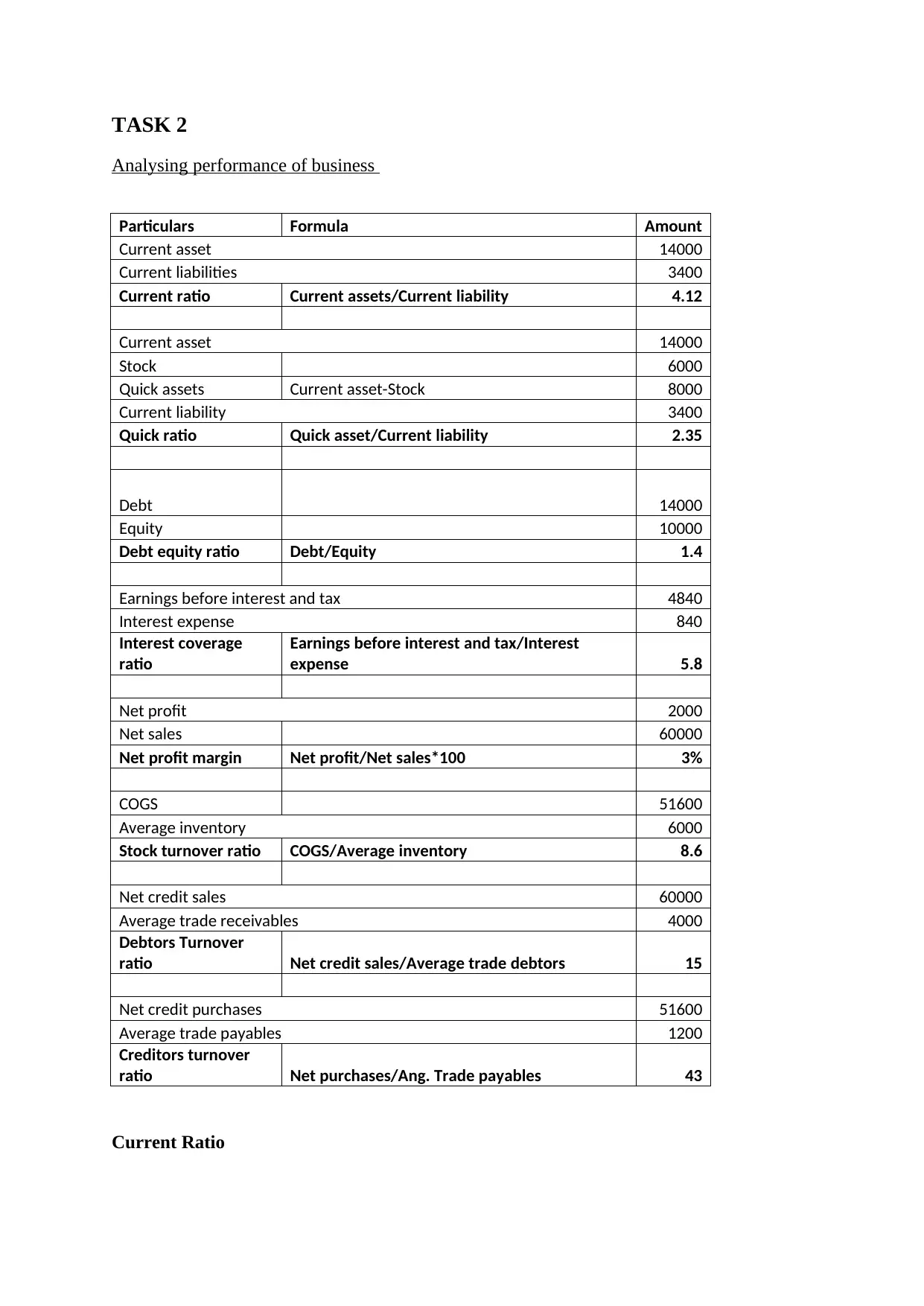

Particulars Formula Amount

Current asset 14000

Current liabilities 3400

Current ratio Current assets/Current liability 4.12

Current asset 14000

Stock 6000

Quick assets Current asset-Stock 8000

Current liability 3400

Quick ratio Quick asset/Current liability 2.35

Debt 14000

Equity 10000

Debt equity ratio Debt/Equity 1.4

Earnings before interest and tax 4840

Interest expense 840

Interest coverage

ratio

Earnings before interest and tax/Interest

expense 5.8

Net profit 2000

Net sales 60000

Net profit margin Net profit/Net sales*100 3%

COGS 51600

Average inventory 6000

Stock turnover ratio COGS/Average inventory 8.6

Net credit sales 60000

Average trade receivables 4000

Debtors Turnover

ratio Net credit sales/Average trade debtors 15

Net credit purchases 51600

Average trade payables 1200

Creditors turnover

ratio Net purchases/Ang. Trade payables 43

Current Ratio

Analysing performance of business

Particulars Formula Amount

Current asset 14000

Current liabilities 3400

Current ratio Current assets/Current liability 4.12

Current asset 14000

Stock 6000

Quick assets Current asset-Stock 8000

Current liability 3400

Quick ratio Quick asset/Current liability 2.35

Debt 14000

Equity 10000

Debt equity ratio Debt/Equity 1.4

Earnings before interest and tax 4840

Interest expense 840

Interest coverage

ratio

Earnings before interest and tax/Interest

expense 5.8

Net profit 2000

Net sales 60000

Net profit margin Net profit/Net sales*100 3%

COGS 51600

Average inventory 6000

Stock turnover ratio COGS/Average inventory 8.6

Net credit sales 60000

Average trade receivables 4000

Debtors Turnover

ratio Net credit sales/Average trade debtors 15

Net credit purchases 51600

Average trade payables 1200

Creditors turnover

ratio Net purchases/Ang. Trade payables 43

Current Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: From the above study it can be interpreted that the current ratio is

4.12:1 which is much higher than 2:1 and it indicates that the company has enough liquidity

to pay off its current liabilities by using the current assets. However, in this situation the

current ratio of company is too high and it means that it is not using its current assets

efficiently which may create problems relation to the capital management in the near future.

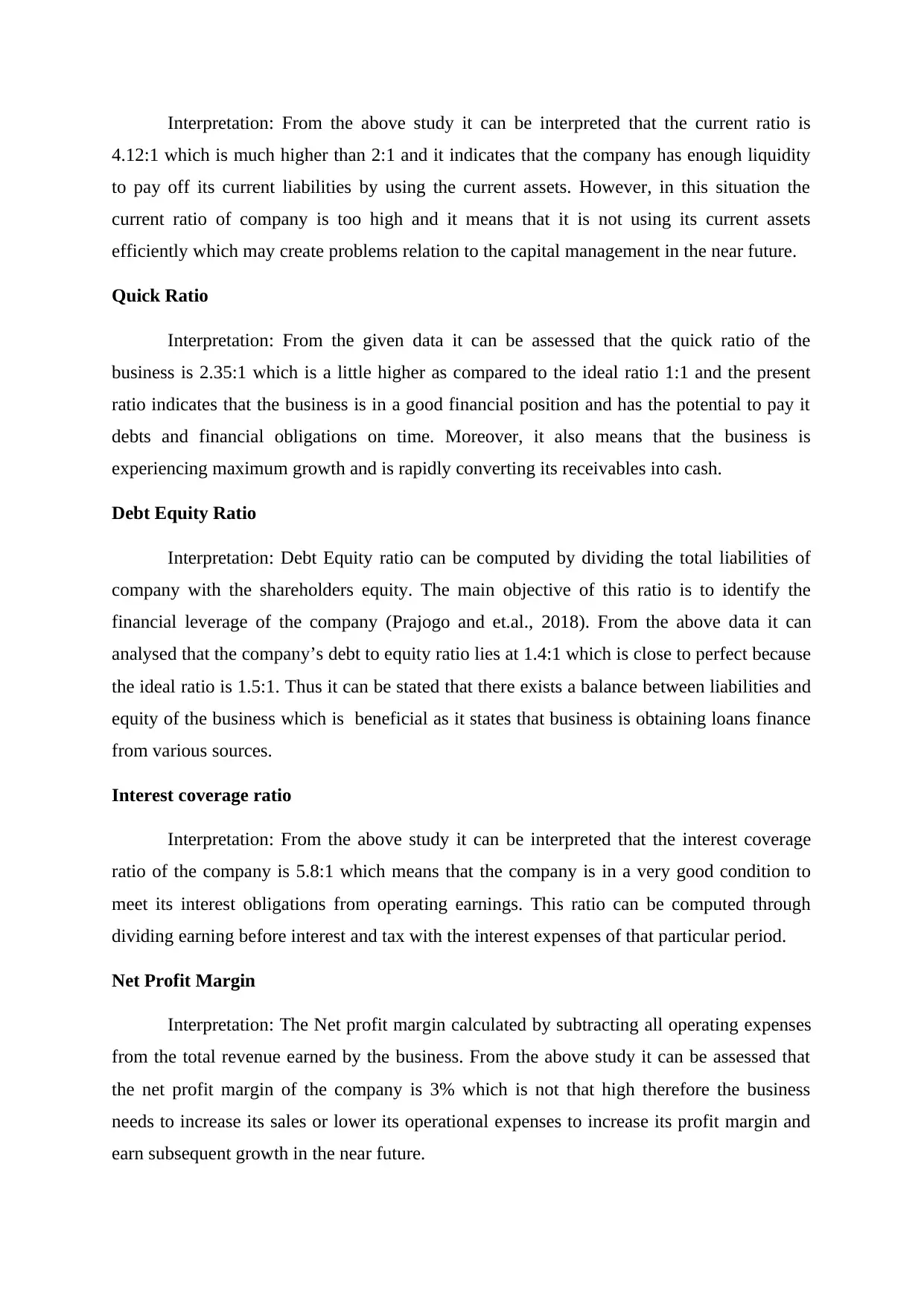

Quick Ratio

Interpretation: From the given data it can be assessed that the quick ratio of the

business is 2.35:1 which is a little higher as compared to the ideal ratio 1:1 and the present

ratio indicates that the business is in a good financial position and has the potential to pay it

debts and financial obligations on time. Moreover, it also means that the business is

experiencing maximum growth and is rapidly converting its receivables into cash.

Debt Equity Ratio

Interpretation: Debt Equity ratio can be computed by dividing the total liabilities of

company with the shareholders equity. The main objective of this ratio is to identify the

financial leverage of the company (Prajogo and et.al., 2018). From the above data it can

analysed that the company’s debt to equity ratio lies at 1.4:1 which is close to perfect because

the ideal ratio is 1.5:1. Thus it can be stated that there exists a balance between liabilities and

equity of the business which is beneficial as it states that business is obtaining loans finance

from various sources.

Interest coverage ratio

Interpretation: From the above study it can be interpreted that the interest coverage

ratio of the company is 5.8:1 which means that the company is in a very good condition to

meet its interest obligations from operating earnings. This ratio can be computed through

dividing earning before interest and tax with the interest expenses of that particular period.

Net Profit Margin

Interpretation: The Net profit margin calculated by subtracting all operating expenses

from the total revenue earned by the business. From the above study it can be assessed that

the net profit margin of the company is 3% which is not that high therefore the business

needs to increase its sales or lower its operational expenses to increase its profit margin and

earn subsequent growth in the near future.

4.12:1 which is much higher than 2:1 and it indicates that the company has enough liquidity

to pay off its current liabilities by using the current assets. However, in this situation the

current ratio of company is too high and it means that it is not using its current assets

efficiently which may create problems relation to the capital management in the near future.

Quick Ratio

Interpretation: From the given data it can be assessed that the quick ratio of the

business is 2.35:1 which is a little higher as compared to the ideal ratio 1:1 and the present

ratio indicates that the business is in a good financial position and has the potential to pay it

debts and financial obligations on time. Moreover, it also means that the business is

experiencing maximum growth and is rapidly converting its receivables into cash.

Debt Equity Ratio

Interpretation: Debt Equity ratio can be computed by dividing the total liabilities of

company with the shareholders equity. The main objective of this ratio is to identify the

financial leverage of the company (Prajogo and et.al., 2018). From the above data it can

analysed that the company’s debt to equity ratio lies at 1.4:1 which is close to perfect because

the ideal ratio is 1.5:1. Thus it can be stated that there exists a balance between liabilities and

equity of the business which is beneficial as it states that business is obtaining loans finance

from various sources.

Interest coverage ratio

Interpretation: From the above study it can be interpreted that the interest coverage

ratio of the company is 5.8:1 which means that the company is in a very good condition to

meet its interest obligations from operating earnings. This ratio can be computed through

dividing earning before interest and tax with the interest expenses of that particular period.

Net Profit Margin

Interpretation: The Net profit margin calculated by subtracting all operating expenses

from the total revenue earned by the business. From the above study it can be assessed that

the net profit margin of the company is 3% which is not that high therefore the business

needs to increase its sales or lower its operational expenses to increase its profit margin and

earn subsequent growth in the near future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

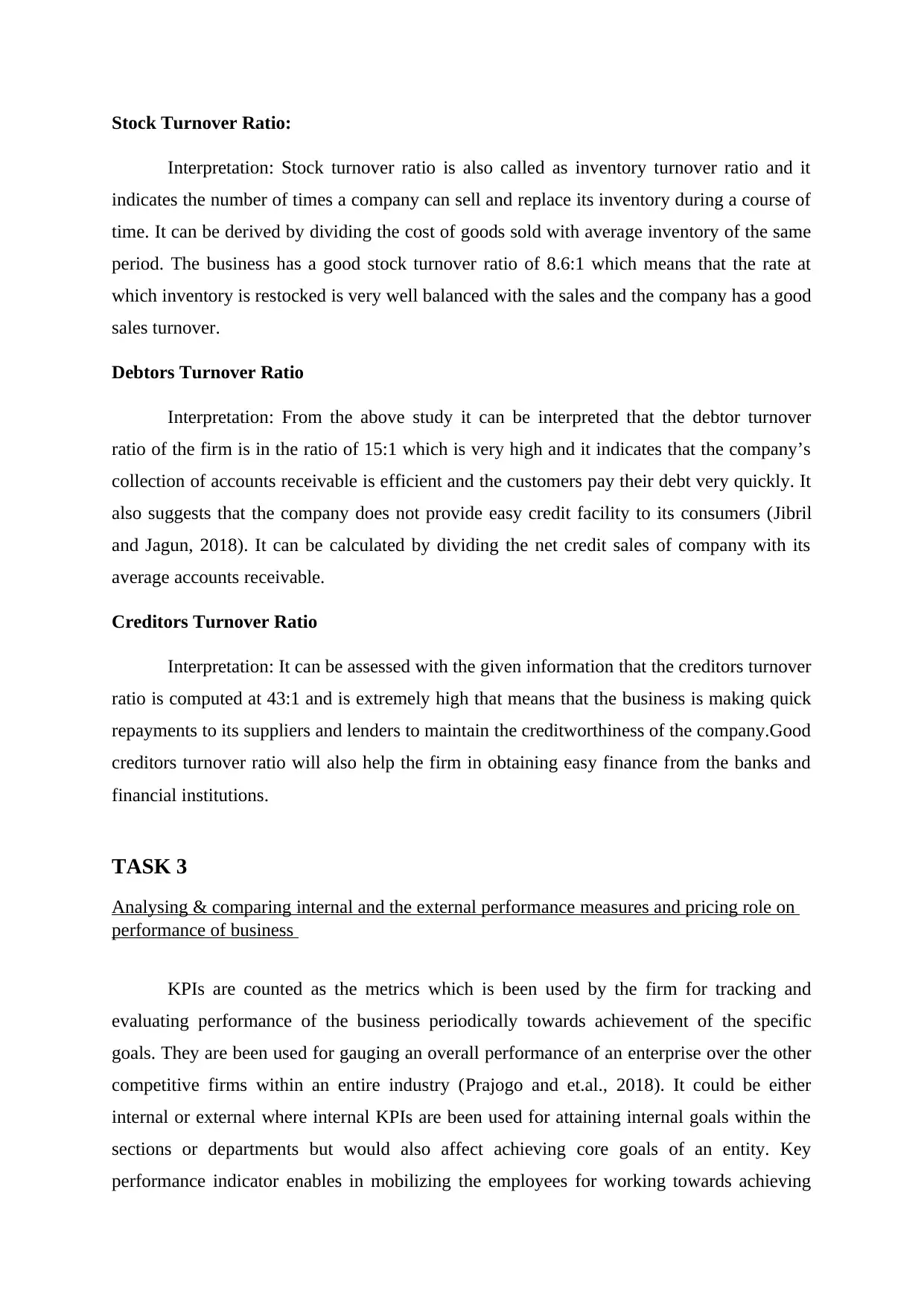

Stock Turnover Ratio:

Interpretation: Stock turnover ratio is also called as inventory turnover ratio and it

indicates the number of times a company can sell and replace its inventory during a course of

time. It can be derived by dividing the cost of goods sold with average inventory of the same

period. The business has a good stock turnover ratio of 8.6:1 which means that the rate at

which inventory is restocked is very well balanced with the sales and the company has a good

sales turnover.

Debtors Turnover Ratio

Interpretation: From the above study it can be interpreted that the debtor turnover

ratio of the firm is in the ratio of 15:1 which is very high and it indicates that the company’s

collection of accounts receivable is efficient and the customers pay their debt very quickly. It

also suggests that the company does not provide easy credit facility to its consumers (Jibril

and Jagun, 2018). It can be calculated by dividing the net credit sales of company with its

average accounts receivable.

Creditors Turnover Ratio

Interpretation: It can be assessed with the given information that the creditors turnover

ratio is computed at 43:1 and is extremely high that means that the business is making quick

repayments to its suppliers and lenders to maintain the creditworthiness of the company.Good

creditors turnover ratio will also help the firm in obtaining easy finance from the banks and

financial institutions.

TASK 3

Analysing & comparing internal and the external performance measures and pricing role on

performance of business

KPIs are counted as the metrics which is been used by the firm for tracking and

evaluating performance of the business periodically towards achievement of the specific

goals. They are been used for gauging an overall performance of an enterprise over the other

competitive firms within an entire industry (Prajogo and et.al., 2018). It could be either

internal or external where internal KPIs are been used for attaining internal goals within the

sections or departments but would also affect achieving core goals of an entity. Key

performance indicator enables in mobilizing the employees for working towards achieving

Interpretation: Stock turnover ratio is also called as inventory turnover ratio and it

indicates the number of times a company can sell and replace its inventory during a course of

time. It can be derived by dividing the cost of goods sold with average inventory of the same

period. The business has a good stock turnover ratio of 8.6:1 which means that the rate at

which inventory is restocked is very well balanced with the sales and the company has a good

sales turnover.

Debtors Turnover Ratio

Interpretation: From the above study it can be interpreted that the debtor turnover

ratio of the firm is in the ratio of 15:1 which is very high and it indicates that the company’s

collection of accounts receivable is efficient and the customers pay their debt very quickly. It

also suggests that the company does not provide easy credit facility to its consumers (Jibril

and Jagun, 2018). It can be calculated by dividing the net credit sales of company with its

average accounts receivable.

Creditors Turnover Ratio

Interpretation: It can be assessed with the given information that the creditors turnover

ratio is computed at 43:1 and is extremely high that means that the business is making quick

repayments to its suppliers and lenders to maintain the creditworthiness of the company.Good

creditors turnover ratio will also help the firm in obtaining easy finance from the banks and

financial institutions.

TASK 3

Analysing & comparing internal and the external performance measures and pricing role on

performance of business

KPIs are counted as the metrics which is been used by the firm for tracking and

evaluating performance of the business periodically towards achievement of the specific

goals. They are been used for gauging an overall performance of an enterprise over the other

competitive firms within an entire industry (Prajogo and et.al., 2018). It could be either

internal or external where internal KPIs are been used for attaining internal goals within the

sections or departments but would also affect achieving core goals of an entity. Key

performance indicator enables in mobilizing the employees for working towards achieving

the core objectives of the business. On the other hand, external KPIs are utilized for reaching

or achieving departmental performance with regards to overall core or main objectives of an

entity.

Role of pricing

Pricing plays a crucial role in increasing the profitability of the company as if the

company sets high prices it will gain higher profits but sometimes it results to reduction in

sales which indirectly lowers down the profits. However, lower prices facilitates lower rate of

return per item with increase in the level of revenue with high pace that in turn leads to

increase in the profits (KanKam-Kwarteng and et.al., 2018). Moreover, it brings out value

that for the company’s products and the services offered and also secured the amount of

profits that a individual needs to invest in the growth and the change. Pricing plays an

important role in increasing the efficiency within the sales of an organization and thus

company need to take initiatives relating to cost cutting on regular basis. Hence, the firm

should set up or seek for setting up reasonable price which all the individuals can affords and

this helps an enterprise in gaining market share and large customer base.

or achieving departmental performance with regards to overall core or main objectives of an

entity.

Role of pricing

Pricing plays a crucial role in increasing the profitability of the company as if the

company sets high prices it will gain higher profits but sometimes it results to reduction in

sales which indirectly lowers down the profits. However, lower prices facilitates lower rate of

return per item with increase in the level of revenue with high pace that in turn leads to

increase in the profits (KanKam-Kwarteng and et.al., 2018). Moreover, it brings out value

that for the company’s products and the services offered and also secured the amount of

profits that a individual needs to invest in the growth and the change. Pricing plays an

important role in increasing the efficiency within the sales of an organization and thus

company need to take initiatives relating to cost cutting on regular basis. Hence, the firm

should set up or seek for setting up reasonable price which all the individuals can affords and

this helps an enterprise in gaining market share and large customer base.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journal

Alkaraan, F., 2017. Strategic investment appraisal: multidisciplinary perspectives. Advances

in Mergers and Acquisitions. p.67.

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

Jibril, J. D. and Jagun, Z. T., 2018. Risk Identification Techniques in Valuation and

Investment Appraisal. International Journal of Engineering & Technology. 7(3.30).

pp.70-73.

KanKam-Kwarteng, C. and et.al., 2018. Service Innovation and Firm Performance of SMEs

auto service: the mediating role of Pricing Capability. Archives of Business

Research. 6(8).

Murad, M. H. and et.al., 2019. When continuous outcomes are measured using different

scales: guide for meta-analysis and interpretation. Bmj. 364. p.k4817.

Prajogo, D. and et.al., 2018. The relationships between information management, process

management and operational performance: Internal and external

contexts. International Journal of Production Economics. 199. pp.95-103.

Books and journal

Alkaraan, F., 2017. Strategic investment appraisal: multidisciplinary perspectives. Advances

in Mergers and Acquisitions. p.67.

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

Jibril, J. D. and Jagun, Z. T., 2018. Risk Identification Techniques in Valuation and

Investment Appraisal. International Journal of Engineering & Technology. 7(3.30).

pp.70-73.

KanKam-Kwarteng, C. and et.al., 2018. Service Innovation and Firm Performance of SMEs

auto service: the mediating role of Pricing Capability. Archives of Business

Research. 6(8).

Murad, M. H. and et.al., 2019. When continuous outcomes are measured using different

scales: guide for meta-analysis and interpretation. Bmj. 364. p.k4817.

Prajogo, D. and et.al., 2018. The relationships between information management, process

management and operational performance: Internal and external

contexts. International Journal of Production Economics. 199. pp.95-103.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.