Case Study on Taxation Law Australia 2022

VerifiedAdded on 2022/10/18

|10

|2771

|12

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

TAXATION LAW AUSTRALIA

CASE STUDY ON CAPITAL GAINS TAX AND CAPITAL

ALLOWANCE

STUDENT’S NAME:

ID:

MODULE:

INSTRUCTOR:

TAXATION LAW AUSTRALIA

CASE STUDY ON CAPITAL GAINS TAX AND CAPITAL

ALLOWANCE

STUDENT’S NAME:

ID:

MODULE:

INSTRUCTOR:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Table of Contents

Introduction...........................................................................................................................................2

Answer to the question no- 1................................................................................................................2

Answer to question no- 2......................................................................................................................6

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Table of Contents

Introduction...........................................................................................................................................2

Answer to the question no- 1................................................................................................................2

Answer to question no- 2......................................................................................................................6

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

3

Introduction

Answer to the question no- 1

This report reveals the key implication of the GST and capital gain tax rules and regulations.

It is analyzed that capital gain is the gains that can be achieved by selling assets, and such

gain acquires payable tax against as per the Australian taxation rules and regulations.

However, the loss can also be occurred due to the sale of assets which in turn supports the

assessed by providing financial back up to reduce the amount of CGT in the same calendar

year.

1. Capital Gains Tax Consequences on sale of Assets by Jasmine

●Capital Gains Tax (CGT)

.In Australia, CGT has been applied by the Australian Taxation Office since 20th September

'85 and generally covers a vast area of assets. Though some exemptions are there which do

not acquire CGT such as personal assets and solely used assets. The CGT becomes payable at

the time of disposal, not at the time when an assessee settles. In addition, the Australian

Taxation Office has implemented CGT by assessing separate heading, instead of integrated

with normal income and arrives at the taxable income which must be paid with the applied

tax rate. For an Australian resident, CGT is applied to his/her assets anywhere in the world

while for Norfolk Island residents, CGT has been applied since 23rd October 2015. There are

some subsidiary discounts for foreign residents in Australia by which they should pay tax for

the 'Taxable Australian Properties' only (Cassidy, and Cheng, 2017). When any asset has

occurred for 12 months at least, it can be enlisted as a long-term asset and a 50% discount can

be achieved by the assessee from the regulatory board. In order to maintain a smooth taxation

process, taxation system of Australia requires the total CGT to be reported in an annual

income tax return which increases the amount of payable tax for an assessed. When an

assessee makes a capital gain, it is added to the annual income which is assessable to pay tax

and thus the amount of tax is increased rapidly. Henceforth, to have a concept of annual tax,

one should calculate it at the early phase of the assessment year (Australian Taxation Office,

2019).

● Set-off and carry forward of loss

Another important note on the implementation of the Australian Taxation System is their Set

off & Carry forward rule which helps the assessee to adjust loss against gain that reduces the

Introduction

Answer to the question no- 1

This report reveals the key implication of the GST and capital gain tax rules and regulations.

It is analyzed that capital gain is the gains that can be achieved by selling assets, and such

gain acquires payable tax against as per the Australian taxation rules and regulations.

However, the loss can also be occurred due to the sale of assets which in turn supports the

assessed by providing financial back up to reduce the amount of CGT in the same calendar

year.

1. Capital Gains Tax Consequences on sale of Assets by Jasmine

●Capital Gains Tax (CGT)

.In Australia, CGT has been applied by the Australian Taxation Office since 20th September

'85 and generally covers a vast area of assets. Though some exemptions are there which do

not acquire CGT such as personal assets and solely used assets. The CGT becomes payable at

the time of disposal, not at the time when an assessee settles. In addition, the Australian

Taxation Office has implemented CGT by assessing separate heading, instead of integrated

with normal income and arrives at the taxable income which must be paid with the applied

tax rate. For an Australian resident, CGT is applied to his/her assets anywhere in the world

while for Norfolk Island residents, CGT has been applied since 23rd October 2015. There are

some subsidiary discounts for foreign residents in Australia by which they should pay tax for

the 'Taxable Australian Properties' only (Cassidy, and Cheng, 2017). When any asset has

occurred for 12 months at least, it can be enlisted as a long-term asset and a 50% discount can

be achieved by the assessee from the regulatory board. In order to maintain a smooth taxation

process, taxation system of Australia requires the total CGT to be reported in an annual

income tax return which increases the amount of payable tax for an assessed. When an

assessee makes a capital gain, it is added to the annual income which is assessable to pay tax

and thus the amount of tax is increased rapidly. Henceforth, to have a concept of annual tax,

one should calculate it at the early phase of the assessment year (Australian Taxation Office,

2019).

● Set-off and carry forward of loss

Another important note on the implementation of the Australian Taxation System is their Set

off & Carry forward rule which helps the assessee to adjust loss against gain that reduces the

4

amount of payable tax as loss refers deduction of capital gain. Set-off & Carry forward rule

allows an assessee to recover the amount payable tax for loss against capital gain.

● Capital Gains Tax (CGT) Events

Capital Gains Tax Events or CGT events are different types of transaction or events which

take place after completion of various CGT related events.

▪ CGT can be applied to the disposal of any CGT asset

▪ Again, it can be applied when the use of the CGT asset passes.

▪ CGT can occur when the loss is discovered.

▪ CGT occurs when an asset ends (Australian Taxation Office, 2019)

▪ Besides, CGT occurs when a contract is entered into or the right is created.

▪ CGT can be occurred due to the grant of options. In addition, CGT can occur when lease,

rent are taken place as trust is created (Hasan, & Sinning, 2018).

● CGT Assets

After the implementation of CGT, a variety of assets are considered as Capital Gains Tax

Assets, though some exceptions do not acquire CGT.

▪ Most of the real estate components are considered as CGT assets which consist of vacant

premises, business or industrial areas, properties on rent, hobby farms and holiday houses. It

is needed for an assessed to keep record of his/her real estate properties including own home

as it can also be used as a rental or business property in the future.

▪ Company shares or units in trusts can be considered as CGT assets as when a CGT event

occurs, the capital gain from shares and units acquire capital gains tax to assess annual

income tax return. On the other hand, profit from the sale of shares or units are considered

under normal taxation system and do not acquire CGT (Australian Taxation Office, 2019).

▪ Cryptocurrencies are subjected as a CGT asset as it is referred to as a digital asset which is

regulated by encryption techniques to generate additional units and verify transactions.

Cryptocurrency operates freely of government or central authority. Bitcoin is one of the most

significant examples of cryptocurrency (Australian Taxation Office, 2019).

▪ In addition, emotional attributes such as goodwill or right of contract can be considered as

CGT assets. Moreover, foreign currencies, leases, licenses are also considered as CGT assets

as all of them should be assessed by the income tax return (Hoopes, Robinson.& Slemrod,

2018).

amount of payable tax as loss refers deduction of capital gain. Set-off & Carry forward rule

allows an assessee to recover the amount payable tax for loss against capital gain.

● Capital Gains Tax (CGT) Events

Capital Gains Tax Events or CGT events are different types of transaction or events which

take place after completion of various CGT related events.

▪ CGT can be applied to the disposal of any CGT asset

▪ Again, it can be applied when the use of the CGT asset passes.

▪ CGT can occur when the loss is discovered.

▪ CGT occurs when an asset ends (Australian Taxation Office, 2019)

▪ Besides, CGT occurs when a contract is entered into or the right is created.

▪ CGT can be occurred due to the grant of options. In addition, CGT can occur when lease,

rent are taken place as trust is created (Hasan, & Sinning, 2018).

● CGT Assets

After the implementation of CGT, a variety of assets are considered as Capital Gains Tax

Assets, though some exceptions do not acquire CGT.

▪ Most of the real estate components are considered as CGT assets which consist of vacant

premises, business or industrial areas, properties on rent, hobby farms and holiday houses. It

is needed for an assessed to keep record of his/her real estate properties including own home

as it can also be used as a rental or business property in the future.

▪ Company shares or units in trusts can be considered as CGT assets as when a CGT event

occurs, the capital gain from shares and units acquire capital gains tax to assess annual

income tax return. On the other hand, profit from the sale of shares or units are considered

under normal taxation system and do not acquire CGT (Australian Taxation Office, 2019).

▪ Cryptocurrencies are subjected as a CGT asset as it is referred to as a digital asset which is

regulated by encryption techniques to generate additional units and verify transactions.

Cryptocurrency operates freely of government or central authority. Bitcoin is one of the most

significant examples of cryptocurrency (Australian Taxation Office, 2019).

▪ In addition, emotional attributes such as goodwill or right of contract can be considered as

CGT assets. Moreover, foreign currencies, leases, licenses are also considered as CGT assets

as all of them should be assessed by the income tax return (Hoopes, Robinson.& Slemrod,

2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

▪ Collectible items above a specific range can be considered as a CGT asset as it includes

valuable arts and crafts such as paintings, sculptures, engravings, jewelry, antiques, coins or

medallions etcetera. However, rare folios, manuscripts, first-day covers are also considered

as CGT assets.

▪ Personal assets such as furniture, boats, electricals items, household assistance are also

recognized as CGT assets. An assessee must pay tax for savings over 10,000 $ (Australian

Taxation Office, 2019).

● CGT Exemptions

Several capital gains are exempted from CGT and on the other hand, some losses are also

exempted from CGT which can not be used to compensate any CGT. Such exemptions need

no enlistment in income tax returns.

The main residence of an assessee is exempted from CGT but to avail the exemption,

the assessee must have lived in it. Foreign residents will not be considered as

exempted assessee as the property should be occupied by Australian only.

A motor vehicle that is used to carry less than one-tonne goods or fewer than nine

people can be exempted from CGT. A motorcycle can also be exempted (James,

2018).

In addition, Exemption from CGT can be considered for collectibles under 500$ when

acquired and personal use items under 1000$ when acquired. Depreciating assets such

as solely used items and assets acquired before 20th September 1985 can be

considered as pre-CGT assets (Australian Taxation Office, 2019).

Rewards that are gained through brave conduct are also considered as CGT exempt

assets. Compensation of damage is also considered as CGT exempt. Gambling is

exempt from CGT and the prize of competitions is also recognized as CGT free assets

(Australian Government, 2019).

● Resident for Tax purpose

Capital Gains Tax (CGT) is a payable tax that varies according to the residential status of an

assessee. To determine the residential status of an assessee, the Border Protection Board and

the Department of immigration use different standards so that the classification regarding the

taxation system can be made properly. Therefore the Australian Taxation Office (ATO) is

providing residential guidelines with the prior aim to make everyone a taxpayer.

▪ Collectible items above a specific range can be considered as a CGT asset as it includes

valuable arts and crafts such as paintings, sculptures, engravings, jewelry, antiques, coins or

medallions etcetera. However, rare folios, manuscripts, first-day covers are also considered

as CGT assets.

▪ Personal assets such as furniture, boats, electricals items, household assistance are also

recognized as CGT assets. An assessee must pay tax for savings over 10,000 $ (Australian

Taxation Office, 2019).

● CGT Exemptions

Several capital gains are exempted from CGT and on the other hand, some losses are also

exempted from CGT which can not be used to compensate any CGT. Such exemptions need

no enlistment in income tax returns.

The main residence of an assessee is exempted from CGT but to avail the exemption,

the assessee must have lived in it. Foreign residents will not be considered as

exempted assessee as the property should be occupied by Australian only.

A motor vehicle that is used to carry less than one-tonne goods or fewer than nine

people can be exempted from CGT. A motorcycle can also be exempted (James,

2018).

In addition, Exemption from CGT can be considered for collectibles under 500$ when

acquired and personal use items under 1000$ when acquired. Depreciating assets such

as solely used items and assets acquired before 20th September 1985 can be

considered as pre-CGT assets (Australian Taxation Office, 2019).

Rewards that are gained through brave conduct are also considered as CGT exempt

assets. Compensation of damage is also considered as CGT exempt. Gambling is

exempt from CGT and the prize of competitions is also recognized as CGT free assets

(Australian Government, 2019).

● Resident for Tax purpose

Capital Gains Tax (CGT) is a payable tax that varies according to the residential status of an

assessee. To determine the residential status of an assessee, the Border Protection Board and

the Department of immigration use different standards so that the classification regarding the

taxation system can be made properly. Therefore the Australian Taxation Office (ATO) is

providing residential guidelines with the prior aim to make everyone a taxpayer.

6

Core Australian residents who reside or have come to reside in Australia are

considered residents for tax purposes.

An assessee who has spent six or more months of the income year in Australia is

considered as a taxpayer.

Students across foreign countries who have spent at least six months for any course

are also considered as taxpayers in Australia.

People who intend to move to Australia for a better future are also considered

residents for tax purposes (Australian Taxation Office, 2019).

● CGT consequences of a sale of assets by Jasmine

▪ Sale of home

Jasmine sold her house for 650,000$ and acquired for 40,000$ as it provides gain which does

not come under CGT rules. Not only the home of Jasmine is purchased before 1985 but it was

her own house where she lived for years. As the conditions have gone in favor of Jasmine,

the gain is exempted for tax purposes. Therefore the sale of the house results in all positive

aspects.

▪ Sale of car

Jasmine sold her car for 10,000$ and acquired for 31,000 and thus it causes a loss for the

assessee. Instead, the car is not a typical antique, thus the loss is exempt from CGT and can

not be used to compensate any other gain and carry forward (Australian Taxation Office,

2019).

▪ Sale of business equipment

Jasmine has sold her business equipment for 65,000$ and acquired for 75,000$ which results

from a loss. The loss is independent of CGT as the equipment was used solely for her

business purposes. Therefore the loss neither offset any gain nor be carried forward

(Australian Government, 2019).

▪ Sale of goodwill

Goodwill is an internal attribute of Jasmine which is not considered as a taxpaying factor. In

addition, as the asset was active prior to sale, there were no CGT liabilities have arisen.

▪ Sale of furniture

Furniture is a personal use asset and in the case of Jasmine, the furniture was sold as a set of

10,000$ which includes items that are valued not more than 2000. Therefore CGT liabilities

have not arisen (Australian Taxation Office, 2019).

Core Australian residents who reside or have come to reside in Australia are

considered residents for tax purposes.

An assessee who has spent six or more months of the income year in Australia is

considered as a taxpayer.

Students across foreign countries who have spent at least six months for any course

are also considered as taxpayers in Australia.

People who intend to move to Australia for a better future are also considered

residents for tax purposes (Australian Taxation Office, 2019).

● CGT consequences of a sale of assets by Jasmine

▪ Sale of home

Jasmine sold her house for 650,000$ and acquired for 40,000$ as it provides gain which does

not come under CGT rules. Not only the home of Jasmine is purchased before 1985 but it was

her own house where she lived for years. As the conditions have gone in favor of Jasmine,

the gain is exempted for tax purposes. Therefore the sale of the house results in all positive

aspects.

▪ Sale of car

Jasmine sold her car for 10,000$ and acquired for 31,000 and thus it causes a loss for the

assessee. Instead, the car is not a typical antique, thus the loss is exempt from CGT and can

not be used to compensate any other gain and carry forward (Australian Taxation Office,

2019).

▪ Sale of business equipment

Jasmine has sold her business equipment for 65,000$ and acquired for 75,000$ which results

from a loss. The loss is independent of CGT as the equipment was used solely for her

business purposes. Therefore the loss neither offset any gain nor be carried forward

(Australian Government, 2019).

▪ Sale of goodwill

Goodwill is an internal attribute of Jasmine which is not considered as a taxpaying factor. In

addition, as the asset was active prior to sale, there were no CGT liabilities have arisen.

▪ Sale of furniture

Furniture is a personal use asset and in the case of Jasmine, the furniture was sold as a set of

10,000$ which includes items that are valued not more than 2000. Therefore CGT liabilities

have not arisen (Australian Taxation Office, 2019).

7

▪ Sale of second-hand paintings

As per the ATO rules for CGT, paintings are considered as a collectible item, but here no

CGT liability arises as not a single painting costs more than 500$. Therefore by selling

second-hand paintings, for 35,000$ Jasmine gained something for her future (Australian

Taxation Office, 2019).

▪ Sale of paintings direct from artists

Jasmine sold her paintings for 5000$ as 1000$ per painting which has acquired directly from

artists. As the paintings are collectible above 1000$, it is not exempt from CGT. As a result,

4000$ was the taxable amount for the sale of those paintings.

Answer to question no- 2

● Capital allowance

Capital allowance or tax depreciation is favorable taxation for business persons which allows

calculating the total amount of payable tax over a specific period for any individual business

and it can be claimed for a span of up to 40 years. In Australia, Capital Allowance has been

implemented on 1 July 2001, by Uniform Capital Allowance rules. Particular types of capital

expenditures for particular time slots are available under such allowance. A declination of

assets may also cause a reduction in the payable amount of tax in Australia while on the other

hand it is allowed as the total amount of assets can not be charged in a single income year.

There is a basic difference that isolates tax depreciation and capital allowance. Depreciation

is referred to as an additional tax but capital allowance is a deductible tax (Australian

Government, 2019).

The regulatory guidelines of capital allowance in Australia, also known as Uniform Capital

Allowance Rules provides important regulations to determine the cost of assets. Such

determination of cost is done to provide capital allowance due to the decline in asset value.

Some of the deductions could not be claimed by an assessee. However, deduction in terms of

certain assets can be claimed now in a new life (Australian Government, 2019).

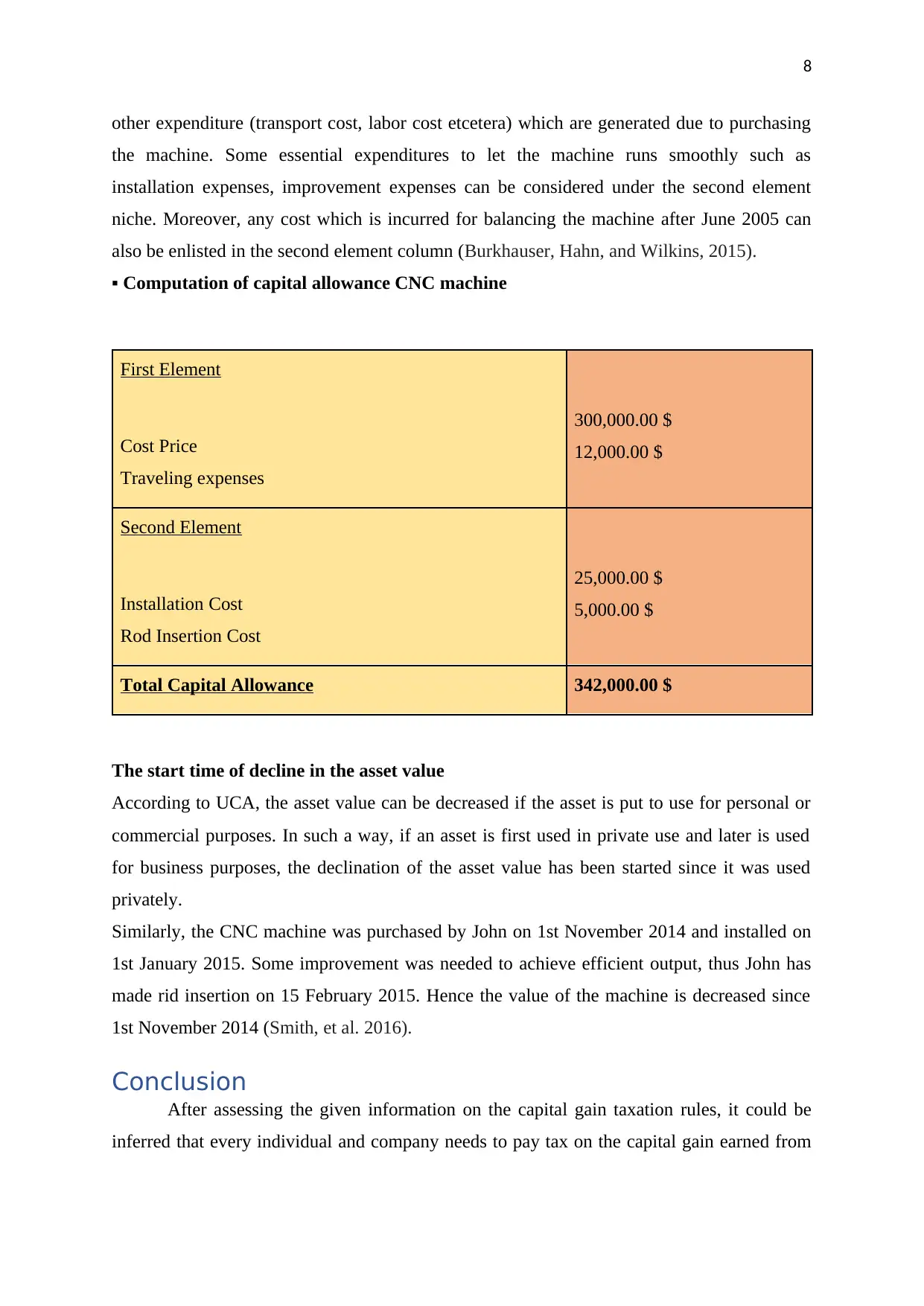

▪ Cost of CNC Machine for Capital Allowance

To determine the total amount of capital allowance, the cost of the assets needs to be

determined at first following the rules which are enlisted in UCA. In addition to the fact, the

computation of capital allowance considers two different types of costs. The first element of

the first type of cost includes the costs that are directly involved in acquiring the CNC

machine. One the other hand, the second element consists of the purchase price and every

▪ Sale of second-hand paintings

As per the ATO rules for CGT, paintings are considered as a collectible item, but here no

CGT liability arises as not a single painting costs more than 500$. Therefore by selling

second-hand paintings, for 35,000$ Jasmine gained something for her future (Australian

Taxation Office, 2019).

▪ Sale of paintings direct from artists

Jasmine sold her paintings for 5000$ as 1000$ per painting which has acquired directly from

artists. As the paintings are collectible above 1000$, it is not exempt from CGT. As a result,

4000$ was the taxable amount for the sale of those paintings.

Answer to question no- 2

● Capital allowance

Capital allowance or tax depreciation is favorable taxation for business persons which allows

calculating the total amount of payable tax over a specific period for any individual business

and it can be claimed for a span of up to 40 years. In Australia, Capital Allowance has been

implemented on 1 July 2001, by Uniform Capital Allowance rules. Particular types of capital

expenditures for particular time slots are available under such allowance. A declination of

assets may also cause a reduction in the payable amount of tax in Australia while on the other

hand it is allowed as the total amount of assets can not be charged in a single income year.

There is a basic difference that isolates tax depreciation and capital allowance. Depreciation

is referred to as an additional tax but capital allowance is a deductible tax (Australian

Government, 2019).

The regulatory guidelines of capital allowance in Australia, also known as Uniform Capital

Allowance Rules provides important regulations to determine the cost of assets. Such

determination of cost is done to provide capital allowance due to the decline in asset value.

Some of the deductions could not be claimed by an assessee. However, deduction in terms of

certain assets can be claimed now in a new life (Australian Government, 2019).

▪ Cost of CNC Machine for Capital Allowance

To determine the total amount of capital allowance, the cost of the assets needs to be

determined at first following the rules which are enlisted in UCA. In addition to the fact, the

computation of capital allowance considers two different types of costs. The first element of

the first type of cost includes the costs that are directly involved in acquiring the CNC

machine. One the other hand, the second element consists of the purchase price and every

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

other expenditure (transport cost, labor cost etcetera) which are generated due to purchasing

the machine. Some essential expenditures to let the machine runs smoothly such as

installation expenses, improvement expenses can be considered under the second element

niche. Moreover, any cost which is incurred for balancing the machine after June 2005 can

also be enlisted in the second element column (Burkhauser, Hahn, and Wilkins, 2015).

▪ Computation of capital allowance CNC machine

First Element

Cost Price

Traveling expenses

300,000.00 $

12,000.00 $

Second Element

Installation Cost

Rod Insertion Cost

25,000.00 $

5,000.00 $

Total Capital Allowance 342,000.00 $

The start time of decline in the asset value

According to UCA, the asset value can be decreased if the asset is put to use for personal or

commercial purposes. In such a way, if an asset is first used in private use and later is used

for business purposes, the declination of the asset value has been started since it was used

privately.

Similarly, the CNC machine was purchased by John on 1st November 2014 and installed on

1st January 2015. Some improvement was needed to achieve efficient output, thus John has

made rid insertion on 15 February 2015. Hence the value of the machine is decreased since

1st November 2014 (Smith, et al. 2016).

Conclusion

After assessing the given information on the capital gain taxation rules, it could be

inferred that every individual and company needs to pay tax on the capital gain earned from

other expenditure (transport cost, labor cost etcetera) which are generated due to purchasing

the machine. Some essential expenditures to let the machine runs smoothly such as

installation expenses, improvement expenses can be considered under the second element

niche. Moreover, any cost which is incurred for balancing the machine after June 2005 can

also be enlisted in the second element column (Burkhauser, Hahn, and Wilkins, 2015).

▪ Computation of capital allowance CNC machine

First Element

Cost Price

Traveling expenses

300,000.00 $

12,000.00 $

Second Element

Installation Cost

Rod Insertion Cost

25,000.00 $

5,000.00 $

Total Capital Allowance 342,000.00 $

The start time of decline in the asset value

According to UCA, the asset value can be decreased if the asset is put to use for personal or

commercial purposes. In such a way, if an asset is first used in private use and later is used

for business purposes, the declination of the asset value has been started since it was used

privately.

Similarly, the CNC machine was purchased by John on 1st November 2014 and installed on

1st January 2015. Some improvement was needed to achieve efficient output, thus John has

made rid insertion on 15 February 2015. Hence the value of the machine is decreased since

1st November 2014 (Smith, et al. 2016).

Conclusion

After assessing the given information on the capital gain taxation rules, it could be

inferred that every individual and company needs to pay tax on the capital gain earned from

9

the sale of assets. However, in the case of GST, the availing of the GST input is allowed

when the company is registered and given GST number.

the sale of assets. However, in the case of GST, the availing of the GST input is allowed

when the company is registered and given GST number.

10

References

Australian Government (2019). Capital Gains Tax (CGT). [online] Retrieved from

https://www.business.gov.au/finance/taxation/capital-gains-tax on 21 September 2019

Australian Taxation Office (2019). CGT assets and exemptions. [online] Retrieved from

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-andexemptions/

#Exemptions1 on 21 September 2019

Australian Taxation Office (2019). Other capital assets and expense deductions. [online]

retrieved from https://www.ato.gov.au/business/depreciation-and-capital-expenses-

andallowances/other-capital-asset-and-expense-deductions/ on 21 September 2019

Australian Taxation Office (2019). Uniform capital allowance system: calculating the decline

in value of depreciating assets. [online] Retrieved from

https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/

Indetail/Depreciating-assets/Uniform-capital-allowance-system--calculating-the-

decline-invalue-of-a-depreciating-asset/ on 21 September 2019

Hasan, S. & Sinning, M., 2018. GST reform in Australia: implications of estimating price

elasticities of demand for food. Economic Record, 94(306), pp.239-254.

Hoopes, J.L., Robinson, L. & Slemrod, J., 2018. Public tax-return disclosure. Journal of

Accounting and Economics, 66(1), pp.142-162.

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low-value goods in Australia,(2018), 47.

Smith, F., Smillie, K., Fitzsimons, J., Lindsay, B., Wells, G., Marles, V., Hutchinson, J.,

O'Hara, B., Perrigo, T & Atkison, I., (2016). Reforms required to the Australian tax

system to improve biodiversity conservation on private land. Environmental and

planning law journal, 33, pp.443-450.

References

Australian Government (2019). Capital Gains Tax (CGT). [online] Retrieved from

https://www.business.gov.au/finance/taxation/capital-gains-tax on 21 September 2019

Australian Taxation Office (2019). CGT assets and exemptions. [online] Retrieved from

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-andexemptions/

#Exemptions1 on 21 September 2019

Australian Taxation Office (2019). Other capital assets and expense deductions. [online]

retrieved from https://www.ato.gov.au/business/depreciation-and-capital-expenses-

andallowances/other-capital-asset-and-expense-deductions/ on 21 September 2019

Australian Taxation Office (2019). Uniform capital allowance system: calculating the decline

in value of depreciating assets. [online] Retrieved from

https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/

Indetail/Depreciating-assets/Uniform-capital-allowance-system--calculating-the-

decline-invalue-of-a-depreciating-asset/ on 21 September 2019

Hasan, S. & Sinning, M., 2018. GST reform in Australia: implications of estimating price

elasticities of demand for food. Economic Record, 94(306), pp.239-254.

Hoopes, J.L., Robinson, L. & Slemrod, J., 2018. Public tax-return disclosure. Journal of

Accounting and Economics, 66(1), pp.142-162.

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low-value goods in Australia,(2018), 47.

Smith, F., Smillie, K., Fitzsimons, J., Lindsay, B., Wells, G., Marles, V., Hutchinson, J.,

O'Hara, B., Perrigo, T & Atkison, I., (2016). Reforms required to the Australian tax

system to improve biodiversity conservation on private land. Environmental and

planning law journal, 33, pp.443-450.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.