Company Accounting 2019: Business Combination, Surplus on Fair Valuation

Added on 2023-03-21

24 Pages4199 Words32 Views

Company Accounting 2019

Table of Contents

Answer to Question No.1............................................................................................................................3

Answer to Question 1 (1).........................................................................................................................3

Answer to Question 1 (2).........................................................................................................................3

Answer to Question 1 (3).........................................................................................................................4

Answer to Question 1 (4).........................................................................................................................4

Answer to Question No.2 (Part A) (1)..........................................................................................................5

Answer to Question No.2 (Part A) (2)..........................................................................................................6

Answer to Question No.2 (Part B)...............................................................................................................7

Business Combination.............................................................................................................................7

Answer to Question No.3 (1).......................................................................................................................8

Answer to Question No.3 (2) & (3)..............................................................................................................9

Answer to Question No.3 (4).....................................................................................................................13

Answer to Question No.3 (5) (a)................................................................................................................14

Answer to Question No.3 (5) (b)................................................................................................................15

Answer to Question No.3 (5) (c)................................................................................................................16

Answer to Question No.4 (1).....................................................................................................................17

Answer to Question No.4 (2).....................................................................................................................18

Answer to Question No.4 (3).....................................................................................................................18

Answer to Question No.4 (4).....................................................................................................................19

Answer to Question No.4 (5).....................................................................................................................20

Bibliography...............................................................................................................................................23

Name of the Student Page 2

Table of Contents

Answer to Question No.1............................................................................................................................3

Answer to Question 1 (1).........................................................................................................................3

Answer to Question 1 (2).........................................................................................................................3

Answer to Question 1 (3).........................................................................................................................4

Answer to Question 1 (4).........................................................................................................................4

Answer to Question No.2 (Part A) (1)..........................................................................................................5

Answer to Question No.2 (Part A) (2)..........................................................................................................6

Answer to Question No.2 (Part B)...............................................................................................................7

Business Combination.............................................................................................................................7

Answer to Question No.3 (1).......................................................................................................................8

Answer to Question No.3 (2) & (3)..............................................................................................................9

Answer to Question No.3 (4).....................................................................................................................13

Answer to Question No.3 (5) (a)................................................................................................................14

Answer to Question No.3 (5) (b)................................................................................................................15

Answer to Question No.3 (5) (c)................................................................................................................16

Answer to Question No.4 (1).....................................................................................................................17

Answer to Question No.4 (2).....................................................................................................................18

Answer to Question No.4 (3).....................................................................................................................18

Answer to Question No.4 (4).....................................................................................................................19

Answer to Question No.4 (5).....................................................................................................................20

Bibliography...............................................................................................................................................23

Name of the Student Page 2

Company Accounting 2019

Answer to Question No.1

Answer to Question 1 (1)

In the books of Baby Shark Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

30 June 2019 Retained Earnings 1,800

Deferred Tax Assets 1,800

(Being deduction of earlier years disallowed by

Australian Tax Officer)

Answer to Question 1 (2)

Baby Shark Limited

Computation of Tax for the year ended 30 June 2019

Particulars Amount ($) Amount ($)

Profit before tax (A) 92,550

Add: Expenses Disallowed in Tax (B)

Carrying amount of plant sold 30,000

Amortization of development costs 15,000

Depreciation expense - equipment 5,500

Depreciation expense – plant 24,000

Provision for employee benefits (Incremental Provision) 4,400

Doubtful debts expense 8,100

Entertainment expense 13,200

Goodwill impairment 2,000

Insurance expense 12,900

Proceeds from sale of plant 33,000

Warranty expense 1,500

Accrual for accounting fees (“g”) 4,500 154,100

Less: Expenses Allowed/Income Exempt in Tax (C)

Proceeds from sale of plant 33,000

Government grant (exempt income) 2,200

Development expenditure (125% of 45,000) (“j”) 56,250

Plant Depreciation (“d”) 28,800

Equipment Depreciation (“e”) 7,000

Carrying amount of plant sold (“c”) 26,000

Doubtful Debts 7,900

Warranties 600

Insurance Expenses (Paid in Current Year) 10,700 172,450

Taxable Income (A+B-C) 74,200

Tax on above @ 30% 22,260

Name of the Student Page 3

Answer to Question No.1

Answer to Question 1 (1)

In the books of Baby Shark Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

30 June 2019 Retained Earnings 1,800

Deferred Tax Assets 1,800

(Being deduction of earlier years disallowed by

Australian Tax Officer)

Answer to Question 1 (2)

Baby Shark Limited

Computation of Tax for the year ended 30 June 2019

Particulars Amount ($) Amount ($)

Profit before tax (A) 92,550

Add: Expenses Disallowed in Tax (B)

Carrying amount of plant sold 30,000

Amortization of development costs 15,000

Depreciation expense - equipment 5,500

Depreciation expense – plant 24,000

Provision for employee benefits (Incremental Provision) 4,400

Doubtful debts expense 8,100

Entertainment expense 13,200

Goodwill impairment 2,000

Insurance expense 12,900

Proceeds from sale of plant 33,000

Warranty expense 1,500

Accrual for accounting fees (“g”) 4,500 154,100

Less: Expenses Allowed/Income Exempt in Tax (C)

Proceeds from sale of plant 33,000

Government grant (exempt income) 2,200

Development expenditure (125% of 45,000) (“j”) 56,250

Plant Depreciation (“d”) 28,800

Equipment Depreciation (“e”) 7,000

Carrying amount of plant sold (“c”) 26,000

Doubtful Debts 7,900

Warranties 600

Insurance Expenses (Paid in Current Year) 10,700 172,450

Taxable Income (A+B-C) 74,200

Tax on above @ 30% 22,260

Name of the Student Page 3

Company Accounting 2019

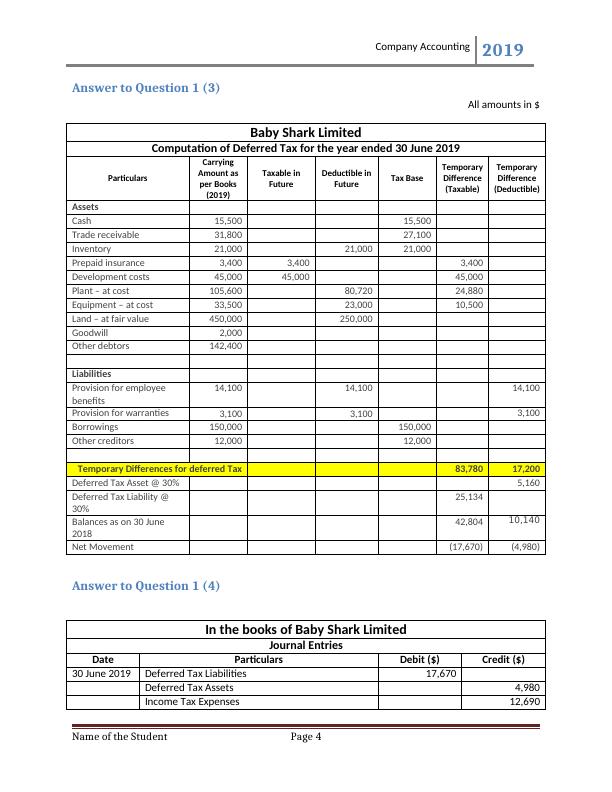

Answer to Question 1 (3)

All amounts in $

Baby Shark Limited

Computation of Deferred Tax for the year ended 30 June 2019

Particulars

Carrying

Amount as

per Books

(2019)

Taxable in

Future

Deductible in

Future Tax Base

Temporary

Difference

(Taxable)

Temporary

Difference

(Deductible)

Assets

Cash 15,500 15,500

Trade receivable 31,800 27,100

Inventory 21,000 21,000 21,000

Prepaid insurance 3,400 3,400 3,400

Development costs 45,000 45,000 45,000

Plant – at cost 105,600 80,720 24,880

Equipment – at cost 33,500 23,000 10,500

Land – at fair value 450,000 250,000

Goodwill 2,000

Other debtors 142,400

Liabilities

Provision for employee

benefits

14,100 14,100 14,100

Provision for warranties 3,100 3,100 3,100

Borrowings 150,000 150,000

Other creditors 12,000 12,000

Temporary Differences for deferred Tax 83,780 17,200

Deferred Tax Asset @ 30% 5,160

Deferred Tax Liability @

30%

25,134

Balances as on 30 June

2018

42,804 10,140

Net Movement (17,670) (4,980)

Answer to Question 1 (4)

In the books of Baby Shark Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

30 June 2019 Deferred Tax Liabilities 17,670

Deferred Tax Assets 4,980

Income Tax Expenses 12,690

Name of the Student Page 4

Answer to Question 1 (3)

All amounts in $

Baby Shark Limited

Computation of Deferred Tax for the year ended 30 June 2019

Particulars

Carrying

Amount as

per Books

(2019)

Taxable in

Future

Deductible in

Future Tax Base

Temporary

Difference

(Taxable)

Temporary

Difference

(Deductible)

Assets

Cash 15,500 15,500

Trade receivable 31,800 27,100

Inventory 21,000 21,000 21,000

Prepaid insurance 3,400 3,400 3,400

Development costs 45,000 45,000 45,000

Plant – at cost 105,600 80,720 24,880

Equipment – at cost 33,500 23,000 10,500

Land – at fair value 450,000 250,000

Goodwill 2,000

Other debtors 142,400

Liabilities

Provision for employee

benefits

14,100 14,100 14,100

Provision for warranties 3,100 3,100 3,100

Borrowings 150,000 150,000

Other creditors 12,000 12,000

Temporary Differences for deferred Tax 83,780 17,200

Deferred Tax Asset @ 30% 5,160

Deferred Tax Liability @

30%

25,134

Balances as on 30 June

2018

42,804 10,140

Net Movement (17,670) (4,980)

Answer to Question 1 (4)

In the books of Baby Shark Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

30 June 2019 Deferred Tax Liabilities 17,670

Deferred Tax Assets 4,980

Income Tax Expenses 12,690

Name of the Student Page 4

Company Accounting 2019

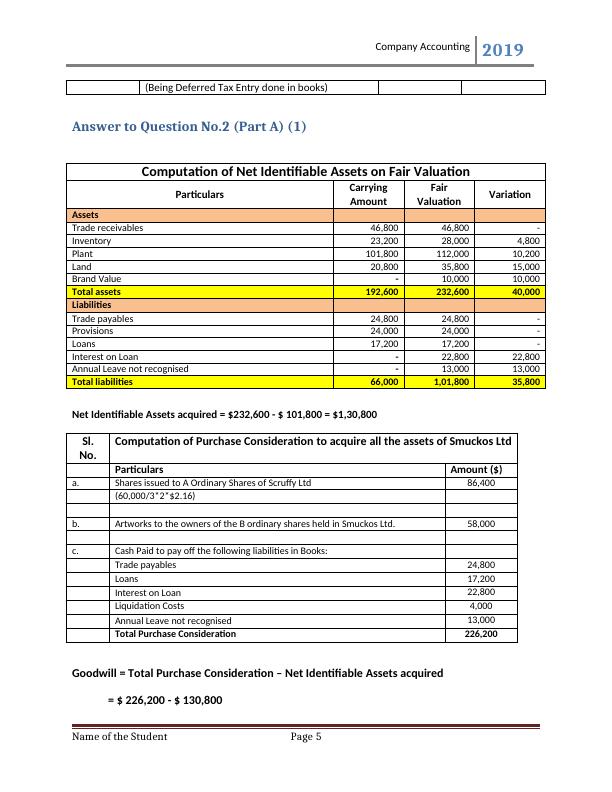

(Being Deferred Tax Entry done in books)

Answer to Question No.2 (Part A) (1)

Computation of Net Identifiable Assets on Fair Valuation

Particulars Carrying

Amount

Fair

Valuation Variation

Assets

Trade receivables 46,800 46,800 -

Inventory 23,200 28,000 4,800

Plant 101,800 112,000 10,200

Land 20,800 35,800 15,000

Brand Value - 10,000 10,000

Total assets 192,600 232,600 40,000

Liabilities

Trade payables 24,800 24,800 -

Provisions 24,000 24,000 -

Loans 17,200 17,200 -

Interest on Loan - 22,800 22,800

Annual Leave not recognised - 13,000 13,000

Total liabilities 66,000 1,01,800 35,800

Net Identifiable Assets acquired = $232,600 - $ 101,800 = $1,30,800

Sl.

No.

Computation of Purchase Consideration to acquire all the assets of Smuckos Ltd

Particulars Amount ($)

a. Shares issued to A Ordinary Shares of Scruffy Ltd 86,400

(60,000/3*2*$2.16)

b. Artworks to the owners of the B ordinary shares held in Smuckos Ltd. 58,000

c. Cash Paid to pay off the following liabilities in Books:

Trade payables 24,800

Loans 17,200

Interest on Loan 22,800

Liquidation Costs 4,000

Annual Leave not recognised 13,000

Total Purchase Consideration 226,200

Goodwill = Total Purchase Consideration – Net Identifiable Assets acquired

= $ 226,200 - $ 130,800

Name of the Student Page 5

(Being Deferred Tax Entry done in books)

Answer to Question No.2 (Part A) (1)

Computation of Net Identifiable Assets on Fair Valuation

Particulars Carrying

Amount

Fair

Valuation Variation

Assets

Trade receivables 46,800 46,800 -

Inventory 23,200 28,000 4,800

Plant 101,800 112,000 10,200

Land 20,800 35,800 15,000

Brand Value - 10,000 10,000

Total assets 192,600 232,600 40,000

Liabilities

Trade payables 24,800 24,800 -

Provisions 24,000 24,000 -

Loans 17,200 17,200 -

Interest on Loan - 22,800 22,800

Annual Leave not recognised - 13,000 13,000

Total liabilities 66,000 1,01,800 35,800

Net Identifiable Assets acquired = $232,600 - $ 101,800 = $1,30,800

Sl.

No.

Computation of Purchase Consideration to acquire all the assets of Smuckos Ltd

Particulars Amount ($)

a. Shares issued to A Ordinary Shares of Scruffy Ltd 86,400

(60,000/3*2*$2.16)

b. Artworks to the owners of the B ordinary shares held in Smuckos Ltd. 58,000

c. Cash Paid to pay off the following liabilities in Books:

Trade payables 24,800

Loans 17,200

Interest on Loan 22,800

Liquidation Costs 4,000

Annual Leave not recognised 13,000

Total Purchase Consideration 226,200

Goodwill = Total Purchase Consideration – Net Identifiable Assets acquired

= $ 226,200 - $ 130,800

Name of the Student Page 5

Company Accounting 2019

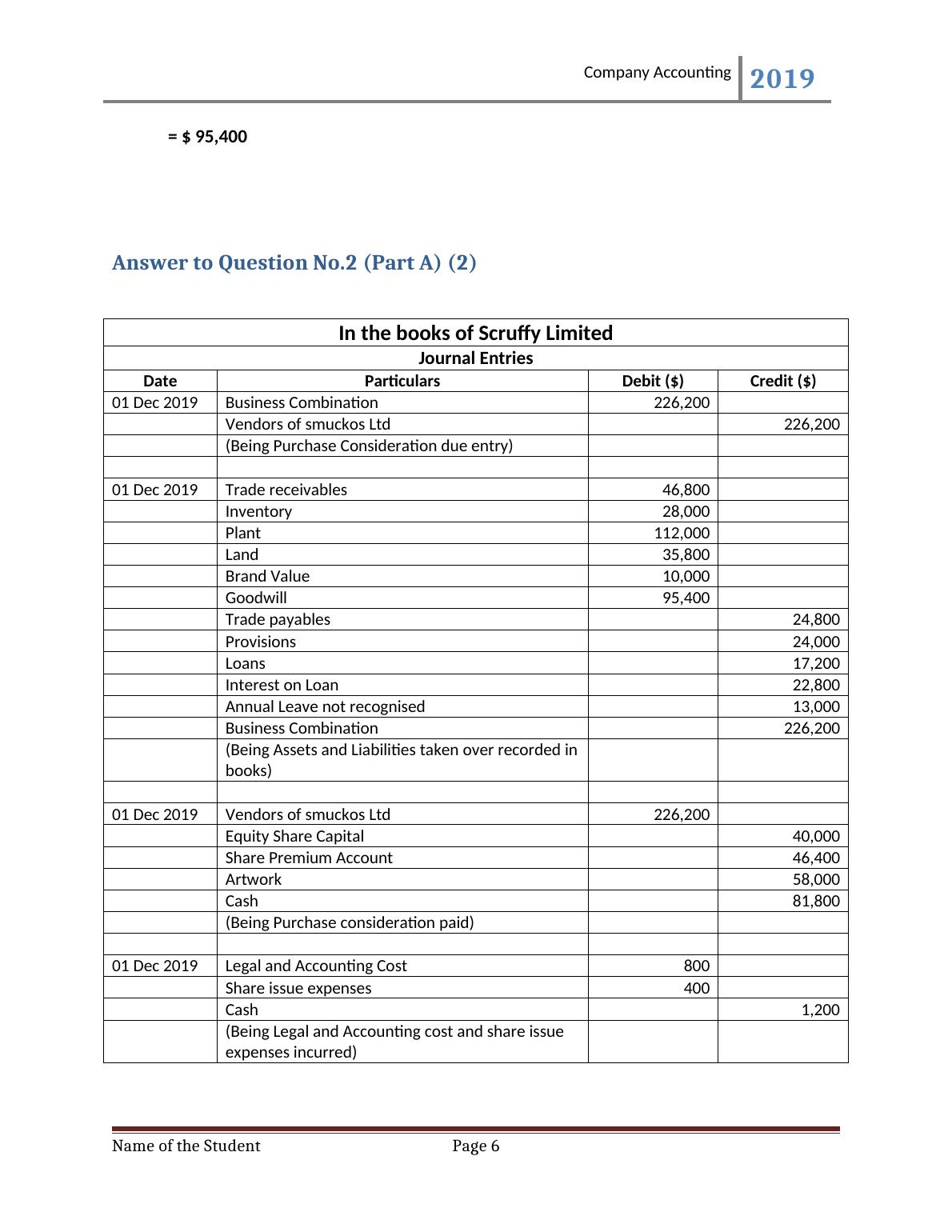

= $ 95,400

Answer to Question No.2 (Part A) (2)

In the books of Scruffy Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

01 Dec 2019 Business Combination 226,200

Vendors of smuckos Ltd 226,200

(Being Purchase Consideration due entry)

01 Dec 2019 Trade receivables 46,800

Inventory 28,000

Plant 112,000

Land 35,800

Brand Value 10,000

Goodwill 95,400

Trade payables 24,800

Provisions 24,000

Loans 17,200

Interest on Loan 22,800

Annual Leave not recognised 13,000

Business Combination 226,200

(Being Assets and Liabilities taken over recorded in

books)

01 Dec 2019 Vendors of smuckos Ltd 226,200

Equity Share Capital 40,000

Share Premium Account 46,400

Artwork 58,000

Cash 81,800

(Being Purchase consideration paid)

01 Dec 2019 Legal and Accounting Cost 800

Share issue expenses 400

Cash 1,200

(Being Legal and Accounting cost and share issue

expenses incurred)

Name of the Student Page 6

= $ 95,400

Answer to Question No.2 (Part A) (2)

In the books of Scruffy Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

01 Dec 2019 Business Combination 226,200

Vendors of smuckos Ltd 226,200

(Being Purchase Consideration due entry)

01 Dec 2019 Trade receivables 46,800

Inventory 28,000

Plant 112,000

Land 35,800

Brand Value 10,000

Goodwill 95,400

Trade payables 24,800

Provisions 24,000

Loans 17,200

Interest on Loan 22,800

Annual Leave not recognised 13,000

Business Combination 226,200

(Being Assets and Liabilities taken over recorded in

books)

01 Dec 2019 Vendors of smuckos Ltd 226,200

Equity Share Capital 40,000

Share Premium Account 46,400

Artwork 58,000

Cash 81,800

(Being Purchase consideration paid)

01 Dec 2019 Legal and Accounting Cost 800

Share issue expenses 400

Cash 1,200

(Being Legal and Accounting cost and share issue

expenses incurred)

Name of the Student Page 6

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Advanced Corporate Reportinglg...

|15

|1731

|32

Calculation of Taxable Incomelg...

|11

|1807

|53

MAA363 Corporate Accountinglg...

|6

|913

|174

Corporate Accountinglg...

|12

|915

|78

Company Accounting: Tax Effect Accounting, Business Combinations, Consolidationlg...

|20

|3778

|72

Calculation of Deferred Tax Asset and Liabilitylg...

|31

|5355

|83