Company Accounting Report: Elevated Enterprise Ltd Analysis

VerifiedAdded on 2022/10/14

|20

|2766

|208

Report

AI Summary

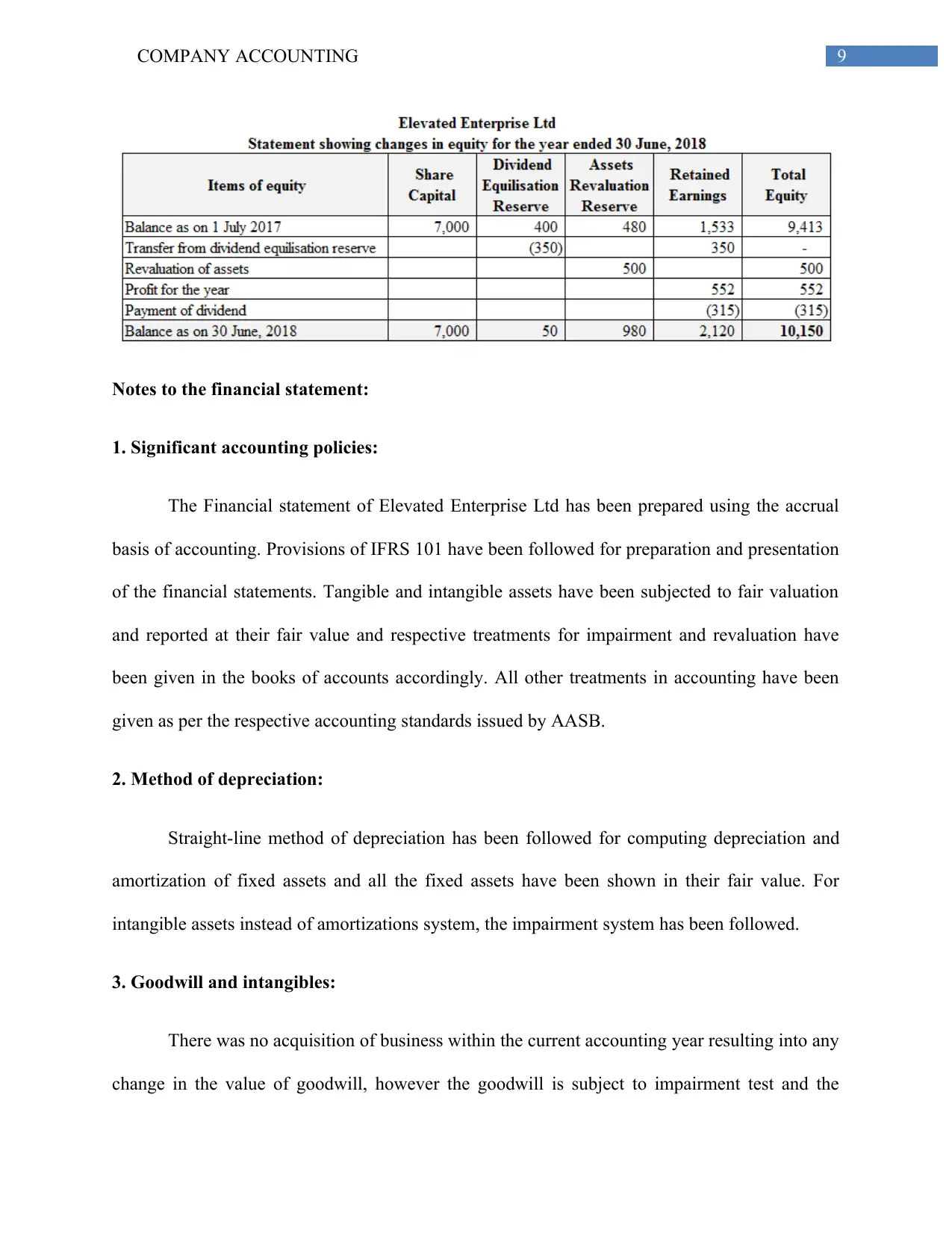

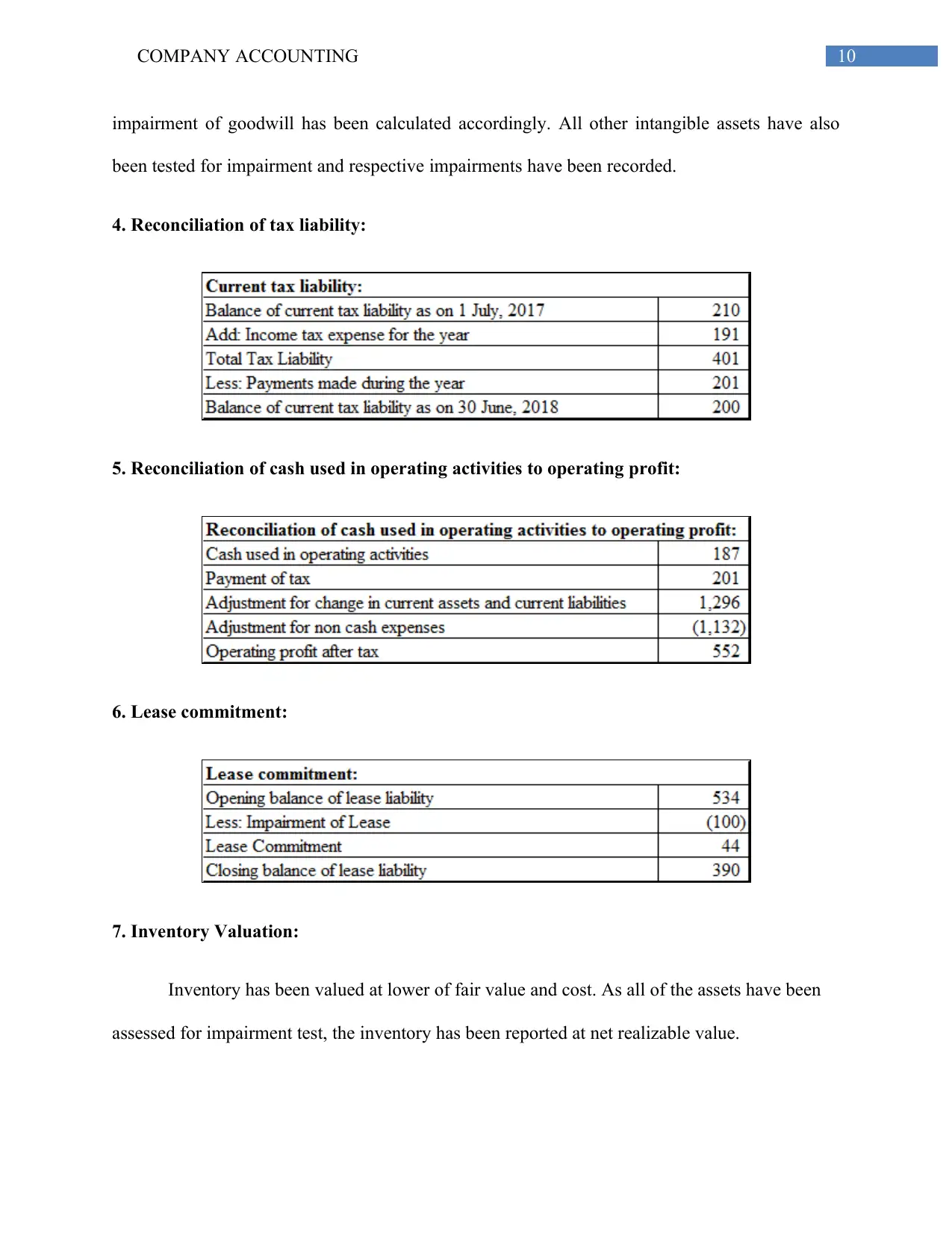

This comprehensive report delves into the realm of company accounting, encompassing a detailed analysis of financial statements, shareholder reports, and key financial metrics. The report begins with a corrected financial statement for Elevated Enterprise Ltd and progresses to a thorough financial report, which includes notes on significant accounting policies, depreciation methods, goodwill, and tax reconciliation. A shareholder's report is also presented, offering an executive summary, introduction, discussions on taxation, director's duties, and material items. The report explores integrated computer accounting systems, various formats, and crucial topics like leave provisions, depreciation calculations, and double-entry bookkeeping. It also provides a comparison between credit cash and credit balance accountants. Furthermore, the report incorporates an analysis of financial statements from Lynch Quality Goods, evaluating their income statements and balance sheets from 2016/2017 and 2017/2018, including ratio analysis, and the impact of a potential investment on financial ratios. The report offers insights into the business's performance and provides advice on financial strategies.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.