FNCE 3006 Company Analysis Group Assignment

VerifiedAdded on 2019/09/18

|12

|2305

|146

Case Study

AI Summary

This document presents a comprehensive case study of Algonquin Power & Utilities Corporation (APUC), a North American renewable energy and utility company. The analysis includes an executive summary, an introduction to APUC's operations and market position, and a detailed examination of its financial performance using various ratios. Profitability ratios, such as profit margin, return on assets, and return on equity, are analyzed, along with market value ratios like earnings per share and price-to-earnings ratio. Growth ratios, asset utilization ratios, and short-term solvency and long-term debt ratios are also evaluated. The study compares APUC's performance against industry averages and key competitors, providing insights into the company's strengths and areas for potential growth. The document also includes exhibits with detailed financial data and competitor information.

COMPANY ANALYSIS FNCE 3006: Group

Assignment

COMPANY NAME:

________________________________________________________

Group # ____________ Members:

1. ______________________________________.

2.______________________________________

3.______________________________________

4.______________________________________

5.______________________________________

EXECUTIVE SUMMARY:

Assignment

COMPANY NAME:

________________________________________________________

Group # ____________ Members:

1. ______________________________________.

2.______________________________________

3.______________________________________

4.______________________________________

5.______________________________________

EXECUTIVE SUMMARY:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction:

The Algonquin Power & Utilities Corporation (APUC) is a North American

renewable energy and well-controlled utility company with an operating asset of about

$5 billion. The corporation operates and acquires clean and green energy assets. These

assets include the wind, solar power facilities, hydroelectric, and thermal. Also, the

company provides sustainable utility distribution of natural gas, electricity, and water.

APUC serves an extensive customer base of more than 564,000 consumers in America.

The company has two fully functional subsidiaries, which are Liberty Utilities and

Algonquin Power Company. The Algonquin Power Company has an equity interest in

over 33 clean energy facilities that deals with solar, thermal, wind, and hydroelectric

energy. The Liberty Utilities has more than 560,000 customers and serves 11 states in

the United States. This company has over 175,000 customers in wastewater treatment

and water distribution, 92,000 customers in electricity distribution, and 293,000

connections in natural gas distribution.

APUC transmission group invests in a rate controlled electric transmission and

pipeline systems of natural gas in Canada and the United States. APUC being the

biggest utility company in North America, it commits itself to sustainability and

development in economic, environmental, and social values. The company’s corporate

responsibility programs serve to conserve, preserve, and improve the environment. The

primary pillar of sustainability for the corporation is the planet. APUC prioritize in

protecting the natural environment by funding various projects. The company’s market

value as of 18th November 2016 was $2,926.74 million, and it is expected to grow in

the future (Algonquin Power & Utilities Corporation). APUC has a projected growth of

0.47%. The company’s instalment receipts, preferred shares, and common shares are

renewable energy and well-controlled utility company with an operating asset of about

$5 billion. The corporation operates and acquires clean and green energy assets. These

assets include the wind, solar power facilities, hydroelectric, and thermal. Also, the

company provides sustainable utility distribution of natural gas, electricity, and water.

APUC serves an extensive customer base of more than 564,000 consumers in America.

The company has two fully functional subsidiaries, which are Liberty Utilities and

Algonquin Power Company. The Algonquin Power Company has an equity interest in

over 33 clean energy facilities that deals with solar, thermal, wind, and hydroelectric

energy. The Liberty Utilities has more than 560,000 customers and serves 11 states in

the United States. This company has over 175,000 customers in wastewater treatment

and water distribution, 92,000 customers in electricity distribution, and 293,000

connections in natural gas distribution.

APUC transmission group invests in a rate controlled electric transmission and

pipeline systems of natural gas in Canada and the United States. APUC being the

biggest utility company in North America, it commits itself to sustainability and

development in economic, environmental, and social values. The company’s corporate

responsibility programs serve to conserve, preserve, and improve the environment. The

primary pillar of sustainability for the corporation is the planet. APUC prioritize in

protecting the natural environment by funding various projects. The company’s market

value as of 18th November 2016 was $2,926.74 million, and it is expected to grow in

the future (Algonquin Power & Utilities Corporation). APUC has a projected growth of

0.47%. The company’s instalment receipts, preferred shares, and common shares are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

traded on the Toronto Stock Exchange (TSE) under the symbols AQN.IR, AQN.PR.A,

and AQN respectively. By investing in APUC, one is assured of great returns because

the demand for the products the company offers is rapidly increasing.

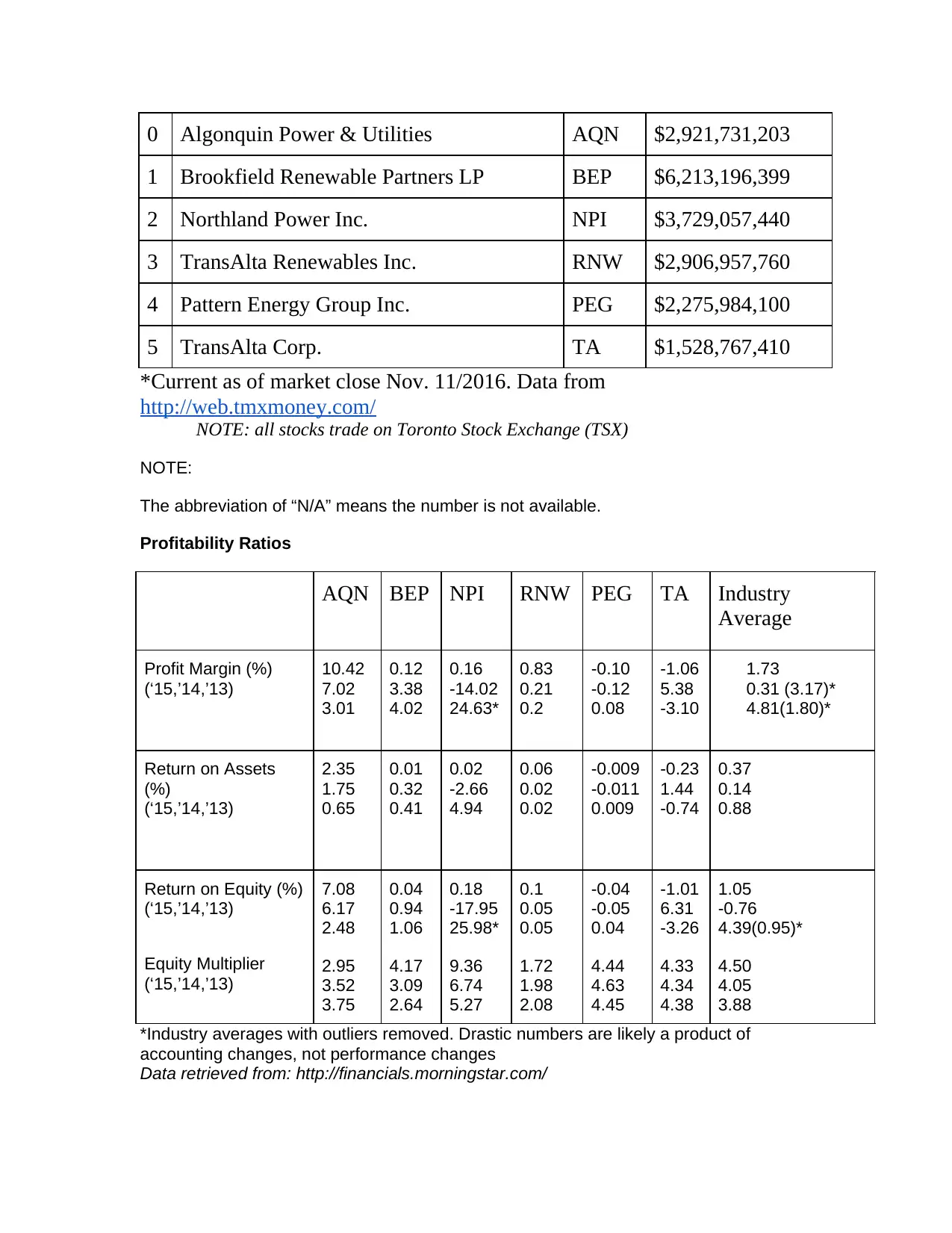

Profitability Ratios

In the past three years, AQN’s return on equity has augmented. Examining the DuPont

Identity while considering operating efficiency, asset use efficiency, and financial

leverage will explain this growth. Refer to EXHIBIT X for financial data.

Profit Margin

AQN’s profit margin gives insight to how efficiently they manage their operations.

Comparatively, in AQN’s last two years of operations, the differences between revenues

and costs have been more significant than industry standards. With NPI’s abnormally

high outlier ignored, even 2013’s profit margin for AQN is better than the industry

average. In other words, through its efficient operations, AQN receives more bottom

line than it’s competitors.

Return on Assets

The returns on book assets are favourable. Not only have the last two years been above

the industry average, but since 2013 it has been growing. This is strength since asset

usage is becoming more efficient. In 2015, about $0.10 of profit is made per dollar of

asset owned compared to the $0.02 industry average. It is also important to note that the

return on equity is higher than the return on assets. This gives insight to AQN’s use of

financial leverage.

and AQN respectively. By investing in APUC, one is assured of great returns because

the demand for the products the company offers is rapidly increasing.

Profitability Ratios

In the past three years, AQN’s return on equity has augmented. Examining the DuPont

Identity while considering operating efficiency, asset use efficiency, and financial

leverage will explain this growth. Refer to EXHIBIT X for financial data.

Profit Margin

AQN’s profit margin gives insight to how efficiently they manage their operations.

Comparatively, in AQN’s last two years of operations, the differences between revenues

and costs have been more significant than industry standards. With NPI’s abnormally

high outlier ignored, even 2013’s profit margin for AQN is better than the industry

average. In other words, through its efficient operations, AQN receives more bottom

line than it’s competitors.

Return on Assets

The returns on book assets are favourable. Not only have the last two years been above

the industry average, but since 2013 it has been growing. This is strength since asset

usage is becoming more efficient. In 2015, about $0.10 of profit is made per dollar of

asset owned compared to the $0.02 industry average. It is also important to note that the

return on equity is higher than the return on assets. This gives insight to AQN’s use of

financial leverage.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

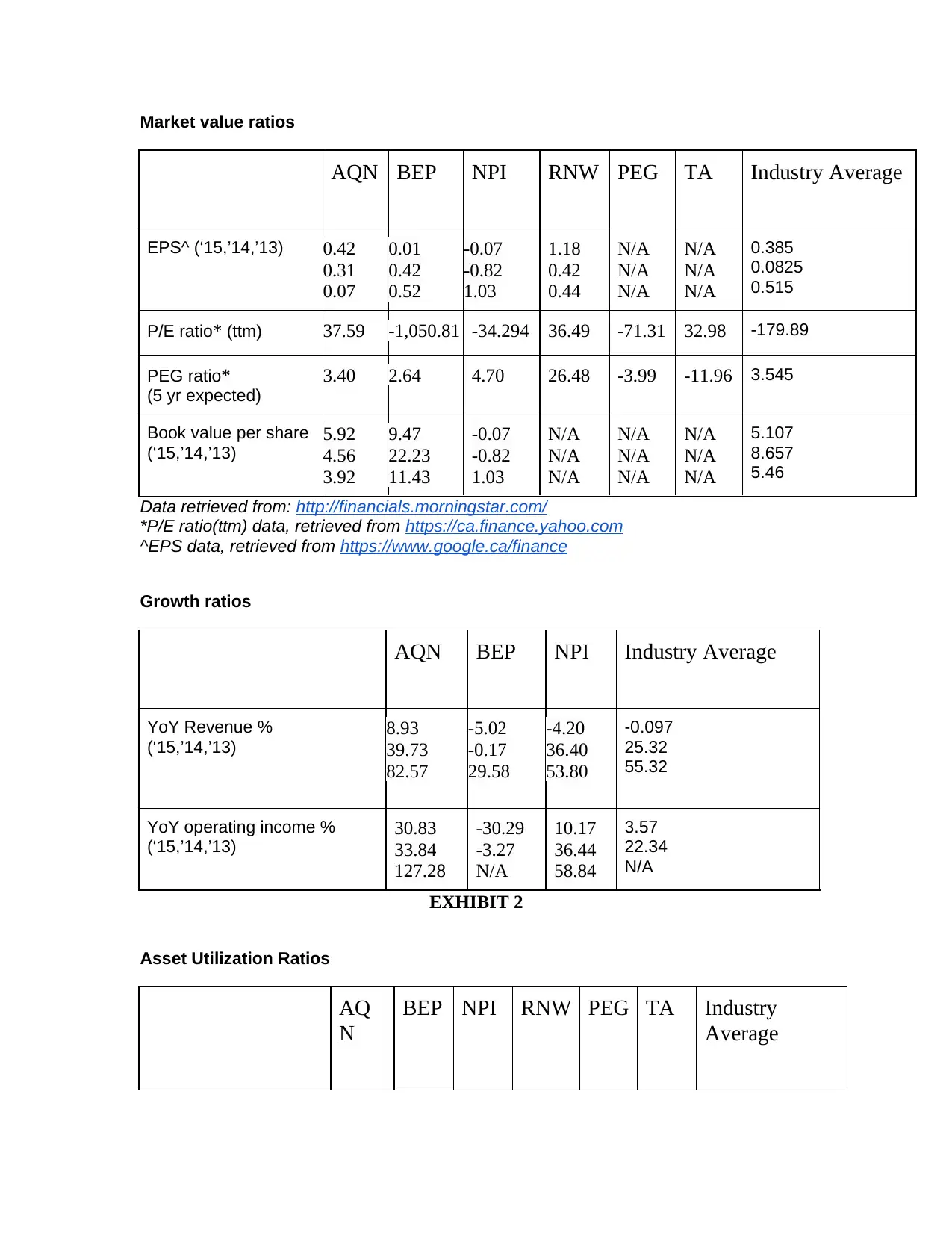

Return on Equity, the Equity Multiplier, and the DuPont Identity

The ROE can be leveraged up by increasing the amount of debt AQN holds. This

happens when the interest rate of these loans are higher than the return on assets.

Despite taking large amounts of debt in 2014 and 2015, this is not the case for AQN; the

interest rate is lower than the return on assets. AQN shows strength relative to the

industry average in avoiding increased leverage. Also, the equity multiplier is below the

industry average. This means AQN holds more assets relative to its equity than normal

or that AQN has less risk in regards to debt financing.

Profit Margin Total Asset Turnover Equity Multiplier ROE

10.42 X 0.23 X 2.95 = 7.08 (2015)

7.02 X 0.25 X 3.52 = 6.17 (2014)

3.01 X 0.25 X 3.75 = 2.48 (2013)

This comparison shows that the improvement in ROE was mainly caused by AQN’s

growing profit margin.

Market value ratios

AQN’s earnings per share (EPS) has been on a gradual rise since 2013. In the past two

years their EPS has exceeded the industry average. Therefore, this is a good indication

the AQN is doing well compared to their competitors, and they should continue doing

well in the future. AQN’s price to earnings ratio for the past 12 months is doing

exceedingly well compared to the industry average. Thus this is another very good sign

The ROE can be leveraged up by increasing the amount of debt AQN holds. This

happens when the interest rate of these loans are higher than the return on assets.

Despite taking large amounts of debt in 2014 and 2015, this is not the case for AQN; the

interest rate is lower than the return on assets. AQN shows strength relative to the

industry average in avoiding increased leverage. Also, the equity multiplier is below the

industry average. This means AQN holds more assets relative to its equity than normal

or that AQN has less risk in regards to debt financing.

Profit Margin Total Asset Turnover Equity Multiplier ROE

10.42 X 0.23 X 2.95 = 7.08 (2015)

7.02 X 0.25 X 3.52 = 6.17 (2014)

3.01 X 0.25 X 3.75 = 2.48 (2013)

This comparison shows that the improvement in ROE was mainly caused by AQN’s

growing profit margin.

Market value ratios

AQN’s earnings per share (EPS) has been on a gradual rise since 2013. In the past two

years their EPS has exceeded the industry average. Therefore, this is a good indication

the AQN is doing well compared to their competitors, and they should continue doing

well in the future. AQN’s price to earnings ratio for the past 12 months is doing

exceedingly well compared to the industry average. Thus this is another very good sign

for the company. AQN’s price an earnings to growth over the next 5 years (PEG ratio)

is slightly under industry average, but it still has strong growth potential. Refer to

exhibit x for financial details.

Growth ratios

The growth ratios for AQN look very good compared to the industry average. AQN

experienced rapid growth for year-over-year (YoY) revenue and operating income. This

growth has been in a downward decline since 2013, but in 2015 the YoY revenue and

operating income was still much higher than the industry average. This is a good sign,

as it shows AQN still has many years ahead of it in growth, as its largest competitor has

experienced negative growth for the past two years, while NPI (AQN’s next competitor)

recently in 2015 experienced negative revenue growth. Refer to exhibit x for financial

details.

The total debt ratio: AQN’s use of debt has declined over 3 years and is lower than the

industry average.

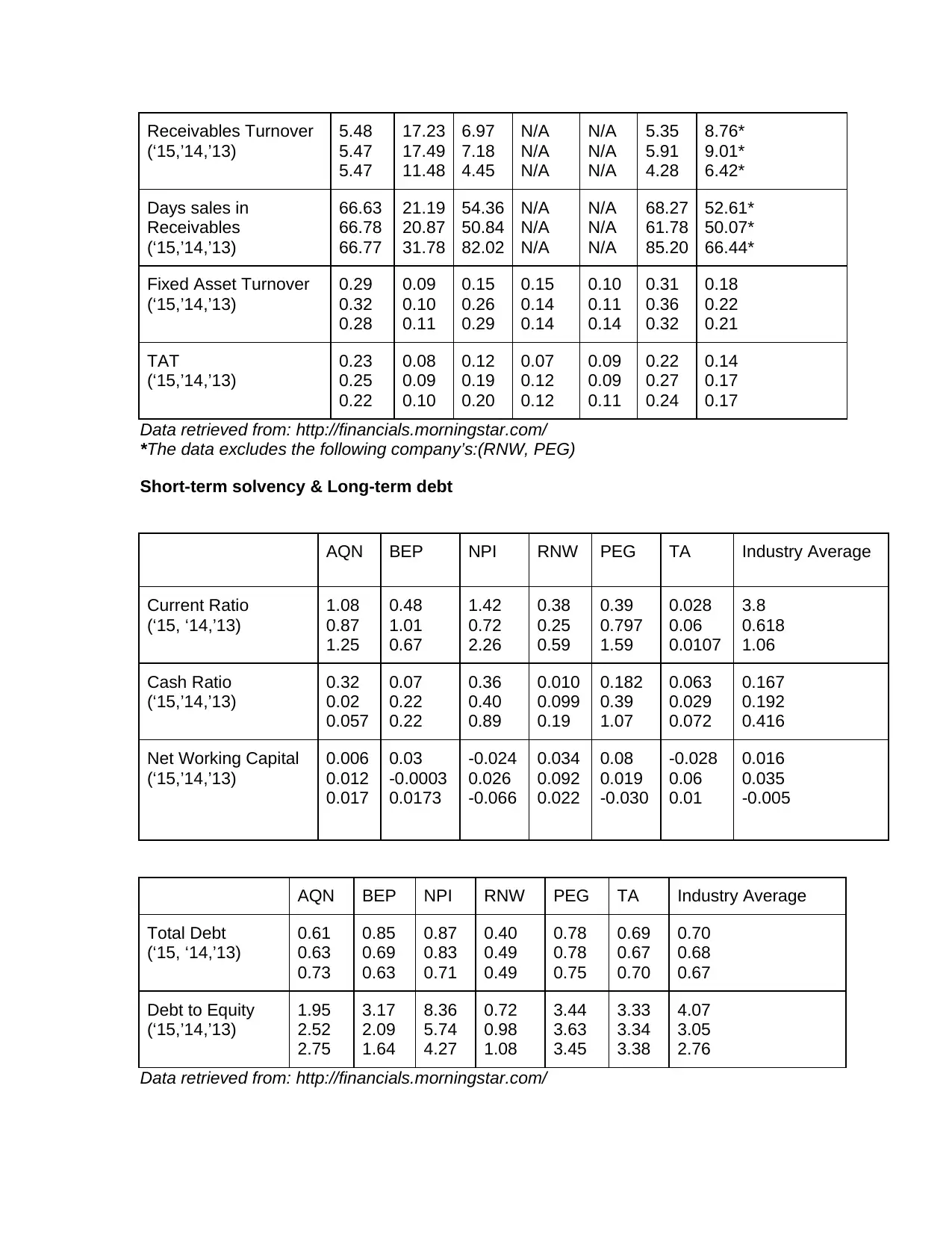

Asset Utilization Ratios Analysis

From a three-year industry average we can see that AQN has been the most

effective with the uses of their assets. Relative to companies with similar size and market

capitalization (PEG, RNW, NPI), AQN is more than double than the three leading

competitors. AQN has the highest TAT in its last year and second highest FAT in 2015.

We can see that the company uses its assets to increase its revenue by the greatest amount

in the same market capitalization. AQN also has one of the lowest receivable turn ratios.

This mean that they are able to get their money faster than most companies in their

is slightly under industry average, but it still has strong growth potential. Refer to

exhibit x for financial details.

Growth ratios

The growth ratios for AQN look very good compared to the industry average. AQN

experienced rapid growth for year-over-year (YoY) revenue and operating income. This

growth has been in a downward decline since 2013, but in 2015 the YoY revenue and

operating income was still much higher than the industry average. This is a good sign,

as it shows AQN still has many years ahead of it in growth, as its largest competitor has

experienced negative growth for the past two years, while NPI (AQN’s next competitor)

recently in 2015 experienced negative revenue growth. Refer to exhibit x for financial

details.

The total debt ratio: AQN’s use of debt has declined over 3 years and is lower than the

industry average.

Asset Utilization Ratios Analysis

From a three-year industry average we can see that AQN has been the most

effective with the uses of their assets. Relative to companies with similar size and market

capitalization (PEG, RNW, NPI), AQN is more than double than the three leading

competitors. AQN has the highest TAT in its last year and second highest FAT in 2015.

We can see that the company uses its assets to increase its revenue by the greatest amount

in the same market capitalization. AQN also has one of the lowest receivable turn ratios.

This mean that they are able to get their money faster than most companies in their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

industry and are able to put that money back into the company to grow. Based on the data

from exhibit ( ) we can see that the company has room to grow and get a larger market

capital in the years to come.

Short-term solvency & Long-term debt

Analyzing AQN’s short-term solvency and long-term debt ratios while comparing the

numbers to industry averages can aid investors on future decisions. According to the data

above, Algonquin Power and Utilities Corp has the second highest current ratio compared

to its competitors. With a ratio over one, investors are able to conclude that the company

is able to pay its current obligations. Firm’s that are in this industry particularly have high

liabilities and debt which decreases the current ratio figures. Similarly, the cash ratio also

indicates the company’s capabilities to pay off obligations using only cash or cash

equivalents. The chart above indicates that AQN and its competitors are not able to pay

off these debts with cash since the ratio is less than one. However, this does not

effectively illustrate whether these firms are successful or not, since utility businesses in

North America typically can not achieve a cash ratio valued over one. In terms of total

debt, a lower ratio is more favourable than a high ratio, which shows that AQN is a stable

business with future growth opportunities. Referring to exhbit X, AQN has the second

lowest debt ratio out of the top competitors.

Conclusion:

from exhibit ( ) we can see that the company has room to grow and get a larger market

capital in the years to come.

Short-term solvency & Long-term debt

Analyzing AQN’s short-term solvency and long-term debt ratios while comparing the

numbers to industry averages can aid investors on future decisions. According to the data

above, Algonquin Power and Utilities Corp has the second highest current ratio compared

to its competitors. With a ratio over one, investors are able to conclude that the company

is able to pay its current obligations. Firm’s that are in this industry particularly have high

liabilities and debt which decreases the current ratio figures. Similarly, the cash ratio also

indicates the company’s capabilities to pay off obligations using only cash or cash

equivalents. The chart above indicates that AQN and its competitors are not able to pay

off these debts with cash since the ratio is less than one. However, this does not

effectively illustrate whether these firms are successful or not, since utility businesses in

North America typically can not achieve a cash ratio valued over one. In terms of total

debt, a lower ratio is more favourable than a high ratio, which shows that AQN is a stable

business with future growth opportunities. Referring to exhbit X, AQN has the second

lowest debt ratio out of the top competitors.

Conclusion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXHIBIT 1

Competitors:

Corporation Name Ticker Market Cap*

Competitors:

Corporation Name Ticker Market Cap*

0 Algonquin Power & Utilities AQN $2,921,731,203

1 Brookfield Renewable Partners LP BEP $6,213,196,399

2 Northland Power Inc. NPI $3,729,057,440

3 TransAlta Renewables Inc. RNW $2,906,957,760

4 Pattern Energy Group Inc. PEG $2,275,984,100

5 TransAlta Corp. TA $1,528,767,410

*Current as of market close Nov. 11/2016. Data from

http://web.tmxmoney.com/

NOTE: all stocks trade on Toronto Stock Exchange (TSX)

NOTE:

The abbreviation of “N/A” means the number is not available.

Profitability Ratios

AQN BEP NPI RNW PEG TA Industry

Average

Profit Margin (%)

(‘15,’14,’13)

10.42

7.02

3.01

0.12

3.38

4.02

0.16

-14.02

24.63*

0.83

0.21

0.2

-0.10

-0.12

0.08

-1.06

5.38

-3.10

1.73

0.31 (3.17)*

4.81(1.80)*

Return on Assets

(%)

(‘15,’14,’13)

2.35

1.75

0.65

0.01

0.32

0.41

0.02

-2.66

4.94

0.06

0.02

0.02

-0.009

-0.011

0.009

-0.23

1.44

-0.74

0.37

0.14

0.88

Return on Equity (%)

(‘15,’14,’13)

Equity Multiplier

(‘15,’14,’13)

7.08

6.17

2.48

2.95

3.52

3.75

0.04

0.94

1.06

4.17

3.09

2.64

0.18

-17.95

25.98*

9.36

6.74

5.27

0.1

0.05

0.05

1.72

1.98

2.08

-0.04

-0.05

0.04

4.44

4.63

4.45

-1.01

6.31

-3.26

4.33

4.34

4.38

1.05

-0.76

4.39(0.95)*

4.50

4.05

3.88

*Industry averages with outliers removed. Drastic numbers are likely a product of

accounting changes, not performance changes

Data retrieved from: http://financials.morningstar.com/

1 Brookfield Renewable Partners LP BEP $6,213,196,399

2 Northland Power Inc. NPI $3,729,057,440

3 TransAlta Renewables Inc. RNW $2,906,957,760

4 Pattern Energy Group Inc. PEG $2,275,984,100

5 TransAlta Corp. TA $1,528,767,410

*Current as of market close Nov. 11/2016. Data from

http://web.tmxmoney.com/

NOTE: all stocks trade on Toronto Stock Exchange (TSX)

NOTE:

The abbreviation of “N/A” means the number is not available.

Profitability Ratios

AQN BEP NPI RNW PEG TA Industry

Average

Profit Margin (%)

(‘15,’14,’13)

10.42

7.02

3.01

0.12

3.38

4.02

0.16

-14.02

24.63*

0.83

0.21

0.2

-0.10

-0.12

0.08

-1.06

5.38

-3.10

1.73

0.31 (3.17)*

4.81(1.80)*

Return on Assets

(%)

(‘15,’14,’13)

2.35

1.75

0.65

0.01

0.32

0.41

0.02

-2.66

4.94

0.06

0.02

0.02

-0.009

-0.011

0.009

-0.23

1.44

-0.74

0.37

0.14

0.88

Return on Equity (%)

(‘15,’14,’13)

Equity Multiplier

(‘15,’14,’13)

7.08

6.17

2.48

2.95

3.52

3.75

0.04

0.94

1.06

4.17

3.09

2.64

0.18

-17.95

25.98*

9.36

6.74

5.27

0.1

0.05

0.05

1.72

1.98

2.08

-0.04

-0.05

0.04

4.44

4.63

4.45

-1.01

6.31

-3.26

4.33

4.34

4.38

1.05

-0.76

4.39(0.95)*

4.50

4.05

3.88

*Industry averages with outliers removed. Drastic numbers are likely a product of

accounting changes, not performance changes

Data retrieved from: http://financials.morningstar.com/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Market value ratios

AQN BEP NPI RNW PEG TA Industry Average

EPS^ (‘15,’14,’13) 0.42

0.31

0.07

0.01

0.42

0.52

-0.07

-0.82

1.03

1.18

0.42

0.44

N/A

N/A

N/A

N/A

N/A

N/A

0.385

0.0825

0.515

P/E ratio* (ttm) 37.59 -1,050.81 -34.294 36.49 -71.31 32.98 -179.89

PEG ratio*

(5 yr expected)

3.40 2.64 4.70 26.48 -3.99 -11.96 3.545

Book value per share

(‘15,’14,’13)

5.92

4.56

3.92

9.47

22.23

11.43

-0.07

-0.82

1.03

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

5.107

8.657

5.46

Data retrieved from: http://financials.morningstar.com/

*P/E ratio(ttm) data, retrieved from https://ca.finance.yahoo.com

^EPS data, retrieved from https://www.google.ca/finance

Growth ratios

AQN BEP NPI Industry Average

YoY Revenue %

(‘15,’14,’13)

8.93

39.73

82.57

-5.02

-0.17

29.58

-4.20

36.40

53.80

-0.097

25.32

55.32

YoY operating income %

(‘15,’14,’13)

30.83

33.84

127.28

-30.29

-3.27

N/A

10.17

36.44

58.84

3.57

22.34

N/A

EXHIBIT 2

Asset Utilization Ratios

AQ

N

BEP NPI RNW PEG TA Industry

Average

AQN BEP NPI RNW PEG TA Industry Average

EPS^ (‘15,’14,’13) 0.42

0.31

0.07

0.01

0.42

0.52

-0.07

-0.82

1.03

1.18

0.42

0.44

N/A

N/A

N/A

N/A

N/A

N/A

0.385

0.0825

0.515

P/E ratio* (ttm) 37.59 -1,050.81 -34.294 36.49 -71.31 32.98 -179.89

PEG ratio*

(5 yr expected)

3.40 2.64 4.70 26.48 -3.99 -11.96 3.545

Book value per share

(‘15,’14,’13)

5.92

4.56

3.92

9.47

22.23

11.43

-0.07

-0.82

1.03

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

5.107

8.657

5.46

Data retrieved from: http://financials.morningstar.com/

*P/E ratio(ttm) data, retrieved from https://ca.finance.yahoo.com

^EPS data, retrieved from https://www.google.ca/finance

Growth ratios

AQN BEP NPI Industry Average

YoY Revenue %

(‘15,’14,’13)

8.93

39.73

82.57

-5.02

-0.17

29.58

-4.20

36.40

53.80

-0.097

25.32

55.32

YoY operating income %

(‘15,’14,’13)

30.83

33.84

127.28

-30.29

-3.27

N/A

10.17

36.44

58.84

3.57

22.34

N/A

EXHIBIT 2

Asset Utilization Ratios

AQ

N

BEP NPI RNW PEG TA Industry

Average

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Receivables Turnover

(‘15,’14,’13)

5.48

5.47

5.47

17.23

17.49

11.48

6.97

7.18

4.45

N/A

N/A

N/A

N/A

N/A

N/A

5.35

5.91

4.28

8.76*

9.01*

6.42*

Days sales in

Receivables

(‘15,’14,’13)

66.63

66.78

66.77

21.19

20.87

31.78

54.36

50.84

82.02

N/A

N/A

N/A

N/A

N/A

N/A

68.27

61.78

85.20

52.61*

50.07*

66.44*

Fixed Asset Turnover

(‘15,’14,’13)

0.29

0.32

0.28

0.09

0.10

0.11

0.15

0.26

0.29

0.15

0.14

0.14

0.10

0.11

0.14

0.31

0.36

0.32

0.18

0.22

0.21

TAT

(‘15,’14,’13)

0.23

0.25

0.22

0.08

0.09

0.10

0.12

0.19

0.20

0.07

0.12

0.12

0.09

0.09

0.11

0.22

0.27

0.24

0.14

0.17

0.17

Data retrieved from: http://financials.morningstar.com/

*The data excludes the following company’s:(RNW, PEG)

Short-term solvency & Long-term debt

AQN BEP NPI RNW PEG TA Industry Average

Current Ratio

(‘15, ‘14,’13)

1.08

0.87

1.25

0.48

1.01

0.67

1.42

0.72

2.26

0.38

0.25

0.59

0.39

0.797

1.59

0.028

0.06

0.0107

3.8

0.618

1.06

Cash Ratio

(‘15,’14,’13)

0.32

0.02

0.057

0.07

0.22

0.22

0.36

0.40

0.89

0.010

0.099

0.19

0.182

0.39

1.07

0.063

0.029

0.072

0.167

0.192

0.416

Net Working Capital

(‘15,’14,’13)

0.006

0.012

0.017

0.03

-0.0003

0.0173

-0.024

0.026

-0.066

0.034

0.092

0.022

0.08

0.019

-0.030

-0.028

0.06

0.01

0.016

0.035

-0.005

AQN BEP NPI RNW PEG TA Industry Average

Total Debt

(‘15, ‘14,’13)

0.61

0.63

0.73

0.85

0.69

0.63

0.87

0.83

0.71

0.40

0.49

0.49

0.78

0.78

0.75

0.69

0.67

0.70

0.70

0.68

0.67

Debt to Equity

(‘15,’14,’13)

1.95

2.52

2.75

3.17

2.09

1.64

8.36

5.74

4.27

0.72

0.98

1.08

3.44

3.63

3.45

3.33

3.34

3.38

4.07

3.05

2.76

Data retrieved from: http://financials.morningstar.com/

(‘15,’14,’13)

5.48

5.47

5.47

17.23

17.49

11.48

6.97

7.18

4.45

N/A

N/A

N/A

N/A

N/A

N/A

5.35

5.91

4.28

8.76*

9.01*

6.42*

Days sales in

Receivables

(‘15,’14,’13)

66.63

66.78

66.77

21.19

20.87

31.78

54.36

50.84

82.02

N/A

N/A

N/A

N/A

N/A

N/A

68.27

61.78

85.20

52.61*

50.07*

66.44*

Fixed Asset Turnover

(‘15,’14,’13)

0.29

0.32

0.28

0.09

0.10

0.11

0.15

0.26

0.29

0.15

0.14

0.14

0.10

0.11

0.14

0.31

0.36

0.32

0.18

0.22

0.21

TAT

(‘15,’14,’13)

0.23

0.25

0.22

0.08

0.09

0.10

0.12

0.19

0.20

0.07

0.12

0.12

0.09

0.09

0.11

0.22

0.27

0.24

0.14

0.17

0.17

Data retrieved from: http://financials.morningstar.com/

*The data excludes the following company’s:(RNW, PEG)

Short-term solvency & Long-term debt

AQN BEP NPI RNW PEG TA Industry Average

Current Ratio

(‘15, ‘14,’13)

1.08

0.87

1.25

0.48

1.01

0.67

1.42

0.72

2.26

0.38

0.25

0.59

0.39

0.797

1.59

0.028

0.06

0.0107

3.8

0.618

1.06

Cash Ratio

(‘15,’14,’13)

0.32

0.02

0.057

0.07

0.22

0.22

0.36

0.40

0.89

0.010

0.099

0.19

0.182

0.39

1.07

0.063

0.029

0.072

0.167

0.192

0.416

Net Working Capital

(‘15,’14,’13)

0.006

0.012

0.017

0.03

-0.0003

0.0173

-0.024

0.026

-0.066

0.034

0.092

0.022

0.08

0.019

-0.030

-0.028

0.06

0.01

0.016

0.035

-0.005

AQN BEP NPI RNW PEG TA Industry Average

Total Debt

(‘15, ‘14,’13)

0.61

0.63

0.73

0.85

0.69

0.63

0.87

0.83

0.71

0.40

0.49

0.49

0.78

0.78

0.75

0.69

0.67

0.70

0.70

0.68

0.67

Debt to Equity

(‘15,’14,’13)

1.95

2.52

2.75

3.17

2.09

1.64

8.36

5.74

4.27

0.72

0.98

1.08

3.44

3.63

3.45

3.33

3.34

3.38

4.07

3.05

2.76

Data retrieved from: http://financials.morningstar.com/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.