Course of Taxation Law 2022

Added on 2022-10-09

19 Pages3678 Words21 Views

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

TAXATION LAW1

Table of Contents

Answer to question 1:.................................................................................................................2

Requirement A:......................................................................................................................2

Requirement B:......................................................................................................................2

Requirement C:......................................................................................................................2

Requirement D:......................................................................................................................3

Requirement E:.......................................................................................................................3

Requirement F:.......................................................................................................................3

Requirement G:..........................................................................................................................3

Requirement H:......................................................................................................................4

Requirement I:........................................................................................................................4

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................7

Answer to question 4:...............................................................................................................11

Answer to A:........................................................................................................................11

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................11

Answer to D:........................................................................................................................12

Answer to question 5:...............................................................................................................13

Answer A:............................................................................................................................13

Answer B:.............................................................................................................................13

Table of Contents

Answer to question 1:.................................................................................................................2

Requirement A:......................................................................................................................2

Requirement B:......................................................................................................................2

Requirement C:......................................................................................................................2

Requirement D:......................................................................................................................3

Requirement E:.......................................................................................................................3

Requirement F:.......................................................................................................................3

Requirement G:..........................................................................................................................3

Requirement H:......................................................................................................................4

Requirement I:........................................................................................................................4

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................7

Answer to question 4:...............................................................................................................11

Answer to A:........................................................................................................................11

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................11

Answer to D:........................................................................................................................12

Answer to question 5:...............................................................................................................13

Answer A:............................................................................................................................13

Answer B:.............................................................................................................................13

TAXATION LAW2

Answer to C:........................................................................................................................14

Answer to D:........................................................................................................................14

Answer to E:.........................................................................................................................15

References:...............................................................................................................................16

Answer to C:........................................................................................................................14

Answer to D:........................................................................................................................14

Answer to E:.........................................................................................................................15

References:...............................................................................................................................16

TAXATION LAW3

Answer to question 1:

Requirement A:

The “Taxation Ruling of TR 2019/1” lay down the commissioner views on when the

company conducts its business inside the connotation of small business entity under the “sec-

25, ITRA 1986” as applied in 2015-16 and 2016-17 years of income and “sec-328-110, ITAA

1997”1.

Requirement B:

Explanations relating to the deductions of gifts or contributions has been explained

under the “Division 30, ITAA 1997”2.

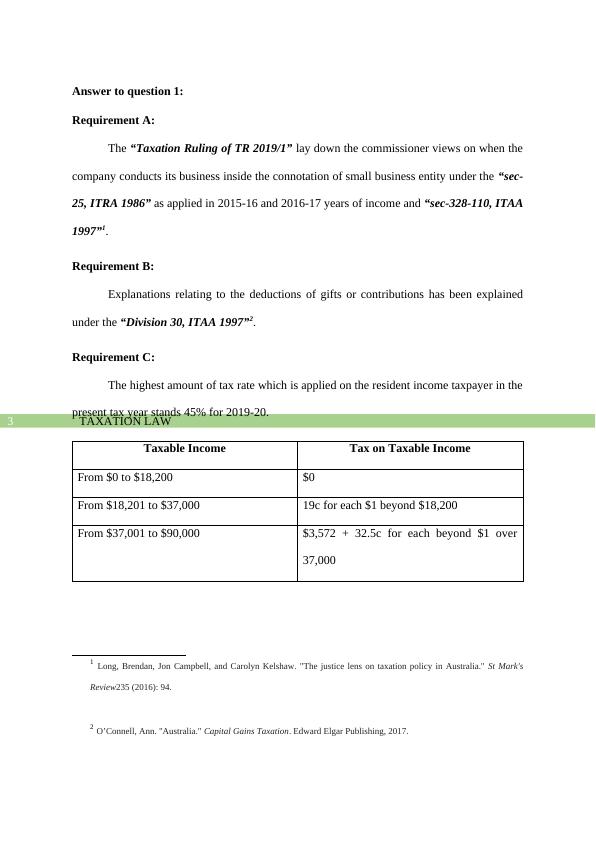

Requirement C:

The highest amount of tax rate which is applied on the resident income taxpayer in the

present tax year stands 45% for 2019-20.

Taxable Income Tax on Taxable Income

From $0 to $18,200 $0

From $18,201 to $37,000 19c for each $1 beyond $18,200

From $37,001 to $90,000 $3,572 + 32.5c for each beyond $1 over

37,000

1 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in Australia." St Mark's

Review235 (2016): 94.

2 O’Connell, Ann. "Australia." Capital Gains Taxation. Edward Elgar Publishing, 2017.

Answer to question 1:

Requirement A:

The “Taxation Ruling of TR 2019/1” lay down the commissioner views on when the

company conducts its business inside the connotation of small business entity under the “sec-

25, ITRA 1986” as applied in 2015-16 and 2016-17 years of income and “sec-328-110, ITAA

1997”1.

Requirement B:

Explanations relating to the deductions of gifts or contributions has been explained

under the “Division 30, ITAA 1997”2.

Requirement C:

The highest amount of tax rate which is applied on the resident income taxpayer in the

present tax year stands 45% for 2019-20.

Taxable Income Tax on Taxable Income

From $0 to $18,200 $0

From $18,201 to $37,000 19c for each $1 beyond $18,200

From $37,001 to $90,000 $3,572 + 32.5c for each beyond $1 over

37,000

1 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in Australia." St Mark's

Review235 (2016): 94.

2 O’Connell, Ann. "Australia." Capital Gains Taxation. Edward Elgar Publishing, 2017.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Answer to question 1: Taxation Law Name of the University Authors' Namelg...

|17

|3562

|242

Taxation Lawlg...

|21

|4006

|65

Answer to question 1: Taxation Law Name of the University Authors' Namelg...

|16

|3607

|257

Assignment (doc) | Taxation Lawlg...

|20

|4272

|42

Taxation Law 2022 Question Answerlg...

|18

|3538

|24

Taxation Lawlg...

|20

|4118

|77