Answer to question 1: Taxation Law Name of the University Authors' Name

Added on 2022-10-16

16 Pages3607 Words257 Views

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

TAXATION LAW1

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................7

Answer to question 4:...............................................................................................................10

Answer to A:........................................................................................................................10

Answer to B:........................................................................................................................10

Answer to C:........................................................................................................................10

Answer to D:........................................................................................................................11

Answer to question 5:...............................................................................................................11

Answer A:............................................................................................................................11

Answer B:.............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................7

Answer to question 4:...............................................................................................................10

Answer to A:........................................................................................................................10

Answer to B:........................................................................................................................10

Answer to C:........................................................................................................................10

Answer to D:........................................................................................................................11

Answer to question 5:...............................................................................................................11

Answer A:............................................................................................................................11

Answer B:.............................................................................................................................11

TAXATION LAW2

Answer to C:........................................................................................................................12

Answer to D:........................................................................................................................12

Answer to E:.........................................................................................................................13

References:...............................................................................................................................14

Answer to C:........................................................................................................................12

Answer to D:........................................................................................................................12

Answer to E:.........................................................................................................................13

References:...............................................................................................................................14

TAXATION LAW3

Answer to question 1:

Answer A:

The taxation ruling of TR 2019/1 lay down the views of commissioner on when the

company conducts a business inside the sense of small business entity within the section 23,

“Income Tax Rates Act 1986” as the application in the income years of 2015-16 and 2016-17

or inside the “section 328-110, ITAA 1997”.

Answer B:

“Division 30, ITAA 1997” summaries the legislation relating to deductibility of gifts

or contributions.

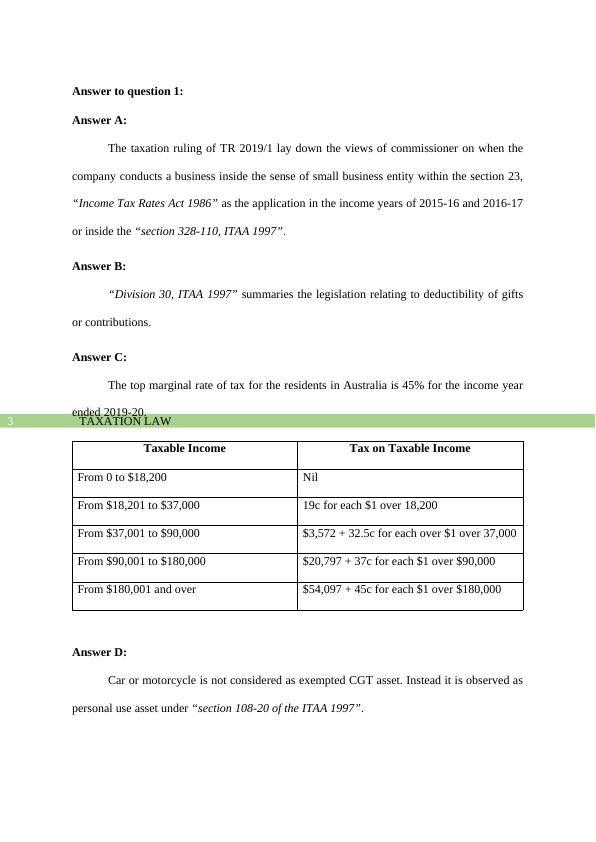

Answer C:

The top marginal rate of tax for the residents in Australia is 45% for the income year

ended 2019-20.

Taxable Income Tax on Taxable Income

From 0 to $18,200 Nil

From $18,201 to $37,000 19c for each $1 over 18,200

From $37,001 to $90,000 $3,572 + 32.5c for each over $1 over 37,000

From $90,001 to $180,000 $20,797 + 37c for each $1 over $90,000

From $180,001 and over $54,097 + 45c for each $1 over $180,000

Answer D:

Car or motorcycle is not considered as exempted CGT asset. Instead it is observed as

personal use asset under “section 108-20 of the ITAA 1997”.

Answer to question 1:

Answer A:

The taxation ruling of TR 2019/1 lay down the views of commissioner on when the

company conducts a business inside the sense of small business entity within the section 23,

“Income Tax Rates Act 1986” as the application in the income years of 2015-16 and 2016-17

or inside the “section 328-110, ITAA 1997”.

Answer B:

“Division 30, ITAA 1997” summaries the legislation relating to deductibility of gifts

or contributions.

Answer C:

The top marginal rate of tax for the residents in Australia is 45% for the income year

ended 2019-20.

Taxable Income Tax on Taxable Income

From 0 to $18,200 Nil

From $18,201 to $37,000 19c for each $1 over 18,200

From $37,001 to $90,000 $3,572 + 32.5c for each over $1 over 37,000

From $90,001 to $180,000 $20,797 + 37c for each $1 over $90,000

From $180,001 and over $54,097 + 45c for each $1 over $180,000

Answer D:

Car or motorcycle is not considered as exempted CGT asset. Instead it is observed as

personal use asset under “section 108-20 of the ITAA 1997”.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Answer to question 1: Taxation Law Name of the University Authors' Namelg...

|17

|3562

|242

Assignment (Doc) | Taxation Lawlg...

|19

|3343

|26

Course of Taxation Law 2022lg...

|19

|3678

|21

Taxation Law 2022 Question Answerlg...

|18

|3538

|24

Assignment (doc) | Taxation Lawlg...

|20

|4272

|42

Taxaxtion Law Question Answer 2022lg...

|19

|3519

|12