Financial Analysis of Company Valuation using DDM and DuPont Approach

VerifiedAdded on 2020/12/10

|44

|14181

|485

Project

AI Summary

This assignment presents a comprehensive company valuation analysis, employing the Dividend Discount Model (DDM) and DuPont analysis to assess financial performance and determine intrinsic value. The project begins with an examination of the DuPont model, calculating Return on Equity (ROE) for Flight Centre Travel Group (FLT), Webjet, and Hello World from 2014 to 2018. This includes detailed calculations of profit margin, asset turnover, and financial leverage. The second part of the assignment focuses on estimating share price using the DDM, calculating the cost of equity and the current stock value. The analysis includes dividend forecasting and sensitivity analysis to evaluate the impact of uncertainties on the valuation. The appendix provides detailed financial data and sensitivity analysis results. The assignment aims to provide a thorough understanding of valuation methodologies and their application in financial analysis.

Company Valuation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

PART 1............................................................................................................................................1

Q.4 Estimating the ROE of the company for five years by using DU PONT ROE approach....1

PART 2............................................................................................................................................2

Q.2 Estimating share price using dividend discount model (DDM) for estimating intrinsic

value of the company...................................................................................................................2

REFERENCES................................................................................................................................4

APPENDIX......................................................................................................................................5

TABLE OF CONTENTS................................................................................................................2

PART 1............................................................................................................................................1

Q.4 Estimating the ROE of the company for five years by using DU PONT ROE approach....1

PART 2............................................................................................................................................2

Q.2 Estimating share price using dividend discount model (DDM) for estimating intrinsic

value of the company...................................................................................................................2

REFERENCES................................................................................................................................4

APPENDIX......................................................................................................................................5

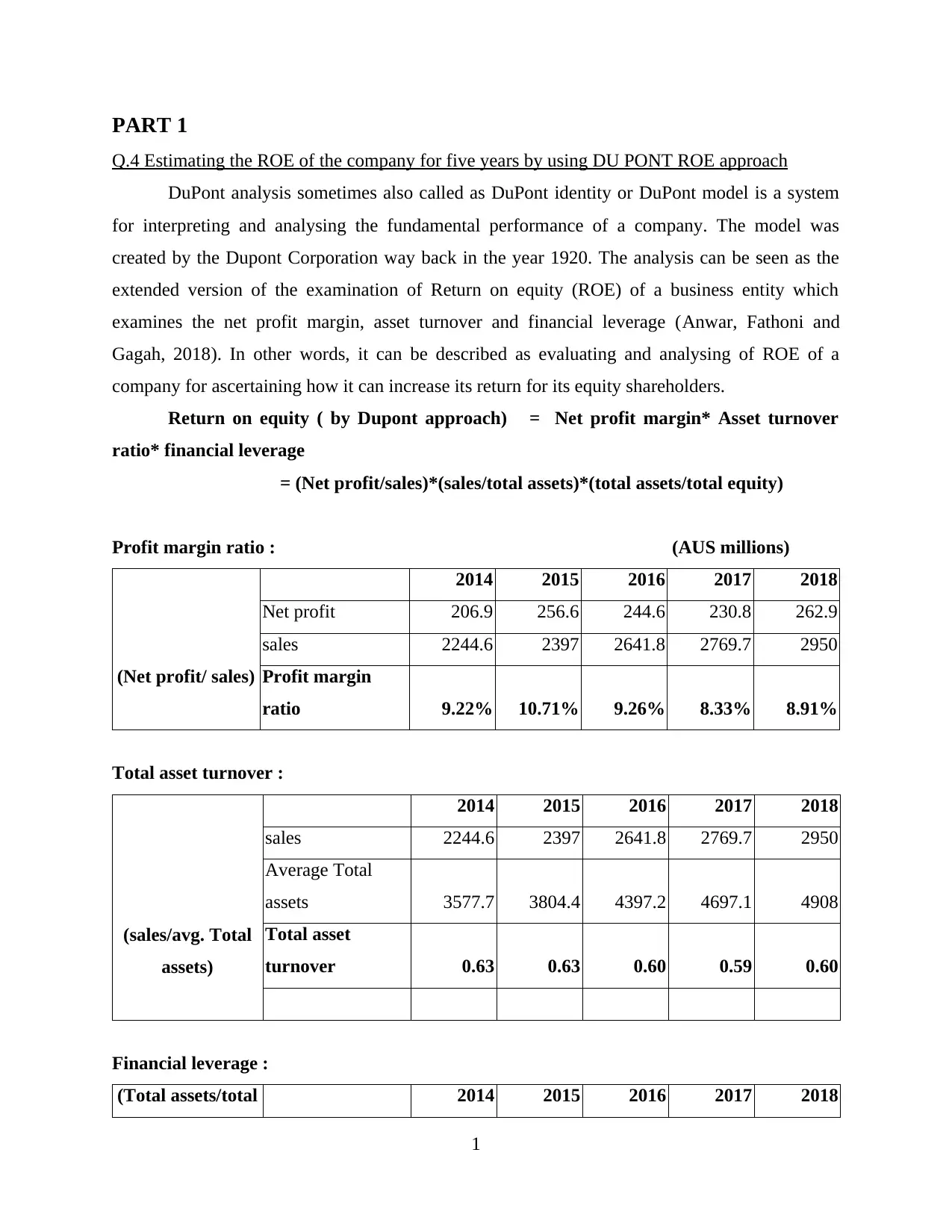

PART 1

Q.4 Estimating the ROE of the company for five years by using DU PONT ROE approach

DuPont analysis sometimes also called as DuPont identity or DuPont model is a system

for interpreting and analysing the fundamental performance of a company. The model was

created by the Dupont Corporation way back in the year 1920. The analysis can be seen as the

extended version of the examination of Return on equity (ROE) of a business entity which

examines the net profit margin, asset turnover and financial leverage (Anwar, Fathoni and

Gagah, 2018). In other words, it can be described as evaluating and analysing of ROE of a

company for ascertaining how it can increase its return for its equity shareholders.

Return on equity ( by Dupont approach) = Net profit margin* Asset turnover

ratio* financial leverage

= (Net profit/sales)*(sales/total assets)*(total assets/total equity)

Profit margin ratio : (AUS millions)

(Net profit/ sales)

2014 2015 2016 2017 2018

Net profit 206.9 256.6 244.6 230.8 262.9

sales 2244.6 2397 2641.8 2769.7 2950

Profit margin

ratio 9.22% 10.71% 9.26% 8.33% 8.91%

Total asset turnover :

(sales/avg. Total

assets)

2014 2015 2016 2017 2018

sales 2244.6 2397 2641.8 2769.7 2950

Average Total

assets 3577.7 3804.4 4397.2 4697.1 4908

Total asset

turnover 0.63 0.63 0.60 0.59 0.60

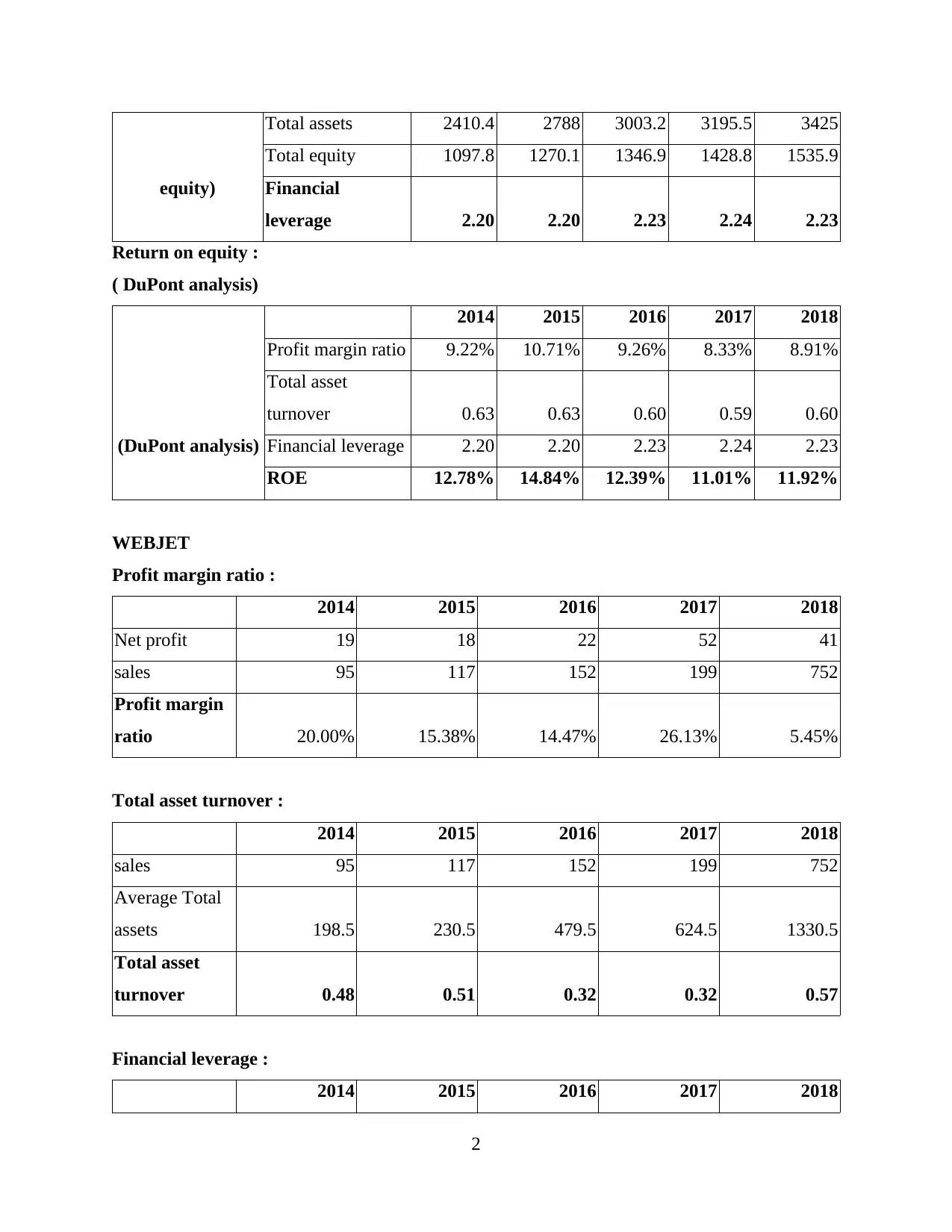

Financial leverage :

(Total assets/total 2014 2015 2016 2017 2018

1

Q.4 Estimating the ROE of the company for five years by using DU PONT ROE approach

DuPont analysis sometimes also called as DuPont identity or DuPont model is a system

for interpreting and analysing the fundamental performance of a company. The model was

created by the Dupont Corporation way back in the year 1920. The analysis can be seen as the

extended version of the examination of Return on equity (ROE) of a business entity which

examines the net profit margin, asset turnover and financial leverage (Anwar, Fathoni and

Gagah, 2018). In other words, it can be described as evaluating and analysing of ROE of a

company for ascertaining how it can increase its return for its equity shareholders.

Return on equity ( by Dupont approach) = Net profit margin* Asset turnover

ratio* financial leverage

= (Net profit/sales)*(sales/total assets)*(total assets/total equity)

Profit margin ratio : (AUS millions)

(Net profit/ sales)

2014 2015 2016 2017 2018

Net profit 206.9 256.6 244.6 230.8 262.9

sales 2244.6 2397 2641.8 2769.7 2950

Profit margin

ratio 9.22% 10.71% 9.26% 8.33% 8.91%

Total asset turnover :

(sales/avg. Total

assets)

2014 2015 2016 2017 2018

sales 2244.6 2397 2641.8 2769.7 2950

Average Total

assets 3577.7 3804.4 4397.2 4697.1 4908

Total asset

turnover 0.63 0.63 0.60 0.59 0.60

Financial leverage :

(Total assets/total 2014 2015 2016 2017 2018

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

equity)

Total assets 2410.4 2788 3003.2 3195.5 3425

Total equity 1097.8 1270.1 1346.9 1428.8 1535.9

Financial

leverage 2.20 2.20 2.23 2.24 2.23

Return on equity :

( DuPont analysis)

(DuPont analysis)

2014 2015 2016 2017 2018

Profit margin ratio 9.22% 10.71% 9.26% 8.33% 8.91%

Total asset

turnover 0.63 0.63 0.60 0.59 0.60

Financial leverage 2.20 2.20 2.23 2.24 2.23

ROE 12.78% 14.84% 12.39% 11.01% 11.92%

WEBJET

Profit margin ratio :

2014 2015 2016 2017 2018

Net profit 19 18 22 52 41

sales 95 117 152 199 752

Profit margin

ratio 20.00% 15.38% 14.47% 26.13% 5.45%

Total asset turnover :

2014 2015 2016 2017 2018

sales 95 117 152 199 752

Average Total

assets 198.5 230.5 479.5 624.5 1330.5

Total asset

turnover 0.48 0.51 0.32 0.32 0.57

Financial leverage :

2014 2015 2016 2017 2018

2

Total assets 2410.4 2788 3003.2 3195.5 3425

Total equity 1097.8 1270.1 1346.9 1428.8 1535.9

Financial

leverage 2.20 2.20 2.23 2.24 2.23

Return on equity :

( DuPont analysis)

(DuPont analysis)

2014 2015 2016 2017 2018

Profit margin ratio 9.22% 10.71% 9.26% 8.33% 8.91%

Total asset

turnover 0.63 0.63 0.60 0.59 0.60

Financial leverage 2.20 2.20 2.23 2.24 2.23

ROE 12.78% 14.84% 12.39% 11.01% 11.92%

WEBJET

Profit margin ratio :

2014 2015 2016 2017 2018

Net profit 19 18 22 52 41

sales 95 117 152 199 752

Profit margin

ratio 20.00% 15.38% 14.47% 26.13% 5.45%

Total asset turnover :

2014 2015 2016 2017 2018

sales 95 117 152 199 752

Average Total

assets 198.5 230.5 479.5 624.5 1330.5

Total asset

turnover 0.48 0.51 0.32 0.32 0.57

Financial leverage :

2014 2015 2016 2017 2018

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

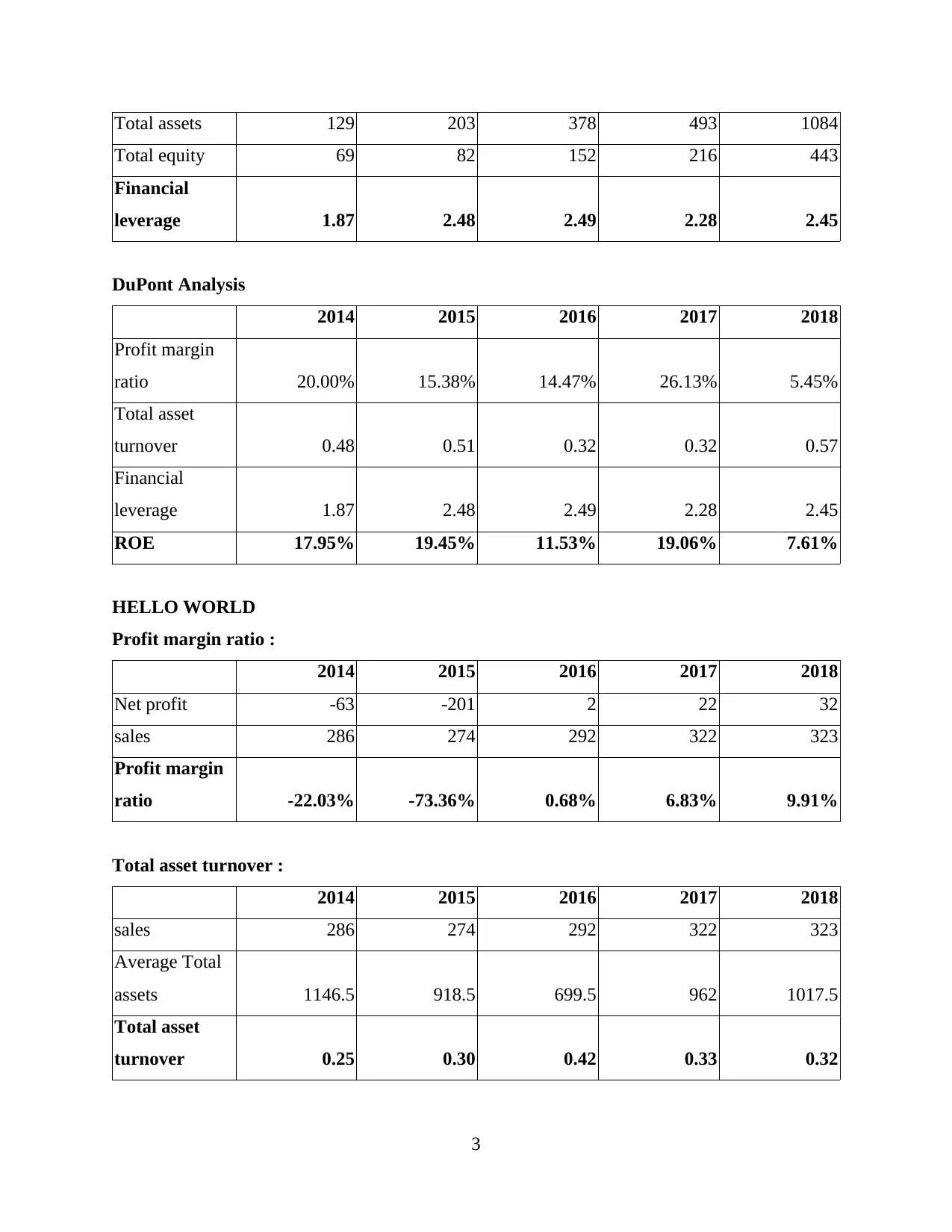

Total assets 129 203 378 493 1084

Total equity 69 82 152 216 443

Financial

leverage 1.87 2.48 2.49 2.28 2.45

DuPont Analysis

2014 2015 2016 2017 2018

Profit margin

ratio 20.00% 15.38% 14.47% 26.13% 5.45%

Total asset

turnover 0.48 0.51 0.32 0.32 0.57

Financial

leverage 1.87 2.48 2.49 2.28 2.45

ROE 17.95% 19.45% 11.53% 19.06% 7.61%

HELLO WORLD

Profit margin ratio :

2014 2015 2016 2017 2018

Net profit -63 -201 2 22 32

sales 286 274 292 322 323

Profit margin

ratio -22.03% -73.36% 0.68% 6.83% 9.91%

Total asset turnover :

2014 2015 2016 2017 2018

sales 286 274 292 322 323

Average Total

assets 1146.5 918.5 699.5 962 1017.5

Total asset

turnover 0.25 0.30 0.42 0.33 0.32

3

Total equity 69 82 152 216 443

Financial

leverage 1.87 2.48 2.49 2.28 2.45

DuPont Analysis

2014 2015 2016 2017 2018

Profit margin

ratio 20.00% 15.38% 14.47% 26.13% 5.45%

Total asset

turnover 0.48 0.51 0.32 0.32 0.57

Financial

leverage 1.87 2.48 2.49 2.28 2.45

ROE 17.95% 19.45% 11.53% 19.06% 7.61%

HELLO WORLD

Profit margin ratio :

2014 2015 2016 2017 2018

Net profit -63 -201 2 22 32

sales 286 274 292 322 323

Profit margin

ratio -22.03% -73.36% 0.68% 6.83% 9.91%

Total asset turnover :

2014 2015 2016 2017 2018

sales 286 274 292 322 323

Average Total

assets 1146.5 918.5 699.5 962 1017.5

Total asset

turnover 0.25 0.30 0.42 0.33 0.32

3

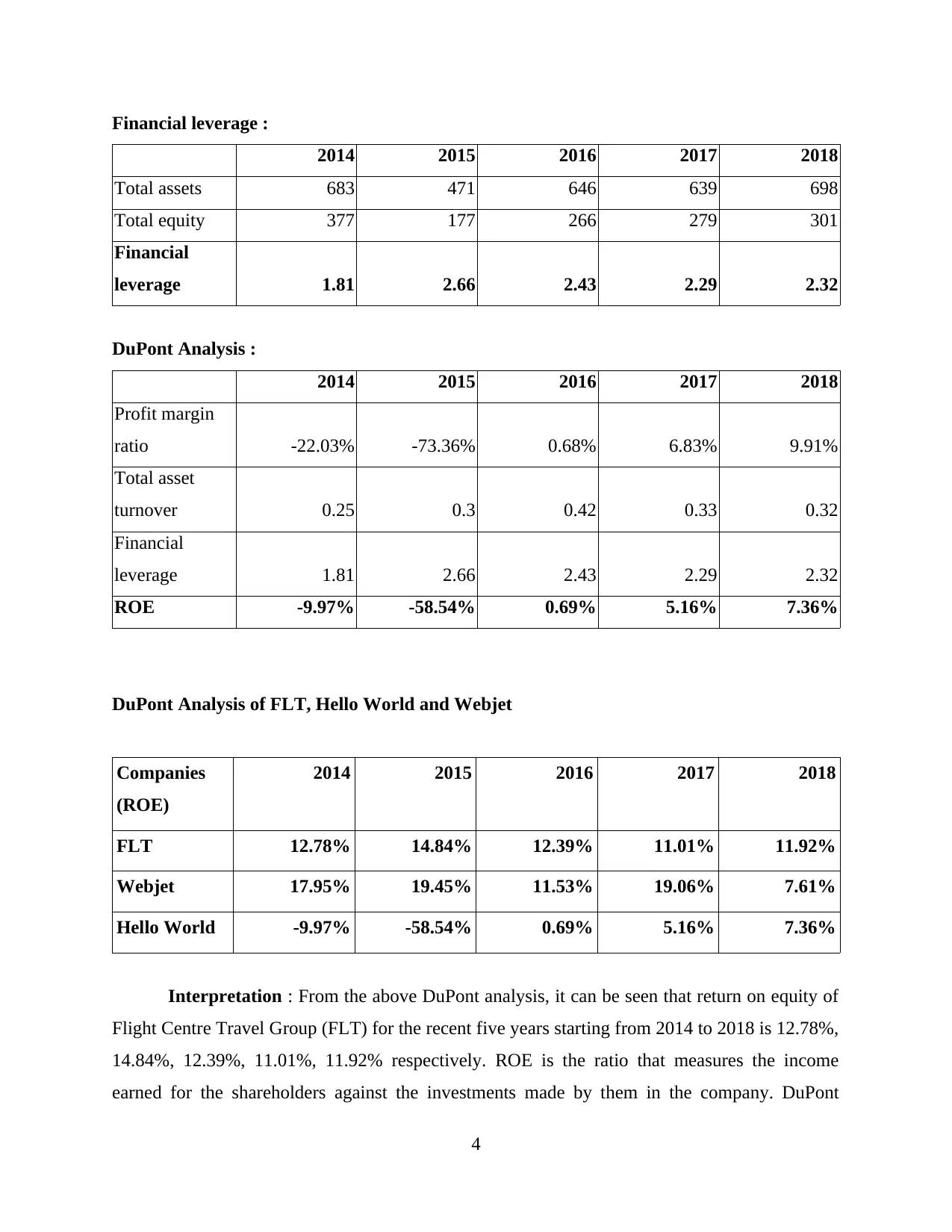

Financial leverage :

2014 2015 2016 2017 2018

Total assets 683 471 646 639 698

Total equity 377 177 266 279 301

Financial

leverage 1.81 2.66 2.43 2.29 2.32

DuPont Analysis :

2014 2015 2016 2017 2018

Profit margin

ratio -22.03% -73.36% 0.68% 6.83% 9.91%

Total asset

turnover 0.25 0.3 0.42 0.33 0.32

Financial

leverage 1.81 2.66 2.43 2.29 2.32

ROE -9.97% -58.54% 0.69% 5.16% 7.36%

DuPont Analysis of FLT, Hello World and Webjet

Companies

(ROE)

2014 2015 2016 2017 2018

FLT 12.78% 14.84% 12.39% 11.01% 11.92%

Webjet 17.95% 19.45% 11.53% 19.06% 7.61%

Hello World -9.97% -58.54% 0.69% 5.16% 7.36%

Interpretation : From the above DuPont analysis, it can be seen that return on equity of

Flight Centre Travel Group (FLT) for the recent five years starting from 2014 to 2018 is 12.78%,

14.84%, 12.39%, 11.01%, 11.92% respectively. ROE is the ratio that measures the income

earned for the shareholders against the investments made by them in the company. DuPont

4

2014 2015 2016 2017 2018

Total assets 683 471 646 639 698

Total equity 377 177 266 279 301

Financial

leverage 1.81 2.66 2.43 2.29 2.32

DuPont Analysis :

2014 2015 2016 2017 2018

Profit margin

ratio -22.03% -73.36% 0.68% 6.83% 9.91%

Total asset

turnover 0.25 0.3 0.42 0.33 0.32

Financial

leverage 1.81 2.66 2.43 2.29 2.32

ROE -9.97% -58.54% 0.69% 5.16% 7.36%

DuPont Analysis of FLT, Hello World and Webjet

Companies

(ROE)

2014 2015 2016 2017 2018

FLT 12.78% 14.84% 12.39% 11.01% 11.92%

Webjet 17.95% 19.45% 11.53% 19.06% 7.61%

Hello World -9.97% -58.54% 0.69% 5.16% 7.36%

Interpretation : From the above DuPont analysis, it can be seen that return on equity of

Flight Centre Travel Group (FLT) for the recent five years starting from 2014 to 2018 is 12.78%,

14.84%, 12.39%, 11.01%, 11.92% respectively. ROE is the ratio that measures the income

earned for the shareholders against the investments made by them in the company. DuPont

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analysis shows the ability of company to increase its return on equity. Operational efficiency is

reflected from this analysis which could be used by investors in assessing the financial efficiency

of the company. ROE was highest in 2015 at 14.84% which means that company earned

impressive income on the investments of the shareholders as compared to other years. After the

2015, ROE has decreased to 11 % approx which depicts that company's income has decreased

owing to high cost of revenue which in turn has reduced the income attributed to the

shareholders in the respective years.

PART 2

Q.2 Estimating share price using dividend discount model (DDM) for estimating intrinsic value

of the company

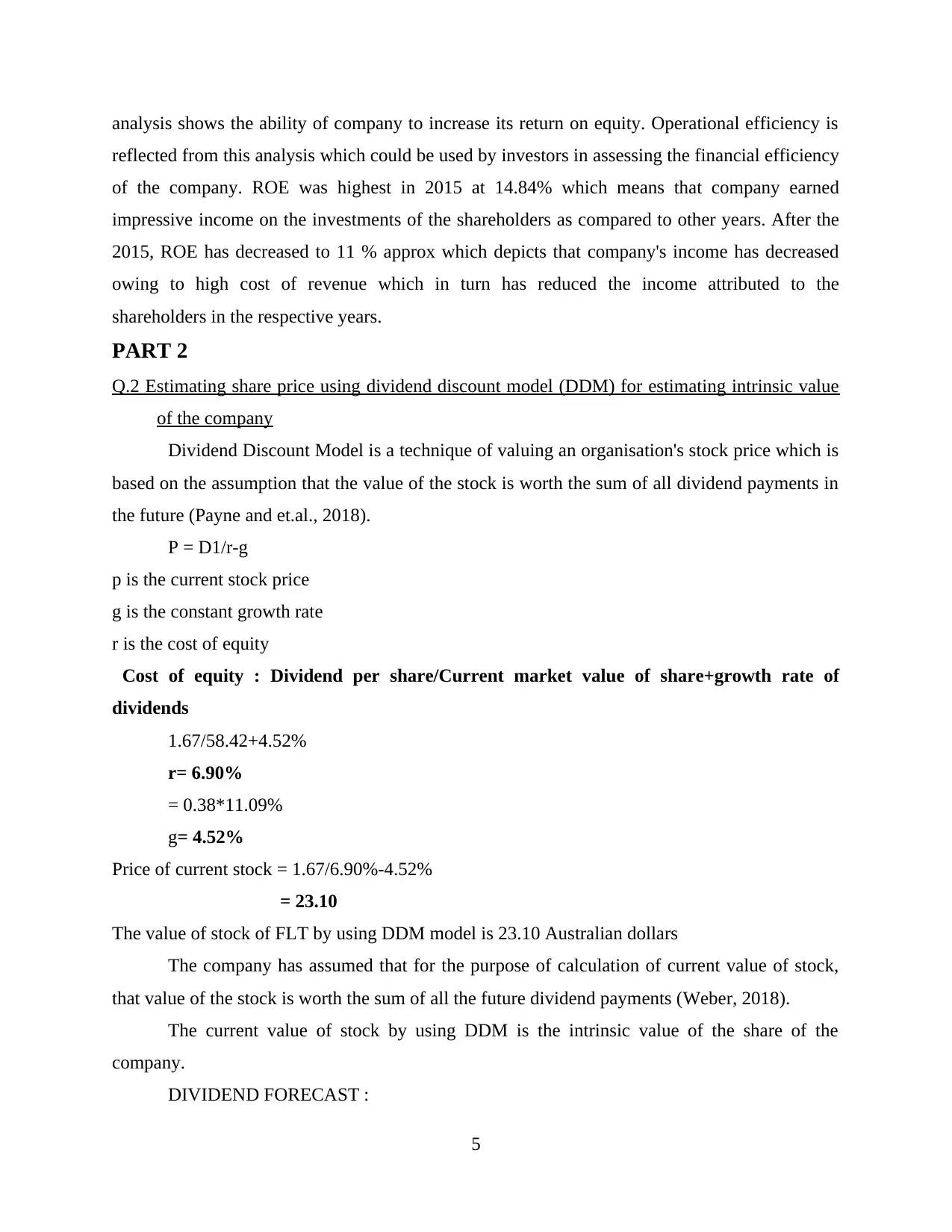

Dividend Discount Model is a technique of valuing an organisation's stock price which is

based on the assumption that the value of the stock is worth the sum of all dividend payments in

the future (Payne and et.al., 2018).

P = D1/r-g

p is the current stock price

g is the constant growth rate

r is the cost of equity

Cost of equity : Dividend per share/Current market value of share+growth rate of

dividends

1.67/58.42+4.52%

r= 6.90%

= 0.38*11.09%

g= 4.52%

Price of current stock = 1.67/6.90%-4.52%

= 23.10

The value of stock of FLT by using DDM model is 23.10 Australian dollars

The company has assumed that for the purpose of calculation of current value of stock,

that value of the stock is worth the sum of all the future dividend payments (Weber, 2018).

The current value of stock by using DDM is the intrinsic value of the share of the

company.

DIVIDEND FORECAST :

5

reflected from this analysis which could be used by investors in assessing the financial efficiency

of the company. ROE was highest in 2015 at 14.84% which means that company earned

impressive income on the investments of the shareholders as compared to other years. After the

2015, ROE has decreased to 11 % approx which depicts that company's income has decreased

owing to high cost of revenue which in turn has reduced the income attributed to the

shareholders in the respective years.

PART 2

Q.2 Estimating share price using dividend discount model (DDM) for estimating intrinsic value

of the company

Dividend Discount Model is a technique of valuing an organisation's stock price which is

based on the assumption that the value of the stock is worth the sum of all dividend payments in

the future (Payne and et.al., 2018).

P = D1/r-g

p is the current stock price

g is the constant growth rate

r is the cost of equity

Cost of equity : Dividend per share/Current market value of share+growth rate of

dividends

1.67/58.42+4.52%

r= 6.90%

= 0.38*11.09%

g= 4.52%

Price of current stock = 1.67/6.90%-4.52%

= 23.10

The value of stock of FLT by using DDM model is 23.10 Australian dollars

The company has assumed that for the purpose of calculation of current value of stock,

that value of the stock is worth the sum of all the future dividend payments (Weber, 2018).

The current value of stock by using DDM is the intrinsic value of the share of the

company.

DIVIDEND FORECAST :

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

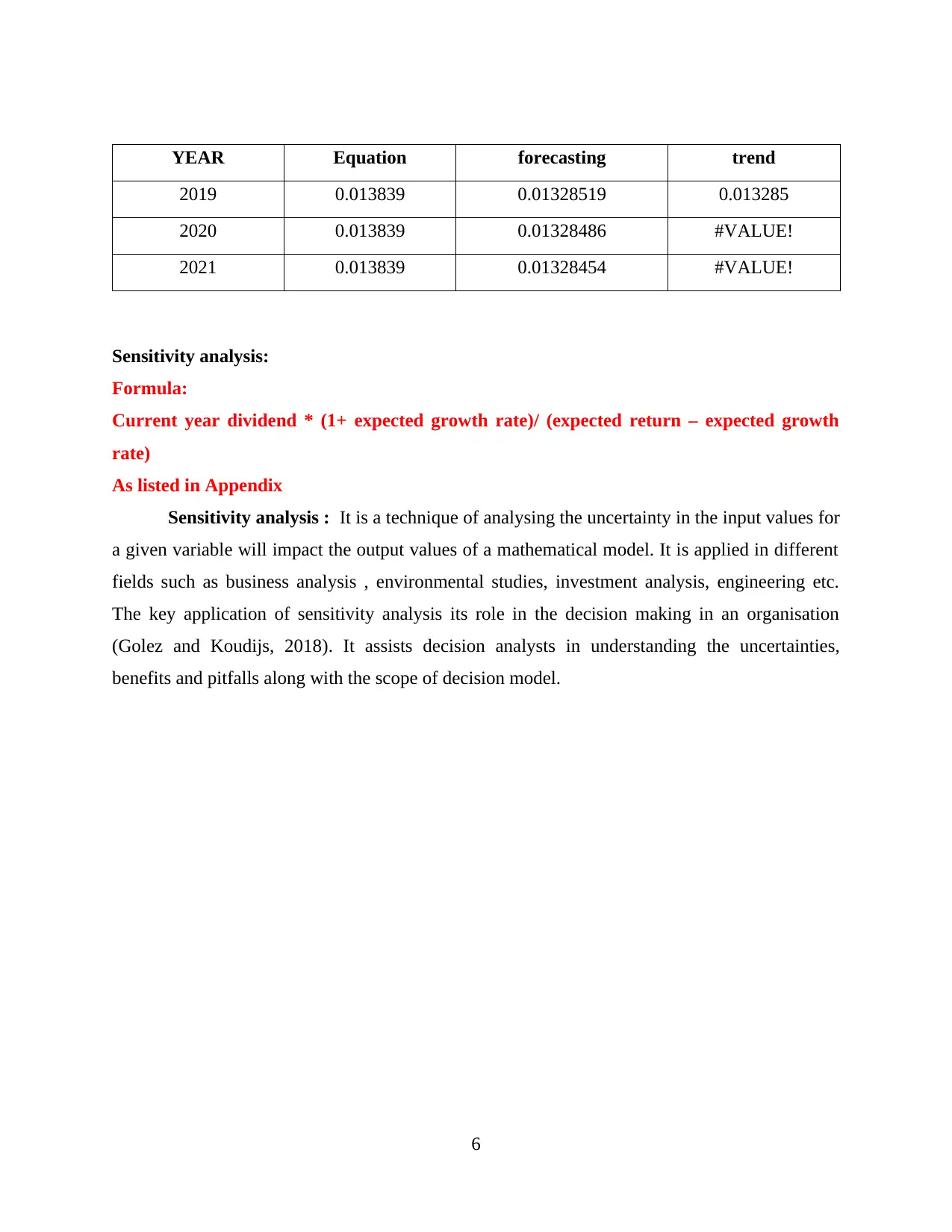

YEAR Equation forecasting trend

2019 0.013839 0.01328519 0.013285

2020 0.013839 0.01328486 #VALUE!

2021 0.013839 0.01328454 #VALUE!

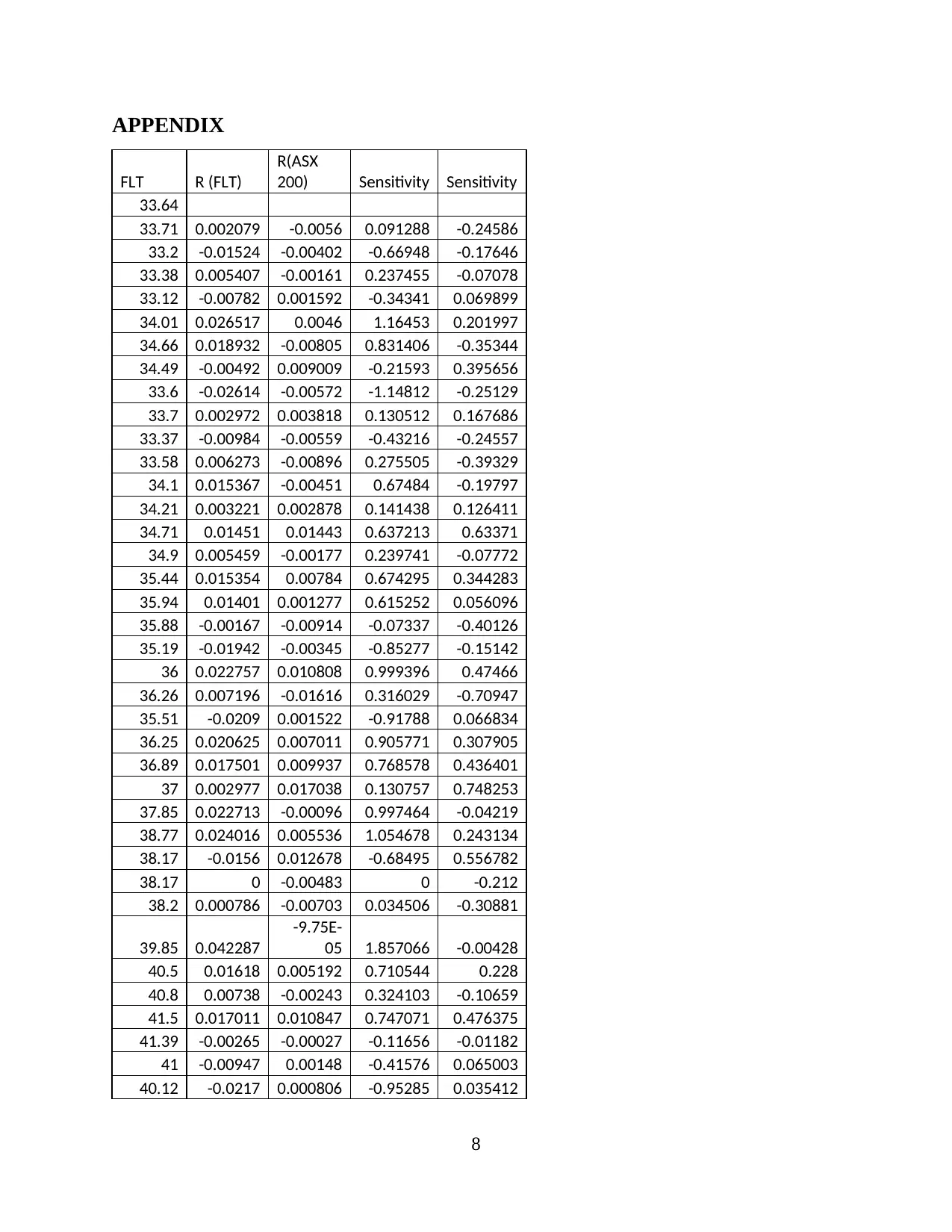

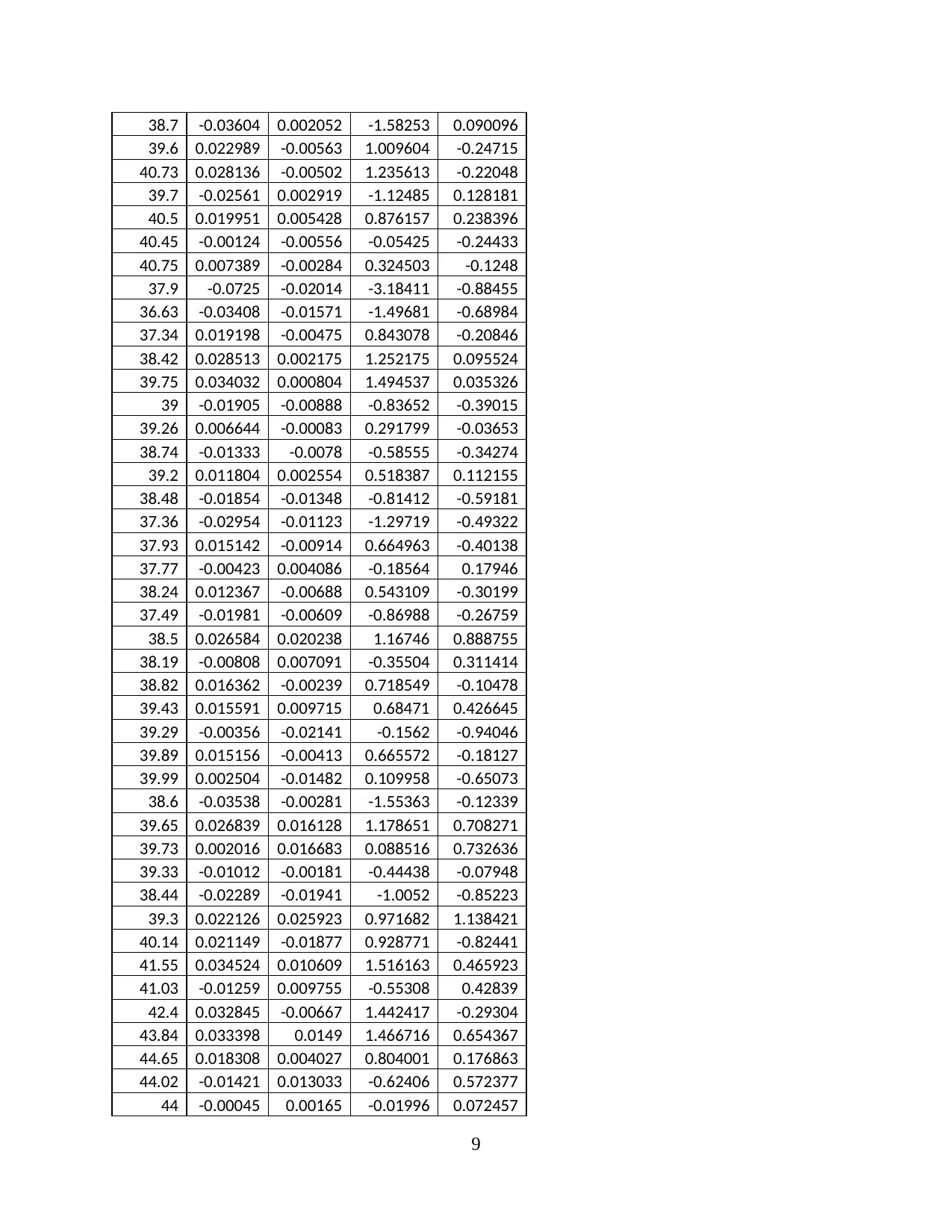

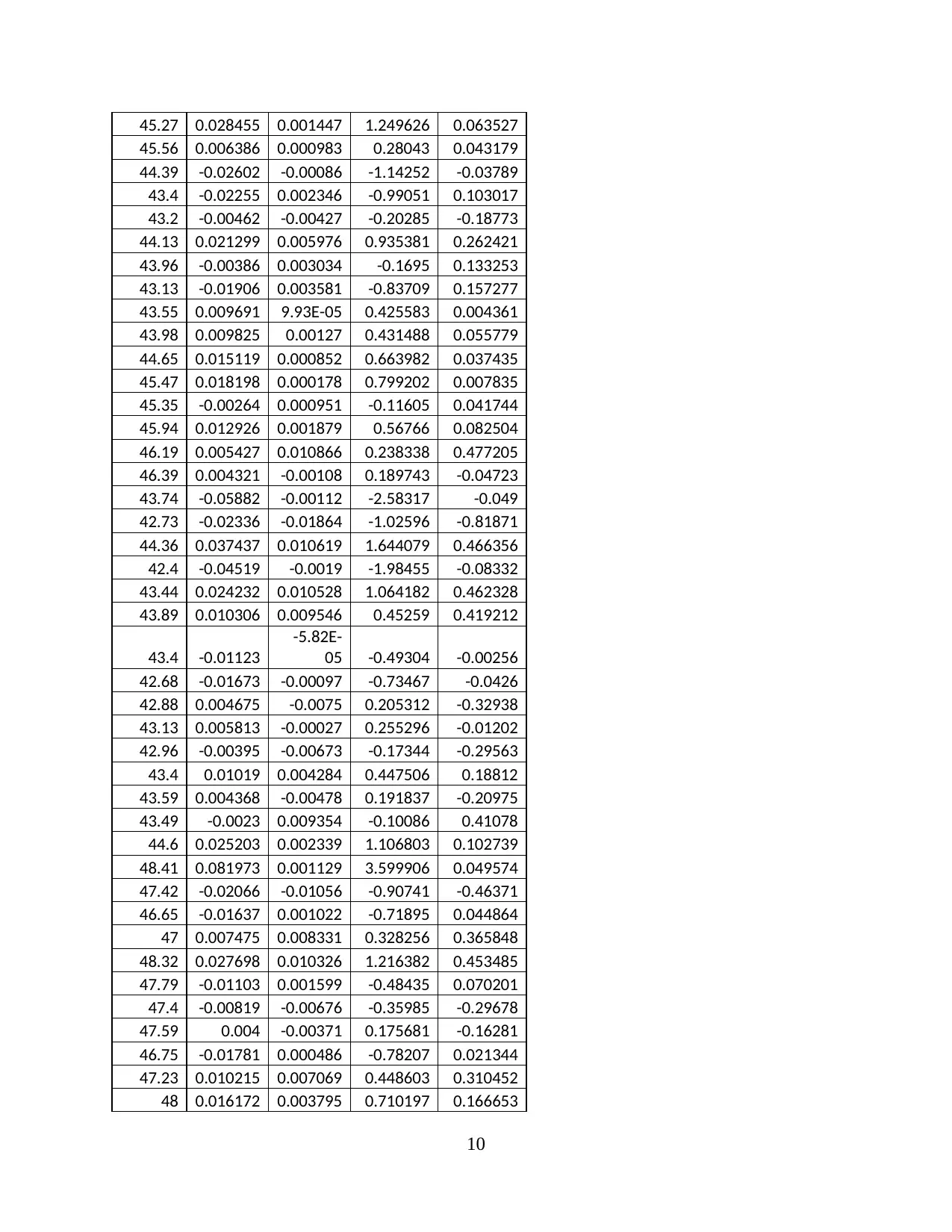

Sensitivity analysis:

Formula:

Current year dividend * (1+ expected growth rate)/ (expected return – expected growth

rate)

As listed in Appendix

Sensitivity analysis : It is a technique of analysing the uncertainty in the input values for

a given variable will impact the output values of a mathematical model. It is applied in different

fields such as business analysis , environmental studies, investment analysis, engineering etc.

The key application of sensitivity analysis its role in the decision making in an organisation

(Golez and Koudijs, 2018). It assists decision analysts in understanding the uncertainties,

benefits and pitfalls along with the scope of decision model.

6

2019 0.013839 0.01328519 0.013285

2020 0.013839 0.01328486 #VALUE!

2021 0.013839 0.01328454 #VALUE!

Sensitivity analysis:

Formula:

Current year dividend * (1+ expected growth rate)/ (expected return – expected growth

rate)

As listed in Appendix

Sensitivity analysis : It is a technique of analysing the uncertainty in the input values for

a given variable will impact the output values of a mathematical model. It is applied in different

fields such as business analysis , environmental studies, investment analysis, engineering etc.

The key application of sensitivity analysis its role in the decision making in an organisation

(Golez and Koudijs, 2018). It assists decision analysts in understanding the uncertainties,

benefits and pitfalls along with the scope of decision model.

6

REFERENCES

Books and Journals

Anwar, S., Fathoni, A. and Gagah, E., 2018. ANALYSIS OF THE EFFECT OF CURRENT

RATIO, TOTAL TURN OVER ASSETS, DEBT TO EQUITY RATIO AND NET

PROFIT MAGRIN ON CHANGES OF PROFIT WITH ON EQUITY RETURN AS

INTERVENING VARIABLES ON PHARMACEUTICAL COMPANIES LISTED IN

INDONESIA STOCK EXCHANGE (BEI) 2013-2017 PERIOD. Journal of

Management. 4(4).

Golez, B. and Koudijs, P., 2018. Four centuries of return predictability. Journal of Financial

Economics. 127(2). pp.248-263.

Payne, B. C. and et.al., 2018. A FINANCIAL PROFILE OF THOSE FIRMS WITH THE

LOWEST COST OF EQUITY FUNDS, AND A CANONICAL RANKING OF THE

RISK–RETURN FACTORS. Southeast Asia Review of Economics and Business. 1(1).

Weber, M., 2018. Cash flow duration and the term structure of equity returns. Journal of

Financial Economics. 128(3). pp.486-503.

7

Books and Journals

Anwar, S., Fathoni, A. and Gagah, E., 2018. ANALYSIS OF THE EFFECT OF CURRENT

RATIO, TOTAL TURN OVER ASSETS, DEBT TO EQUITY RATIO AND NET

PROFIT MAGRIN ON CHANGES OF PROFIT WITH ON EQUITY RETURN AS

INTERVENING VARIABLES ON PHARMACEUTICAL COMPANIES LISTED IN

INDONESIA STOCK EXCHANGE (BEI) 2013-2017 PERIOD. Journal of

Management. 4(4).

Golez, B. and Koudijs, P., 2018. Four centuries of return predictability. Journal of Financial

Economics. 127(2). pp.248-263.

Payne, B. C. and et.al., 2018. A FINANCIAL PROFILE OF THOSE FIRMS WITH THE

LOWEST COST OF EQUITY FUNDS, AND A CANONICAL RANKING OF THE

RISK–RETURN FACTORS. Southeast Asia Review of Economics and Business. 1(1).

Weber, M., 2018. Cash flow duration and the term structure of equity returns. Journal of

Financial Economics. 128(3). pp.486-503.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

FLT R (FLT)

R(ASX

200) Sensitivity Sensitivity

33.64

33.71 0.002079 -0.0056 0.091288 -0.24586

33.2 -0.01524 -0.00402 -0.66948 -0.17646

33.38 0.005407 -0.00161 0.237455 -0.07078

33.12 -0.00782 0.001592 -0.34341 0.069899

34.01 0.026517 0.0046 1.16453 0.201997

34.66 0.018932 -0.00805 0.831406 -0.35344

34.49 -0.00492 0.009009 -0.21593 0.395656

33.6 -0.02614 -0.00572 -1.14812 -0.25129

33.7 0.002972 0.003818 0.130512 0.167686

33.37 -0.00984 -0.00559 -0.43216 -0.24557

33.58 0.006273 -0.00896 0.275505 -0.39329

34.1 0.015367 -0.00451 0.67484 -0.19797

34.21 0.003221 0.002878 0.141438 0.126411

34.71 0.01451 0.01443 0.637213 0.63371

34.9 0.005459 -0.00177 0.239741 -0.07772

35.44 0.015354 0.00784 0.674295 0.344283

35.94 0.01401 0.001277 0.615252 0.056096

35.88 -0.00167 -0.00914 -0.07337 -0.40126

35.19 -0.01942 -0.00345 -0.85277 -0.15142

36 0.022757 0.010808 0.999396 0.47466

36.26 0.007196 -0.01616 0.316029 -0.70947

35.51 -0.0209 0.001522 -0.91788 0.066834

36.25 0.020625 0.007011 0.905771 0.307905

36.89 0.017501 0.009937 0.768578 0.436401

37 0.002977 0.017038 0.130757 0.748253

37.85 0.022713 -0.00096 0.997464 -0.04219

38.77 0.024016 0.005536 1.054678 0.243134

38.17 -0.0156 0.012678 -0.68495 0.556782

38.17 0 -0.00483 0 -0.212

38.2 0.000786 -0.00703 0.034506 -0.30881

39.85 0.042287

-9.75E-

05 1.857066 -0.00428

40.5 0.01618 0.005192 0.710544 0.228

40.8 0.00738 -0.00243 0.324103 -0.10659

41.5 0.017011 0.010847 0.747071 0.476375

41.39 -0.00265 -0.00027 -0.11656 -0.01182

41 -0.00947 0.00148 -0.41576 0.065003

40.12 -0.0217 0.000806 -0.95285 0.035412

8

FLT R (FLT)

R(ASX

200) Sensitivity Sensitivity

33.64

33.71 0.002079 -0.0056 0.091288 -0.24586

33.2 -0.01524 -0.00402 -0.66948 -0.17646

33.38 0.005407 -0.00161 0.237455 -0.07078

33.12 -0.00782 0.001592 -0.34341 0.069899

34.01 0.026517 0.0046 1.16453 0.201997

34.66 0.018932 -0.00805 0.831406 -0.35344

34.49 -0.00492 0.009009 -0.21593 0.395656

33.6 -0.02614 -0.00572 -1.14812 -0.25129

33.7 0.002972 0.003818 0.130512 0.167686

33.37 -0.00984 -0.00559 -0.43216 -0.24557

33.58 0.006273 -0.00896 0.275505 -0.39329

34.1 0.015367 -0.00451 0.67484 -0.19797

34.21 0.003221 0.002878 0.141438 0.126411

34.71 0.01451 0.01443 0.637213 0.63371

34.9 0.005459 -0.00177 0.239741 -0.07772

35.44 0.015354 0.00784 0.674295 0.344283

35.94 0.01401 0.001277 0.615252 0.056096

35.88 -0.00167 -0.00914 -0.07337 -0.40126

35.19 -0.01942 -0.00345 -0.85277 -0.15142

36 0.022757 0.010808 0.999396 0.47466

36.26 0.007196 -0.01616 0.316029 -0.70947

35.51 -0.0209 0.001522 -0.91788 0.066834

36.25 0.020625 0.007011 0.905771 0.307905

36.89 0.017501 0.009937 0.768578 0.436401

37 0.002977 0.017038 0.130757 0.748253

37.85 0.022713 -0.00096 0.997464 -0.04219

38.77 0.024016 0.005536 1.054678 0.243134

38.17 -0.0156 0.012678 -0.68495 0.556782

38.17 0 -0.00483 0 -0.212

38.2 0.000786 -0.00703 0.034506 -0.30881

39.85 0.042287

-9.75E-

05 1.857066 -0.00428

40.5 0.01618 0.005192 0.710544 0.228

40.8 0.00738 -0.00243 0.324103 -0.10659

41.5 0.017011 0.010847 0.747071 0.476375

41.39 -0.00265 -0.00027 -0.11656 -0.01182

41 -0.00947 0.00148 -0.41576 0.065003

40.12 -0.0217 0.000806 -0.95285 0.035412

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

38.7 -0.03604 0.002052 -1.58253 0.090096

39.6 0.022989 -0.00563 1.009604 -0.24715

40.73 0.028136 -0.00502 1.235613 -0.22048

39.7 -0.02561 0.002919 -1.12485 0.128181

40.5 0.019951 0.005428 0.876157 0.238396

40.45 -0.00124 -0.00556 -0.05425 -0.24433

40.75 0.007389 -0.00284 0.324503 -0.1248

37.9 -0.0725 -0.02014 -3.18411 -0.88455

36.63 -0.03408 -0.01571 -1.49681 -0.68984

37.34 0.019198 -0.00475 0.843078 -0.20846

38.42 0.028513 0.002175 1.252175 0.095524

39.75 0.034032 0.000804 1.494537 0.035326

39 -0.01905 -0.00888 -0.83652 -0.39015

39.26 0.006644 -0.00083 0.291799 -0.03653

38.74 -0.01333 -0.0078 -0.58555 -0.34274

39.2 0.011804 0.002554 0.518387 0.112155

38.48 -0.01854 -0.01348 -0.81412 -0.59181

37.36 -0.02954 -0.01123 -1.29719 -0.49322

37.93 0.015142 -0.00914 0.664963 -0.40138

37.77 -0.00423 0.004086 -0.18564 0.17946

38.24 0.012367 -0.00688 0.543109 -0.30199

37.49 -0.01981 -0.00609 -0.86988 -0.26759

38.5 0.026584 0.020238 1.16746 0.888755

38.19 -0.00808 0.007091 -0.35504 0.311414

38.82 0.016362 -0.00239 0.718549 -0.10478

39.43 0.015591 0.009715 0.68471 0.426645

39.29 -0.00356 -0.02141 -0.1562 -0.94046

39.89 0.015156 -0.00413 0.665572 -0.18127

39.99 0.002504 -0.01482 0.109958 -0.65073

38.6 -0.03538 -0.00281 -1.55363 -0.12339

39.65 0.026839 0.016128 1.178651 0.708271

39.73 0.002016 0.016683 0.088516 0.732636

39.33 -0.01012 -0.00181 -0.44438 -0.07948

38.44 -0.02289 -0.01941 -1.0052 -0.85223

39.3 0.022126 0.025923 0.971682 1.138421

40.14 0.021149 -0.01877 0.928771 -0.82441

41.55 0.034524 0.010609 1.516163 0.465923

41.03 -0.01259 0.009755 -0.55308 0.42839

42.4 0.032845 -0.00667 1.442417 -0.29304

43.84 0.033398 0.0149 1.466716 0.654367

44.65 0.018308 0.004027 0.804001 0.176863

44.02 -0.01421 0.013033 -0.62406 0.572377

44 -0.00045 0.00165 -0.01996 0.072457

9

39.6 0.022989 -0.00563 1.009604 -0.24715

40.73 0.028136 -0.00502 1.235613 -0.22048

39.7 -0.02561 0.002919 -1.12485 0.128181

40.5 0.019951 0.005428 0.876157 0.238396

40.45 -0.00124 -0.00556 -0.05425 -0.24433

40.75 0.007389 -0.00284 0.324503 -0.1248

37.9 -0.0725 -0.02014 -3.18411 -0.88455

36.63 -0.03408 -0.01571 -1.49681 -0.68984

37.34 0.019198 -0.00475 0.843078 -0.20846

38.42 0.028513 0.002175 1.252175 0.095524

39.75 0.034032 0.000804 1.494537 0.035326

39 -0.01905 -0.00888 -0.83652 -0.39015

39.26 0.006644 -0.00083 0.291799 -0.03653

38.74 -0.01333 -0.0078 -0.58555 -0.34274

39.2 0.011804 0.002554 0.518387 0.112155

38.48 -0.01854 -0.01348 -0.81412 -0.59181

37.36 -0.02954 -0.01123 -1.29719 -0.49322

37.93 0.015142 -0.00914 0.664963 -0.40138

37.77 -0.00423 0.004086 -0.18564 0.17946

38.24 0.012367 -0.00688 0.543109 -0.30199

37.49 -0.01981 -0.00609 -0.86988 -0.26759

38.5 0.026584 0.020238 1.16746 0.888755

38.19 -0.00808 0.007091 -0.35504 0.311414

38.82 0.016362 -0.00239 0.718549 -0.10478

39.43 0.015591 0.009715 0.68471 0.426645

39.29 -0.00356 -0.02141 -0.1562 -0.94046

39.89 0.015156 -0.00413 0.665572 -0.18127

39.99 0.002504 -0.01482 0.109958 -0.65073

38.6 -0.03538 -0.00281 -1.55363 -0.12339

39.65 0.026839 0.016128 1.178651 0.708271

39.73 0.002016 0.016683 0.088516 0.732636

39.33 -0.01012 -0.00181 -0.44438 -0.07948

38.44 -0.02289 -0.01941 -1.0052 -0.85223

39.3 0.022126 0.025923 0.971682 1.138421

40.14 0.021149 -0.01877 0.928771 -0.82441

41.55 0.034524 0.010609 1.516163 0.465923

41.03 -0.01259 0.009755 -0.55308 0.42839

42.4 0.032845 -0.00667 1.442417 -0.29304

43.84 0.033398 0.0149 1.466716 0.654367

44.65 0.018308 0.004027 0.804001 0.176863

44.02 -0.01421 0.013033 -0.62406 0.572377

44 -0.00045 0.00165 -0.01996 0.072457

9

45.27 0.028455 0.001447 1.249626 0.063527

45.56 0.006386 0.000983 0.28043 0.043179

44.39 -0.02602 -0.00086 -1.14252 -0.03789

43.4 -0.02255 0.002346 -0.99051 0.103017

43.2 -0.00462 -0.00427 -0.20285 -0.18773

44.13 0.021299 0.005976 0.935381 0.262421

43.96 -0.00386 0.003034 -0.1695 0.133253

43.13 -0.01906 0.003581 -0.83709 0.157277

43.55 0.009691 9.93E-05 0.425583 0.004361

43.98 0.009825 0.00127 0.431488 0.055779

44.65 0.015119 0.000852 0.663982 0.037435

45.47 0.018198 0.000178 0.799202 0.007835

45.35 -0.00264 0.000951 -0.11605 0.041744

45.94 0.012926 0.001879 0.56766 0.082504

46.19 0.005427 0.010866 0.238338 0.477205

46.39 0.004321 -0.00108 0.189743 -0.04723

43.74 -0.05882 -0.00112 -2.58317 -0.049

42.73 -0.02336 -0.01864 -1.02596 -0.81871

44.36 0.037437 0.010619 1.644079 0.466356

42.4 -0.04519 -0.0019 -1.98455 -0.08332

43.44 0.024232 0.010528 1.064182 0.462328

43.89 0.010306 0.009546 0.45259 0.419212

43.4 -0.01123

-5.82E-

05 -0.49304 -0.00256

42.68 -0.01673 -0.00097 -0.73467 -0.0426

42.88 0.004675 -0.0075 0.205312 -0.32938

43.13 0.005813 -0.00027 0.255296 -0.01202

42.96 -0.00395 -0.00673 -0.17344 -0.29563

43.4 0.01019 0.004284 0.447506 0.18812

43.59 0.004368 -0.00478 0.191837 -0.20975

43.49 -0.0023 0.009354 -0.10086 0.41078

44.6 0.025203 0.002339 1.106803 0.102739

48.41 0.081973 0.001129 3.599906 0.049574

47.42 -0.02066 -0.01056 -0.90741 -0.46371

46.65 -0.01637 0.001022 -0.71895 0.044864

47 0.007475 0.008331 0.328256 0.365848

48.32 0.027698 0.010326 1.216382 0.453485

47.79 -0.01103 0.001599 -0.48435 0.070201

47.4 -0.00819 -0.00676 -0.35985 -0.29678

47.59 0.004 -0.00371 0.175681 -0.16281

46.75 -0.01781 0.000486 -0.78207 0.021344

47.23 0.010215 0.007069 0.448603 0.310452

48 0.016172 0.003795 0.710197 0.166653

10

45.56 0.006386 0.000983 0.28043 0.043179

44.39 -0.02602 -0.00086 -1.14252 -0.03789

43.4 -0.02255 0.002346 -0.99051 0.103017

43.2 -0.00462 -0.00427 -0.20285 -0.18773

44.13 0.021299 0.005976 0.935381 0.262421

43.96 -0.00386 0.003034 -0.1695 0.133253

43.13 -0.01906 0.003581 -0.83709 0.157277

43.55 0.009691 9.93E-05 0.425583 0.004361

43.98 0.009825 0.00127 0.431488 0.055779

44.65 0.015119 0.000852 0.663982 0.037435

45.47 0.018198 0.000178 0.799202 0.007835

45.35 -0.00264 0.000951 -0.11605 0.041744

45.94 0.012926 0.001879 0.56766 0.082504

46.19 0.005427 0.010866 0.238338 0.477205

46.39 0.004321 -0.00108 0.189743 -0.04723

43.74 -0.05882 -0.00112 -2.58317 -0.049

42.73 -0.02336 -0.01864 -1.02596 -0.81871

44.36 0.037437 0.010619 1.644079 0.466356

42.4 -0.04519 -0.0019 -1.98455 -0.08332

43.44 0.024232 0.010528 1.064182 0.462328

43.89 0.010306 0.009546 0.45259 0.419212

43.4 -0.01123

-5.82E-

05 -0.49304 -0.00256

42.68 -0.01673 -0.00097 -0.73467 -0.0426

42.88 0.004675 -0.0075 0.205312 -0.32938

43.13 0.005813 -0.00027 0.255296 -0.01202

42.96 -0.00395 -0.00673 -0.17344 -0.29563

43.4 0.01019 0.004284 0.447506 0.18812

43.59 0.004368 -0.00478 0.191837 -0.20975

43.49 -0.0023 0.009354 -0.10086 0.41078

44.6 0.025203 0.002339 1.106803 0.102739

48.41 0.081973 0.001129 3.599906 0.049574

47.42 -0.02066 -0.01056 -0.90741 -0.46371

46.65 -0.01637 0.001022 -0.71895 0.044864

47 0.007475 0.008331 0.328256 0.365848

48.32 0.027698 0.010326 1.216382 0.453485

47.79 -0.01103 0.001599 -0.48435 0.070201

47.4 -0.00819 -0.00676 -0.35985 -0.29678

47.59 0.004 -0.00371 0.175681 -0.16281

46.75 -0.01781 0.000486 -0.78207 0.021344

47.23 0.010215 0.007069 0.448603 0.310452

48 0.016172 0.003795 0.710197 0.166653

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.