Compsoft Limited: Financial Analysis and Break-Even Point

VerifiedAdded on 2024/05/31

|8

|1369

|161

AI Summary

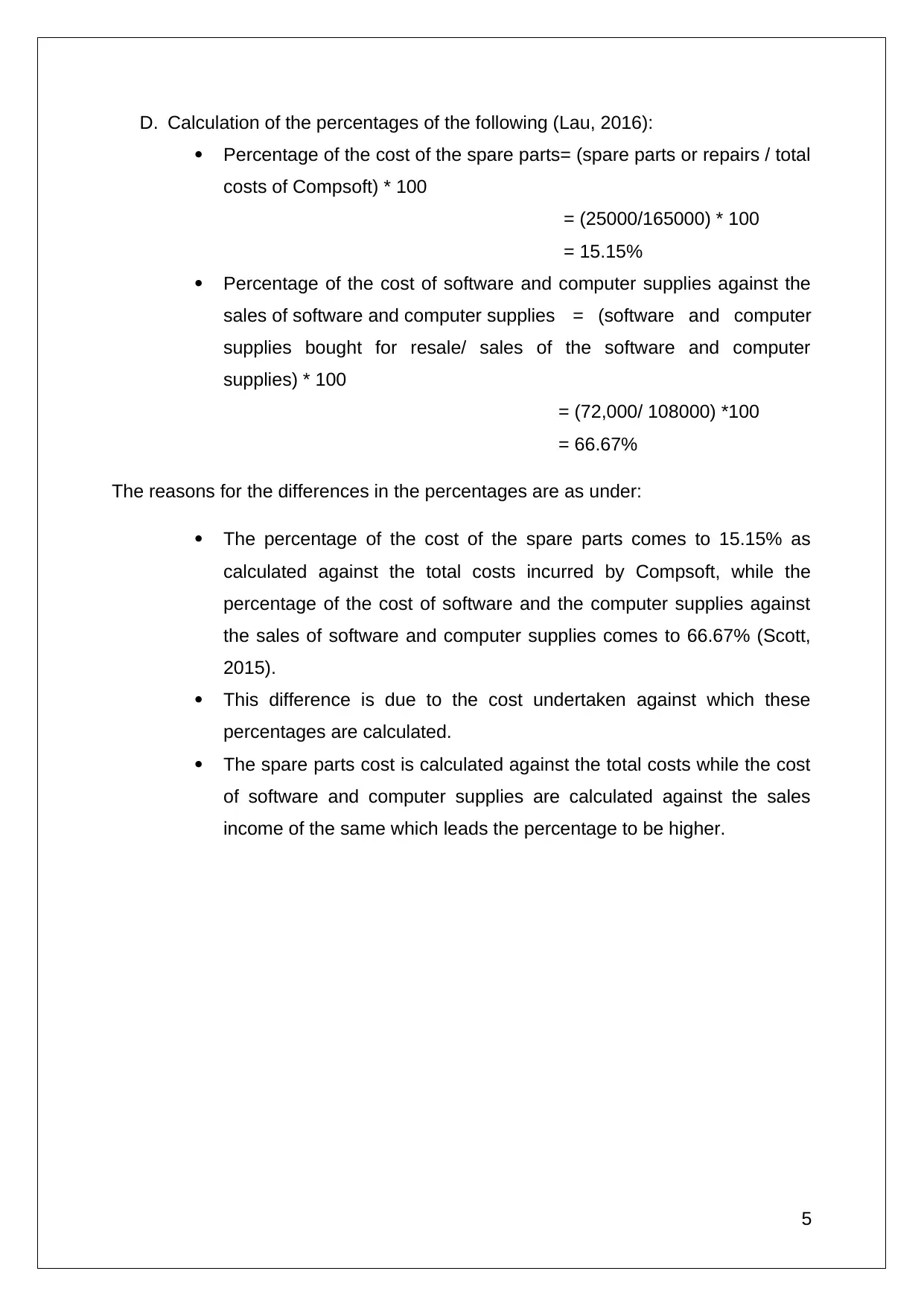

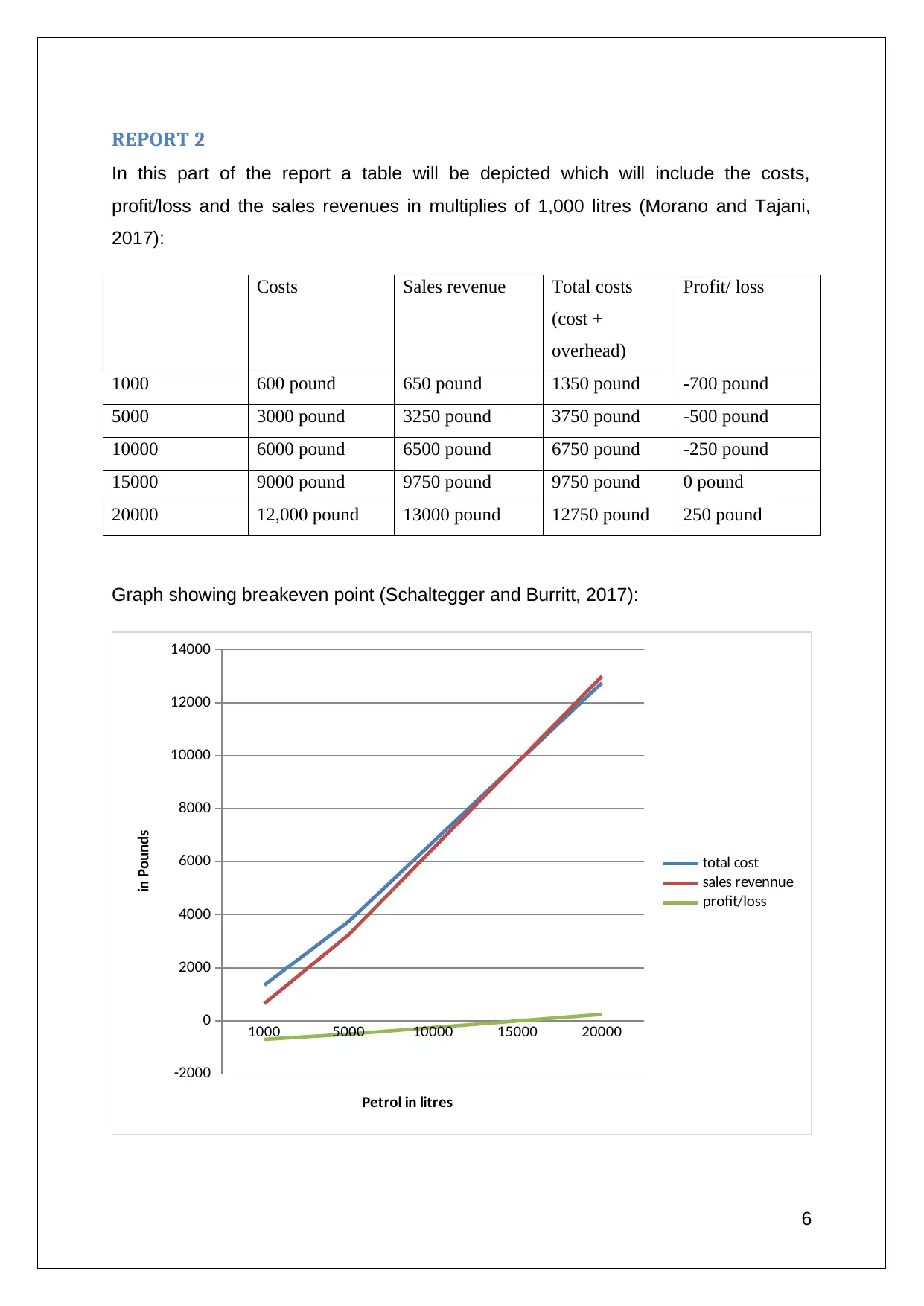

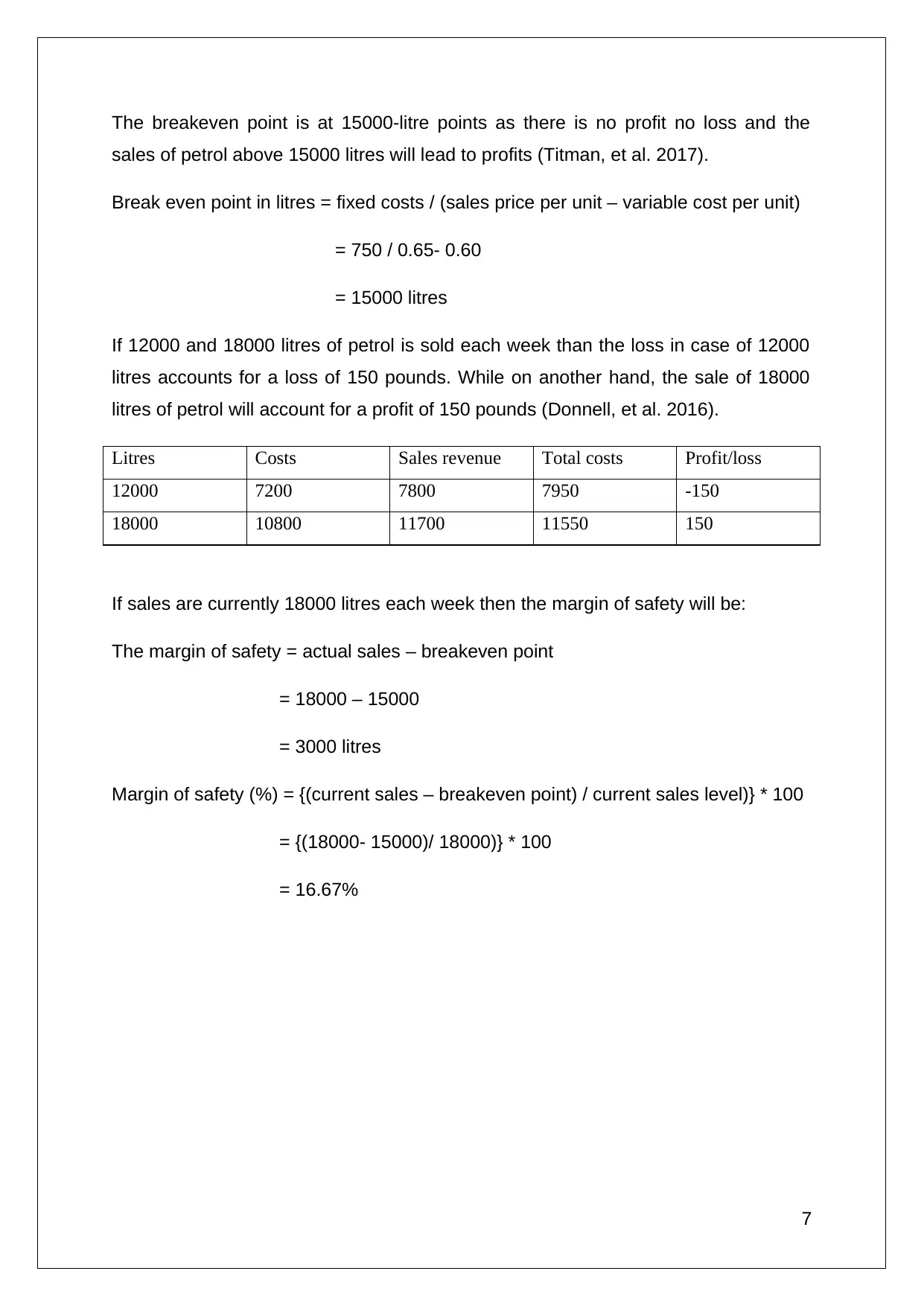

This report analyzes the financial performance of Compsoft Limited, a newly established computer services and repair business. It examines the company's added value, surplus funds, and cost percentages. The report also includes a break-even analysis, calculating the break-even point in liters of petrol sold and the margin of safety. The analysis provides insights into the company's financial health and potential areas for improvement.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.