Consolidated and Separate Financial Statements - PDF

Added on 2021-06-17

13 Pages3457 Words68 Views

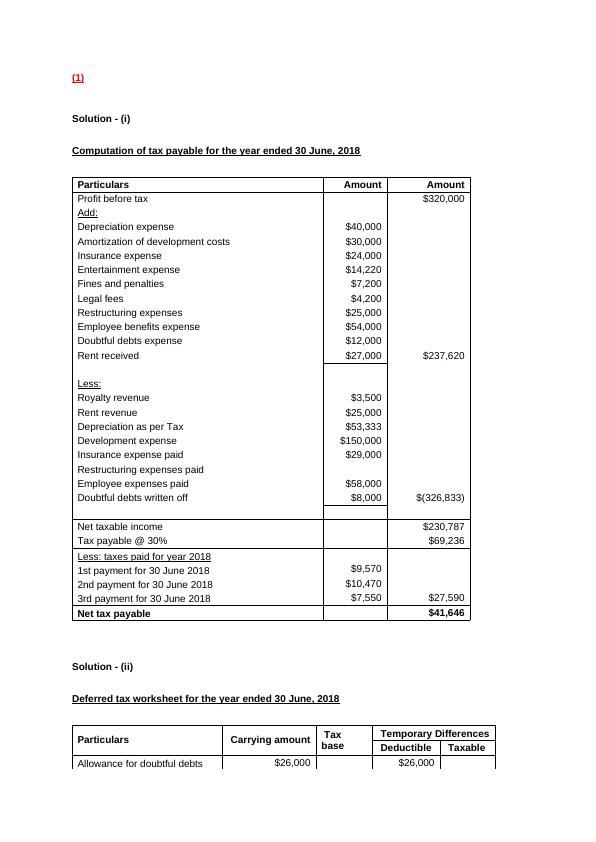

(1)Solution - (i)Computation of tax payable for the year ended 30 June, 2018Particulars Amount Amount Profit before tax$320,000Add:Depreciation expense$40,000Amortization of development costs$30,000Insurance expense$24,000Entertainment expense$14,220Fines and penalties$7,200Legal fees$4,200Restructuring expenses$25,000Employee benefits expense$54,000Doubtful debts expense$12,000Rent received$27,000$237,620Less:Royalty revenue$3,500Rent revenue$25,000Depreciation as per Tax$53,333Development expense$150,000Insurance expense paid$29,000Restructuring expenses paidEmployee expenses paid$58,000Doubtful debts written off$8,000$(326,833)Net taxable income$230,787Tax payable @ 30%$69,236Less: taxes paid for year 20181st payment for 30 June 2018$9,5702nd payment for 30 June 2018$10,4703rd payment for 30 June 2018$7,550$27,590Net tax payable$41,646Solution - (ii)Deferred tax worksheet for the year ended 30 June, 2018Particulars Carrying amount Tax base Temporary Differences Deductible Taxable Allowance for doubtful debts$26,000$26,000

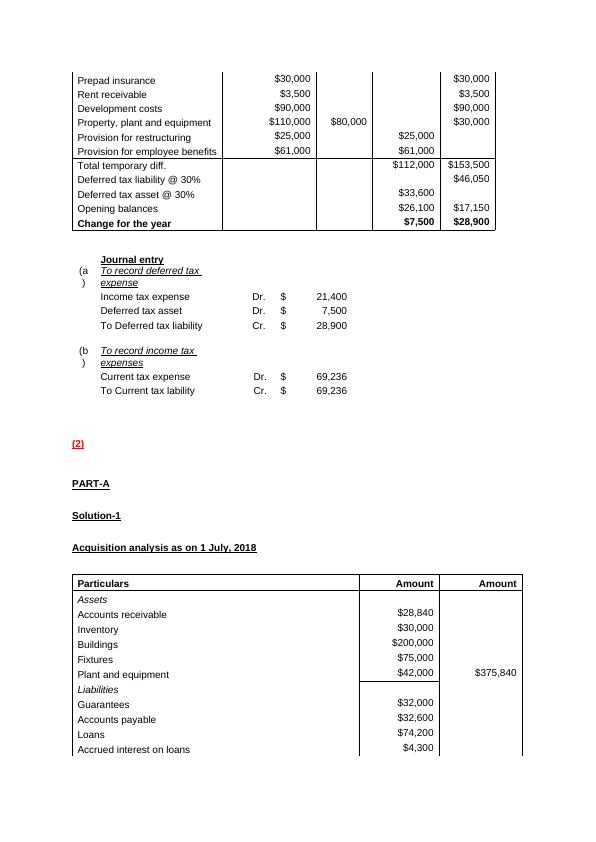

Prepad insurance$30,000$30,000Rent receivable$3,500$3,500Development costs$90,000$90,000Property, plant and equipment$110,000$80,000$30,000Provision for restructuring$25,000$25,000Provision for employee benefits$61,000$61,000Total temporary diff.$112,000$153,500Deferred tax liability @ 30%$46,050Deferred tax asset @ 30%$33,600Opening balances$26,100$17,150Change for the year$7,500$28,900Journal entry(a)To record deferred tax expenseIncome tax expenseDr. $ 21,400Deferred tax assetDr. $ 7,500To Deferred tax liabilityCr. $ 28,900(b)To record income tax expensesCurrent tax expense Dr. $ 69,236To Current tax lability Cr. $ 69,236(2)PART-ASolution-1Acquisition analysis as on 1 July, 2018Particulars Amount Amount AssetsAccounts receivable$28,840Inventory$30,000Buildings$200,000Fixtures$75,000Plant and equipment$42,000$375,840LiabilitiesGuarantees$32,000Accounts payable$32,600Loans$74,200Accrued interest on loans$4,300

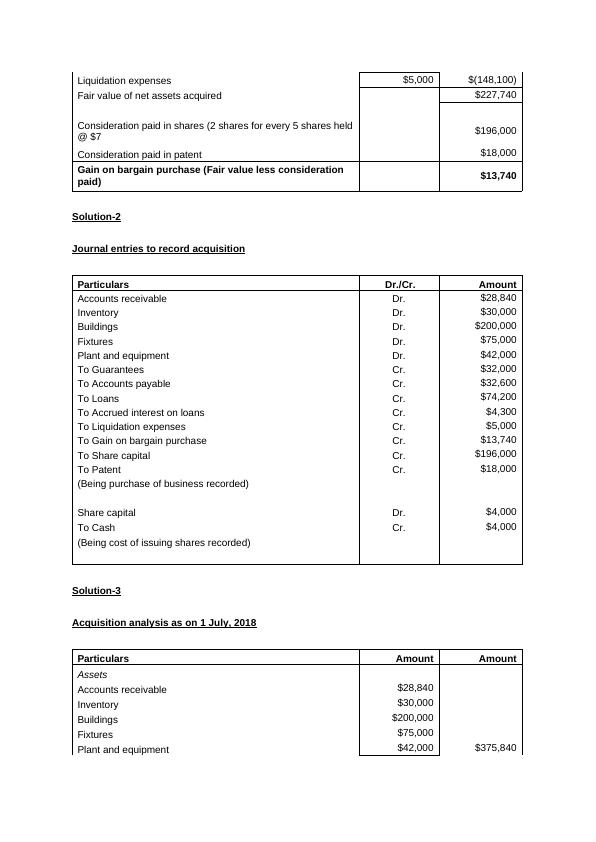

Liquidation expenses$5,000$(148,100)Fair value of net assets acquired$227,740Consideration paid in shares (2 shares for every 5 shares held@ $7$196,000Consideration paid in patent$18,000Gain on bargain purchase (Fair value less consideration paid)$13,740Solution-2Journal entries to record acquisitionParticulars Dr./Cr. Amount Accounts receivableDr.$28,840InventoryDr.$30,000BuildingsDr.$200,000FixturesDr.$75,000Plant and equipmentDr.$42,000To GuaranteesCr.$32,000To Accounts payableCr.$32,600To LoansCr.$74,200To Accrued interest on loansCr.$4,300To Liquidation expensesCr.$5,000To Gain on bargain purchaseCr.$13,740To Share capitalCr.$196,000To PatentCr.$18,000(Being purchase of business recorded)Share capitalDr.$4,000To CashCr.$4,000(Being cost of issuing shares recorded)Solution-3Acquisition analysis as on 1 July, 2018Particulars Amount Amount AssetsAccounts receivable$28,840Inventory$30,000Buildings$200,000Fixtures$75,000Plant and equipment$42,000$375,840

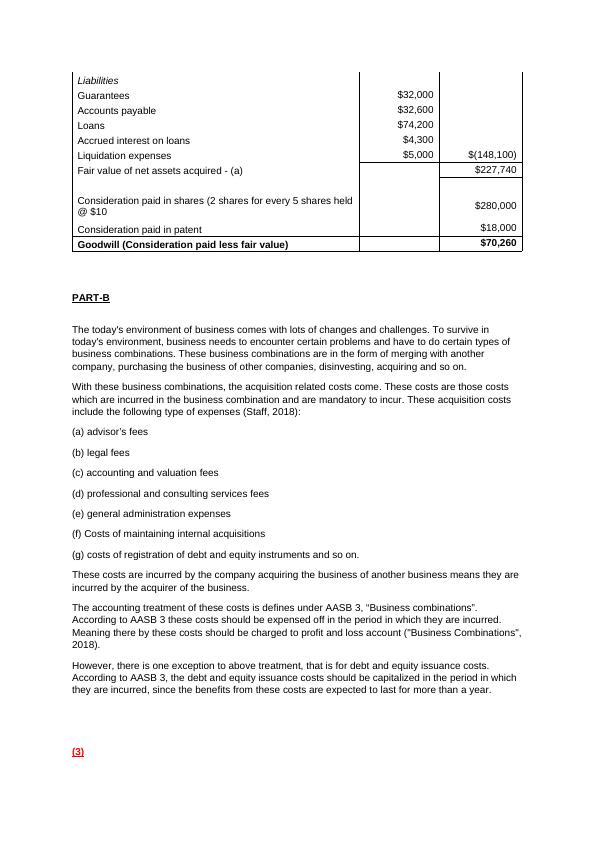

LiabilitiesGuarantees$32,000Accounts payable$32,600Loans$74,200Accrued interest on loans$4,300Liquidation expenses$5,000$(148,100)Fair value of net assets acquired - (a)$227,740Consideration paid in shares (2 shares for every 5 shares held@ $10$280,000Consideration paid in patent$18,000Goodwill (Consideration paid less fair value)$70,260PART-BThe today's environment of business comes with lots of changes and challenges. To survive in today's environment, business needs to encounter certain problems and have to do certain types of business combinations. These business combinations are in the form of merging with another company, purchasing the business of other companies, disinvesting, acquiring and so on.With these business combinations, the acquisition related costs come. These costs are those costs which are incurred in the business combination and are mandatory to incur. These acquisition costs include the following type of expenses (Staff, 2018):(a) advisor’s fees(b) legal fees(c) accounting and valuation fees(d) professional and consulting services fees(e) general administration expenses (f) Costs of maintaining internal acquisitions(g) costs of registration of debt and equity instruments and so on.These costs are incurred by the company acquiring the business of another business means they are incurred by the acquirer of the business.The accounting treatment of these costs is defines under AASB 3, “Business combinations”. According to AASB 3 these costs should be expensed off in the period in which they are incurred. Meaning there by these costs should be charged to profit and loss account ("Business Combinations",2018).However, there is one exception to above treatment, that is for debt and equity issuance costs. According to AASB 3, the debt and equity issuance costs should be capitalized in the period in which they are incurred, since the benefits from these costs are expected to last for more than a year.(3)

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Computation of Acquisition Analysis and Consolidation Worksheet Entrieslg...

|7

|949

|72

ACC705 Accounting Assignment- Sam Ltdlg...

|4

|690

|113

Consolidation of Financial Statementlg...

|8

|873

|144

Corporate Accounting and Reportinglg...

|6

|630

|100

Calculation of Taxable Incomelg...

|11

|1807

|53

Acquisition Analysis as on 1 July, 2018lg...

|5

|1082

|355