Financial Analysis Report: Investment Appraisal and Analysis

VerifiedAdded on 2020/12/09

|17

|4217

|343

Report

AI Summary

This report presents a detailed financial analysis, beginning with the preparation of an income statement and balance sheet for Gravepale Plc, followed by a contribution and break-even analysis for Cornpeace Ltd. The report then delves into investment planning for Dane Jones Ltd, utilizing capital budgeting tools such as payback period, net present value (NPV), and accounting rate of return (ARR). It assesses the viability of capital projects, compares different investment appraisal techniques, and evaluates the benefits and limitations of using budgets as a strategic planning tool. The analysis includes interpretations of financial data, calculations of profitability, and strategic recommendations regarding advertisement expenses and sales levels. The report concludes with an evaluation of investment appraisal techniques, offering insights into their advantages and disadvantages, and providing a comprehensive overview of financial management principles.

UGB163

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

PART A...........................................................................................................................................1

Income Statement for year ended 31/12/2017........................................................................1

Balance Sheet as on 31/03/2017.............................................................................................1

Interpretation:...................................................................................................................................4

PART B............................................................................................................................................4

a. Calculation of contribution per unit for Cornpeace Ltd.....................................................4

b. Computation of break even point and margin of safety.....................................................5

c. Computation of profits of the company at different sales levels........................................5

d. Analysis of the strategy for change in advertisement expenses and sales level.................5

PART C............................................................................................................................................6

a. Assessing the viability of capital projects using investment appraisal tools and techniques .6

B. Advantages and disadvantages of different investment appraisal techniques..................8

C. Report on benefits and limitation of using budgets as strategic planning tool...............11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

PART A...........................................................................................................................................1

Income Statement for year ended 31/12/2017........................................................................1

Balance Sheet as on 31/03/2017.............................................................................................1

Interpretation:...................................................................................................................................4

PART B............................................................................................................................................4

a. Calculation of contribution per unit for Cornpeace Ltd.....................................................4

b. Computation of break even point and margin of safety.....................................................5

c. Computation of profits of the company at different sales levels........................................5

d. Analysis of the strategy for change in advertisement expenses and sales level.................5

PART C............................................................................................................................................6

a. Assessing the viability of capital projects using investment appraisal tools and techniques .6

B. Advantages and disadvantages of different investment appraisal techniques..................8

C. Report on benefits and limitation of using budgets as strategic planning tool...............11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

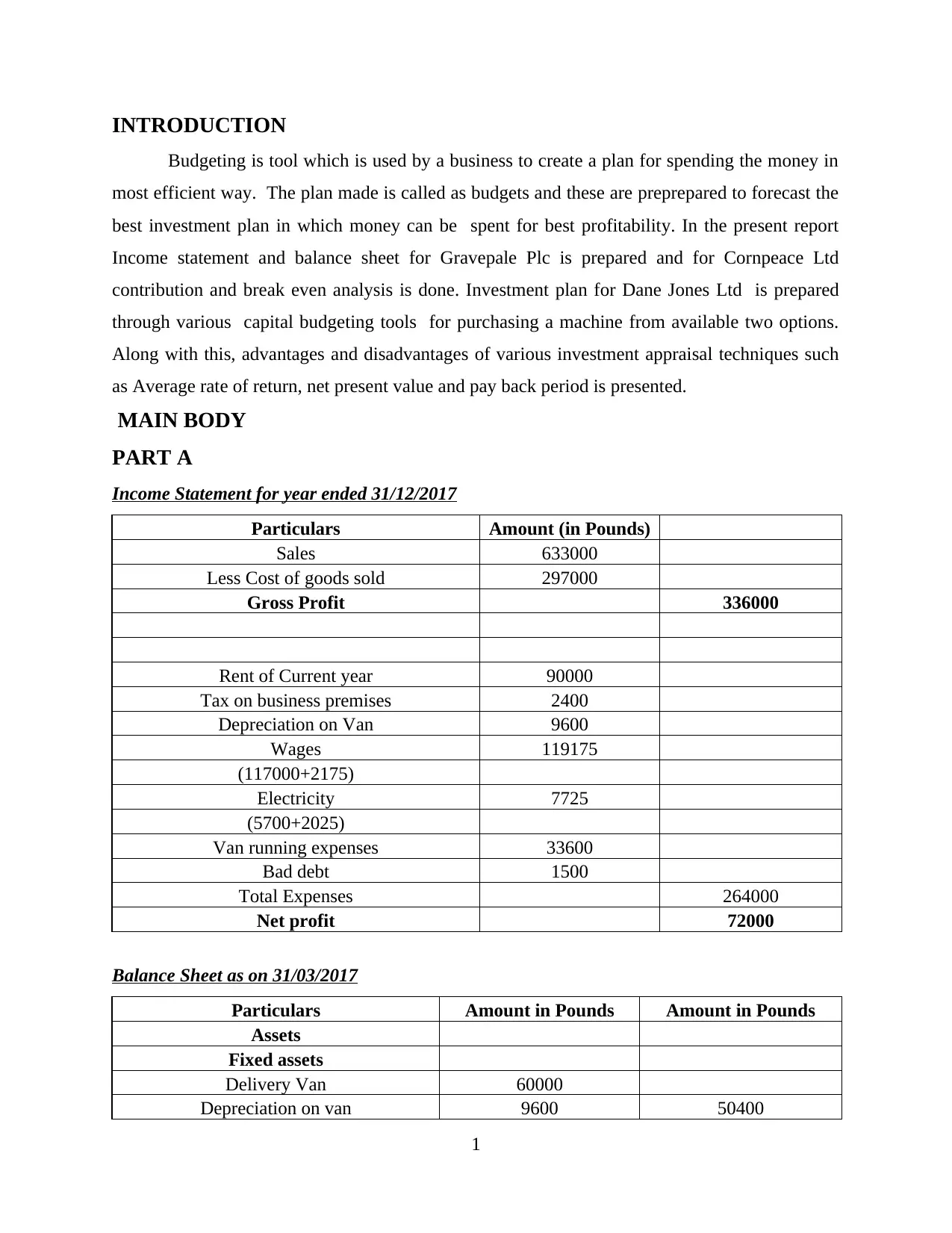

INTRODUCTION

Budgeting is tool which is used by a business to create a plan for spending the money in

most efficient way. The plan made is called as budgets and these are preprepared to forecast the

best investment plan in which money can be spent for best profitability. In the present report

Income statement and balance sheet for Gravepale Plc is prepared and for Cornpeace Ltd

contribution and break even analysis is done. Investment plan for Dane Jones Ltd is prepared

through various capital budgeting tools for purchasing a machine from available two options.

Along with this, advantages and disadvantages of various investment appraisal techniques such

as Average rate of return, net present value and pay back period is presented.

MAIN BODY

PART A

Income Statement for year ended 31/12/2017

Particulars Amount (in Pounds)

Sales 633000

Less Cost of goods sold 297000

Gross Profit 336000

Rent of Current year 90000

Tax on business premises 2400

Depreciation on Van 9600

Wages 119175

(117000+2175)

Electricity 7725

(5700+2025)

Van running expenses 33600

Bad debt 1500

Total Expenses 264000

Net profit 72000

Balance Sheet as on 31/03/2017

Particulars Amount in Pounds Amount in Pounds

Assets

Fixed assets

Delivery Van 60000

Depreciation on van 9600 50400

1

Budgeting is tool which is used by a business to create a plan for spending the money in

most efficient way. The plan made is called as budgets and these are preprepared to forecast the

best investment plan in which money can be spent for best profitability. In the present report

Income statement and balance sheet for Gravepale Plc is prepared and for Cornpeace Ltd

contribution and break even analysis is done. Investment plan for Dane Jones Ltd is prepared

through various capital budgeting tools for purchasing a machine from available two options.

Along with this, advantages and disadvantages of various investment appraisal techniques such

as Average rate of return, net present value and pay back period is presented.

MAIN BODY

PART A

Income Statement for year ended 31/12/2017

Particulars Amount (in Pounds)

Sales 633000

Less Cost of goods sold 297000

Gross Profit 336000

Rent of Current year 90000

Tax on business premises 2400

Depreciation on Van 9600

Wages 119175

(117000+2175)

Electricity 7725

(5700+2025)

Van running expenses 33600

Bad debt 1500

Total Expenses 264000

Net profit 72000

Balance Sheet as on 31/03/2017

Particulars Amount in Pounds Amount in Pounds

Assets

Fixed assets

Delivery Van 60000

Depreciation on van 9600 50400

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current assets

Accounts Receivables 64500

Closing Stock 228000

Prepaid Rent 22500

(112500-90000)

Prepaid tax 4500

Total Assets 369900

Liabilities and shareholder’s equity

Shareholders’ equity

Capital 180000

Add Net Profit 72000 252000

Current Liabilities

O/s wages 2175

O/s Electricity 2025

Bank overdraft 20700

Accounts Payables 93000

Total Liabilities and shareholder’s

equity 369900

Working notes

Bank a/c

Particulars Amount in Pounds

bank 180000

rent -112500

rates -6900

wages -117000

van -60000

Electricity -5700

Purchase -39000

Cash Sales 129000

Cash Receipts 438000

Cash payments -393000

Van running expenses -33600

Net cash at bank or Bank overdraft -20700

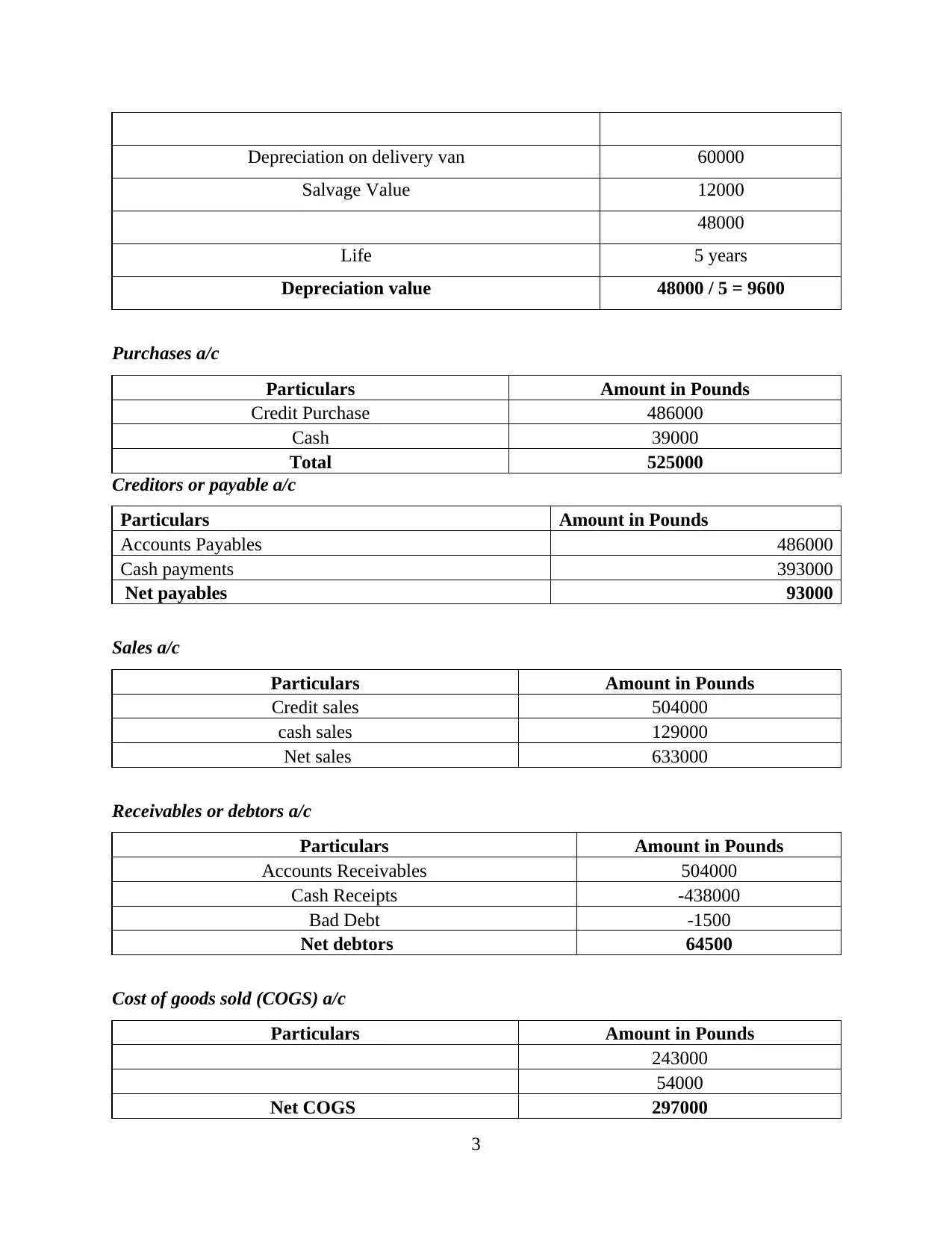

Computation of depreciation

Particulars Amount in Pounds

2

Accounts Receivables 64500

Closing Stock 228000

Prepaid Rent 22500

(112500-90000)

Prepaid tax 4500

Total Assets 369900

Liabilities and shareholder’s equity

Shareholders’ equity

Capital 180000

Add Net Profit 72000 252000

Current Liabilities

O/s wages 2175

O/s Electricity 2025

Bank overdraft 20700

Accounts Payables 93000

Total Liabilities and shareholder’s

equity 369900

Working notes

Bank a/c

Particulars Amount in Pounds

bank 180000

rent -112500

rates -6900

wages -117000

van -60000

Electricity -5700

Purchase -39000

Cash Sales 129000

Cash Receipts 438000

Cash payments -393000

Van running expenses -33600

Net cash at bank or Bank overdraft -20700

Computation of depreciation

Particulars Amount in Pounds

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Depreciation on delivery van 60000

Salvage Value 12000

48000

Life 5 years

Depreciation value 48000 / 5 = 9600

Purchases a/c

Particulars Amount in Pounds

Credit Purchase 486000

Cash 39000

Total 525000

Creditors or payable a/c

Particulars Amount in Pounds

Accounts Payables 486000

Cash payments 393000

Net payables 93000

Sales a/c

Particulars Amount in Pounds

Credit sales 504000

cash sales 129000

Net sales 633000

Receivables or debtors a/c

Particulars Amount in Pounds

Accounts Receivables 504000

Cash Receipts -438000

Bad Debt -1500

Net debtors 64500

Cost of goods sold (COGS) a/c

Particulars Amount in Pounds

243000

54000

Net COGS 297000

3

Salvage Value 12000

48000

Life 5 years

Depreciation value 48000 / 5 = 9600

Purchases a/c

Particulars Amount in Pounds

Credit Purchase 486000

Cash 39000

Total 525000

Creditors or payable a/c

Particulars Amount in Pounds

Accounts Payables 486000

Cash payments 393000

Net payables 93000

Sales a/c

Particulars Amount in Pounds

Credit sales 504000

cash sales 129000

Net sales 633000

Receivables or debtors a/c

Particulars Amount in Pounds

Accounts Receivables 504000

Cash Receipts -438000

Bad Debt -1500

Net debtors 64500

Cost of goods sold (COGS) a/c

Particulars Amount in Pounds

243000

54000

Net COGS 297000

3

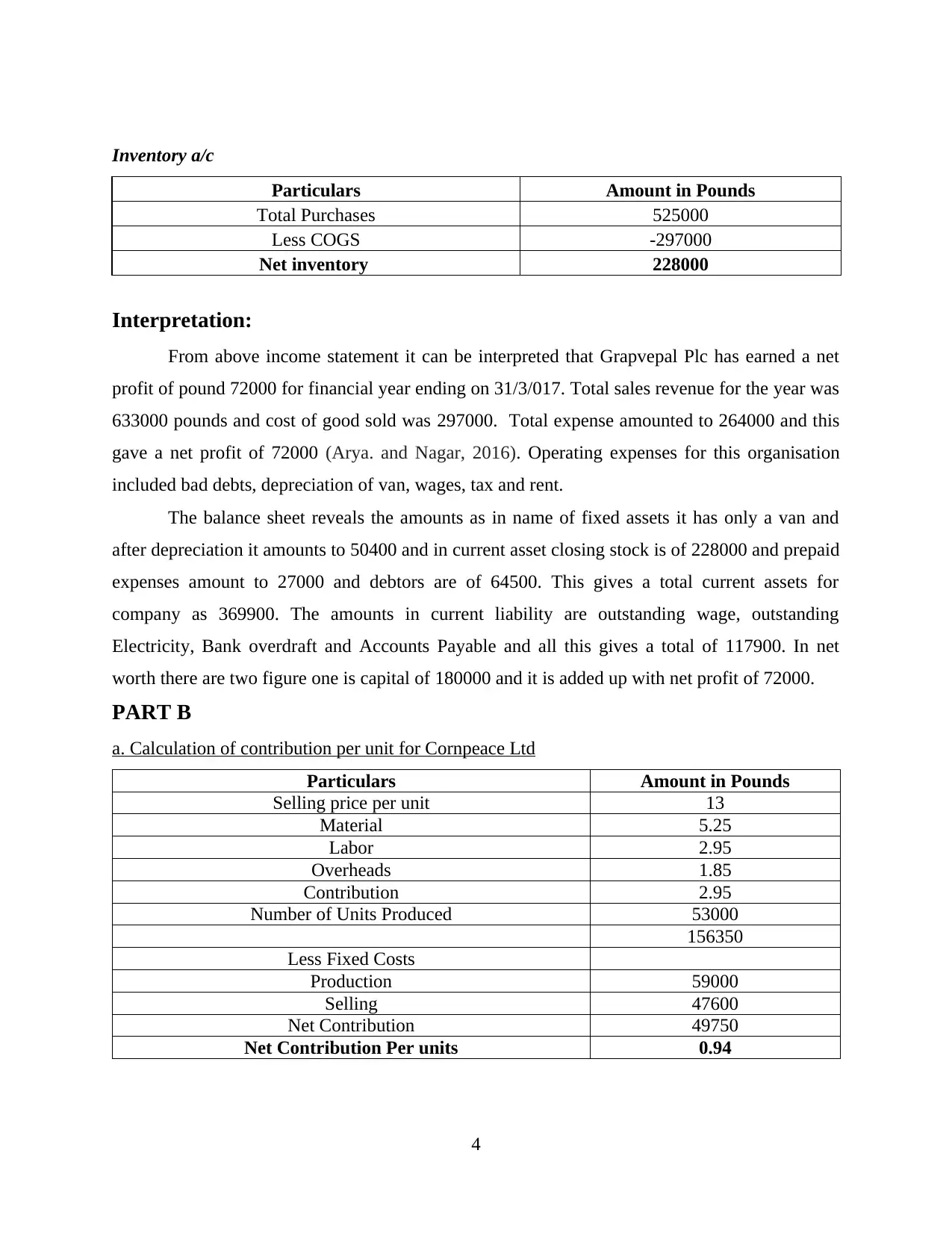

Inventory a/c

Particulars Amount in Pounds

Total Purchases 525000

Less COGS -297000

Net inventory 228000

Interpretation:

From above income statement it can be interpreted that Grapvepal Plc has earned a net

profit of pound 72000 for financial year ending on 31/3/017. Total sales revenue for the year was

633000 pounds and cost of good sold was 297000. Total expense amounted to 264000 and this

gave a net profit of 72000 (Arya. and Nagar, 2016). Operating expenses for this organisation

included bad debts, depreciation of van, wages, tax and rent.

The balance sheet reveals the amounts as in name of fixed assets it has only a van and

after depreciation it amounts to 50400 and in current asset closing stock is of 228000 and prepaid

expenses amount to 27000 and debtors are of 64500. This gives a total current assets for

company as 369900. The amounts in current liability are outstanding wage, outstanding

Electricity, Bank overdraft and Accounts Payable and all this gives a total of 117900. In net

worth there are two figure one is capital of 180000 and it is added up with net profit of 72000.

PART B

a. Calculation of contribution per unit for Cornpeace Ltd

Particulars Amount in Pounds

Selling price per unit 13

Material 5.25

Labor 2.95

Overheads 1.85

Contribution 2.95

Number of Units Produced 53000

156350

Less Fixed Costs

Production 59000

Selling 47600

Net Contribution 49750

Net Contribution Per units 0.94

4

Particulars Amount in Pounds

Total Purchases 525000

Less COGS -297000

Net inventory 228000

Interpretation:

From above income statement it can be interpreted that Grapvepal Plc has earned a net

profit of pound 72000 for financial year ending on 31/3/017. Total sales revenue for the year was

633000 pounds and cost of good sold was 297000. Total expense amounted to 264000 and this

gave a net profit of 72000 (Arya. and Nagar, 2016). Operating expenses for this organisation

included bad debts, depreciation of van, wages, tax and rent.

The balance sheet reveals the amounts as in name of fixed assets it has only a van and

after depreciation it amounts to 50400 and in current asset closing stock is of 228000 and prepaid

expenses amount to 27000 and debtors are of 64500. This gives a total current assets for

company as 369900. The amounts in current liability are outstanding wage, outstanding

Electricity, Bank overdraft and Accounts Payable and all this gives a total of 117900. In net

worth there are two figure one is capital of 180000 and it is added up with net profit of 72000.

PART B

a. Calculation of contribution per unit for Cornpeace Ltd

Particulars Amount in Pounds

Selling price per unit 13

Material 5.25

Labor 2.95

Overheads 1.85

Contribution 2.95

Number of Units Produced 53000

156350

Less Fixed Costs

Production 59000

Selling 47600

Net Contribution 49750

Net Contribution Per units 0.94

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

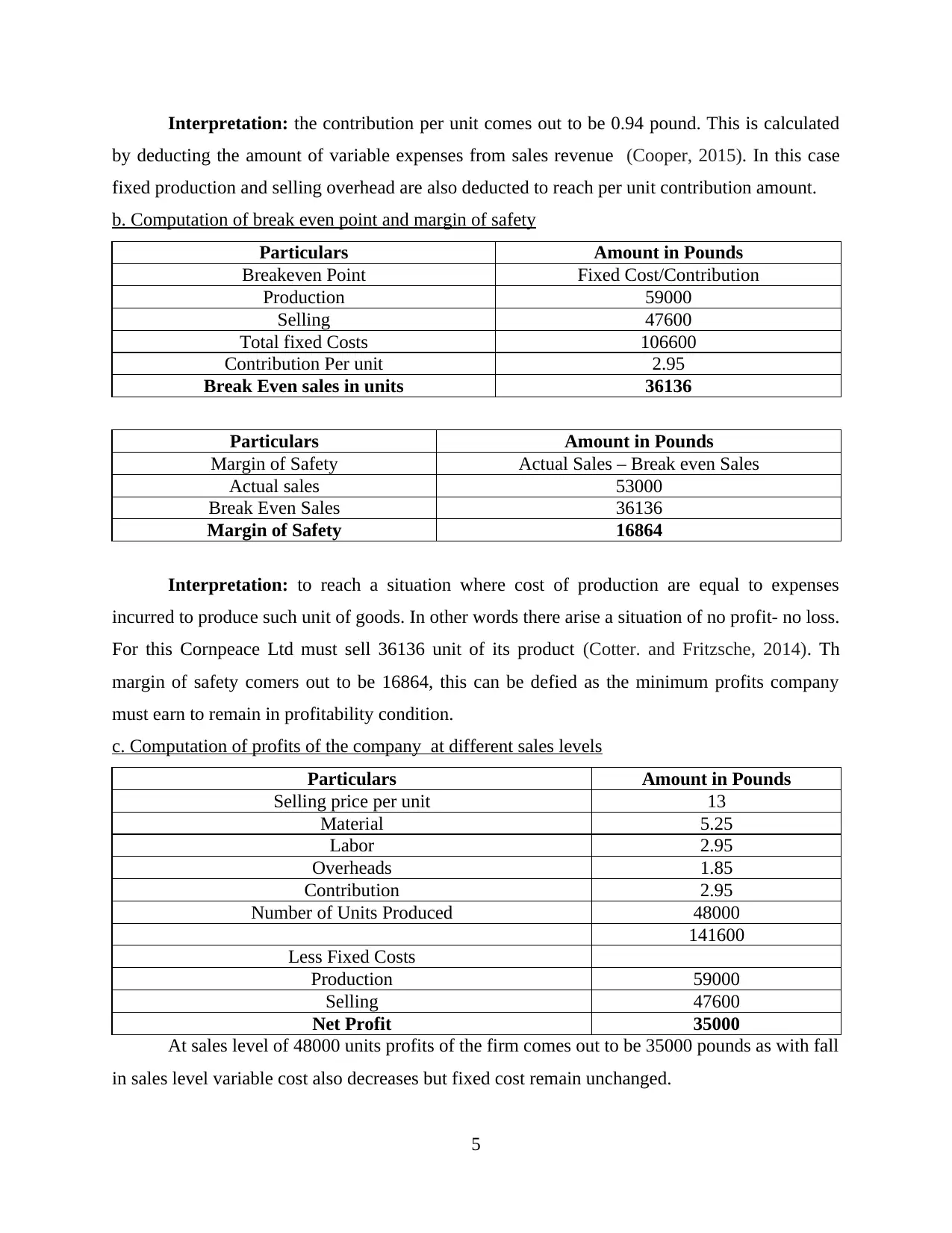

Interpretation: the contribution per unit comes out to be 0.94 pound. This is calculated

by deducting the amount of variable expenses from sales revenue (Cooper, 2015). In this case

fixed production and selling overhead are also deducted to reach per unit contribution amount.

b. Computation of break even point and margin of safety

Particulars Amount in Pounds

Breakeven Point Fixed Cost/Contribution

Production 59000

Selling 47600

Total fixed Costs 106600

Contribution Per unit 2.95

Break Even sales in units 36136

Particulars Amount in Pounds

Margin of Safety Actual Sales – Break even Sales

Actual sales 53000

Break Even Sales 36136

Margin of Safety 16864

Interpretation: to reach a situation where cost of production are equal to expenses

incurred to produce such unit of goods. In other words there arise a situation of no profit- no loss.

For this Cornpeace Ltd must sell 36136 unit of its product (Cotter. and Fritzsche, 2014). Th

margin of safety comers out to be 16864, this can be defied as the minimum profits company

must earn to remain in profitability condition.

c. Computation of profits of the company at different sales levels

Particulars Amount in Pounds

Selling price per unit 13

Material 5.25

Labor 2.95

Overheads 1.85

Contribution 2.95

Number of Units Produced 48000

141600

Less Fixed Costs

Production 59000

Selling 47600

Net Profit 35000

At sales level of 48000 units profits of the firm comes out to be 35000 pounds as with fall

in sales level variable cost also decreases but fixed cost remain unchanged.

5

by deducting the amount of variable expenses from sales revenue (Cooper, 2015). In this case

fixed production and selling overhead are also deducted to reach per unit contribution amount.

b. Computation of break even point and margin of safety

Particulars Amount in Pounds

Breakeven Point Fixed Cost/Contribution

Production 59000

Selling 47600

Total fixed Costs 106600

Contribution Per unit 2.95

Break Even sales in units 36136

Particulars Amount in Pounds

Margin of Safety Actual Sales – Break even Sales

Actual sales 53000

Break Even Sales 36136

Margin of Safety 16864

Interpretation: to reach a situation where cost of production are equal to expenses

incurred to produce such unit of goods. In other words there arise a situation of no profit- no loss.

For this Cornpeace Ltd must sell 36136 unit of its product (Cotter. and Fritzsche, 2014). Th

margin of safety comers out to be 16864, this can be defied as the minimum profits company

must earn to remain in profitability condition.

c. Computation of profits of the company at different sales levels

Particulars Amount in Pounds

Selling price per unit 13

Material 5.25

Labor 2.95

Overheads 1.85

Contribution 2.95

Number of Units Produced 48000

141600

Less Fixed Costs

Production 59000

Selling 47600

Net Profit 35000

At sales level of 48000 units profits of the firm comes out to be 35000 pounds as with fall

in sales level variable cost also decreases but fixed cost remain unchanged.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d. Analysis of the strategy for change in advertisement expenses and sales level

Particulars Amount in Pounds

Selling price per unit 13

Increase in Price 9.00%

14.09

Sales 53000

Increase in units 17.00%

62010

Selling price per unit 13

Material 5.25

Labor 2.95

Overheads 1.85

Contribution 2.95

No. of Units Sold 62010

182930

Less Fixed Costs

Production 59000

Selling 47600

76329.5

Marketing Expenses 45000

31329.5

PART C

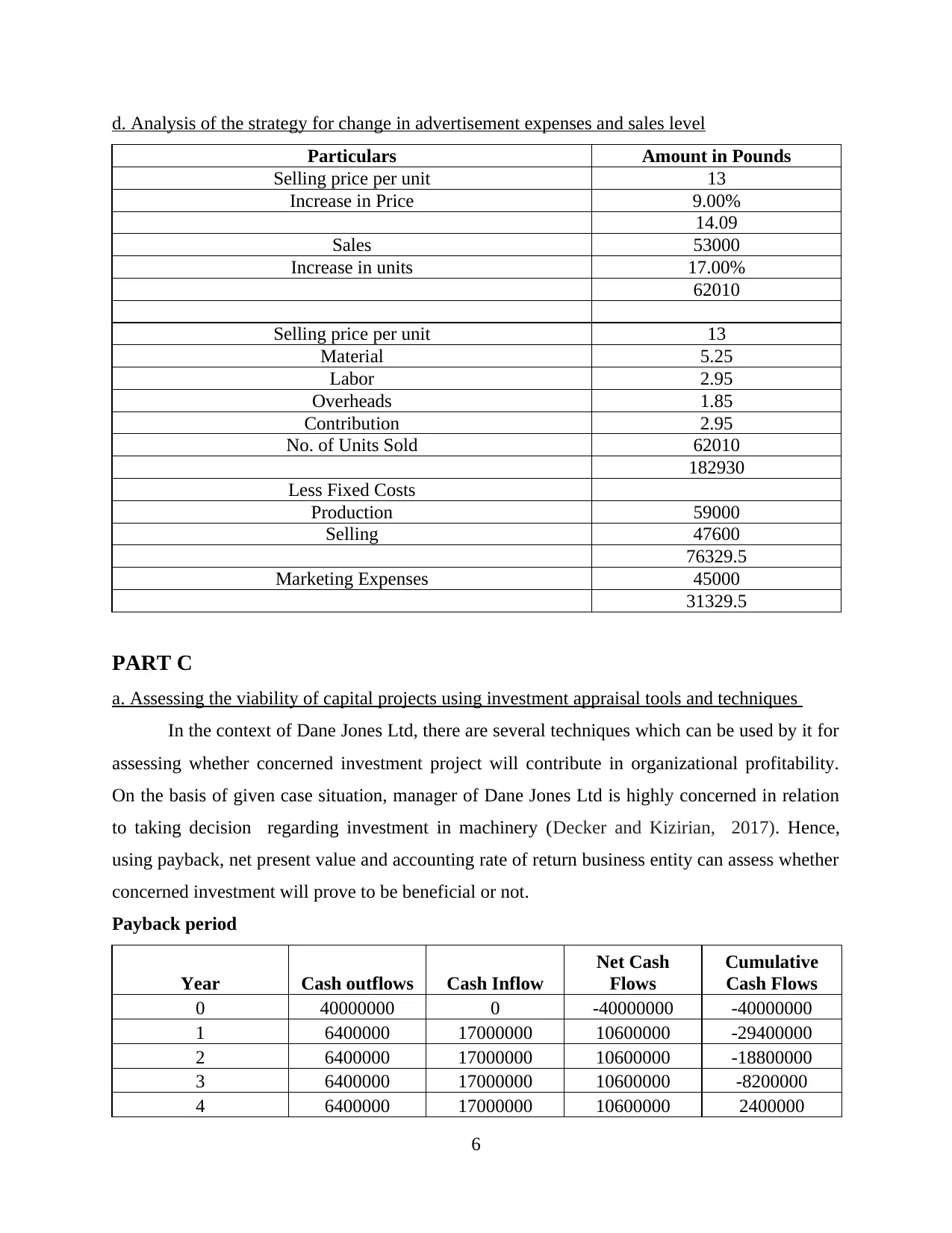

a. Assessing the viability of capital projects using investment appraisal tools and techniques

In the context of Dane Jones Ltd, there are several techniques which can be used by it for

assessing whether concerned investment project will contribute in organizational profitability.

On the basis of given case situation, manager of Dane Jones Ltd is highly concerned in relation

to taking decision regarding investment in machinery (Decker and Kizirian, 2017). Hence,

using payback, net present value and accounting rate of return business entity can assess whether

concerned investment will prove to be beneficial or not.

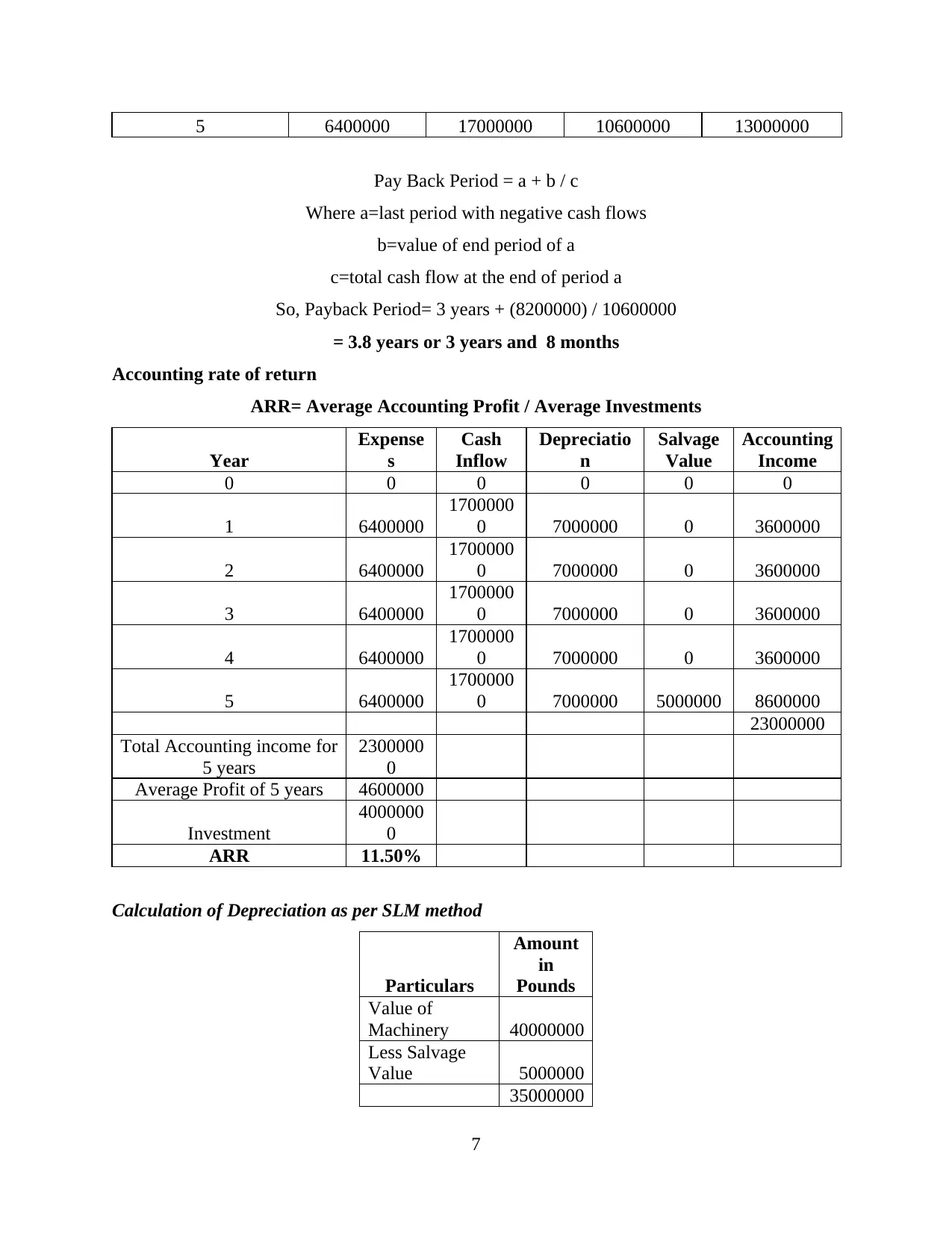

Payback period

Year Cash outflows Cash Inflow

Net Cash

Flows

Cumulative

Cash Flows

0 40000000 0 -40000000 -40000000

1 6400000 17000000 10600000 -29400000

2 6400000 17000000 10600000 -18800000

3 6400000 17000000 10600000 -8200000

4 6400000 17000000 10600000 2400000

6

Particulars Amount in Pounds

Selling price per unit 13

Increase in Price 9.00%

14.09

Sales 53000

Increase in units 17.00%

62010

Selling price per unit 13

Material 5.25

Labor 2.95

Overheads 1.85

Contribution 2.95

No. of Units Sold 62010

182930

Less Fixed Costs

Production 59000

Selling 47600

76329.5

Marketing Expenses 45000

31329.5

PART C

a. Assessing the viability of capital projects using investment appraisal tools and techniques

In the context of Dane Jones Ltd, there are several techniques which can be used by it for

assessing whether concerned investment project will contribute in organizational profitability.

On the basis of given case situation, manager of Dane Jones Ltd is highly concerned in relation

to taking decision regarding investment in machinery (Decker and Kizirian, 2017). Hence,

using payback, net present value and accounting rate of return business entity can assess whether

concerned investment will prove to be beneficial or not.

Payback period

Year Cash outflows Cash Inflow

Net Cash

Flows

Cumulative

Cash Flows

0 40000000 0 -40000000 -40000000

1 6400000 17000000 10600000 -29400000

2 6400000 17000000 10600000 -18800000

3 6400000 17000000 10600000 -8200000

4 6400000 17000000 10600000 2400000

6

5 6400000 17000000 10600000 13000000

Pay Back Period = a + b / c

Where a=last period with negative cash flows

b=value of end period of a

c=total cash flow at the end of period a

So, Payback Period= 3 years + (8200000) / 10600000

= 3.8 years or 3 years and 8 months

Accounting rate of return

ARR= Average Accounting Profit / Average Investments

Year

Expense

s

Cash

Inflow

Depreciatio

n

Salvage

Value

Accounting

Income

0 0 0 0 0 0

1 6400000

1700000

0 7000000 0 3600000

2 6400000

1700000

0 7000000 0 3600000

3 6400000

1700000

0 7000000 0 3600000

4 6400000

1700000

0 7000000 0 3600000

5 6400000

1700000

0 7000000 5000000 8600000

23000000

Total Accounting income for

5 years

2300000

0

Average Profit of 5 years 4600000

Investment

4000000

0

ARR 11.50%

Calculation of Depreciation as per SLM method

Particulars

Amount

in

Pounds

Value of

Machinery 40000000

Less Salvage

Value 5000000

35000000

7

Pay Back Period = a + b / c

Where a=last period with negative cash flows

b=value of end period of a

c=total cash flow at the end of period a

So, Payback Period= 3 years + (8200000) / 10600000

= 3.8 years or 3 years and 8 months

Accounting rate of return

ARR= Average Accounting Profit / Average Investments

Year

Expense

s

Cash

Inflow

Depreciatio

n

Salvage

Value

Accounting

Income

0 0 0 0 0 0

1 6400000

1700000

0 7000000 0 3600000

2 6400000

1700000

0 7000000 0 3600000

3 6400000

1700000

0 7000000 0 3600000

4 6400000

1700000

0 7000000 0 3600000

5 6400000

1700000

0 7000000 5000000 8600000

23000000

Total Accounting income for

5 years

2300000

0

Average Profit of 5 years 4600000

Investment

4000000

0

ARR 11.50%

Calculation of Depreciation as per SLM method

Particulars

Amount

in

Pounds

Value of

Machinery 40000000

Less Salvage

Value 5000000

35000000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

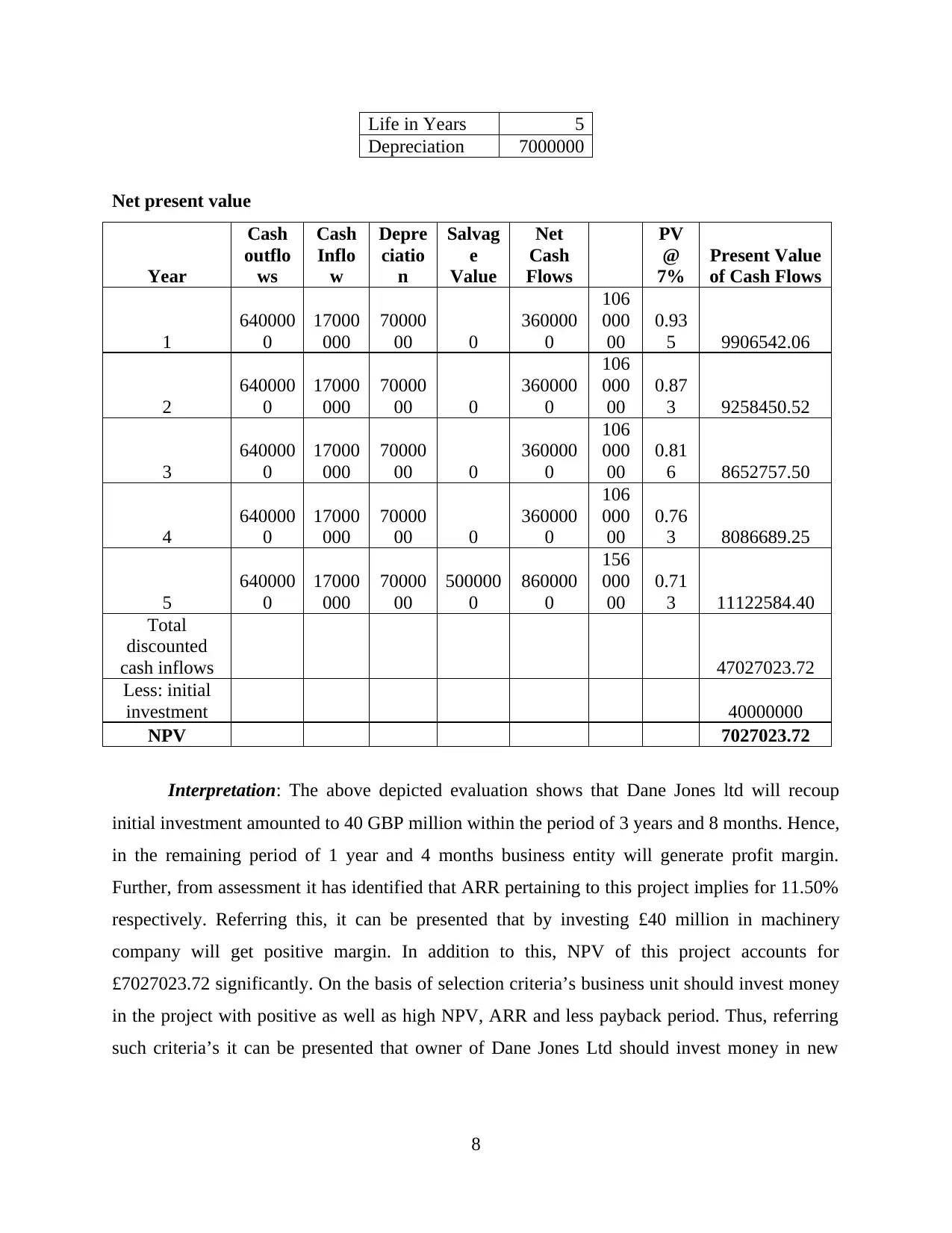

Life in Years 5

Depreciation 7000000

Net present value

Year

Cash

outflo

ws

Cash

Inflo

w

Depre

ciatio

n

Salvag

e

Value

Net

Cash

Flows

PV

@

7%

Present Value

of Cash Flows

1

640000

0

17000

000

70000

00 0

360000

0

106

000

00

0.93

5 9906542.06

2

640000

0

17000

000

70000

00 0

360000

0

106

000

00

0.87

3 9258450.52

3

640000

0

17000

000

70000

00 0

360000

0

106

000

00

0.81

6 8652757.50

4

640000

0

17000

000

70000

00 0

360000

0

106

000

00

0.76

3 8086689.25

5

640000

0

17000

000

70000

00

500000

0

860000

0

156

000

00

0.71

3 11122584.40

Total

discounted

cash inflows 47027023.72

Less: initial

investment 40000000

NPV 7027023.72

Interpretation: The above depicted evaluation shows that Dane Jones ltd will recoup

initial investment amounted to 40 GBP million within the period of 3 years and 8 months. Hence,

in the remaining period of 1 year and 4 months business entity will generate profit margin.

Further, from assessment it has identified that ARR pertaining to this project implies for 11.50%

respectively. Referring this, it can be presented that by investing £40 million in machinery

company will get positive margin. In addition to this, NPV of this project accounts for

£7027023.72 significantly. On the basis of selection criteria’s business unit should invest money

in the project with positive as well as high NPV, ARR and less payback period. Thus, referring

such criteria’s it can be presented that owner of Dane Jones Ltd should invest money in new

8

Depreciation 7000000

Net present value

Year

Cash

outflo

ws

Cash

Inflo

w

Depre

ciatio

n

Salvag

e

Value

Net

Cash

Flows

PV

@

7%

Present Value

of Cash Flows

1

640000

0

17000

000

70000

00 0

360000

0

106

000

00

0.93

5 9906542.06

2

640000

0

17000

000

70000

00 0

360000

0

106

000

00

0.87

3 9258450.52

3

640000

0

17000

000

70000

00 0

360000

0

106

000

00

0.81

6 8652757.50

4

640000

0

17000

000

70000

00 0

360000

0

106

000

00

0.76

3 8086689.25

5

640000

0

17000

000

70000

00

500000

0

860000

0

156

000

00

0.71

3 11122584.40

Total

discounted

cash inflows 47027023.72

Less: initial

investment 40000000

NPV 7027023.72

Interpretation: The above depicted evaluation shows that Dane Jones ltd will recoup

initial investment amounted to 40 GBP million within the period of 3 years and 8 months. Hence,

in the remaining period of 1 year and 4 months business entity will generate profit margin.

Further, from assessment it has identified that ARR pertaining to this project implies for 11.50%

respectively. Referring this, it can be presented that by investing £40 million in machinery

company will get positive margin. In addition to this, NPV of this project accounts for

£7027023.72 significantly. On the basis of selection criteria’s business unit should invest money

in the project with positive as well as high NPV, ARR and less payback period. Thus, referring

such criteria’s it can be presented that owner of Dane Jones Ltd should invest money in new

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

machinery. As, it will provide firm with positive and high returns which in turn makes

contribution in the achievement of organizational goals.

B. Advantages and disadvantages of different investment appraisal techniques

PAY BACK PERIOD- this is a non discounting traditional method of capital budgeting.

It is considered as simplest and is most widely used quantitative tool for appraisal of a capital

investment decision. In this, numbers of years are taken are determined for recovering the

original initial cash outflows invested in project (BUDGET RESOURCE, 2018). There are two

method for calculartion of pay back period

(I) PBP= Initial Investment/Constant Annual Cash flow

(II)PBP= first cumulative cash flow for each year is calculated and year in which initial

invest is recovered is found out. In case amount is recovered in a part of year then it is

calculated on pro rata basis.

Decision rule:

PBP < maximum acceptable payback period = accept PBP > maximum acceptable payback period = reject

Advantages:

This method is simple both in understanding and application and does not include

complicated calculations.

Cost effective method as does requires experts for commutation so no need to hire

financial executive ans is less time consuming.

This method deals with risk as project which generates cash flow in starting years are

considered and project which generate cash in later years are discarded. This is a method of liquidity as project selection is on basis of earlier recovery of output

cash.

Disadvantages:

This method do not consider time value of money.

This method only take into account capital investment recovery but not profitability

which is main aim of every business.

Project in this method are not given preference as per their cash flow patters rather on

basis of recovery of initial investment.

Cash inflow beyond pay back period is ignored.

9

contribution in the achievement of organizational goals.

B. Advantages and disadvantages of different investment appraisal techniques

PAY BACK PERIOD- this is a non discounting traditional method of capital budgeting.

It is considered as simplest and is most widely used quantitative tool for appraisal of a capital

investment decision. In this, numbers of years are taken are determined for recovering the

original initial cash outflows invested in project (BUDGET RESOURCE, 2018). There are two

method for calculartion of pay back period

(I) PBP= Initial Investment/Constant Annual Cash flow

(II)PBP= first cumulative cash flow for each year is calculated and year in which initial

invest is recovered is found out. In case amount is recovered in a part of year then it is

calculated on pro rata basis.

Decision rule:

PBP < maximum acceptable payback period = accept PBP > maximum acceptable payback period = reject

Advantages:

This method is simple both in understanding and application and does not include

complicated calculations.

Cost effective method as does requires experts for commutation so no need to hire

financial executive ans is less time consuming.

This method deals with risk as project which generates cash flow in starting years are

considered and project which generate cash in later years are discarded. This is a method of liquidity as project selection is on basis of earlier recovery of output

cash.

Disadvantages:

This method do not consider time value of money.

This method only take into account capital investment recovery but not profitability

which is main aim of every business.

Project in this method are not given preference as per their cash flow patters rather on

basis of recovery of initial investment.

Cash inflow beyond pay back period is ignored.

9

NET PRESENT VALUE- this is a discounting cash flow or time adjustment technique. In this

method, present value of future cash flow is considered. Recognition of cash flows at different

time period is done in this method.

The NPV can be calculated with the help of equation:-

NPV = Present value of cash inflows – Initial investment

Decision Rule:

If the,

NPV >0, accept the project.

NPV < 0, reject the project.

Advantages:

In this method the time value of money is recognized.

Cash flows of all years are considered over its useful life.

It is an independent measurement of profits earned ion a project.

This is the only method which fulfill the value-additive principle. Outputs are calculated

on absolute terms, and NPV of projects can be added to reach a decision. This method is consistent with wealth maximization goal of shareholders.

Disadvantages:

Estimation cash flow is required in this method which is a difficult task due to

involvement of uncertainties related with business environment.

While valuation of project is carried out contingencies are not fully considered in this

method.

The value of exploring other option is ignored in this method.

In case of mutually exclusive projects, reasonable results are not found as projects have

unequal life, different cash flows, outflows.

Calculation under this method are complicated as discounted cash flows are determined

on given rate of return. The rate must be taken same as different rate will give changed

result (Sunder, Sunder and Zhang, 2018).

AVERAGE RATE OF RETURN- this is also known as return on investment(ROI), return on

capital employed (ROEC) and considers accounting information rather than cash flows.

Calculation under this is done as:

ARR= Average annual profits after tax * 100

10

method, present value of future cash flow is considered. Recognition of cash flows at different

time period is done in this method.

The NPV can be calculated with the help of equation:-

NPV = Present value of cash inflows – Initial investment

Decision Rule:

If the,

NPV >0, accept the project.

NPV < 0, reject the project.

Advantages:

In this method the time value of money is recognized.

Cash flows of all years are considered over its useful life.

It is an independent measurement of profits earned ion a project.

This is the only method which fulfill the value-additive principle. Outputs are calculated

on absolute terms, and NPV of projects can be added to reach a decision. This method is consistent with wealth maximization goal of shareholders.

Disadvantages:

Estimation cash flow is required in this method which is a difficult task due to

involvement of uncertainties related with business environment.

While valuation of project is carried out contingencies are not fully considered in this

method.

The value of exploring other option is ignored in this method.

In case of mutually exclusive projects, reasonable results are not found as projects have

unequal life, different cash flows, outflows.

Calculation under this method are complicated as discounted cash flows are determined

on given rate of return. The rate must be taken same as different rate will give changed

result (Sunder, Sunder and Zhang, 2018).

AVERAGE RATE OF RETURN- this is also known as return on investment(ROI), return on

capital employed (ROEC) and considers accounting information rather than cash flows.

Calculation under this is done as:

ARR= Average annual profits after tax * 100

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.