Conventional Cost Allocation with Job Order Costing - Week 4 Notes

VerifiedAdded on 2024/04/29

|26

|5222

|55

AI Summary

This document covers conventional cost allocation with job order costing, discussing product and service costing, flow of costs in manufacturing firms, types of product costing systems, job-order costing, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCT6008 WEEK4 NOTES

Conventional Cost Allocation with Job Order Costing

Required study prior to attending workshop in Week 4:

1. Read Hilton 13th ed., Chapter 3

2. Complete and compare answers with solutions provided (on Canvas) for the following

Chapter 3 questions:

– Part A, Simple exercises to reinforce basic concepts: 3-5, 3-8, 3-10, 3-11, 3- 17, 3-18

– Part B, More advanced exercises with more realistic scenarios and data: 3-24, 3-28, 3-37

– Part C, Exam standard (or higher) questions: 3-48, 3-54, 3-55, 3-60

*3-55 will be the basis for the business practical in the workshop, and therefore the

solutions are not given.

Learning outcomes

1. Discuss the role of product and service costing in manufacturing and non-manufacturing

firms.

2. Diagram and explain the flow of costs through the manufacturing accounts used in

product costing.

3. Distinguish between job-order costing and process costing.

4. Distinguish between direct and indirect costs via traceability and cost objects.

5. Compute a predetermined overhead rate and explain its use in job-order costing.

6. Prepare a schedule of cost of goods manufactured, a schedule of cost of goods sold, and

an income statement for a manufacturer (preparation of journal entries is not required).

7. Describe the two-stage allocation process used to assign manufacturing overhead costs to

production jobs.

8. Describe the process of project (job) costing used in service firms and non-profit

organisations.

Product and service costing

Product and Service Costing

Financial Accounting: Product costs are used to value inventory on the balance sheet and to

compute cost of goods sold on the income statement.

Managerial Accounting and Cost Management: Product costs are used for planning, control,

directing, and management decision making.

Other Interested Organisations: There is an ever increasing need to use data for external

organisations as well. e.g. interaction with government agencies.

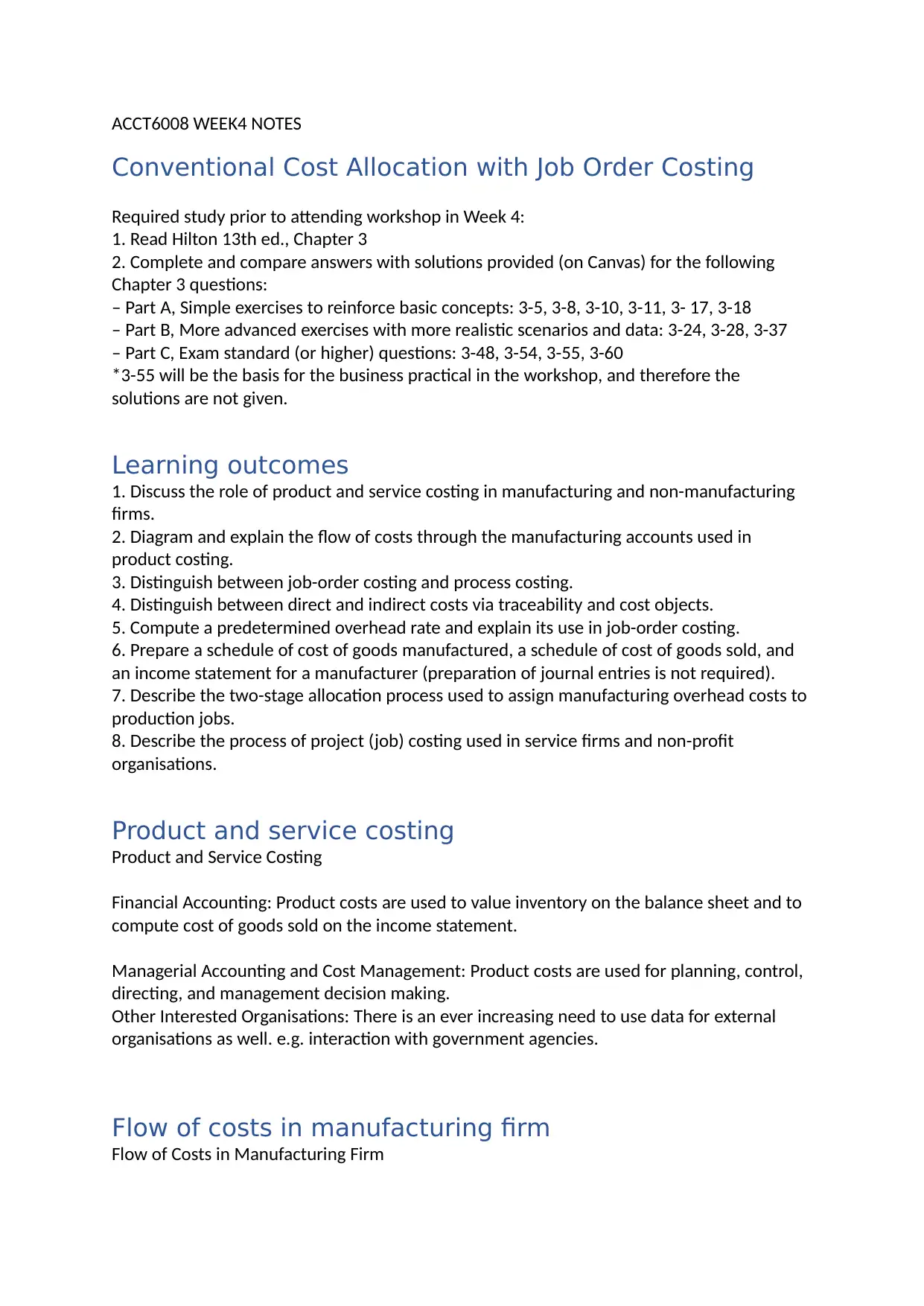

Flow of costs in manufacturing firm

Flow of Costs in Manufacturing Firm

Conventional Cost Allocation with Job Order Costing

Required study prior to attending workshop in Week 4:

1. Read Hilton 13th ed., Chapter 3

2. Complete and compare answers with solutions provided (on Canvas) for the following

Chapter 3 questions:

– Part A, Simple exercises to reinforce basic concepts: 3-5, 3-8, 3-10, 3-11, 3- 17, 3-18

– Part B, More advanced exercises with more realistic scenarios and data: 3-24, 3-28, 3-37

– Part C, Exam standard (or higher) questions: 3-48, 3-54, 3-55, 3-60

*3-55 will be the basis for the business practical in the workshop, and therefore the

solutions are not given.

Learning outcomes

1. Discuss the role of product and service costing in manufacturing and non-manufacturing

firms.

2. Diagram and explain the flow of costs through the manufacturing accounts used in

product costing.

3. Distinguish between job-order costing and process costing.

4. Distinguish between direct and indirect costs via traceability and cost objects.

5. Compute a predetermined overhead rate and explain its use in job-order costing.

6. Prepare a schedule of cost of goods manufactured, a schedule of cost of goods sold, and

an income statement for a manufacturer (preparation of journal entries is not required).

7. Describe the two-stage allocation process used to assign manufacturing overhead costs to

production jobs.

8. Describe the process of project (job) costing used in service firms and non-profit

organisations.

Product and service costing

Product and Service Costing

Financial Accounting: Product costs are used to value inventory on the balance sheet and to

compute cost of goods sold on the income statement.

Managerial Accounting and Cost Management: Product costs are used for planning, control,

directing, and management decision making.

Other Interested Organisations: There is an ever increasing need to use data for external

organisations as well. e.g. interaction with government agencies.

Flow of costs in manufacturing firm

Flow of Costs in Manufacturing Firm

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cost concept General terms:

1. Cost—a sacrificed or forgone resource to achieve a specific objective

2. Actual cost—a cost that has occurred

3. Budgeted cost—a predicted cost

4. Cost object—anything for which a cost measurement is desired

5. Cost driver—a variable, such as the level of activity or volume, that causally affects costs

over a given time span

1) Product cost VS period cost

Product cost: cost assigned to inventory (we dr to asset first, when sold we dr to expense)

AKA inventoriable cost

= Direct material + direct labour + manufacturing overhead

Direct material eg: steel that used on the car

Direct labour eg: staff’s salary that directly work on the production line

Manufacturing overhead eg: electircity; production department manager’s salary

Period cost: cost that expensed during the period in which they are incurred Eg: marketing

expense/ administration expense

Direct cost VS indirect cost

Cost object: anything can be a cost object. When you want to calculate the cost of a specific

object (eg: a product/ a customer/a department), this object is the cost object.

Direct cost: economically, conveniently, traceable to the cost object Indirect cost: costs that

are not direct cost (eg: manufacturing overhead)

Variable cost VS Fixed cost 可可 VS 可可可可

Variable cost 可可可可:changes, in total, in direct proportion to a change in the level of

activity (or cost driver).

Fixed cost 可可可可:remains unchanged in total as the level of activity (or cost driver) varies.

Relevant range: the span of activity levels for which the cost behaviour patterns hold. Mixed

costs are partly fixed and partly variable.

Direct materials—resources in stock and available for use‐

Work in process (or progress)—goods partially worked on but not yet completed Finished‐ ‐

goods—goods completed but not yet sold

1. Cost—a sacrificed or forgone resource to achieve a specific objective

2. Actual cost—a cost that has occurred

3. Budgeted cost—a predicted cost

4. Cost object—anything for which a cost measurement is desired

5. Cost driver—a variable, such as the level of activity or volume, that causally affects costs

over a given time span

1) Product cost VS period cost

Product cost: cost assigned to inventory (we dr to asset first, when sold we dr to expense)

AKA inventoriable cost

= Direct material + direct labour + manufacturing overhead

Direct material eg: steel that used on the car

Direct labour eg: staff’s salary that directly work on the production line

Manufacturing overhead eg: electircity; production department manager’s salary

Period cost: cost that expensed during the period in which they are incurred Eg: marketing

expense/ administration expense

Direct cost VS indirect cost

Cost object: anything can be a cost object. When you want to calculate the cost of a specific

object (eg: a product/ a customer/a department), this object is the cost object.

Direct cost: economically, conveniently, traceable to the cost object Indirect cost: costs that

are not direct cost (eg: manufacturing overhead)

Variable cost VS Fixed cost 可可 VS 可可可可

Variable cost 可可可可:changes, in total, in direct proportion to a change in the level of

activity (or cost driver).

Fixed cost 可可可可:remains unchanged in total as the level of activity (or cost driver) varies.

Relevant range: the span of activity levels for which the cost behaviour patterns hold. Mixed

costs are partly fixed and partly variable.

Direct materials—resources in stock and available for use‐

Work in process (or progress)—goods partially worked on but not yet completed Finished‐ ‐

goods—goods completed but not yet sold

Cost of Goods Manufactured Cost of Goods Sold

Total manufacturing costs = direct material + direct labour + overhead

Cost of goods manufactured = beginning WIP inventory +total manufacturing cost – ending

WIP inventory

Cost of goods sold = beginning FG inventory + Cost of goods manufactured – ending FG

inventory

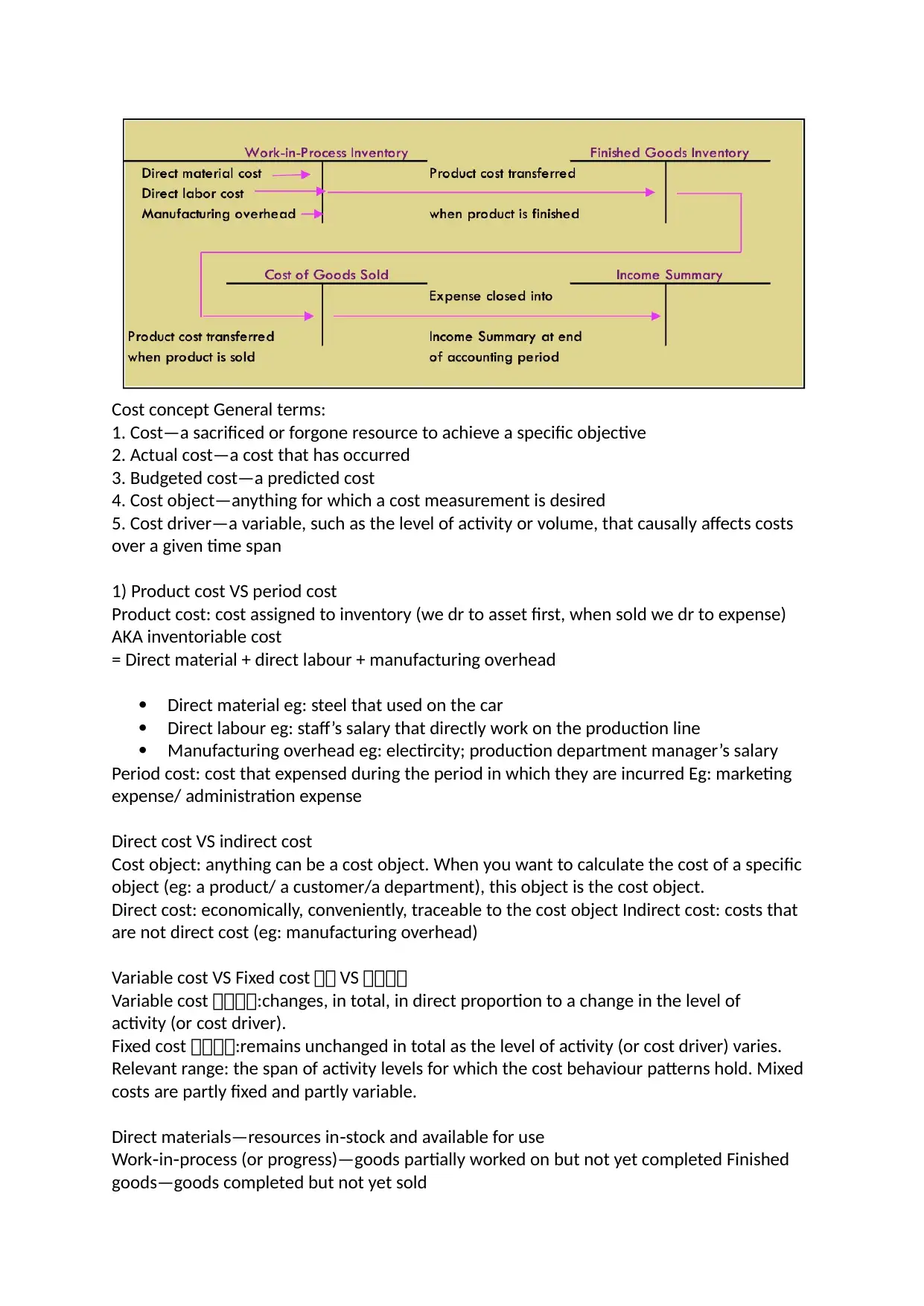

Types of product costing system

Product costing system

Product-costing system accumulates the costs incurred in a production process and assigns

those costs to the organization’s outputs.

Product costing 可可可可可可可可可可 production cost assign 可可可可可可 output 可 Product costing

data 可 financial accounting(value inventory可COGS)可managerial

accounting(可可可可可可可...)可可可可

Types of Product-Costing Systems

1. Process Costing

A process-costing system accumulates all the production costs for a large number of units of

output, and then these costs are averaged over all of the units.

– Used for production of small, identical, low cost items

– Mass produced in automated continuous production process

– Costs cannot be directly traced to each unit of product

Eg: Petrochemical refinery 可可, paint manufacturer 可可, paper mill 可可, 可可可可…

2. Job-Order Costing

Job-order costing is used by companies with job-shop or batch-production manufacturing

processes.

– Used for production of large unique high-cost items

– Built to order rather than mass produced

– Many costs can be directly traced to each job

EG: 可可 可可、

Process Costing

Typical process cost applications:

– Petrochemical refinery

– Paint manufacturer

– Paper mill

Job-Order Costing 可可可可可可可 large, unique, high value product

Two types:

Total manufacturing costs = direct material + direct labour + overhead

Cost of goods manufactured = beginning WIP inventory +total manufacturing cost – ending

WIP inventory

Cost of goods sold = beginning FG inventory + Cost of goods manufactured – ending FG

inventory

Types of product costing system

Product costing system

Product-costing system accumulates the costs incurred in a production process and assigns

those costs to the organization’s outputs.

Product costing 可可可可可可可可可可 production cost assign 可可可可可可 output 可 Product costing

data 可 financial accounting(value inventory可COGS)可managerial

accounting(可可可可可可可...)可可可可

Types of Product-Costing Systems

1. Process Costing

A process-costing system accumulates all the production costs for a large number of units of

output, and then these costs are averaged over all of the units.

– Used for production of small, identical, low cost items

– Mass produced in automated continuous production process

– Costs cannot be directly traced to each unit of product

Eg: Petrochemical refinery 可可, paint manufacturer 可可, paper mill 可可, 可可可可…

2. Job-Order Costing

Job-order costing is used by companies with job-shop or batch-production manufacturing

processes.

– Used for production of large unique high-cost items

– Built to order rather than mass produced

– Many costs can be directly traced to each job

EG: 可可 可可、

Process Costing

Typical process cost applications:

– Petrochemical refinery

– Paint manufacturer

– Paper mill

Job-Order Costing 可可可可可可可 large, unique, high value product

Two types:

1. Job-shop operations

– Products manufactured in very low volumes or one at a time

2. Batch-production operations

– Multiple products in batches of relatively small quantity

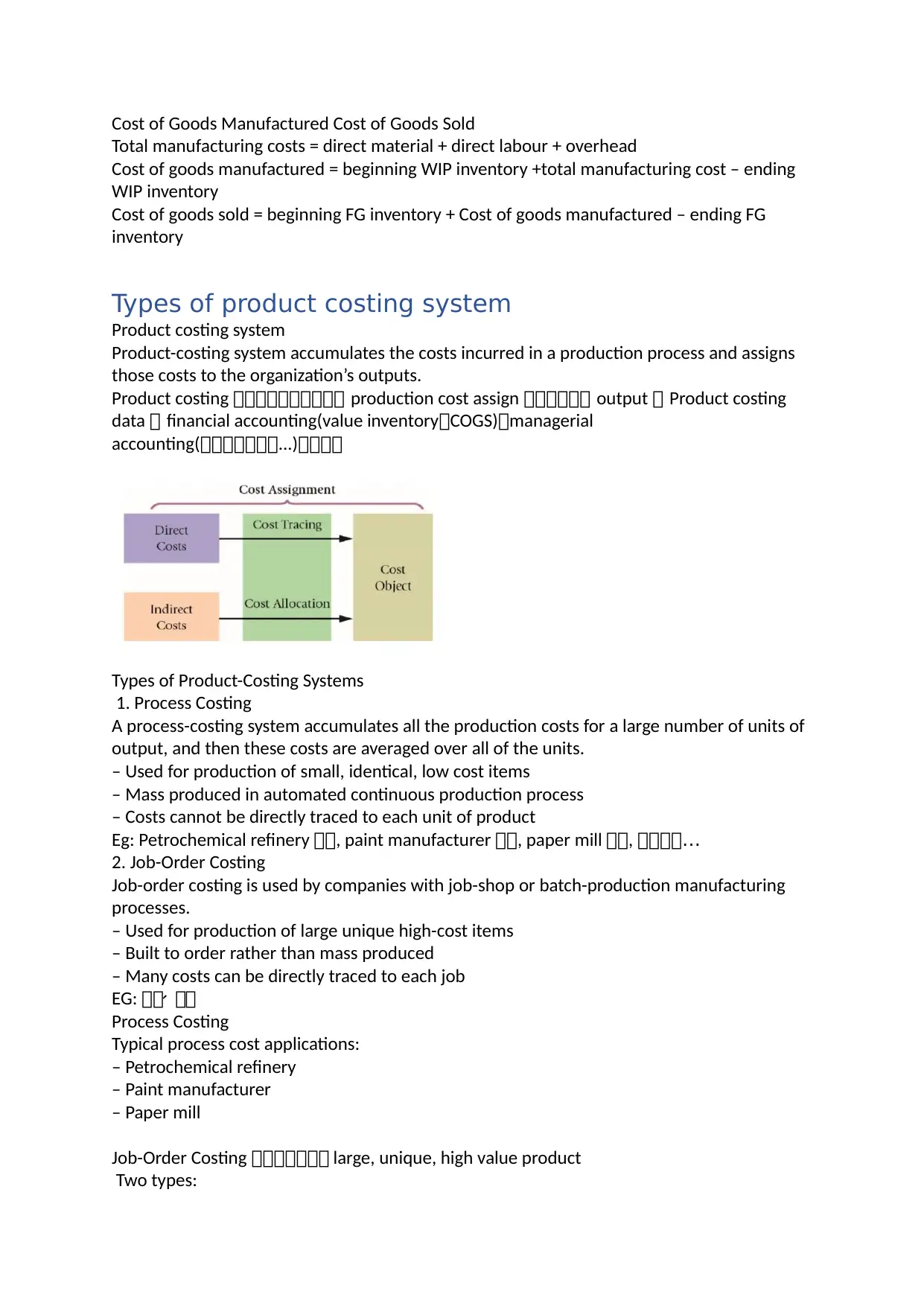

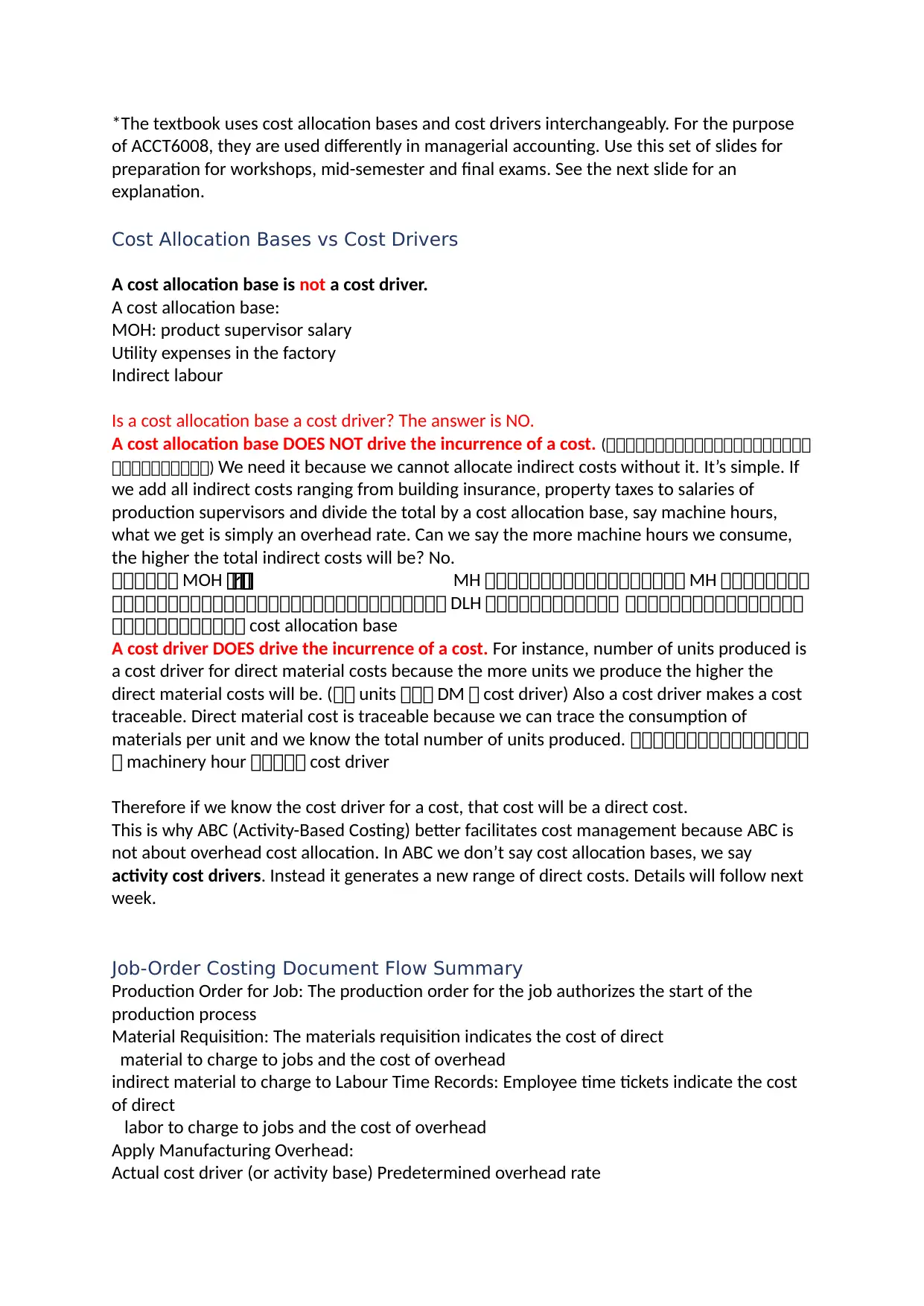

Job Costing System explained (IMPORTANT)

Steps in Job Costing

1. Identify the Job-Order that is the chosen Cost Object

2. Identify the direct and indirect costs of the Job-Order

3. Select the cost allocation base(s) to use for allocating Indirect costs to the Job-Order

4. Match Indirect costs to their respective cost allocation base(s)

5. Calculate an overhead (OH) cost allocation rate(s)

(budgeted or actual) OH Costs ÷ (budgeted or actual) OH allocation base (e.g.

machine hours)

6. Allocate overhead costs to the Job

(budgeted or actual) OH allocation rate x Actual consumption of the allocation base

for the Job

7. Compute Total Job Costs

Sum of all direct costs + all indirect costs

Job order costing 可可可可

1. 可可可可可可 job 可 direct costs 可 indirect costs

2. 可可可可 indirect costs, cost allocation base 可可可? (可可可可可可可可可可可 direct labor hour,

machine hour, etc)可可可可可可可可可可可可可 (可可可可 department 可可可可可可可可可可可)可可可可可可

3. 可可可可 indirect cost pool 可可可可可可可可可可可可可可可可 overhead allocation rate 可可可可可可可可可可。

可可可可可可可可可可可可可可可可可 indirect costs 可 可可可可可可可可可 the amount of cost allocation base 可可可可可可。

可 normal costing VS actual costing 可可可可, 可可可可可可可可可可:

可可可可可可可可可可可可可可 actual costing 可可 normal costing可可可可 MOH rate 可可可可可可可可可可可可可

actual 可可可可可可 budgeted.

4. 可可可可可可 MOH Allocation Rate x Actual consumption of the allocation base for the Job=

Allocated Overhead Costs to the Job

5. 可可可可可可 job 可 direct cost 可可可可可可可可可 MOH可可可可可 job 可可可。

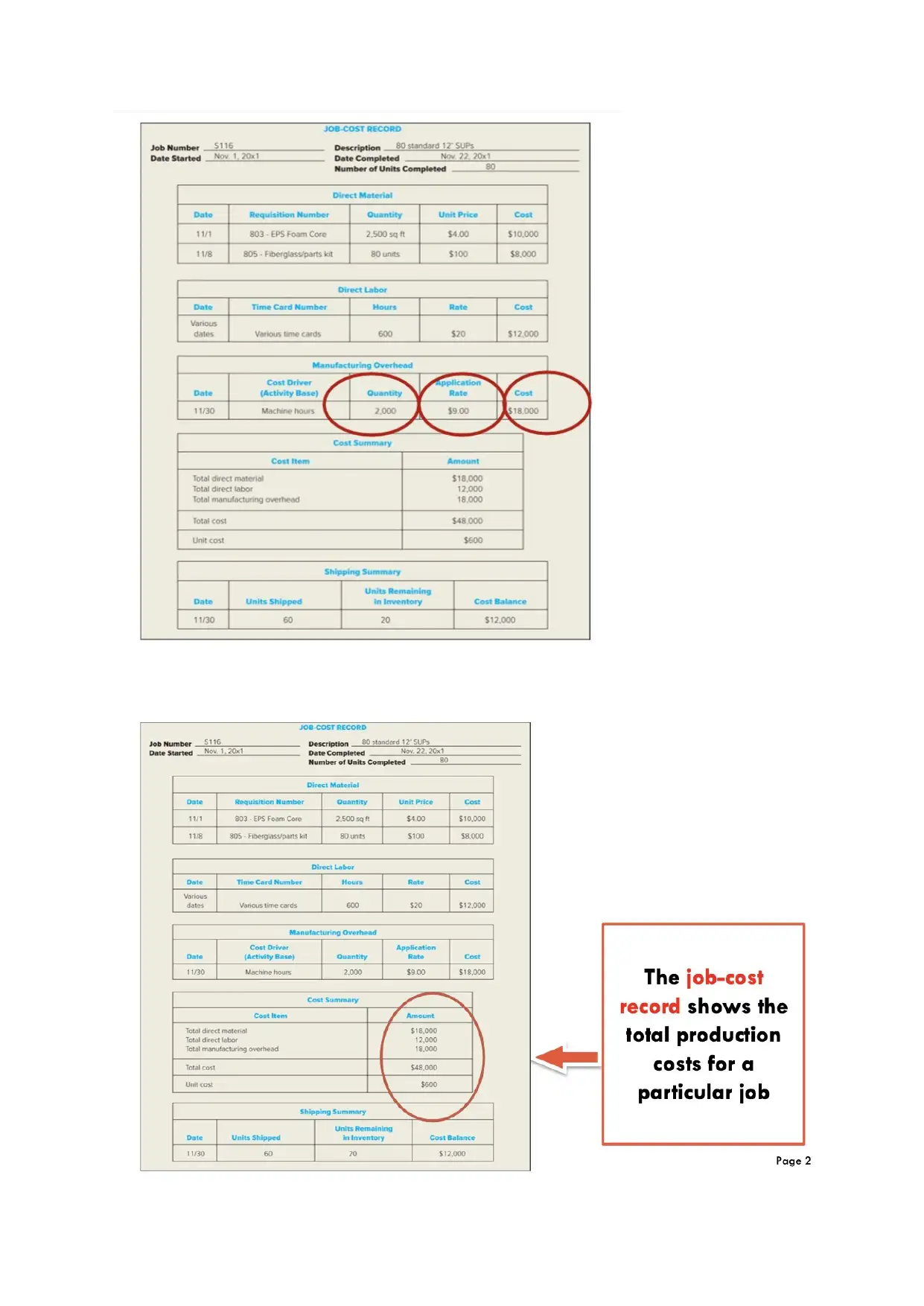

Accumulating Costs in a Job-Order Costing System

The primary document for tracking the costs associated with a given job is the job-cost

record.

– Products manufactured in very low volumes or one at a time

2. Batch-production operations

– Multiple products in batches of relatively small quantity

Job Costing System explained (IMPORTANT)

Steps in Job Costing

1. Identify the Job-Order that is the chosen Cost Object

2. Identify the direct and indirect costs of the Job-Order

3. Select the cost allocation base(s) to use for allocating Indirect costs to the Job-Order

4. Match Indirect costs to their respective cost allocation base(s)

5. Calculate an overhead (OH) cost allocation rate(s)

(budgeted or actual) OH Costs ÷ (budgeted or actual) OH allocation base (e.g.

machine hours)

6. Allocate overhead costs to the Job

(budgeted or actual) OH allocation rate x Actual consumption of the allocation base

for the Job

7. Compute Total Job Costs

Sum of all direct costs + all indirect costs

Job order costing 可可可可

1. 可可可可可可 job 可 direct costs 可 indirect costs

2. 可可可可 indirect costs, cost allocation base 可可可? (可可可可可可可可可可可 direct labor hour,

machine hour, etc)可可可可可可可可可可可可可 (可可可可 department 可可可可可可可可可可可)可可可可可可

3. 可可可可 indirect cost pool 可可可可可可可可可可可可可可可可 overhead allocation rate 可可可可可可可可可可。

可可可可可可可可可可可可可可可可可 indirect costs 可 可可可可可可可可可 the amount of cost allocation base 可可可可可可。

可 normal costing VS actual costing 可可可可, 可可可可可可可可可可:

可可可可可可可可可可可可可可 actual costing 可可 normal costing可可可可 MOH rate 可可可可可可可可可可可可可

actual 可可可可可可 budgeted.

4. 可可可可可可 MOH Allocation Rate x Actual consumption of the allocation base for the Job=

Allocated Overhead Costs to the Job

5. 可可可可可可 job 可 direct cost 可可可可可可可可可 MOH可可可可可 job 可可可。

Accumulating Costs in a Job-Order Costing System

The primary document for tracking the costs associated with a given job is the job-cost

record.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

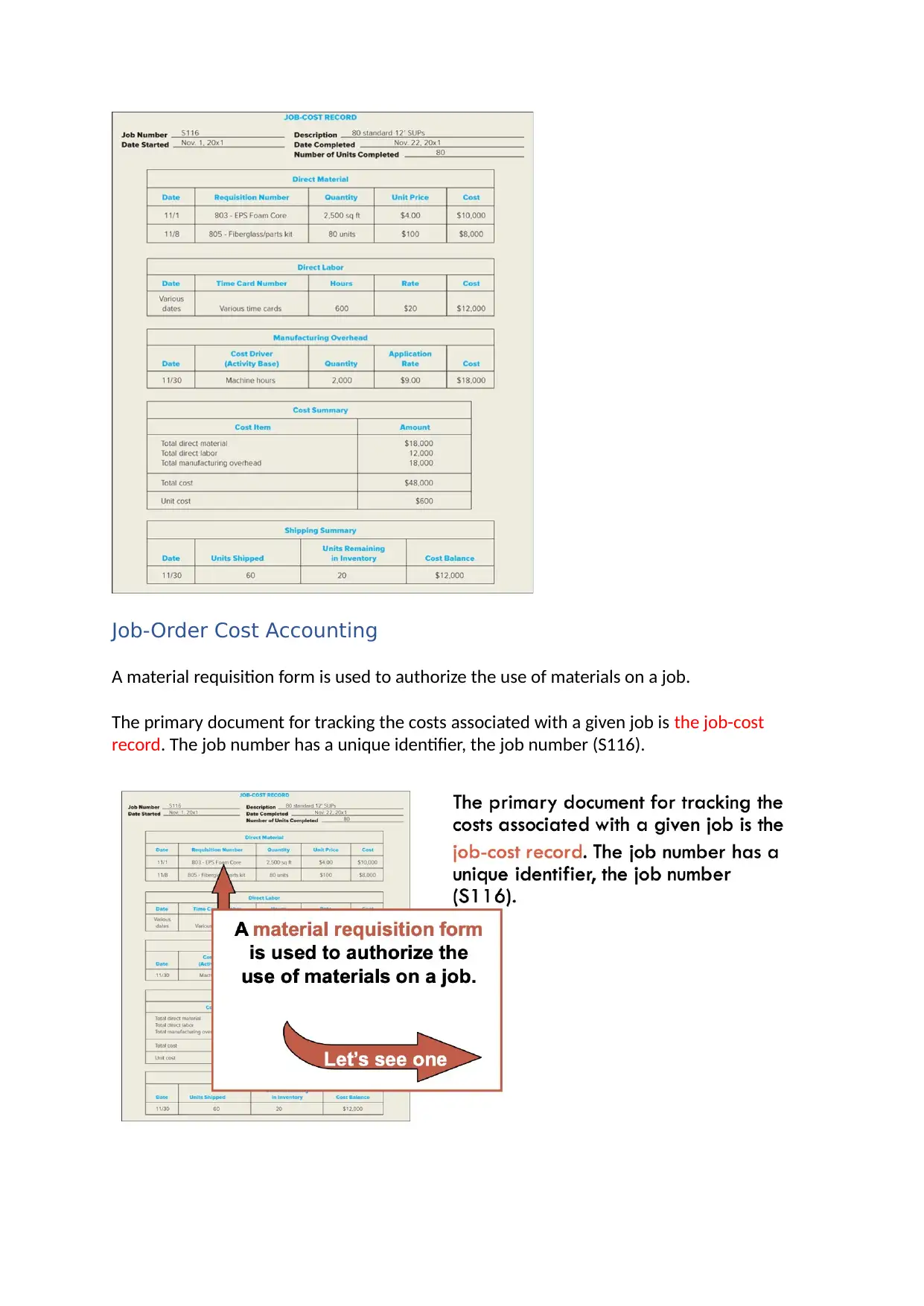

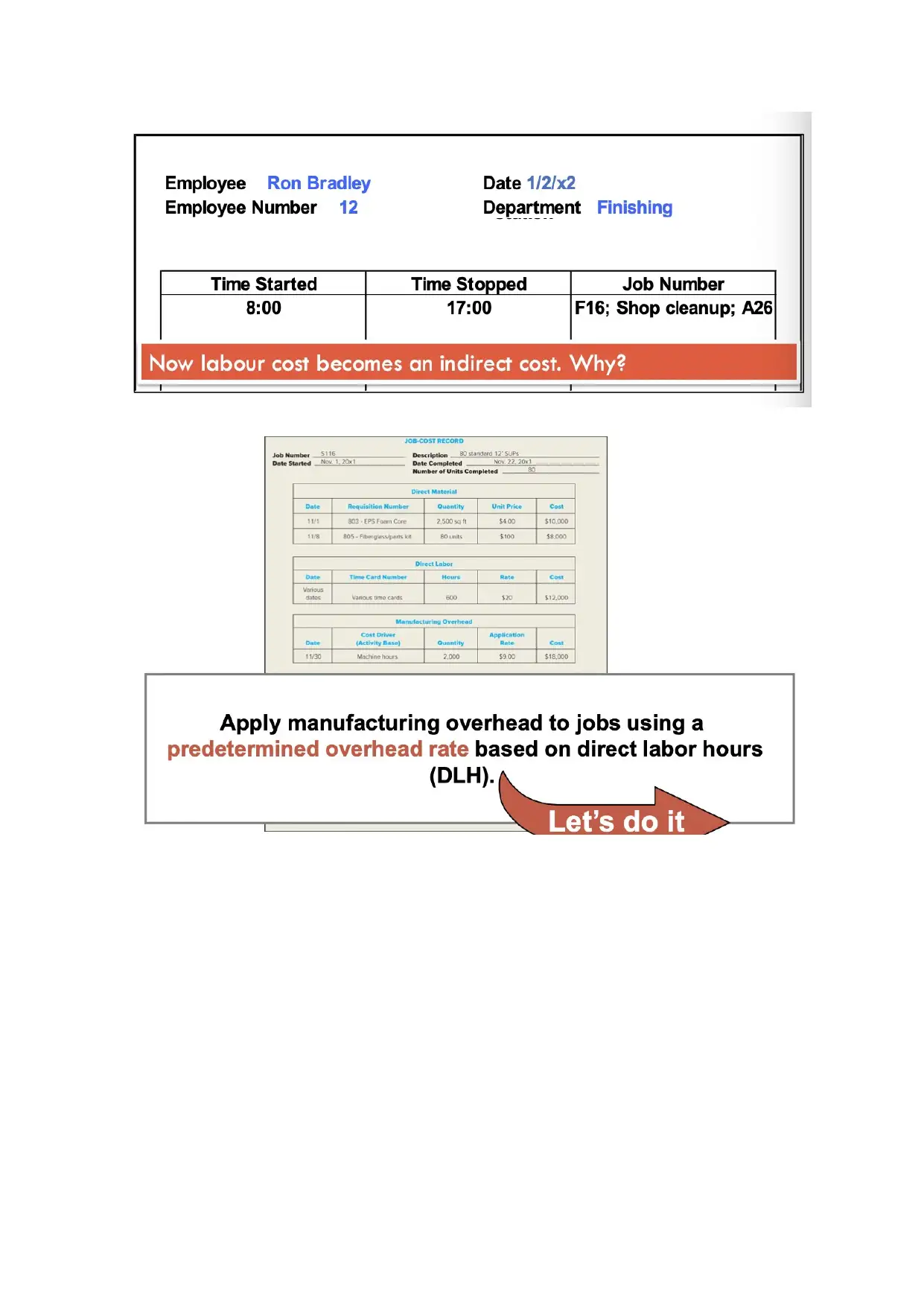

Job-Order Cost Accounting

A material requisition form is used to authorize the use of materials on a job.

The primary document for tracking the costs associated with a given job is the job-cost

record. The job number has a unique identifier, the job number (S116).

A material requisition form is used to authorize the use of materials on a job.

The primary document for tracking the costs associated with a given job is the job-cost

record. The job number has a unique identifier, the job number (S116).

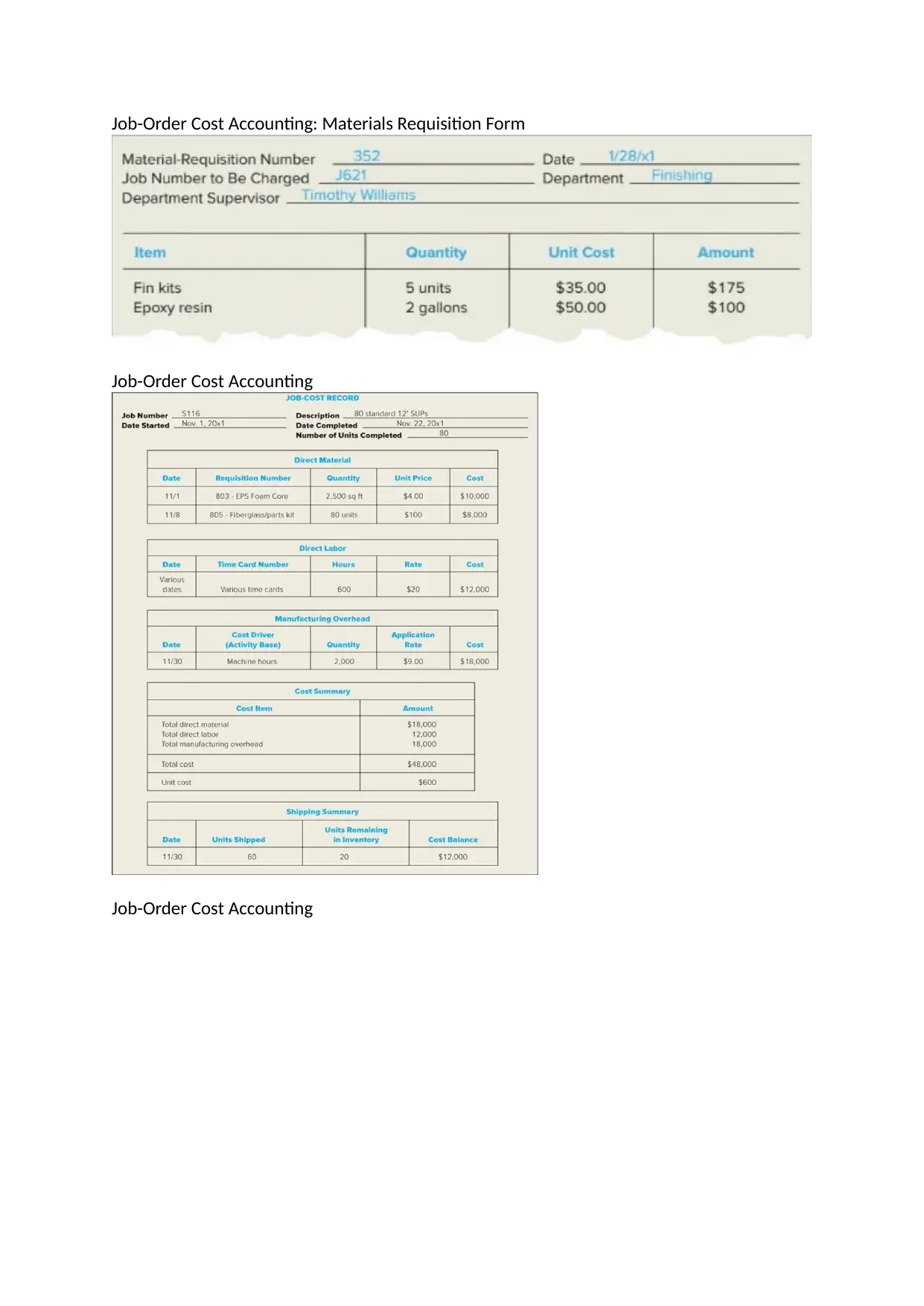

Job-Order Cost Accounting: Materials Requisition Form

Job-Order Cost Accounting

Job-Order Cost Accounting

Job-Order Cost Accounting

Job-Order Cost Accounting

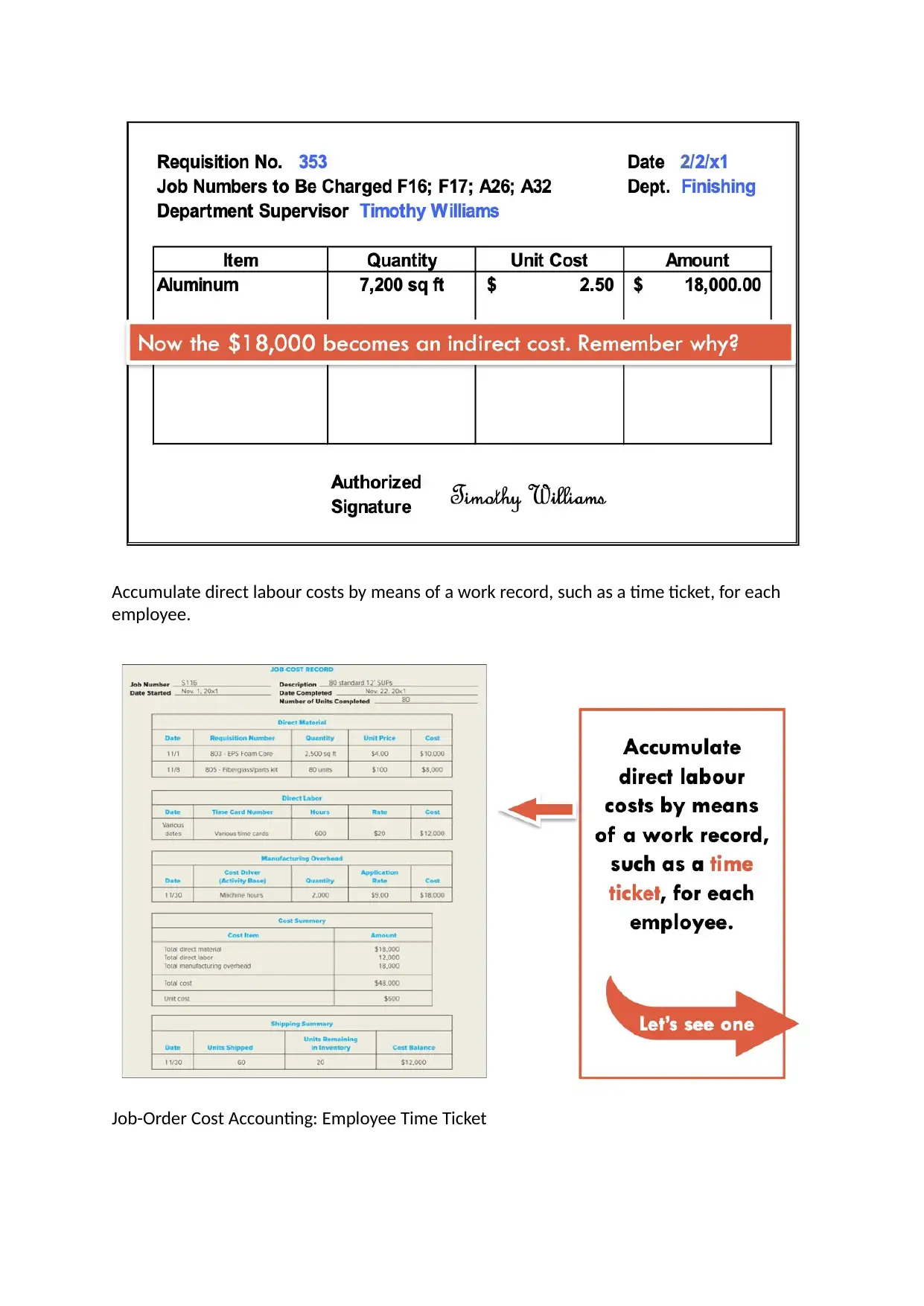

Accumulate direct labour costs by means of a work record, such as a time ticket, for each

employee.

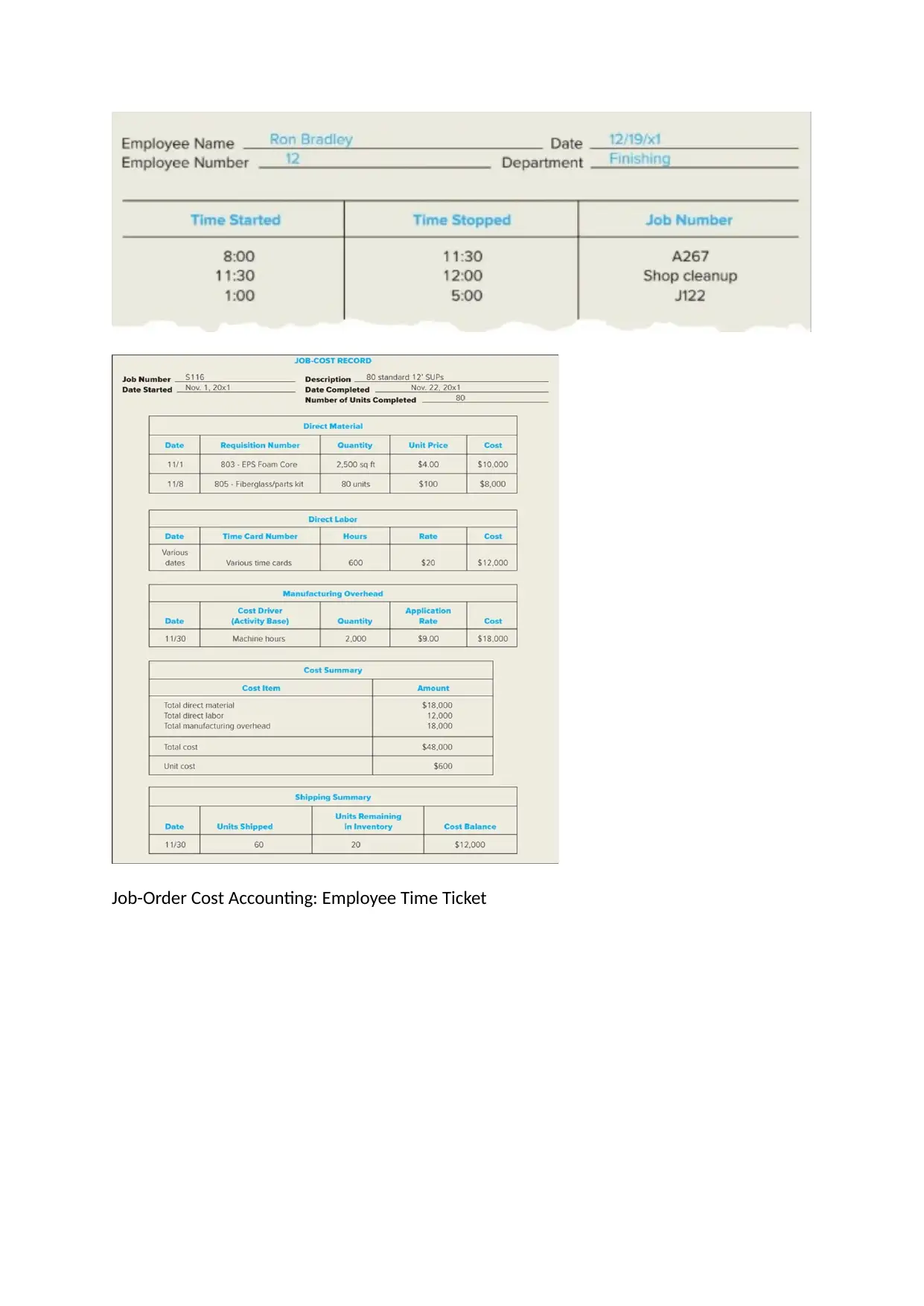

Job-Order Cost Accounting: Employee Time Ticket

employee.

Job-Order Cost Accounting: Employee Time Ticket

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job-Order Cost Accounting: Employee Time Ticket

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

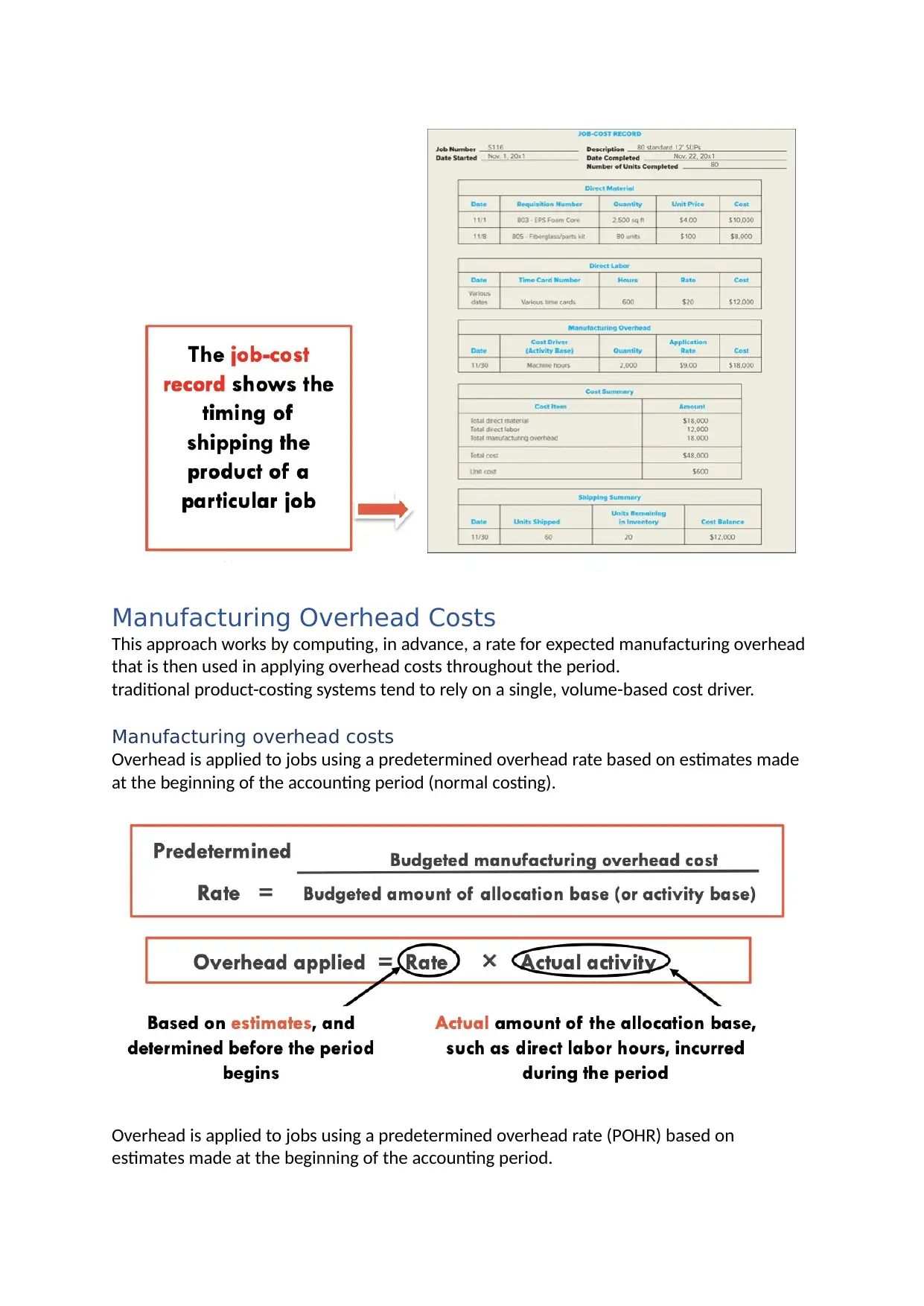

Manufacturing Overhead Costs

This approach works by computing, in advance, a rate for expected manufacturing overhead

that is then used in applying overhead costs throughout the period.

traditional product-costing systems tend to rely on a single, volume-based cost driver.

Manufacturing overhead costs

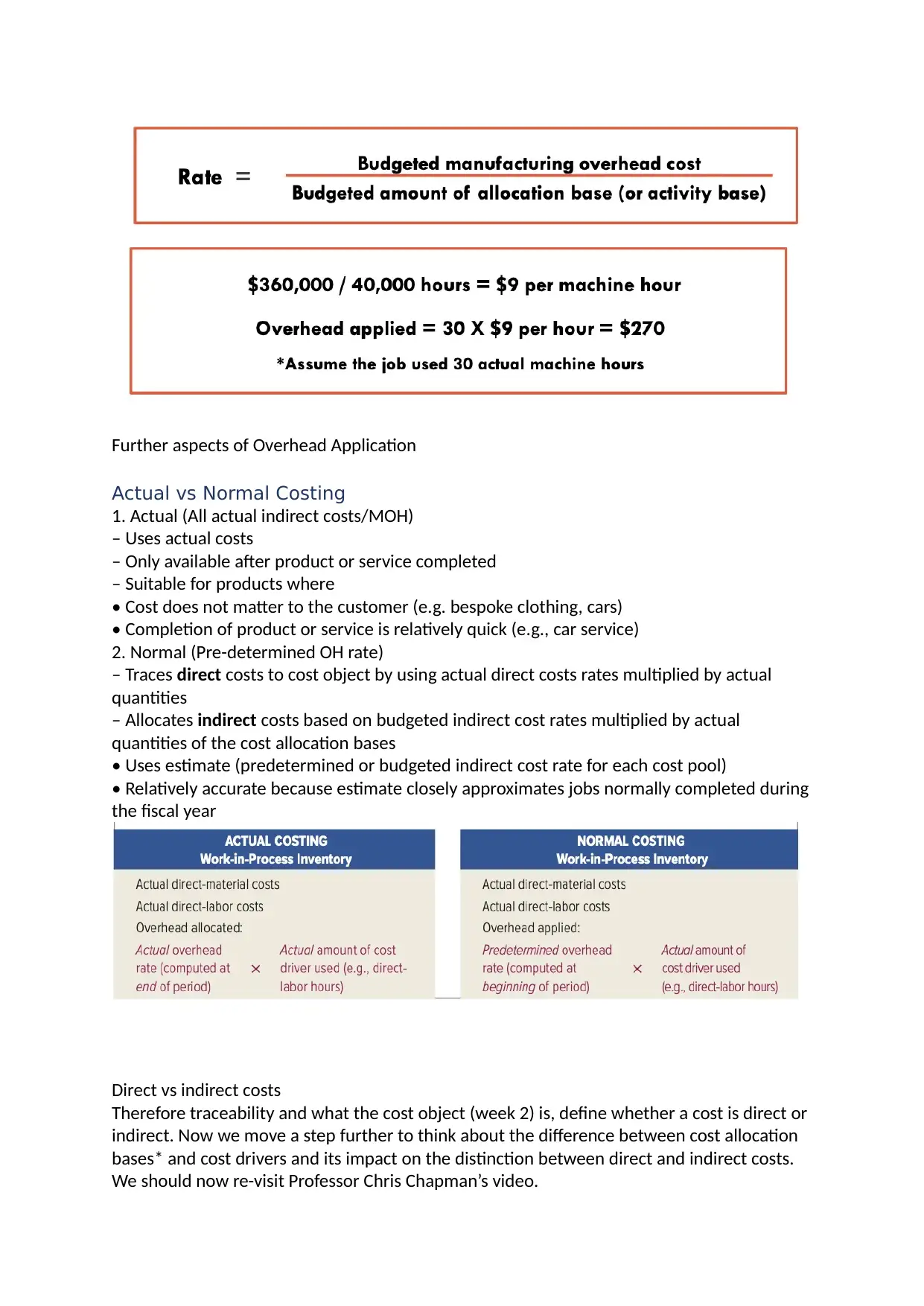

Overhead is applied to jobs using a predetermined overhead rate based on estimates made

at the beginning of the accounting period (normal costing).

Overhead is applied to jobs using a predetermined overhead rate (POHR) based on

estimates made at the beginning of the accounting period.

This approach works by computing, in advance, a rate for expected manufacturing overhead

that is then used in applying overhead costs throughout the period.

traditional product-costing systems tend to rely on a single, volume-based cost driver.

Manufacturing overhead costs

Overhead is applied to jobs using a predetermined overhead rate based on estimates made

at the beginning of the accounting period (normal costing).

Overhead is applied to jobs using a predetermined overhead rate (POHR) based on

estimates made at the beginning of the accounting period.

Further aspects of Overhead Application

Actual vs Normal Costing

1. Actual (All actual indirect costs/MOH)

– Uses actual costs

– Only available after product or service completed

– Suitable for products where

• Cost does not matter to the customer (e.g. bespoke clothing, cars)

• Completion of product or service is relatively quick (e.g., car service)

2. Normal (Pre-determined OH rate)

– Traces direct costs to cost object by using actual direct costs rates multiplied by actual

quantities

– Allocates indirect costs based on budgeted indirect cost rates multiplied by actual

quantities of the cost allocation bases

• Uses estimate (predetermined or budgeted indirect cost rate for each cost pool)

• Relatively accurate because estimate closely approximates jobs normally completed during

the fiscal year

Direct vs indirect costs

Therefore traceability and what the cost object (week 2) is, define whether a cost is direct or

indirect. Now we move a step further to think about the difference between cost allocation

bases* and cost drivers and its impact on the distinction between direct and indirect costs.

We should now re-visit Professor Chris Chapman’s video.

Actual vs Normal Costing

1. Actual (All actual indirect costs/MOH)

– Uses actual costs

– Only available after product or service completed

– Suitable for products where

• Cost does not matter to the customer (e.g. bespoke clothing, cars)

• Completion of product or service is relatively quick (e.g., car service)

2. Normal (Pre-determined OH rate)

– Traces direct costs to cost object by using actual direct costs rates multiplied by actual

quantities

– Allocates indirect costs based on budgeted indirect cost rates multiplied by actual

quantities of the cost allocation bases

• Uses estimate (predetermined or budgeted indirect cost rate for each cost pool)

• Relatively accurate because estimate closely approximates jobs normally completed during

the fiscal year

Direct vs indirect costs

Therefore traceability and what the cost object (week 2) is, define whether a cost is direct or

indirect. Now we move a step further to think about the difference between cost allocation

bases* and cost drivers and its impact on the distinction between direct and indirect costs.

We should now re-visit Professor Chris Chapman’s video.

*The textbook uses cost allocation bases and cost drivers interchangeably. For the purpose

of ACCT6008, they are used differently in managerial accounting. Use this set of slides for

preparation for workshops, mid-semester and final exams. See the next slide for an

explanation.

Cost Allocation Bases vs Cost Drivers

A cost allocation base is not a cost driver.

A cost allocation base:

MOH: product supervisor salary

Utility expenses in the factory

Indirect labour

Is a cost allocation base a cost driver? The answer is NO.

A cost allocation base DOES NOT drive the incurrence of a cost. (可可可可可可可可可可可可可可可可可可可可可

可可可可可可可可可可) We need it because we cannot allocate indirect costs without it. It’s simple. If

we add all indirect costs ranging from building insurance, property taxes to salaries of

production supervisors and divide the total by a cost allocation base, say machine hours,

what we get is simply an overhead rate. Can we say the more machine hours we consume,

the higher the total indirect costs will be? No.

可可可可可可 MOH 可可可可可可可可可可可可可可可可可可可、、 MH 可可可可可可可可可可可可可可可可可可 MH 可可可可可可可可

可可可可可可可可可可可可可可可可可可可可可可可可可可可可可可 DLH 可可可可可可可可可可可可 可可可可可可可可可可可可可可可可

可可可可可可可可可可可可 cost allocation base

A cost driver DOES drive the incurrence of a cost. For instance, number of units produced is

a cost driver for direct material costs because the more units we produce the higher the

direct material costs will be. (可可 units 可可可 DM 可 cost driver) Also a cost driver makes a cost

traceable. Direct material cost is traceable because we can trace the consumption of

materials per unit and we know the total number of units produced. 可可可可可可可可可可可可可可可可

可 machinery hour 可可可可可 cost driver

Therefore if we know the cost driver for a cost, that cost will be a direct cost.

This is why ABC (Activity-Based Costing) better facilitates cost management because ABC is

not about overhead cost allocation. In ABC we don’t say cost allocation bases, we say

activity cost drivers. Instead it generates a new range of direct costs. Details will follow next

week.

Job-Order Costing Document Flow Summary

Production Order for Job: The production order for the job authorizes the start of the

production process

Material Requisition: The materials requisition indicates the cost of direct

material to charge to jobs and the cost of overhead

indirect material to charge to Labour Time Records: Employee time tickets indicate the cost

of direct

labor to charge to jobs and the cost of overhead

Apply Manufacturing Overhead:

Actual cost driver (or activity base) Predetermined overhead rate

of ACCT6008, they are used differently in managerial accounting. Use this set of slides for

preparation for workshops, mid-semester and final exams. See the next slide for an

explanation.

Cost Allocation Bases vs Cost Drivers

A cost allocation base is not a cost driver.

A cost allocation base:

MOH: product supervisor salary

Utility expenses in the factory

Indirect labour

Is a cost allocation base a cost driver? The answer is NO.

A cost allocation base DOES NOT drive the incurrence of a cost. (可可可可可可可可可可可可可可可可可可可可可

可可可可可可可可可可) We need it because we cannot allocate indirect costs without it. It’s simple. If

we add all indirect costs ranging from building insurance, property taxes to salaries of

production supervisors and divide the total by a cost allocation base, say machine hours,

what we get is simply an overhead rate. Can we say the more machine hours we consume,

the higher the total indirect costs will be? No.

可可可可可可 MOH 可可可可可可可可可可可可可可可可可可可、、 MH 可可可可可可可可可可可可可可可可可可 MH 可可可可可可可可

可可可可可可可可可可可可可可可可可可可可可可可可可可可可可可 DLH 可可可可可可可可可可可可 可可可可可可可可可可可可可可可可

可可可可可可可可可可可可 cost allocation base

A cost driver DOES drive the incurrence of a cost. For instance, number of units produced is

a cost driver for direct material costs because the more units we produce the higher the

direct material costs will be. (可可 units 可可可 DM 可 cost driver) Also a cost driver makes a cost

traceable. Direct material cost is traceable because we can trace the consumption of

materials per unit and we know the total number of units produced. 可可可可可可可可可可可可可可可可

可 machinery hour 可可可可可 cost driver

Therefore if we know the cost driver for a cost, that cost will be a direct cost.

This is why ABC (Activity-Based Costing) better facilitates cost management because ABC is

not about overhead cost allocation. In ABC we don’t say cost allocation bases, we say

activity cost drivers. Instead it generates a new range of direct costs. Details will follow next

week.

Job-Order Costing Document Flow Summary

Production Order for Job: The production order for the job authorizes the start of the

production process

Material Requisition: The materials requisition indicates the cost of direct

material to charge to jobs and the cost of overhead

indirect material to charge to Labour Time Records: Employee time tickets indicate the cost

of direct

labor to charge to jobs and the cost of overhead

Apply Manufacturing Overhead:

Actual cost driver (or activity base) Predetermined overhead rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

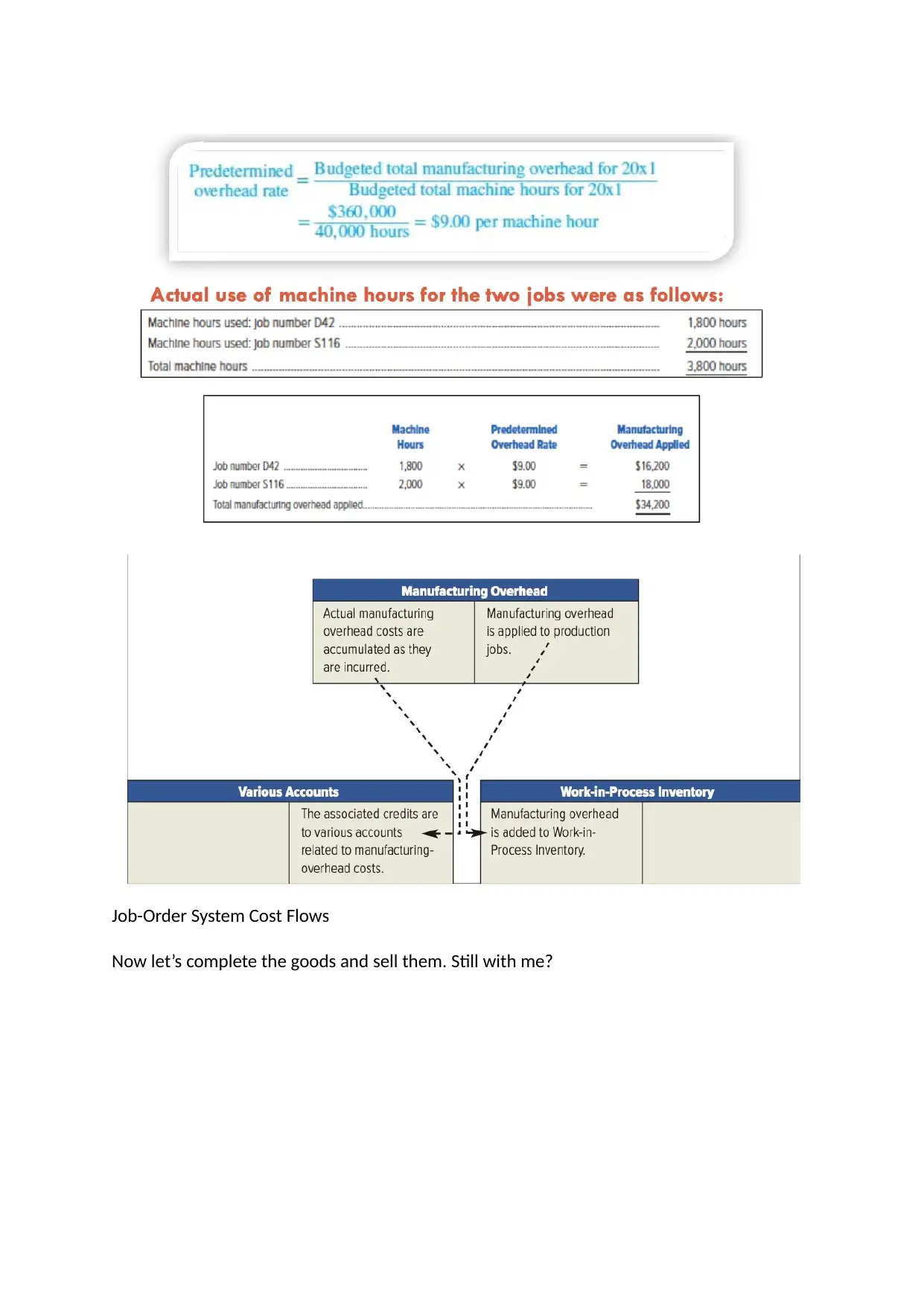

Job-Order System Cost Flows

Now let’s complete the goods and sell them. Still with me?

Now let’s complete the goods and sell them. Still with me?

Let’s see what we will do if actual and applied overhead are not equal

Underapplied VS overapplied (Underallocated/overallocated)

Underapplied overhead: The amount by which actual overhead exceeds applied overhead 可

可可可可可可可 overhead 可可可可 apply 可 overhead 可可可可可可可可 applied overhead 可可可可可可可可可可

可可

If actual overhead had been less than applied overhead, the difference would have been

called overapplied overhead.

可可可可可applied overhead=predetermined overhead rate* actual usage of cost allocation

base, 可可可可可可 budgeted overhead 可可

Underapplied: Applied OH < Actual OH

Overapplied: Applied OH > Actual OH

Overapplied and Underapplied Manufacturing Overhead - Summary

Underapplied VS overapplied (Underallocated/overallocated)

Underapplied overhead: The amount by which actual overhead exceeds applied overhead 可

可可可可可可可 overhead 可可可可 apply 可 overhead 可可可可可可可可 applied overhead 可可可可可可可可可可

可可

If actual overhead had been less than applied overhead, the difference would have been

called overapplied overhead.

可可可可可applied overhead=predetermined overhead rate* actual usage of cost allocation

base, 可可可可可可 budgeted overhead 可可

Underapplied: Applied OH < Actual OH

Overapplied: Applied OH > Actual OH

Overapplied and Underapplied Manufacturing Overhead - Summary

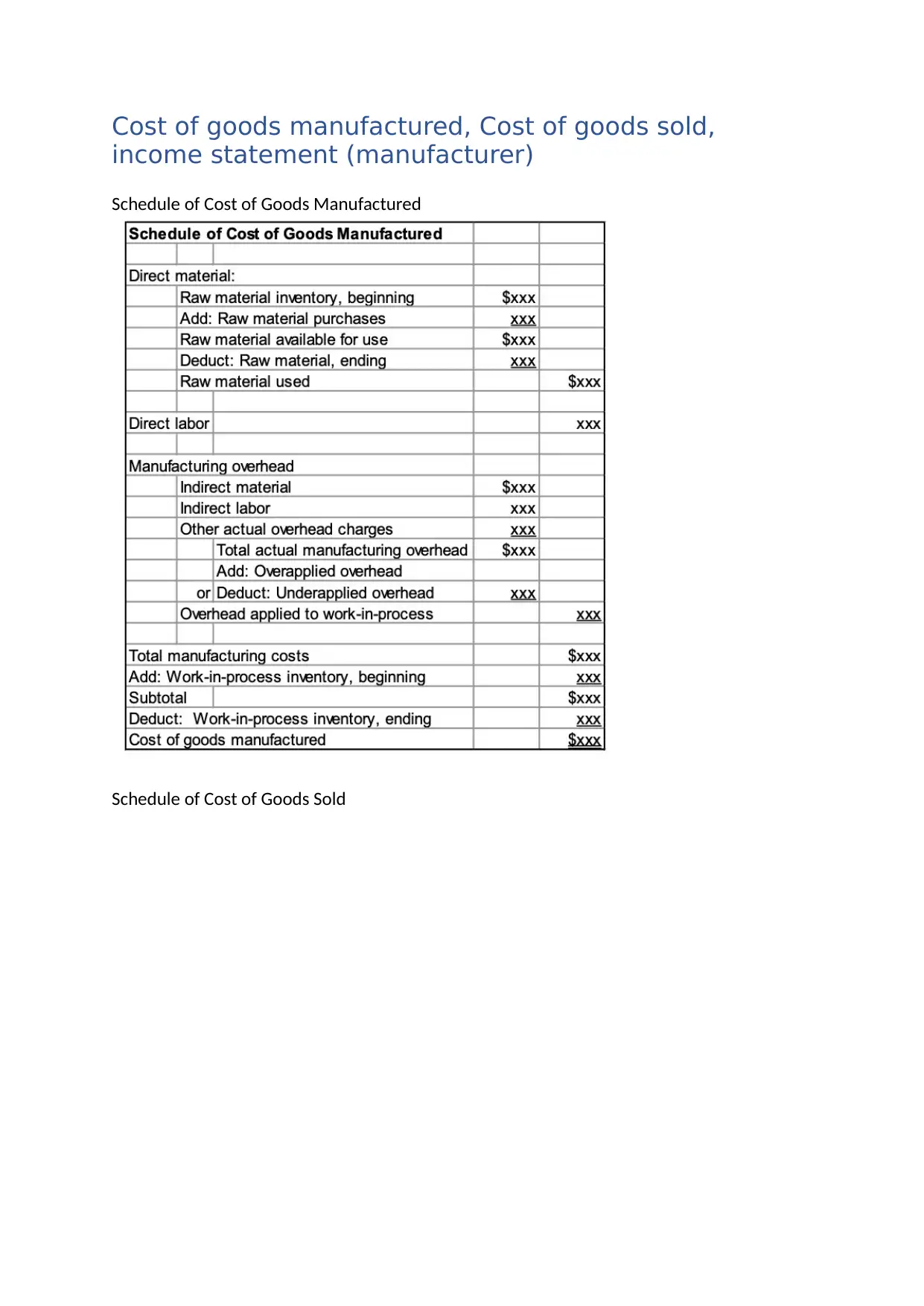

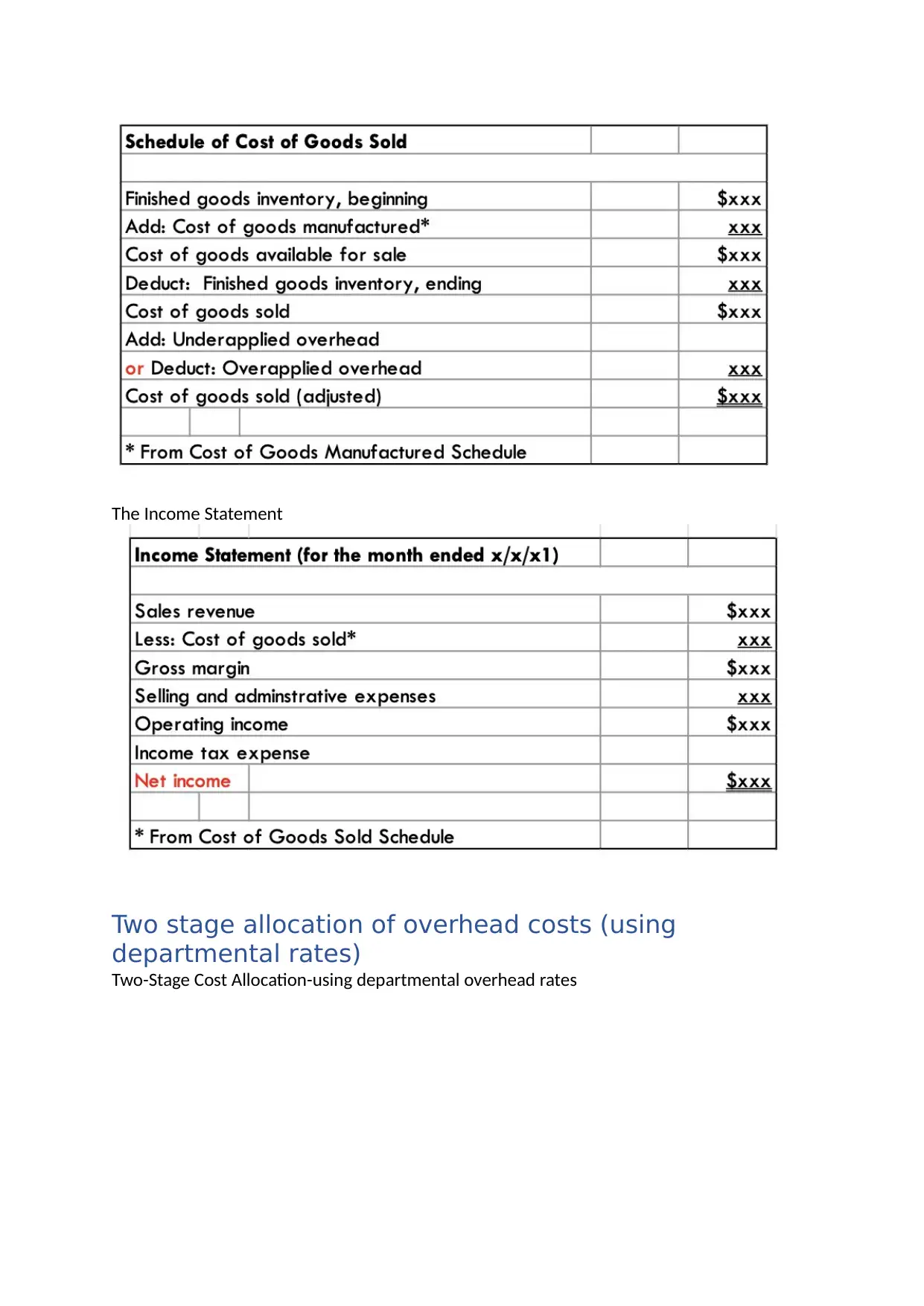

Cost of goods manufactured, Cost of goods sold,

income statement (manufacturer)

Schedule of Cost of Goods Manufactured

Schedule of Cost of Goods Sold

income statement (manufacturer)

Schedule of Cost of Goods Manufactured

Schedule of Cost of Goods Sold

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The Income Statement

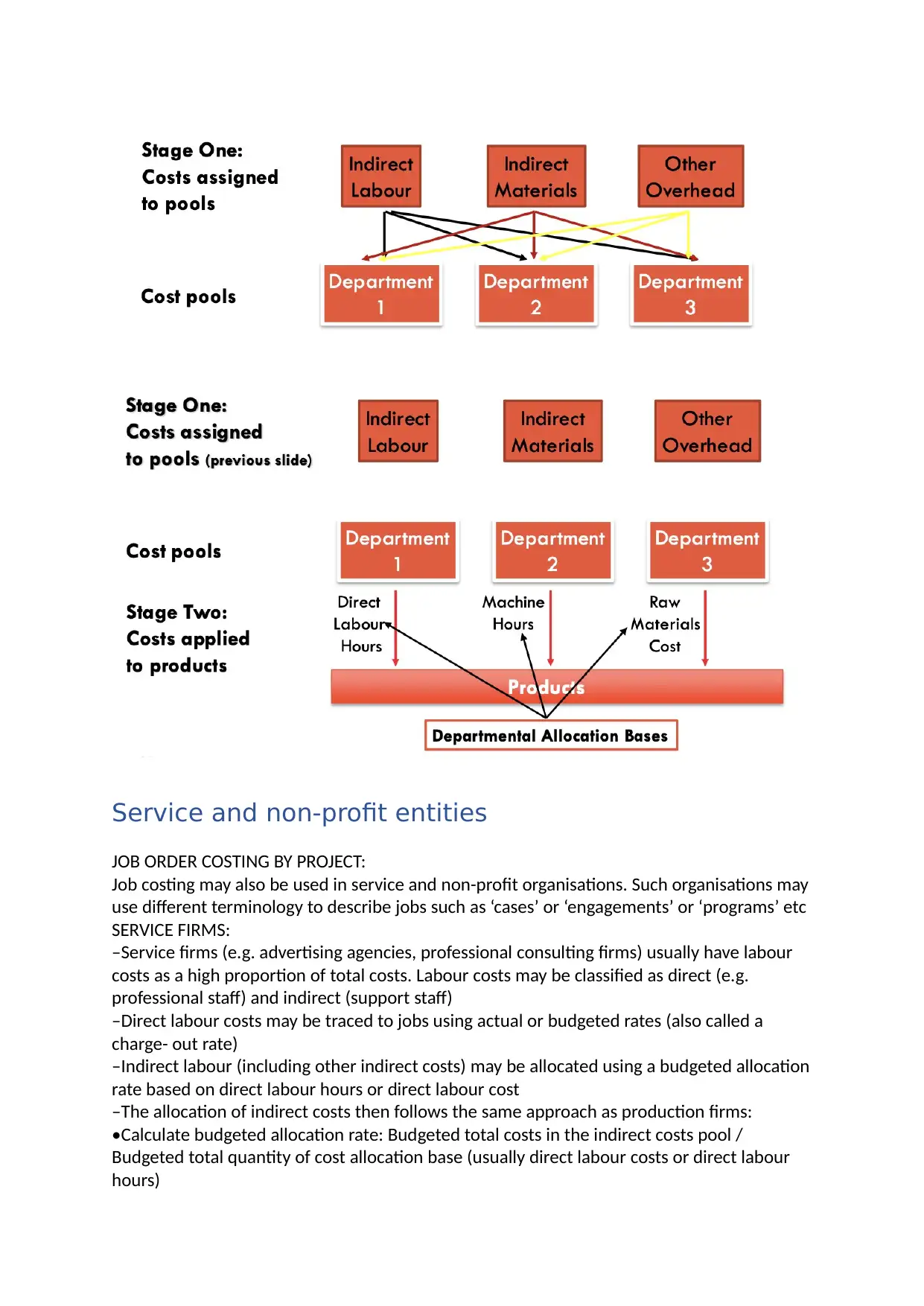

Two stage allocation of overhead costs (using

departmental rates)

Two-Stage Cost Allocation-using departmental overhead rates

Two stage allocation of overhead costs (using

departmental rates)

Two-Stage Cost Allocation-using departmental overhead rates

Service and non-profit entities

JOB ORDER COSTING BY PROJECT:

Job costing may also be used in service and non-profit organisations. Such organisations may

use different terminology to describe jobs such as ‘cases’ or ‘engagements’ or ‘programs’ etc

SERVICE FIRMS:

–Service firms (e.g. advertising agencies, professional consulting firms) usually have labour

costs as a high proportion of total costs. Labour costs may be classified as direct (e.g.

professional staff) and indirect (support staff)

–Direct labour costs may be traced to jobs using actual or budgeted rates (also called a

charge- out rate)

–Indirect labour (including other indirect costs) may be allocated using a budgeted allocation

rate based on direct labour hours or direct labour cost

–The allocation of indirect costs then follows the same approach as production firms:

•Calculate budgeted allocation rate: Budgeted total costs in the indirect costs pool /

Budgeted total quantity of cost allocation base (usually direct labour costs or direct labour

hours)

JOB ORDER COSTING BY PROJECT:

Job costing may also be used in service and non-profit organisations. Such organisations may

use different terminology to describe jobs such as ‘cases’ or ‘engagements’ or ‘programs’ etc

SERVICE FIRMS:

–Service firms (e.g. advertising agencies, professional consulting firms) usually have labour

costs as a high proportion of total costs. Labour costs may be classified as direct (e.g.

professional staff) and indirect (support staff)

–Direct labour costs may be traced to jobs using actual or budgeted rates (also called a

charge- out rate)

–Indirect labour (including other indirect costs) may be allocated using a budgeted allocation

rate based on direct labour hours or direct labour cost

–The allocation of indirect costs then follows the same approach as production firms:

•Calculate budgeted allocation rate: Budgeted total costs in the indirect costs pool /

Budgeted total quantity of cost allocation base (usually direct labour costs or direct labour

hours)

•Allocate indirect cost: Budgeted allocation rate x actual level of the allocation base (usually

direct labour costs or direct labour hours)

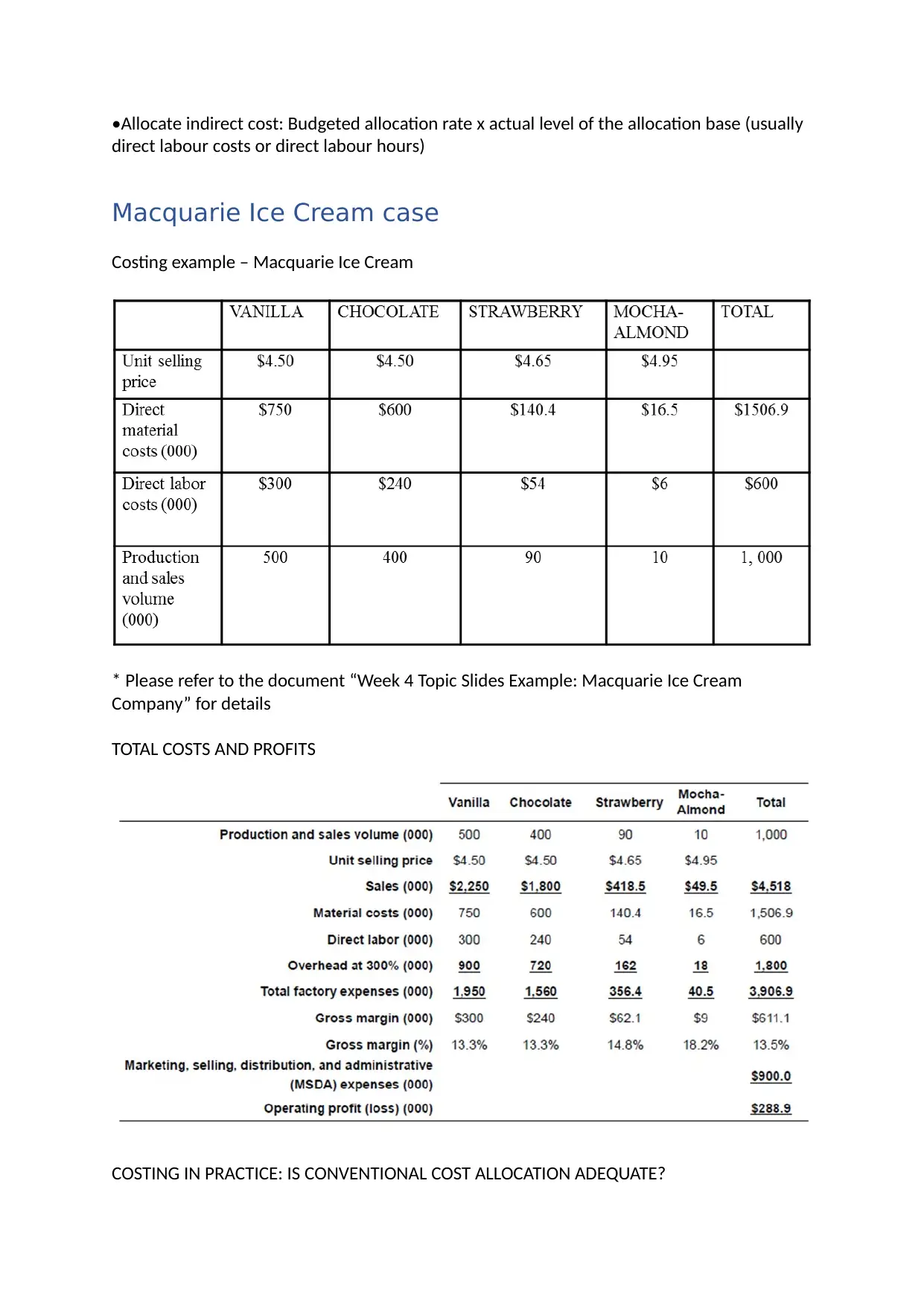

Macquarie Ice Cream case

Costing example – Macquarie Ice Cream

* Please refer to the document “Week 4 Topic Slides Example: Macquarie Ice Cream

Company” for details

TOTAL COSTS AND PROFITS

COSTING IN PRACTICE: IS CONVENTIONAL COST ALLOCATION ADEQUATE?

direct labour costs or direct labour hours)

Macquarie Ice Cream case

Costing example – Macquarie Ice Cream

* Please refer to the document “Week 4 Topic Slides Example: Macquarie Ice Cream

Company” for details

TOTAL COSTS AND PROFITS

COSTING IN PRACTICE: IS CONVENTIONAL COST ALLOCATION ADEQUATE?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ask yourselves the following questions:

1. Is Conventional Cost Allocation adequate when the organisation only produces one

product, for instance, only the chocolate flavour ice cream at Macquarie?

2. Is Conventional Cost Allocation adequate when the organisation produce several products

that use resources in a uniform or similar way, for instance, the chocolate and vanilla

flavours of ice cream?

3. Is Conventional Cost Allocation adequate when the organisation produces products that

use resources in a non-uniform way, for instance, the four flavours of ice cream?

4. If not, how do we refine the costing system?

A. Increase the number of allocation bases or indirect cost pools.

B. Think about ‘what drives the incurrence of costs’?

Workshop

RASA

1. Budgeted cost rates are preferred over actual cost rates for all of the following reasons

except: (D)

A. budgeted indirect-cost rates are known prior to the inception of a new job;

B. budgeted-cost rates can be used to assign indirect costs;

C. budgeted costs allow managers to have cost information on a timely basis;

D. budgeted costs may be subject to short-run fluctuations

2. Actual manufacturing overhead at Pencil Manufacturing Limited is AUD1,400,000.

Overhead is allocated on the basis of direct labour hours. The direct labour hours were

25,000 for the period. In one hour, 100 pencils are manufactured. What is the applied

manufacturing overhead rate? (B)

A. AUD5,600;

B. AUD56.00;

C. AUD47.00;

D. AUD4.70

3. The Best Cost Company, which used labour hours to apply overhead to manufacturing

may have increased amounts of underapplied overhead at month end if: (C)

A. Suppliers of direct materials have an across-the-board price increase;

B. Advertising expenditure is increased during the month;

C. There is an outbreak of flu and many employees are off work during the month;

D. An accountant failed to record the month’s charges for plant maintenance and equipment

depreciation

[C, Employees that are hard hit with a flu outbreak would be a cause for underapplied

overhead based on labor hours.]

4. After implementing the conventional costing system, the management accountant would

only recommend change if: (A)

A. a new product was introduced that was different to the existing products in its use of

resources;

B. price of an existing product was discounted and the sales volume of the existing product

doubled or tripled;

C. employees classed as direct labour were granted a major pay rise during the month (e.g.,

20%);

1. Is Conventional Cost Allocation adequate when the organisation only produces one

product, for instance, only the chocolate flavour ice cream at Macquarie?

2. Is Conventional Cost Allocation adequate when the organisation produce several products

that use resources in a uniform or similar way, for instance, the chocolate and vanilla

flavours of ice cream?

3. Is Conventional Cost Allocation adequate when the organisation produces products that

use resources in a non-uniform way, for instance, the four flavours of ice cream?

4. If not, how do we refine the costing system?

A. Increase the number of allocation bases or indirect cost pools.

B. Think about ‘what drives the incurrence of costs’?

Workshop

RASA

1. Budgeted cost rates are preferred over actual cost rates for all of the following reasons

except: (D)

A. budgeted indirect-cost rates are known prior to the inception of a new job;

B. budgeted-cost rates can be used to assign indirect costs;

C. budgeted costs allow managers to have cost information on a timely basis;

D. budgeted costs may be subject to short-run fluctuations

2. Actual manufacturing overhead at Pencil Manufacturing Limited is AUD1,400,000.

Overhead is allocated on the basis of direct labour hours. The direct labour hours were

25,000 for the period. In one hour, 100 pencils are manufactured. What is the applied

manufacturing overhead rate? (B)

A. AUD5,600;

B. AUD56.00;

C. AUD47.00;

D. AUD4.70

3. The Best Cost Company, which used labour hours to apply overhead to manufacturing

may have increased amounts of underapplied overhead at month end if: (C)

A. Suppliers of direct materials have an across-the-board price increase;

B. Advertising expenditure is increased during the month;

C. There is an outbreak of flu and many employees are off work during the month;

D. An accountant failed to record the month’s charges for plant maintenance and equipment

depreciation

[C, Employees that are hard hit with a flu outbreak would be a cause for underapplied

overhead based on labor hours.]

4. After implementing the conventional costing system, the management accountant would

only recommend change if: (A)

A. a new product was introduced that was different to the existing products in its use of

resources;

B. price of an existing product was discounted and the sales volume of the existing product

doubled or tripled;

C. employees classed as direct labour were granted a major pay rise during the month (e.g.,

20%);

D. newspaper, magazine and TV advertising expenditure is replaced with pop-up ads on the

internet for the foreseeable future

Business Practical

Energy Electronics Company (EEC) produces a wide range of consumer electronics and

electrical components for a variety of products such as mobile devices, televisions, digital

cameras and video game consoles. EEC’s strategy for the last decade has been “beating the

competitors by offering less expensive products” because of the intensive rivalry between a

large number of companies producing similar products.

EEC is considering launching a new digital camera A200 to replace its predecessor, the A180.

The A200, A180 and their predecessors require similar production processes. During the first

six months of selling the A200s, EEC have decided to keep manufacturing the A180s. The

A180 has been regarded as “a stunner with good optics” and “good value for money” by the

market. EEC’s entire factory has been used to produce only A180 and its predecessors. While

direct material and labour costs can be traced to products directly, overheads such as the

operations of machines and production supervisors will be shared between A200s and

A180s. The company will wait to see if A180 should be discontinued after the first two

quarters.

Compared to A180, the A200 produces better performance on optics, colour, dynamic

lighting and includes new and improved waterproof ratings and high magnification. Despite

the market popularity of the A180s, the CEO of EEC thinks the A200 camera needs to be

launched to market quickly because competitors will release similar cameras very soon.

You are part of the MA team at EEC. One of your team’s tasks is to suggest the price of A200

on the basis of its cost. For this line of digital cameras (A200, A180 and their predecessors),

the accounting system uses a conventional cost allocation method that uses machine hour

as a plant-wide allocation base to allocate overheads. Normal costing is used because MAs

believe that it will lead to more timely decision making. The current accounting system also

calculates overhead costs on a quarterly basis. The following estimates are made for the

current year.

internet for the foreseeable future

Business Practical

Energy Electronics Company (EEC) produces a wide range of consumer electronics and

electrical components for a variety of products such as mobile devices, televisions, digital

cameras and video game consoles. EEC’s strategy for the last decade has been “beating the

competitors by offering less expensive products” because of the intensive rivalry between a

large number of companies producing similar products.

EEC is considering launching a new digital camera A200 to replace its predecessor, the A180.

The A200, A180 and their predecessors require similar production processes. During the first

six months of selling the A200s, EEC have decided to keep manufacturing the A180s. The

A180 has been regarded as “a stunner with good optics” and “good value for money” by the

market. EEC’s entire factory has been used to produce only A180 and its predecessors. While

direct material and labour costs can be traced to products directly, overheads such as the

operations of machines and production supervisors will be shared between A200s and

A180s. The company will wait to see if A180 should be discontinued after the first two

quarters.

Compared to A180, the A200 produces better performance on optics, colour, dynamic

lighting and includes new and improved waterproof ratings and high magnification. Despite

the market popularity of the A180s, the CEO of EEC thinks the A200 camera needs to be

launched to market quickly because competitors will release similar cameras very soon.

You are part of the MA team at EEC. One of your team’s tasks is to suggest the price of A200

on the basis of its cost. For this line of digital cameras (A200, A180 and their predecessors),

the accounting system uses a conventional cost allocation method that uses machine hour

as a plant-wide allocation base to allocate overheads. Normal costing is used because MAs

believe that it will lead to more timely decision making. The current accounting system also

calculates overhead costs on a quarterly basis. The following estimates are made for the

current year.

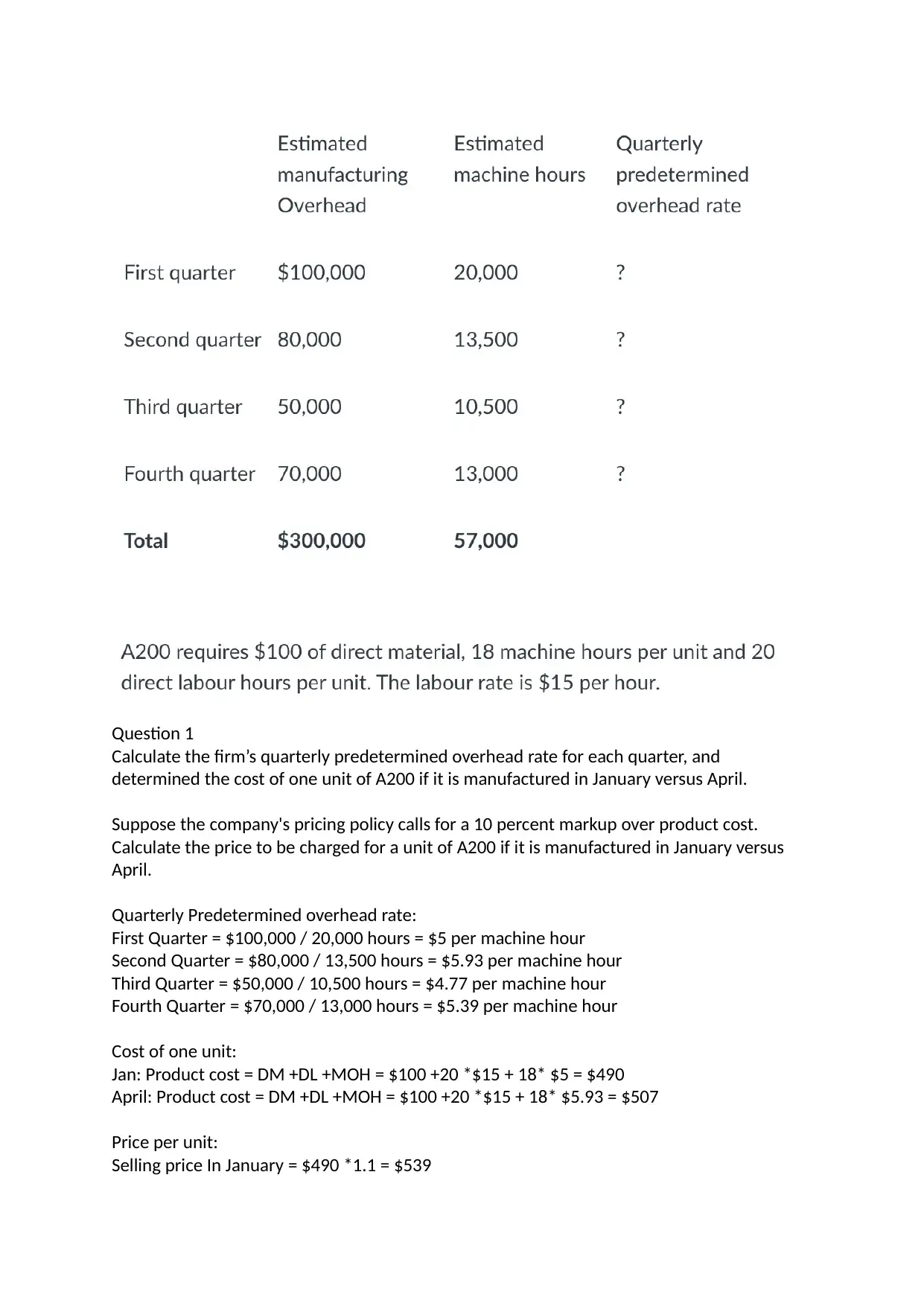

Question 1

Calculate the firm’s quarterly predetermined overhead rate for each quarter, and

determined the cost of one unit of A200 if it is manufactured in January versus April.

Suppose the company's pricing policy calls for a 10 percent markup over product cost.

Calculate the price to be charged for a unit of A200 if it is manufactured in January versus

April.

Quarterly Predetermined overhead rate:

First Quarter = $100,000 / 20,000 hours = $5 per machine hour

Second Quarter = $80,000 / 13,500 hours = $5.93 per machine hour

Third Quarter = $50,000 / 10,500 hours = $4.77 per machine hour

Fourth Quarter = $70,000 / 13,000 hours = $5.39 per machine hour

Cost of one unit:

Jan: Product cost = DM +DL +MOH = $100 +20 *$15 + 18* $5 = $490

April: Product cost = DM +DL +MOH = $100 +20 *$15 + 18* $5.93 = $507

Price per unit:

Selling price In January = $490 *1.1 = $539

Calculate the firm’s quarterly predetermined overhead rate for each quarter, and

determined the cost of one unit of A200 if it is manufactured in January versus April.

Suppose the company's pricing policy calls for a 10 percent markup over product cost.

Calculate the price to be charged for a unit of A200 if it is manufactured in January versus

April.

Quarterly Predetermined overhead rate:

First Quarter = $100,000 / 20,000 hours = $5 per machine hour

Second Quarter = $80,000 / 13,500 hours = $5.93 per machine hour

Third Quarter = $50,000 / 10,500 hours = $4.77 per machine hour

Fourth Quarter = $70,000 / 13,000 hours = $5.39 per machine hour

Cost of one unit:

Jan: Product cost = DM +DL +MOH = $100 +20 *$15 + 18* $5 = $490

April: Product cost = DM +DL +MOH = $100 +20 *$15 + 18* $5.93 = $507

Price per unit:

Selling price In January = $490 *1.1 = $539

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Selling price In April = $507 *1.1 = $558

Question 2:

a) Calculate the company's predetermined overhead rate for the year if the rate is calculated

annually, and determine the cost of one unit of A200 if it is manufactured in January versus

April.

b) Calculate the price to be charged for a unit of A200 if it is manufactured in January versus

April, assuming the company's pricing policy calls for a 10 percent markup over product cost.

For the whole year:

Predetermined overhead rate (annually) = $300,000 / 57000 = $5.26 per machine hour

A200 product cost = DM + DL + MOH = $100 +20 *$15 + 18* $5.26 = $495 (no matter it’s Jan

or Apr, the number is the same)

The cost is the same whether it is produced in a month or in April

Sale Price = $495 * 1.1 = $545

Question 3:

Based on the calculations you have done so far:

state one advantage and one disadvantage of using the quarterly rates,

state one advantage and one disadvantage of using the annual rate.

Quarterly rates:

Advantage: It's more accurate and frequently to calculate predetermined overhead

rate and product cost, which tells how much machine hours or labor hours using

quarter to quarter. It helps the manufacturer consider what accounts for why using

more direct labor hours or machine hours for the between different quarters. The

fundamental question for this case is that the managers are undecided as to whether

to use machine hours all labor hours to allocate the amount of factory overhead that

impacts the decision. So, knowing how that number changes between different

quarters can be beneficial.

Disadvantage: In the long run, flexibility leads to changes in fixed costs. It make

product cost volatile, if the company's pricing of products is based on production

costs, then sales price is unstable.

Disadvantage: No meaning to change: The allocation base in different quarter cause

the change of manufacturing overhead cost. Actual manufacturing overhead isn't the

same amount regardless of your allocation base is your application and changes.

Annual rates:

Advantage: The stability overhead rate make the product costs and sale price stable,

which help the company easier to set price strategy.

Disadvantage: It mixes the whole year cost data, it is difficult to show how product

costs change over an accounting period, which might cause a delay in responding to

rapidly changing

Question 4:

Question 2:

a) Calculate the company's predetermined overhead rate for the year if the rate is calculated

annually, and determine the cost of one unit of A200 if it is manufactured in January versus

April.

b) Calculate the price to be charged for a unit of A200 if it is manufactured in January versus

April, assuming the company's pricing policy calls for a 10 percent markup over product cost.

For the whole year:

Predetermined overhead rate (annually) = $300,000 / 57000 = $5.26 per machine hour

A200 product cost = DM + DL + MOH = $100 +20 *$15 + 18* $5.26 = $495 (no matter it’s Jan

or Apr, the number is the same)

The cost is the same whether it is produced in a month or in April

Sale Price = $495 * 1.1 = $545

Question 3:

Based on the calculations you have done so far:

state one advantage and one disadvantage of using the quarterly rates,

state one advantage and one disadvantage of using the annual rate.

Quarterly rates:

Advantage: It's more accurate and frequently to calculate predetermined overhead

rate and product cost, which tells how much machine hours or labor hours using

quarter to quarter. It helps the manufacturer consider what accounts for why using

more direct labor hours or machine hours for the between different quarters. The

fundamental question for this case is that the managers are undecided as to whether

to use machine hours all labor hours to allocate the amount of factory overhead that

impacts the decision. So, knowing how that number changes between different

quarters can be beneficial.

Disadvantage: In the long run, flexibility leads to changes in fixed costs. It make

product cost volatile, if the company's pricing of products is based on production

costs, then sales price is unstable.

Disadvantage: No meaning to change: The allocation base in different quarter cause

the change of manufacturing overhead cost. Actual manufacturing overhead isn't the

same amount regardless of your allocation base is your application and changes.

Annual rates:

Advantage: The stability overhead rate make the product costs and sale price stable,

which help the company easier to set price strategy.

Disadvantage: It mixes the whole year cost data, it is difficult to show how product

costs change over an accounting period, which might cause a delay in responding to

rapidly changing

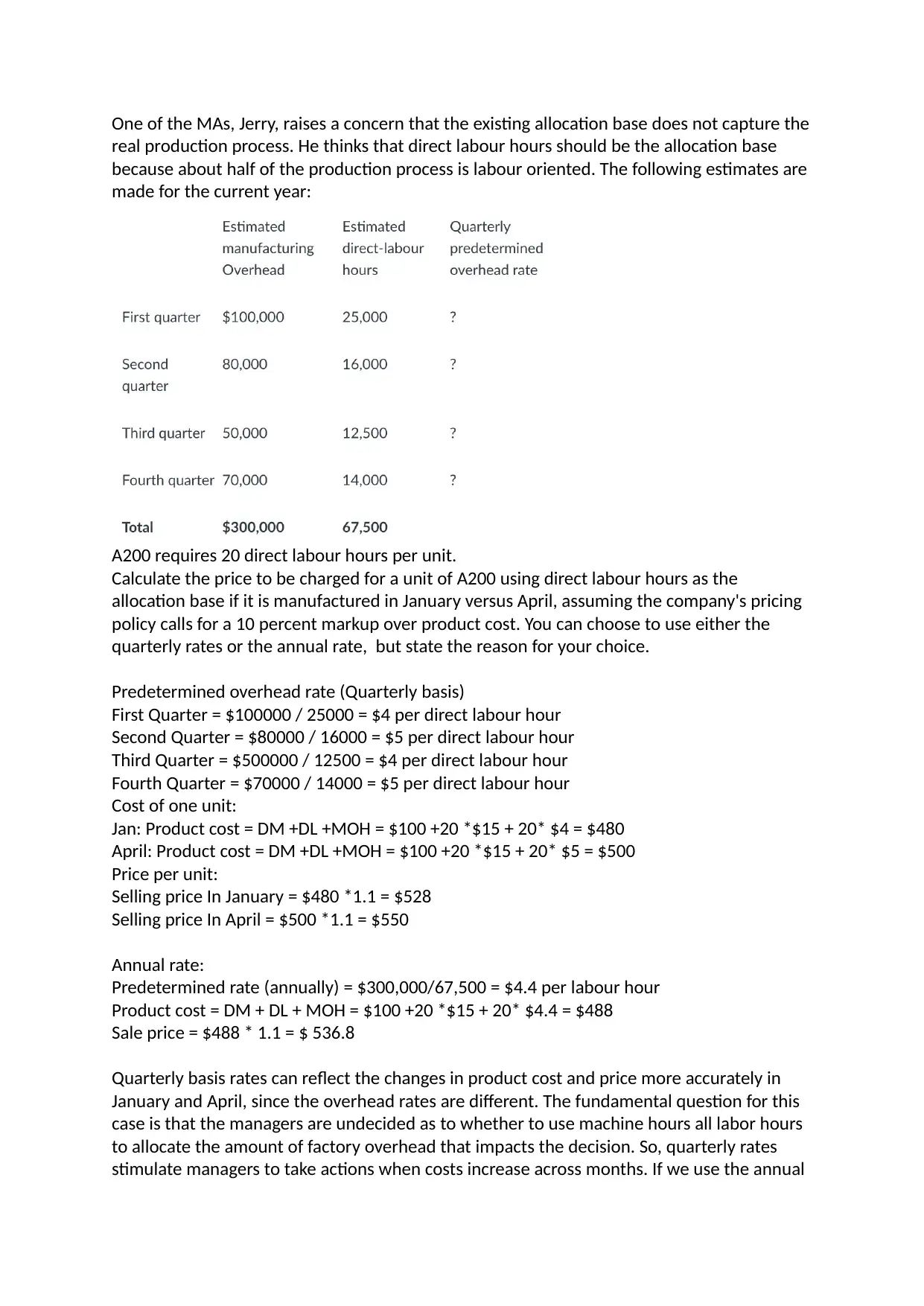

Question 4:

One of the MAs, Jerry, raises a concern that the existing allocation base does not capture the

real production process. He thinks that direct labour hours should be the allocation base

because about half of the production process is labour oriented. The following estimates are

made for the current year:

A200 requires 20 direct labour hours per unit.

Calculate the price to be charged for a unit of A200 using direct labour hours as the

allocation base if it is manufactured in January versus April, assuming the company's pricing

policy calls for a 10 percent markup over product cost. You can choose to use either the

quarterly rates or the annual rate, but state the reason for your choice.

Predetermined overhead rate (Quarterly basis)

First Quarter = $100000 / 25000 = $4 per direct labour hour

Second Quarter = $80000 / 16000 = $5 per direct labour hour

Third Quarter = $500000 / 12500 = $4 per direct labour hour

Fourth Quarter = $70000 / 14000 = $5 per direct labour hour

Cost of one unit:

Jan: Product cost = DM +DL +MOH = $100 +20 *$15 + 20* $4 = $480

April: Product cost = DM +DL +MOH = $100 +20 *$15 + 20* $5 = $500

Price per unit:

Selling price In January = $480 *1.1 = $528

Selling price In April = $500 *1.1 = $550

Annual rate:

Predetermined rate (annually) = $300,000/67,500 = $4.4 per labour hour

Product cost = DM + DL + MOH = $100 +20 *$15 + 20* $4.4 = $488

Sale price = $488 * 1.1 = $ 536.8

Quarterly basis rates can reflect the changes in product cost and price more accurately in

January and April, since the overhead rates are different. The fundamental question for this

case is that the managers are undecided as to whether to use machine hours all labor hours

to allocate the amount of factory overhead that impacts the decision. So, quarterly rates

stimulate managers to take actions when costs increase across months. If we use the annual

real production process. He thinks that direct labour hours should be the allocation base

because about half of the production process is labour oriented. The following estimates are

made for the current year:

A200 requires 20 direct labour hours per unit.

Calculate the price to be charged for a unit of A200 using direct labour hours as the

allocation base if it is manufactured in January versus April, assuming the company's pricing

policy calls for a 10 percent markup over product cost. You can choose to use either the

quarterly rates or the annual rate, but state the reason for your choice.

Predetermined overhead rate (Quarterly basis)

First Quarter = $100000 / 25000 = $4 per direct labour hour

Second Quarter = $80000 / 16000 = $5 per direct labour hour

Third Quarter = $500000 / 12500 = $4 per direct labour hour

Fourth Quarter = $70000 / 14000 = $5 per direct labour hour

Cost of one unit:

Jan: Product cost = DM +DL +MOH = $100 +20 *$15 + 20* $4 = $480

April: Product cost = DM +DL +MOH = $100 +20 *$15 + 20* $5 = $500

Price per unit:

Selling price In January = $480 *1.1 = $528

Selling price In April = $500 *1.1 = $550

Annual rate:

Predetermined rate (annually) = $300,000/67,500 = $4.4 per labour hour

Product cost = DM + DL + MOH = $100 +20 *$15 + 20* $4.4 = $488

Sale price = $488 * 1.1 = $ 536.8

Quarterly basis rates can reflect the changes in product cost and price more accurately in

January and April, since the overhead rates are different. The fundamental question for this

case is that the managers are undecided as to whether to use machine hours all labor hours

to allocate the amount of factory overhead that impacts the decision. So, quarterly rates

stimulate managers to take actions when costs increase across months. If we use the annual

rate, we cannot find out the different in product costs and prices between January and April.

Therefore, we choose to use Quarterly basis rates.

[There is no absolute judgement criterion on which rate is better. You always have to link the

question to the business context of the case. The quarterly rates reflect changes in costs but

the question is whether the prices should be altered accordingly given this is a new product.

The annual rate will address such a pricing concern but it does not create incentive for cost

control. Quarterly rates stimulate managers to take actions when costs increase across

months.]

Question 5:

Please recommend one of the following options to help the company make the pricing

decision on A200:

A. To use machine hours as the plant-wide cost allocation base. Please specify whether you

suggest use the quarterly overhead rates or the annual overhead rate.

B. To use direct labour hours as the plant-wide cost allocation base. Please specify whether

you suggest use the quarterly overhead rates or the annual overhead rate.

C. To use a refined cost allocation method. Please specify what the refinements are.

D. To conduct a more detailed cost analysis including observing the production process

before making a suggestion on the cost allocation method.

key contextual information: (1) the use of both machine and labour hours in production; (2)

the potential for A180 to be discontinued; (3) the similarity in production process between

all camera models.

For option D

Reasons:

1. Gain a more accurate understanding of production. Observing the production process

provides insight into how costs are actually incurred, allowing companies to more accurately

allocate overhead. 可eg. cooling process will cost more in electricity——in traditional cost

calculation it may be ignore and be added in to fixed cost)

2. Flexibility. If the production process varies depending on the different manufacturing time

or productions, company can adjust the cost structure and calculation on time. 可eg.

shopping festival——black friday/double 11——fixed cost may change-- work overtime可

3. Reasonable decision-making. A more comprehensive observation of production process

helps company reveal potential cost or undiscovered production issues or low efficiency.

可eg. recurring failure--Interruption of production and repeated repair costs可

Overall, observing the production process enable company to find the unmatched part

between the theoretical calculation and real production and then narrow the gap between

estimated budget and actual cost.

Therefore, we choose to use Quarterly basis rates.

[There is no absolute judgement criterion on which rate is better. You always have to link the

question to the business context of the case. The quarterly rates reflect changes in costs but

the question is whether the prices should be altered accordingly given this is a new product.

The annual rate will address such a pricing concern but it does not create incentive for cost

control. Quarterly rates stimulate managers to take actions when costs increase across

months.]

Question 5:

Please recommend one of the following options to help the company make the pricing

decision on A200:

A. To use machine hours as the plant-wide cost allocation base. Please specify whether you

suggest use the quarterly overhead rates or the annual overhead rate.

B. To use direct labour hours as the plant-wide cost allocation base. Please specify whether

you suggest use the quarterly overhead rates or the annual overhead rate.

C. To use a refined cost allocation method. Please specify what the refinements are.

D. To conduct a more detailed cost analysis including observing the production process

before making a suggestion on the cost allocation method.

key contextual information: (1) the use of both machine and labour hours in production; (2)

the potential for A180 to be discontinued; (3) the similarity in production process between

all camera models.

For option D

Reasons:

1. Gain a more accurate understanding of production. Observing the production process

provides insight into how costs are actually incurred, allowing companies to more accurately

allocate overhead. 可eg. cooling process will cost more in electricity——in traditional cost

calculation it may be ignore and be added in to fixed cost)

2. Flexibility. If the production process varies depending on the different manufacturing time

or productions, company can adjust the cost structure and calculation on time. 可eg.

shopping festival——black friday/double 11——fixed cost may change-- work overtime可

3. Reasonable decision-making. A more comprehensive observation of production process

helps company reveal potential cost or undiscovered production issues or low efficiency.

可eg. recurring failure--Interruption of production and repeated repair costs可

Overall, observing the production process enable company to find the unmatched part

between the theoretical calculation and real production and then narrow the gap between

estimated budget and actual cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

We choose Option D for the following reason:

1.Option A and B cannot accurately reflect the relationship between overhead costs and the

level of activities.

2. For Option C, we cannot find a refined cost allocation method to accurate reflect the

relationship between overhead costs and the level of activities now.

3. Therefore, we need to conduct a more detailed cost analysis.

We challenged Team 50X (they choose Option A) on the following:

1. ignores the influence of factors like direct labor, material costs, and other overhead costs

2.If different products or production lines rely on machines differently in their production

process, this approach may result in some products being over-costed and others under-

costed. Additionally, it can also lead to inaccurate cost allocations if the maintenance and

operating costs of the machines change.

We challenged Team 50X (they choose Option C) on the following:

1. Option C depending on the specific circumstances of the company and the nature of the

product A200, need to give more specified calculation and explanation.

2.

We challenged Team 504 (They choose Option D) on the following:

How do they adjust the quarterly different of product cost.

The incurrence of cost, we are not sure which factor is more aligned to the cost incurrence

pattern, is it labor hour or machine hour? We need more info to find out which one is the

better cost allocation base.

1.Option A and B cannot accurately reflect the relationship between overhead costs and the

level of activities.

2. For Option C, we cannot find a refined cost allocation method to accurate reflect the

relationship between overhead costs and the level of activities now.

3. Therefore, we need to conduct a more detailed cost analysis.

We challenged Team 50X (they choose Option A) on the following:

1. ignores the influence of factors like direct labor, material costs, and other overhead costs

2.If different products or production lines rely on machines differently in their production

process, this approach may result in some products being over-costed and others under-

costed. Additionally, it can also lead to inaccurate cost allocations if the maintenance and

operating costs of the machines change.

We challenged Team 50X (they choose Option C) on the following:

1. Option C depending on the specific circumstances of the company and the nature of the

product A200, need to give more specified calculation and explanation.

2.

We challenged Team 504 (They choose Option D) on the following:

How do they adjust the quarterly different of product cost.

The incurrence of cost, we are not sure which factor is more aligned to the cost incurrence

pattern, is it labor hour or machine hour? We need more info to find out which one is the

better cost allocation base.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.