Corporate Accounting

VerifiedAdded on 2023/03/20

|10

|1245

|42

AI Summary

This document provides comprehensive study material on corporate accounting, including acquisition analysis, journal entries, consolidated worksheet, and the preparation of consolidated financial statements. It also includes a bibliography for further reference.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE ACCOUNTING

Table of Contents

Acquisition Analysis:.......................................................................................................................2

Journal Entries:................................................................................................................................3

Consolidated Worksheet:.................................................................................................................4

Prepare the consolidated financial statements of Griffin Ltd at 30 June 2019:...............................6

Bibliography:...................................................................................................................................9

Table of Contents

Acquisition Analysis:.......................................................................................................................2

Journal Entries:................................................................................................................................3

Consolidated Worksheet:.................................................................................................................4

Prepare the consolidated financial statements of Griffin Ltd at 30 June 2019:...............................6

Bibliography:...................................................................................................................................9

2CORPORATE ACCOUNTING

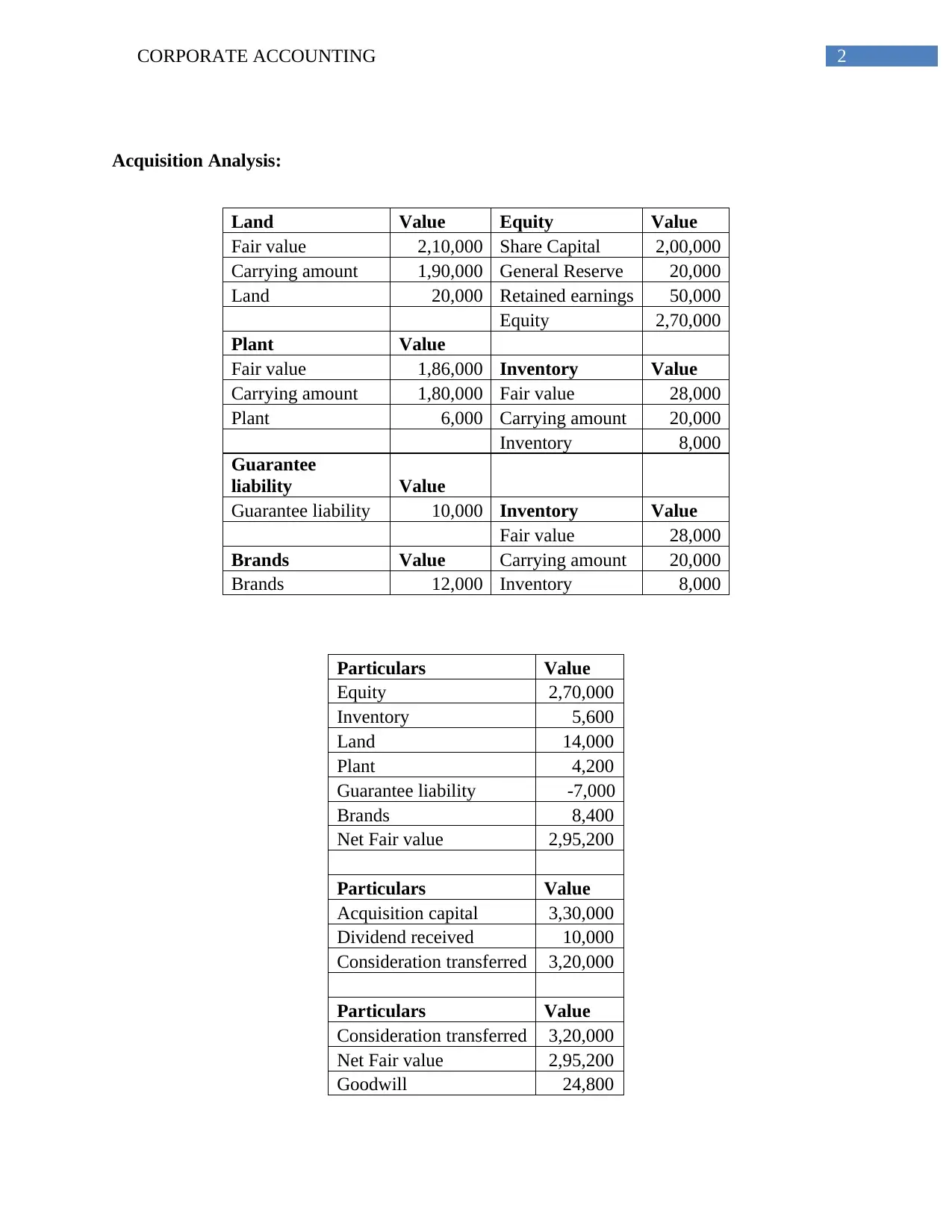

Acquisition Analysis:

Land Value Equity Value

Fair value 2,10,000 Share Capital 2,00,000

Carrying amount 1,90,000 General Reserve 20,000

Land 20,000 Retained earnings 50,000

Equity 2,70,000

Plant Value

Fair value 1,86,000 Inventory Value

Carrying amount 1,80,000 Fair value 28,000

Plant 6,000 Carrying amount 20,000

Inventory 8,000

Guarantee

liability Value

Guarantee liability 10,000 Inventory Value

Fair value 28,000

Brands Value Carrying amount 20,000

Brands 12,000 Inventory 8,000

Particulars Value

Equity 2,70,000

Inventory 5,600

Land 14,000

Plant 4,200

Guarantee liability -7,000

Brands 8,400

Net Fair value 2,95,200

Particulars Value

Acquisition capital 3,30,000

Dividend received 10,000

Consideration transferred 3,20,000

Particulars Value

Consideration transferred 3,20,000

Net Fair value 2,95,200

Goodwill 24,800

Acquisition Analysis:

Land Value Equity Value

Fair value 2,10,000 Share Capital 2,00,000

Carrying amount 1,90,000 General Reserve 20,000

Land 20,000 Retained earnings 50,000

Equity 2,70,000

Plant Value

Fair value 1,86,000 Inventory Value

Carrying amount 1,80,000 Fair value 28,000

Plant 6,000 Carrying amount 20,000

Inventory 8,000

Guarantee

liability Value

Guarantee liability 10,000 Inventory Value

Fair value 28,000

Brands Value Carrying amount 20,000

Brands 12,000 Inventory 8,000

Particulars Value

Equity 2,70,000

Inventory 5,600

Land 14,000

Plant 4,200

Guarantee liability -7,000

Brands 8,400

Net Fair value 2,95,200

Particulars Value

Acquisition capital 3,30,000

Dividend received 10,000

Consideration transferred 3,20,000

Particulars Value

Consideration transferred 3,20,000

Net Fair value 2,95,200

Goodwill 24,800

3CORPORATE ACCOUNTING

The above table provides information about the calculation of goodwill, which is

conducted after evaluating the fair value of assets that is been acquired by Griffin Ltd of Frank

Ltd.

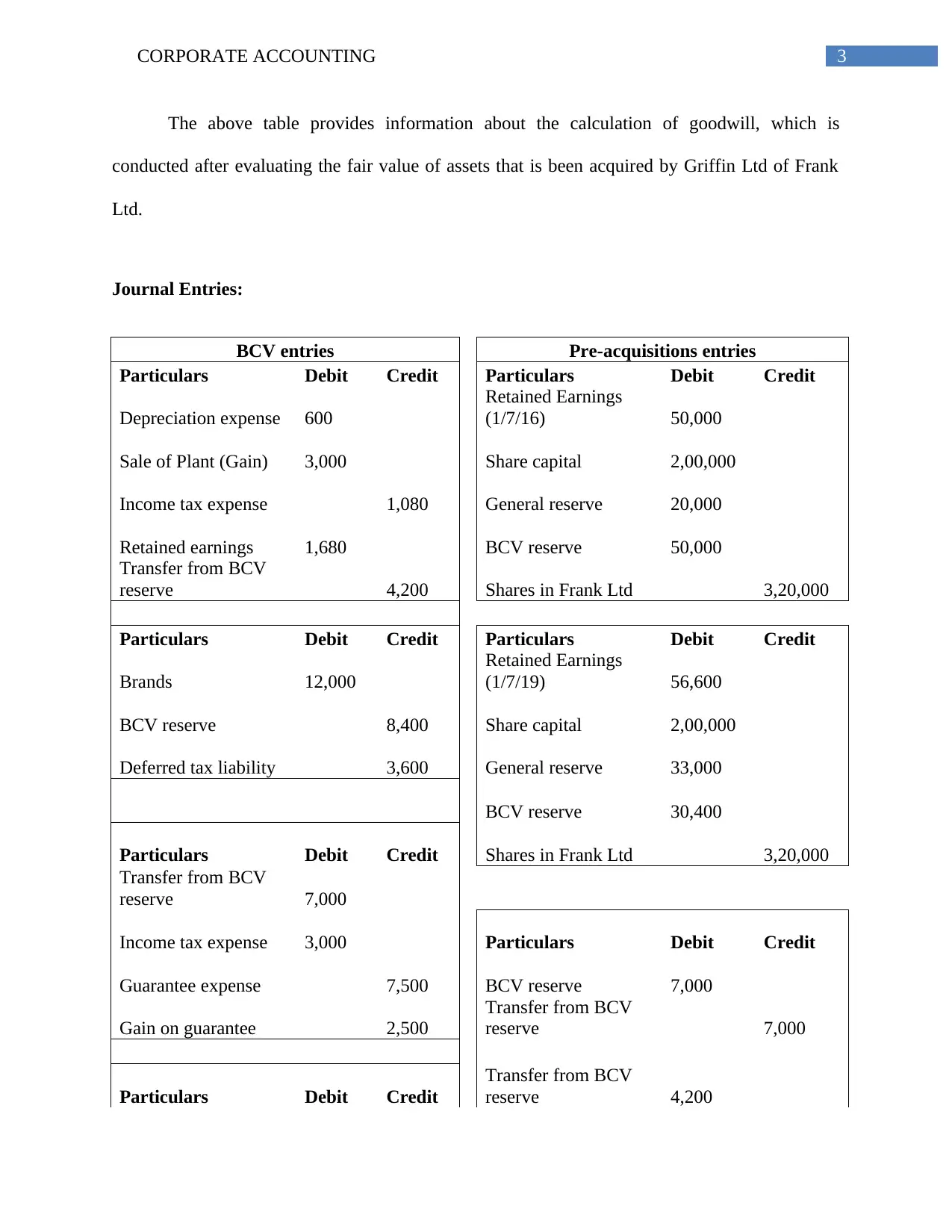

Journal Entries:

BCV entries Pre-acquisitions entries

Particulars Debit Credit Particulars Debit Credit

Depreciation expense 600

Retained Earnings

(1/7/16) 50,000

Sale of Plant (Gain) 3,000 Share capital 2,00,000

Income tax expense 1,080 General reserve 20,000

Retained earnings 1,680 BCV reserve 50,000

Transfer from BCV

reserve 4,200 Shares in Frank Ltd 3,20,000

Particulars Debit Credit Particulars Debit Credit

Brands 12,000

Retained Earnings

(1/7/19) 56,600

BCV reserve 8,400 Share capital 2,00,000

Deferred tax liability 3,600 General reserve 33,000

BCV reserve 30,400

Particulars Debit Credit Shares in Frank Ltd 3,20,000

Transfer from BCV

reserve 7,000

Income tax expense 3,000 Particulars Debit Credit

Guarantee expense 7,500 BCV reserve 7,000

Gain on guarantee 2,500

Transfer from BCV

reserve 7,000

Particulars Debit Credit

Transfer from BCV

reserve 4,200

The above table provides information about the calculation of goodwill, which is

conducted after evaluating the fair value of assets that is been acquired by Griffin Ltd of Frank

Ltd.

Journal Entries:

BCV entries Pre-acquisitions entries

Particulars Debit Credit Particulars Debit Credit

Depreciation expense 600

Retained Earnings

(1/7/16) 50,000

Sale of Plant (Gain) 3,000 Share capital 2,00,000

Income tax expense 1,080 General reserve 20,000

Retained earnings 1,680 BCV reserve 50,000

Transfer from BCV

reserve 4,200 Shares in Frank Ltd 3,20,000

Particulars Debit Credit Particulars Debit Credit

Brands 12,000

Retained Earnings

(1/7/19) 56,600

BCV reserve 8,400 Share capital 2,00,000

Deferred tax liability 3,600 General reserve 33,000

BCV reserve 30,400

Particulars Debit Credit Shares in Frank Ltd 3,20,000

Transfer from BCV

reserve 7,000

Income tax expense 3,000 Particulars Debit Credit

Guarantee expense 7,500 BCV reserve 7,000

Gain on guarantee 2,500

Transfer from BCV

reserve 7,000

Particulars Debit Credit

Transfer from BCV

reserve 4,200

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE ACCOUNTING

Goodwill 24,800 BCV reserve 4,200

BCV reserve 24,800

General reserve 15,000

Transfer to general

reserve 15,000

The journal entries depicted in the above table states about the overall BCV and other

acquisition entries, which is required for completing consolidated worksheet and deriving the

accurate value of the firm.

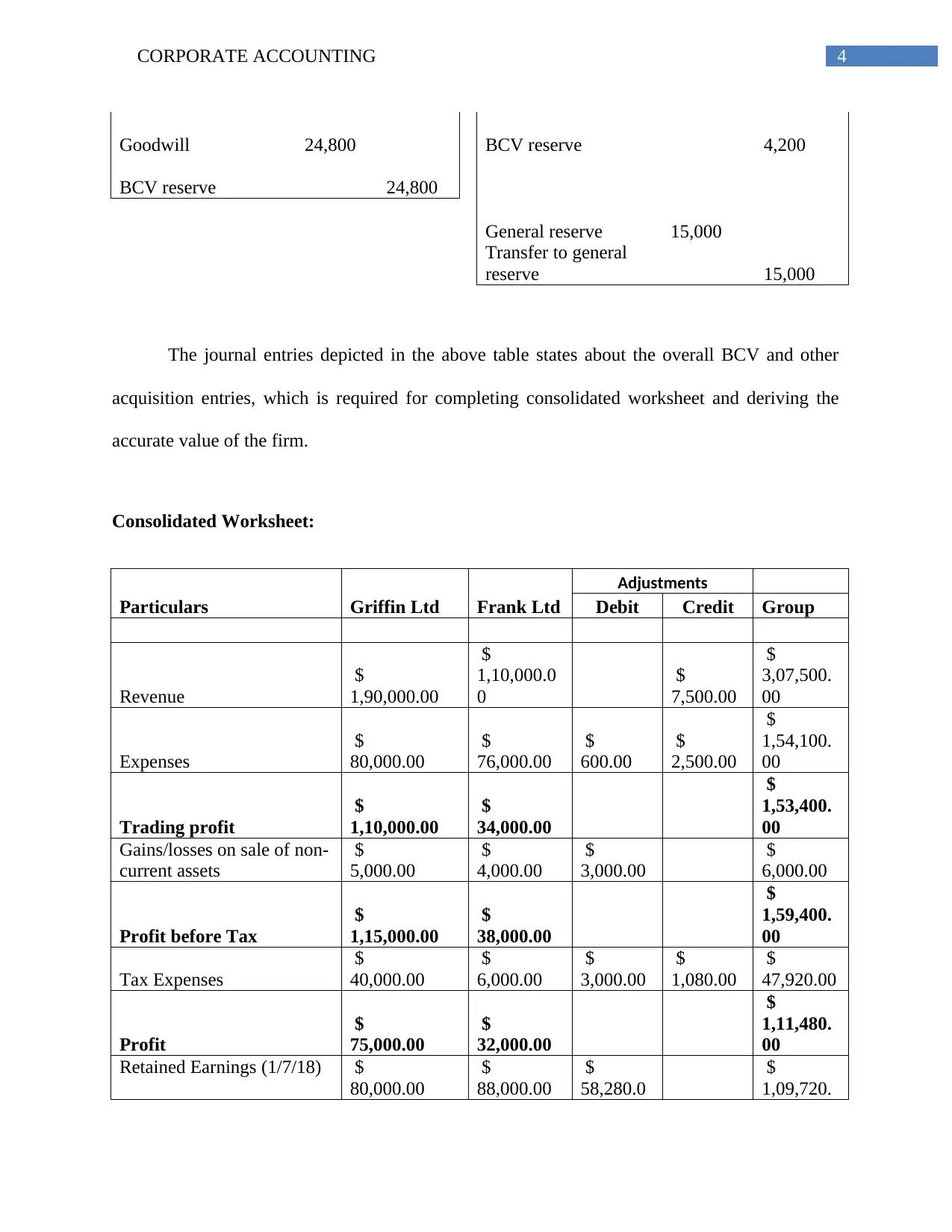

Consolidated Worksheet:

Particulars Griffin Ltd Frank Ltd

Adjustments

Debit Credit Group

Revenue

$

1,90,000.00

$

1,10,000.0

0

$

7,500.00

$

3,07,500.

00

Expenses

$

80,000.00

$

76,000.00

$

600.00

$

2,500.00

$

1,54,100.

00

Trading profit

$

1,10,000.00

$

34,000.00

$

1,53,400.

00

Gains/losses on sale of non-

current assets

$

5,000.00

$

4,000.00

$

3,000.00

$

6,000.00

Profit before Tax

$

1,15,000.00

$

38,000.00

$

1,59,400.

00

Tax Expenses

$

40,000.00

$

6,000.00

$

3,000.00

$

1,080.00

$

47,920.00

Profit

$

75,000.00

$

32,000.00

$

1,11,480.

00

Retained Earnings (1/7/18) $

80,000.00

$

88,000.00

$

58,280.0

$

1,09,720.

Goodwill 24,800 BCV reserve 4,200

BCV reserve 24,800

General reserve 15,000

Transfer to general

reserve 15,000

The journal entries depicted in the above table states about the overall BCV and other

acquisition entries, which is required for completing consolidated worksheet and deriving the

accurate value of the firm.

Consolidated Worksheet:

Particulars Griffin Ltd Frank Ltd

Adjustments

Debit Credit Group

Revenue

$

1,90,000.00

$

1,10,000.0

0

$

7,500.00

$

3,07,500.

00

Expenses

$

80,000.00

$

76,000.00

$

600.00

$

2,500.00

$

1,54,100.

00

Trading profit

$

1,10,000.00

$

34,000.00

$

1,53,400.

00

Gains/losses on sale of non-

current assets

$

5,000.00

$

4,000.00

$

3,000.00

$

6,000.00

Profit before Tax

$

1,15,000.00

$

38,000.00

$

1,59,400.

00

Tax Expenses

$

40,000.00

$

6,000.00

$

3,000.00

$

1,080.00

$

47,920.00

Profit

$

75,000.00

$

32,000.00

$

1,11,480.

00

Retained Earnings (1/7/18) $

80,000.00

$

88,000.00

$

58,280.0

$

1,09,720.

5CORPORATE ACCOUNTING

0 00

Transfer from BCVR

$

-

$

-

$

11,200.0

0

$

11,200.0

0

$

-

Dividend declared

$

34,000.00

$

-

$

34,000.00

T'fer to gen reserve

$

15,000.00

$

15,000.0

0

$

-

Retained Earnings

(30/6/19)

$

1,21,000.00

$

1,05,000.0

0

$

1,87,200.

00

Share Capital

$

2,80,000.00

$

2,00,000.0

0

$

2,00,000.

00

$

2,80,000.

00

General reserve

$

20,000.00

$

48,000.00

$

48,000.0

0

$

20,000.00

BCVR

$

-

$

-

$

37,400.0

0

$

37,400.0

0

$

-

$

4,21,000.00

$

3,53,000.0

0

$

4,87,200.

00

Asset Revaluation Surplus

(1/7/18)

$

12,000.00

$

-

$

12,000.00

Gains/Losses

$

12,000.00

$

-

$

12,000.00

Asset Revaluation Surplus

(30/6/19)

$

24,000.00

$

-

$

24,000.00

Total Equity

$

4,45,000.00

$

3,53,000.0

0

$

5,11,200.

00

Provisions

$

15,000.00

$

12,000.00

$

27,000.00

Payables

$

40,000.00

$

8,000.00

$

48,000.00

Defer.tax liabilities

$

-

$

-

$

3,600.00

$

3,600.00

Total Liabilities

$

55,000.00

$

20,000.00

$

78,600.00

Total Equity & Liabilities

$

5,00,000.00

$

3,73,000.0

0

$

5,89,800.

00

Shares in Frank Ltd

$

3,20,000.00

$

-

$

3,20,000.

$

-

0 00

Transfer from BCVR

$

-

$

-

$

11,200.0

0

$

11,200.0

0

$

-

Dividend declared

$

34,000.00

$

-

$

34,000.00

T'fer to gen reserve

$

15,000.00

$

15,000.0

0

$

-

Retained Earnings

(30/6/19)

$

1,21,000.00

$

1,05,000.0

0

$

1,87,200.

00

Share Capital

$

2,80,000.00

$

2,00,000.0

0

$

2,00,000.

00

$

2,80,000.

00

General reserve

$

20,000.00

$

48,000.00

$

48,000.0

0

$

20,000.00

BCVR

$

-

$

-

$

37,400.0

0

$

37,400.0

0

$

-

$

4,21,000.00

$

3,53,000.0

0

$

4,87,200.

00

Asset Revaluation Surplus

(1/7/18)

$

12,000.00

$

-

$

12,000.00

Gains/Losses

$

12,000.00

$

-

$

12,000.00

Asset Revaluation Surplus

(30/6/19)

$

24,000.00

$

-

$

24,000.00

Total Equity

$

4,45,000.00

$

3,53,000.0

0

$

5,11,200.

00

Provisions

$

15,000.00

$

12,000.00

$

27,000.00

Payables

$

40,000.00

$

8,000.00

$

48,000.00

Defer.tax liabilities

$

-

$

-

$

3,600.00

$

3,600.00

Total Liabilities

$

55,000.00

$

20,000.00

$

78,600.00

Total Equity & Liabilities

$

5,00,000.00

$

3,73,000.0

0

$

5,89,800.

00

Shares in Frank Ltd

$

3,20,000.00

$

-

$

3,20,000.

$

-

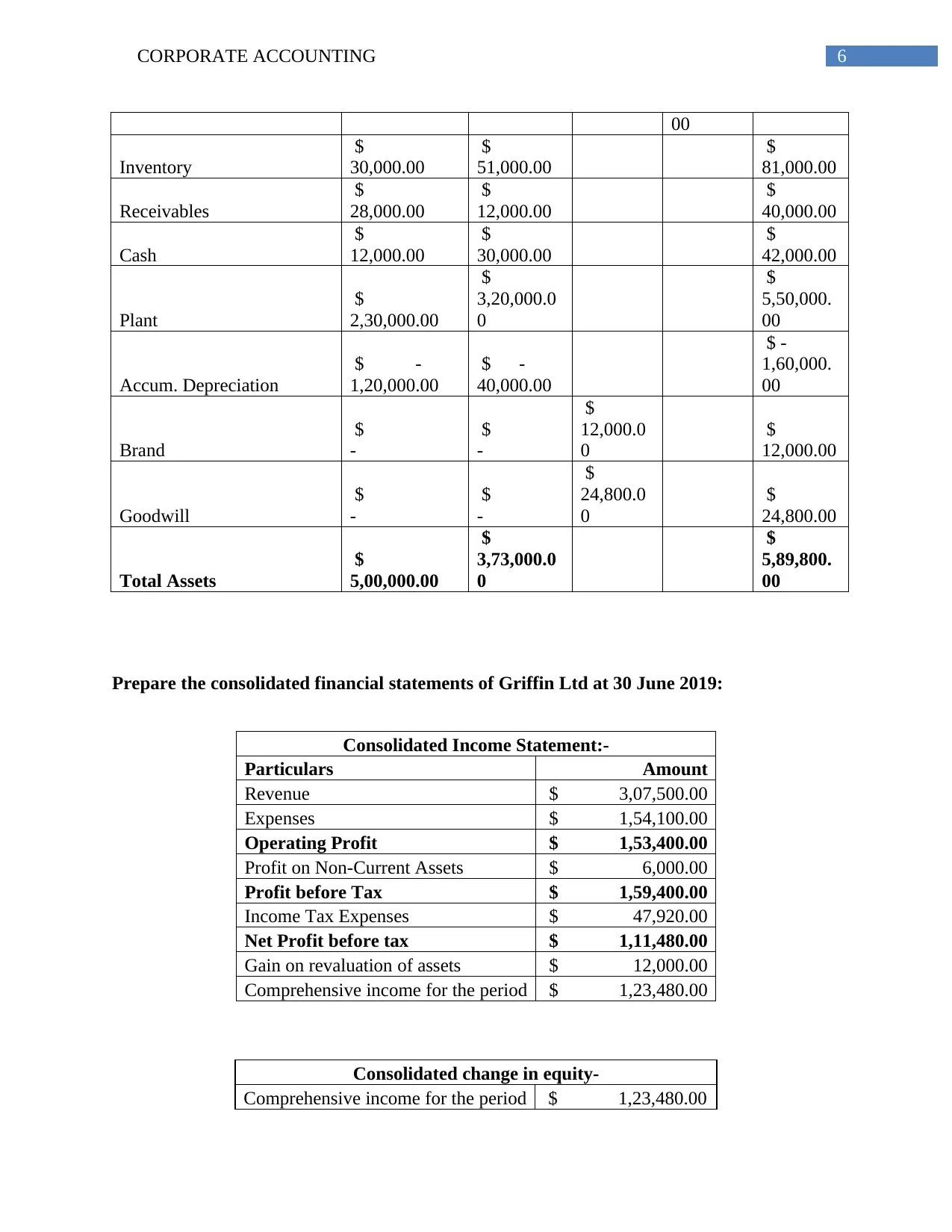

6CORPORATE ACCOUNTING

00

Inventory

$

30,000.00

$

51,000.00

$

81,000.00

Receivables

$

28,000.00

$

12,000.00

$

40,000.00

Cash

$

12,000.00

$

30,000.00

$

42,000.00

Plant

$

2,30,000.00

$

3,20,000.0

0

$

5,50,000.

00

Accum. Depreciation

$ -

1,20,000.00

$ -

40,000.00

$ -

1,60,000.

00

Brand

$

-

$

-

$

12,000.0

0

$

12,000.00

Goodwill

$

-

$

-

$

24,800.0

0

$

24,800.00

Total Assets

$

5,00,000.00

$

3,73,000.0

0

$

5,89,800.

00

Prepare the consolidated financial statements of Griffin Ltd at 30 June 2019:

Consolidated Income Statement:-

Particulars Amount

Revenue $ 3,07,500.00

Expenses $ 1,54,100.00

Operating Profit $ 1,53,400.00

Profit on Non-Current Assets $ 6,000.00

Profit before Tax $ 1,59,400.00

Income Tax Expenses $ 47,920.00

Net Profit before tax $ 1,11,480.00

Gain on revaluation of assets $ 12,000.00

Comprehensive income for the period $ 1,23,480.00

Consolidated change in equity-

Comprehensive income for the period $ 1,23,480.00

00

Inventory

$

30,000.00

$

51,000.00

$

81,000.00

Receivables

$

28,000.00

$

12,000.00

$

40,000.00

Cash

$

12,000.00

$

30,000.00

$

42,000.00

Plant

$

2,30,000.00

$

3,20,000.0

0

$

5,50,000.

00

Accum. Depreciation

$ -

1,20,000.00

$ -

40,000.00

$ -

1,60,000.

00

Brand

$

-

$

-

$

12,000.0

0

$

12,000.00

Goodwill

$

-

$

-

$

24,800.0

0

$

24,800.00

Total Assets

$

5,00,000.00

$

3,73,000.0

0

$

5,89,800.

00

Prepare the consolidated financial statements of Griffin Ltd at 30 June 2019:

Consolidated Income Statement:-

Particulars Amount

Revenue $ 3,07,500.00

Expenses $ 1,54,100.00

Operating Profit $ 1,53,400.00

Profit on Non-Current Assets $ 6,000.00

Profit before Tax $ 1,59,400.00

Income Tax Expenses $ 47,920.00

Net Profit before tax $ 1,11,480.00

Gain on revaluation of assets $ 12,000.00

Comprehensive income for the period $ 1,23,480.00

Consolidated change in equity-

Comprehensive income for the period $ 1,23,480.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

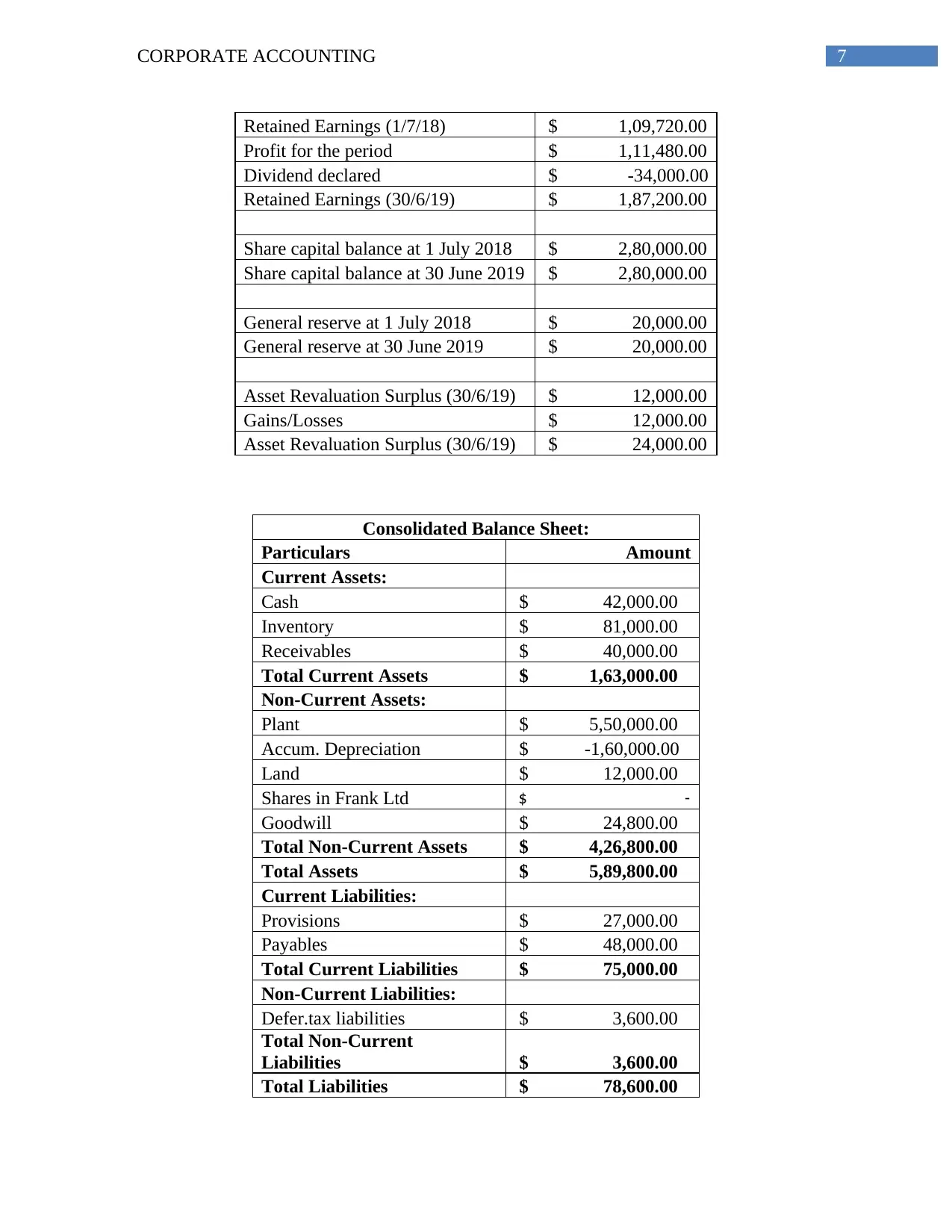

Retained Earnings (1/7/18) $ 1,09,720.00

Profit for the period $ 1,11,480.00

Dividend declared $ -34,000.00

Retained Earnings (30/6/19) $ 1,87,200.00

Share capital balance at 1 July 2018 $ 2,80,000.00

Share capital balance at 30 June 2019 $ 2,80,000.00

General reserve at 1 July 2018 $ 20,000.00

General reserve at 30 June 2019 $ 20,000.00

Asset Revaluation Surplus (30/6/19) $ 12,000.00

Gains/Losses $ 12,000.00

Asset Revaluation Surplus (30/6/19) $ 24,000.00

Consolidated Balance Sheet:

Particulars Amount

Current Assets:

Cash $ 42,000.00

Inventory $ 81,000.00

Receivables $ 40,000.00

Total Current Assets $ 1,63,000.00

Non-Current Assets:

Plant $ 5,50,000.00

Accum. Depreciation $ -1,60,000.00

Land $ 12,000.00

Shares in Frank Ltd $ -

Goodwill $ 24,800.00

Total Non-Current Assets $ 4,26,800.00

Total Assets $ 5,89,800.00

Current Liabilities:

Provisions $ 27,000.00

Payables $ 48,000.00

Total Current Liabilities $ 75,000.00

Non-Current Liabilities:

Defer.tax liabilities $ 3,600.00

Total Non-Current

Liabilities $ 3,600.00

Total Liabilities $ 78,600.00

Retained Earnings (1/7/18) $ 1,09,720.00

Profit for the period $ 1,11,480.00

Dividend declared $ -34,000.00

Retained Earnings (30/6/19) $ 1,87,200.00

Share capital balance at 1 July 2018 $ 2,80,000.00

Share capital balance at 30 June 2019 $ 2,80,000.00

General reserve at 1 July 2018 $ 20,000.00

General reserve at 30 June 2019 $ 20,000.00

Asset Revaluation Surplus (30/6/19) $ 12,000.00

Gains/Losses $ 12,000.00

Asset Revaluation Surplus (30/6/19) $ 24,000.00

Consolidated Balance Sheet:

Particulars Amount

Current Assets:

Cash $ 42,000.00

Inventory $ 81,000.00

Receivables $ 40,000.00

Total Current Assets $ 1,63,000.00

Non-Current Assets:

Plant $ 5,50,000.00

Accum. Depreciation $ -1,60,000.00

Land $ 12,000.00

Shares in Frank Ltd $ -

Goodwill $ 24,800.00

Total Non-Current Assets $ 4,26,800.00

Total Assets $ 5,89,800.00

Current Liabilities:

Provisions $ 27,000.00

Payables $ 48,000.00

Total Current Liabilities $ 75,000.00

Non-Current Liabilities:

Defer.tax liabilities $ 3,600.00

Total Non-Current

Liabilities $ 3,600.00

Total Liabilities $ 78,600.00

8CORPORATE ACCOUNTING

Equity:

Share Capital $ 2,80,000.00

Asset Revaluation Surplus $ 44,000.00

Retained Earnings $ 1,87,200.00

Total Equity $ 5,11,200.00

Total Liabilities and Equity $ 5,89,800.00

Equity:

Share Capital $ 2,80,000.00

Asset Revaluation Surplus $ 44,000.00

Retained Earnings $ 1,87,200.00

Total Equity $ 5,11,200.00

Total Liabilities and Equity $ 5,89,800.00

9CORPORATE ACCOUNTING

Bibliography:

Cîrstea, A., 2014. The need for public sector consolidated financial statements. Procedia

Economics and Finance, 15, pp.1289-1296.

edia-Social and Behavioral Sciences, 109, pp.976-982.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Proc

Palea, V., 2014. Are IFRS value-relevant for separate financial statements? Evidence from the

Italian stock market. Journal of International Accounting, Auditing and Taxation, 23(1), pp.1-17.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Sedki, S.S., Smith, A. and Strickland, A., 2014. Differences and similarities between IFRS and

GAAP on inventory, revenue recognition and consolidated financial statements. Journal of

Accounting and Finance, 14(2), p.120.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

Bibliography:

Cîrstea, A., 2014. The need for public sector consolidated financial statements. Procedia

Economics and Finance, 15, pp.1289-1296.

edia-Social and Behavioral Sciences, 109, pp.976-982.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Proc

Palea, V., 2014. Are IFRS value-relevant for separate financial statements? Evidence from the

Italian stock market. Journal of International Accounting, Auditing and Taxation, 23(1), pp.1-17.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Sedki, S.S., Smith, A. and Strickland, A., 2014. Differences and similarities between IFRS and

GAAP on inventory, revenue recognition and consolidated financial statements. Journal of

Accounting and Finance, 14(2), p.120.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.