Corporate Accounting: Analysis of Financial Statements of Adalta Limited and Acrux Limited

VerifiedAdded on 2023/06/05

|34

|3747

|150

AI Summary

The report analyzes the financial statements of Adalta Limited and Acrux Limited, both belonging to the pharmaceutical industry. It covers the equity, cash flow, and other comprehensive income statements, along with deferred tax assets and liabilities. The report also compares the two companies and highlights the importance of financial statements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CORPORATE ACCOUNTING 1

CORPORATE

ACCOUNTING

CORPORATE

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 2

Executive summary:

The assignment sought to choose 2 companies and do analysis of the financial statements.

The companies chosen for review are Adalta Limited and Acrux Limited. Both of these

companies belong to the industry of Pharmaceuticals.

The report talks about the break-up of the equity of the company, its other comprehensive

statement, the statement of cash flows. The report further throws light on the comparison of

these two as well (ASX, 2018). The report further talks about the deferred tax assets or the

deferred tax liabilities of the company, the difference between the effective tax rate and the

cash tax rate along with the importance of these financial statements.

Executive summary:

The assignment sought to choose 2 companies and do analysis of the financial statements.

The companies chosen for review are Adalta Limited and Acrux Limited. Both of these

companies belong to the industry of Pharmaceuticals.

The report talks about the break-up of the equity of the company, its other comprehensive

statement, the statement of cash flows. The report further throws light on the comparison of

these two as well (ASX, 2018). The report further talks about the deferred tax assets or the

deferred tax liabilities of the company, the difference between the effective tax rate and the

cash tax rate along with the importance of these financial statements.

CORPORATE ACCOUNTING 3

Contents

Introduction:..........................................................................................................................................4

Owners’ equity:.....................................................................................................................................4

Part i:.................................................................................................................................................4

Part ii:................................................................................................................................................8

Cash flow statement:.............................................................................................................................9

Part iii:...............................................................................................................................................9

Part IV:............................................................................................................................................21

Part v:..............................................................................................................................................22

Other comprehensive income statement:.............................................................................................23

Part vi:.............................................................................................................................................23

Part vii:............................................................................................................................................26

Part viii:...........................................................................................................................................27

Part ix:.............................................................................................................................................27

Accounting for corporate income tax:.................................................................................................28

Part x:..............................................................................................................................................28

Part xi:.............................................................................................................................................28

Part xii:............................................................................................................................................29

Part xiii:...........................................................................................................................................29

Part xiv:...........................................................................................................................................29

Part xv:............................................................................................................................................30

Part xvi:...........................................................................................................................................31

References:......................................................................................................................................33

Contents

Introduction:..........................................................................................................................................4

Owners’ equity:.....................................................................................................................................4

Part i:.................................................................................................................................................4

Part ii:................................................................................................................................................8

Cash flow statement:.............................................................................................................................9

Part iii:...............................................................................................................................................9

Part IV:............................................................................................................................................21

Part v:..............................................................................................................................................22

Other comprehensive income statement:.............................................................................................23

Part vi:.............................................................................................................................................23

Part vii:............................................................................................................................................26

Part viii:...........................................................................................................................................27

Part ix:.............................................................................................................................................27

Accounting for corporate income tax:.................................................................................................28

Part x:..............................................................................................................................................28

Part xi:.............................................................................................................................................28

Part xii:............................................................................................................................................29

Part xiii:...........................................................................................................................................29

Part xiv:...........................................................................................................................................29

Part xv:............................................................................................................................................30

Part xvi:...........................................................................................................................................31

References:......................................................................................................................................33

CORPORATE ACCOUNTING 4

Introduction:

The company chosen for review are Adalta Limited and Acrux Limited. Both of these

companies belong to the sector of Pharmaceuticals.

Adalta limited is the company deals in the technology that copies the shape and the stability

of the crucial antigen binding domain that was initially discovered in the sharks and then

were successfully developed as the human protein. It contains a unique I-body which is then

used for the purposes of treating the serious illnesses or the diseases. The initial focus of such

a company was the creation of the pipeline for the drugs, and were used for the purposes of

treating the fibrotic diseases (Adalta, 2018).

The seocn company is Acrux limited which is the company which is concerned with the

development and the commercialisation of the topical pharmaceuticals. The company came

into being in the year 1998 and uses many of the in house facilities and capabilities. The

company has successfully developed and commercialised through many of the licensees

through a number of different topically applied pharmaceuticals products in the countries of

the US and Europe. The company is in the course of developing an increased range of the

generic products for the market of the United States and the company had achieved this

through its on-site laboratories so that the products could be brought into the market at lower

prices (Acrux, 2018).

Owners’ equity:

Part i:

The following are the desired statements:

Adalta:

Introduction:

The company chosen for review are Adalta Limited and Acrux Limited. Both of these

companies belong to the sector of Pharmaceuticals.

Adalta limited is the company deals in the technology that copies the shape and the stability

of the crucial antigen binding domain that was initially discovered in the sharks and then

were successfully developed as the human protein. It contains a unique I-body which is then

used for the purposes of treating the serious illnesses or the diseases. The initial focus of such

a company was the creation of the pipeline for the drugs, and were used for the purposes of

treating the fibrotic diseases (Adalta, 2018).

The seocn company is Acrux limited which is the company which is concerned with the

development and the commercialisation of the topical pharmaceuticals. The company came

into being in the year 1998 and uses many of the in house facilities and capabilities. The

company has successfully developed and commercialised through many of the licensees

through a number of different topically applied pharmaceuticals products in the countries of

the US and Europe. The company is in the course of developing an increased range of the

generic products for the market of the United States and the company had achieved this

through its on-site laboratories so that the products could be brought into the market at lower

prices (Acrux, 2018).

Owners’ equity:

Part i:

The following are the desired statements:

Adalta:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 5

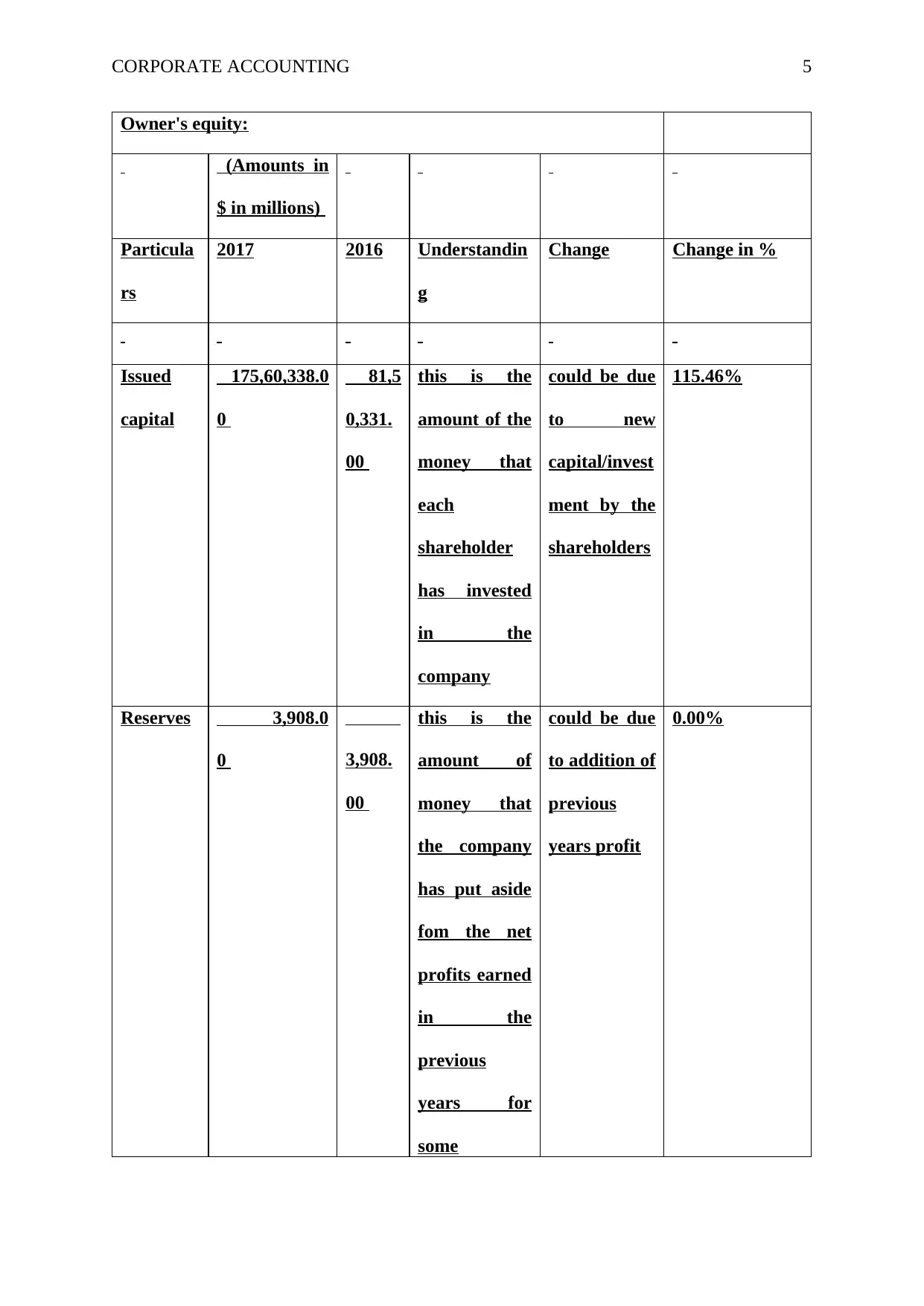

Owner's equity:

(Amounts in

$ in millions)

Particula

rs

2017 2016 Understandin

g

Change Change in %

Issued

capital

175,60,338.0

0

81,5

0,331.

00

this is the

amount of the

money that

each

shareholder

has invested

in the

company

could be due

to new

capital/invest

ment by the

shareholders

115.46%

Reserves 3,908.0

0 3,908.

00

this is the

amount of

money that

the company

has put aside

fom the net

profits earned

in the

previous

years for

some

could be due

to addition of

previous

years profit

0.00%

Owner's equity:

(Amounts in

$ in millions)

Particula

rs

2017 2016 Understandin

g

Change Change in %

Issued

capital

175,60,338.0

0

81,5

0,331.

00

this is the

amount of the

money that

each

shareholder

has invested

in the

company

could be due

to new

capital/invest

ment by the

shareholders

115.46%

Reserves 3,908.0

0 3,908.

00

this is the

amount of

money that

the company

has put aside

fom the net

profits earned

in the

previous

years for

some

could be due

to addition of

previous

years profit

0.00%

CORPORATE ACCOUNTING 6

contingency

that may

arise in future

or for future

unforseen

circumstances

Retained

earnings

-

98,18,868.00

-

69,86,

351.00

these are the

part of the

profits earned

in the

previous

years after

paying off

dividend etc

could be due

to previous

year’s profits

being

transferred

in this

account

40.54%

Total 77,45,378.0

0

11,6

7,888.

00

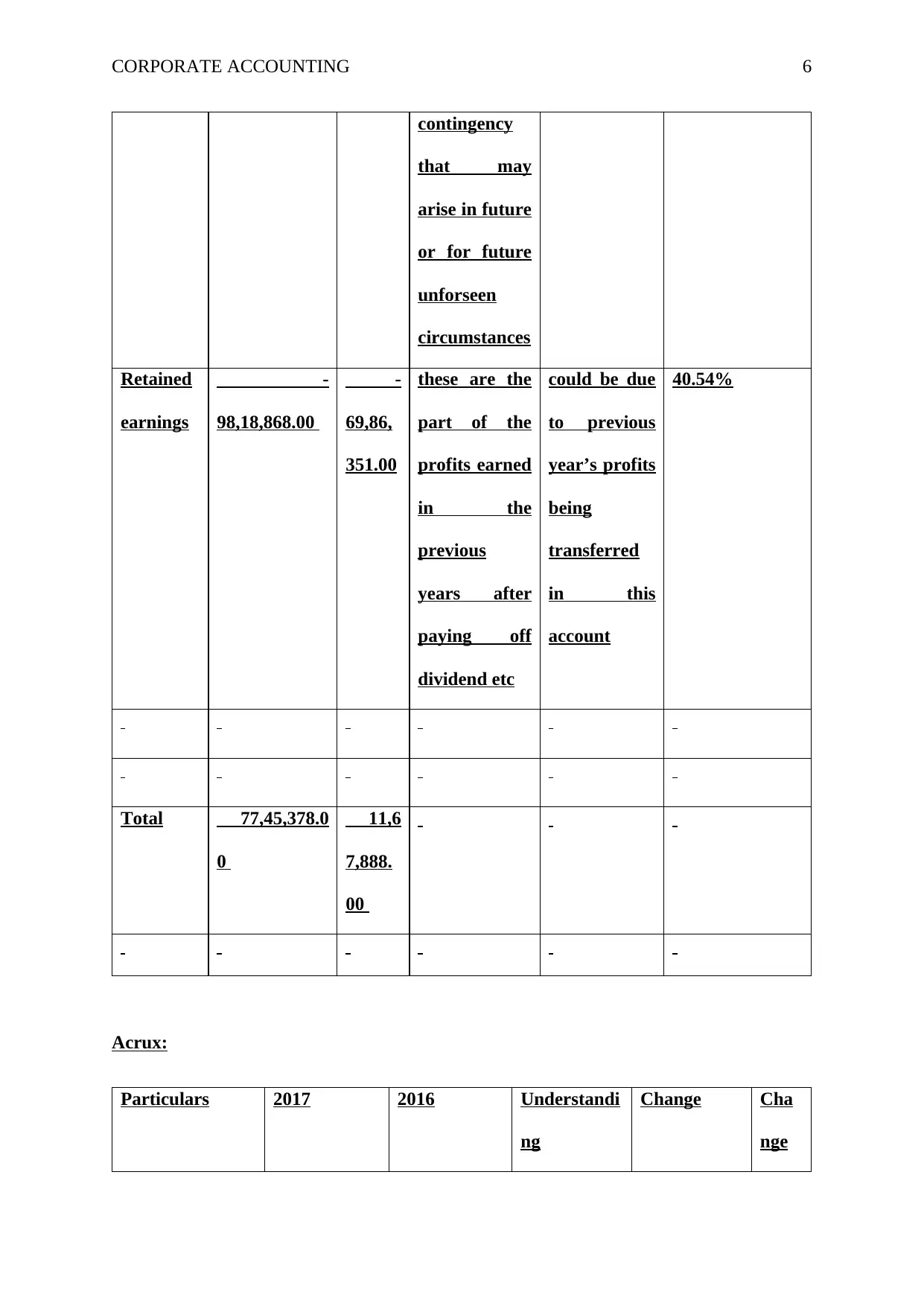

Acrux:

Particulars 2017 2016 Understandi

ng

Change Cha

nge

contingency

that may

arise in future

or for future

unforseen

circumstances

Retained

earnings

-

98,18,868.00

-

69,86,

351.00

these are the

part of the

profits earned

in the

previous

years after

paying off

dividend etc

could be due

to previous

year’s profits

being

transferred

in this

account

40.54%

Total 77,45,378.0

0

11,6

7,888.

00

Acrux:

Particulars 2017 2016 Understandi

ng

Change Cha

nge

CORPORATE ACCOUNTING 7

in %

Contributed

equity

95,

873.00

95,

873.00

this is the

amount of

the money

that each

shareholder

has invested

in the

company

could be due

to no change

in the new

capital/inves

tment by the

shareholders

0.00

%

Retained

earnings

1,

215.00

1,

454.00

these are the

part of the

profits

earned in

the previous

years after

paying off

dividend etc

could be due

to previous

years

profits/(losse

s) being

transferred

in this

account

-

16.44

%

Reserves -

53,163.00

-

53,438.00

this is the

amount of

money that

the company

has put

aside fom

the net

could be due

to addition

of previous

years

profit/(losses

)

-

0.51

%

in %

Contributed

equity

95,

873.00

95,

873.00

this is the

amount of

the money

that each

shareholder

has invested

in the

company

could be due

to no change

in the new

capital/inves

tment by the

shareholders

0.00

%

Retained

earnings

1,

215.00

1,

454.00

these are the

part of the

profits

earned in

the previous

years after

paying off

dividend etc

could be due

to previous

years

profits/(losse

s) being

transferred

in this

account

-

16.44

%

Reserves -

53,163.00

-

53,438.00

this is the

amount of

money that

the company

has put

aside fom

the net

could be due

to addition

of previous

years

profit/(losses

)

-

0.51

%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING 8

profits

earned in

the previous

years for

some

contingency

that may

arise in

future or for

future

unforseen

circumstanc

es

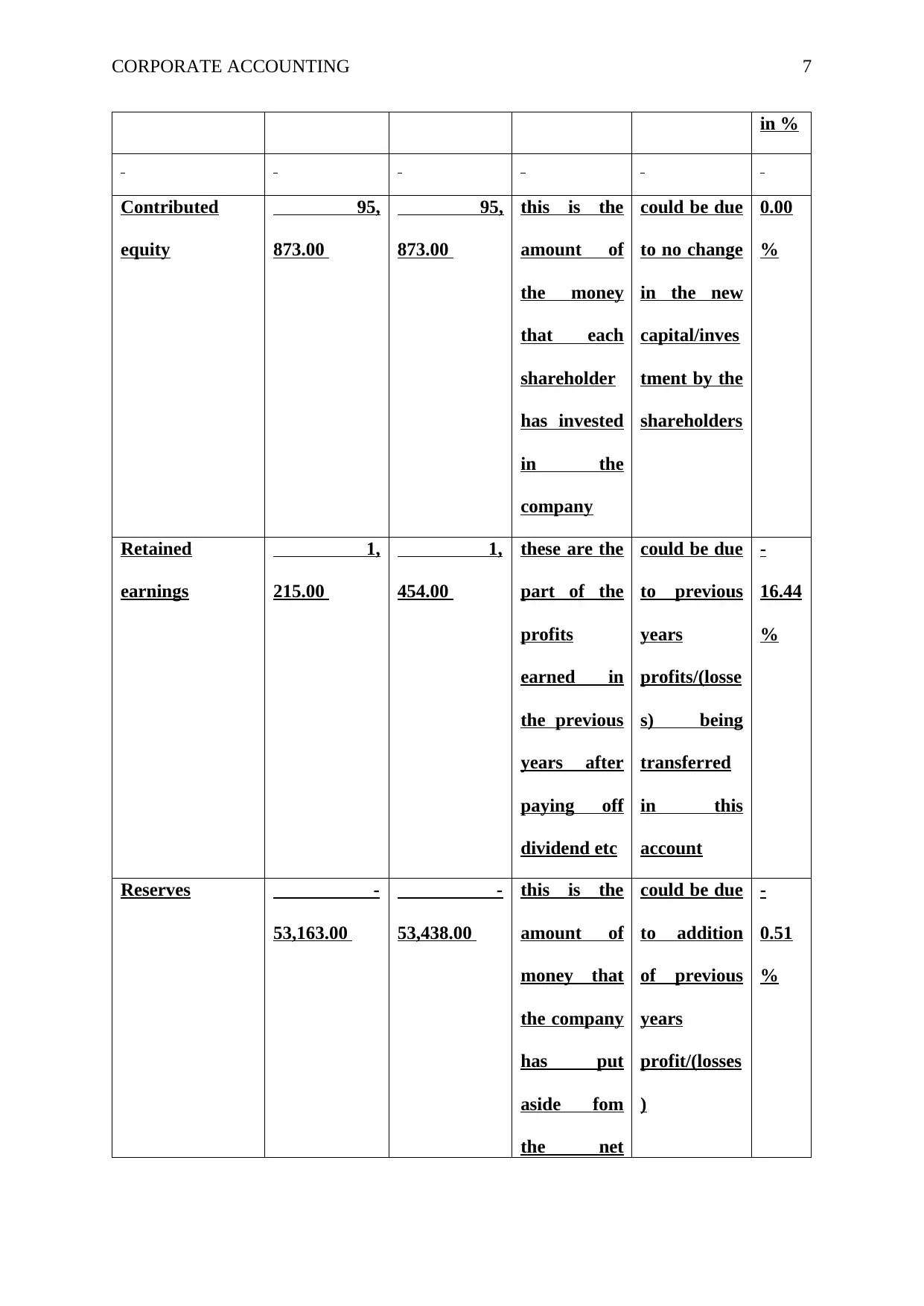

Total 43,

925.00

43,

889.00

Part ii:

The following is the desired analysis:

Adalta Acrux

profits

earned in

the previous

years for

some

contingency

that may

arise in

future or for

future

unforseen

circumstanc

es

Total 43,

925.00

43,

889.00

Part ii:

The following is the desired analysis:

Adalta Acrux

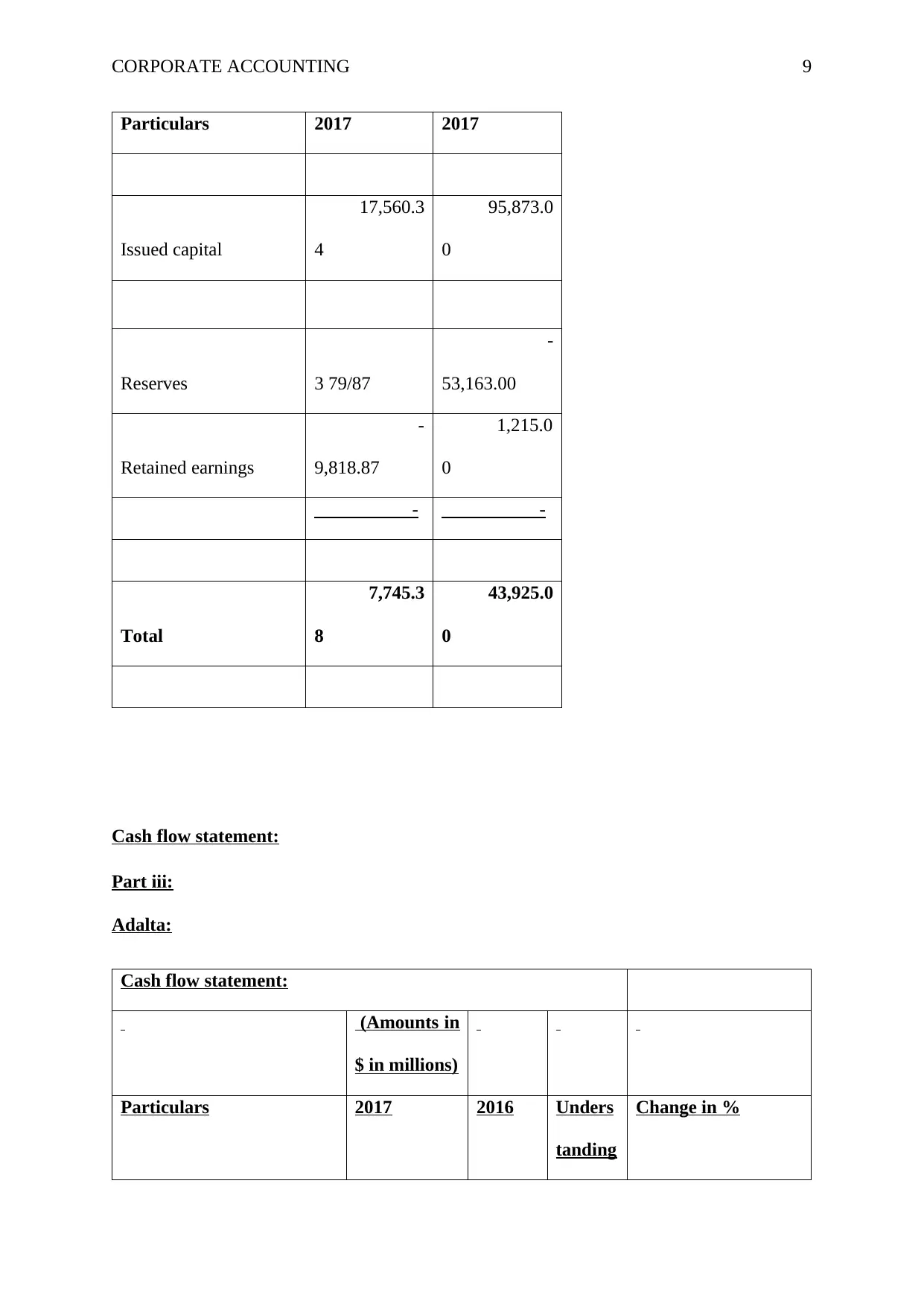

CORPORATE ACCOUNTING 9

Particulars 2017 2017

Issued capital

17,560.3

4

95,873.0

0

Reserves 3 79/87

-

53,163.00

Retained earnings

-

9,818.87

1,215.0

0

- -

Total

7,745.3

8

43,925.0

0

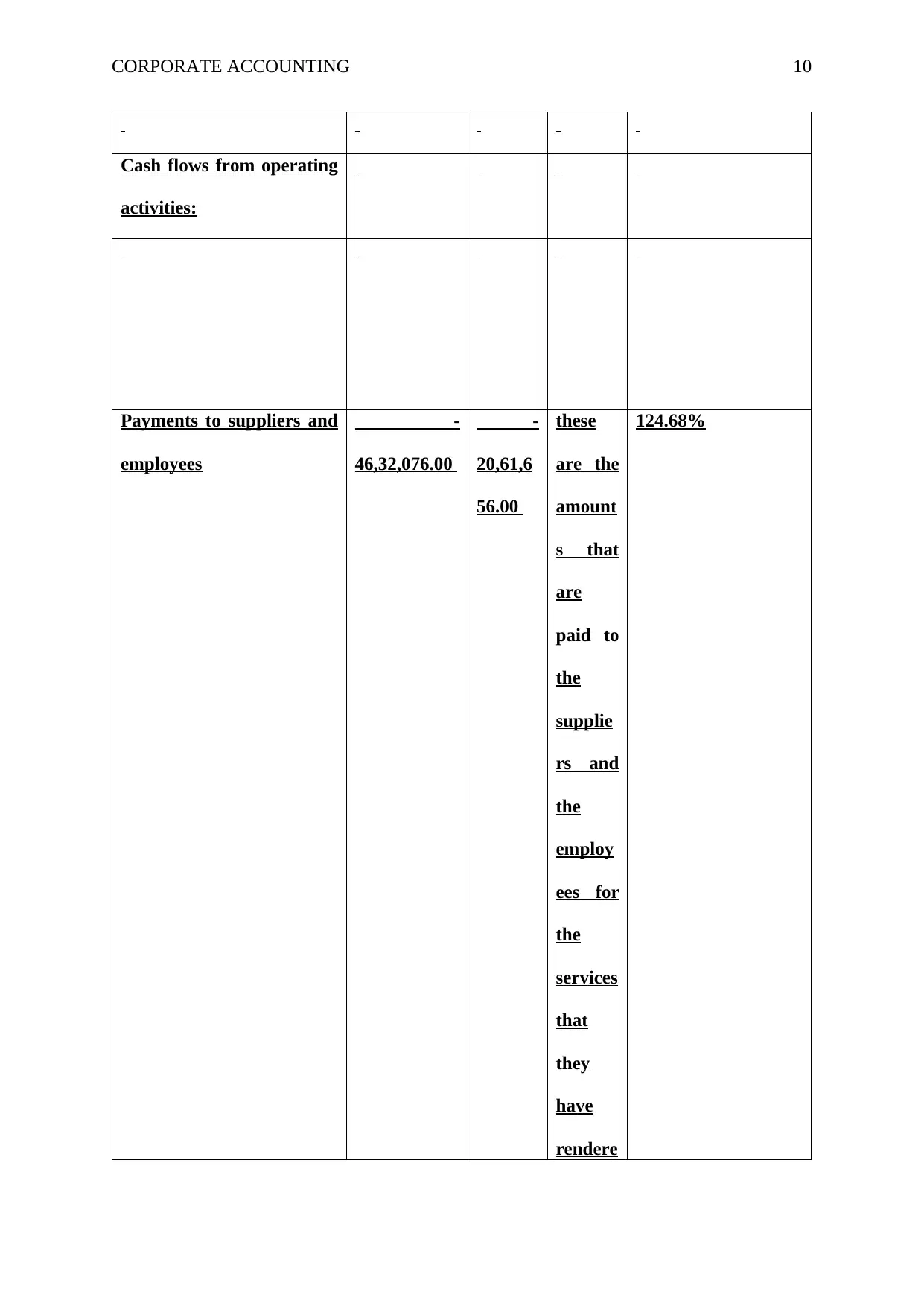

Cash flow statement:

Part iii:

Adalta:

Cash flow statement:

(Amounts in

$ in millions)

Particulars 2017 2016 Unders

tanding

Change in %

Particulars 2017 2017

Issued capital

17,560.3

4

95,873.0

0

Reserves 3 79/87

-

53,163.00

Retained earnings

-

9,818.87

1,215.0

0

- -

Total

7,745.3

8

43,925.0

0

Cash flow statement:

Part iii:

Adalta:

Cash flow statement:

(Amounts in

$ in millions)

Particulars 2017 2016 Unders

tanding

Change in %

CORPORATE ACCOUNTING 10

Cash flows from operating

activities:

Payments to suppliers and

employees

-

46,32,076.00

-

20,61,6

56.00

these

are the

amount

s that

are

paid to

the

supplie

rs and

the

employ

ees for

the

services

that

they

have

rendere

124.68%

Cash flows from operating

activities:

Payments to suppliers and

employees

-

46,32,076.00

-

20,61,6

56.00

these

are the

amount

s that

are

paid to

the

supplie

rs and

the

employ

ees for

the

services

that

they

have

rendere

124.68%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 11

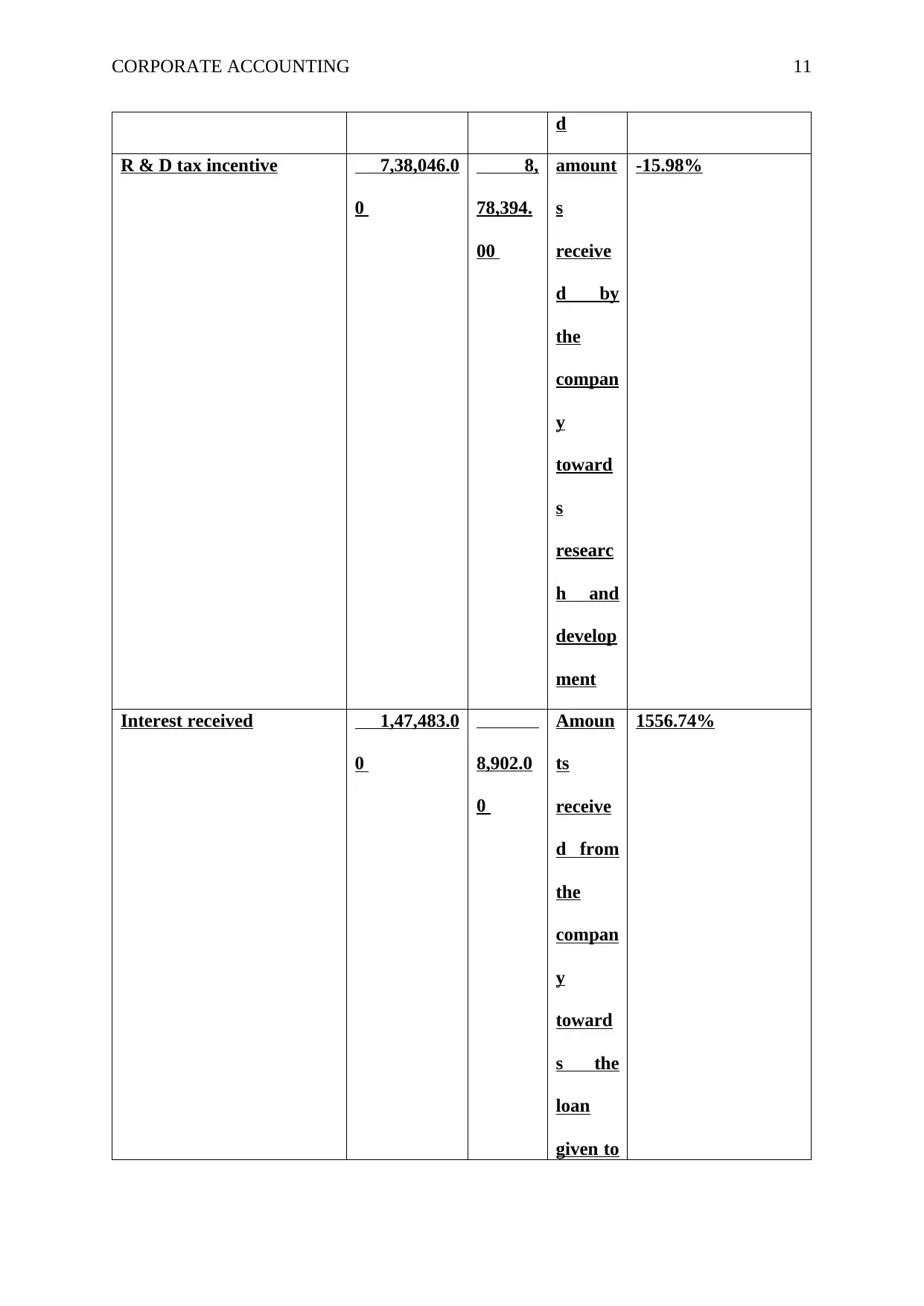

d

R & D tax incentive 7,38,046.0

0

8,

78,394.

00

amount

s

receive

d by

the

compan

y

toward

s

researc

h and

develop

ment

-15.98%

Interest received 1,47,483.0

0 8,902.0

0

Amoun

ts

receive

d from

the

compan

y

toward

s the

loan

given to

1556.74%

d

R & D tax incentive 7,38,046.0

0

8,

78,394.

00

amount

s

receive

d by

the

compan

y

toward

s

researc

h and

develop

ment

-15.98%

Interest received 1,47,483.0

0 8,902.0

0

Amoun

ts

receive

d from

the

compan

y

toward

s the

loan

given to

1556.74%

CORPORATE ACCOUNTING 12

the

outside

rs

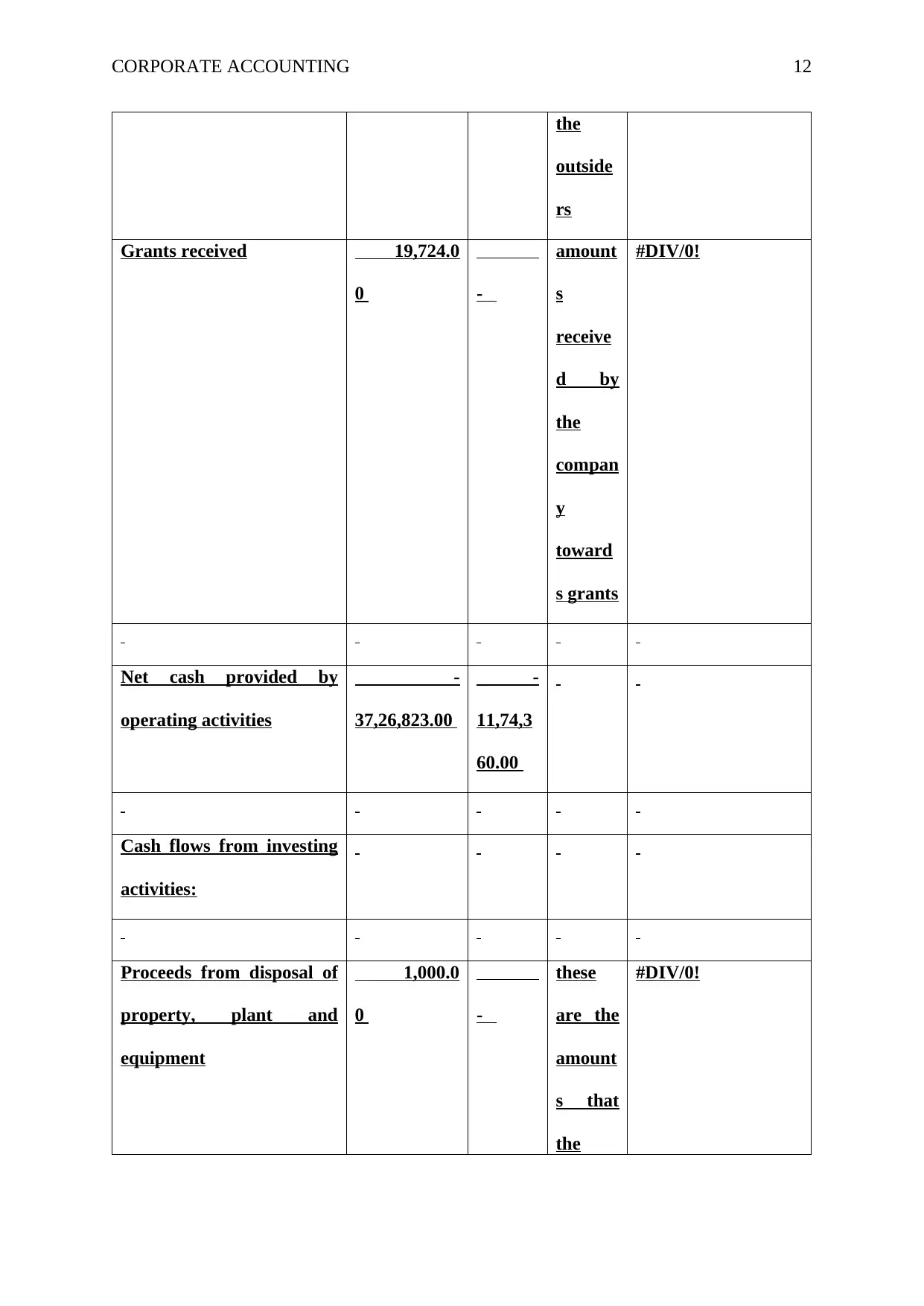

Grants received 19,724.0

0 -

amount

s

receive

d by

the

compan

y

toward

s grants

#DIV/0!

Net cash provided by

operating activities

-

37,26,823.00

-

11,74,3

60.00

Cash flows from investing

activities:

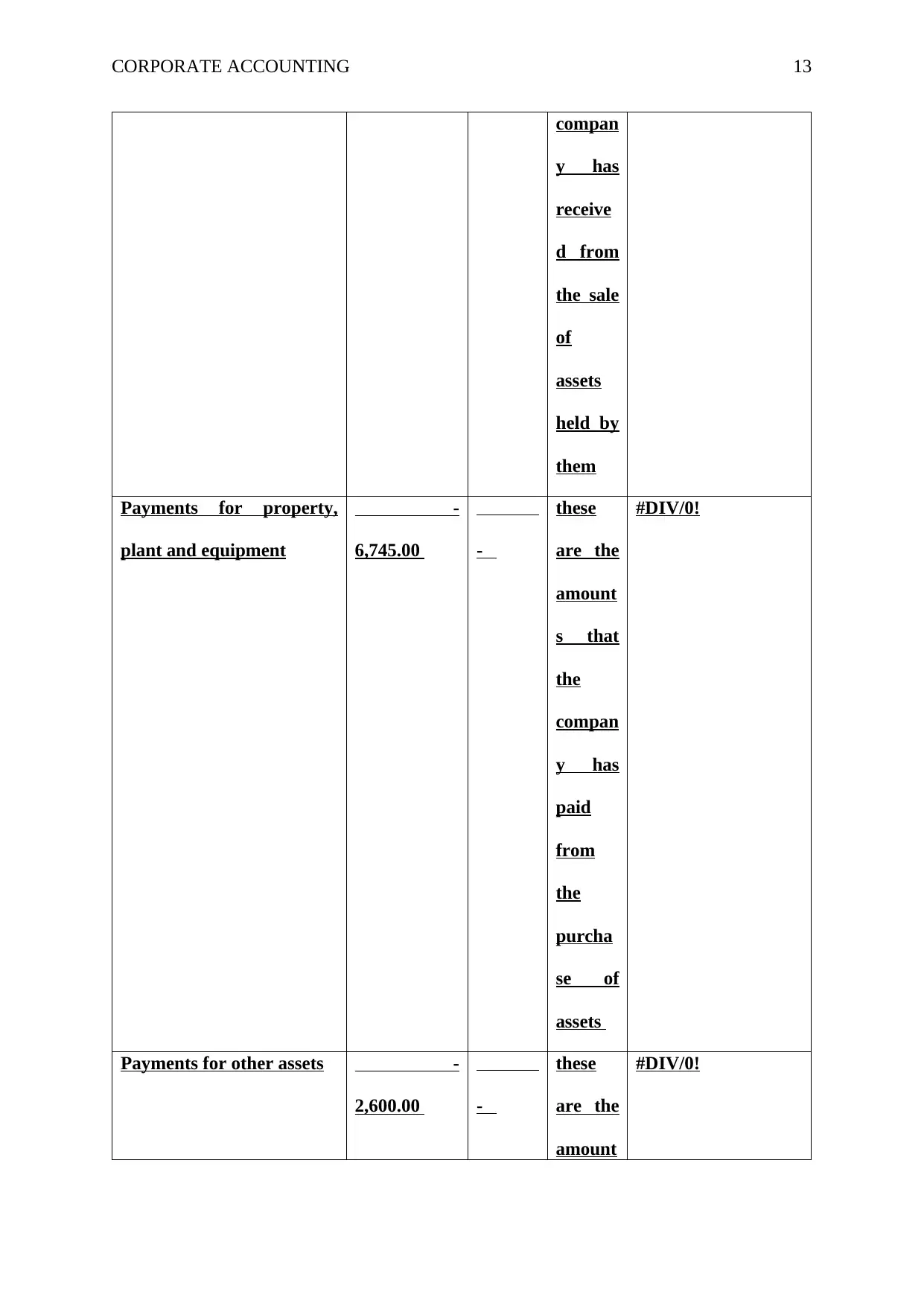

Proceeds from disposal of

property, plant and

equipment

1,000.0

0 -

these

are the

amount

s that

the

#DIV/0!

the

outside

rs

Grants received 19,724.0

0 -

amount

s

receive

d by

the

compan

y

toward

s grants

#DIV/0!

Net cash provided by

operating activities

-

37,26,823.00

-

11,74,3

60.00

Cash flows from investing

activities:

Proceeds from disposal of

property, plant and

equipment

1,000.0

0 -

these

are the

amount

s that

the

#DIV/0!

CORPORATE ACCOUNTING 13

compan

y has

receive

d from

the sale

of

assets

held by

them

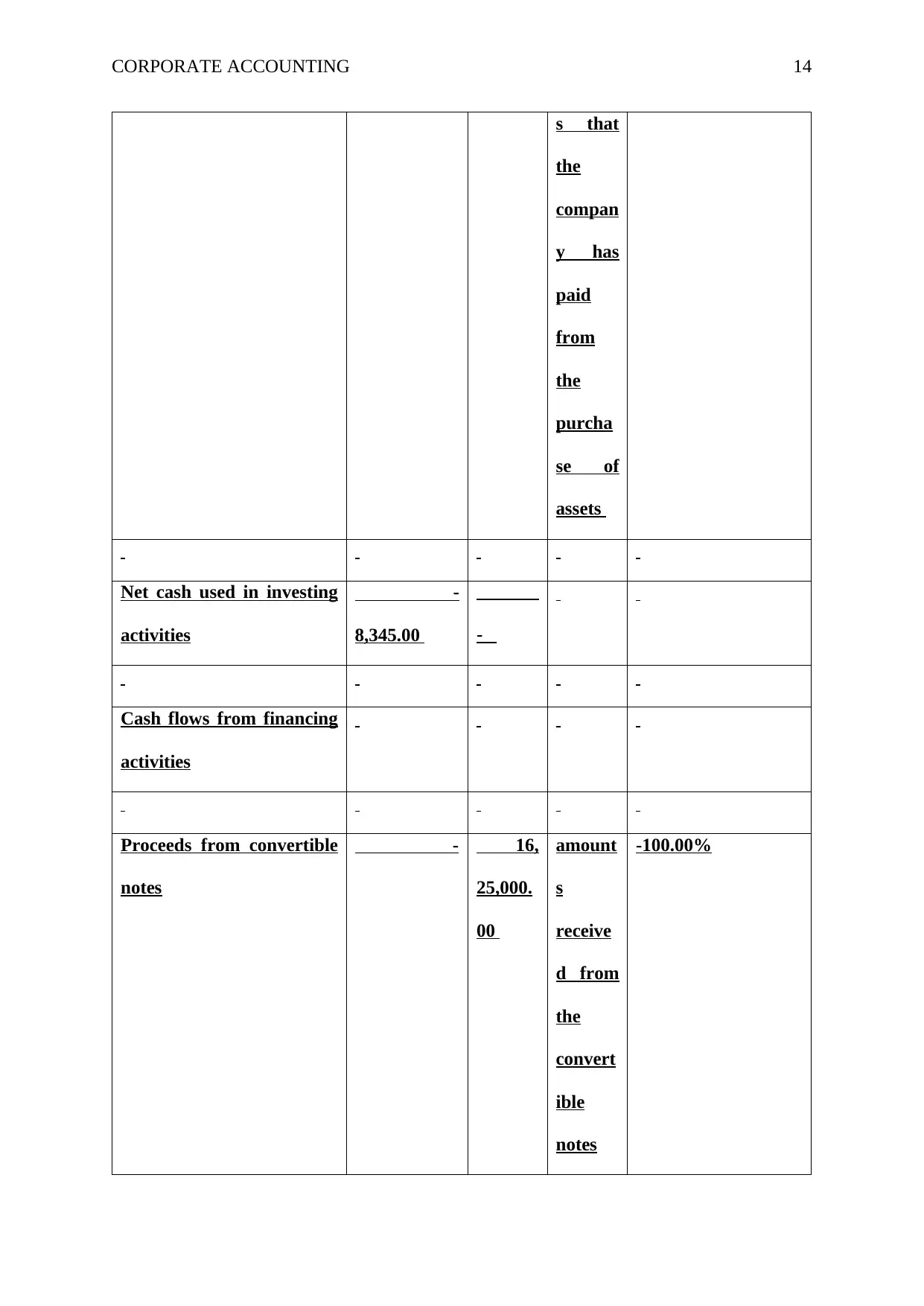

Payments for property,

plant and equipment

-

6,745.00 -

these

are the

amount

s that

the

compan

y has

paid

from

the

purcha

se of

assets

#DIV/0!

Payments for other assets -

2,600.00 -

these

are the

amount

#DIV/0!

compan

y has

receive

d from

the sale

of

assets

held by

them

Payments for property,

plant and equipment

-

6,745.00 -

these

are the

amount

s that

the

compan

y has

paid

from

the

purcha

se of

assets

#DIV/0!

Payments for other assets -

2,600.00 -

these

are the

amount

#DIV/0!

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING 14

s that

the

compan

y has

paid

from

the

purcha

se of

assets

Net cash used in investing

activities

-

8,345.00 -

Cash flows from financing

activities

Proceeds from convertible

notes

- 16,

25,000.

00

amount

s

receive

d from

the

convert

ible

notes

-100.00%

s that

the

compan

y has

paid

from

the

purcha

se of

assets

Net cash used in investing

activities

-

8,345.00 -

Cash flows from financing

activities

Proceeds from convertible

notes

- 16,

25,000.

00

amount

s

receive

d from

the

convert

ible

notes

-100.00%

CORPORATE ACCOUNTING 15

Proceeds from share

capital

100,00,000.0

0 54.00

amount

s

receive

d from

the

issue of

new

shares

of the

compan

y

18518418.52%

Proceeds from option

conversions

58,984.0

0 -

amount

s

receive

d from

the

issue of

new

options

of the

compan

y

#DIV/0!

Payment of share issue

costs

-

5,84,757.00 -

amount

s paid

toward

#DIV/0!

Proceeds from share

capital

100,00,000.0

0 54.00

amount

s

receive

d from

the

issue of

new

shares

of the

compan

y

18518418.52%

Proceeds from option

conversions

58,984.0

0 -

amount

s

receive

d from

the

issue of

new

options

of the

compan

y

#DIV/0!

Payment of share issue

costs

-

5,84,757.00 -

amount

s paid

toward

#DIV/0!

CORPORATE ACCOUNTING 16

s the

share

issue

costs

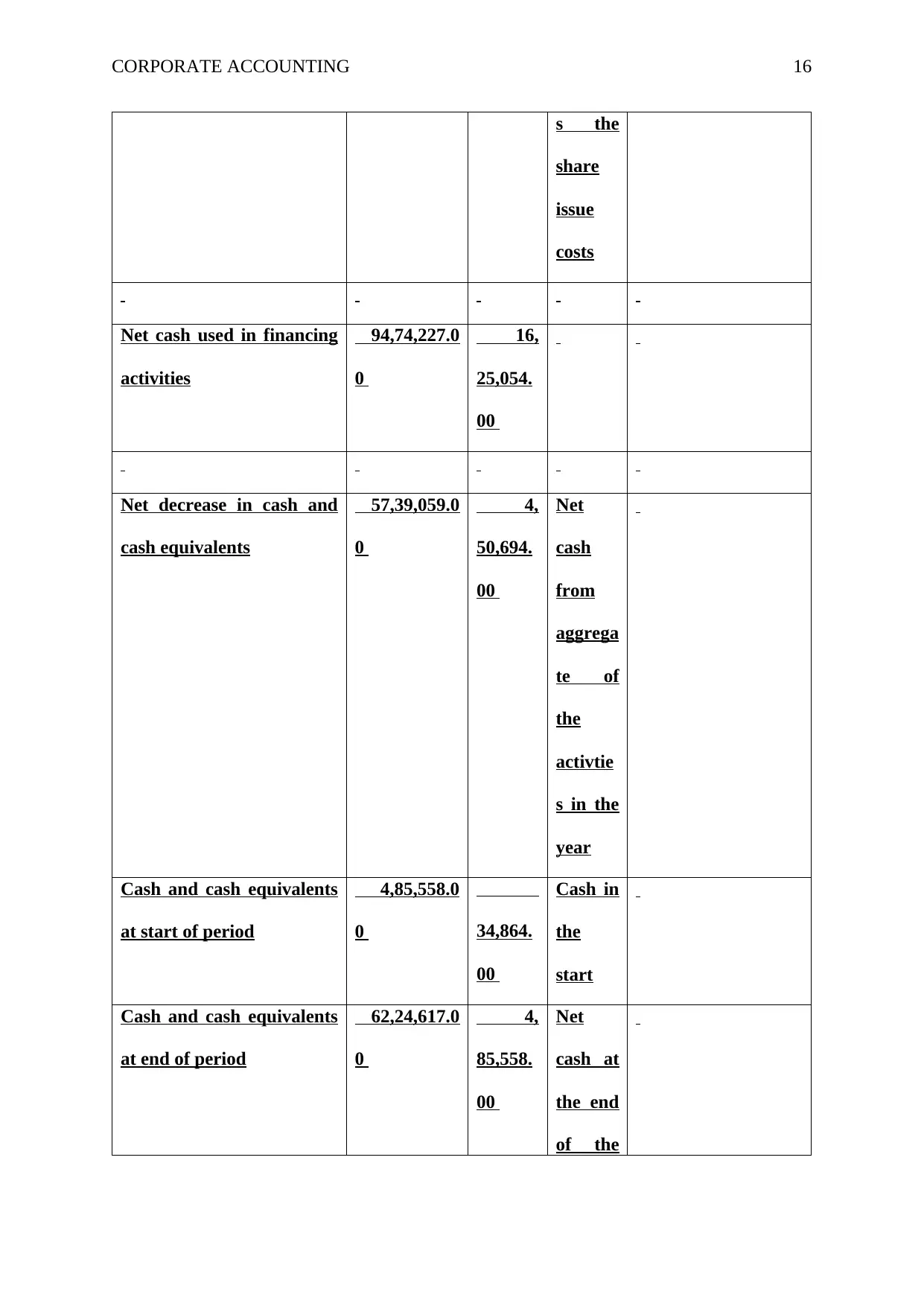

Net cash used in financing

activities

94,74,227.0

0

16,

25,054.

00

Net decrease in cash and

cash equivalents

57,39,059.0

0

4,

50,694.

00

Net

cash

from

aggrega

te of

the

activtie

s in the

year

Cash and cash equivalents

at start of period

4,85,558.0

0 34,864.

00

Cash in

the

start

Cash and cash equivalents

at end of period

62,24,617.0

0

4,

85,558.

00

Net

cash at

the end

of the

s the

share

issue

costs

Net cash used in financing

activities

94,74,227.0

0

16,

25,054.

00

Net decrease in cash and

cash equivalents

57,39,059.0

0

4,

50,694.

00

Net

cash

from

aggrega

te of

the

activtie

s in the

year

Cash and cash equivalents

at start of period

4,85,558.0

0 34,864.

00

Cash in

the

start

Cash and cash equivalents

at end of period

62,24,617.0

0

4,

85,558.

00

Net

cash at

the end

of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

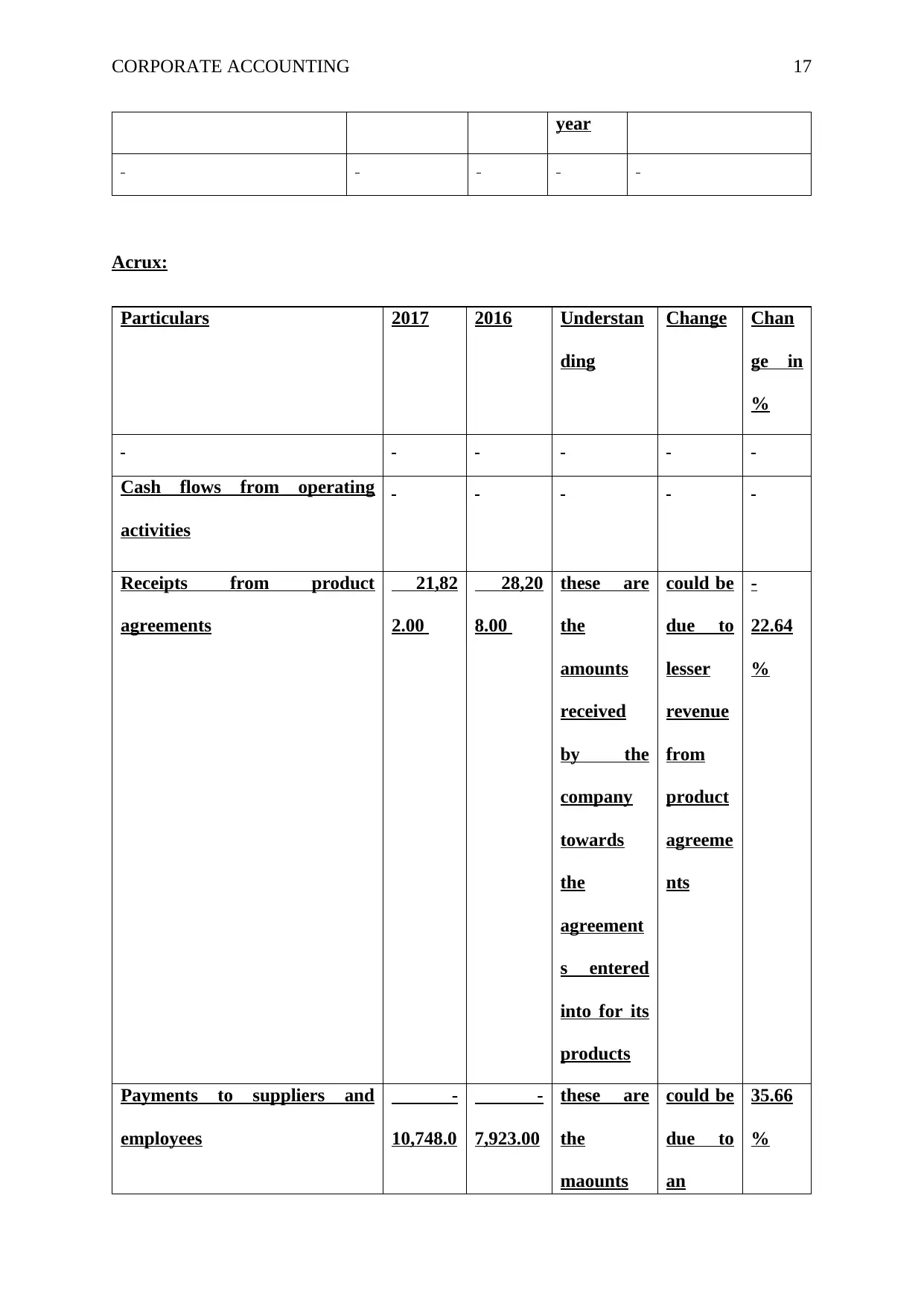

CORPORATE ACCOUNTING 17

year

Acrux:

Particulars 2017 2016 Understan

ding

Change Chan

ge in

%

Cash flows from operating

activities

Receipts from product

agreements

21,82

2.00

28,20

8.00

these are

the

amounts

received

by the

company

towards

the

agreement

s entered

into for its

products

could be

due to

lesser

revenue

from

product

agreeme

nts

-

22.64

%

Payments to suppliers and

employees

-

10,748.0

-

7,923.00

these are

the

maounts

could be

due to

an

35.66

%

year

Acrux:

Particulars 2017 2016 Understan

ding

Change Chan

ge in

%

Cash flows from operating

activities

Receipts from product

agreements

21,82

2.00

28,20

8.00

these are

the

amounts

received

by the

company

towards

the

agreement

s entered

into for its

products

could be

due to

lesser

revenue

from

product

agreeme

nts

-

22.64

%

Payments to suppliers and

employees

-

10,748.0

-

7,923.00

these are

the

maounts

could be

due to

an

35.66

%

CORPORATE ACCOUNTING 18

0 paid by the

company

towards

the

payments

to the

suppliers

and the

salaries of

the

employees

increase

in the

salaries

and

wages to

the

employe

rs and

more

purchas

es from

the

supplier

s

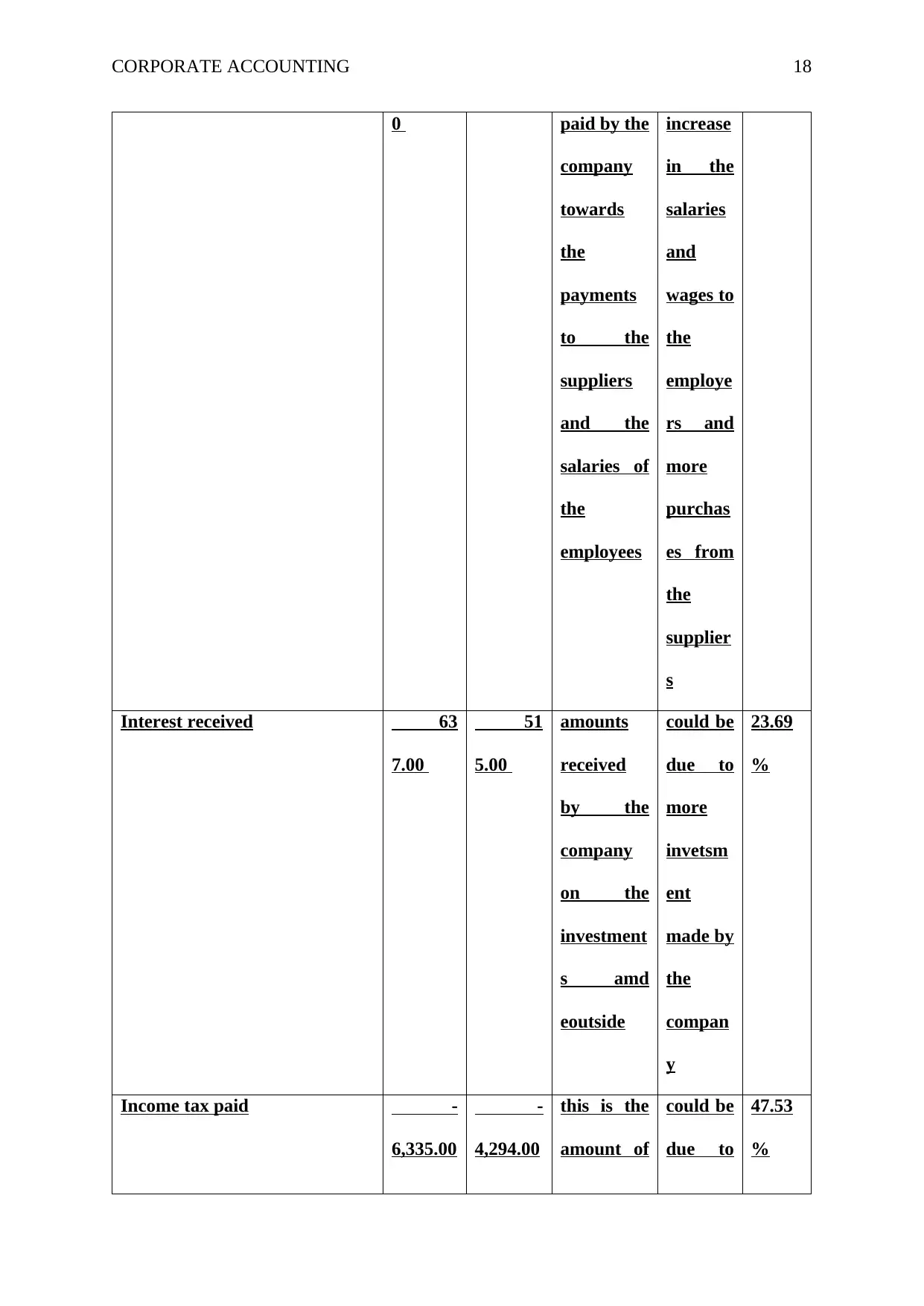

Interest received 63

7.00

51

5.00

amounts

received

by the

company

on the

investment

s amd

eoutside

could be

due to

more

invetsm

ent

made by

the

compan

y

23.69

%

Income tax paid -

6,335.00

-

4,294.00

this is the

amount of

could be

due to

47.53

%

0 paid by the

company

towards

the

payments

to the

suppliers

and the

salaries of

the

employees

increase

in the

salaries

and

wages to

the

employe

rs and

more

purchas

es from

the

supplier

s

Interest received 63

7.00

51

5.00

amounts

received

by the

company

on the

investment

s amd

eoutside

could be

due to

more

invetsm

ent

made by

the

compan

y

23.69

%

Income tax paid -

6,335.00

-

4,294.00

this is the

amount of

could be

due to

47.53

%

CORPORATE ACCOUNTING 19

money

paid by the

company

to Income

tax

authorities

for the

income

earned

during the

year

more

income

earned

during

the year

Net cash flows used in

operating activities

5,37

6.00

16,50

6.00

Cash flows from investing

activities

Payment for property, plant

and equipment

-

629.00

23

6.00

amounts

paid by the

company

towards

the

purchase

of

property,

could be

due to

addition

al

paymen

ts

towards

plant

-

366.53

%

money

paid by the

company

to Income

tax

authorities

for the

income

earned

during the

year

more

income

earned

during

the year

Net cash flows used in

operating activities

5,37

6.00

16,50

6.00

Cash flows from investing

activities

Payment for property, plant

and equipment

-

629.00

23

6.00

amounts

paid by the

company

towards

the

purchase

of

property,

could be

due to

addition

al

paymen

ts

towards

plant

-

366.53

%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

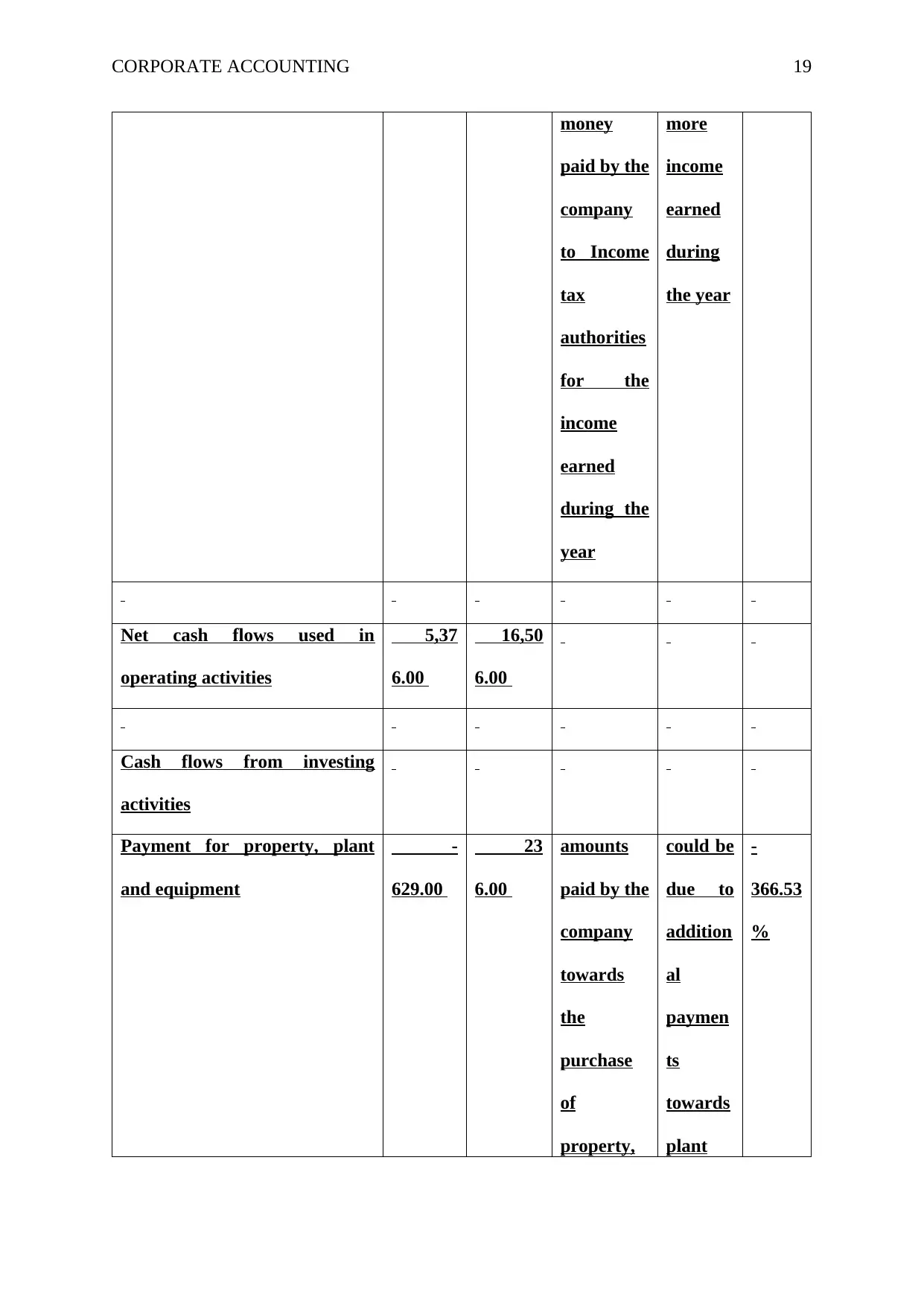

CORPORATE ACCOUNTING 20

plant and

equipment

purchas

e made

during

the year

Net cash flows used in investing

activities

-

629.00

23

6.00

Cash flows from financing

activities

Equity dividends paid

-

-

9,992.00

amounts of

dividends

paid to

shareholde

rs

Could

be due

to no

dividen

d paid

during

the

current

year

-

100.00

%

Net cash flows used in financing

activities -

-

9,992.00

Net decrease in cash and cash

equivalents

4,74

7.00

6,75

0.00

Net cash

from

plant and

equipment

purchas

e made

during

the year

Net cash flows used in investing

activities

-

629.00

23

6.00

Cash flows from financing

activities

Equity dividends paid

-

-

9,992.00

amounts of

dividends

paid to

shareholde

rs

Could

be due

to no

dividen

d paid

during

the

current

year

-

100.00

%

Net cash flows used in financing

activities -

-

9,992.00

Net decrease in cash and cash

equivalents

4,74

7.00

6,75

0.00

Net cash

from

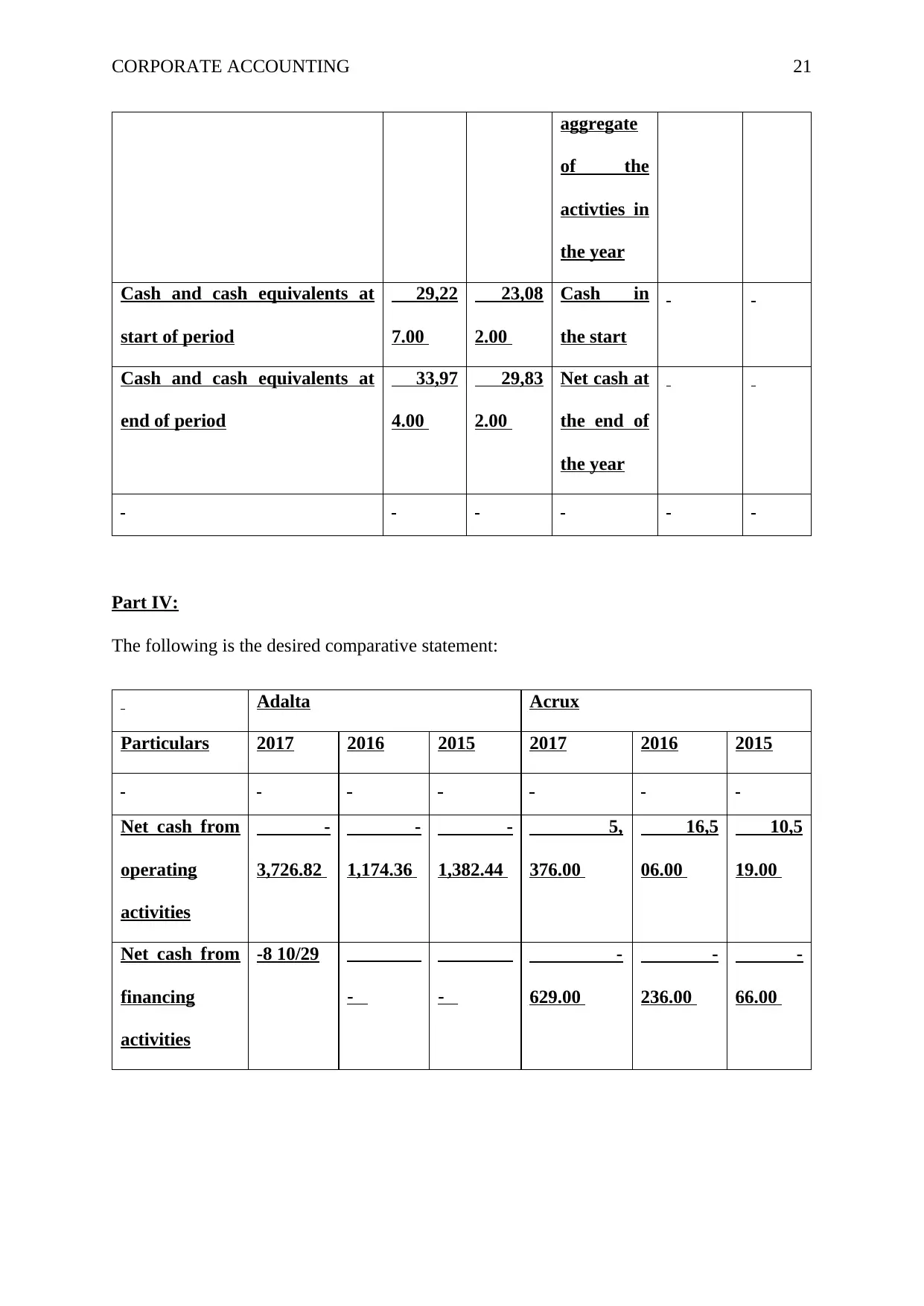

CORPORATE ACCOUNTING 21

aggregate

of the

activties in

the year

Cash and cash equivalents at

start of period

29,22

7.00

23,08

2.00

Cash in

the start

Cash and cash equivalents at

end of period

33,97

4.00

29,83

2.00

Net cash at

the end of

the year

Part IV:

The following is the desired comparative statement:

Adalta Acrux

Particulars 2017 2016 2015 2017 2016 2015

Net cash from

operating

activities

-

3,726.82

-

1,174.36

-

1,382.44

5,

376.00

16,5

06.00

10,5

19.00

Net cash from

financing

activities

-8 10/29

- -

-

629.00

-

236.00

-

66.00

aggregate

of the

activties in

the year

Cash and cash equivalents at

start of period

29,22

7.00

23,08

2.00

Cash in

the start

Cash and cash equivalents at

end of period

33,97

4.00

29,83

2.00

Net cash at

the end of

the year

Part IV:

The following is the desired comparative statement:

Adalta Acrux

Particulars 2017 2016 2015 2017 2016 2015

Net cash from

operating

activities

-

3,726.82

-

1,174.36

-

1,382.44

5,

376.00

16,5

06.00

10,5

19.00

Net cash from

financing

activities

-8 10/29

- -

-

629.00

-

236.00

-

66.00

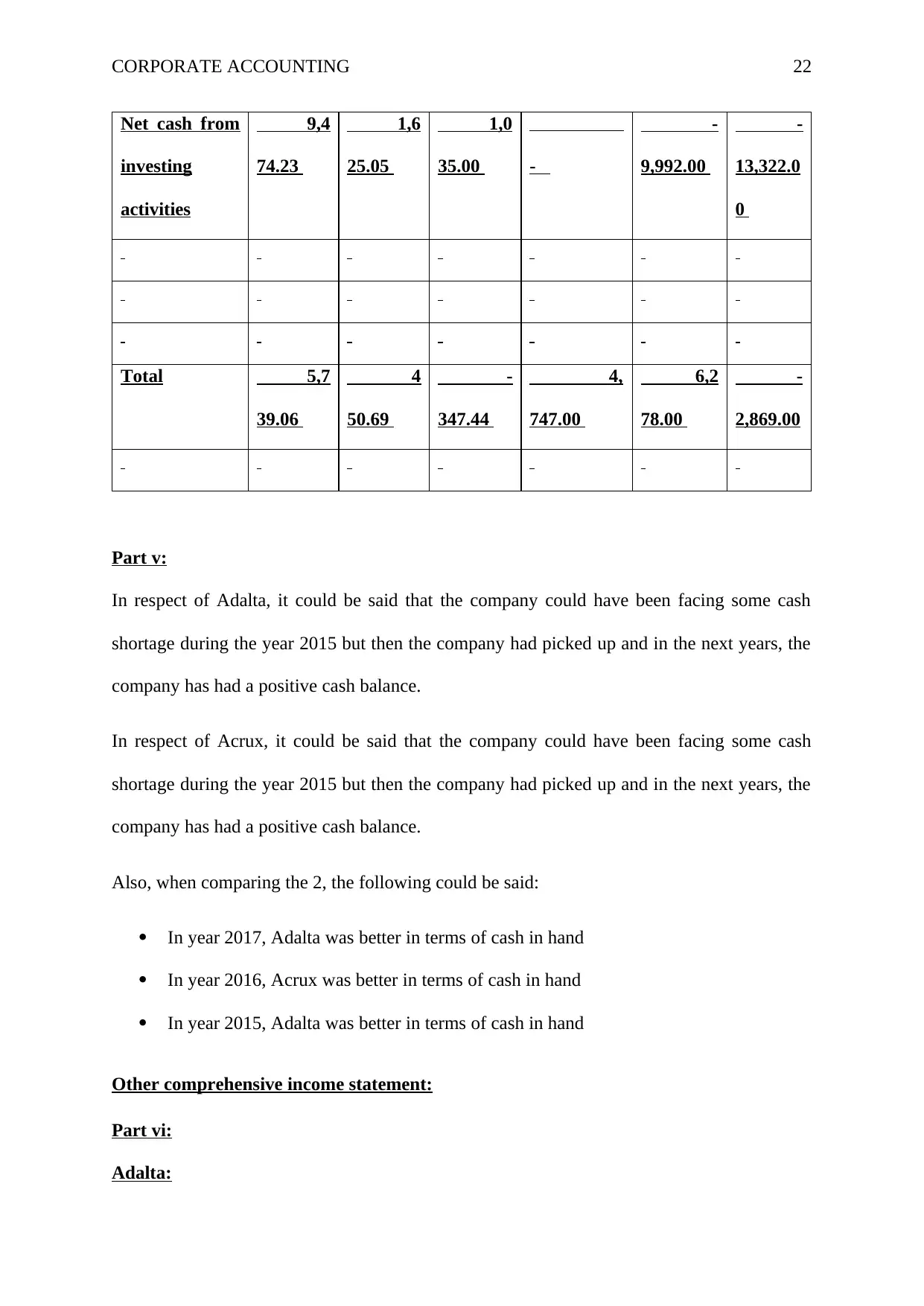

CORPORATE ACCOUNTING 22

Net cash from

investing

activities

9,4

74.23

1,6

25.05

1,0

35.00 -

-

9,992.00

-

13,322.0

0

Total 5,7

39.06

4

50.69

-

347.44

4,

747.00

6,2

78.00

-

2,869.00

Part v:

In respect of Adalta, it could be said that the company could have been facing some cash

shortage during the year 2015 but then the company had picked up and in the next years, the

company has had a positive cash balance.

In respect of Acrux, it could be said that the company could have been facing some cash

shortage during the year 2015 but then the company had picked up and in the next years, the

company has had a positive cash balance.

Also, when comparing the 2, the following could be said:

In year 2017, Adalta was better in terms of cash in hand

In year 2016, Acrux was better in terms of cash in hand

In year 2015, Adalta was better in terms of cash in hand

Other comprehensive income statement:

Part vi:

Adalta:

Net cash from

investing

activities

9,4

74.23

1,6

25.05

1,0

35.00 -

-

9,992.00

-

13,322.0

0

Total 5,7

39.06

4

50.69

-

347.44

4,

747.00

6,2

78.00

-

2,869.00

Part v:

In respect of Adalta, it could be said that the company could have been facing some cash

shortage during the year 2015 but then the company had picked up and in the next years, the

company has had a positive cash balance.

In respect of Acrux, it could be said that the company could have been facing some cash

shortage during the year 2015 but then the company had picked up and in the next years, the

company has had a positive cash balance.

Also, when comparing the 2, the following could be said:

In year 2017, Adalta was better in terms of cash in hand

In year 2016, Acrux was better in terms of cash in hand

In year 2015, Adalta was better in terms of cash in hand

Other comprehensive income statement:

Part vi:

Adalta:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

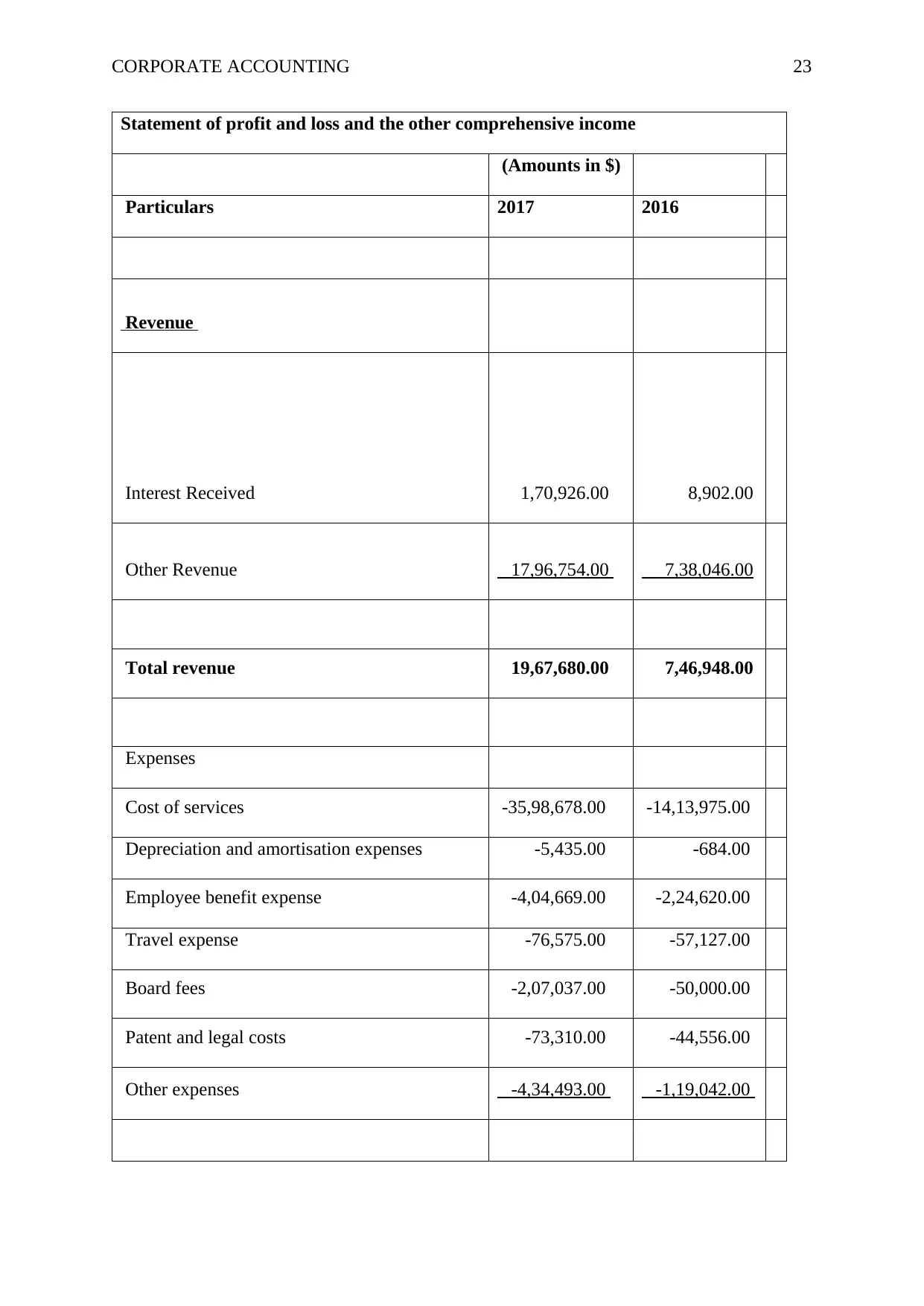

CORPORATE ACCOUNTING 23

Statement of profit and loss and the other comprehensive income

(Amounts in $)

Particulars 2017 2016

Revenue

Interest Received 1,70,926.00 8,902.00

Other Revenue 17,96,754.00 7,38,046.00

Total revenue 19,67,680.00 7,46,948.00

Expenses

Cost of services -35,98,678.00 -14,13,975.00

Depreciation and amortisation expenses -5,435.00 -684.00

Employee benefit expense -4,04,669.00 -2,24,620.00

Travel expense -76,575.00 -57,127.00

Board fees -2,07,037.00 -50,000.00

Patent and legal costs -73,310.00 -44,556.00

Other expenses -4,34,493.00 -1,19,042.00

Statement of profit and loss and the other comprehensive income

(Amounts in $)

Particulars 2017 2016

Revenue

Interest Received 1,70,926.00 8,902.00

Other Revenue 17,96,754.00 7,38,046.00

Total revenue 19,67,680.00 7,46,948.00

Expenses

Cost of services -35,98,678.00 -14,13,975.00

Depreciation and amortisation expenses -5,435.00 -684.00

Employee benefit expense -4,04,669.00 -2,24,620.00

Travel expense -76,575.00 -57,127.00

Board fees -2,07,037.00 -50,000.00

Patent and legal costs -73,310.00 -44,556.00

Other expenses -4,34,493.00 -1,19,042.00

CORPORATE ACCOUNTING 24

Profit (loss) before income tax -28,32,517.00 -11,63,056.00

Tax expense - -

Profit (loss) for the year -28,32,517.00 -11,63,056.00

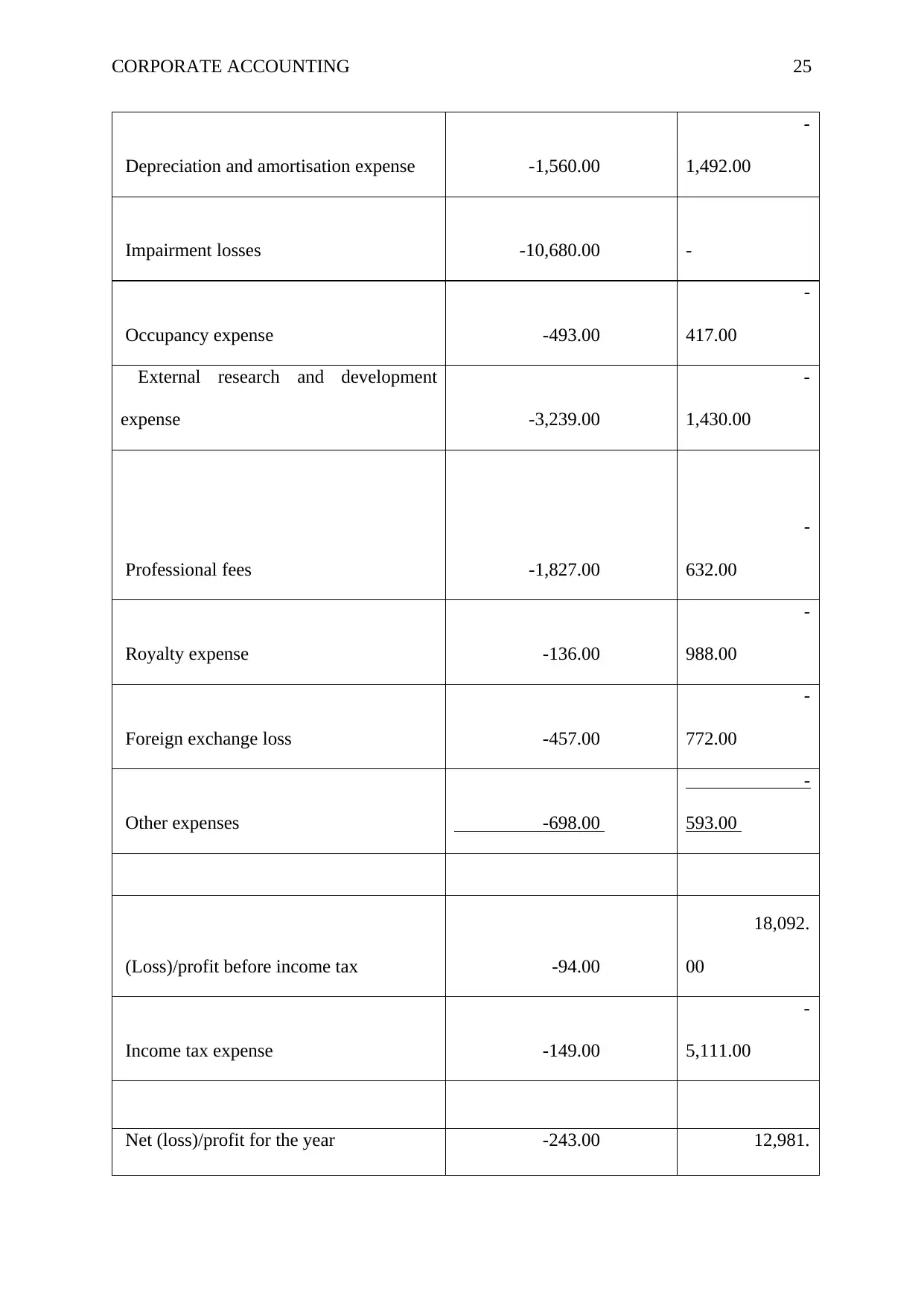

Acrux:

Statement of comprehensive income

(Amounts in $ in

thousands)

Particulars 2017 2016

Revenue 23,934.00

28,557.

00

Employee benefits expense -4,277.00

-

3,582.00

Directors’ fees -382.00

-

284.00

Share options expense -279.00

-

275.00

Profit (loss) before income tax -28,32,517.00 -11,63,056.00

Tax expense - -

Profit (loss) for the year -28,32,517.00 -11,63,056.00

Acrux:

Statement of comprehensive income

(Amounts in $ in

thousands)

Particulars 2017 2016

Revenue 23,934.00

28,557.

00

Employee benefits expense -4,277.00

-

3,582.00

Directors’ fees -382.00

-

284.00

Share options expense -279.00

-

275.00

CORPORATE ACCOUNTING 25

Depreciation and amortisation expense -1,560.00

-

1,492.00

Impairment losses -10,680.00 -

Occupancy expense -493.00

-

417.00

External research and development

expense -3,239.00

-

1,430.00

Professional fees -1,827.00

-

632.00

Royalty expense -136.00

-

988.00

Foreign exchange loss -457.00

-

772.00

Other expenses -698.00

-

593.00

(Loss)/profit before income tax -94.00

18,092.

00

Income tax expense -149.00

-

5,111.00

Net (loss)/profit for the year -243.00 12,981.

Depreciation and amortisation expense -1,560.00

-

1,492.00

Impairment losses -10,680.00 -

Occupancy expense -493.00

-

417.00

External research and development

expense -3,239.00

-

1,430.00

Professional fees -1,827.00

-

632.00

Royalty expense -136.00

-

988.00

Foreign exchange loss -457.00

-

772.00

Other expenses -698.00

-

593.00

(Loss)/profit before income tax -94.00

18,092.

00

Income tax expense -149.00

-

5,111.00

Net (loss)/profit for the year -243.00 12,981.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING 26

00

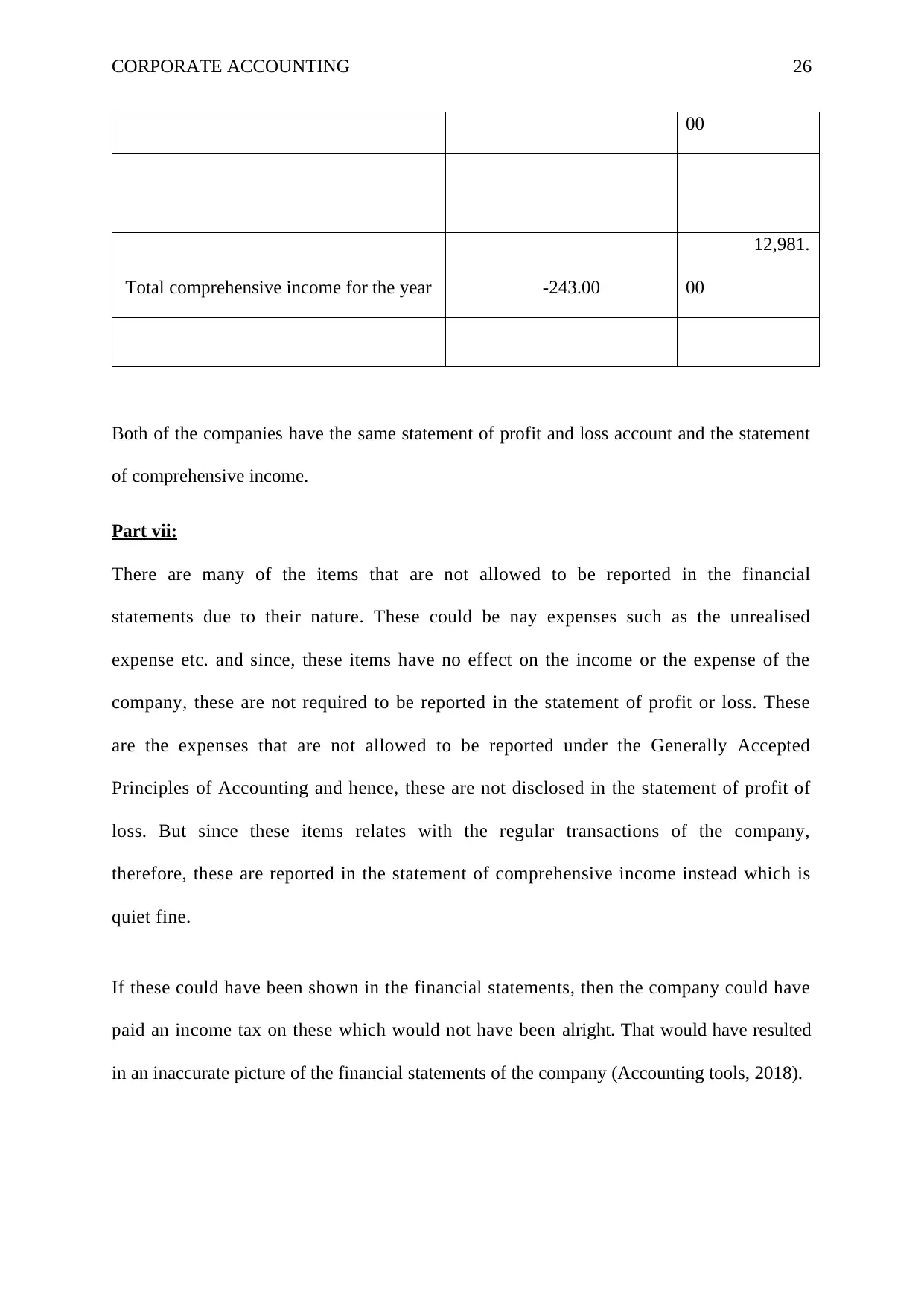

Total comprehensive income for the year -243.00

12,981.

00

Both of the companies have the same statement of profit and loss account and the statement

of comprehensive income.

Part vii:

There are many of the items that are not allowed to be reported in the financial

statements due to their nature. These could be nay expenses such as the unrealised

expense etc. and since, these items have no effect on the income or the expense of the

company, these are not required to be reported in the statement of profit or loss. These

are the expenses that are not allowed to be reported under the Generally Accepted

Principles of Accounting and hence, these are not disclosed in the statement of profit of

loss. But since these items relates with the regular transactions of the company,

therefore, these are reported in the statement of comprehensive income instead which is

quiet fine.

If these could have been shown in the financial statements, then the company could have

paid an income tax on these which would not have been alright. That would have resulted

in an inaccurate picture of the financial statements of the company (Accounting tools, 2018).

00

Total comprehensive income for the year -243.00

12,981.

00

Both of the companies have the same statement of profit and loss account and the statement

of comprehensive income.

Part vii:

There are many of the items that are not allowed to be reported in the financial

statements due to their nature. These could be nay expenses such as the unrealised

expense etc. and since, these items have no effect on the income or the expense of the

company, these are not required to be reported in the statement of profit or loss. These

are the expenses that are not allowed to be reported under the Generally Accepted

Principles of Accounting and hence, these are not disclosed in the statement of profit of

loss. But since these items relates with the regular transactions of the company,

therefore, these are reported in the statement of comprehensive income instead which is

quiet fine.

If these could have been shown in the financial statements, then the company could have

paid an income tax on these which would not have been alright. That would have resulted

in an inaccurate picture of the financial statements of the company (Accounting tools, 2018).

CORPORATE ACCOUNTING 27

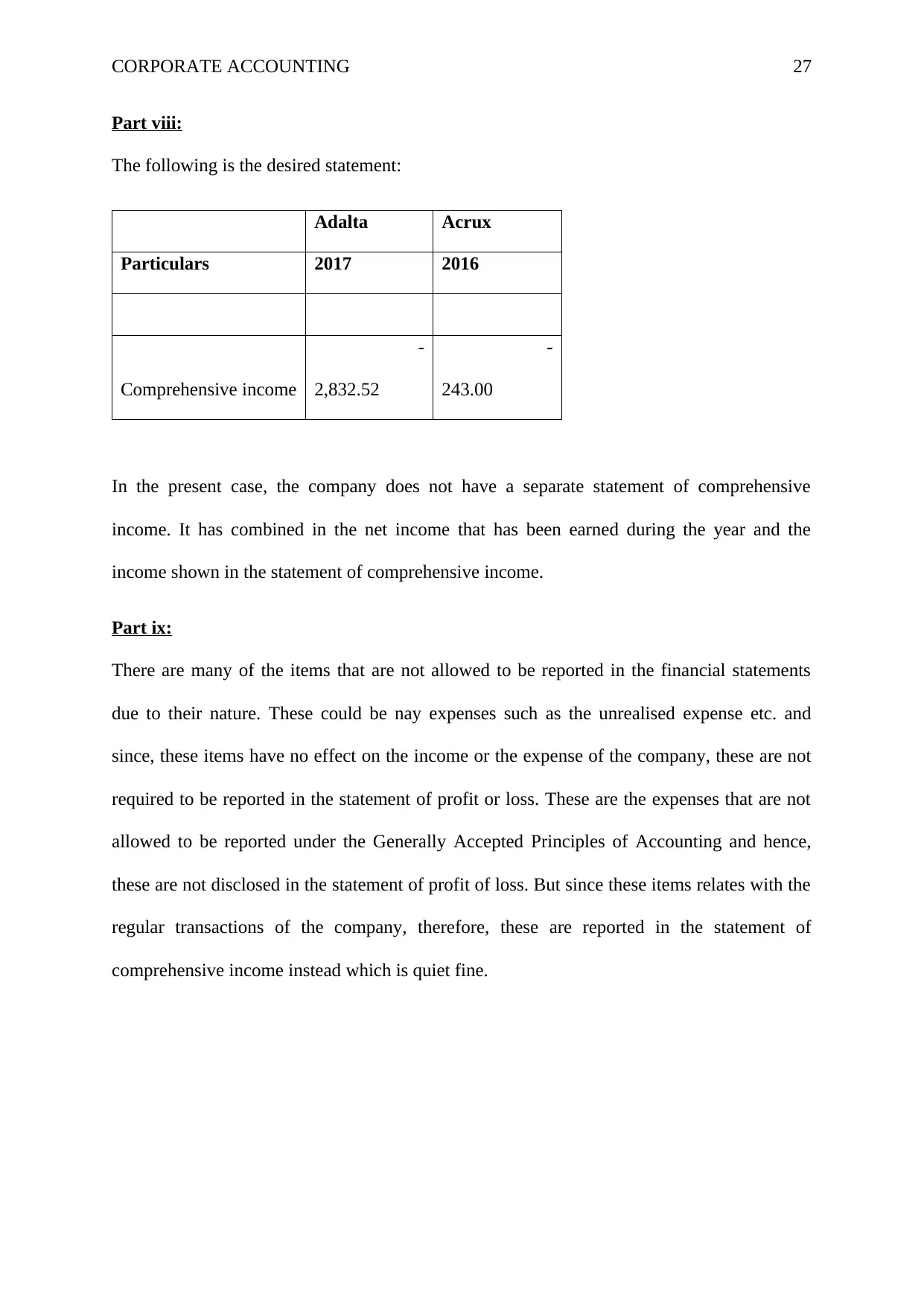

Part viii:

The following is the desired statement:

Adalta Acrux

Particulars 2017 2016

Comprehensive income

-

2,832.52

-

243.00

In the present case, the company does not have a separate statement of comprehensive

income. It has combined in the net income that has been earned during the year and the

income shown in the statement of comprehensive income.

Part ix:

There are many of the items that are not allowed to be reported in the financial statements

due to their nature. These could be nay expenses such as the unrealised expense etc. and

since, these items have no effect on the income or the expense of the company, these are not

required to be reported in the statement of profit or loss. These are the expenses that are not

allowed to be reported under the Generally Accepted Principles of Accounting and hence,

these are not disclosed in the statement of profit of loss. But since these items relates with the

regular transactions of the company, therefore, these are reported in the statement of

comprehensive income instead which is quiet fine.

Part viii:

The following is the desired statement:

Adalta Acrux

Particulars 2017 2016

Comprehensive income

-

2,832.52

-

243.00

In the present case, the company does not have a separate statement of comprehensive

income. It has combined in the net income that has been earned during the year and the

income shown in the statement of comprehensive income.

Part ix:

There are many of the items that are not allowed to be reported in the financial statements

due to their nature. These could be nay expenses such as the unrealised expense etc. and

since, these items have no effect on the income or the expense of the company, these are not

required to be reported in the statement of profit or loss. These are the expenses that are not

allowed to be reported under the Generally Accepted Principles of Accounting and hence,

these are not disclosed in the statement of profit of loss. But since these items relates with the

regular transactions of the company, therefore, these are reported in the statement of

comprehensive income instead which is quiet fine.

CORPORATE ACCOUNTING 28

If these could have been shown in the financial statements, then the company could have paid

an income tax on these which would not have been alright. That would have resulted in an

inaccurate picture of the financial statements of the company

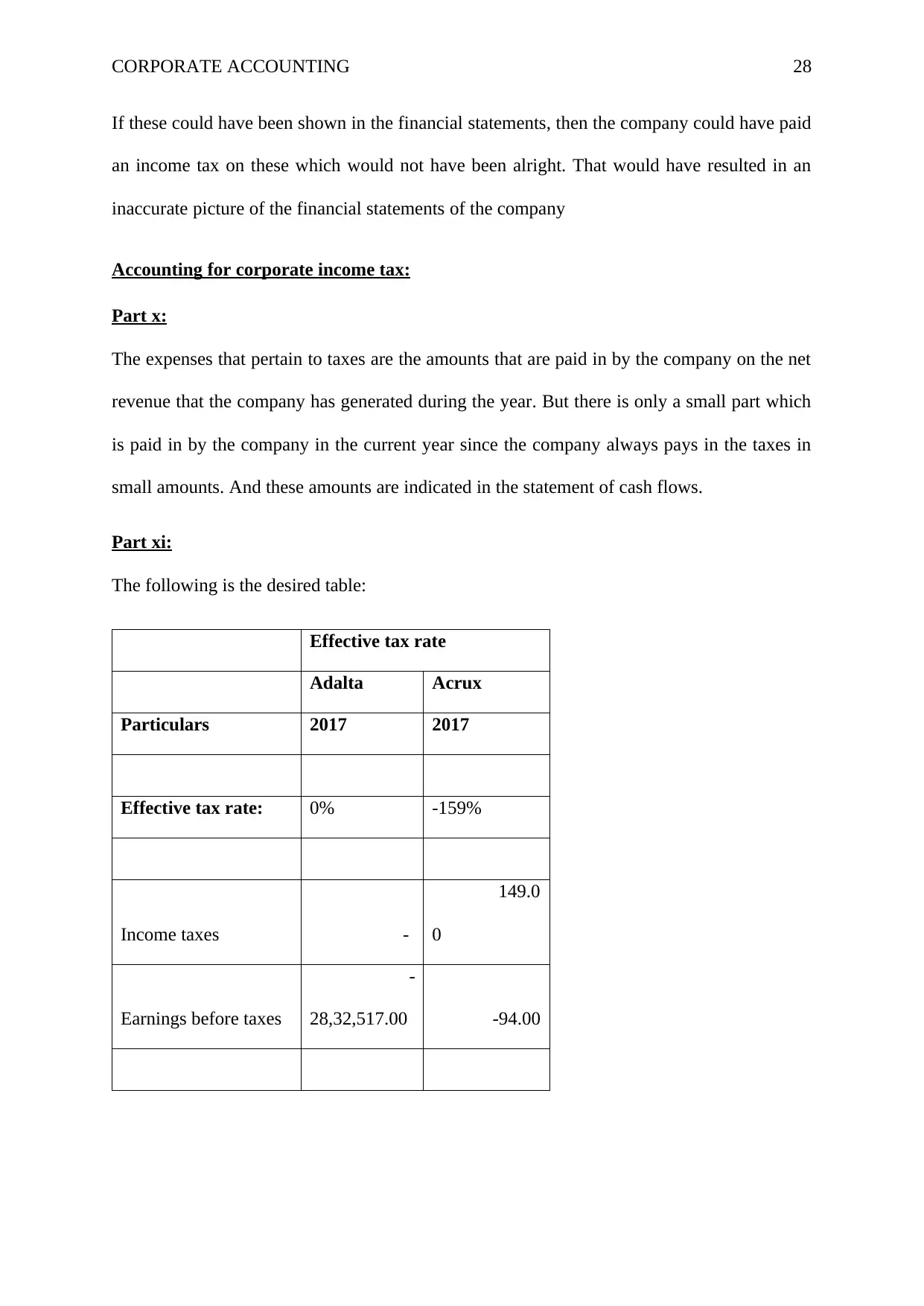

Accounting for corporate income tax:

Part x:

The expenses that pertain to taxes are the amounts that are paid in by the company on the net

revenue that the company has generated during the year. But there is only a small part which

is paid in by the company in the current year since the company always pays in the taxes in

small amounts. And these amounts are indicated in the statement of cash flows.

Part xi:

The following is the desired table:

Effective tax rate

Adalta Acrux

Particulars 2017 2017

Effective tax rate: 0% -159%

Income taxes -

149.0

0

Earnings before taxes

-

28,32,517.00 -94.00

If these could have been shown in the financial statements, then the company could have paid

an income tax on these which would not have been alright. That would have resulted in an

inaccurate picture of the financial statements of the company

Accounting for corporate income tax:

Part x:

The expenses that pertain to taxes are the amounts that are paid in by the company on the net

revenue that the company has generated during the year. But there is only a small part which

is paid in by the company in the current year since the company always pays in the taxes in

small amounts. And these amounts are indicated in the statement of cash flows.

Part xi:

The following is the desired table:

Effective tax rate

Adalta Acrux

Particulars 2017 2017

Effective tax rate: 0% -159%

Income taxes -

149.0

0

Earnings before taxes

-

28,32,517.00 -94.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 29

Both of the companies have reported a loss during the year and hence, the effective rate of the

income tax is in negative.

Part xii:

There are few of the expenses that are not allowed to be reported in the income statement due

to their timing difference. The timing difference arises due to the taxation rules and

regulations. There are some cases when the company did not pay the amount within some

specified date and as the result, the company could not deduct that expense in that year and

so, it can now claim the deduction of the expense in the next year. In such cases, though the

expense is deductible but only in the next year (Taxman, 2018).

Part xiii:

There are few of the expenses that are not allowed to be reported in the income statement due

to their timing difference. The timing difference arises due to the taxation rules and

regulations. There are some cases when the company did not pay the amount within some

specified date and as the result, the company could not deduct that expense in that year and

so, it can now claim the deduction of the expense in the next year. In such cases, though the

expense is deductible but only in the next year. Hence, these are the cases that serve as the

assets for the company.

In respect of Adalta, there has been no deferred tax assets or no deferred tax liabilities.

In respect of Acrux, there has been an increase in the amounts of the deferred tax assets and

the company has no deferred tax liabilities..

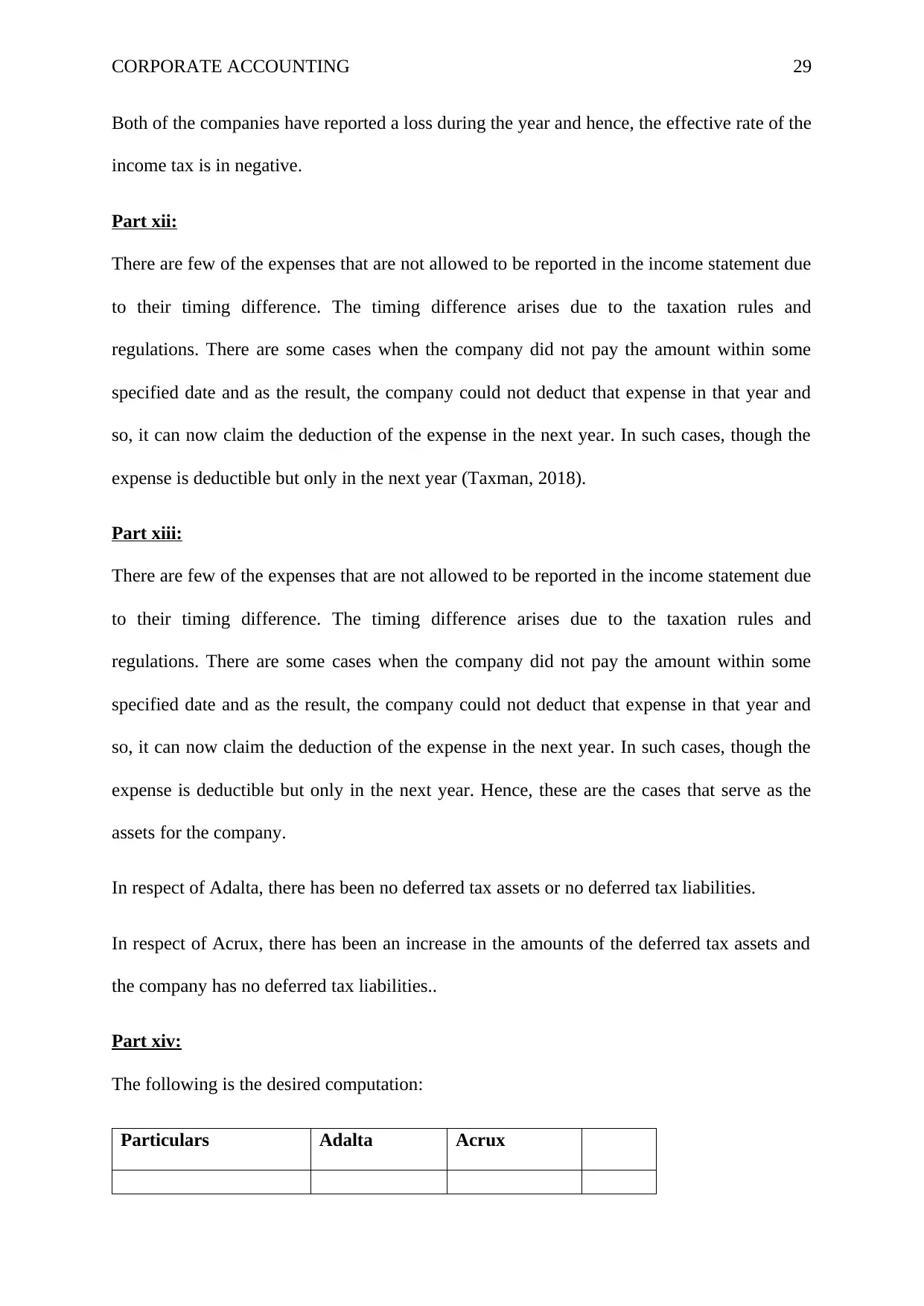

Part xiv:

The following is the desired computation:

Particulars Adalta Acrux

Both of the companies have reported a loss during the year and hence, the effective rate of the

income tax is in negative.

Part xii:

There are few of the expenses that are not allowed to be reported in the income statement due

to their timing difference. The timing difference arises due to the taxation rules and

regulations. There are some cases when the company did not pay the amount within some

specified date and as the result, the company could not deduct that expense in that year and

so, it can now claim the deduction of the expense in the next year. In such cases, though the

expense is deductible but only in the next year (Taxman, 2018).

Part xiii:

There are few of the expenses that are not allowed to be reported in the income statement due

to their timing difference. The timing difference arises due to the taxation rules and

regulations. There are some cases when the company did not pay the amount within some

specified date and as the result, the company could not deduct that expense in that year and

so, it can now claim the deduction of the expense in the next year. In such cases, though the

expense is deductible but only in the next year. Hence, these are the cases that serve as the

assets for the company.

In respect of Adalta, there has been no deferred tax assets or no deferred tax liabilities.

In respect of Acrux, there has been an increase in the amounts of the deferred tax assets and

the company has no deferred tax liabilities..

Part xiv:

The following is the desired computation:

Particulars Adalta Acrux

CORPORATE ACCOUNTING 30

Net income

-

28,32,517.00

-

243.00

Less: deferred tax assets -

92.0

0

Income on which taxes

would have been paid

-

28,32,517.00

-

335.00

Part xv:

Both of these companies have a loss and so, the cash effective tax rate would not be possible.

Particulars Adalta Acrux

Income tax

provision - -

Increase in deferred

tax assets -

92.0

0

Current income

taxes -

92.0

0

Other income

17,96,754.0

0 -

Taxes paid on other - -

Net income

-

28,32,517.00

-

243.00

Less: deferred tax assets -

92.0

0

Income on which taxes

would have been paid

-

28,32,517.00

-

335.00

Part xv:

Both of these companies have a loss and so, the cash effective tax rate would not be possible.

Particulars Adalta Acrux

Income tax

provision - -

Increase in deferred

tax assets -

92.0

0

Current income

taxes -

92.0

0

Other income

17,96,754.0

0 -

Taxes paid on other - -

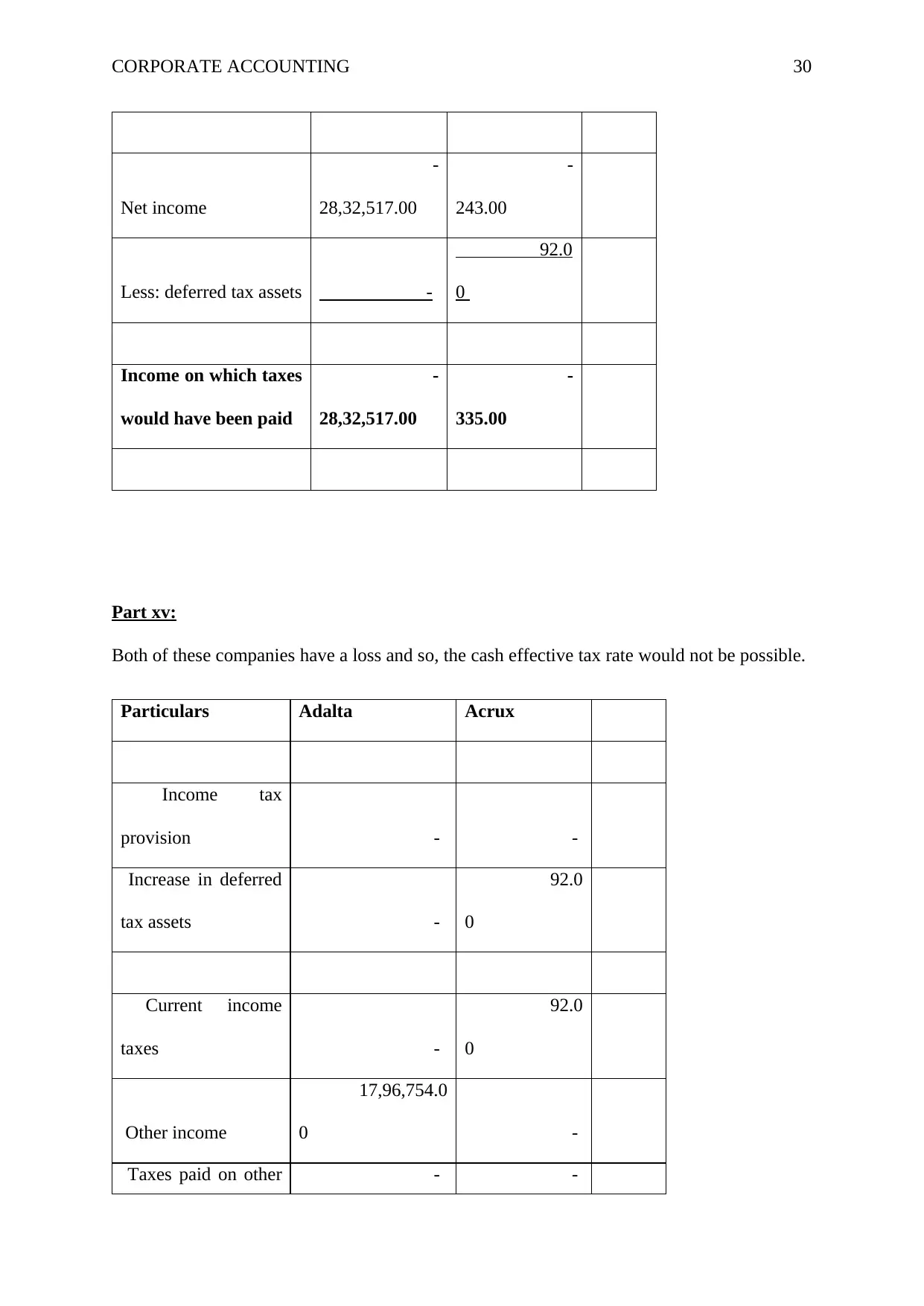

CORPORATE ACCOUNTING 31

income

Unlevered cash

taxes -

92.0

0

EBITA

-

28,32,517.00

-

243.00

Cash tax rate 0.00% -37.86%

Part xvi:

The cash tax rate is always different from the amount of the taxes that are paid in by the

company. The company usually as a general practise follows the rule of paying off the taxes

that pertains to the previous year and records the tax expense of the current year as “income

taxes payable”. But there is only a small part which is paid in by the company in the current

year since the company always pays in the taxes in small amounts. And these amounts are

indicated in the statement of cash flows. Also, the company does have the deferred tax assets

and the deferred tax liabilities that are considered while paying the taxes of the current year.

And it is due to this reason that the cash tax rate and the other tax rate are very much

different.

Conclusion:

The above report talks about the equity breakup of the company. The equity or the

contributed capital as it is generally called is one of the most important components when it

comes to the calculating in the debt to equity ratio. This is very much fine. The amount that

has been invested into the company has to be determined and the return that the company is

income

Unlevered cash

taxes -

92.0

0

EBITA

-

28,32,517.00

-

243.00

Cash tax rate 0.00% -37.86%

Part xvi:

The cash tax rate is always different from the amount of the taxes that are paid in by the

company. The company usually as a general practise follows the rule of paying off the taxes

that pertains to the previous year and records the tax expense of the current year as “income

taxes payable”. But there is only a small part which is paid in by the company in the current

year since the company always pays in the taxes in small amounts. And these amounts are

indicated in the statement of cash flows. Also, the company does have the deferred tax assets

and the deferred tax liabilities that are considered while paying the taxes of the current year.

And it is due to this reason that the cash tax rate and the other tax rate are very much

different.

Conclusion:

The above report talks about the equity breakup of the company. The equity or the

contributed capital as it is generally called is one of the most important components when it

comes to the calculating in the debt to equity ratio. This is very much fine. The amount that

has been invested into the company has to be determined and the return that the company is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING 32

able to generate on it is also very important since every shareholder would like to have a

return on his investment.

The statement of cash flows have bene discussed above, the various difference have ben

calculated and the reasons for such changes have been listed down. This statement of very

important since it shows in the cash that is readily available in the hands of the company to

meet its cash expenses or other such expenses.

Deferred taxes have been discussed, Adalta does not have any deferred taxes but Acrux has.

These assets or liabilities are very much important for the company. Both of the companies

have reported losses during the year and hence, there is as such no effective tax rate.

able to generate on it is also very important since every shareholder would like to have a

return on his investment.

The statement of cash flows have bene discussed above, the various difference have ben

calculated and the reasons for such changes have been listed down. This statement of very

important since it shows in the cash that is readily available in the hands of the company to

meet its cash expenses or other such expenses.

Deferred taxes have been discussed, Adalta does not have any deferred taxes but Acrux has.

These assets or liabilities are very much important for the company. Both of the companies

have reported losses during the year and hence, there is as such no effective tax rate.

CORPORATE ACCOUNTING 33

References:

Bragg, S. and Bragg, S. (2018). Other comprehensive income. [online] AccountingTools.

Available at: https://www.accountingtools.com/articles/what-is-other-comprehensive-

income.html [Accessed 2 Sep. 2018].

https://www.taxmann.com. (2018). Difference between Deferred Tax Asset (DTA) and

Deferred Tax Liability (DTL). [online] Available at:

https://www.taxmann.com/blogpost/2000000449/difference-between-deferred-tax-asset-dta-

and-deferred-tax-liability-dtl.aspx [Accessed 2 Sep. 2018].

Acrux. (2018). About Acrux - Acrux. [online] Available at: http://www.acrux.com.au/about/

[Accessed 17 Sep. 2018].

AdAlta - Developing i-body drugs to treat fibrotic diseases. (2018). Home - AdAlta -

Developing i-body drugs to treat fibrotic diseases. [online] Available at: http://adalta.com.au/

[Accessed 17 Sep. 2018].

Asx.com.au. (2018). The official list. [online] Available at:

https://www.asx.com.au/asx/research/listedCompanies.do?coName=A [Accessed 17 Sep.

2018].

www.acrux.au. (2018). Annual report 2015. [online] Available at:

http://www.annualreports.com/HostedData/AnnualReportArchive/a/ASX_ACR_2015.pdf

[Accessed 17 Sep. 2018].

www.acrux.au. (2018). Annual report 2017. [online] Available at:

http://www.annualreports.com/HostedData/AnnualReportArchive/a/ASX_ACR_2017.pdf

[Accessed 17 Sep. 2018].

References:

Bragg, S. and Bragg, S. (2018). Other comprehensive income. [online] AccountingTools.

Available at: https://www.accountingtools.com/articles/what-is-other-comprehensive-

income.html [Accessed 2 Sep. 2018].

https://www.taxmann.com. (2018). Difference between Deferred Tax Asset (DTA) and

Deferred Tax Liability (DTL). [online] Available at:

https://www.taxmann.com/blogpost/2000000449/difference-between-deferred-tax-asset-dta-

and-deferred-tax-liability-dtl.aspx [Accessed 2 Sep. 2018].

Acrux. (2018). About Acrux - Acrux. [online] Available at: http://www.acrux.com.au/about/

[Accessed 17 Sep. 2018].

AdAlta - Developing i-body drugs to treat fibrotic diseases. (2018). Home - AdAlta -

Developing i-body drugs to treat fibrotic diseases. [online] Available at: http://adalta.com.au/

[Accessed 17 Sep. 2018].

Asx.com.au. (2018). The official list. [online] Available at:

https://www.asx.com.au/asx/research/listedCompanies.do?coName=A [Accessed 17 Sep.

2018].

www.acrux.au. (2018). Annual report 2015. [online] Available at:

http://www.annualreports.com/HostedData/AnnualReportArchive/a/ASX_ACR_2015.pdf

[Accessed 17 Sep. 2018].

www.acrux.au. (2018). Annual report 2017. [online] Available at:

http://www.annualreports.com/HostedData/AnnualReportArchive/a/ASX_ACR_2017.pdf

[Accessed 17 Sep. 2018].

CORPORATE ACCOUNTING 34

www.adalta.au. (2018). Annual report 2015. [online] Available at:

http://1ad.live.irmau.com/irm/PDF/1012_0/2015AnnualReport [Accessed 17 Sep. 2018].

www.adalta.au. (2018). Annual report 2017. [online] Available at:

http://1ad.live.irmau.com/irm/PDF/1180_0/AnnualReporttoshareholders [Accessed 17 Sep.

2018].

www.adalta.au. (2018). Annual report 2015. [online] Available at:

http://1ad.live.irmau.com/irm/PDF/1012_0/2015AnnualReport [Accessed 17 Sep. 2018].

www.adalta.au. (2018). Annual report 2017. [online] Available at:

http://1ad.live.irmau.com/irm/PDF/1180_0/AnnualReporttoshareholders [Accessed 17 Sep.

2018].

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.