Corporate Accounting: Financial Analysis of Rio Tinto, Altura Mining, and BHP Billiton

Added on 2023-04-21

43 Pages5039 Words237 Views

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

1CORPORATE ACCOUNTING

Executive summary

Purpose of the report is to analyse various financial aspects of 3 companies from mining

industry of Australia that is Rio Tinto, Altura Mining and BHP Billiton. It will focus on

equities and liabilities reported by the entities and changes in the amount thereon. It will

further highlight the capital structure of the companies and will also analyse the other

comprehensive income statement and cash flow statement. Moreover the report will focus on

accounting aspects of corporate income tax.

Executive summary

Purpose of the report is to analyse various financial aspects of 3 companies from mining

industry of Australia that is Rio Tinto, Altura Mining and BHP Billiton. It will focus on

equities and liabilities reported by the entities and changes in the amount thereon. It will

further highlight the capital structure of the companies and will also analyse the other

comprehensive income statement and cash flow statement. Moreover the report will focus on

accounting aspects of corporate income tax.

2CORPORATE ACCOUNTING

Table of Contents

Introduction................................................................................................................................4

Equity and liabilities..................................................................................................................5

(i) Items of equity.............................................................................................................5

(ii) Items of liabilities........................................................................................................7

(iii) Comparative analysis of debt and equity...................................................................11

Cash flow statements................................................................................................................12

(iv) Items listed under cash flow statement......................................................................12

(v) Comparative analysis.................................................................................................13

(vi) Comparative analysis for explaining insights............................................................16

Other comprehensive income statement..................................................................................16

(vii) Items reported in other comprehensive income (OCI) statement..............................16

(viii) Reasons why the items not recognised under income statement...........................18

(ix) Comparative analysis.................................................................................................18

(x) Inclusion of comprehensive income for evaluation of manager’s performance.......18

Accounting for corporate income tax.......................................................................................19

(xi) Tax expenses.............................................................................................................19

(xii) Effective tax rate........................................................................................................19

(xiii) Deferred tax assets or liabilities.............................................................................19

(xiv) Increase or decrease in the deferred tax assets or liabilities..................................20

Table of Contents

Introduction................................................................................................................................4

Equity and liabilities..................................................................................................................5

(i) Items of equity.............................................................................................................5

(ii) Items of liabilities........................................................................................................7

(iii) Comparative analysis of debt and equity...................................................................11

Cash flow statements................................................................................................................12

(iv) Items listed under cash flow statement......................................................................12

(v) Comparative analysis.................................................................................................13

(vi) Comparative analysis for explaining insights............................................................16

Other comprehensive income statement..................................................................................16

(vii) Items reported in other comprehensive income (OCI) statement..............................16

(viii) Reasons why the items not recognised under income statement...........................18

(ix) Comparative analysis.................................................................................................18

(x) Inclusion of comprehensive income for evaluation of manager’s performance.......18

Accounting for corporate income tax.......................................................................................19

(xi) Tax expenses.............................................................................................................19

(xii) Effective tax rate........................................................................................................19

(xiii) Deferred tax assets or liabilities.............................................................................19

(xiv) Increase or decrease in the deferred tax assets or liabilities..................................20

3CORPORATE ACCOUNTING

(xv) Cash tax.....................................................................................................................20

(xvi) Cash tax rate...........................................................................................................20

(xvii) Difference among book tax rate and cash tax rate.................................................21

Conclusion................................................................................................................................21

References................................................................................................................................22

Appendix..................................................................................................................................24

(xv) Cash tax.....................................................................................................................20

(xvi) Cash tax rate...........................................................................................................20

(xvii) Difference among book tax rate and cash tax rate.................................................21

Conclusion................................................................................................................................21

References................................................................................................................................22

Appendix..................................................................................................................................24

4CORPORATE ACCOUNTING

Introduction

Rio Tinto Plc. That was incorporated on 30th March 1962 is the leading metals and

mining entity in Australia. The major business of the entity is finding, processing and mining

of the mineral resources. Various segments of the entity includes Aluminium, Iron Ore,

Diamonds and copper, minerals and energy and different other operations. Materials from the

company are essential for making the modern life work and their economies assist the

communities to prosper and economies to grow. Further, through various innovations and

researches they help to meet the requirements of the society in changing as well as growing

the world. Moreover, they bring benefits to the people, to the communities under which it

operates and beyond (Riotinto.com 2018).

Altura Mining is the key player in the global market for lithium that is based in

Perth, Australia. It is leveraging the growing demand for the raw materials to manufacture

lithium ion batteries used in electric vehicles and for static usages. The entity is further

engaged in development and exploration activities and its segments include exploration

services, coal mining and exploration of minerals. Coal mining sector of the company is

involved in selling of coal. Further, the company is focussed on development and

construction of Pilgangoora Lithium project that is 100% owned by it and situated in Pilbara

region of Western Australia. Moreover, the company delivers drilling services to the

exploration and mining companies (Alturamining.com 2018).

BHP Billiton that was established in 2001 with the merger of Broken Hill, Proprietary

(BHP) and Billiton is one of the largest global resources and mining company that has more

than 100,000 employees in more than 25 nations. Headquarter of the company is in

Melbourne, Australia. It is among the largest producers for copper, aluminium, iron ore,

manganese, nickel, titanium, silver and uranium. Further, it is the 7th largest aluminium

Introduction

Rio Tinto Plc. That was incorporated on 30th March 1962 is the leading metals and

mining entity in Australia. The major business of the entity is finding, processing and mining

of the mineral resources. Various segments of the entity includes Aluminium, Iron Ore,

Diamonds and copper, minerals and energy and different other operations. Materials from the

company are essential for making the modern life work and their economies assist the

communities to prosper and economies to grow. Further, through various innovations and

researches they help to meet the requirements of the society in changing as well as growing

the world. Moreover, they bring benefits to the people, to the communities under which it

operates and beyond (Riotinto.com 2018).

Altura Mining is the key player in the global market for lithium that is based in

Perth, Australia. It is leveraging the growing demand for the raw materials to manufacture

lithium ion batteries used in electric vehicles and for static usages. The entity is further

engaged in development and exploration activities and its segments include exploration

services, coal mining and exploration of minerals. Coal mining sector of the company is

involved in selling of coal. Further, the company is focussed on development and

construction of Pilgangoora Lithium project that is 100% owned by it and situated in Pilbara

region of Western Australia. Moreover, the company delivers drilling services to the

exploration and mining companies (Alturamining.com 2018).

BHP Billiton that was established in 2001 with the merger of Broken Hill, Proprietary

(BHP) and Billiton is one of the largest global resources and mining company that has more

than 100,000 employees in more than 25 nations. Headquarter of the company is in

Melbourne, Australia. It is among the largest producers for copper, aluminium, iron ore,

manganese, nickel, titanium, silver and uranium. Further, it is the 7th largest aluminium

5CORPORATE ACCOUNTING

producer in the world. Aluminium portfolio of the entity includes bauxite refining for

producing alumina, bauxite production and smelting of the aluminium metal (BHP 2018).

Equity and liabilities

(i) Items of equity

Rio Tinto – listed equity items for the entity are as follows –

Share capital – share capital is the fund that is raised by issuing shares for cash or

consideration. It is the long-term source for finance. Shareholders get share of

ownership in the company in return of their share holdings

Share premium – it is the amount that is subscribed to for the new issue of shares

over and above its par value. It can be used only for specific purposes mentioned in

the bylaws of the entity (Marshall 2016).

Other reserves – other reserves is the part of equity that excludes the basic share

capital part. Generally the other reserves includes specified part of the surplus fund

generated through various other sources like selling the shares at premium or upward

revaluation of fixed asset

Retained earnings – it is the profit available with the company at the balance sheet

date and is decreased by the amount of any distribution made to the the stockholders

as a means of dividend. However, the amounts of retained earnings are also re-

invested in business or are maintained as reserve for particular purposes (Melloni, Lai

and Stacchezzini 2018).

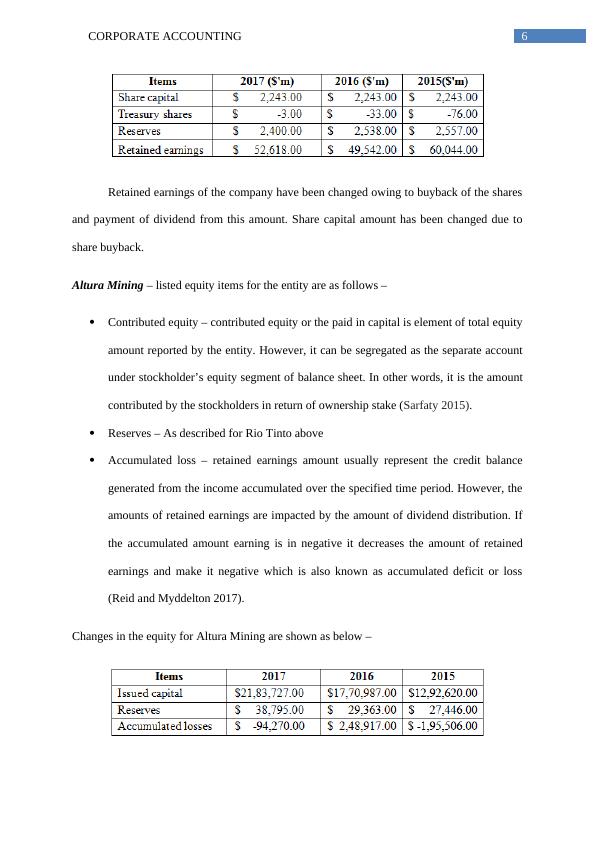

Changes in the equity for Rio Tinto are shown as below –

producer in the world. Aluminium portfolio of the entity includes bauxite refining for

producing alumina, bauxite production and smelting of the aluminium metal (BHP 2018).

Equity and liabilities

(i) Items of equity

Rio Tinto – listed equity items for the entity are as follows –

Share capital – share capital is the fund that is raised by issuing shares for cash or

consideration. It is the long-term source for finance. Shareholders get share of

ownership in the company in return of their share holdings

Share premium – it is the amount that is subscribed to for the new issue of shares

over and above its par value. It can be used only for specific purposes mentioned in

the bylaws of the entity (Marshall 2016).

Other reserves – other reserves is the part of equity that excludes the basic share

capital part. Generally the other reserves includes specified part of the surplus fund

generated through various other sources like selling the shares at premium or upward

revaluation of fixed asset

Retained earnings – it is the profit available with the company at the balance sheet

date and is decreased by the amount of any distribution made to the the stockholders

as a means of dividend. However, the amounts of retained earnings are also re-

invested in business or are maintained as reserve for particular purposes (Melloni, Lai

and Stacchezzini 2018).

Changes in the equity for Rio Tinto are shown as below –

6CORPORATE ACCOUNTING

Retained earnings of the company have been changed owing to buyback of the shares

and payment of dividend from this amount. Share capital amount has been changed due to

share buyback.

Altura Mining – listed equity items for the entity are as follows –

Contributed equity – contributed equity or the paid in capital is element of total equity

amount reported by the entity. However, it can be segregated as the separate account

under stockholder’s equity segment of balance sheet. In other words, it is the amount

contributed by the stockholders in return of ownership stake (Sarfaty 2015).

Reserves – As described for Rio Tinto above

Accumulated loss – retained earnings amount usually represent the credit balance

generated from the income accumulated over the specified time period. However, the

amounts of retained earnings are impacted by the amount of dividend distribution. If

the accumulated amount earning is in negative it decreases the amount of retained

earnings and make it negative which is also known as accumulated deficit or loss

(Reid and Myddelton 2017).

Changes in the equity for Altura Mining are shown as below –

Retained earnings of the company have been changed owing to buyback of the shares

and payment of dividend from this amount. Share capital amount has been changed due to

share buyback.

Altura Mining – listed equity items for the entity are as follows –

Contributed equity – contributed equity or the paid in capital is element of total equity

amount reported by the entity. However, it can be segregated as the separate account

under stockholder’s equity segment of balance sheet. In other words, it is the amount

contributed by the stockholders in return of ownership stake (Sarfaty 2015).

Reserves – As described for Rio Tinto above

Accumulated loss – retained earnings amount usually represent the credit balance

generated from the income accumulated over the specified time period. However, the

amounts of retained earnings are impacted by the amount of dividend distribution. If

the accumulated amount earning is in negative it decreases the amount of retained

earnings and make it negative which is also known as accumulated deficit or loss

(Reid and Myddelton 2017).

Changes in the equity for Altura Mining are shown as below –

7CORPORATE ACCOUNTING

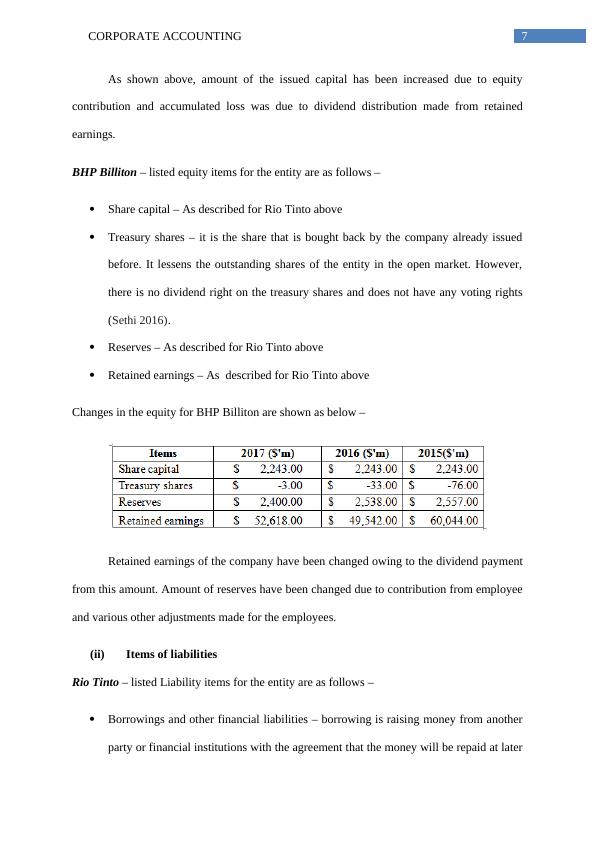

As shown above, amount of the issued capital has been increased due to equity

contribution and accumulated loss was due to dividend distribution made from retained

earnings.

BHP Billiton – listed equity items for the entity are as follows –

Share capital – As described for Rio Tinto above

Treasury shares – it is the share that is bought back by the company already issued

before. It lessens the outstanding shares of the entity in the open market. However,

there is no dividend right on the treasury shares and does not have any voting rights

(Sethi 2016).

Reserves – As described for Rio Tinto above

Retained earnings – As described for Rio Tinto above

Changes in the equity for BHP Billiton are shown as below –

Retained earnings of the company have been changed owing to the dividend payment

from this amount. Amount of reserves have been changed due to contribution from employee

and various other adjustments made for the employees.

(ii) Items of liabilities

Rio Tinto – listed Liability items for the entity are as follows –

Borrowings and other financial liabilities – borrowing is raising money from another

party or financial institutions with the agreement that the money will be repaid at later

As shown above, amount of the issued capital has been increased due to equity

contribution and accumulated loss was due to dividend distribution made from retained

earnings.

BHP Billiton – listed equity items for the entity are as follows –

Share capital – As described for Rio Tinto above

Treasury shares – it is the share that is bought back by the company already issued

before. It lessens the outstanding shares of the entity in the open market. However,

there is no dividend right on the treasury shares and does not have any voting rights

(Sethi 2016).

Reserves – As described for Rio Tinto above

Retained earnings – As described for Rio Tinto above

Changes in the equity for BHP Billiton are shown as below –

Retained earnings of the company have been changed owing to the dividend payment

from this amount. Amount of reserves have been changed due to contribution from employee

and various other adjustments made for the employees.

(ii) Items of liabilities

Rio Tinto – listed Liability items for the entity are as follows –

Borrowings and other financial liabilities – borrowing is raising money from another

party or financial institutions with the agreement that the money will be repaid at later

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Corporate Accounting: Analysis of Finance Statements of ASX Listed Entitieslg...

|25

|4640

|111

Corporate Accountinglg...

|23

|4909

|209

Corporate Accounting: Analysis of Financial Statements of Ausdrill Ltd and Rio Tinto Ltdlg...

|19

|4875

|228

Corporate Accounting: Analysis of Financial Statements of Ausdrill Ltd and Rio Tinto Ltdlg...

|17

|4368

|489

Financial Ratio Analysis of BHP Billiton and Rio Tintolg...

|32

|4468

|343

Financial Reporting Analysis of BHP and Rio Tintolg...

|15

|3353

|303