Corporate Accounting

VerifiedAdded on 2023/04/20

|23

|4909

|209

AI Summary

The report is focused on analysing the various items listed in the financial statements of BHP Billiton, Rio Tinto and Ausdrill Limited. The objective is to evaluate their cash flow position, other comprehensive income statement, debt and equity positions along with corporate taxation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE ACCOUNTING

Executive Summary:

The report is focused on analysing the various items listed in the financial statements of BHP

Billiton, Rio Tinto and Ausdrill Limited. The objective is to evaluate their cash flow position,

other comprehensive income statement, debt and equity positions along with corporate taxation.

The initial section of the report has emphasised on the debt and equity aspects of the three above-

mentioned organisations. After this, the cash flow positions of the organisations are evaluated

effectively. The next section has dealt with assessing the other comprehensive income statements

of the organisations. Finally, the report has shed light on evaluating the different aspects of

taxation of the organisations.

Executive Summary:

The report is focused on analysing the various items listed in the financial statements of BHP

Billiton, Rio Tinto and Ausdrill Limited. The objective is to evaluate their cash flow position,

other comprehensive income statement, debt and equity positions along with corporate taxation.

The initial section of the report has emphasised on the debt and equity aspects of the three above-

mentioned organisations. After this, the cash flow positions of the organisations are evaluated

effectively. The next section has dealt with assessing the other comprehensive income statements

of the organisations. Finally, the report has shed light on evaluating the different aspects of

taxation of the organisations.

2CORPORATE ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................4

Equity and liability:.........................................................................................................................5

Question (i):.................................................................................................................................5

Question (ii):................................................................................................................................6

Question (iii):...............................................................................................................................7

Cash flow statement:........................................................................................................................8

Question (iv):...............................................................................................................................8

Question (v):..............................................................................................................................10

Question (vi):.............................................................................................................................13

Other comprehensive income statement:.......................................................................................14

Question (vii):............................................................................................................................14

Question (viii):...........................................................................................................................14

Question (ix):.............................................................................................................................14

Question (x):..............................................................................................................................15

Accounting for corporate income tax:...........................................................................................15

Question (xi):.............................................................................................................................15

Question (xii):............................................................................................................................16

Question (xiii):...........................................................................................................................17

Table of Contents

Introduction:....................................................................................................................................4

Equity and liability:.........................................................................................................................5

Question (i):.................................................................................................................................5

Question (ii):................................................................................................................................6

Question (iii):...............................................................................................................................7

Cash flow statement:........................................................................................................................8

Question (iv):...............................................................................................................................8

Question (v):..............................................................................................................................10

Question (vi):.............................................................................................................................13

Other comprehensive income statement:.......................................................................................14

Question (vii):............................................................................................................................14

Question (viii):...........................................................................................................................14

Question (ix):.............................................................................................................................14

Question (x):..............................................................................................................................15

Accounting for corporate income tax:...........................................................................................15

Question (xi):.............................................................................................................................15

Question (xii):............................................................................................................................16

Question (xiii):...........................................................................................................................17

3CORPORATE ACCOUNTING

Question (xiv):...........................................................................................................................17

Question (xv):............................................................................................................................18

Question (xvi):...........................................................................................................................18

Question (xvii):..........................................................................................................................18

Conclusion:....................................................................................................................................19

References and Bibliographies:.....................................................................................................20

Question (xiv):...........................................................................................................................17

Question (xv):............................................................................................................................18

Question (xvi):...........................................................................................................................18

Question (xvii):..........................................................................................................................18

Conclusion:....................................................................................................................................19

References and Bibliographies:.....................................................................................................20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE ACCOUNTING

Introduction:

The report intends to analyse the financial statements of three ASX listed organisations

functioning in the same industrial sector. The organisations chosen include BHP Billiton, Rio

Tinto and Ausdrill Limited, as they operate in the Australian mining sector. The report takes into

account the evaluation of the latest annual reports of the three organisations including the

assessment of segments such as equity and liability, other comprehensive income statement and

corporate income tax.

BHP Billiton is one of the leading mining companies in Australia, which is involved in

inventing, acquiring, developing and marketing natural resources globally. The main products of

the organisation include copper, petroleum, coal and iron ore. It has been founded in 1851 with

an employee base of 27,161 staffs (BHP 2018).

Rio Tinto is engaged in mining, finding along with processing mineral resources globally.

The organisation provides copper, aluminium, molybdenum, silver, industrial minerals, gold,

titanium dioxide, borates, iron ore, salt, uranium, metallurgical coal and iron ore. It is an Anglo-

Australian organisation established in 1973 with workforce of around 46,807 staffs

(Riotinto.com 2018).

Ausdrill Limited functions as a global mining services organisation. The main operations

include Drilling Services Australia, Contract Mining Services Africa, Equipment Services and

Supplies and other segments. The organisation is engaged in reverse circulation, rotary air blast,

diamond drilling, bores production and monitoring, surface hole drilling, rotary air blast and

Introduction:

The report intends to analyse the financial statements of three ASX listed organisations

functioning in the same industrial sector. The organisations chosen include BHP Billiton, Rio

Tinto and Ausdrill Limited, as they operate in the Australian mining sector. The report takes into

account the evaluation of the latest annual reports of the three organisations including the

assessment of segments such as equity and liability, other comprehensive income statement and

corporate income tax.

BHP Billiton is one of the leading mining companies in Australia, which is involved in

inventing, acquiring, developing and marketing natural resources globally. The main products of

the organisation include copper, petroleum, coal and iron ore. It has been founded in 1851 with

an employee base of 27,161 staffs (BHP 2018).

Rio Tinto is engaged in mining, finding along with processing mineral resources globally.

The organisation provides copper, aluminium, molybdenum, silver, industrial minerals, gold,

titanium dioxide, borates, iron ore, salt, uranium, metallurgical coal and iron ore. It is an Anglo-

Australian organisation established in 1973 with workforce of around 46,807 staffs

(Riotinto.com 2018).

Ausdrill Limited functions as a global mining services organisation. The main operations

include Drilling Services Australia, Contract Mining Services Africa, Equipment Services and

Supplies and other segments. The organisation is engaged in reverse circulation, rotary air blast,

diamond drilling, bores production and monitoring, surface hole drilling, rotary air blast and

5CORPORATE ACCOUNTING

others. The organisation is founded in 1987 having employee base of around 5,278

(Ausdrill.com.au 2018).

Equity and liability:

Question (i):

From the annual reports of the three chosen organisations, it is apparent that all of them

have certain equity items in their balance sheet statement.

As per the annual reports of Rio Tinto, there are three main equity items, which include

share capital, reserves and retained earnings. The share capital of the organisation has increased

from $4,174 million in 2015 to $4,360 million in 2017 owing to the rise in number of equity

shares. Increase in reserves could be observed from $9,139 million in 2015 to $12,284 million in

2017 owing to the increase in foreign currency translation reserve, hedge reserve and others

(Brigham et al. 2016). Finally, increase in retained earnings could be observed from $19,736

million in 2015 to $23,761 million in 2017, as it has managed to increase its profit over margin

over the years (Riotinto.com 2018).

For BHP Billiton, the main equity items include share capital, treasury shares, reserved

and retained earnings. No change could be observed in share capital from 2015 to 2017, as the

organisation has not issued additional equity shares in the market (Miller-Nobles, Mattison and

Matsumura 2016). Treasury shares are observed to decline significantly from $76 million in

2015 to $3 million in 2017, as it has minimised its share buyback strategy. Reserves are observed

to decline from $2,557 million in 2015 to $2,400 million in 2017 due to the fall in hedge reserve

and foreign currency translation reserve (Marshall 2016). Finally, retained earnings have fallen

others. The organisation is founded in 1987 having employee base of around 5,278

(Ausdrill.com.au 2018).

Equity and liability:

Question (i):

From the annual reports of the three chosen organisations, it is apparent that all of them

have certain equity items in their balance sheet statement.

As per the annual reports of Rio Tinto, there are three main equity items, which include

share capital, reserves and retained earnings. The share capital of the organisation has increased

from $4,174 million in 2015 to $4,360 million in 2017 owing to the rise in number of equity

shares. Increase in reserves could be observed from $9,139 million in 2015 to $12,284 million in

2017 owing to the increase in foreign currency translation reserve, hedge reserve and others

(Brigham et al. 2016). Finally, increase in retained earnings could be observed from $19,736

million in 2015 to $23,761 million in 2017, as it has managed to increase its profit over margin

over the years (Riotinto.com 2018).

For BHP Billiton, the main equity items include share capital, treasury shares, reserved

and retained earnings. No change could be observed in share capital from 2015 to 2017, as the

organisation has not issued additional equity shares in the market (Miller-Nobles, Mattison and

Matsumura 2016). Treasury shares are observed to decline significantly from $76 million in

2015 to $3 million in 2017, as it has minimised its share buyback strategy. Reserves are observed

to decline from $2,557 million in 2015 to $2,400 million in 2017 due to the fall in hedge reserve

and foreign currency translation reserve (Marshall 2016). Finally, retained earnings have fallen

6CORPORATE ACCOUNTING

from $60,044 million in 2015 to $52,618 million in 2017 due to decline in overall profit level of

the organisation (BHP 2018).

In case of Ausdrill Limited, the three equity items include contributed equity, reserves

and retained earnings. Like BHP Billiton, no change could be observed in contributed equity of

the organisation due to no additional shares issued in the meantime. However, there are

significant fall in reserves over the three-year period. Finally, significant rise in retained earnings

could be witnessed from 2015 to 2017 due to considerable increase in profitability

(Ausdrill.com.au 2018).

Question (ii):

From the annual report of Rio Tinto in 2017, there is presence of both current and non-

current liabilities. The current liabilities include borrowings and other financial liabilities, trade

payables, tax payable and provisions comprising of post-retirement benefits. The total current

liabilities have increased mainly due to rise in trade payables. Non-current liabilities comprise of

borrowings and other financial liabilities, trade payables, deferred tax liabilities, tax payables and

provisions comprising of post-retirement benefits. However, non-current liabilities have

decreased owing to considerable decline in long-term borrowings and other financial liabilities

(Riotinto.com 2018). As a result, the total liabilities have decreased from 2015 to 2017 for Rio

Tinto.

In case of BHP Billiton, the current liabilities constitute of trade payables, interest

bearing liabilities, other financial liabilities, current tax payable, provisions and deferred income.

The current liabilities have declined from $12,853 million in 2015 to $11,366 million in 2017

due to fall in trade payables. On the other hand, the non-current liabilities include trade payables,

from $60,044 million in 2015 to $52,618 million in 2017 due to decline in overall profit level of

the organisation (BHP 2018).

In case of Ausdrill Limited, the three equity items include contributed equity, reserves

and retained earnings. Like BHP Billiton, no change could be observed in contributed equity of

the organisation due to no additional shares issued in the meantime. However, there are

significant fall in reserves over the three-year period. Finally, significant rise in retained earnings

could be witnessed from 2015 to 2017 due to considerable increase in profitability

(Ausdrill.com.au 2018).

Question (ii):

From the annual report of Rio Tinto in 2017, there is presence of both current and non-

current liabilities. The current liabilities include borrowings and other financial liabilities, trade

payables, tax payable and provisions comprising of post-retirement benefits. The total current

liabilities have increased mainly due to rise in trade payables. Non-current liabilities comprise of

borrowings and other financial liabilities, trade payables, deferred tax liabilities, tax payables and

provisions comprising of post-retirement benefits. However, non-current liabilities have

decreased owing to considerable decline in long-term borrowings and other financial liabilities

(Riotinto.com 2018). As a result, the total liabilities have decreased from 2015 to 2017 for Rio

Tinto.

In case of BHP Billiton, the current liabilities constitute of trade payables, interest

bearing liabilities, other financial liabilities, current tax payable, provisions and deferred income.

The current liabilities have declined from $12,853 million in 2015 to $11,366 million in 2017

due to fall in trade payables. On the other hand, the non-current liabilities include trade payables,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

interest bearing liabilities, other financial liabilities, deferred tax liabilities, provisions and

deferred income. There has been significant decline in non-current liabilities from $54,035

million in 2015 to $42,914 million in 2017, as interest bearing liabilities have declined

considerably. This has resulted in decline in total liabilities of the organisation in 2017 (BHP

2018).

According to the annual reports of Ausdrill Limited, current liabilities include trade

payables, borrowings; current tax liabilities and employee benefit obligations, which have

increased owing to increase in employee benefit obligations. The non-current liabilities include

borrowings, deferred tax liabilities and employee benefit obligations. The amount has declined

from $433,300,000 in 2015 to $408,852 million in 2017 due to fall in long-term borrowings

(Ausdrill.com.au 2018).

Question (iii):

In order to contrast the debt and equity position of the three organisations, debt-to-equity

ratio is deemed to be the most suitable measure.

interest bearing liabilities, other financial liabilities, deferred tax liabilities, provisions and

deferred income. There has been significant decline in non-current liabilities from $54,035

million in 2015 to $42,914 million in 2017, as interest bearing liabilities have declined

considerably. This has resulted in decline in total liabilities of the organisation in 2017 (BHP

2018).

According to the annual reports of Ausdrill Limited, current liabilities include trade

payables, borrowings; current tax liabilities and employee benefit obligations, which have

increased owing to increase in employee benefit obligations. The non-current liabilities include

borrowings, deferred tax liabilities and employee benefit obligations. The amount has declined

from $433,300,000 in 2015 to $408,852 million in 2017 due to fall in long-term borrowings

(Ausdrill.com.au 2018).

Question (iii):

In order to contrast the debt and equity position of the three organisations, debt-to-equity

ratio is deemed to be the most suitable measure.

8CORPORATE ACCOUNTING

2016 2017 2018

-

0.20

0.40

0.60

0.80

1.00

1.20

0.77

0.98

0.87

1.07

0.95

0.87

1.04

0.90 0.88

Debt to Equity Ratio

BHP Billiton Rio Rinto Ausdrill Limited

From the above table and figure, it could be observed that all three organisations utilise

more debt capital rather than equity financing for meeting their capital needs. Out of these

organisations, the maximum amount of debt capital is used by Rio Tinto and Ausdrill Limited.

However, in terms of liabilities, Ausdrill Limited has the lowest liability amount compared to the

other two organisations. Thus, in terms of financial leverage, BHP Billiton has the lowest

amount of risk followed by Ausdrill Limited and Rio Tinto.

Cash flow statement:

Question (iv):

From the cash flow statements of BHP Billiton, the main items under operating cash

flows include dividends received, interest paid and interest received, income tax refund and

payment and changes in assets and liabilities. These cash flows have fallen considerably from

2015 to 2016; however, improvements could be observed in 2017. The investing cash flows of

the organisation mainly include purchase of property, plant and equipment, exploration expense,

2016 2017 2018

-

0.20

0.40

0.60

0.80

1.00

1.20

0.77

0.98

0.87

1.07

0.95

0.87

1.04

0.90 0.88

Debt to Equity Ratio

BHP Billiton Rio Rinto Ausdrill Limited

From the above table and figure, it could be observed that all three organisations utilise

more debt capital rather than equity financing for meeting their capital needs. Out of these

organisations, the maximum amount of debt capital is used by Rio Tinto and Ausdrill Limited.

However, in terms of liabilities, Ausdrill Limited has the lowest liability amount compared to the

other two organisations. Thus, in terms of financial leverage, BHP Billiton has the lowest

amount of risk followed by Ausdrill Limited and Rio Tinto.

Cash flow statement:

Question (iv):

From the cash flow statements of BHP Billiton, the main items under operating cash

flows include dividends received, interest paid and interest received, income tax refund and

payment and changes in assets and liabilities. These cash flows have fallen considerably from

2015 to 2016; however, improvements could be observed in 2017. The investing cash flows of

the organisation mainly include purchase of property, plant and equipment, exploration expense,

9CORPORATE ACCOUNTING

proceeds from asset sale and proceeds from divestment of operations, subsidiaries and joint

operations. The investing cash flows have fallen over the year mainly due to decline in purchase

of property, plant and equipment implying less investment on fixed assets (Gordon et al. 2017).

In case of financing cash flows, the significant items include proceeds from interest bearing

liabilities, settlements or proceeds from instruments associated with debt, repayment of interest

bearing liabilities, ordinary share proceeds, share purchase for staffs and others. These cash

flows have increased significantly in 2017 owing to lower proceeds generated from interest

bearing liabilities. However, the significant rise in operating cash flows have offset such increase

due to which increase in closing cash balance could be observed in 2017 (BHP 2018).

In case of Rio Tinto, the major items falling under operating cash flows include dividend

from equity-accounted units, consolidated operational cash flows, payment of net interest and

dividend and tax payment. These cash flows have increased considerably from 2015 to 2017

owing to increase in consolidated operational cash flows. The investing cash flows of the

organisation constitute of purchase and sale of fixed and intangible assets, disposals of

subsidiaries, joint ventures and subsidiaries, purchase and sale of financial assets acquisitions of

subsidiaries, joint ventures and subsidiaries. These cash flows have fallen from 2015 to 2017 due

to increased earnings from disposals made. The financing cash flows include payment of equity

dividends, proceeds from and repayment of borrowings, share repurchase and others. The main

reason that these cash flows have increased in 2017 is due to share repurchase and payment of

equity dividend. As a result, positive increase in cash balance could be observed in 2017

(Riotinto.com 2018).

For Ausdrill Limited, the main items falling under operating cash flows include customer

receipts, supplier payments, interest receipt and payment, income tax refund and payment along

proceeds from asset sale and proceeds from divestment of operations, subsidiaries and joint

operations. The investing cash flows have fallen over the year mainly due to decline in purchase

of property, plant and equipment implying less investment on fixed assets (Gordon et al. 2017).

In case of financing cash flows, the significant items include proceeds from interest bearing

liabilities, settlements or proceeds from instruments associated with debt, repayment of interest

bearing liabilities, ordinary share proceeds, share purchase for staffs and others. These cash

flows have increased significantly in 2017 owing to lower proceeds generated from interest

bearing liabilities. However, the significant rise in operating cash flows have offset such increase

due to which increase in closing cash balance could be observed in 2017 (BHP 2018).

In case of Rio Tinto, the major items falling under operating cash flows include dividend

from equity-accounted units, consolidated operational cash flows, payment of net interest and

dividend and tax payment. These cash flows have increased considerably from 2015 to 2017

owing to increase in consolidated operational cash flows. The investing cash flows of the

organisation constitute of purchase and sale of fixed and intangible assets, disposals of

subsidiaries, joint ventures and subsidiaries, purchase and sale of financial assets acquisitions of

subsidiaries, joint ventures and subsidiaries. These cash flows have fallen from 2015 to 2017 due

to increased earnings from disposals made. The financing cash flows include payment of equity

dividends, proceeds from and repayment of borrowings, share repurchase and others. The main

reason that these cash flows have increased in 2017 is due to share repurchase and payment of

equity dividend. As a result, positive increase in cash balance could be observed in 2017

(Riotinto.com 2018).

For Ausdrill Limited, the main items falling under operating cash flows include customer

receipts, supplier payments, interest receipt and payment, income tax refund and payment along

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE ACCOUNTING

with receipt of management fee. These cash flows have decreased from 2015 to 2017 due to fall

in receipts from customers. The investing cash flow items primarily include payments for fixed

assets and investments, proceeds from fixed assets and business sale and others. The reason that

these cash flows have increased from 2015 to 2017 is due to considerable payment for fixed

assets, particularly, property, plant and equipment. The financing cash flow items include

repayment of hire purchase, secured borrowings and lease liabilities, dividend payment to

shareholders and proceeds from and repayment of unsecured borrowings. These cash flows have

decreased considerably due to repayment of secured borrowings. Due to this, increase in cash

balance could be observed in 2017 compared to 2016 (Ausdrill.com.au 2018).

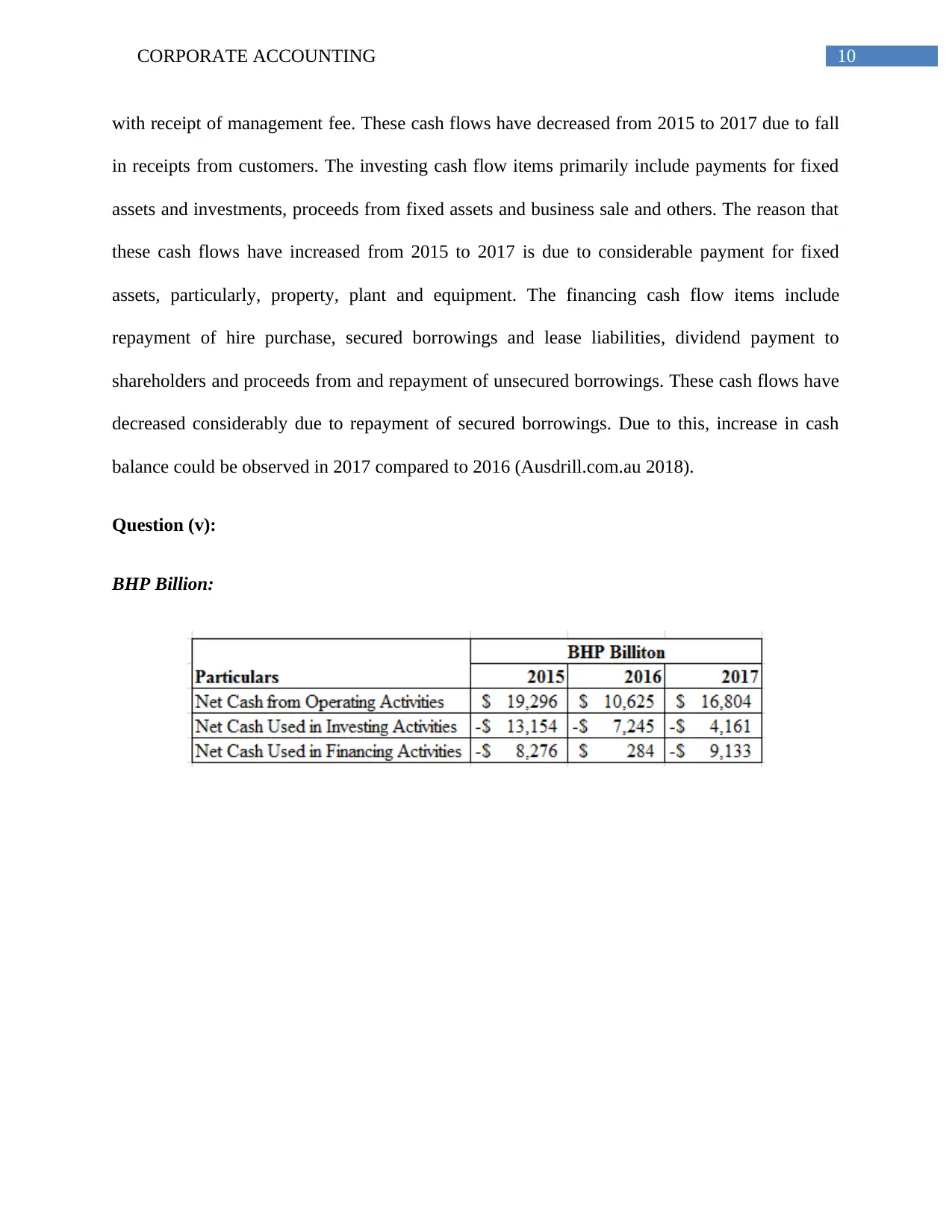

Question (v):

BHP Billion:

with receipt of management fee. These cash flows have decreased from 2015 to 2017 due to fall

in receipts from customers. The investing cash flow items primarily include payments for fixed

assets and investments, proceeds from fixed assets and business sale and others. The reason that

these cash flows have increased from 2015 to 2017 is due to considerable payment for fixed

assets, particularly, property, plant and equipment. The financing cash flow items include

repayment of hire purchase, secured borrowings and lease liabilities, dividend payment to

shareholders and proceeds from and repayment of unsecured borrowings. These cash flows have

decreased considerably due to repayment of secured borrowings. Due to this, increase in cash

balance could be observed in 2017 compared to 2016 (Ausdrill.com.au 2018).

Question (v):

BHP Billion:

11CORPORATE ACCOUNTING

2015 2016 2017

-$15,000

-$10,000

-$5,000

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$19,296

$10,625

$16,804

-$13,154

-$7,245

-$4,161

-$8,276

$284

-$9,133

BHP Billiton

Net Cash from Operating Activities Net Cash Used in Investing Activities

Net Cash Used in Financing Activities

It could be observed from the above figure that the operating cash flows of the

organisation have declined from 2015 to 2017 and this denotes falling business income from

operational business functions (Khansalar and Namazi 2017). After this, the organisation has

decreased its investment over the years by minimising the payment of fixed assets. However, it

has incurred huge expenses for repaying interest bearing liabilities (BHP 2018).

Rio Tinto:

2015 2016 2017

-$15,000

-$10,000

-$5,000

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$19,296

$10,625

$16,804

-$13,154

-$7,245

-$4,161

-$8,276

$284

-$9,133

BHP Billiton

Net Cash from Operating Activities Net Cash Used in Investing Activities

Net Cash Used in Financing Activities

It could be observed from the above figure that the operating cash flows of the

organisation have declined from 2015 to 2017 and this denotes falling business income from

operational business functions (Khansalar and Namazi 2017). After this, the organisation has

decreased its investment over the years by minimising the payment of fixed assets. However, it

has incurred huge expenses for repaying interest bearing liabilities (BHP 2018).

Rio Tinto:

12CORPORATE ACCOUNTING

2015 2016 2017

-$15,000

-$10,000

-$5,000

$-

$5,000

$10,000

$15,000

$20,000

$9,383 $8,465

$13,884

-$4,600

-$2,104 -$2,373

-$7,670 -$7,491 -$9,141

Rio Tinto

Net Cash from Operating Activities Net Cash Used in Investing Activities

Net Cash Used in Financing Activities

Froom the above figure, it is apparent that there is huge increase in operating cash flows

due to increased earnings from consolidated operational cash flows. However, there is fall in

investing cash flows due to earnings from disposals (Reid and Myddelton 2017). Finally, there

has been rise in financing cash flows due to share buyback by the owners of the organisation

(Riotinto.com 2018).

Ausdrill Limited:

i

2015 2016 2017

-$15,000

-$10,000

-$5,000

$-

$5,000

$10,000

$15,000

$20,000

$9,383 $8,465

$13,884

-$4,600

-$2,104 -$2,373

-$7,670 -$7,491 -$9,141

Rio Tinto

Net Cash from Operating Activities Net Cash Used in Investing Activities

Net Cash Used in Financing Activities

Froom the above figure, it is apparent that there is huge increase in operating cash flows

due to increased earnings from consolidated operational cash flows. However, there is fall in

investing cash flows due to earnings from disposals (Reid and Myddelton 2017). Finally, there

has been rise in financing cash flows due to share buyback by the owners of the organisation

(Riotinto.com 2018).

Ausdrill Limited:

i

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CORPORATE ACCOUNTING

2015 2016 2017

-$150,000

-$100,000

-$50,000

$-

$50,000

$100,000

$150,000 $117,936

$91,006 $94,613

-$738

$60,853

-$101,127-$104,693

-$47,772

-$6,965

Ausdrill Limited

Net Cash from Operating Activities Net Cash Used in Investing Activities

Net Cash Used in Financing Activities

The above figure clearly indicates that the operating cash flows have fallen from 2015 to

2017 due to decline in customer receipts. However, huge expenses incurred for property, plant

and equipment have increased the investing cash flows for Ausdrill Limited. On the other hand,

financing cash flows have fallen in 2017 from 2015 due to no expenses incurred in repaying

secured borrowings (Ausdrill.com.au 2018).

Question (vi):

Based on the above analysis, it could be stated that BHP Billiton has earned maximum

amount from operating cash flows followed by Rio Tinto and Ausdrill Limited, even though the

trend is declining over the years. It could be witnessed that all organisations are involved in

investment of buying property, plant and equipment, intangibles and other business acquisitions.

When all the aspects are combined together, it could be observed that they have made huge

investments. Finally, the three organisations have incurred huge expenses for interest, finance

costs and dividends, which have resulted in increased cash flows.

2015 2016 2017

-$150,000

-$100,000

-$50,000

$-

$50,000

$100,000

$150,000 $117,936

$91,006 $94,613

-$738

$60,853

-$101,127-$104,693

-$47,772

-$6,965

Ausdrill Limited

Net Cash from Operating Activities Net Cash Used in Investing Activities

Net Cash Used in Financing Activities

The above figure clearly indicates that the operating cash flows have fallen from 2015 to

2017 due to decline in customer receipts. However, huge expenses incurred for property, plant

and equipment have increased the investing cash flows for Ausdrill Limited. On the other hand,

financing cash flows have fallen in 2017 from 2015 due to no expenses incurred in repaying

secured borrowings (Ausdrill.com.au 2018).

Question (vi):

Based on the above analysis, it could be stated that BHP Billiton has earned maximum

amount from operating cash flows followed by Rio Tinto and Ausdrill Limited, even though the

trend is declining over the years. It could be witnessed that all organisations are involved in

investment of buying property, plant and equipment, intangibles and other business acquisitions.

When all the aspects are combined together, it could be observed that they have made huge

investments. Finally, the three organisations have incurred huge expenses for interest, finance

costs and dividends, which have resulted in increased cash flows.

14CORPORATE ACCOUNTING

Other comprehensive income statement:

Question (vii):

From the annual reports of BHP Billiton, the main items reported in other comprehensive

income statement include available for sale investment, cash flow hedge and the items that could

not be reclassified to the income statement (BHP 2018).

For Rio Tinto, the main items included in its other comprehensive income statement are

cash flow hedges, foreign currency translation reserves, profit or loss on foreign operation

transactions and others (Riotinto.com 2018).

Ausdrill Limited has reported certain items in its other comprehensive income statement

that include foreign currency translation, net exchange differences, non-controlling interests and

others (Ausdrill.com.au 2018).

Question (viii):

The three organisations have not recorded the above-mentioned items in other

comprehensive income statement, as their nature is extraordinary and they are not used for

carrying out their daily business operations. The organisations use them for disclosing their

business activities during the year (Black 2016). Therefore, these reasons prevent the

organisations to report the items in their income statement for which comprehensive income

statement is used to report them.

Question (ix):

From the annual reports of the three organisations, cash flow hedges are common in other

comprehensive income statement. Rio Tinto has registered the highest other comprehensive

Other comprehensive income statement:

Question (vii):

From the annual reports of BHP Billiton, the main items reported in other comprehensive

income statement include available for sale investment, cash flow hedge and the items that could

not be reclassified to the income statement (BHP 2018).

For Rio Tinto, the main items included in its other comprehensive income statement are

cash flow hedges, foreign currency translation reserves, profit or loss on foreign operation

transactions and others (Riotinto.com 2018).

Ausdrill Limited has reported certain items in its other comprehensive income statement

that include foreign currency translation, net exchange differences, non-controlling interests and

others (Ausdrill.com.au 2018).

Question (viii):

The three organisations have not recorded the above-mentioned items in other

comprehensive income statement, as their nature is extraordinary and they are not used for

carrying out their daily business operations. The organisations use them for disclosing their

business activities during the year (Black 2016). Therefore, these reasons prevent the

organisations to report the items in their income statement for which comprehensive income

statement is used to report them.

Question (ix):

From the annual reports of the three organisations, cash flow hedges are common in other

comprehensive income statement. Rio Tinto has registered the highest other comprehensive

15CORPORATE ACCOUNTING

income followed by Rio Tinto and Ausdrill Limited, as identified from their annual reports.

Moreover, it could be seen that these organisations have taken into consideration foreign

currency translation transactions in their other comprehensive income statement. These have

resulted in attributing income to non-controlling interests as well as shareholders of the

organisation (Bratten, Causholli and Khan 2016).

Therefore, if these items are recorded in the income statements of the three chosen

organisations, the impact would be on net profit directly with increase or decline in extraordinary

items. This clearly implies that the profitability aspects of the organisation would be affected by

inclusion of these items in other comprehensive income statement (Graham and Lin 2018).

Question (x):

The performance of entities need not depend on comprehensive business items, as they

are depicted characteristically in their annual reports. Moreover, it is evident that these items are

extraordinary and periodic in nature. Furthermore, the items incorporated in other comprehensive

income statement are mainly extraordinary in nature. Hence, when all these aspects are present,

the management of the business organisations need not use other comprehensive income for

analysing the performance of the managers (Khan, Bradbury and Courtenay 2018).

Accounting for corporate income tax:

Question (xi):

The annual reports of the organisation have disclosed the tax expenses incurred for both

the existing year and the previous year. Based on the annual report of BHP Billiton in 2017, the

organisation has incurred income tax expense of $3,933 million in 2017, while it has received

income followed by Rio Tinto and Ausdrill Limited, as identified from their annual reports.

Moreover, it could be seen that these organisations have taken into consideration foreign

currency translation transactions in their other comprehensive income statement. These have

resulted in attributing income to non-controlling interests as well as shareholders of the

organisation (Bratten, Causholli and Khan 2016).

Therefore, if these items are recorded in the income statements of the three chosen

organisations, the impact would be on net profit directly with increase or decline in extraordinary

items. This clearly implies that the profitability aspects of the organisation would be affected by

inclusion of these items in other comprehensive income statement (Graham and Lin 2018).

Question (x):

The performance of entities need not depend on comprehensive business items, as they

are depicted characteristically in their annual reports. Moreover, it is evident that these items are

extraordinary and periodic in nature. Furthermore, the items incorporated in other comprehensive

income statement are mainly extraordinary in nature. Hence, when all these aspects are present,

the management of the business organisations need not use other comprehensive income for

analysing the performance of the managers (Khan, Bradbury and Courtenay 2018).

Accounting for corporate income tax:

Question (xi):

The annual reports of the organisation have disclosed the tax expenses incurred for both

the existing year and the previous year. Based on the annual report of BHP Billiton in 2017, the

organisation has incurred income tax expense of $3,933 million in 2017, while it has received

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16CORPORATE ACCOUNTING

income tax benefit of $1,297 million in 2016. Thus, it has experienced increase in tax expense in

2017 (BHP 2018).

As observed from the 2017 annual report of Rio Tinto, the income tax expense of the

organisation has been $3,965 million in 2017 compared to $1,567 million in 2016, which

signifies that the tax amount has increased considerably over the year (Riotinto.com 2018).

The 2017 annual report of Ausdrill Limited discloses income tax expense of $13,885,000

in 2017 in contrast to $4,581,000 in 2016. This denotes that the organisation has experienced

significant increase in tax expense in 2017 like the other two organisations (Ausdrill.com.au

2018).

Question (xii):

In order to compute the effective tax rate of BHP Billiton, Rio Tinto and Ausdrill

Limited, the following calculation is performed, which is shown in the form of a table as follows:

The effective tax rate of the organisations implies the average tax rate, which they use for

computing the taxable amount on business profit (Richardson, Taylor and Lanis 2015). By

dividing the earnings before tax by income tax expense, effective tax rate is considered. The

above table clearly shows that BHP Billiton has incurred the highest effective tax rate followed

by Rio Tinto and Ausdrill Limited.

income tax benefit of $1,297 million in 2016. Thus, it has experienced increase in tax expense in

2017 (BHP 2018).

As observed from the 2017 annual report of Rio Tinto, the income tax expense of the

organisation has been $3,965 million in 2017 compared to $1,567 million in 2016, which

signifies that the tax amount has increased considerably over the year (Riotinto.com 2018).

The 2017 annual report of Ausdrill Limited discloses income tax expense of $13,885,000

in 2017 in contrast to $4,581,000 in 2016. This denotes that the organisation has experienced

significant increase in tax expense in 2017 like the other two organisations (Ausdrill.com.au

2018).

Question (xii):

In order to compute the effective tax rate of BHP Billiton, Rio Tinto and Ausdrill

Limited, the following calculation is performed, which is shown in the form of a table as follows:

The effective tax rate of the organisations implies the average tax rate, which they use for

computing the taxable amount on business profit (Richardson, Taylor and Lanis 2015). By

dividing the earnings before tax by income tax expense, effective tax rate is considered. The

above table clearly shows that BHP Billiton has incurred the highest effective tax rate followed

by Rio Tinto and Ausdrill Limited.

17CORPORATE ACCOUNTING

Question (xiii):

One of the most vital aspects for financial reporting of business organisations is deferred

tax assets and liabilities and the organisations are liable to disclose the amounts in their financial

statements at the end of an accounting period (Dyreng, Hoopes and Wilde 2016). From the

annual reports of BHP Billiton, Rio Tinto and Ausdrill Limited, it could be seen that they have

disclosed the amounts of deferred tax assets and deferred tax liabilities supported by financial

footnotes. The main reason that these items are recorded is that provisional variation exists

between tax profit and accounting profit. Another reason that supports their inclusion in the

financial reports includes carry forward of tax assets and tax liabilities in the existing year from

the previous period (Anesa et al. 2018).

Question (xiv):

From the annual report of BHP Billiton in 2017, it is found that deferred tax assets

amount to $5,788 million in 2017, which have been $6,147 million in 2016. Hence, there is

downfall in the amount of deferred tax assets. On the other hand, the organisation has deferred

tax liabilities of $3,765 million in 2017 compared to $4,324 million in 2016 implying decline in

the same (BHP 2018).

From the annual report of Rio Tinto in 2017, the amount of deferred tax assets has been

$3,395 million in 2017 compared to $3,728 million in 2016. On the other hand, deferred tax

liabilities have increased from $3,121 million in 2016 to $3,628 million in 2017 (Riotinto.com

2018).

Question (xiii):

One of the most vital aspects for financial reporting of business organisations is deferred

tax assets and liabilities and the organisations are liable to disclose the amounts in their financial

statements at the end of an accounting period (Dyreng, Hoopes and Wilde 2016). From the

annual reports of BHP Billiton, Rio Tinto and Ausdrill Limited, it could be seen that they have

disclosed the amounts of deferred tax assets and deferred tax liabilities supported by financial

footnotes. The main reason that these items are recorded is that provisional variation exists

between tax profit and accounting profit. Another reason that supports their inclusion in the

financial reports includes carry forward of tax assets and tax liabilities in the existing year from

the previous period (Anesa et al. 2018).

Question (xiv):

From the annual report of BHP Billiton in 2017, it is found that deferred tax assets

amount to $5,788 million in 2017, which have been $6,147 million in 2016. Hence, there is

downfall in the amount of deferred tax assets. On the other hand, the organisation has deferred

tax liabilities of $3,765 million in 2017 compared to $4,324 million in 2016 implying decline in

the same (BHP 2018).

From the annual report of Rio Tinto in 2017, the amount of deferred tax assets has been

$3,395 million in 2017 compared to $3,728 million in 2016. On the other hand, deferred tax

liabilities have increased from $3,121 million in 2016 to $3,628 million in 2017 (Riotinto.com

2018).

18CORPORATE ACCOUNTING

As per the 2017 annual report of Ausdrill Limited, deferred tax assets have been

$36,372,000 in 2017 in contrast to $37,300,000 million. On the contrary, deferred tax liabilities

are observed to fall from $23,584,000 in 2016 to $22,077,000 in 2017 (Ausdrill.com.au 2018).

Question (xv):

Question (xvi):

From the above table, it could be seen that Rio Tinto has the highest cash tax rate of

31.08% followed by BHP Billiton and Ausdrill Limited having cash tax rates of 30.73% and

29.21% respectively.

Question (xvii):

The main reason that the cash tax rate and the book tax rate do not resemble each other is

that the organisations project the cash tax rate depending on the existing year. However, the

estimation of book tax rate is conducted depending on the existing and the upcoming year

(Taylor and Richardson 2014). When cash tax rate is computed, the deferred tax assets, deferred

tax liabilities and weight of interest are taken into consideration, which could result in tax

As per the 2017 annual report of Ausdrill Limited, deferred tax assets have been

$36,372,000 in 2017 in contrast to $37,300,000 million. On the contrary, deferred tax liabilities

are observed to fall from $23,584,000 in 2016 to $22,077,000 in 2017 (Ausdrill.com.au 2018).

Question (xv):

Question (xvi):

From the above table, it could be seen that Rio Tinto has the highest cash tax rate of

31.08% followed by BHP Billiton and Ausdrill Limited having cash tax rates of 30.73% and

29.21% respectively.

Question (xvii):

The main reason that the cash tax rate and the book tax rate do not resemble each other is

that the organisations project the cash tax rate depending on the existing year. However, the

estimation of book tax rate is conducted depending on the existing and the upcoming year

(Taylor and Richardson 2014). When cash tax rate is computed, the deferred tax assets, deferred

tax liabilities and weight of interest are taken into consideration, which could result in tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19CORPORATE ACCOUNTING

savings. However, in order to compute the book tax rate, the above items are not taken into

consideration (Kawano and Slemrod 2016).

Conclusion:

From the above discussion, it is clear that all the three organisations comprising of BHP

Billiton, Rio Tinto and Ausdrill Limited are dependent primarily on debt financing so that

adequate amount is obtained for financing the business operations. Moreover, it could be

witnessed that these organisations collect considerable cash amounts from the customers and

they invest heavily for the purchase and repayment of fixed assets, intangible assets and others.

Along with this, it has been analysed that all the three organisations do not consider

extraordinary items in other comprehensive income statement, since they do not have direct

associations with the day-to-day business activities of the organisations. From the taxation

section, it is evident that all the three organisations have to take into account finance costs,

deferred tax assets as well as deferred tax liabilities so that the cash tax rate could be calculated

effectively.

savings. However, in order to compute the book tax rate, the above items are not taken into

consideration (Kawano and Slemrod 2016).

Conclusion:

From the above discussion, it is clear that all the three organisations comprising of BHP

Billiton, Rio Tinto and Ausdrill Limited are dependent primarily on debt financing so that

adequate amount is obtained for financing the business operations. Moreover, it could be

witnessed that these organisations collect considerable cash amounts from the customers and

they invest heavily for the purchase and repayment of fixed assets, intangible assets and others.

Along with this, it has been analysed that all the three organisations do not consider

extraordinary items in other comprehensive income statement, since they do not have direct

associations with the day-to-day business activities of the organisations. From the taxation

section, it is evident that all the three organisations have to take into account finance costs,

deferred tax assets as well as deferred tax liabilities so that the cash tax rate could be calculated

effectively.

20CORPORATE ACCOUNTING

References and Bibliographies:

Anesa, M., Gillespie, N., Spee, A.P. and Sadiq, K., 2018. The legitimation of corporate tax

minimization. Accounting, Organizations and Society, 65(4), pp.137-156.

Ausdrill.com.au., 2018. Annual Reports: Ausdrill. [online] Available at:

http://www.ausdrill.com.au/investors/annual-reports.html [Accessed 31 Dec. 2018].

Ausdrill.com.au., 2018. Home : Ausdrill. [online] Available at: http://www.ausdrill.com.au/

[Accessed 31 Dec. 2018].

BHP., 2018. BHP | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 31 Dec. 2018].

BHP., 2018. BHP | Reports and presentations. [online] Available at:

https://www.bhp.com/media-and-insights/reports-and-presentations?q0_r=category%3DAnnual

%2BReports [Accessed 31 Dec. 2018].

Black, D.E., 2016. Other comprehensive income: a review and directions for future

research. Accounting & Finance, 56(1), pp.9-45.

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315.

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

References and Bibliographies:

Anesa, M., Gillespie, N., Spee, A.P. and Sadiq, K., 2018. The legitimation of corporate tax

minimization. Accounting, Organizations and Society, 65(4), pp.137-156.

Ausdrill.com.au., 2018. Annual Reports: Ausdrill. [online] Available at:

http://www.ausdrill.com.au/investors/annual-reports.html [Accessed 31 Dec. 2018].

Ausdrill.com.au., 2018. Home : Ausdrill. [online] Available at: http://www.ausdrill.com.au/

[Accessed 31 Dec. 2018].

BHP., 2018. BHP | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 31 Dec. 2018].

BHP., 2018. BHP | Reports and presentations. [online] Available at:

https://www.bhp.com/media-and-insights/reports-and-presentations?q0_r=category%3DAnnual

%2BReports [Accessed 31 Dec. 2018].

Black, D.E., 2016. Other comprehensive income: a review and directions for future

research. Accounting & Finance, 56(1), pp.9-45.

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315.

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

21CORPORATE ACCOUNTING

Collins, D.W., Hribar, P. and Tian, X.S., 2014. Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics, 58(2-3), pp.173-

200.

Dowling, G.R., 2014. The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), pp.173-184.

Dyreng, S.D., Hoopes, J.L. and Wilde, J.H., 2016. Public pressure and corporate tax

behavior. Journal of Accounting Research, 54(1), pp.147-186.

Gordon, E.A., Henry, E., Jorgensen, B.N. and Linthicum, C.L., 2017. Flexibility in cash-flow

classification under IFRS: determinants and consequences. Review of Accounting Studies, 22(2),

pp.839-872.

Graham, R.C. and Lin, K.C., 2018. The influence of other comprehensive income on

discretionary expenditures. Journal of Business Finance & Accounting, 45(1-2), pp.72-91.

Kawano, L. and Slemrod, J., 2016. How do corporate tax bases change when corporate tax rates

change? With implications for the tax rate elasticity of corporate tax revenues. International Tax

and Public Finance, 23(3), pp.401-433.

Khan, S., Bradbury, M.E. and Courtenay, S., 2018. Value Relevance of Comprehensive

Income. Australian Accounting Review, 28(2), pp.279-287.

Khansalar, E. and Namazi, M., 2017. Cash flow disaggregation and prediction of cash

flow. Journal of Applied Accounting Research, 18(4), pp.464-479.

Marshall, D., 2016. Accounting: what the numbers mean. McGraw-Hill Higher Education.

Collins, D.W., Hribar, P. and Tian, X.S., 2014. Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics, 58(2-3), pp.173-

200.

Dowling, G.R., 2014. The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), pp.173-184.

Dyreng, S.D., Hoopes, J.L. and Wilde, J.H., 2016. Public pressure and corporate tax

behavior. Journal of Accounting Research, 54(1), pp.147-186.

Gordon, E.A., Henry, E., Jorgensen, B.N. and Linthicum, C.L., 2017. Flexibility in cash-flow

classification under IFRS: determinants and consequences. Review of Accounting Studies, 22(2),

pp.839-872.

Graham, R.C. and Lin, K.C., 2018. The influence of other comprehensive income on

discretionary expenditures. Journal of Business Finance & Accounting, 45(1-2), pp.72-91.

Kawano, L. and Slemrod, J., 2016. How do corporate tax bases change when corporate tax rates

change? With implications for the tax rate elasticity of corporate tax revenues. International Tax

and Public Finance, 23(3), pp.401-433.

Khan, S., Bradbury, M.E. and Courtenay, S., 2018. Value Relevance of Comprehensive

Income. Australian Accounting Review, 28(2), pp.279-287.

Khansalar, E. and Namazi, M., 2017. Cash flow disaggregation and prediction of cash

flow. Journal of Applied Accounting Research, 18(4), pp.464-479.

Marshall, D., 2016. Accounting: what the numbers mean. McGraw-Hill Higher Education.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22CORPORATE ACCOUNTING

Miller-Nobles, T.L., Mattison, B. and Matsumura, E.M., 2016. Horngren's Financial &

Managerial Accounting: The Managerial Chapters. Pearson.

Öztürk, C., 2015. Some issues related to cash flow statement in accounting education: The case

of Turkey. Accounting and Management Information Systems, 14(2), p.398.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Richardson, G., Taylor, G. and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, pp.44-53.

Rimmer, X., Smith, J. and Wende, S., 2014. The incidence of company tax in

Australia. Economic Round-up, 109(1), pp.33-42.

Riotinto.com., 2018. Global home. [online] Available at: https://www.riotinto.com/ [Accessed 31

Dec. 2018].

Riotinto.com., 2018. Results & reports. [online] Available at:

https://www.riotinto.com/investors/results-and-reports-2146.aspx [Accessed 31 Dec. 2018].

Taylor, G. and Richardson, G., 2014. Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting & Economics, 10(1),

pp.1-15.

Miller-Nobles, T.L., Mattison, B. and Matsumura, E.M., 2016. Horngren's Financial &

Managerial Accounting: The Managerial Chapters. Pearson.

Öztürk, C., 2015. Some issues related to cash flow statement in accounting education: The case

of Turkey. Accounting and Management Information Systems, 14(2), p.398.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Richardson, G., Taylor, G. and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, pp.44-53.

Rimmer, X., Smith, J. and Wende, S., 2014. The incidence of company tax in

Australia. Economic Round-up, 109(1), pp.33-42.

Riotinto.com., 2018. Global home. [online] Available at: https://www.riotinto.com/ [Accessed 31

Dec. 2018].

Riotinto.com., 2018. Results & reports. [online] Available at:

https://www.riotinto.com/investors/results-and-reports-2146.aspx [Accessed 31 Dec. 2018].

Taylor, G. and Richardson, G., 2014. Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting & Economics, 10(1),

pp.1-15.

1 out of 23

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.