Corporate Finance: Analysis of Bond, Share Prices, and Project NPV

VerifiedAdded on 2020/05/28

|8

|1388

|63

Homework Assignment

AI Summary

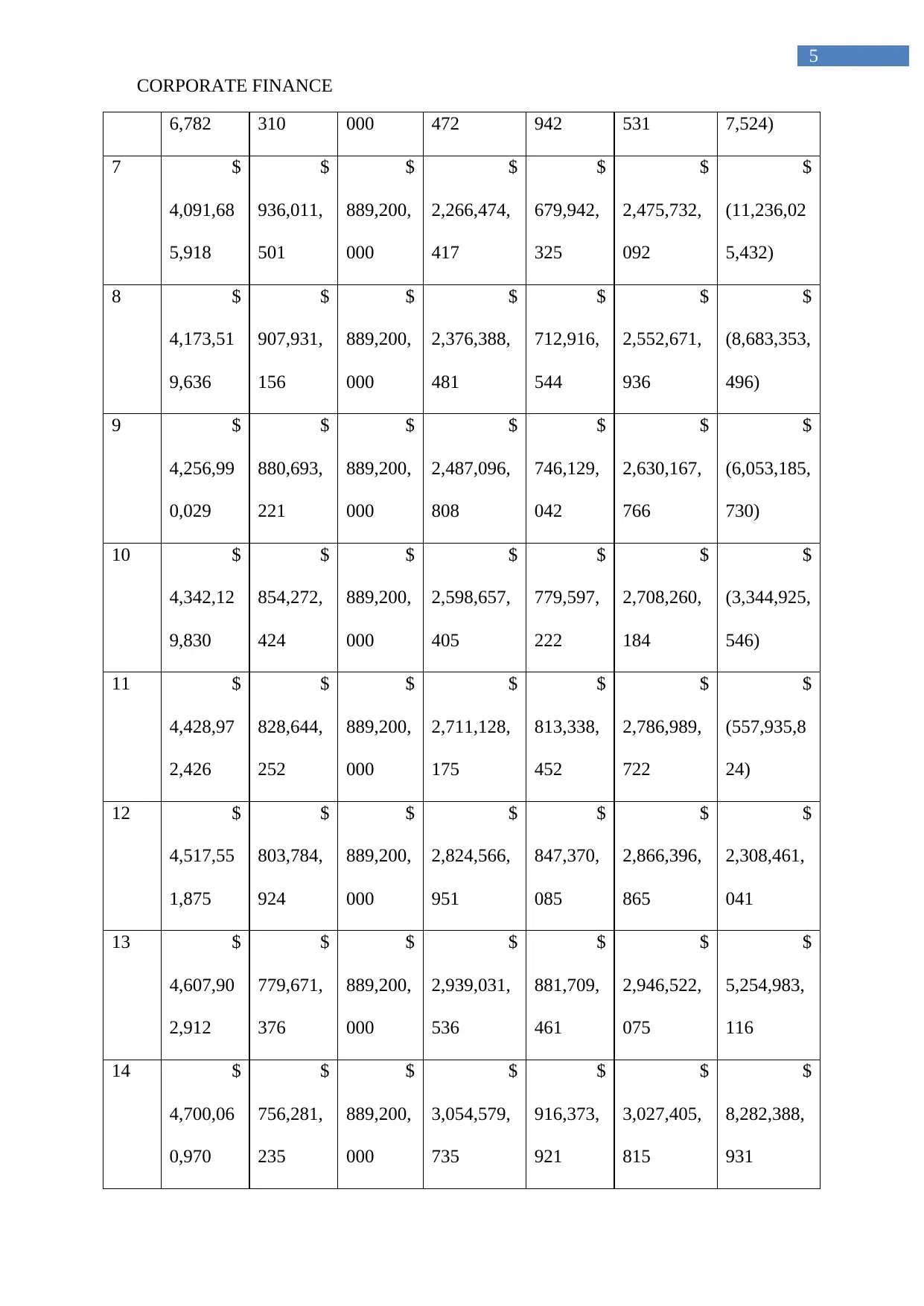

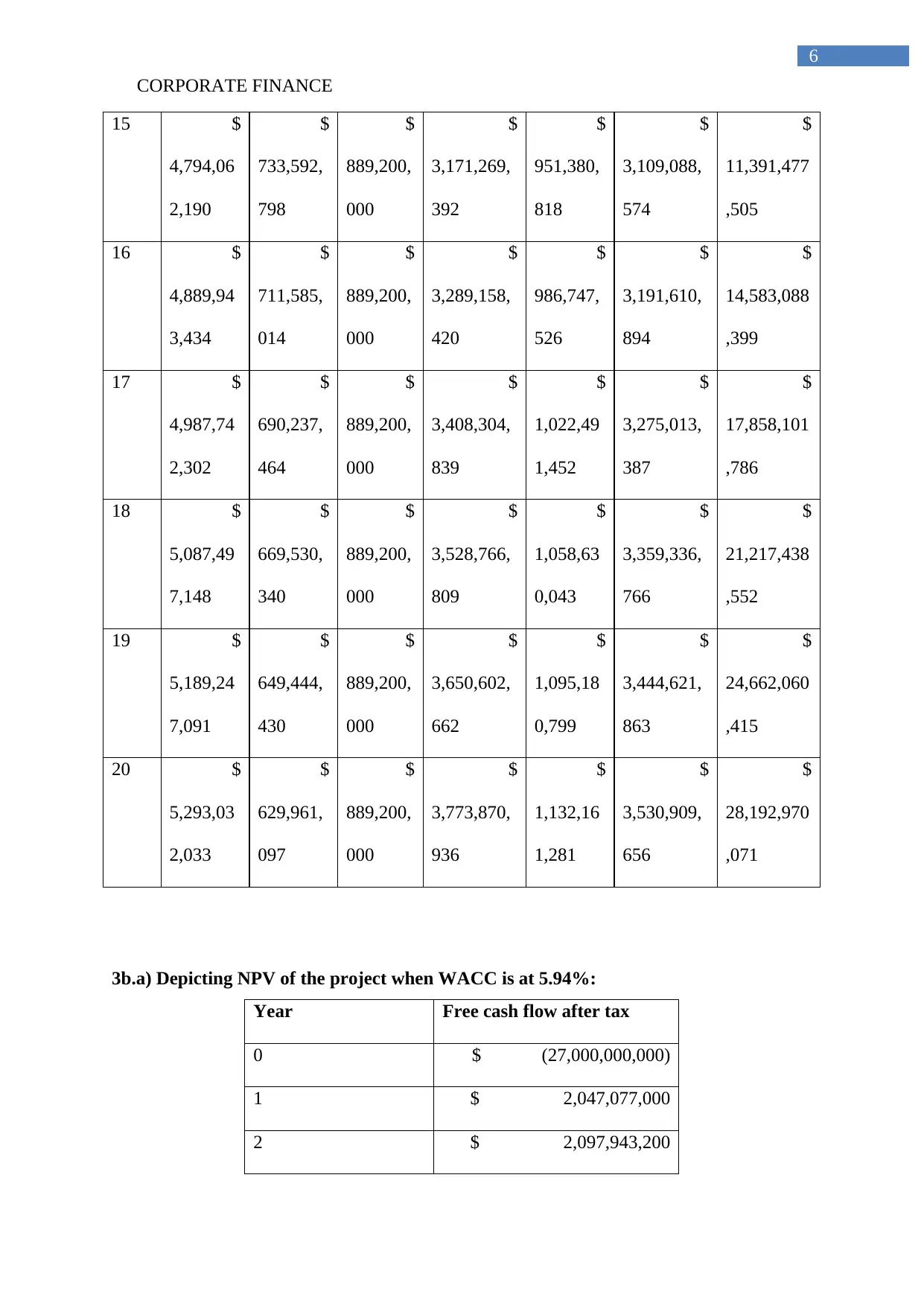

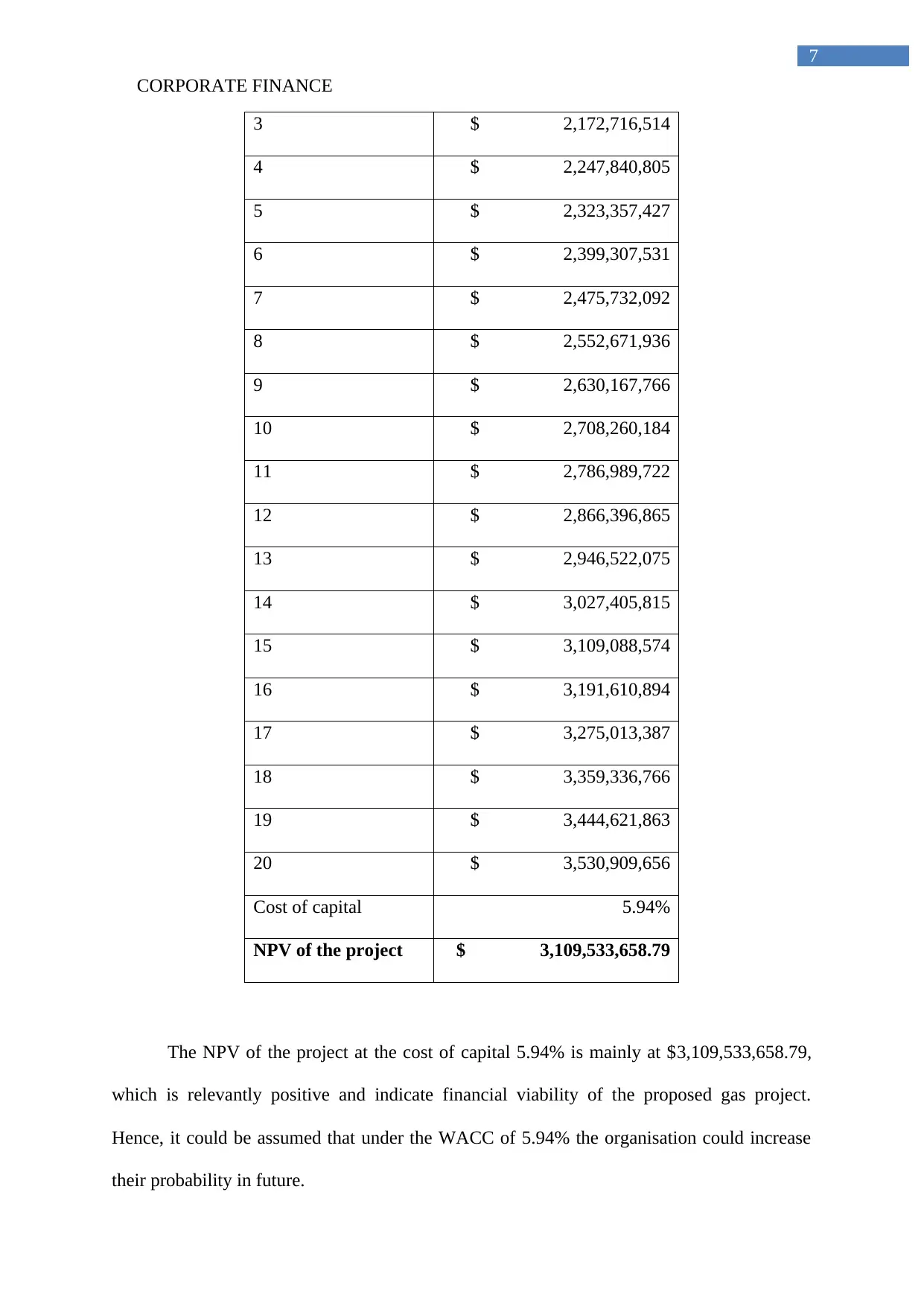

This assignment delves into key aspects of corporate finance, offering a detailed analysis of bond valuation, share price determination, and project Net Present Value (NPV) calculations. The analysis begins with the calculation of a bond price, considering factors such as face value, coupon rate, yield rate, and the number of coupon payments. It then compares the calculated bond price to the par value, explaining the reasons behind any discrepancies, such as the impact of changing yield rates. The assignment further extends to the valuation of Shell's current share price in euros, using data like the EUR to USD exchange rate, market return, risk-free rate, annual dividend, and growth rate to determine the cost of capital. The assignment also includes a detailed Free Cash Flow (FCF) analysis for a gas project, projecting incremental revenue, costs, depreciation, and taxes over a 20-year period to arrive at the FCF and cumulative cash flow. Finally, the project's NPV is calculated under different Weighted Average Cost of Capital (WACC) scenarios (5.94% and 8%), providing insights into the project's financial viability. The analysis concludes with a discussion of the project's profitability based on the NPV results, offering recommendations for investment decisions. The student references several academic sources to support the financial analysis and conclusions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.