Corporate Finance: Origin Energy WACC and Gearing Analysis

VerifiedAdded on 2021/05/31

|16

|2810

|87

Report

AI Summary

This report provides a comprehensive analysis of corporate finance principles, focusing on the Weighted Average Cost of Capital (WACC), gearing ratios, and capital structure. It begins with a calculation of WACC for Origin Energy Limited, detailing the cost of equity and cost of debt, and explaining how these components are combined. The report then explores the company's capital structure, including the weights of debt and equity, and calculates various gearing ratios like interest coverage ratio, debt to equity ratio, debt ratio, and equity ratio. The report discusses the difficulties associated with gearing ratios and the impact of high leverage. It delves into capital structure theory, comparing traditional approaches and highlighting the importance of finding an optimal capital structure to minimize WACC. Finally, the report offers recommendations for Origin Energy Limited's capital structure, weighing the pros and cons of debt and equity financing to guide the company's financial strategy.

Running Head: CORPORATE FINANCE 0

Corporate Finance

Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 1

Table of Contents

Introduction................................................................................................................................1

Answer to Question 1.............................................................................................................2

Answer to Question-2................................................................................................................5

Overview................................................................................................................................5

Weights...................................................................................................................................5

Cost of Equity.........................................................................................................................6

Cost of Debt............................................................................................................................6

Answer to Question-3................................................................................................................7

Calculation of Gearing Ratios................................................................................................7

Difficulties..............................................................................................................................8

Answer to Question-4................................................................................................................9

Capital Structure Theory........................................................................................................9

Answer to Question-5..............................................................................................................10

Recommendations................................................................................................................10

Pros...................................................................................................................................11

Cons..................................................................................................................................11

Pros...................................................................................................................................12

Cons..................................................................................................................................12

Conclusion................................................................................................................................12

Bibliography.............................................................................................................................13

Articles/Books/Journal.........................................................................................................13

Others...................................................................................................................................14

Table of Contents

Introduction................................................................................................................................1

Answer to Question 1.............................................................................................................2

Answer to Question-2................................................................................................................5

Overview................................................................................................................................5

Weights...................................................................................................................................5

Cost of Equity.........................................................................................................................6

Cost of Debt............................................................................................................................6

Answer to Question-3................................................................................................................7

Calculation of Gearing Ratios................................................................................................7

Difficulties..............................................................................................................................8

Answer to Question-4................................................................................................................9

Capital Structure Theory........................................................................................................9

Answer to Question-5..............................................................................................................10

Recommendations................................................................................................................10

Pros...................................................................................................................................11

Cons..................................................................................................................................11

Pros...................................................................................................................................12

Cons..................................................................................................................................12

Conclusion................................................................................................................................12

Bibliography.............................................................................................................................13

Articles/Books/Journal.........................................................................................................13

Others...................................................................................................................................14

CORPORATE FINANCE 2

Introduction

WACC is the simple weighted average cost of equity and cost of the debt. The combination

of both is necessary to keep the capital structure of the company with full of variety and

leverage against tax and interest component. Under this paper a detailed analysis of the

WACC of the Origin Energy Limited has been conducted along with the relevant gearing

ratios and optimal capital structure formation.

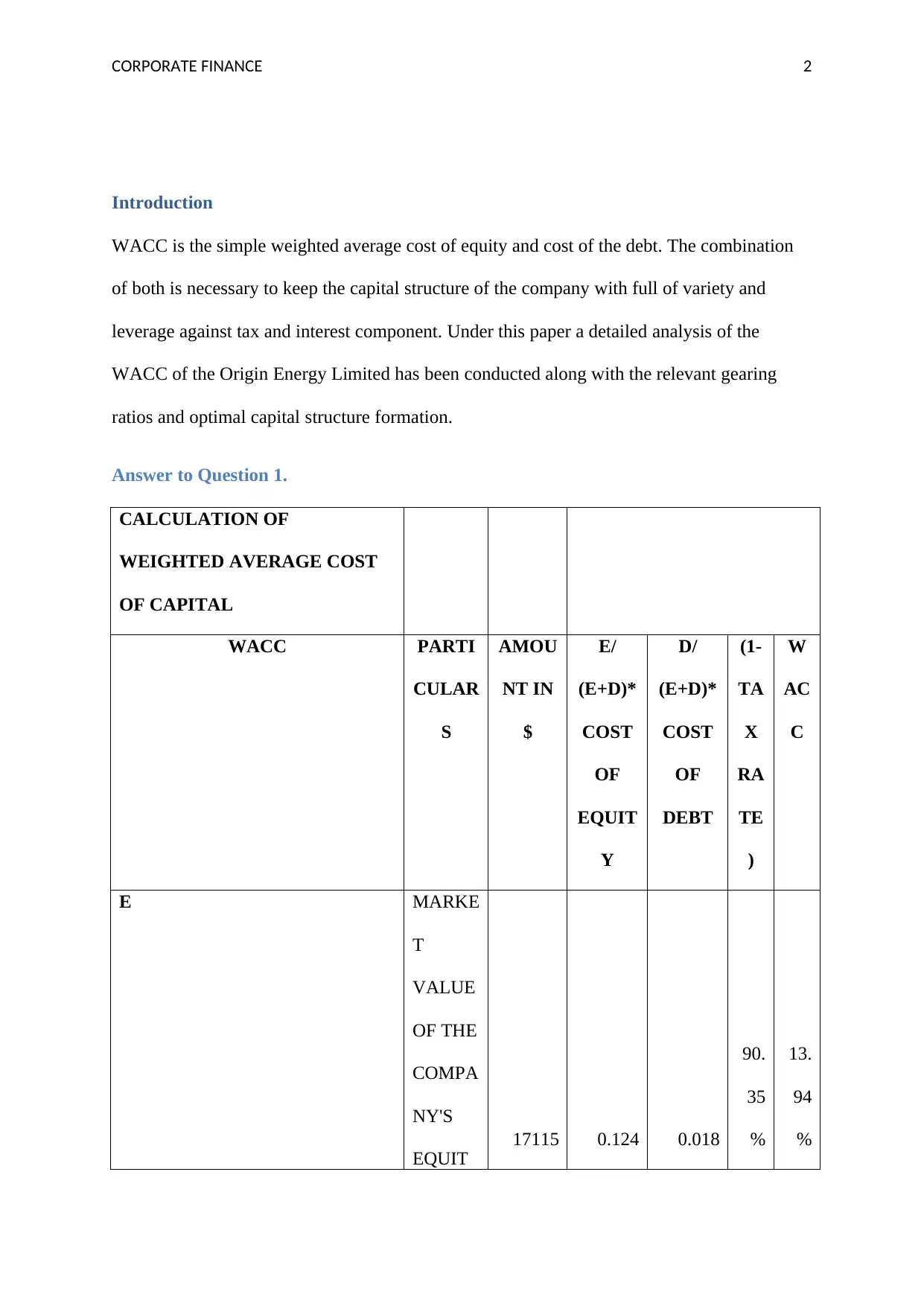

Answer to Question 1.

CALCULATION OF

WEIGHTED AVERAGE COST

OF CAPITAL

WACC PARTI

CULAR

S

AMOU

NT IN

$

E/

(E+D)*

COST

OF

EQUIT

Y

D/

(E+D)*

COST

OF

DEBT

(1-

TA

X

RA

TE

)

W

AC

C

E MARKE

T

VALUE

OF THE

COMPA

NY'S

EQUIT

17115 0.124 0.018

90.

35

%

13.

94

%

Introduction

WACC is the simple weighted average cost of equity and cost of the debt. The combination

of both is necessary to keep the capital structure of the company with full of variety and

leverage against tax and interest component. Under this paper a detailed analysis of the

WACC of the Origin Energy Limited has been conducted along with the relevant gearing

ratios and optimal capital structure formation.

Answer to Question 1.

CALCULATION OF

WEIGHTED AVERAGE COST

OF CAPITAL

WACC PARTI

CULAR

S

AMOU

NT IN

$

E/

(E+D)*

COST

OF

EQUIT

Y

D/

(E+D)*

COST

OF

DEBT

(1-

TA

X

RA

TE

)

W

AC

C

E MARKE

T

VALUE

OF THE

COMPA

NY'S

EQUIT

17115 0.124 0.018

90.

35

%

13.

94

%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 3

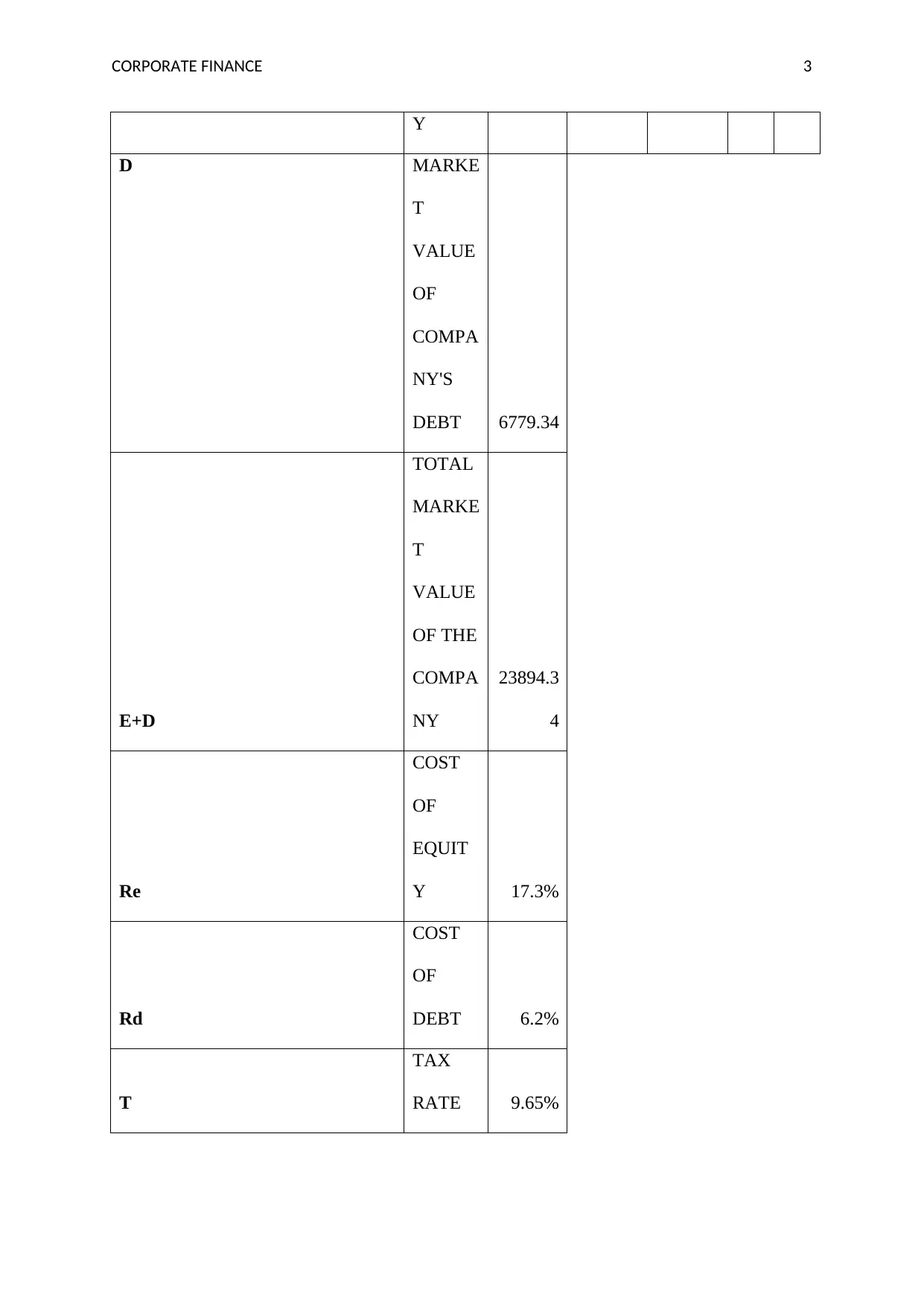

Y

D MARKE

T

VALUE

OF

COMPA

NY'S

DEBT 6779.34

E+D

TOTAL

MARKE

T

VALUE

OF THE

COMPA

NY

23894.3

4

Re

COST

OF

EQUIT

Y 17.3%

Rd

COST

OF

DEBT 6.2%

T

TAX

RATE 9.65%

Y

D MARKE

T

VALUE

OF

COMPA

NY'S

DEBT 6779.34

E+D

TOTAL

MARKE

T

VALUE

OF THE

COMPA

NY

23894.3

4

Re

COST

OF

EQUIT

Y 17.3%

Rd

COST

OF

DEBT 6.2%

T

TAX

RATE 9.65%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

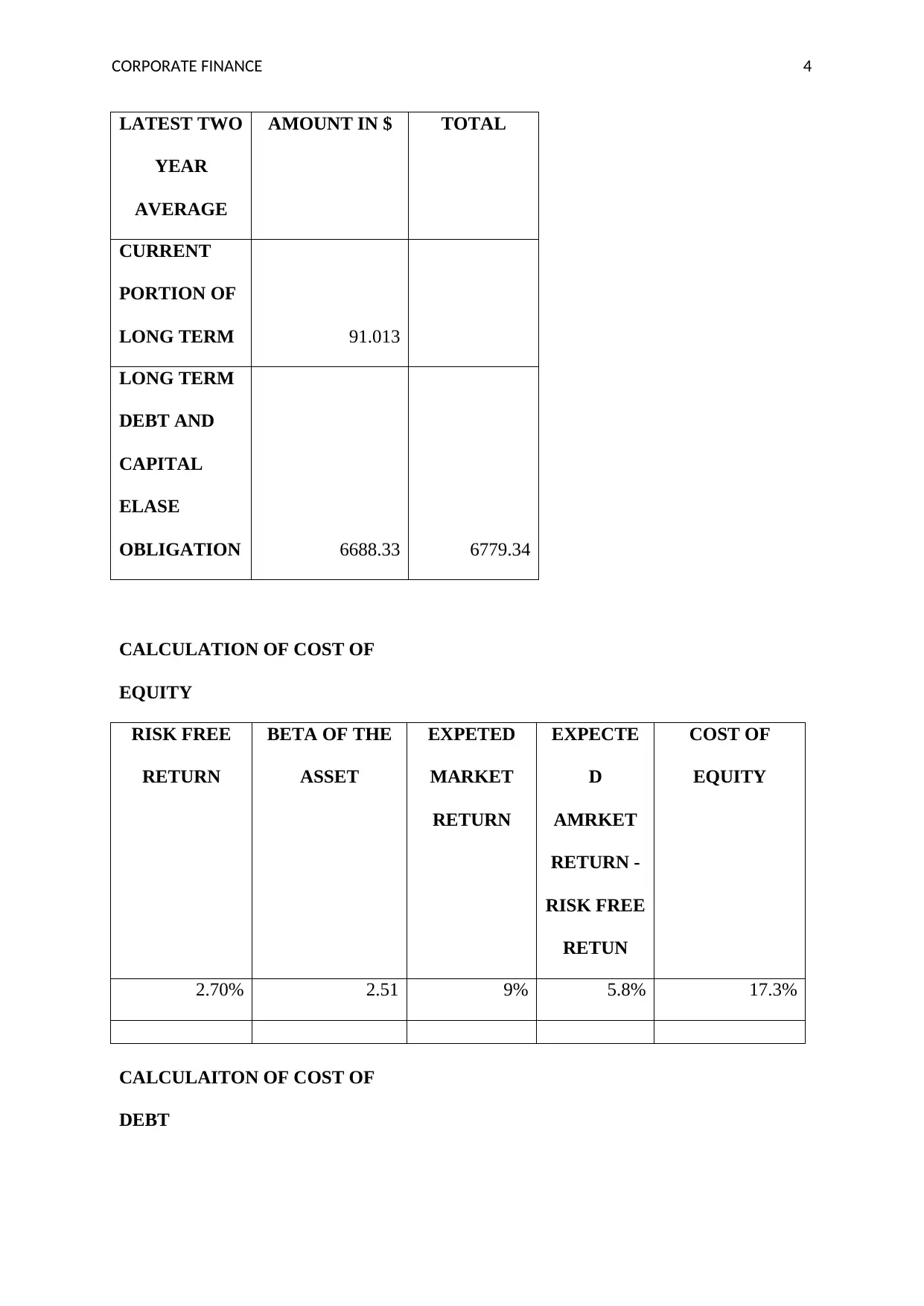

CORPORATE FINANCE 4

LATEST TWO

YEAR

AVERAGE

AMOUNT IN $ TOTAL

CURRENT

PORTION OF

LONG TERM 91.013

LONG TERM

DEBT AND

CAPITAL

ELASE

OBLIGATION 6688.33 6779.34

CALCULATION OF COST OF

EQUITY

RISK FREE

RETURN

BETA OF THE

ASSET

EXPETED

MARKET

RETURN

EXPECTE

D

AMRKET

RETURN -

RISK FREE

RETUN

COST OF

EQUITY

2.70% 2.51 9% 5.8% 17.3%

CALCULAITON OF COST OF

DEBT

LATEST TWO

YEAR

AVERAGE

AMOUNT IN $ TOTAL

CURRENT

PORTION OF

LONG TERM 91.013

LONG TERM

DEBT AND

CAPITAL

ELASE

OBLIGATION 6688.33 6779.34

CALCULATION OF COST OF

EQUITY

RISK FREE

RETURN

BETA OF THE

ASSET

EXPETED

MARKET

RETURN

EXPECTE

D

AMRKET

RETURN -

RISK FREE

RETUN

COST OF

EQUITY

2.70% 2.51 9% 5.8% 17.3%

CALCULAITON OF COST OF

DEBT

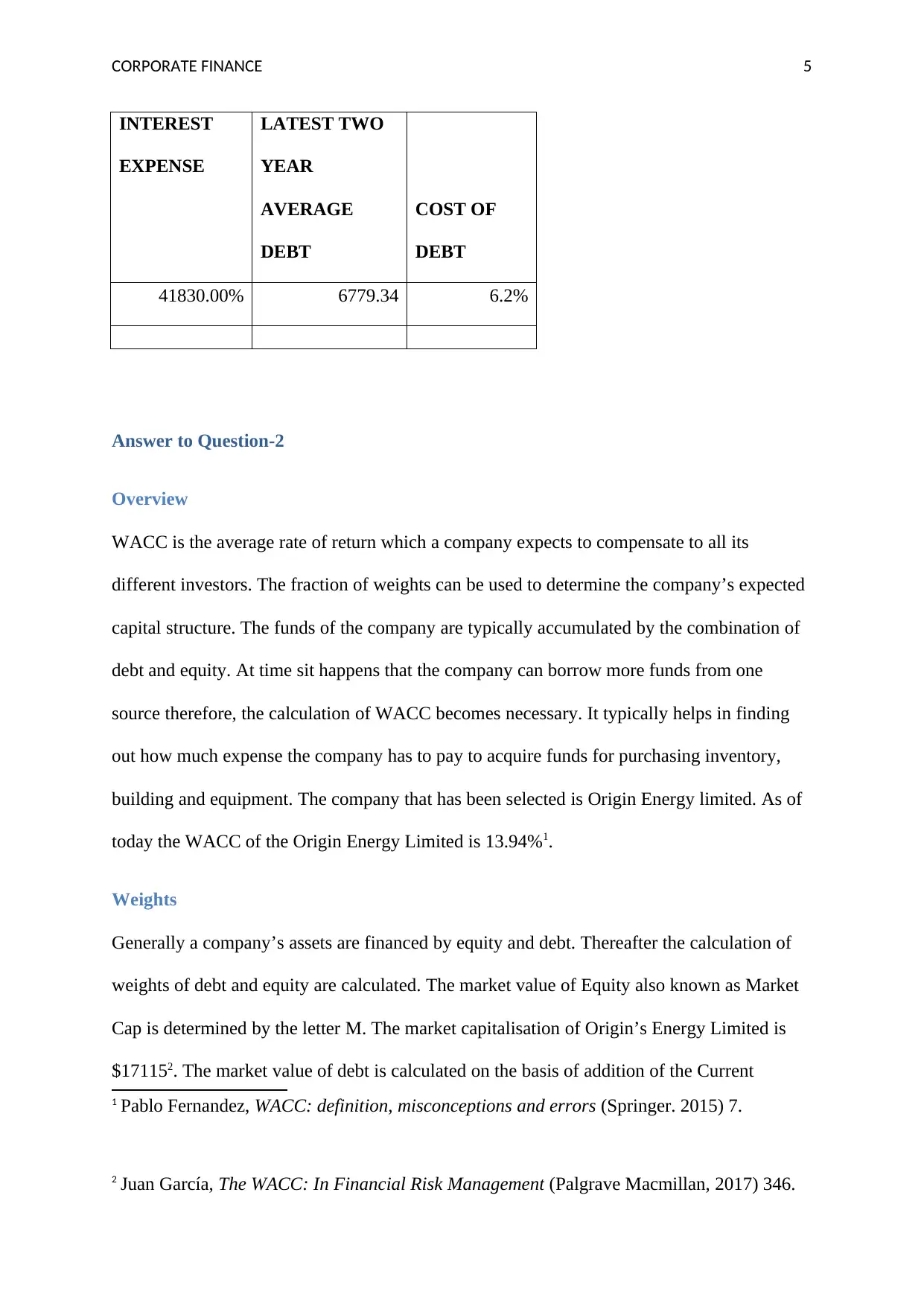

CORPORATE FINANCE 5

INTEREST

EXPENSE

LATEST TWO

YEAR

AVERAGE

DEBT

COST OF

DEBT

41830.00% 6779.34 6.2%

Answer to Question-2

Overview

WACC is the average rate of return which a company expects to compensate to all its

different investors. The fraction of weights can be used to determine the company’s expected

capital structure. The funds of the company are typically accumulated by the combination of

debt and equity. At time sit happens that the company can borrow more funds from one

source therefore, the calculation of WACC becomes necessary. It typically helps in finding

out how much expense the company has to pay to acquire funds for purchasing inventory,

building and equipment. The company that has been selected is Origin Energy limited. As of

today the WACC of the Origin Energy Limited is 13.94%1.

Weights

Generally a company’s assets are financed by equity and debt. Thereafter the calculation of

weights of debt and equity are calculated. The market value of Equity also known as Market

Cap is determined by the letter M. The market capitalisation of Origin’s Energy Limited is

$171152. The market value of debt is calculated on the basis of addition of the Current

1 Pablo Fernandez, WACC: definition, misconceptions and errors (Springer. 2015) 7.

2 Juan García, The WACC: In Financial Risk Management (Palgrave Macmillan, 2017) 346.

INTEREST

EXPENSE

LATEST TWO

YEAR

AVERAGE

DEBT

COST OF

DEBT

41830.00% 6779.34 6.2%

Answer to Question-2

Overview

WACC is the average rate of return which a company expects to compensate to all its

different investors. The fraction of weights can be used to determine the company’s expected

capital structure. The funds of the company are typically accumulated by the combination of

debt and equity. At time sit happens that the company can borrow more funds from one

source therefore, the calculation of WACC becomes necessary. It typically helps in finding

out how much expense the company has to pay to acquire funds for purchasing inventory,

building and equipment. The company that has been selected is Origin Energy limited. As of

today the WACC of the Origin Energy Limited is 13.94%1.

Weights

Generally a company’s assets are financed by equity and debt. Thereafter the calculation of

weights of debt and equity are calculated. The market value of Equity also known as Market

Cap is determined by the letter M. The market capitalisation of Origin’s Energy Limited is

$171152. The market value of debt is calculated on the basis of addition of the Current

1 Pablo Fernandez, WACC: definition, misconceptions and errors (Springer. 2015) 7.

2 Juan García, The WACC: In Financial Risk Management (Palgrave Macmillan, 2017) 346.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 6

Portion of long term liabilities and Long-term Debt & Capital Lease Obligation. The current

portion of long term is $91.013 million and its latest two year average Long Term Debt &

Capital is $6688.33. Therefore the total book value amounts to $6779.34. The information

can be found in the annual report of Origin Energy Limited.

The weight of equity is the company’s overall capital. The weight of Equity = E/(E+D)* Cost

of Equity. It is derived from the addition of Equity and Debt and the same is being divided by

the Equity. The current year’s weight of equity is 0.71 and the current year’s weight of debt is

0.283. The weight of the debt component determines the capital structure of the company. It is

calculated by dividing the debt’s market value by the summation of Equity and Debt. The

weight of Debt = D/(E+D).

Ideally the estimation of WACC is done using the formation of capital structure which the

management tends to keep for the long duration. If the market values are not available then

the book values can be taken to arrive at calculation.

Cost of Equity

In the formula of WACC Re represents the cost of equity which is calculated using the

formula Rf+B(Mr-Rf). Here the Rf represents the Risk free rate of return which is 2.70% of

the Origin Energy Limited. Next the risk free rate of return is subtracted from market rate of

return which is expected at the rate of 9% and is multiplied by the Beta factor to get the

overall cost of equity4.

3 Morningstar, Origin Energy Limited (17th May 2018)

<http://financials.morningstar.com/income-statement/is.html?t=ORG®ion=aus>

4 Phillip Krüger , Augustin Landier & Daniel Thesmar, The WACC fallacy: The real effects

of using a unique discount rate, (2015) 70(3) The Journal of Finance 1253, 1285.

Portion of long term liabilities and Long-term Debt & Capital Lease Obligation. The current

portion of long term is $91.013 million and its latest two year average Long Term Debt &

Capital is $6688.33. Therefore the total book value amounts to $6779.34. The information

can be found in the annual report of Origin Energy Limited.

The weight of equity is the company’s overall capital. The weight of Equity = E/(E+D)* Cost

of Equity. It is derived from the addition of Equity and Debt and the same is being divided by

the Equity. The current year’s weight of equity is 0.71 and the current year’s weight of debt is

0.283. The weight of the debt component determines the capital structure of the company. It is

calculated by dividing the debt’s market value by the summation of Equity and Debt. The

weight of Debt = D/(E+D).

Ideally the estimation of WACC is done using the formation of capital structure which the

management tends to keep for the long duration. If the market values are not available then

the book values can be taken to arrive at calculation.

Cost of Equity

In the formula of WACC Re represents the cost of equity which is calculated using the

formula Rf+B(Mr-Rf). Here the Rf represents the Risk free rate of return which is 2.70% of

the Origin Energy Limited. Next the risk free rate of return is subtracted from market rate of

return which is expected at the rate of 9% and is multiplied by the Beta factor to get the

overall cost of equity4.

3 Morningstar, Origin Energy Limited (17th May 2018)

<http://financials.morningstar.com/income-statement/is.html?t=ORG®ion=aus>

4 Phillip Krüger , Augustin Landier & Daniel Thesmar, The WACC fallacy: The real effects

of using a unique discount rate, (2015) 70(3) The Journal of Finance 1253, 1285.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 7

Cost of Debt

In the formula of WACC Rd represents the cost of debt which is calculated using the formula

of interest expense being divided by the latest two year average debt. The interest expense of

the current year of the Origin’s Energy Limited is 418.30. The latest two year average debt

amounts to 6779.34. After applying the formula the cost of debt comes to 6.2%. But the debt

is generally calculated post tax rate. The after tax return determines the need of the holders of

debt to determine the earnings till maturity. Debt basically offers the tax protection which

means the interest expense reduces the taxes on the debt. This ultimately reduces the cost of

debt.

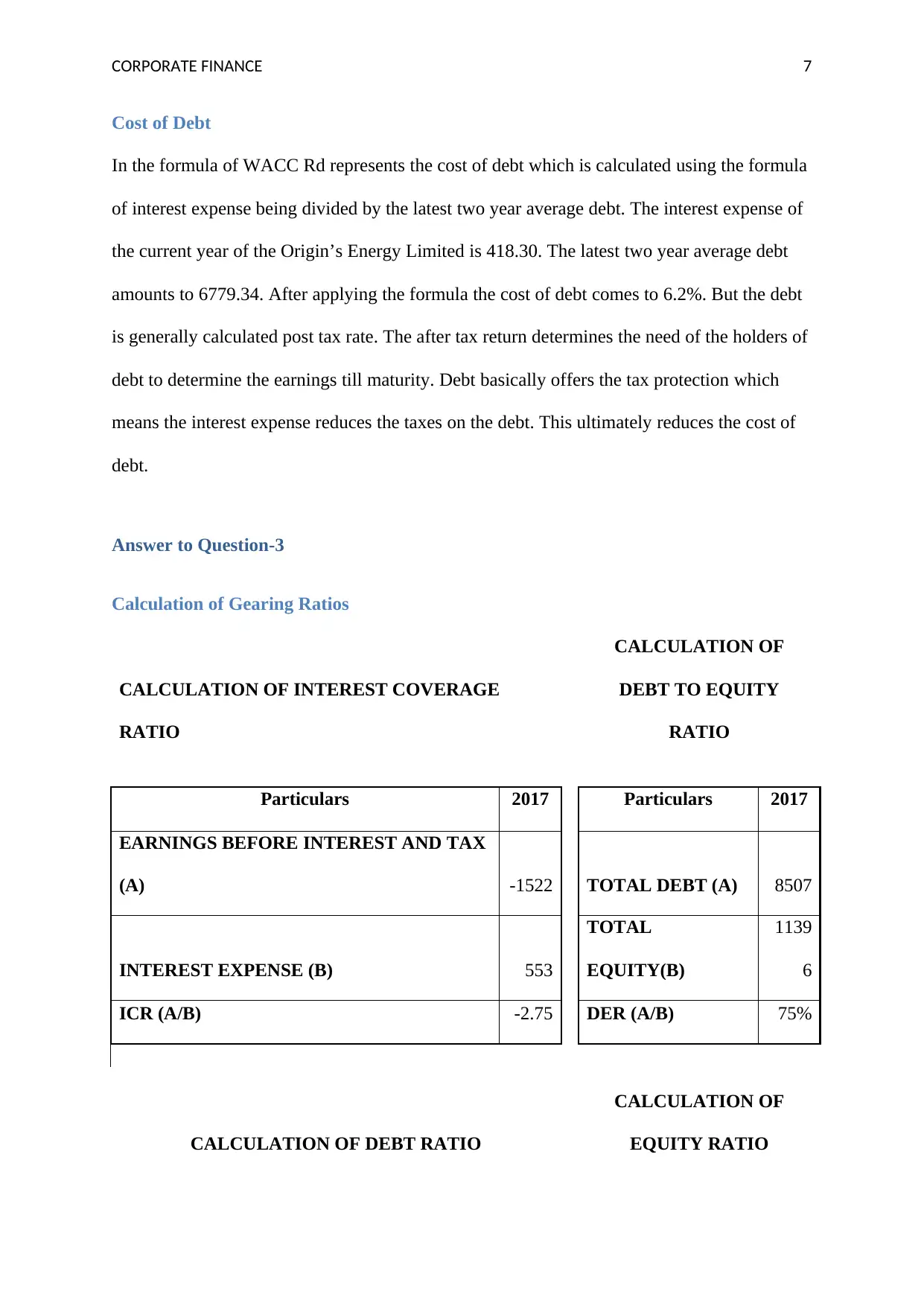

Answer to Question-3

Calculation of Gearing Ratios

CALCULATION OF INTEREST COVERAGE

RATIO

CALCULATION OF

DEBT TO EQUITY

RATIO

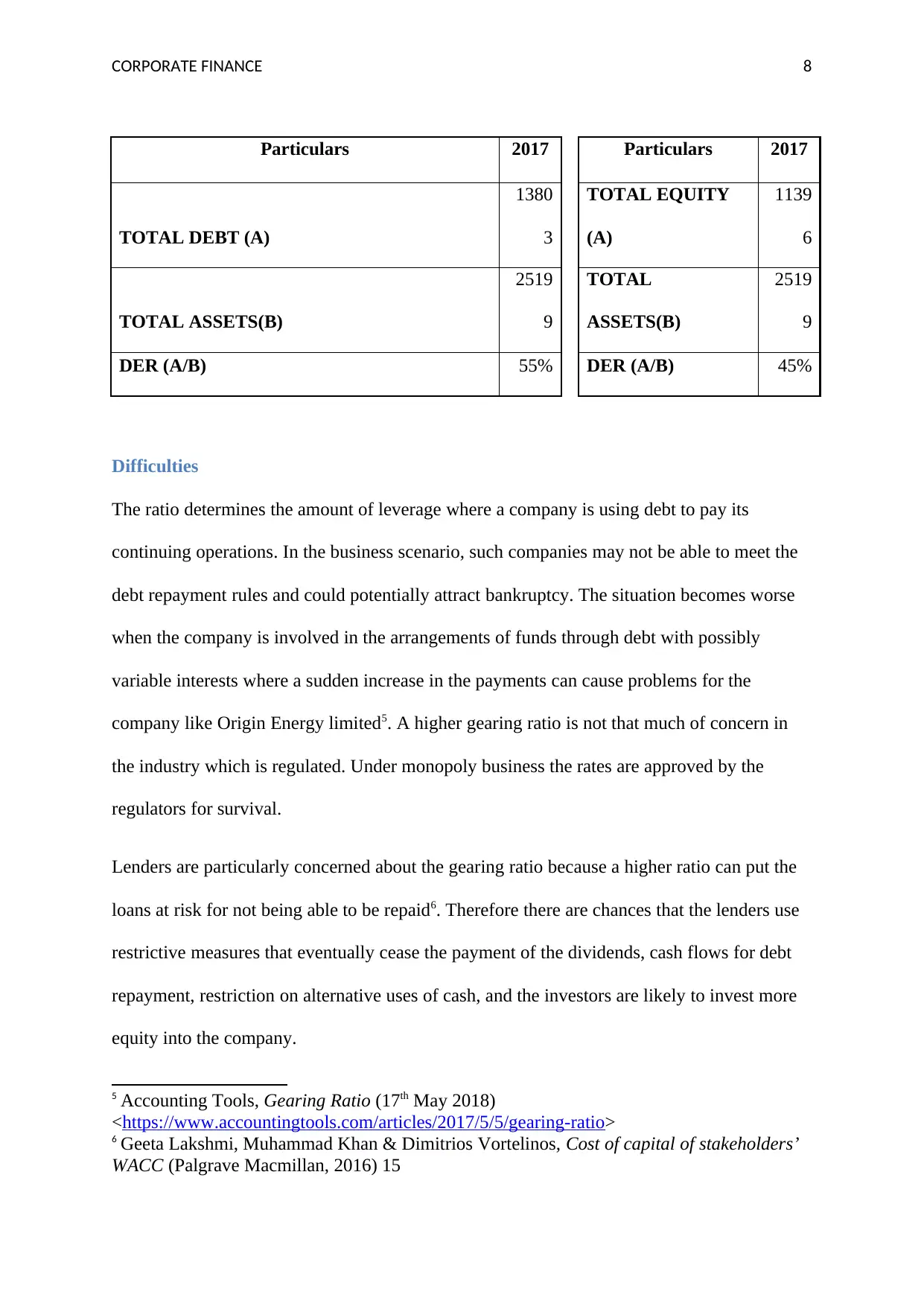

Particulars 2017 Particulars 2017

EARNINGS BEFORE INTEREST AND TAX

(A) -1522 TOTAL DEBT (A) 8507

INTEREST EXPENSE (B) 553

TOTAL

EQUITY(B)

1139

6

ICR (A/B) -2.75 DER (A/B) 75%

CALCULATION OF DEBT RATIO

CALCULATION OF

EQUITY RATIO

Cost of Debt

In the formula of WACC Rd represents the cost of debt which is calculated using the formula

of interest expense being divided by the latest two year average debt. The interest expense of

the current year of the Origin’s Energy Limited is 418.30. The latest two year average debt

amounts to 6779.34. After applying the formula the cost of debt comes to 6.2%. But the debt

is generally calculated post tax rate. The after tax return determines the need of the holders of

debt to determine the earnings till maturity. Debt basically offers the tax protection which

means the interest expense reduces the taxes on the debt. This ultimately reduces the cost of

debt.

Answer to Question-3

Calculation of Gearing Ratios

CALCULATION OF INTEREST COVERAGE

RATIO

CALCULATION OF

DEBT TO EQUITY

RATIO

Particulars 2017 Particulars 2017

EARNINGS BEFORE INTEREST AND TAX

(A) -1522 TOTAL DEBT (A) 8507

INTEREST EXPENSE (B) 553

TOTAL

EQUITY(B)

1139

6

ICR (A/B) -2.75 DER (A/B) 75%

CALCULATION OF DEBT RATIO

CALCULATION OF

EQUITY RATIO

CORPORATE FINANCE 8

Particulars 2017 Particulars 2017

TOTAL DEBT (A)

1380

3

TOTAL EQUITY

(A)

1139

6

TOTAL ASSETS(B)

2519

9

TOTAL

ASSETS(B)

2519

9

DER (A/B) 55% DER (A/B) 45%

Difficulties

The ratio determines the amount of leverage where a company is using debt to pay its

continuing operations. In the business scenario, such companies may not be able to meet the

debt repayment rules and could potentially attract bankruptcy. The situation becomes worse

when the company is involved in the arrangements of funds through debt with possibly

variable interests where a sudden increase in the payments can cause problems for the

company like Origin Energy limited5. A higher gearing ratio is not that much of concern in

the industry which is regulated. Under monopoly business the rates are approved by the

regulators for survival.

Lenders are particularly concerned about the gearing ratio because a higher ratio can put the

loans at risk for not being able to be repaid6. Therefore there are chances that the lenders use

restrictive measures that eventually cease the payment of the dividends, cash flows for debt

repayment, restriction on alternative uses of cash, and the investors are likely to invest more

equity into the company.

5 Accounting Tools, Gearing Ratio (17th May 2018)

<https://www.accountingtools.com/articles/2017/5/5/gearing-ratio>

6 Geeta Lakshmi, Muhammad Khan & Dimitrios Vortelinos, Cost of capital of stakeholders’

WACC (Palgrave Macmillan, 2016) 15

Particulars 2017 Particulars 2017

TOTAL DEBT (A)

1380

3

TOTAL EQUITY

(A)

1139

6

TOTAL ASSETS(B)

2519

9

TOTAL

ASSETS(B)

2519

9

DER (A/B) 55% DER (A/B) 45%

Difficulties

The ratio determines the amount of leverage where a company is using debt to pay its

continuing operations. In the business scenario, such companies may not be able to meet the

debt repayment rules and could potentially attract bankruptcy. The situation becomes worse

when the company is involved in the arrangements of funds through debt with possibly

variable interests where a sudden increase in the payments can cause problems for the

company like Origin Energy limited5. A higher gearing ratio is not that much of concern in

the industry which is regulated. Under monopoly business the rates are approved by the

regulators for survival.

Lenders are particularly concerned about the gearing ratio because a higher ratio can put the

loans at risk for not being able to be repaid6. Therefore there are chances that the lenders use

restrictive measures that eventually cease the payment of the dividends, cash flows for debt

repayment, restriction on alternative uses of cash, and the investors are likely to invest more

equity into the company.

5 Accounting Tools, Gearing Ratio (17th May 2018)

<https://www.accountingtools.com/articles/2017/5/5/gearing-ratio>

6 Geeta Lakshmi, Muhammad Khan & Dimitrios Vortelinos, Cost of capital of stakeholders’

WACC (Palgrave Macmillan, 2016) 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 9

Creditors also have similar kind of concern. At times gearing ratios does not provide the true

picture of the company’s financial position. The figures of short term debt and long term debt

are commonly included with other liabilities and the debt to equity ratio calculation becomes

different to compute7. This ultimately gives a poor ratio and the creditors rely on the figures

which can mislead their decision. They are usually not able to impose any changes on the

company.

Answer to Question-4

Capital Structure Theory

In financial management the capital structure theory can be derived as a systematic approach

or the methodology to decide the financing business activities through a combination of

equities and liabilities8. The relationship between the equity, debt and the market can be

explored using the help of competing capital structure theories.

Traditional approach

According to the ancient approach a company shall minimise the WACC or weighted average

cost of capital and shall maximise the value of the assets readily available for the market9.

This approach suggests that the debt financing can be used only to a certain limit and extent.

Any debt capital beyond this point will lead to the devaluation of the company and

unnecessary cost of leverage10.

7 Reuben S Harris, A Comparison of the Weighted-Average Cost of Capital and Equity-

Residual Approaches to Valuation, (2017) 4(3) Journal of Darden Business Publishing Cases

1, 5.

8Colin T Campbell, Neal Galpin & Shane A Johnson, Optimal inside debt compensation and

the value of equity and debt, (2016) 119(2), Journal of Financial Economics 336, 352.

9 Geeta Lakshmi, Muhammad Khan & Dimitrios Vortelinos, Cost of capital of stakeholders’

WACC (Palgrave Macmillan, 2016) 15

10 Paul Asquith & Lawrence A Weiss, A Continuation of Capital Structure Theory, (2016)

11(3). Lessons in Corporate Finance: A Case Studies Approach to Financial Tools, Financial

Policies, and Valuation 261, 285.

Creditors also have similar kind of concern. At times gearing ratios does not provide the true

picture of the company’s financial position. The figures of short term debt and long term debt

are commonly included with other liabilities and the debt to equity ratio calculation becomes

different to compute7. This ultimately gives a poor ratio and the creditors rely on the figures

which can mislead their decision. They are usually not able to impose any changes on the

company.

Answer to Question-4

Capital Structure Theory

In financial management the capital structure theory can be derived as a systematic approach

or the methodology to decide the financing business activities through a combination of

equities and liabilities8. The relationship between the equity, debt and the market can be

explored using the help of competing capital structure theories.

Traditional approach

According to the ancient approach a company shall minimise the WACC or weighted average

cost of capital and shall maximise the value of the assets readily available for the market9.

This approach suggests that the debt financing can be used only to a certain limit and extent.

Any debt capital beyond this point will lead to the devaluation of the company and

unnecessary cost of leverage10.

7 Reuben S Harris, A Comparison of the Weighted-Average Cost of Capital and Equity-

Residual Approaches to Valuation, (2017) 4(3) Journal of Darden Business Publishing Cases

1, 5.

8Colin T Campbell, Neal Galpin & Shane A Johnson, Optimal inside debt compensation and

the value of equity and debt, (2016) 119(2), Journal of Financial Economics 336, 352.

9 Geeta Lakshmi, Muhammad Khan & Dimitrios Vortelinos, Cost of capital of stakeholders’

WACC (Palgrave Macmillan, 2016) 15

10 Paul Asquith & Lawrence A Weiss, A Continuation of Capital Structure Theory, (2016)

11(3). Lessons in Corporate Finance: A Case Studies Approach to Financial Tools, Financial

Policies, and Valuation 261, 285.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 10

Under this theory the managers and the financial analysts are required to make certain

assumptions. For example the debt has an interest portion which remains constant during one

period and eventually increases when the leverage is additionally increased over the time.

The equity’s expected rate of return is also constant before the leverage of the company

increases gradually11. This creates an optimal point for the WACC to be small.

The financing decision has a direct impact on the WACC of the company. It is important to

note that the lower the WACC of the company the higher the market value will be of the

company. From the above calculations it can be observed that the WACC of the Origin

Energy Limited is 13.94%. The market value of the company increases when the WACC of

the company decreases. The relationship is of inverse nature. Therefore, the search for the

optimal capital structure of the company becomes the important factor. It is the responsibility

of the financial managers of the Origin Energy Limited to find the optimal capital structure

that will result in the lowest WACC.

As WACC is simply an average between the cost of debt and cost of equity, it becomes

necessary to determine which component is cheaper. The cost of debt is cheaper as compared

to the cost of equity. Debt is a component which carries less risk, the required return which is

need to be given to the investors is also less against the equity investors. The payment of

interest received by the debt holders is an amount of fixed nature and it is paid in priority

over the payment of the cumulative dividends. Another reason for the debt component to

carry less risk is derived at the time of liquidation of the company. Debt holders at the time of

liquidation will receive the payments before the shareholders12.

11 Edwin O Fischer, Robert Heinkel & Joseph Zechner, Dynamic capital structure choice:

Theory and tests, (2014) 44(1), The Journal of Finance, 19, 40.

12 Emanuel Camilleri and Roxanne Camilleri, Accounting for Financial Instruments: A Guide

to Valuation and Risk Management (Taylor & Francis, 2017) 10.

Under this theory the managers and the financial analysts are required to make certain

assumptions. For example the debt has an interest portion which remains constant during one

period and eventually increases when the leverage is additionally increased over the time.

The equity’s expected rate of return is also constant before the leverage of the company

increases gradually11. This creates an optimal point for the WACC to be small.

The financing decision has a direct impact on the WACC of the company. It is important to

note that the lower the WACC of the company the higher the market value will be of the

company. From the above calculations it can be observed that the WACC of the Origin

Energy Limited is 13.94%. The market value of the company increases when the WACC of

the company decreases. The relationship is of inverse nature. Therefore, the search for the

optimal capital structure of the company becomes the important factor. It is the responsibility

of the financial managers of the Origin Energy Limited to find the optimal capital structure

that will result in the lowest WACC.

As WACC is simply an average between the cost of debt and cost of equity, it becomes

necessary to determine which component is cheaper. The cost of debt is cheaper as compared

to the cost of equity. Debt is a component which carries less risk, the required return which is

need to be given to the investors is also less against the equity investors. The payment of

interest received by the debt holders is an amount of fixed nature and it is paid in priority

over the payment of the cumulative dividends. Another reason for the debt component to

carry less risk is derived at the time of liquidation of the company. Debt holders at the time of

liquidation will receive the payments before the shareholders12.

11 Edwin O Fischer, Robert Heinkel & Joseph Zechner, Dynamic capital structure choice:

Theory and tests, (2014) 44(1), The Journal of Finance, 19, 40.

12 Emanuel Camilleri and Roxanne Camilleri, Accounting for Financial Instruments: A Guide

to Valuation and Risk Management (Taylor & Francis, 2017) 10.

CORPORATE FINANCE 11

The treatment of tax is also different in case of debt. And with the help of debt component the

company gets relieved from the tax factor when it is subtracted from the profit and loss

account of the company. Henceforth, the Origin Energy Limited has a capital structure of

debt being 55% an equity being 45%. And origin energy being the Natural Gas company is

very capital intensive in nature13. The ideal debt to equity ratio is 2:1, which determines that

the 2/3rd funds of the company are financed through the debt component and 1/3rd through

equity. The ideal ratio for origin energy limited company is 1.3. The calculations derived

above shows that the debt to equity ratio of the Origin Energy Limited is 0.75 which is below

of what is set as a standard benchmark. Henceforth company needs to improve on this by

financing the activities using the debt component more than the equity14.

Answer to Question-5

Recommendations

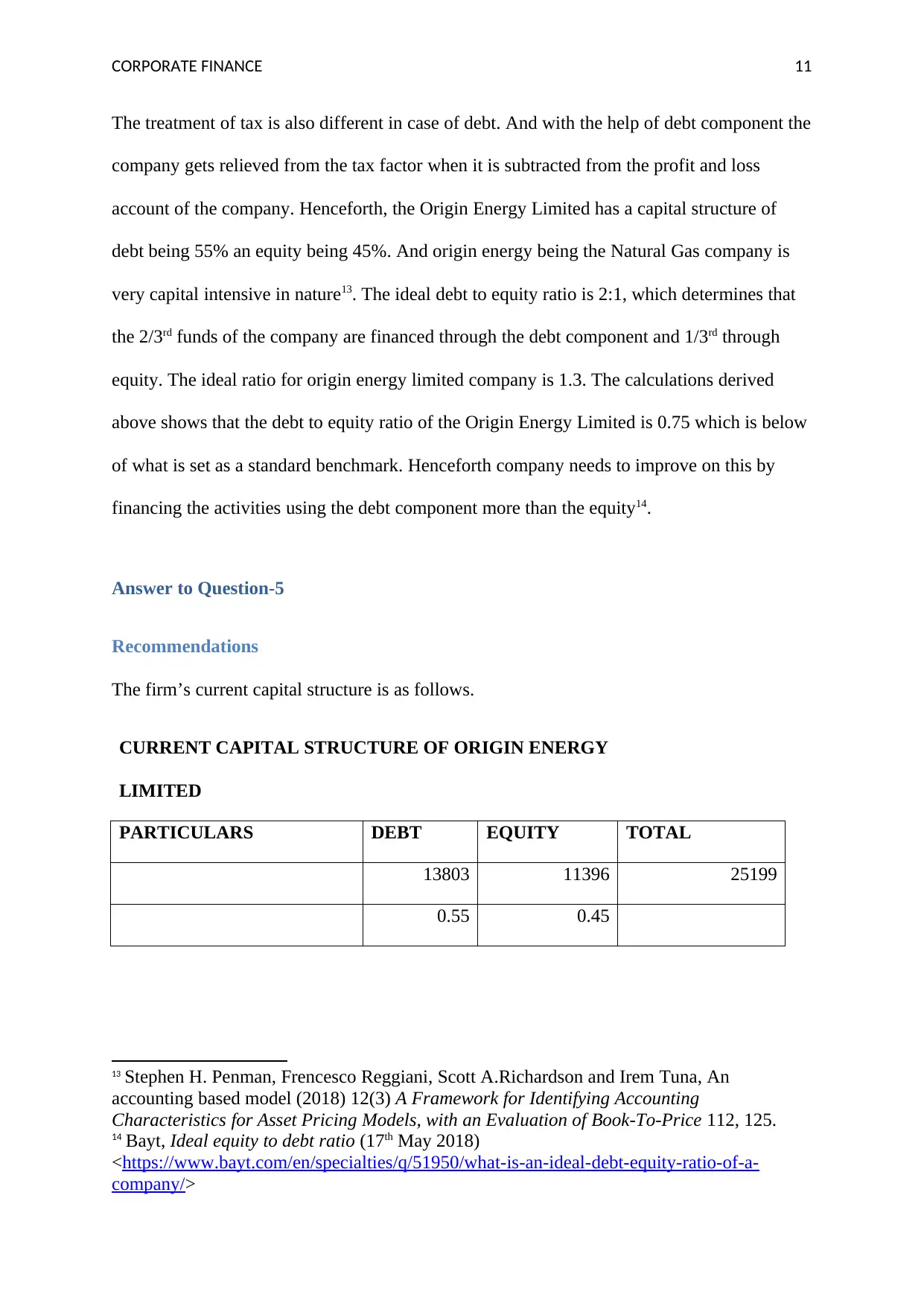

The firm’s current capital structure is as follows.

CURRENT CAPITAL STRUCTURE OF ORIGIN ENERGY

LIMITED

PARTICULARS DEBT EQUITY TOTAL

13803 11396 25199

0.55 0.45

13 Stephen H. Penman, Frencesco Reggiani, Scott A.Richardson and Irem Tuna, An

accounting based model (2018) 12(3) A Framework for Identifying Accounting

Characteristics for Asset Pricing Models, with an Evaluation of Book-To-Price 112, 125.

14 Bayt, Ideal equity to debt ratio (17th May 2018)

<https://www.bayt.com/en/specialties/q/51950/what-is-an-ideal-debt-equity-ratio-of-a-

company/>

The treatment of tax is also different in case of debt. And with the help of debt component the

company gets relieved from the tax factor when it is subtracted from the profit and loss

account of the company. Henceforth, the Origin Energy Limited has a capital structure of

debt being 55% an equity being 45%. And origin energy being the Natural Gas company is

very capital intensive in nature13. The ideal debt to equity ratio is 2:1, which determines that

the 2/3rd funds of the company are financed through the debt component and 1/3rd through

equity. The ideal ratio for origin energy limited company is 1.3. The calculations derived

above shows that the debt to equity ratio of the Origin Energy Limited is 0.75 which is below

of what is set as a standard benchmark. Henceforth company needs to improve on this by

financing the activities using the debt component more than the equity14.

Answer to Question-5

Recommendations

The firm’s current capital structure is as follows.

CURRENT CAPITAL STRUCTURE OF ORIGIN ENERGY

LIMITED

PARTICULARS DEBT EQUITY TOTAL

13803 11396 25199

0.55 0.45

13 Stephen H. Penman, Frencesco Reggiani, Scott A.Richardson and Irem Tuna, An

accounting based model (2018) 12(3) A Framework for Identifying Accounting

Characteristics for Asset Pricing Models, with an Evaluation of Book-To-Price 112, 125.

14 Bayt, Ideal equity to debt ratio (17th May 2018)

<https://www.bayt.com/en/specialties/q/51950/what-is-an-ideal-debt-equity-ratio-of-a-

company/>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.