Corporate Governance and Sustainability Reporting

VerifiedAdded on 2023/06/04

|10

|1936

|498

AI Summary

This paper highlights the importance of sustainability accounting and the extent up to which it can be sufficiently improved by efficient implementation of corporate governance and operational management in the fields of communication, accounting as well as organizational strategy making.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

0

Running head: CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

Name of the Student

Name of the University

Author’s Note

Running head: CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

Table of Contents

Introduction......................................................................................................................................2

Overview/ Background Information................................................................................................2

Frameworks/Standards/Legislations relevant to Reporting.............................................................3

Corporate Governance.....................................................................................................................4

Current Issues & Challenges of sustainability Reporting................................................................5

Future Prospects of Sustainability Reporting..................................................................................5

Conclusion.......................................................................................................................................6

References........................................................................................................................................8

Table of Contents

Introduction......................................................................................................................................2

Overview/ Background Information................................................................................................2

Frameworks/Standards/Legislations relevant to Reporting.............................................................3

Corporate Governance.....................................................................................................................4

Current Issues & Challenges of sustainability Reporting................................................................5

Future Prospects of Sustainability Reporting..................................................................................5

Conclusion.......................................................................................................................................6

References........................................................................................................................................8

2CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

Introduction

The aspect of sustainability is a major issue of concern in the modern business world

where every organization should be abide by the protocols of the society as well as maintain

ethical practice as a part of their organizational strategy. It is important that organizations should

include sustainability reporting in order to strategize their organizational culture and societal

practices towards redesigning an improved framework of business environment in terms of its

accounting practices as well as communicational practices within the managerial hierarchy of the

organization (Gallego-Álvarez & Ortas, 2017). The paper highlights the importance of

sustainability accounting and the extent up to which it can be sufficiently improved by efficient

implementation of corporate governance and operational management in the fields of

communication, accounting as well as organizational strategy making.

Overview/ Background Information

As the survey data as conducted by KPMG in Australia by 2013, it was been found that

the corporate reputation is highly dependent upon effective reporting practice regarding

sustainability as well as expanding investment financially in positive deeds with transparency

(Ganesan et al., 2017). These are the major factors in building public trust and increasing loyal

employee retention within the organization. Moreover, the K-Z Index (Kaplan – Zingales Index)

came out to be 0.6 lower compared to the lower sustainability companies. The lower score is a

better parametric indicator of the fact that few funding constraints in terms of capital is present

within the financial initiatives of the organizations. Through the process of sustainability

reporting companies not only of Australia but also of companies throughout the world gather

data and relevant information regarding the firms existing performance with the objective of

creating a platform where transparent exchange and utilization of available resources takes place

Introduction

The aspect of sustainability is a major issue of concern in the modern business world

where every organization should be abide by the protocols of the society as well as maintain

ethical practice as a part of their organizational strategy. It is important that organizations should

include sustainability reporting in order to strategize their organizational culture and societal

practices towards redesigning an improved framework of business environment in terms of its

accounting practices as well as communicational practices within the managerial hierarchy of the

organization (Gallego-Álvarez & Ortas, 2017). The paper highlights the importance of

sustainability accounting and the extent up to which it can be sufficiently improved by efficient

implementation of corporate governance and operational management in the fields of

communication, accounting as well as organizational strategy making.

Overview/ Background Information

As the survey data as conducted by KPMG in Australia by 2013, it was been found that

the corporate reputation is highly dependent upon effective reporting practice regarding

sustainability as well as expanding investment financially in positive deeds with transparency

(Ganesan et al., 2017). These are the major factors in building public trust and increasing loyal

employee retention within the organization. Moreover, the K-Z Index (Kaplan – Zingales Index)

came out to be 0.6 lower compared to the lower sustainability companies. The lower score is a

better parametric indicator of the fact that few funding constraints in terms of capital is present

within the financial initiatives of the organizations. Through the process of sustainability

reporting companies not only of Australia but also of companies throughout the world gather

data and relevant information regarding the firms existing performance with the objective of

creating a platform where transparent exchange and utilization of available resources takes place

3CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

without wastage. Corporate governance on the other hand is important for improving operational

performance apart from regulating the financial effectiveness the other purposes that get fulfilled

due to sustainability reporting are monitoring of long term risk and mitigating socio-

environmental risk followed by improvement of the organizational value of the business.

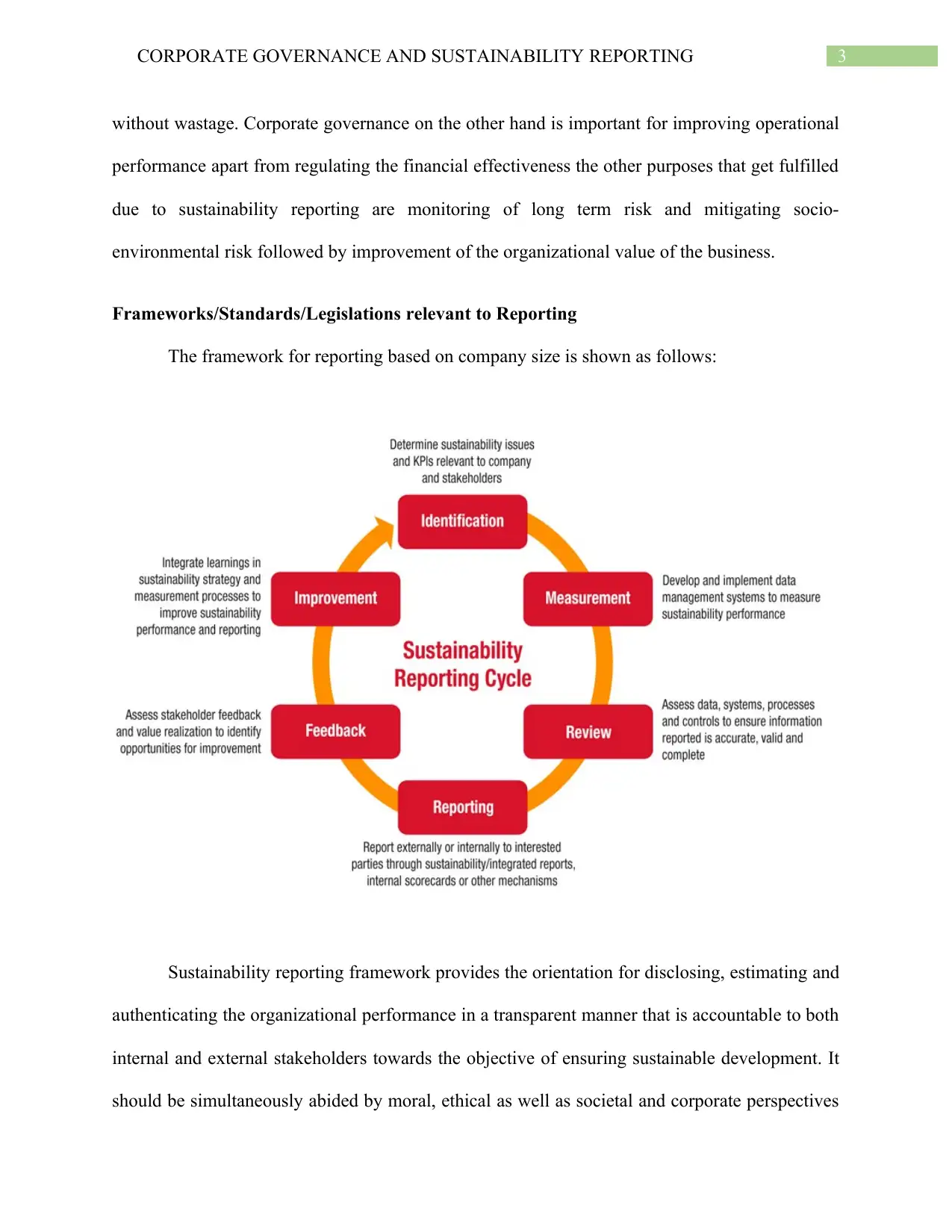

Frameworks/Standards/Legislations relevant to Reporting

The framework for reporting based on company size is shown as follows:

Sustainability reporting framework provides the orientation for disclosing, estimating and

authenticating the organizational performance in a transparent manner that is accountable to both

internal and external stakeholders towards the objective of ensuring sustainable development. It

should be simultaneously abided by moral, ethical as well as societal and corporate perspectives

without wastage. Corporate governance on the other hand is important for improving operational

performance apart from regulating the financial effectiveness the other purposes that get fulfilled

due to sustainability reporting are monitoring of long term risk and mitigating socio-

environmental risk followed by improvement of the organizational value of the business.

Frameworks/Standards/Legislations relevant to Reporting

The framework for reporting based on company size is shown as follows:

Sustainability reporting framework provides the orientation for disclosing, estimating and

authenticating the organizational performance in a transparent manner that is accountable to both

internal and external stakeholders towards the objective of ensuring sustainable development. It

should be simultaneously abided by moral, ethical as well as societal and corporate perspectives

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

through legislation and standardized framework. The framework of sustainability strategizes

ways for pollution prevention which enhances the environmental efficiency and reduce risks for

environmental degradation without lowering the profits of the organization and without raising

their total cost of production. Along with considering the benefits of all the stakeholders

associated both with the society and the organization, sustainability reporting takes under

consideration the impact of environmental, social and economic contribution of the corporate

world so that it can render a balanced performance beside simultaneously achieving its targets

and objectives. Benchmarking and assessing the economic affairs of profit maximization, cost

savings, inclusive growth as well as investments for research and development are the parts and

parcel of this process. Apart from that the framework of sustainability reporting considers the

environmental management aspect of natural resources like air, water, land and waste followed

by pollution prevention. Bettering off the corporate efficiency without worsening off the

environmental justice both locally and globally are of the sole aspect of concern that is

established through the legislative initiative taken for protecting accountable sustainability

reporting (O’Mahony & Mason, 2017). Moreover, product stewardship builds value between the

products and the organization by enhancing the efficiency of the business process. This

framework enables the creation of a clean technologically efficient sustainable energy based

corporate environment that takes care of the society and all its related entities.

Corporate Governance

Corporate governance covers the framework of transparent operational mechanism

preserving the balance and protecting the interest of all the stakeholders’ corporate purposes

which are being abided by ethical norms and government rules and regulations. It essentially

directs and controls the involvement and interest of shareholders, management, customers,

through legislation and standardized framework. The framework of sustainability strategizes

ways for pollution prevention which enhances the environmental efficiency and reduce risks for

environmental degradation without lowering the profits of the organization and without raising

their total cost of production. Along with considering the benefits of all the stakeholders

associated both with the society and the organization, sustainability reporting takes under

consideration the impact of environmental, social and economic contribution of the corporate

world so that it can render a balanced performance beside simultaneously achieving its targets

and objectives. Benchmarking and assessing the economic affairs of profit maximization, cost

savings, inclusive growth as well as investments for research and development are the parts and

parcel of this process. Apart from that the framework of sustainability reporting considers the

environmental management aspect of natural resources like air, water, land and waste followed

by pollution prevention. Bettering off the corporate efficiency without worsening off the

environmental justice both locally and globally are of the sole aspect of concern that is

established through the legislative initiative taken for protecting accountable sustainability

reporting (O’Mahony & Mason, 2017). Moreover, product stewardship builds value between the

products and the organization by enhancing the efficiency of the business process. This

framework enables the creation of a clean technologically efficient sustainable energy based

corporate environment that takes care of the society and all its related entities.

Corporate Governance

Corporate governance covers the framework of transparent operational mechanism

preserving the balance and protecting the interest of all the stakeholders’ corporate purposes

which are being abided by ethical norms and government rules and regulations. It essentially

directs and controls the involvement and interest of shareholders, management, customers,

5CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

government, suppliers, and investors as well as the community that is associated with the

respective organization. It provides strategic action plans, compliance, risk oversights, corporate

disclosure, crisis preparedness as well as internal performance controlling measurements on

stakeholders’ engagement. Corporate governance raises firm’s performance through

sustainability and reduce risk of scandals and corporate crisis by Pareto optimal allocation,

utilization and distribution of wealth. Corporate governance takes care of profits of the

organization, the stakeholders which are associated with the organization as well as preserves the

human and social rights and the planet as a whole. This enhances the socio-economic balance

and keep the corporate initiatives adhere to ethical standards. Major pillars of corporate

governance are accountability, transparency, independence and fairness.

Current Issues & Challenges of sustainability Reporting

The current issues and challenge that is being faced internally in the process of

sustainability reporting is to identify who is the target audience. Sustainability report remains

abided by the objective of putting forth the performance of the organization related to issues of

governance, economic and of socio-environmental significance. Hence, lack of effective

compliance as per the assurance standards of GRI if not accomplished then it may lead to green

washing. Organizational commitment and reliable efforts are necessary for ensuring effective

compliance regarding sustainability reporting. Moreover, another challenge is the immature and

substantially fragmented data collection system greatly reduces the performance of the

sustainability reporting process (Ioannou & Serafeim, 2017).

Future Prospects of Sustainability Reporting

Sustainability reporting not only increases the consumer loyalty but also improves the

entire trustworthiness of a company and establishes the company as a brand (Hussain et al.,

government, suppliers, and investors as well as the community that is associated with the

respective organization. It provides strategic action plans, compliance, risk oversights, corporate

disclosure, crisis preparedness as well as internal performance controlling measurements on

stakeholders’ engagement. Corporate governance raises firm’s performance through

sustainability and reduce risk of scandals and corporate crisis by Pareto optimal allocation,

utilization and distribution of wealth. Corporate governance takes care of profits of the

organization, the stakeholders which are associated with the organization as well as preserves the

human and social rights and the planet as a whole. This enhances the socio-economic balance

and keep the corporate initiatives adhere to ethical standards. Major pillars of corporate

governance are accountability, transparency, independence and fairness.

Current Issues & Challenges of sustainability Reporting

The current issues and challenge that is being faced internally in the process of

sustainability reporting is to identify who is the target audience. Sustainability report remains

abided by the objective of putting forth the performance of the organization related to issues of

governance, economic and of socio-environmental significance. Hence, lack of effective

compliance as per the assurance standards of GRI if not accomplished then it may lead to green

washing. Organizational commitment and reliable efforts are necessary for ensuring effective

compliance regarding sustainability reporting. Moreover, another challenge is the immature and

substantially fragmented data collection system greatly reduces the performance of the

sustainability reporting process (Ioannou & Serafeim, 2017).

Future Prospects of Sustainability Reporting

Sustainability reporting not only increases the consumer loyalty but also improves the

entire trustworthiness of a company and establishes the company as a brand (Hussain et al.,

6CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

2018). Sustainability reporting along with corporate governance is able to relate community

expectations by enhancing transparency, authenticity and trustworthiness through public

disclosure and hence they are credible tools to ensure ethical business in the long run. It will

better off the society without worsening off the functioning of the corporate business. The

process of sustainability reporting is currently moving towards the aspect of integrated reporting

where usage of creative online reporting and sophisticated communication are made in the

compliance driven sustainability reports that serves the interest of the stakeholders as well as the

interest of the society. The trends that are destined to determine the future of corporate

governance and sustainability reporting can be incorporated as follows:

Enhanced creative ways of communication is able to channelize the stakeholders needs

and reach the target audience in an improved manner

The extension of reporting through the value chain in impacting the corporate business

framework in a socio-environmental friendly way

In Australia, the development of integrated reporting is the coming future of

sustainability reporting accompanied by corporate governance and based on the G4

guidelines.

Sustainability reporting is increasingly becoming mainstream for its improved

measurement impacts.

The mandatory reporting system as initiated by the government is expanding up to the

global standard for evolution in the process of sustainability reporting system.

Conclusion

It can be concluded that the relevance of effective sustainability reporting is widely

associated with the improvements that are made to enhance internal efficiency of any

2018). Sustainability reporting along with corporate governance is able to relate community

expectations by enhancing transparency, authenticity and trustworthiness through public

disclosure and hence they are credible tools to ensure ethical business in the long run. It will

better off the society without worsening off the functioning of the corporate business. The

process of sustainability reporting is currently moving towards the aspect of integrated reporting

where usage of creative online reporting and sophisticated communication are made in the

compliance driven sustainability reports that serves the interest of the stakeholders as well as the

interest of the society. The trends that are destined to determine the future of corporate

governance and sustainability reporting can be incorporated as follows:

Enhanced creative ways of communication is able to channelize the stakeholders needs

and reach the target audience in an improved manner

The extension of reporting through the value chain in impacting the corporate business

framework in a socio-environmental friendly way

In Australia, the development of integrated reporting is the coming future of

sustainability reporting accompanied by corporate governance and based on the G4

guidelines.

Sustainability reporting is increasingly becoming mainstream for its improved

measurement impacts.

The mandatory reporting system as initiated by the government is expanding up to the

global standard for evolution in the process of sustainability reporting system.

Conclusion

It can be concluded that the relevance of effective sustainability reporting is widely

associated with the improvements that are made to enhance internal efficiency of any

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

organization depending upon their respective business environment. In fact, if sustainability

reporting be effectively practices then it will create a benchmark of future success which not

only will design opportunities for firms but also will raise the morale of the stakeholders by

developing strategies that are innovative, product and service oriented and will drive inclusive

growth of the economy and ensure long run qualitative development. Sustainability reporting

along with corporate governance drives the performance improvement procedures of firms and

strengthen their contribution towards the socio-economic as well as environmental causes

through its core business endeavors and maintain an accountable balance between the firms and

the society.

organization depending upon their respective business environment. In fact, if sustainability

reporting be effectively practices then it will create a benchmark of future success which not

only will design opportunities for firms but also will raise the morale of the stakeholders by

developing strategies that are innovative, product and service oriented and will drive inclusive

growth of the economy and ensure long run qualitative development. Sustainability reporting

along with corporate governance drives the performance improvement procedures of firms and

strengthen their contribution towards the socio-economic as well as environmental causes

through its core business endeavors and maintain an accountable balance between the firms and

the society.

8CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

References

Adams, C. (2017). Understanding integrated reporting: the concise guide to integrated thinking

and the future of corporate reporting. Routledge.

https://www.taylorfrancis.com/books/9781351275002

De Villiers, C., & Maroun, W. (Eds.). (2017). Sustainability accounting and integrated

reporting. Routledge. https://books.google.co.in/books?

hl=en&lr=&id=Urw8DwAAQBAJ&oi=fnd&pg=PT14&dq=corporate+governance+

%26+SUSTAINABILITY+REPORTING&ots=3lCHYN5frv&sig=LBDmtrzWuuZbviJE

DgKVPalI63s

Epstein, M. J. (2018). Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

https://www.taylorfrancis.com/books/9781351280112

Gallego-Álvarez, I., & Ortas, E. (2017). Corporate environmental sustainability reporting in the

context of national cultures: A quantile regression approach. International Business

Review, 26(2), 337-353.

https://www.sciencedirect.com/science/article/pii/S0969593116301317

Ganesan, Y., Hwa, Y. W., Jaaffar, A. H., & Hashim, F. (2017). Corporate Governance and

Sustainability Reporting Practices: The Moderating Role of Internal Audit

Function. Global Business and Management Research, 9(4s), 159-179.

http://search.proquest.com/openview/e4454a043765593cee370febbeede101/1?pq-

origsite=gscholar&cbl=696409

Gauthier, J., & Wooldridge, B. (2018). Sustainability Ratings and Organizational Legitimacy:

The Role of Compensating Tactics. In Sustainability and Social Responsibility:

References

Adams, C. (2017). Understanding integrated reporting: the concise guide to integrated thinking

and the future of corporate reporting. Routledge.

https://www.taylorfrancis.com/books/9781351275002

De Villiers, C., & Maroun, W. (Eds.). (2017). Sustainability accounting and integrated

reporting. Routledge. https://books.google.co.in/books?

hl=en&lr=&id=Urw8DwAAQBAJ&oi=fnd&pg=PT14&dq=corporate+governance+

%26+SUSTAINABILITY+REPORTING&ots=3lCHYN5frv&sig=LBDmtrzWuuZbviJE

DgKVPalI63s

Epstein, M. J. (2018). Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

https://www.taylorfrancis.com/books/9781351280112

Gallego-Álvarez, I., & Ortas, E. (2017). Corporate environmental sustainability reporting in the

context of national cultures: A quantile regression approach. International Business

Review, 26(2), 337-353.

https://www.sciencedirect.com/science/article/pii/S0969593116301317

Ganesan, Y., Hwa, Y. W., Jaaffar, A. H., & Hashim, F. (2017). Corporate Governance and

Sustainability Reporting Practices: The Moderating Role of Internal Audit

Function. Global Business and Management Research, 9(4s), 159-179.

http://search.proquest.com/openview/e4454a043765593cee370febbeede101/1?pq-

origsite=gscholar&cbl=696409

Gauthier, J., & Wooldridge, B. (2018). Sustainability Ratings and Organizational Legitimacy:

The Role of Compensating Tactics. In Sustainability and Social Responsibility:

9CORPORATE GOVERNANCE AND SUSTAINABILITY REPORTING

Regulation and Reporting (pp. 141-157). Springer, Singapore.

https://link.springer.com/chapter/10.1007/978-981-10-4502-8_6

Hussain, N., Rigoni, U., & Orij, R. P. (2018). Corporate governance and sustainability

performance: Analysis of triple bottom line performance. Journal of Business

Ethics, 149(2), 411-432. https://link.springer.com/article/10.1007/s10551-016-3099-5

Ioannou, I., & Serafeim, G. (2017). The consequences of mandatory corporate sustainability

reporting. https://papers.ssrn.com/soL3/papers.cfm?abstract_id=1799589

O’Mahony, J., & Mason, M. (2017). Post-traditional corporate governance. In Globalization and

Corporate Citizenship: The Alternative Gaze (pp. 74-90). Routledge.

https://www.taylorfrancis.com/books/e/9781351284233/chapters/10.4324%2F978135128

4240-7

Silva, M., Lourenço, I., & Branco, M. C. (2017). Sustainability reporting in family versus non-

family firms: The role of the richest European families. In XVI Congresso Internacional

de Contabilidade e Auditoria. Ordem dos Contabilistas Certificados.

https://repositorio.iscte-iul.pt/handle/10071/16341

Regulation and Reporting (pp. 141-157). Springer, Singapore.

https://link.springer.com/chapter/10.1007/978-981-10-4502-8_6

Hussain, N., Rigoni, U., & Orij, R. P. (2018). Corporate governance and sustainability

performance: Analysis of triple bottom line performance. Journal of Business

Ethics, 149(2), 411-432. https://link.springer.com/article/10.1007/s10551-016-3099-5

Ioannou, I., & Serafeim, G. (2017). The consequences of mandatory corporate sustainability

reporting. https://papers.ssrn.com/soL3/papers.cfm?abstract_id=1799589

O’Mahony, J., & Mason, M. (2017). Post-traditional corporate governance. In Globalization and

Corporate Citizenship: The Alternative Gaze (pp. 74-90). Routledge.

https://www.taylorfrancis.com/books/e/9781351284233/chapters/10.4324%2F978135128

4240-7

Silva, M., Lourenço, I., & Branco, M. C. (2017). Sustainability reporting in family versus non-

family firms: The role of the richest European families. In XVI Congresso Internacional

de Contabilidade e Auditoria. Ordem dos Contabilistas Certificados.

https://repositorio.iscte-iul.pt/handle/10071/16341

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.