University Cost Accounting Assignment: Detailed Analysis

VerifiedAdded on 2020/04/21

|13

|1898

|131

Homework Assignment

AI Summary

This cost accounting assignment solution provides a comprehensive analysis of various cost accounting concepts and problems. It begins with definitions, objectives, and classifications of cost accounting, followed by the creation of a cost sheet. The solution also includes a break-even analysis, variance analysis, and an in-depth look at ABC costing. Furthermore, it addresses decision analysis problems, comparing traditional costing methods with ABC costing to determine the most effective approach for cost management. The assignment covers topics such as direct material and labor variances, and the evaluation of make-or-buy decisions. The analysis is well-structured, providing detailed calculations and explanations to facilitate understanding of cost accounting principles.

Running head: COST ACCOUNTING

Cost Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Cost Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COST ACCOUNTING

Table of Contents

Cost Accounting Assignment.....................................................................................................2

Part A.........................................................................................................................................2

Answer to Question 1:................................................................................................................2

Definition Cost Accounting Objectives and Classification:......................................................2

Answer to question 2: Cost Sheet:.............................................................................................3

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................5

ABC Costing:.............................................................................................................................6

Answer to question (c):..............................................................................................................7

Answer to Problem 2:.................................................................................................................8

Answer to question (A):.............................................................................................................8

Answer to question (c):..............................................................................................................9

Decision Analysis:.....................................................................................................................9

Answer to question (a):..............................................................................................................9

Answer to question (b):............................................................................................................10

Problem 2 (Traditional Costing):.............................................................................................10

Answer to question 3: Variance Analysis................................................................................10

Reference List:.........................................................................................................................12

Table of Contents

Cost Accounting Assignment.....................................................................................................2

Part A.........................................................................................................................................2

Answer to Question 1:................................................................................................................2

Definition Cost Accounting Objectives and Classification:......................................................2

Answer to question 2: Cost Sheet:.............................................................................................3

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................5

ABC Costing:.............................................................................................................................6

Answer to question (c):..............................................................................................................7

Answer to Problem 2:.................................................................................................................8

Answer to question (A):.............................................................................................................8

Answer to question (c):..............................................................................................................9

Decision Analysis:.....................................................................................................................9

Answer to question (a):..............................................................................................................9

Answer to question (b):............................................................................................................10

Problem 2 (Traditional Costing):.............................................................................................10

Answer to question 3: Variance Analysis................................................................................10

Reference List:.........................................................................................................................12

2COST ACCOUNTING

Cost Accounting Assignment

Part A

Answer to Question 1:

Definition Cost Accounting Objectives and Classification:

Answer: Cost accounting can be defined as the procedure of accounting for cost relating to

one point at which the expenses are incurred or it is committed to the establishment of the

ultimate relationship with the cost centre and cost units (Drury 2013). In other words, cost

accounting takes into account the activities of preparation of the statistical data,

implementation of the cost control methods and ascertainment of the profitability of the work

executed or planned.

Objectives of Cost Accounting are as follows:

a. To determine the cost per unit each items of the different products manufactured by

the business

b. To determine the probability of each products manufactured and serving as the guide

in advising the management in maximising profitability.

c. To offer advice to the management in the future expansion of the business and

projected capital projects (Salako and Yusuf 2016).

Classification of Cost Accounting are as follows:

a. Cost accounting can be classified based on the nature such as material, labour and

overhead

b. Cost can be classified based on the degree of traceability such as direct and indirect

cost.

Cost Accounting Assignment

Part A

Answer to Question 1:

Definition Cost Accounting Objectives and Classification:

Answer: Cost accounting can be defined as the procedure of accounting for cost relating to

one point at which the expenses are incurred or it is committed to the establishment of the

ultimate relationship with the cost centre and cost units (Drury 2013). In other words, cost

accounting takes into account the activities of preparation of the statistical data,

implementation of the cost control methods and ascertainment of the profitability of the work

executed or planned.

Objectives of Cost Accounting are as follows:

a. To determine the cost per unit each items of the different products manufactured by

the business

b. To determine the probability of each products manufactured and serving as the guide

in advising the management in maximising profitability.

c. To offer advice to the management in the future expansion of the business and

projected capital projects (Salako and Yusuf 2016).

Classification of Cost Accounting are as follows:

a. Cost accounting can be classified based on the nature such as material, labour and

overhead

b. Cost can be classified based on the degree of traceability such as direct and indirect

cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COST ACCOUNTING

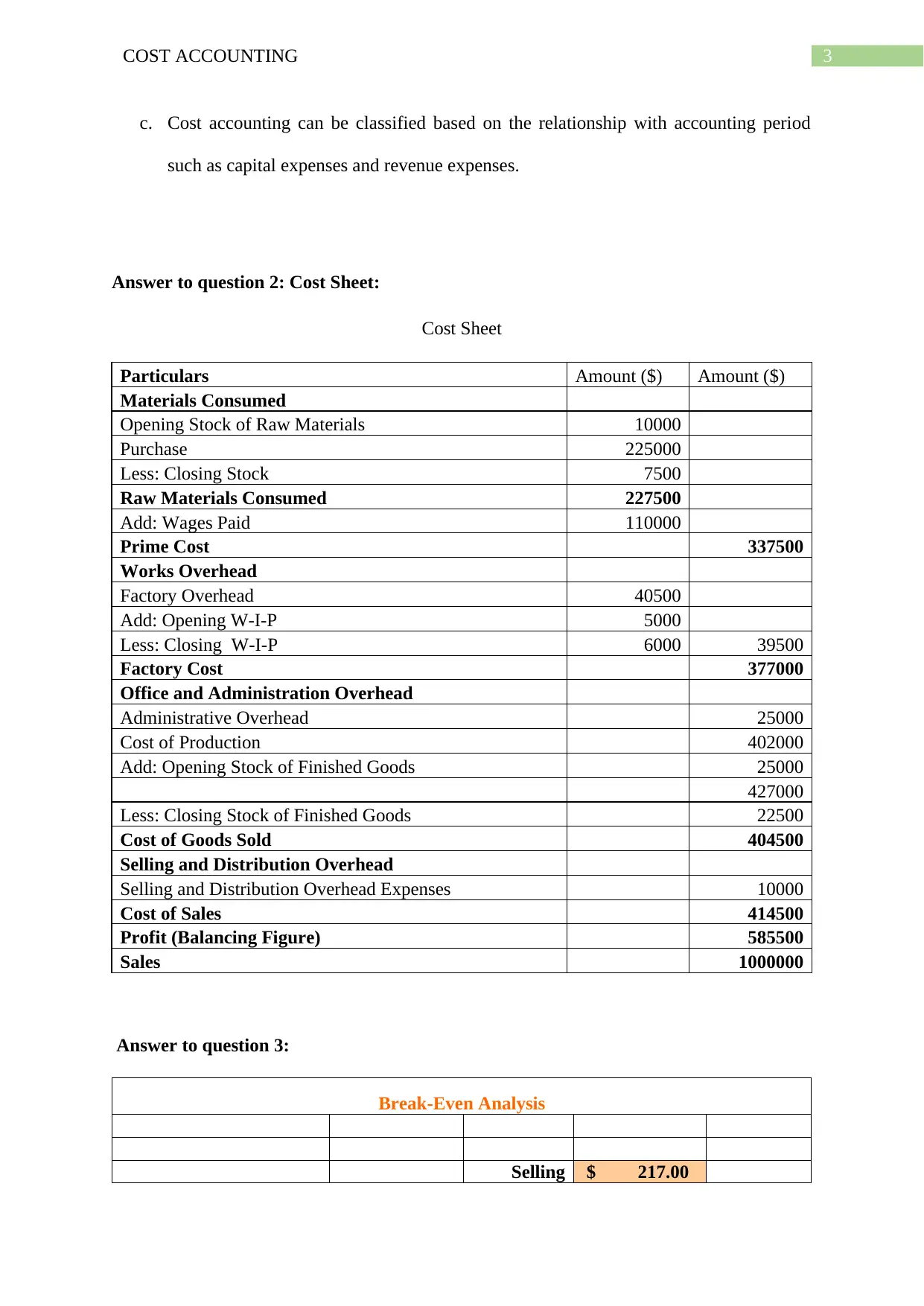

c. Cost accounting can be classified based on the relationship with accounting period

such as capital expenses and revenue expenses.

Answer to question 2: Cost Sheet:

Cost Sheet

Particulars Amount ($) Amount ($)

Materials Consumed

Opening Stock of Raw Materials 10000

Purchase 225000

Less: Closing Stock 7500

Raw Materials Consumed 227500

Add: Wages Paid 110000

Prime Cost 337500

Works Overhead

Factory Overhead 40500

Add: Opening W-I-P 5000

Less: Closing W-I-P 6000 39500

Factory Cost 377000

Office and Administration Overhead

Administrative Overhead 25000

Cost of Production 402000

Add: Opening Stock of Finished Goods 25000

427000

Less: Closing Stock of Finished Goods 22500

Cost of Goods Sold 404500

Selling and Distribution Overhead

Selling and Distribution Overhead Expenses 10000

Cost of Sales 414500

Profit (Balancing Figure) 585500

Sales 1000000

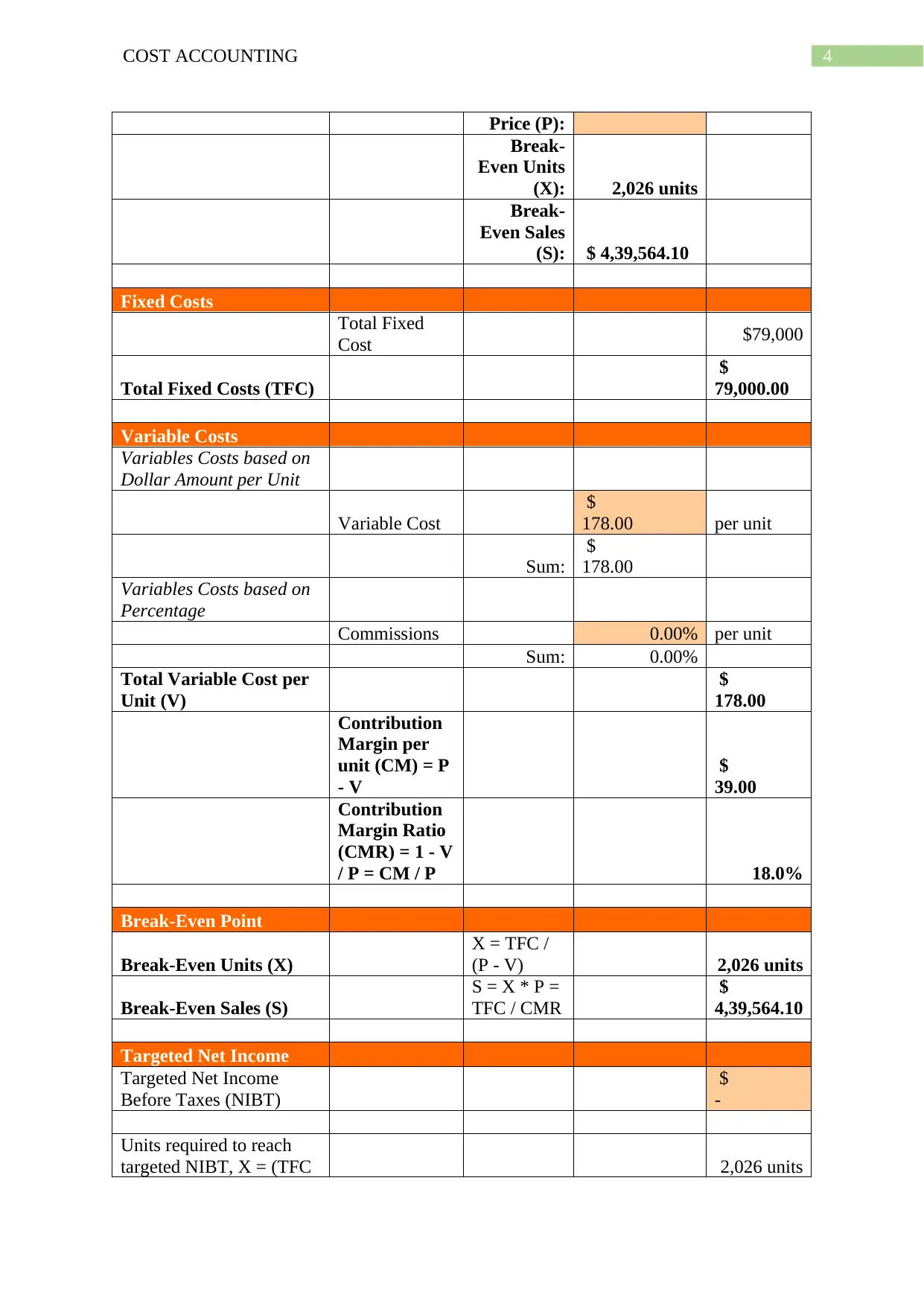

Answer to question 3:

Break-Even Analysis

Selling $ 217.00

c. Cost accounting can be classified based on the relationship with accounting period

such as capital expenses and revenue expenses.

Answer to question 2: Cost Sheet:

Cost Sheet

Particulars Amount ($) Amount ($)

Materials Consumed

Opening Stock of Raw Materials 10000

Purchase 225000

Less: Closing Stock 7500

Raw Materials Consumed 227500

Add: Wages Paid 110000

Prime Cost 337500

Works Overhead

Factory Overhead 40500

Add: Opening W-I-P 5000

Less: Closing W-I-P 6000 39500

Factory Cost 377000

Office and Administration Overhead

Administrative Overhead 25000

Cost of Production 402000

Add: Opening Stock of Finished Goods 25000

427000

Less: Closing Stock of Finished Goods 22500

Cost of Goods Sold 404500

Selling and Distribution Overhead

Selling and Distribution Overhead Expenses 10000

Cost of Sales 414500

Profit (Balancing Figure) 585500

Sales 1000000

Answer to question 3:

Break-Even Analysis

Selling $ 217.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COST ACCOUNTING

Price (P):

Break-

Even Units

(X): 2,026 units

Break-

Even Sales

(S): $ 4,39,564.10

[42]

Fixed Costs

Total Fixed

Cost $79,000

Total Fixed Costs (TFC)

$

79,000.00

Variable Costs

Variables Costs based on

Dollar Amount per Unit

Variable Cost

$

178.00 per unit

Sum:

$

178.00

Variables Costs based on

Percentage

Commissions 0.00% per unit

Sum: 0.00%

Total Variable Cost per

Unit (V)

$

178.00

Contribution

Margin per

unit (CM) = P

- V

$

39.00

Contribution

Margin Ratio

(CMR) = 1 - V

/ P = CM / P 18.0%

Break-Even Point

Break-Even Units (X)

X = TFC /

(P - V) 2,026 units

Break-Even Sales (S)

S = X * P =

TFC / CMR

$

4,39,564.10

Targeted Net Income

Targeted Net Income

Before Taxes (NIBT)

$

-

Units required to reach

targeted NIBT, X = (TFC 2,026 units

Price (P):

Break-

Even Units

(X): 2,026 units

Break-

Even Sales

(S): $ 4,39,564.10

[42]

Fixed Costs

Total Fixed

Cost $79,000

Total Fixed Costs (TFC)

$

79,000.00

Variable Costs

Variables Costs based on

Dollar Amount per Unit

Variable Cost

$

178.00 per unit

Sum:

$

178.00

Variables Costs based on

Percentage

Commissions 0.00% per unit

Sum: 0.00%

Total Variable Cost per

Unit (V)

$

178.00

Contribution

Margin per

unit (CM) = P

- V

$

39.00

Contribution

Margin Ratio

(CMR) = 1 - V

/ P = CM / P 18.0%

Break-Even Point

Break-Even Units (X)

X = TFC /

(P - V) 2,026 units

Break-Even Sales (S)

S = X * P =

TFC / CMR

$

4,39,564.10

Targeted Net Income

Targeted Net Income

Before Taxes (NIBT)

$

-

Units required to reach

targeted NIBT, X = (TFC 2,026 units

5COST ACCOUNTING

+ NIBT) / (P-V)

Sales required to reach

targeted NIBT, S = (TFC

+ NIBT) / CMR

$

4,39,564.10

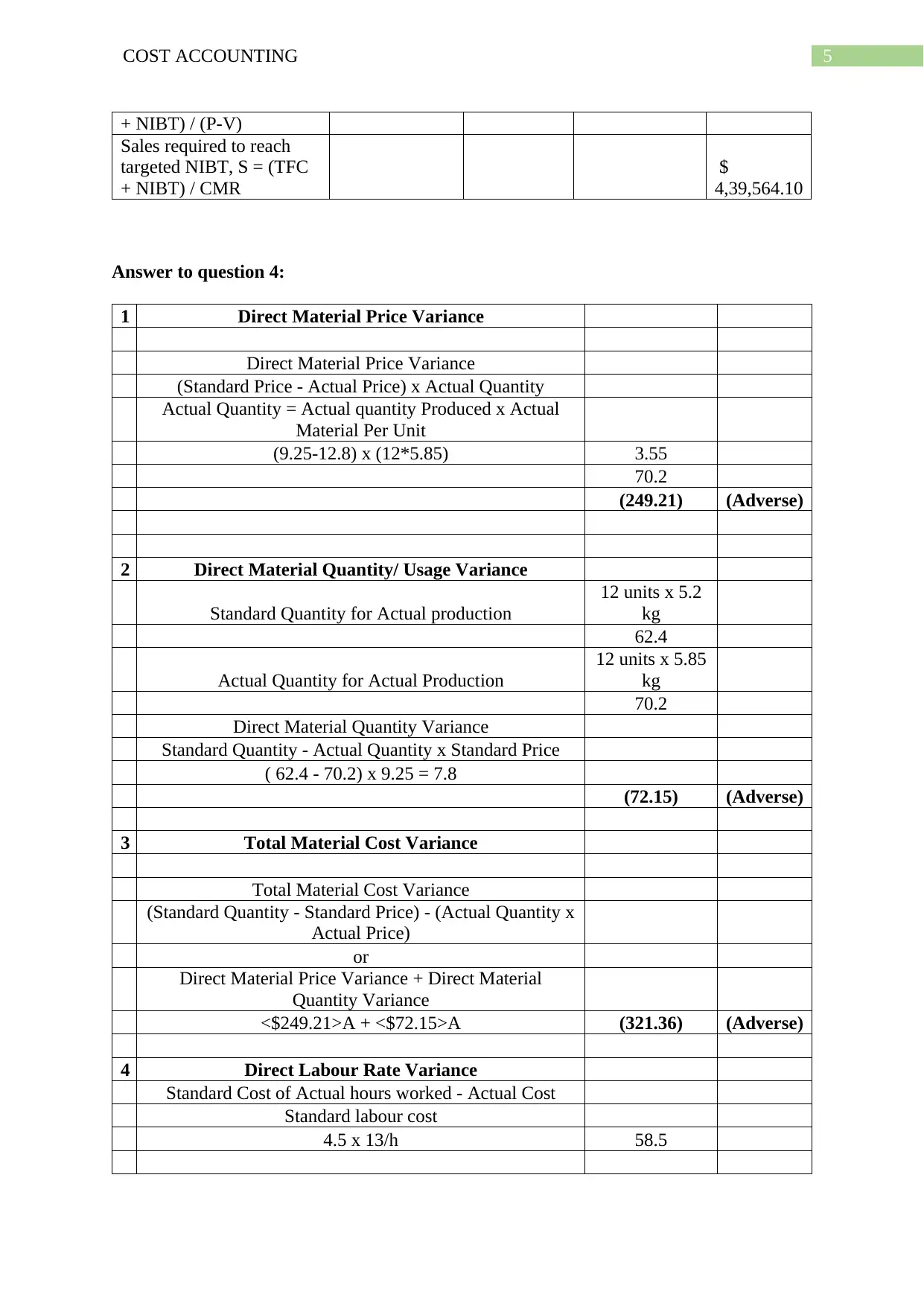

Answer to question 4:

1 Direct Material Price Variance

Direct Material Price Variance

(Standard Price - Actual Price) x Actual Quantity

Actual Quantity = Actual quantity Produced x Actual

Material Per Unit

(9.25-12.8) x (12*5.85) 3.55

70.2

(249.21) (Adverse)

2 Direct Material Quantity/ Usage Variance

Standard Quantity for Actual production

12 units x 5.2

kg

62.4

Actual Quantity for Actual Production

12 units x 5.85

kg

70.2

Direct Material Quantity Variance

Standard Quantity - Actual Quantity x Standard Price

( 62.4 - 70.2) x 9.25 = 7.8

(72.15) (Adverse)

3 Total Material Cost Variance

Total Material Cost Variance

(Standard Quantity - Standard Price) - (Actual Quantity x

Actual Price)

or

Direct Material Price Variance + Direct Material

Quantity Variance

<$249.21>A + <$72.15>A (321.36) (Adverse)

4 Direct Labour Rate Variance

Standard Cost of Actual hours worked - Actual Cost

Standard labour cost

4.5 x 13/h 58.5

+ NIBT) / (P-V)

Sales required to reach

targeted NIBT, S = (TFC

+ NIBT) / CMR

$

4,39,564.10

Answer to question 4:

1 Direct Material Price Variance

Direct Material Price Variance

(Standard Price - Actual Price) x Actual Quantity

Actual Quantity = Actual quantity Produced x Actual

Material Per Unit

(9.25-12.8) x (12*5.85) 3.55

70.2

(249.21) (Adverse)

2 Direct Material Quantity/ Usage Variance

Standard Quantity for Actual production

12 units x 5.2

kg

62.4

Actual Quantity for Actual Production

12 units x 5.85

kg

70.2

Direct Material Quantity Variance

Standard Quantity - Actual Quantity x Standard Price

( 62.4 - 70.2) x 9.25 = 7.8

(72.15) (Adverse)

3 Total Material Cost Variance

Total Material Cost Variance

(Standard Quantity - Standard Price) - (Actual Quantity x

Actual Price)

or

Direct Material Price Variance + Direct Material

Quantity Variance

<$249.21>A + <$72.15>A (321.36) (Adverse)

4 Direct Labour Rate Variance

Standard Cost of Actual hours worked - Actual Cost

Standard labour cost

4.5 x 13/h 58.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

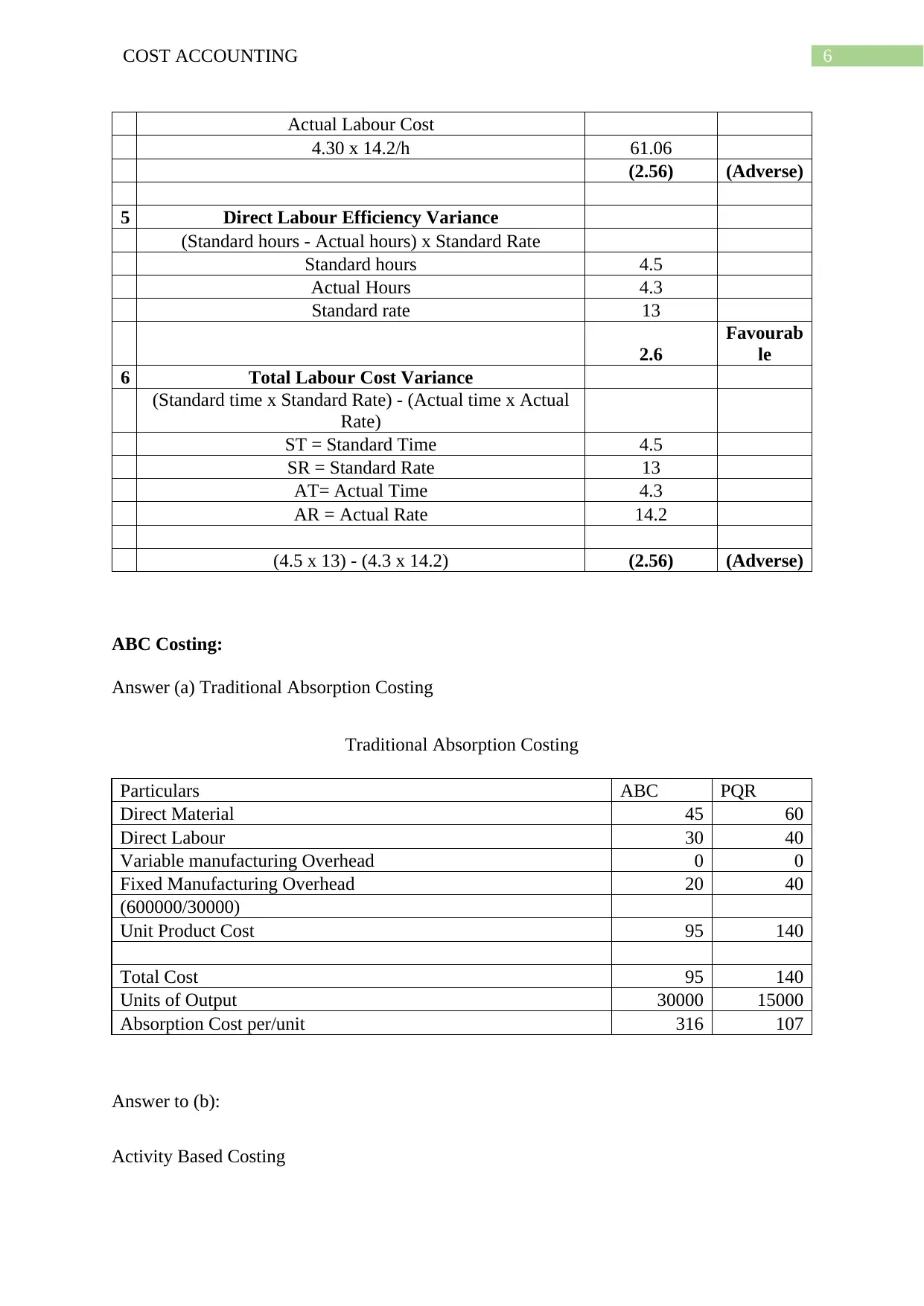

6COST ACCOUNTING

Actual Labour Cost

4.30 x 14.2/h 61.06

(2.56) (Adverse)

5 Direct Labour Efficiency Variance

(Standard hours - Actual hours) x Standard Rate

Standard hours 4.5

Actual Hours 4.3

Standard rate 13

2.6

Favourab

le

6 Total Labour Cost Variance

(Standard time x Standard Rate) - (Actual time x Actual

Rate)

ST = Standard Time 4.5

SR = Standard Rate 13

AT= Actual Time 4.3

AR = Actual Rate 14.2

(4.5 x 13) - (4.3 x 14.2) (2.56) (Adverse)

ABC Costing:

Answer (a) Traditional Absorption Costing

Traditional Absorption Costing

Particulars ABC PQR

Direct Material 45 60

Direct Labour 30 40

Variable manufacturing Overhead 0 0

Fixed Manufacturing Overhead 20 40

(600000/30000)

Unit Product Cost 95 140

Total Cost 95 140

Units of Output 30000 15000

Absorption Cost per/unit 316 107

Answer to (b):

Activity Based Costing

Actual Labour Cost

4.30 x 14.2/h 61.06

(2.56) (Adverse)

5 Direct Labour Efficiency Variance

(Standard hours - Actual hours) x Standard Rate

Standard hours 4.5

Actual Hours 4.3

Standard rate 13

2.6

Favourab

le

6 Total Labour Cost Variance

(Standard time x Standard Rate) - (Actual time x Actual

Rate)

ST = Standard Time 4.5

SR = Standard Rate 13

AT= Actual Time 4.3

AR = Actual Rate 14.2

(4.5 x 13) - (4.3 x 14.2) (2.56) (Adverse)

ABC Costing:

Answer (a) Traditional Absorption Costing

Traditional Absorption Costing

Particulars ABC PQR

Direct Material 45 60

Direct Labour 30 40

Variable manufacturing Overhead 0 0

Fixed Manufacturing Overhead 20 40

(600000/30000)

Unit Product Cost 95 140

Total Cost 95 140

Units of Output 30000 15000

Absorption Cost per/unit 316 107

Answer to (b):

Activity Based Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COST ACCOUNTING

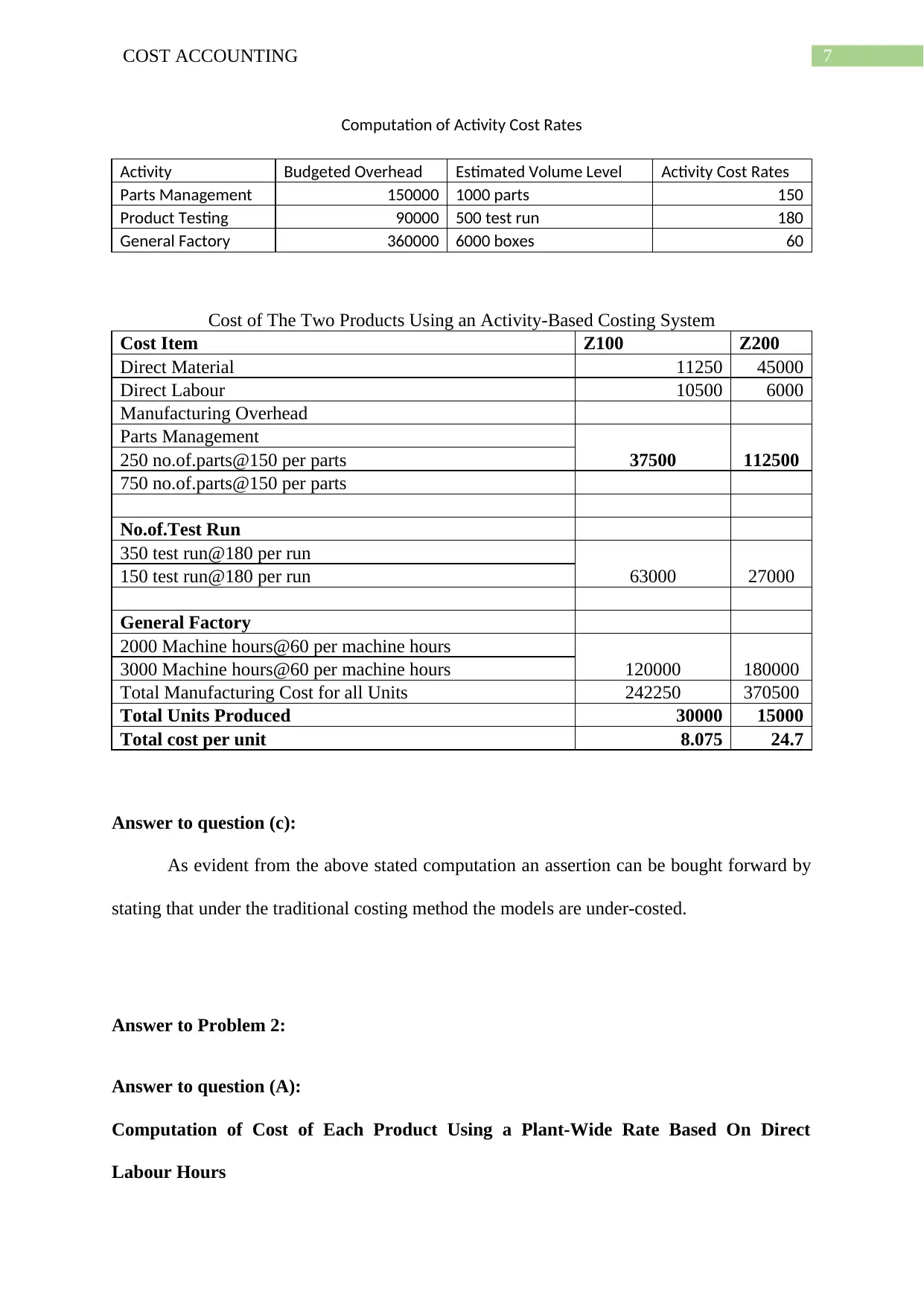

Computation of Activity Cost Rates

Activity Budgeted Overhead Estimated Volume Level Activity Cost Rates

Parts Management 150000 1000 parts 150

Product Testing 90000 500 test run 180

General Factory 360000 6000 boxes 60

Cost of The Two Products Using an Activity-Based Costing System

Cost Item Z100 Z200

Direct Material 11250 45000

Direct Labour 10500 6000

Manufacturing Overhead

Parts Management

37500 112500250 no.of.parts@150 per parts

750 no.of.parts@150 per parts

No.of.Test Run

350 test run@180 per run

63000 27000150 test run@180 per run

General Factory

2000 Machine hours@60 per machine hours

120000 1800003000 Machine hours@60 per machine hours

Total Manufacturing Cost for all Units 242250 370500

Total Units Produced 30000 15000

Total cost per unit 8.075 24.7

Answer to question (c):

As evident from the above stated computation an assertion can be bought forward by

stating that under the traditional costing method the models are under-costed.

Answer to Problem 2:

Answer to question (A):

Computation of Cost of Each Product Using a Plant-Wide Rate Based On Direct

Labour Hours

Computation of Activity Cost Rates

Activity Budgeted Overhead Estimated Volume Level Activity Cost Rates

Parts Management 150000 1000 parts 150

Product Testing 90000 500 test run 180

General Factory 360000 6000 boxes 60

Cost of The Two Products Using an Activity-Based Costing System

Cost Item Z100 Z200

Direct Material 11250 45000

Direct Labour 10500 6000

Manufacturing Overhead

Parts Management

37500 112500250 no.of.parts@150 per parts

750 no.of.parts@150 per parts

No.of.Test Run

350 test run@180 per run

63000 27000150 test run@180 per run

General Factory

2000 Machine hours@60 per machine hours

120000 1800003000 Machine hours@60 per machine hours

Total Manufacturing Cost for all Units 242250 370500

Total Units Produced 30000 15000

Total cost per unit 8.075 24.7

Answer to question (c):

As evident from the above stated computation an assertion can be bought forward by

stating that under the traditional costing method the models are under-costed.

Answer to Problem 2:

Answer to question (A):

Computation of Cost of Each Product Using a Plant-Wide Rate Based On Direct

Labour Hours

8COST ACCOUNTING

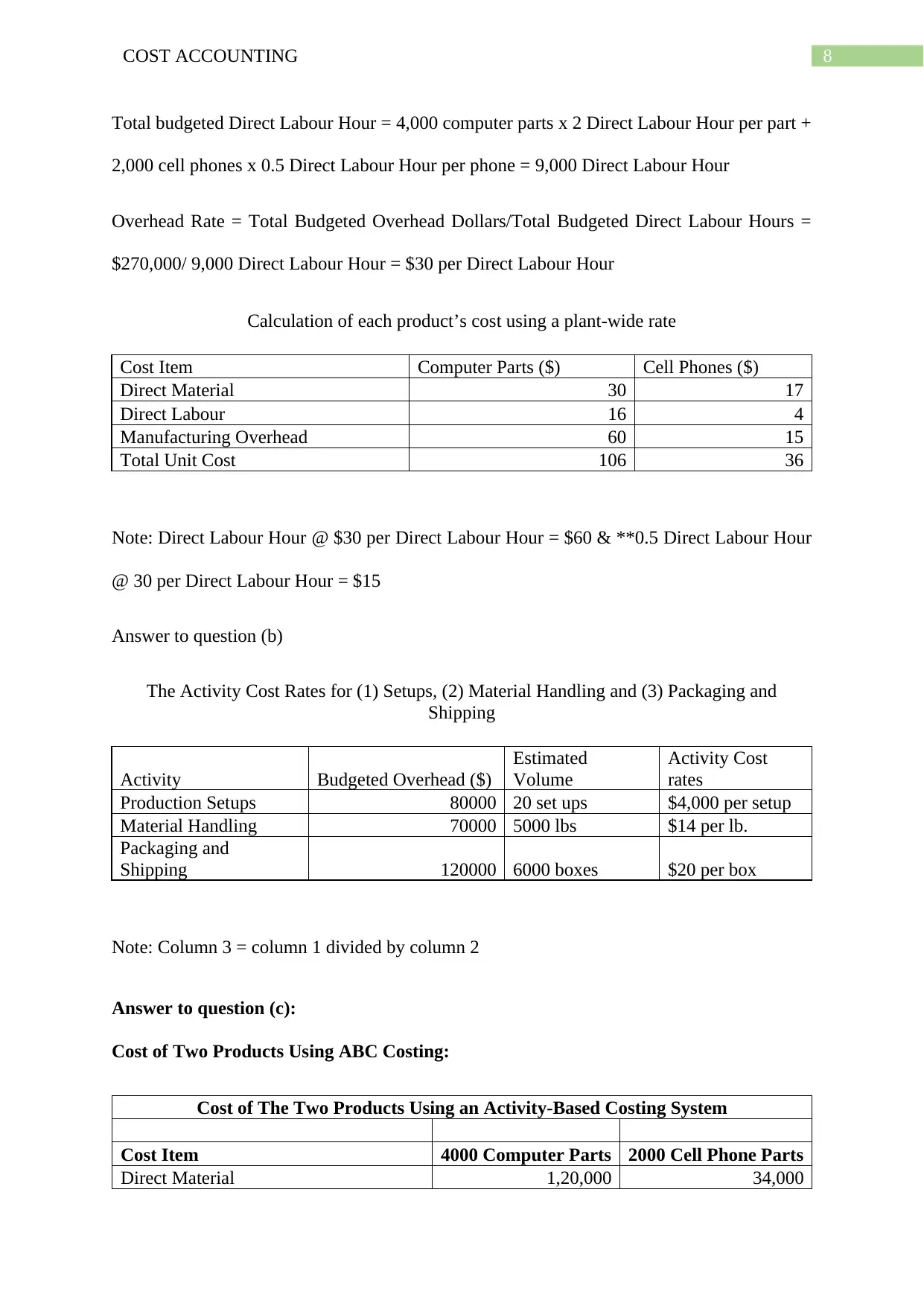

Total budgeted Direct Labour Hour = 4,000 computer parts x 2 Direct Labour Hour per part +

2,000 cell phones x 0.5 Direct Labour Hour per phone = 9,000 Direct Labour Hour

Overhead Rate = Total Budgeted Overhead Dollars/Total Budgeted Direct Labour Hours =

$270,000/ 9,000 Direct Labour Hour = $30 per Direct Labour Hour

Calculation of each product’s cost using a plant-wide rate

Cost Item Computer Parts ($) Cell Phones ($)

Direct Material 30 17

Direct Labour 16 4

Manufacturing Overhead 60 15

Total Unit Cost 106 36

Note: Direct Labour Hour @ $30 per Direct Labour Hour = $60 & **0.5 Direct Labour Hour

@ 30 per Direct Labour Hour = $15

Answer to question (b)

The Activity Cost Rates for (1) Setups, (2) Material Handling and (3) Packaging and

Shipping

Activity Budgeted Overhead ($)

Estimated

Volume

Activity Cost

rates

Production Setups 80000 20 set ups $4,000 per setup

Material Handling 70000 5000 lbs $14 per lb.

Packaging and

Shipping 120000 6000 boxes $20 per box

Note: Column 3 = column 1 divided by column 2

Answer to question (c):

Cost of Two Products Using ABC Costing:

Cost of The Two Products Using an Activity-Based Costing System

Cost Item 4000 Computer Parts 2000 Cell Phone Parts

Direct Material 1,20,000 34,000

Total budgeted Direct Labour Hour = 4,000 computer parts x 2 Direct Labour Hour per part +

2,000 cell phones x 0.5 Direct Labour Hour per phone = 9,000 Direct Labour Hour

Overhead Rate = Total Budgeted Overhead Dollars/Total Budgeted Direct Labour Hours =

$270,000/ 9,000 Direct Labour Hour = $30 per Direct Labour Hour

Calculation of each product’s cost using a plant-wide rate

Cost Item Computer Parts ($) Cell Phones ($)

Direct Material 30 17

Direct Labour 16 4

Manufacturing Overhead 60 15

Total Unit Cost 106 36

Note: Direct Labour Hour @ $30 per Direct Labour Hour = $60 & **0.5 Direct Labour Hour

@ 30 per Direct Labour Hour = $15

Answer to question (b)

The Activity Cost Rates for (1) Setups, (2) Material Handling and (3) Packaging and

Shipping

Activity Budgeted Overhead ($)

Estimated

Volume

Activity Cost

rates

Production Setups 80000 20 set ups $4,000 per setup

Material Handling 70000 5000 lbs $14 per lb.

Packaging and

Shipping 120000 6000 boxes $20 per box

Note: Column 3 = column 1 divided by column 2

Answer to question (c):

Cost of Two Products Using ABC Costing:

Cost of The Two Products Using an Activity-Based Costing System

Cost Item 4000 Computer Parts 2000 Cell Phone Parts

Direct Material 1,20,000 34,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COST ACCOUNTING

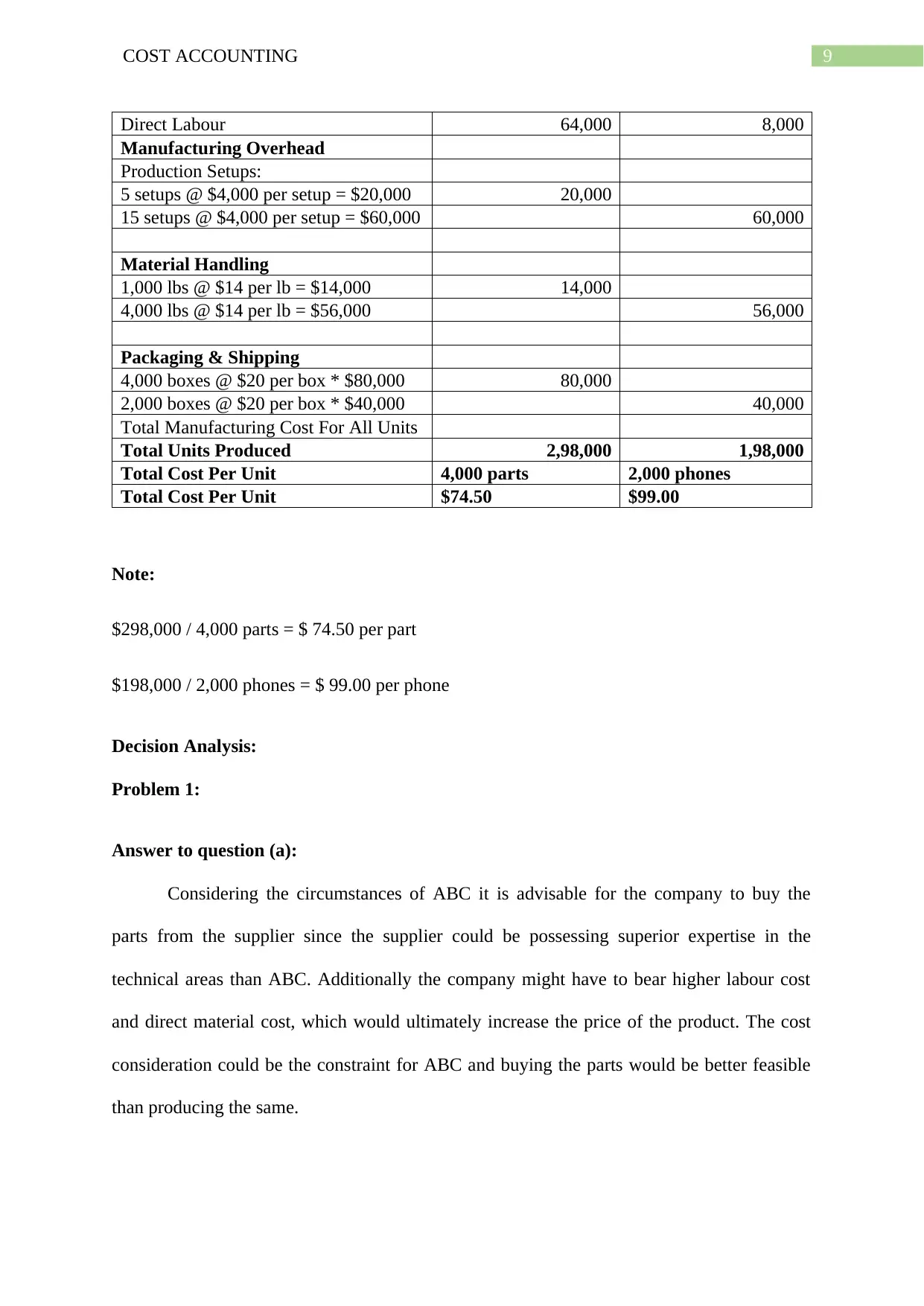

Direct Labour 64,000 8,000

Manufacturing Overhead

Production Setups:

5 setups @ $4,000 per setup = $20,000 20,000

15 setups @ $4,000 per setup = $60,000 60,000

Material Handling

1,000 lbs @ $14 per lb = $14,000 14,000

4,000 lbs @ $14 per lb = $56,000 56,000

Packaging & Shipping

4,000 boxes @ $20 per box * $80,000 80,000

2,000 boxes @ $20 per box * $40,000 40,000

Total Manufacturing Cost For All Units

Total Units Produced 2,98,000 1,98,000

Total Cost Per Unit 4,000 parts 2,000 phones

Total Cost Per Unit $74.50 $99.00

Note:

$298,000 / 4,000 parts = $ 74.50 per part

$198,000 / 2,000 phones = $ 99.00 per phone

Decision Analysis:

Problem 1:

Answer to question (a):

Considering the circumstances of ABC it is advisable for the company to buy the

parts from the supplier since the supplier could be possessing superior expertise in the

technical areas than ABC. Additionally the company might have to bear higher labour cost

and direct material cost, which would ultimately increase the price of the product. The cost

consideration could be the constraint for ABC and buying the parts would be better feasible

than producing the same.

Direct Labour 64,000 8,000

Manufacturing Overhead

Production Setups:

5 setups @ $4,000 per setup = $20,000 20,000

15 setups @ $4,000 per setup = $60,000 60,000

Material Handling

1,000 lbs @ $14 per lb = $14,000 14,000

4,000 lbs @ $14 per lb = $56,000 56,000

Packaging & Shipping

4,000 boxes @ $20 per box * $80,000 80,000

2,000 boxes @ $20 per box * $40,000 40,000

Total Manufacturing Cost For All Units

Total Units Produced 2,98,000 1,98,000

Total Cost Per Unit 4,000 parts 2,000 phones

Total Cost Per Unit $74.50 $99.00

Note:

$298,000 / 4,000 parts = $ 74.50 per part

$198,000 / 2,000 phones = $ 99.00 per phone

Decision Analysis:

Problem 1:

Answer to question (a):

Considering the circumstances of ABC it is advisable for the company to buy the

parts from the supplier since the supplier could be possessing superior expertise in the

technical areas than ABC. Additionally the company might have to bear higher labour cost

and direct material cost, which would ultimately increase the price of the product. The cost

consideration could be the constraint for ABC and buying the parts would be better feasible

than producing the same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COST ACCOUNTING

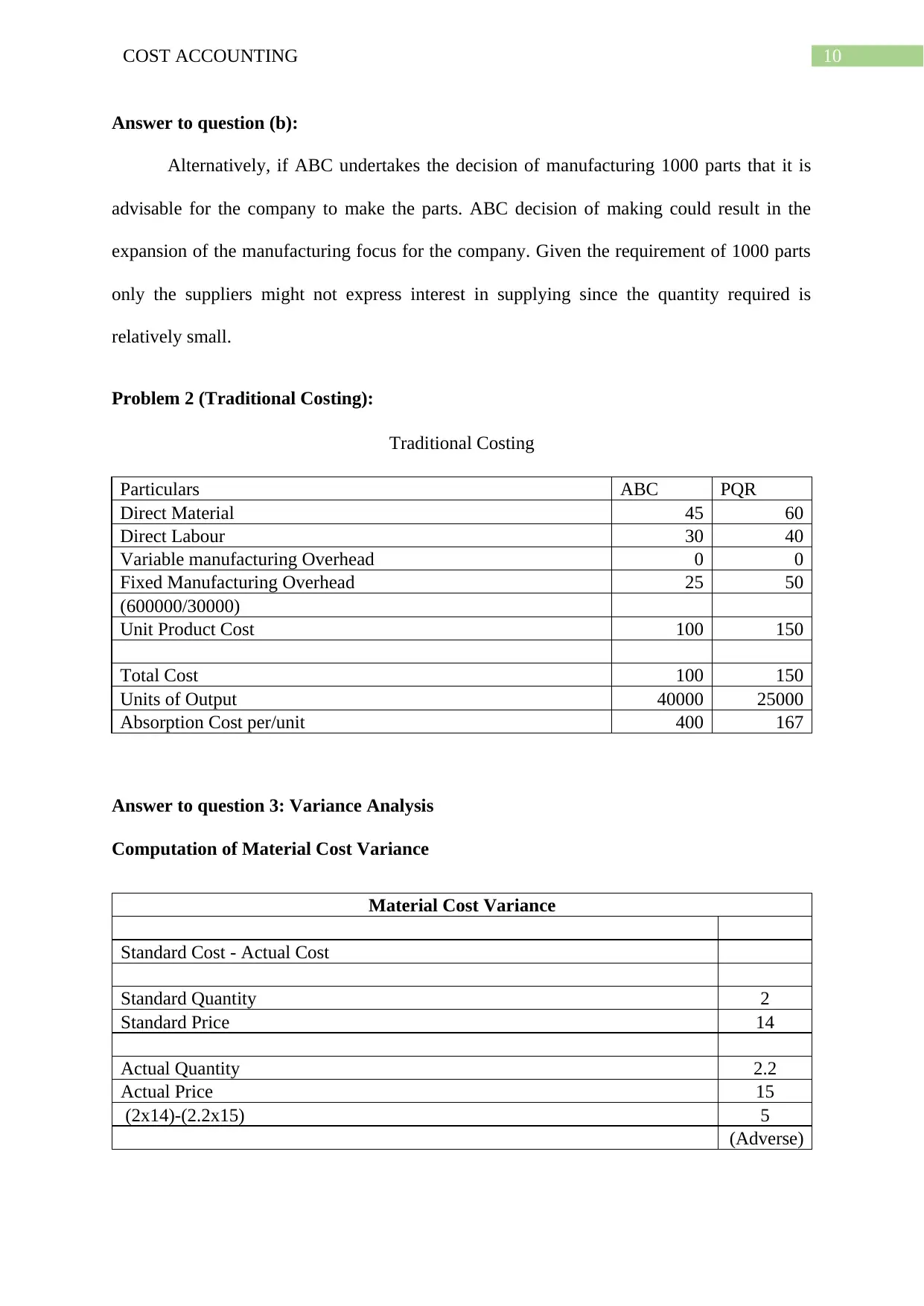

Answer to question (b):

Alternatively, if ABC undertakes the decision of manufacturing 1000 parts that it is

advisable for the company to make the parts. ABC decision of making could result in the

expansion of the manufacturing focus for the company. Given the requirement of 1000 parts

only the suppliers might not express interest in supplying since the quantity required is

relatively small.

Problem 2 (Traditional Costing):

Traditional Costing

Particulars ABC PQR

Direct Material 45 60

Direct Labour 30 40

Variable manufacturing Overhead 0 0

Fixed Manufacturing Overhead 25 50

(600000/30000)

Unit Product Cost 100 150

Total Cost 100 150

Units of Output 40000 25000

Absorption Cost per/unit 400 167

Answer to question 3: Variance Analysis

Computation of Material Cost Variance

Material Cost Variance

Standard Cost - Actual Cost

Standard Quantity 2

Standard Price 14

Actual Quantity 2.2

Actual Price 15

(2x14)-(2.2x15) 5

(Adverse)

Answer to question (b):

Alternatively, if ABC undertakes the decision of manufacturing 1000 parts that it is

advisable for the company to make the parts. ABC decision of making could result in the

expansion of the manufacturing focus for the company. Given the requirement of 1000 parts

only the suppliers might not express interest in supplying since the quantity required is

relatively small.

Problem 2 (Traditional Costing):

Traditional Costing

Particulars ABC PQR

Direct Material 45 60

Direct Labour 30 40

Variable manufacturing Overhead 0 0

Fixed Manufacturing Overhead 25 50

(600000/30000)

Unit Product Cost 100 150

Total Cost 100 150

Units of Output 40000 25000

Absorption Cost per/unit 400 167

Answer to question 3: Variance Analysis

Computation of Material Cost Variance

Material Cost Variance

Standard Cost - Actual Cost

Standard Quantity 2

Standard Price 14

Actual Quantity 2.2

Actual Price 15

(2x14)-(2.2x15) 5

(Adverse)

11COST ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.