Cost and Management Accounting

VerifiedAdded on 2023/01/18

|12

|1250

|55

AI Summary

This document provides an in-depth analysis of cost and management accounting, focusing on the value chain analysis of Bega Cheese in Australia. It discusses the efficiency in operations, inbound and outbound logistics, marketing and sales, and customer support. Additionally, it covers various questions related to cost allocation and lean management accounting practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: COST AND MANAGEMENT ACCOUNTING

Cost and Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Cost and Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1COST AND MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question 1:................................................................................................................3

Answer to question 2:.................................................................................................................5

Sub part 1:..............................................................................................................................5

Sub part 2:..............................................................................................................................6

Sub part 3 and 4:....................................................................................................................6

Answer to question 3:.................................................................................................................7

Sub Part 1:..............................................................................................................................7

Sub Part 2:..............................................................................................................................7

Sub Part 3:..............................................................................................................................7

Sub Part 4:..............................................................................................................................8

Sub Part 5:..............................................................................................................................8

Sub Part 6:..............................................................................................................................8

Sub Part 7:..............................................................................................................................9

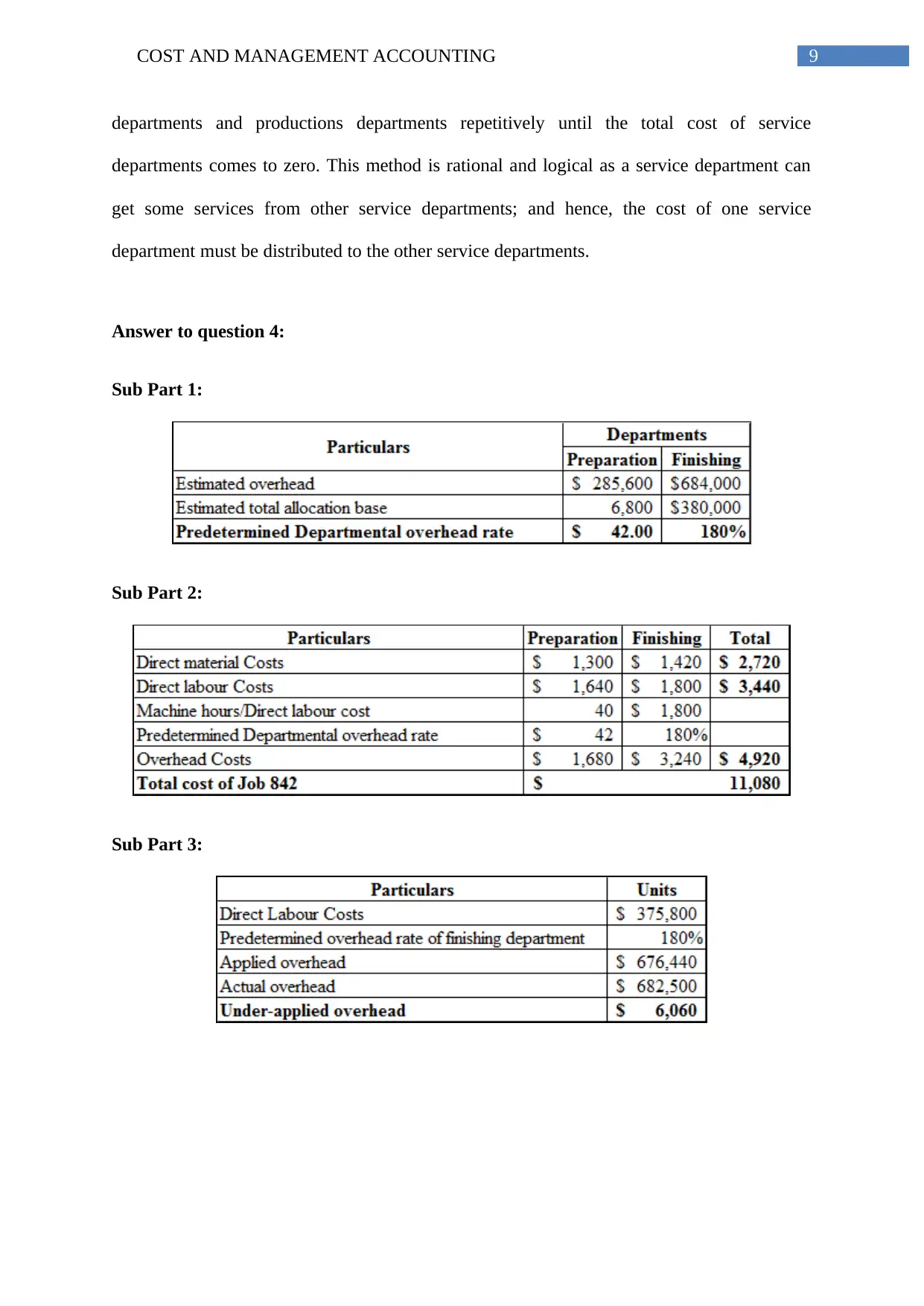

Answer to question 4:.................................................................................................................9

Sub Part 1:..............................................................................................................................9

Sub Part 2:..............................................................................................................................9

Sub Part 3:............................................................................................................................10

Answer to question 5:...............................................................................................................10

Sub Part 1:............................................................................................................................10

Sub Part 2:............................................................................................................................10

Table of Contents

Answer to Question 1:................................................................................................................3

Answer to question 2:.................................................................................................................5

Sub part 1:..............................................................................................................................5

Sub part 2:..............................................................................................................................6

Sub part 3 and 4:....................................................................................................................6

Answer to question 3:.................................................................................................................7

Sub Part 1:..............................................................................................................................7

Sub Part 2:..............................................................................................................................7

Sub Part 3:..............................................................................................................................7

Sub Part 4:..............................................................................................................................8

Sub Part 5:..............................................................................................................................8

Sub Part 6:..............................................................................................................................8

Sub Part 7:..............................................................................................................................9

Answer to question 4:.................................................................................................................9

Sub Part 1:..............................................................................................................................9

Sub Part 2:..............................................................................................................................9

Sub Part 3:............................................................................................................................10

Answer to question 5:...............................................................................................................10

Sub Part 1:............................................................................................................................10

Sub Part 2:............................................................................................................................10

2COST AND MANAGEMENT ACCOUNTING

References and bibliography:...................................................................................................11

References and bibliography:...................................................................................................11

3COST AND MANAGEMENT ACCOUNTING

Answer to Question 1:

Introduction:

Michel Porter introduced the concept of Value chain analysis, which helps in

analysing strategies of a business organization to know the competitive efficiencies of the

company. To achieve the ultimate objective of a business and the goals of their mission and

vision, they need to make efficient their inbound, outbound logistics, process flow and

operations. In this report, Began Cheese of Australia have been selected for a value chain

analysis for better experience and understanding of the topic (Cooper, 2017).

Efficiency in operations:

Began cheese is an Australian company dealing in dairy products. As it can be noticed

from the name of the company, their main product and competencies is in cheese products.

Their huge in-house dairy farm and production process helped them to achieve operational

efficiency and to meet the growing customers’ demand (begacheese.com.au, 2019).

Inbound Logistics:

Inbound logistics includes the procurement of inputs materials and creating good

relationship with the suppliers. Porters Values chain seeks the inbound logistics to be

efficient and strong enough to achieve an operational efficiency. If a good relationship can be

build up with the suppliers and partnerships then it would help the company to procure their

input materials in. Bega Cheese is having various partnerships with various suppliers who are

continuously working with the company to meet their demand of inputs .

Outbound Logistics:

Answer to Question 1:

Introduction:

Michel Porter introduced the concept of Value chain analysis, which helps in

analysing strategies of a business organization to know the competitive efficiencies of the

company. To achieve the ultimate objective of a business and the goals of their mission and

vision, they need to make efficient their inbound, outbound logistics, process flow and

operations. In this report, Began Cheese of Australia have been selected for a value chain

analysis for better experience and understanding of the topic (Cooper, 2017).

Efficiency in operations:

Began cheese is an Australian company dealing in dairy products. As it can be noticed

from the name of the company, their main product and competencies is in cheese products.

Their huge in-house dairy farm and production process helped them to achieve operational

efficiency and to meet the growing customers’ demand (begacheese.com.au, 2019).

Inbound Logistics:

Inbound logistics includes the procurement of inputs materials and creating good

relationship with the suppliers. Porters Values chain seeks the inbound logistics to be

efficient and strong enough to achieve an operational efficiency. If a good relationship can be

build up with the suppliers and partnerships then it would help the company to procure their

input materials in. Bega Cheese is having various partnerships with various suppliers who are

continuously working with the company to meet their demand of inputs .

Outbound Logistics:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COST AND MANAGEMENT ACCOUNTING

Outbound logistics means the distribution and retailing process of goods and services.

It helps an organisation to reach out to the potential customers to serve them with their

quality products and services in time. Bega Cheese Company is having a huge retail and

distribution network. They are having various franchises and partnerships with local business

entities, which help them to distribute their goods to the maximum possible customers all

over the Australia as well as to some international market (begacheese.com.au, 2019).

Marketing and sales:

Marketing and sales is a process of getting the customers known about the products

and services of a company to convert the potential customer into the actual customers. It

includes promotional activities, advertisement, various discount offers and customer

relationships. Bega Cheese’s marketing strategy through reasonable price, quality product

offering is efficient and effective to attract a huge customer. Their customer relationship

policies and activities helped them to increase their market share and retain their customer.

Customer supports and after sales services:

A company should take into consideration the feedbacks and requirements of

customers after the products are sold to the customers. Customer support service addresses all

those requirements and feedbacks of the customers. Bega Cheese is having a good customer

support team who are continuously working to improve the relationship with their customers.

In addition, they distribution system works closely with their customers and they can better

get the feedbacks from their customers (begacheese.com.au, 2019).

Lastly, it can be concluded that, the company’s efficient in-house production system,

and logistics process helped them to reach out to their customers with their quality products.

Outbound logistics means the distribution and retailing process of goods and services.

It helps an organisation to reach out to the potential customers to serve them with their

quality products and services in time. Bega Cheese Company is having a huge retail and

distribution network. They are having various franchises and partnerships with local business

entities, which help them to distribute their goods to the maximum possible customers all

over the Australia as well as to some international market (begacheese.com.au, 2019).

Marketing and sales:

Marketing and sales is a process of getting the customers known about the products

and services of a company to convert the potential customer into the actual customers. It

includes promotional activities, advertisement, various discount offers and customer

relationships. Bega Cheese’s marketing strategy through reasonable price, quality product

offering is efficient and effective to attract a huge customer. Their customer relationship

policies and activities helped them to increase their market share and retain their customer.

Customer supports and after sales services:

A company should take into consideration the feedbacks and requirements of

customers after the products are sold to the customers. Customer support service addresses all

those requirements and feedbacks of the customers. Bega Cheese is having a good customer

support team who are continuously working to improve the relationship with their customers.

In addition, they distribution system works closely with their customers and they can better

get the feedbacks from their customers (begacheese.com.au, 2019).

Lastly, it can be concluded that, the company’s efficient in-house production system,

and logistics process helped them to reach out to their customers with their quality products.

5COST AND MANAGEMENT ACCOUNTING

Answer to question 2:

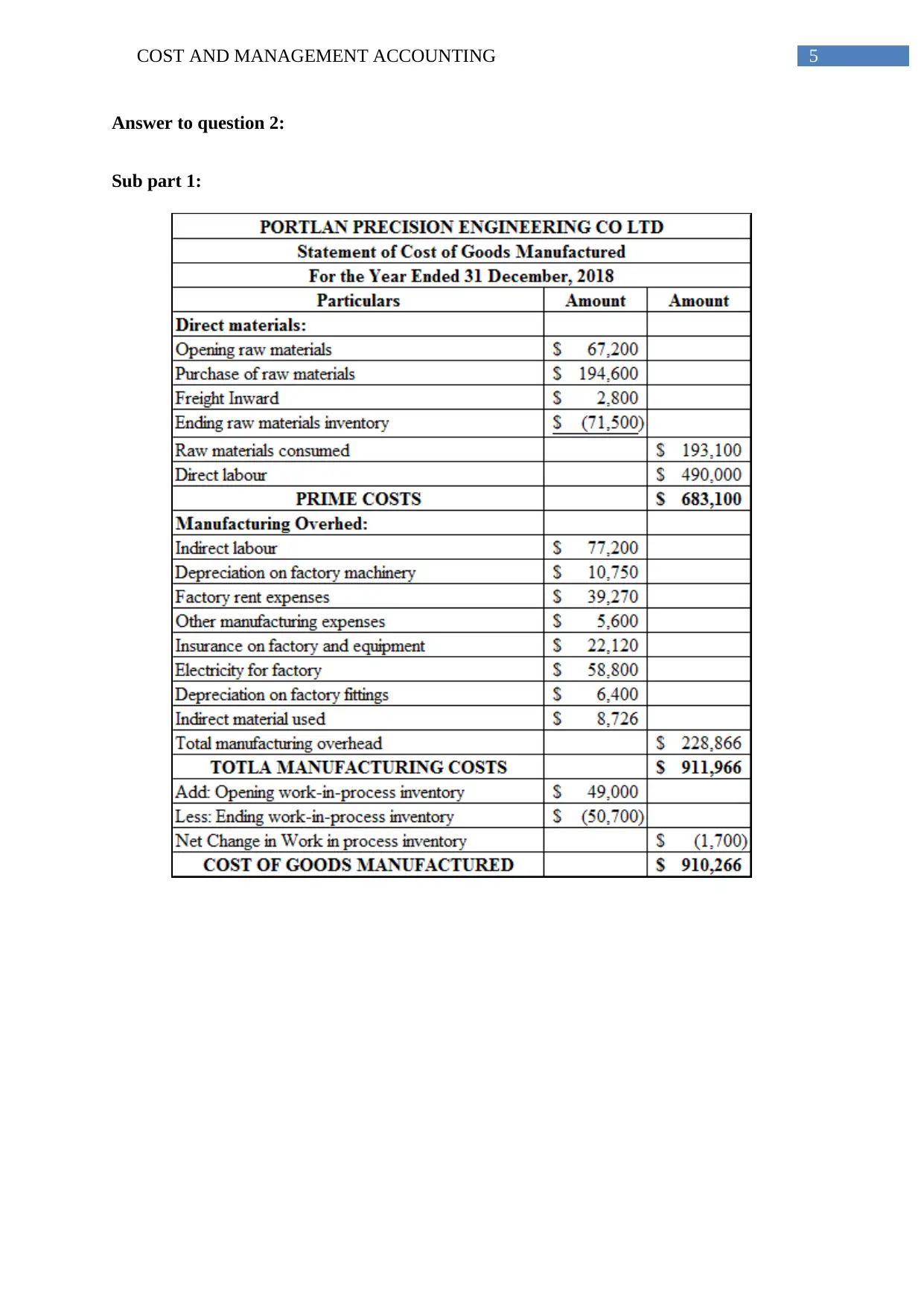

Sub part 1:

Answer to question 2:

Sub part 1:

6COST AND MANAGEMENT ACCOUNTING

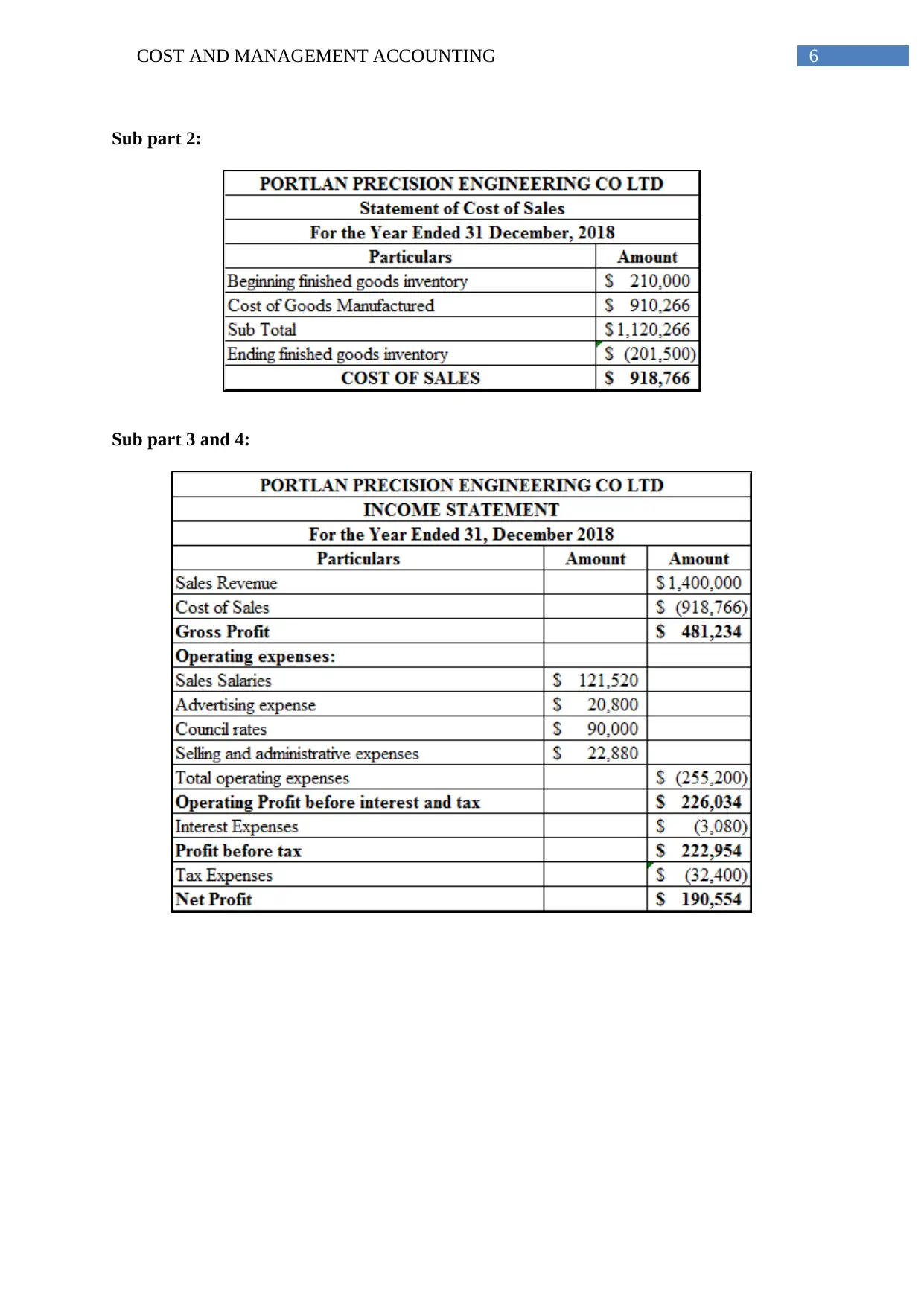

Sub part 2:

Sub part 3 and 4:

Sub part 2:

Sub part 3 and 4:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

7COST AND MANAGEMENT ACCOUNTING

Answer to question 3:

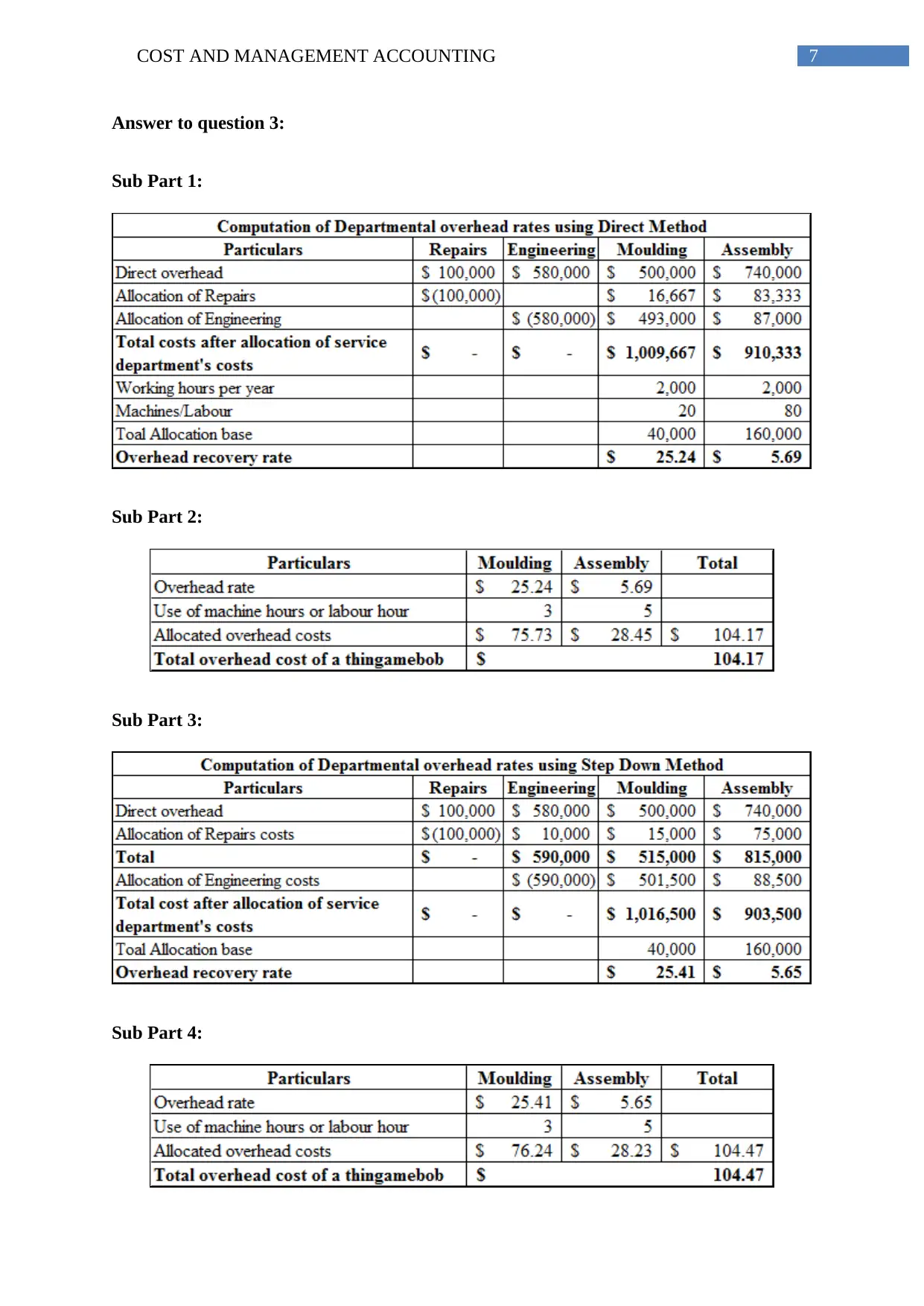

Sub Part 1:

Sub Part 2:

Sub Part 3:

Sub Part 4:

Answer to question 3:

Sub Part 1:

Sub Part 2:

Sub Part 3:

Sub Part 4:

8COST AND MANAGEMENT ACCOUNTING

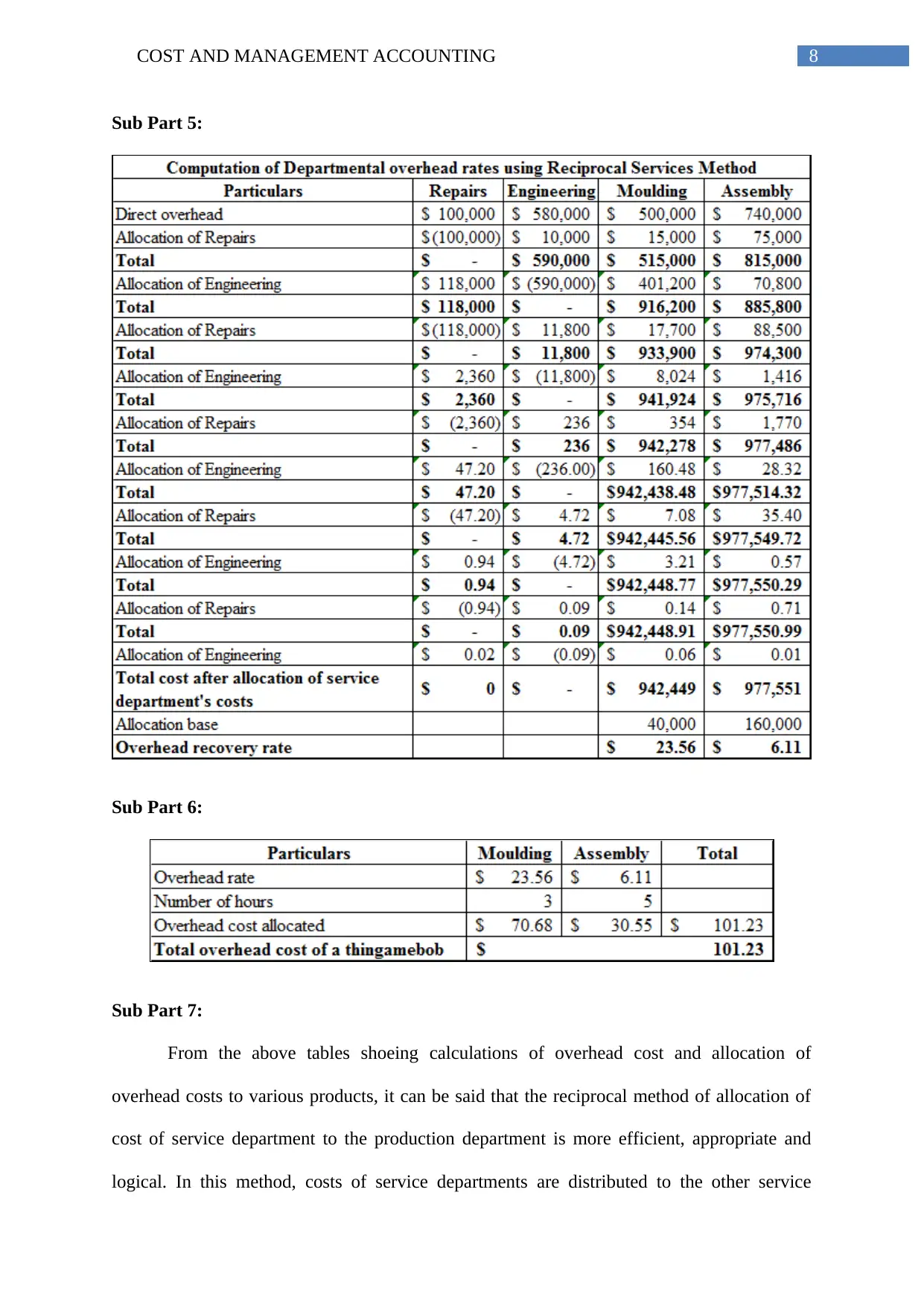

Sub Part 5:

Sub Part 6:

Sub Part 7:

From the above tables shoeing calculations of overhead cost and allocation of

overhead costs to various products, it can be said that the reciprocal method of allocation of

cost of service department to the production department is more efficient, appropriate and

logical. In this method, costs of service departments are distributed to the other service

Sub Part 5:

Sub Part 6:

Sub Part 7:

From the above tables shoeing calculations of overhead cost and allocation of

overhead costs to various products, it can be said that the reciprocal method of allocation of

cost of service department to the production department is more efficient, appropriate and

logical. In this method, costs of service departments are distributed to the other service

9COST AND MANAGEMENT ACCOUNTING

departments and productions departments repetitively until the total cost of service

departments comes to zero. This method is rational and logical as a service department can

get some services from other service departments; and hence, the cost of one service

department must be distributed to the other service departments.

Answer to question 4:

Sub Part 1:

Sub Part 2:

Sub Part 3:

departments and productions departments repetitively until the total cost of service

departments comes to zero. This method is rational and logical as a service department can

get some services from other service departments; and hence, the cost of one service

department must be distributed to the other service departments.

Answer to question 4:

Sub Part 1:

Sub Part 2:

Sub Part 3:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COST AND MANAGEMENT ACCOUNTING

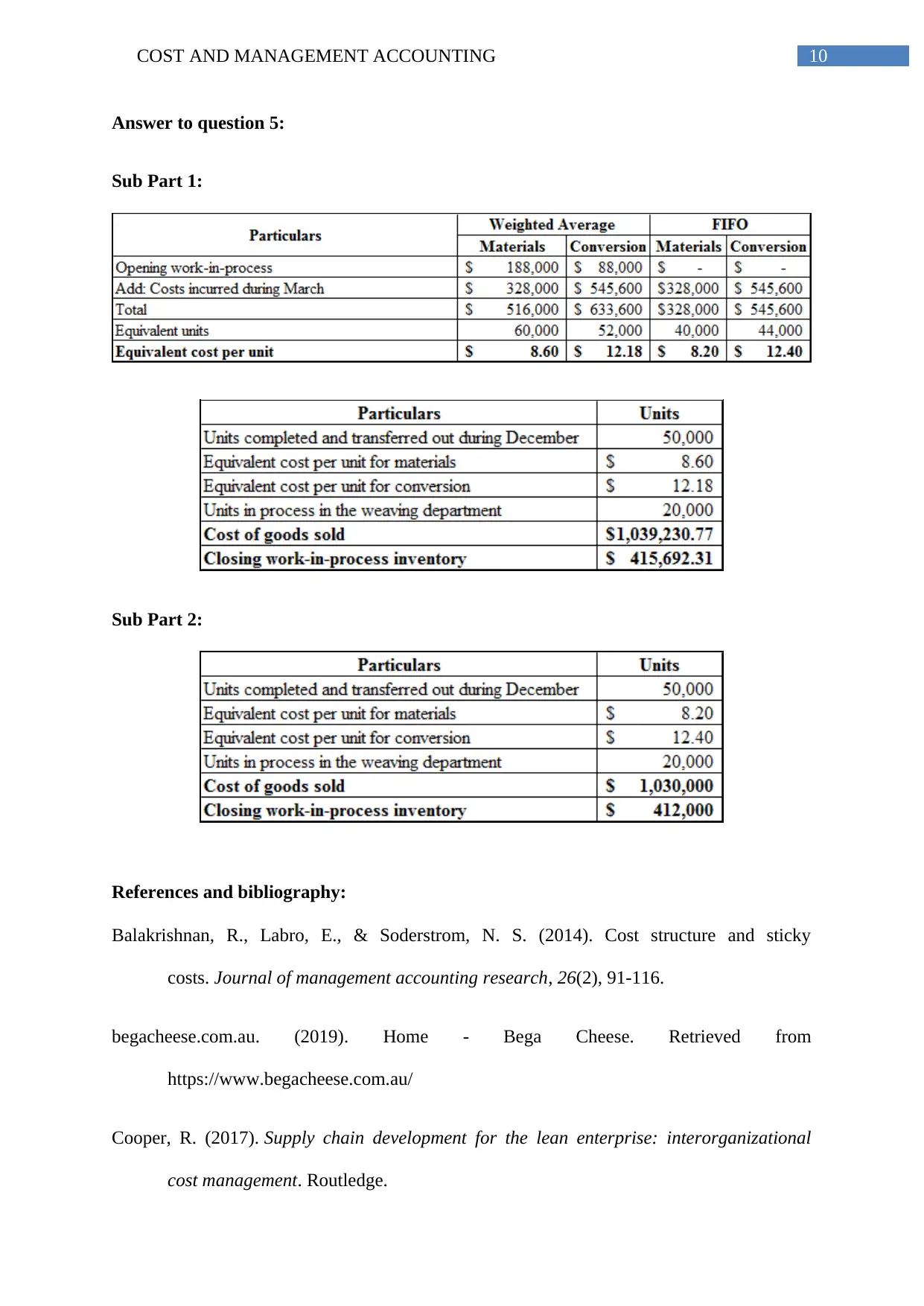

Answer to question 5:

Sub Part 1:

Sub Part 2:

References and bibliography:

Balakrishnan, R., Labro, E., & Soderstrom, N. S. (2014). Cost structure and sticky

costs. Journal of management accounting research, 26(2), 91-116.

begacheese.com.au. (2019). Home - Bega Cheese. Retrieved from

https://www.begacheese.com.au/

Cooper, R. (2017). Supply chain development for the lean enterprise: interorganizational

cost management. Routledge.

Answer to question 5:

Sub Part 1:

Sub Part 2:

References and bibliography:

Balakrishnan, R., Labro, E., & Soderstrom, N. S. (2014). Cost structure and sticky

costs. Journal of management accounting research, 26(2), 91-116.

begacheese.com.au. (2019). Home - Bega Cheese. Retrieved from

https://www.begacheese.com.au/

Cooper, R. (2017). Supply chain development for the lean enterprise: interorganizational

cost management. Routledge.

11COST AND MANAGEMENT ACCOUNTING

Fullerton, R. R., Kennedy, F. A., & Widener, S. K. (2014). Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), 414-428.

Kokubu, K., & Kitada, H. (2015). Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production, 108, 1279-1288.

Maskell, B. H., Baggaley, B., & Grasso, L. (2016). Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Parker, L. D., & Fleischman, R. K. (2017). What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

Passarini, K. C., Pereira, M. A., de Brito Farias, T. M., Calarge, F. A., & Santana, C. C.

(2014). Assessment of the viability and sustainability of an integrated waste

management system for the city of Campinas (Brazil), by means of ecological cost

accounting. Journal of Cleaner Production, 65, 479-488.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K. (2014). Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), 414-428.

Kokubu, K., & Kitada, H. (2015). Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production, 108, 1279-1288.

Maskell, B. H., Baggaley, B., & Grasso, L. (2016). Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Parker, L. D., & Fleischman, R. K. (2017). What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

Passarini, K. C., Pereira, M. A., de Brito Farias, T. M., Calarge, F. A., & Santana, C. C.

(2014). Assessment of the viability and sustainability of an integrated waste

management system for the city of Campinas (Brazil), by means of ecological cost

accounting. Journal of Cleaner Production, 65, 479-488.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.