Current Development in Accounting

VerifiedAdded on 2022/12/15

|22

|4681

|304

AI Summary

This article discusses the current developments in accounting, focusing on agenda decisions made by the IFRS Interpretations Committee. It covers topics such as accounting for deposits relating to taxes, recognition of revenue by stock exchanges, partial disposal of investments, and step acquisition of subsidiaries. The article also highlights the major issues in an exposure draft and includes comment letters from various authorities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Current Development in Accounting

Thoughts

1 | P a g e

Thoughts

1 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Answer to Question No.1............................................................................................................................3

Introduction.............................................................................................................................................3

Agenda decisions.....................................................................................................................................3

Issue 1-Accounting for deposits relating to taxes other than income taxes............................................3

Issue 2-Recognition of Revenue by any stock exchange for service of admission as well as listing

related to IFRS 15- Revenue from contracts with customers (Kalavacherla & O’Donovan, 2018)...........5

Issue 3-Partial disposal of any investment in subsidiary entity accounted for on the basis of cost

related to IAS 27- Separate financial statements....................................................................................6

Issue 4-Step acquisition of the investment in any subsidiary considered for at cost related to IAS 27 –

Separate financial statements.................................................................................................................7

Answer to Question.2..................................................................................................................................9

Outline of the major issues in Exposure Draft.........................................................................................9

Basic Standard IAS 16........................................................................................................................10

Proposed Amendment.......................................................................................................................10

Update from IASB- November 2018..................................................................................................10

Public Interest Theory............................................................................................................................11

Comment Letters...................................................................................................................................11

Letter of Grant Thornton International Limited (Appendix 1)............................................................12

Letter of RSM International Limited (Appendix 2).............................................................................12

Letter of Accounting and Tax Committee of Japan Foreign Trade Council Inc. (Appendix 3).............13

Letter from International Affairs of COMITE DE PRONUNCIAMENTOS CONTABEIS of Brasilia

(Appendix 4)......................................................................................................................................14

Role of the Regulation theory................................................................................................................14

Bibliography...............................................................................................................................................15

Appendices:...............................................................................................................................................17

2 | P a g e

Answer to Question No.1............................................................................................................................3

Introduction.............................................................................................................................................3

Agenda decisions.....................................................................................................................................3

Issue 1-Accounting for deposits relating to taxes other than income taxes............................................3

Issue 2-Recognition of Revenue by any stock exchange for service of admission as well as listing

related to IFRS 15- Revenue from contracts with customers (Kalavacherla & O’Donovan, 2018)...........5

Issue 3-Partial disposal of any investment in subsidiary entity accounted for on the basis of cost

related to IAS 27- Separate financial statements....................................................................................6

Issue 4-Step acquisition of the investment in any subsidiary considered for at cost related to IAS 27 –

Separate financial statements.................................................................................................................7

Answer to Question.2..................................................................................................................................9

Outline of the major issues in Exposure Draft.........................................................................................9

Basic Standard IAS 16........................................................................................................................10

Proposed Amendment.......................................................................................................................10

Update from IASB- November 2018..................................................................................................10

Public Interest Theory............................................................................................................................11

Comment Letters...................................................................................................................................11

Letter of Grant Thornton International Limited (Appendix 1)............................................................12

Letter of RSM International Limited (Appendix 2).............................................................................12

Letter of Accounting and Tax Committee of Japan Foreign Trade Council Inc. (Appendix 3).............13

Letter from International Affairs of COMITE DE PRONUNCIAMENTOS CONTABEIS of Brasilia

(Appendix 4)......................................................................................................................................14

Role of the Regulation theory................................................................................................................14

Bibliography...............................................................................................................................................15

Appendices:...............................................................................................................................................17

2 | P a g e

Answer to Question No.1

Introduction

This article will emphasize on current accounting issues, as published in the BDO Accounting

News, February 2019 edition. (BDONEWS, 2019) Basic objective of this article is to enhance

understanding of contemporary issues in accounting in perspective of Australian and global

context, with changes coming for application with interpretation. This article will concentrate on

the Recent Agenda Decisions of the IFRS Interpretations Committee published in BDO News

February 2019 edition in the pages from 10 to 13.

This journal will cover respective areas of the issues on measurement in accounting; the standard

setting process; and critical perspective of accounting.

Agenda decisions

IFRS Interpretation Committee had issued agenda decisions in its January 2019 meeting to

clarify four issues. They are discussed below as per the guideline of the respective news article

with specific design of fact pattern, rationales, questions related to those issues and respective

conclusions.

Issue 1-Accounting for deposits relating to taxes other than income taxes

Fact pattern-This issue is to determine the treatment of tax liability (IAS 37) (IFRS, 1998)

other than income tax (IAS 12), (Deloitte, 1996) by booking in contingent liability and not in

liability.

Question 1:

If the tax deposit is returned to the payer, will that amount give rise to asset, contingent asset

or none in the financial statement?

Rationale

The committee defined the assets as per IAS 8, (IAS, 2005) paragraph 10-11 in pursuance

with Conceptual Framework for Financial Reporting of March 2018 and earlier conceptual

3 | P a g e

Introduction

This article will emphasize on current accounting issues, as published in the BDO Accounting

News, February 2019 edition. (BDONEWS, 2019) Basic objective of this article is to enhance

understanding of contemporary issues in accounting in perspective of Australian and global

context, with changes coming for application with interpretation. This article will concentrate on

the Recent Agenda Decisions of the IFRS Interpretations Committee published in BDO News

February 2019 edition in the pages from 10 to 13.

This journal will cover respective areas of the issues on measurement in accounting; the standard

setting process; and critical perspective of accounting.

Agenda decisions

IFRS Interpretation Committee had issued agenda decisions in its January 2019 meeting to

clarify four issues. They are discussed below as per the guideline of the respective news article

with specific design of fact pattern, rationales, questions related to those issues and respective

conclusions.

Issue 1-Accounting for deposits relating to taxes other than income taxes

Fact pattern-This issue is to determine the treatment of tax liability (IAS 37) (IFRS, 1998)

other than income tax (IAS 12), (Deloitte, 1996) by booking in contingent liability and not in

liability.

Question 1:

If the tax deposit is returned to the payer, will that amount give rise to asset, contingent asset

or none in the financial statement?

Rationale

The committee defined the assets as per IAS 8, (IAS, 2005) paragraph 10-11 in pursuance

with Conceptual Framework for Financial Reporting of March 2018 and earlier conceptual

3 | P a g e

framework that if the tax deposits are to be treated as assets, it may not fall within the

specified standard with IFRS not dealing with same issues.

Conclusion

It is concluded that tax deposit is an asset as per the definition of the framework to

give the payer the benefit of future tax benefit through receipt of cash refund or

adjustment for payment of coming tax liability.

Nature of the tax deposit has no impact on this assessment and the right is not a

contingent asset as per IAS 37, as it is an asset of the payer when it is paid to the tax

authority.

Question 2:

How to recognize, measure, present and disclose the tax deposit in financial statements of the

payer?

Rationale

In absence of standard for application of the tax deposit, IAS 8 Paragraph 10-11 is to be applied

for developing proper accounting policy by the payer with the policy development criteria for

recognition, measure, presentation and disclosure of financial assets in the reports by referring

IFRS 9 and IFRS 7. (Pwc, 2017)

Conclusion

In case of application of IAS 8 Paragraph 10-11, the applicant should consider developing a

policy by recognizing, measuring, presenting and disclosing the monetary assets referred to IFRS

9 and IFRS 7.

Inference

This issue of Accounting for deposits relating to taxes other than income taxes is to enhance to

scope of measurement in accounting with standard setting process for financial reporting with

suggestion to apply IFRS 9 and 7.

4 | P a g e

specified standard with IFRS not dealing with same issues.

Conclusion

It is concluded that tax deposit is an asset as per the definition of the framework to

give the payer the benefit of future tax benefit through receipt of cash refund or

adjustment for payment of coming tax liability.

Nature of the tax deposit has no impact on this assessment and the right is not a

contingent asset as per IAS 37, as it is an asset of the payer when it is paid to the tax

authority.

Question 2:

How to recognize, measure, present and disclose the tax deposit in financial statements of the

payer?

Rationale

In absence of standard for application of the tax deposit, IAS 8 Paragraph 10-11 is to be applied

for developing proper accounting policy by the payer with the policy development criteria for

recognition, measure, presentation and disclosure of financial assets in the reports by referring

IFRS 9 and IFRS 7. (Pwc, 2017)

Conclusion

In case of application of IAS 8 Paragraph 10-11, the applicant should consider developing a

policy by recognizing, measuring, presenting and disclosing the monetary assets referred to IFRS

9 and IFRS 7.

Inference

This issue of Accounting for deposits relating to taxes other than income taxes is to enhance to

scope of measurement in accounting with standard setting process for financial reporting with

suggestion to apply IFRS 9 and 7.

4 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Issue 2-Recognition of Revenue by any stock exchange for service of admission as well as

listing related to IFRS 15- Revenue from contracts with customers (Kalavacherla &

O’Donovan, 2018)

Question

Is the promise of stock exchange to transfer the admission service from continuing listing service

justifiable?

Rationale

IFRS 15 paragraph 22 needs Stock Exchange to assess the service or good as per promise to any

customer of any contract though identification of obligation of a different performance with each

promise to transfer specific service or goods to the customers.

IFRS 15 Paragraph BC7 denotes that Stock Exchange has to identify first promised service or

good in the agreement to determine the number of obligatory performance it has with the

customer.

IFRS 15 paragraph 25 mentions that performance bindings include no activities, which any entity

must undertake for fulfilling the agreement, if not the customer got those service or good

transferred.

IFRS 15 paragraph B4 denotes that to identify action obligations during the receipt of non-

refundable, upfront fee, the entity has to assess the nature of the fee relating to promised service

or good to the customer. The first fee may be for advance for upcoming good or service.

Conclusion

The actions performed by stock exchange for execution of agreement are needed for transferring

the committed service or good to the customers. But the activities of Stock Exchange do not

transmit committed service or good to the customer except specified listing services for specific

customer. Conclusion made that Stock Exchange promises no transferable service or good for the

customer except listing services. In specific case of admittance of the customer of not getting any

service or good from Stock Exchange other than listing services, the same would be treated as

set-up costs or mobilization fees.

5 | P a g e

listing related to IFRS 15- Revenue from contracts with customers (Kalavacherla &

O’Donovan, 2018)

Question

Is the promise of stock exchange to transfer the admission service from continuing listing service

justifiable?

Rationale

IFRS 15 paragraph 22 needs Stock Exchange to assess the service or good as per promise to any

customer of any contract though identification of obligation of a different performance with each

promise to transfer specific service or goods to the customers.

IFRS 15 Paragraph BC7 denotes that Stock Exchange has to identify first promised service or

good in the agreement to determine the number of obligatory performance it has with the

customer.

IFRS 15 paragraph 25 mentions that performance bindings include no activities, which any entity

must undertake for fulfilling the agreement, if not the customer got those service or good

transferred.

IFRS 15 paragraph B4 denotes that to identify action obligations during the receipt of non-

refundable, upfront fee, the entity has to assess the nature of the fee relating to promised service

or good to the customer. The first fee may be for advance for upcoming good or service.

Conclusion

The actions performed by stock exchange for execution of agreement are needed for transferring

the committed service or good to the customers. But the activities of Stock Exchange do not

transmit committed service or good to the customer except specified listing services for specific

customer. Conclusion made that Stock Exchange promises no transferable service or good for the

customer except listing services. In specific case of admittance of the customer of not getting any

service or good from Stock Exchange other than listing services, the same would be treated as

set-up costs or mobilization fees.

5 | P a g e

Inference

This issue of Recognition of Revenue by any stock exchange for service of admission as well as

listing related to IFRS 15- Revenue from contracts with customers is highlighting the domain of

measurement in accounting with value addition to standard setting process by guiding required

treatment for the financial transaction.

Issue 3-Partial disposal of any investment in subsidiary entity accounted for on the basis of

cost related to IAS 27- Separate financial statements

Fact Pattern

An entity invests in its subsidiary measured at cost in other financial statement as per IAS 27

(ICAEW, 2014) paragraph 10a with the nature of investment as equity defined by IAS 32-

Financial Instruments: Presentation. (BDO, 2016) With subsequent disposal of investment, the

entity loses control over investee. The entity has to apply all IFRS standards as per IAS 27

paragraph 9, which is not applicable for investment specified in Paragraph 10. Post disposal, the

investee is not to be considered as subsidy, associate or joint venture. Hence, the entity applies

IFRS 9 first time to account for the remaining part of interest in the investee.

Question 1:

Confirm the eligibility of the retained investment for the presentation election under IFRS 9

(ACCAGlobal, nd) paragraph 4.1.4 related to fair value changing pattern in OCI (other

comprehensive income).

Rationale

The presentation election of OCI in IFRS 9, paragraph 4.1.4 is applicable to initial recognition

of any investment through equity instrument not held for trading. The assumption of entity’s

remaining investment not holding for trading endorses the eligibility of investment for OCI

presentation election with the first application of IFRS 9 to the retained interest or the date of

losing control by the entity.

Conclusion

6 | P a g e

This issue of Recognition of Revenue by any stock exchange for service of admission as well as

listing related to IFRS 15- Revenue from contracts with customers is highlighting the domain of

measurement in accounting with value addition to standard setting process by guiding required

treatment for the financial transaction.

Issue 3-Partial disposal of any investment in subsidiary entity accounted for on the basis of

cost related to IAS 27- Separate financial statements

Fact Pattern

An entity invests in its subsidiary measured at cost in other financial statement as per IAS 27

(ICAEW, 2014) paragraph 10a with the nature of investment as equity defined by IAS 32-

Financial Instruments: Presentation. (BDO, 2016) With subsequent disposal of investment, the

entity loses control over investee. The entity has to apply all IFRS standards as per IAS 27

paragraph 9, which is not applicable for investment specified in Paragraph 10. Post disposal, the

investee is not to be considered as subsidy, associate or joint venture. Hence, the entity applies

IFRS 9 first time to account for the remaining part of interest in the investee.

Question 1:

Confirm the eligibility of the retained investment for the presentation election under IFRS 9

(ACCAGlobal, nd) paragraph 4.1.4 related to fair value changing pattern in OCI (other

comprehensive income).

Rationale

The presentation election of OCI in IFRS 9, paragraph 4.1.4 is applicable to initial recognition

of any investment through equity instrument not held for trading. The assumption of entity’s

remaining investment not holding for trading endorses the eligibility of investment for OCI

presentation election with the first application of IFRS 9 to the retained interest or the date of

losing control by the entity.

Conclusion

6 | P a g e

IFRS 9 paragraph 4.1.4 endorses permission to the investment selling entity on preliminary

recognition for election of measurement of the retained investment at fair value through other

comprehensive income (FVTOCI).

Question 2

Does entity project the difference between cost of retained interest with respective fair value of it

on date of losing control in P & L or OCI?

Rationale

The difference between the fair value on date of losing control and the cost of retained interest of

investment complies with the definition of income or expenses as mentioned in the chapter of

Conceptual Framework of Financial Reporting. Hence by application of IAS 1 Presentation of

Financial Statements, paragraph 88, IAS 27 paragraph 9 demands the selling entity for

recognition of difference in Profit or loss, regardless of electing OCI presentation option for the

retained interest. This conclusion is showing consistency with the needs of IAS 28- Investments

in Associates and Joint Ventures, paragraph 22(b) and IAS 27 paragraph 11B which are dealing

with these types of issues.

Conclusion

The selling entity should show the difference in profit or loss account.

Inference

The issue of Partial disposal of any investment in subsidiary entity accounted for on the basis of

cost related to IAS 27- Separate financial statements emphasizes on measurement in accounting

by giving direction of the suggested treatment to be followed for the issue for proper accounting

treatment of the specific financial transactions.

Issue 4-Step acquisition of the investment in any subsidiary considered for at cost related to

IAS 27 –Separate financial statements

Fact pattern

An entity measures its investments in subsidiary bodies at its other financial statements specified

in IAS 27, Paragraph 10(a).

7 | P a g e

recognition for election of measurement of the retained investment at fair value through other

comprehensive income (FVTOCI).

Question 2

Does entity project the difference between cost of retained interest with respective fair value of it

on date of losing control in P & L or OCI?

Rationale

The difference between the fair value on date of losing control and the cost of retained interest of

investment complies with the definition of income or expenses as mentioned in the chapter of

Conceptual Framework of Financial Reporting. Hence by application of IAS 1 Presentation of

Financial Statements, paragraph 88, IAS 27 paragraph 9 demands the selling entity for

recognition of difference in Profit or loss, regardless of electing OCI presentation option for the

retained interest. This conclusion is showing consistency with the needs of IAS 28- Investments

in Associates and Joint Ventures, paragraph 22(b) and IAS 27 paragraph 11B which are dealing

with these types of issues.

Conclusion

The selling entity should show the difference in profit or loss account.

Inference

The issue of Partial disposal of any investment in subsidiary entity accounted for on the basis of

cost related to IAS 27- Separate financial statements emphasizes on measurement in accounting

by giving direction of the suggested treatment to be followed for the issue for proper accounting

treatment of the specific financial transactions.

Issue 4-Step acquisition of the investment in any subsidiary considered for at cost related to

IAS 27 –Separate financial statements

Fact pattern

An entity measures its investments in subsidiary bodies at its other financial statements specified

in IAS 27, Paragraph 10(a).

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Other investment is considered as an equity investment under IAS 32- Financial Instruments:

Presentation. This investment is not related to any joint venture, subsidiaries or associates; hence

the investment will be reported at fair value as IFRS 9.

With subsequent acquiring of additional interest in the investee, the investee becomes subsidiary

through obtaining of control by the investing identity.

Question 1

Define the process of measuring the cost of investment in subsidiary by the acquiring entity in

its separate financial statement by deriving the sum of the following considerations:

1) Fair value derivation of the preliminary interest at date of control of the subsidiary by the

acquirer and the consideration payment made for the additional interest( fair value as

deemed cost approach), or

2) The payment for consideration of the initial interest (basic consideration) and any other

payment made for consideration of additional interest (accumulated cost approach).

Rationale

IAS 27 not defines cost, nor provides specification of determining cost of investment acquired in

different stages.

The two approaches outlined in the above fact pattern generate from different views of the step

acquisition approach- if the acquiring entity is exchanging the preliminary interest and payment

for consideration made to acquire additional interest to have controlling interest in the investee;

or the acquiring entity is procuring the additional interest with retention of the preliminary

interest.

A good study of the above requirements in IFRS standards would result in the application of any

of the two probable approaches as given above. However the most suitable approach with

consistency would be applied for transactions of respective step acquisition process.

The preferred approach should be disclosed as per requirement of IAS 1, (IFRT, 2014)

paragraphs 117-124 highlighting the issues of accounting policies related to estimates and

judgments.

8 | P a g e

Presentation. This investment is not related to any joint venture, subsidiaries or associates; hence

the investment will be reported at fair value as IFRS 9.

With subsequent acquiring of additional interest in the investee, the investee becomes subsidiary

through obtaining of control by the investing identity.

Question 1

Define the process of measuring the cost of investment in subsidiary by the acquiring entity in

its separate financial statement by deriving the sum of the following considerations:

1) Fair value derivation of the preliminary interest at date of control of the subsidiary by the

acquirer and the consideration payment made for the additional interest( fair value as

deemed cost approach), or

2) The payment for consideration of the initial interest (basic consideration) and any other

payment made for consideration of additional interest (accumulated cost approach).

Rationale

IAS 27 not defines cost, nor provides specification of determining cost of investment acquired in

different stages.

The two approaches outlined in the above fact pattern generate from different views of the step

acquisition approach- if the acquiring entity is exchanging the preliminary interest and payment

for consideration made to acquire additional interest to have controlling interest in the investee;

or the acquiring entity is procuring the additional interest with retention of the preliminary

interest.

A good study of the above requirements in IFRS standards would result in the application of any

of the two probable approaches as given above. However the most suitable approach with

consistency would be applied for transactions of respective step acquisition process.

The preferred approach should be disclosed as per requirement of IAS 1, (IFRT, 2014)

paragraphs 117-124 highlighting the issues of accounting policies related to estimates and

judgments.

8 | P a g e

Conclusion

Out of the two approaches, most justified and consistent approach for step acquisition

transactions should be through disclosure as significant judgment refers to IAS 1, paragraph 122.

Question 2

As per accumulation cost approach, how difference between fair value of initial interest at the

specific date of having control of subsidiary and basic consideration be derived?

Rationale

The two factors of question 2 needs income or expenses to be defined as per Conceptual

Framework for Financial Reporting.

Hence, the acquiring entity would recognize this profit or loss as per IAS 1, paragraph 88-

presentation of Financial Statements. This is irrespective of previous selection of acquiring entity

to project fair value changes in OCI.

Conclusion

The difference of profit or loss is to be recognized by the Acquiring entity by applying

accumulation cost approach.

Inference

This issue highlighted measurement in accounting and critical perspective of accounting by

suggesting ideal solution for the Step acquisition of the investment in any subsidiary considered

for at cost related to IAS 27 –Separate financial statements.

Answer to Question.2

Outline of the major issues in Exposure Draft

This question demands discussion on any exposure draft of International Accounting Standard

Board followed by four comment letters from authorities of different status. To answer this

9 | P a g e

Out of the two approaches, most justified and consistent approach for step acquisition

transactions should be through disclosure as significant judgment refers to IAS 1, paragraph 122.

Question 2

As per accumulation cost approach, how difference between fair value of initial interest at the

specific date of having control of subsidiary and basic consideration be derived?

Rationale

The two factors of question 2 needs income or expenses to be defined as per Conceptual

Framework for Financial Reporting.

Hence, the acquiring entity would recognize this profit or loss as per IAS 1, paragraph 88-

presentation of Financial Statements. This is irrespective of previous selection of acquiring entity

to project fair value changes in OCI.

Conclusion

The difference of profit or loss is to be recognized by the Acquiring entity by applying

accumulation cost approach.

Inference

This issue highlighted measurement in accounting and critical perspective of accounting by

suggesting ideal solution for the Step acquisition of the investment in any subsidiary considered

for at cost related to IAS 27 –Separate financial statements.

Answer to Question.2

Outline of the major issues in Exposure Draft

This question demands discussion on any exposure draft of International Accounting Standard

Board followed by four comment letters from authorities of different status. To answer this

9 | P a g e

question, the selection of exposure draft is on Property, Plant and Equipment: Proceeds before

Intended Use (Amendments to IAS 16). (Standards, 2017)

Basic Standard IAS 16

The basic contribution of IAS 16 is to recognize and measure respective business assets comes

under the headings of property, plant and equipments.

Proposed Amendment

This amendment is proposed by International Accounting Standard Board with slender scope to

the standard IAS 16 (Property, Plant and Equipments) to reduce diversity while applying this

standard. This proposal had been launched by IASB in June 2017. The acceptance of comment

letter would be done till 19th October, 2017. Then, the discussions would take place to make this

amendment official for the business entities to be followed.

This amendment proposal would make prohibition of deducting the Sales value from the cost of

any item of the any specified assets falling under property, plant and equipment. This evaluation

process is applicable when that asset is being kept in the system of using through availability.

Instead of that treatment to the sale of assets, the business entity can recognize those respective

sales value and allied costs within the report of profit or loss.

This proposal for amendment is forwarded as per discussions of the IFRS Interpretations

Committee on accounting for determination of the impact of sales value and testing expenditure.

(Plus, 2018)

Update from IASB- November 2018

The Board had done discussion for proceeding with the said project- Property, Plant and

Equipment-Proceeds before Intended use; by considering the remarks received on the respective

amendment to IAS 16 Property, Plant and Equipment.

Main objective of this amendment proposal is to prohibit deduction from the value of any asset

item falling under the categories of Property, Plant and equipment when their sales take place.

The prohibition is on deduction of sales value from the value of that specific item with the

consideration to bring that asset to the specific condition and location, which is required for the

asset with the ability of delivering in operation as the company management thinks fit.

10 | P a g e

Intended Use (Amendments to IAS 16). (Standards, 2017)

Basic Standard IAS 16

The basic contribution of IAS 16 is to recognize and measure respective business assets comes

under the headings of property, plant and equipments.

Proposed Amendment

This amendment is proposed by International Accounting Standard Board with slender scope to

the standard IAS 16 (Property, Plant and Equipments) to reduce diversity while applying this

standard. This proposal had been launched by IASB in June 2017. The acceptance of comment

letter would be done till 19th October, 2017. Then, the discussions would take place to make this

amendment official for the business entities to be followed.

This amendment proposal would make prohibition of deducting the Sales value from the cost of

any item of the any specified assets falling under property, plant and equipment. This evaluation

process is applicable when that asset is being kept in the system of using through availability.

Instead of that treatment to the sale of assets, the business entity can recognize those respective

sales value and allied costs within the report of profit or loss.

This proposal for amendment is forwarded as per discussions of the IFRS Interpretations

Committee on accounting for determination of the impact of sales value and testing expenditure.

(Plus, 2018)

Update from IASB- November 2018

The Board had done discussion for proceeding with the said project- Property, Plant and

Equipment-Proceeds before Intended use; by considering the remarks received on the respective

amendment to IAS 16 Property, Plant and Equipment.

Main objective of this amendment proposal is to prohibit deduction from the value of any asset

item falling under the categories of Property, Plant and equipment when their sales take place.

The prohibition is on deduction of sales value from the value of that specific item with the

consideration to bring that asset to the specific condition and location, which is required for the

asset with the ability of delivering in operation as the company management thinks fit.

10 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The Board, in all probability, determined to go ahead with the proposed changes with insertion

of some amendments. These modifications might insert:

a. Requirement of clarification is intended from the entities regarding identification of the

costs for sales of referred items of assets produced before any item falling under

Property, Plant and Equipments, which is able to operate in expected way by the

management, and

b. Assurance of disclosure and presentation requirements.

This proposal was placed before the board with the result of eleven of fourteen Board members

agreed to these modifications, while three members have disagreed.

Public Interest Theory

This exposure draft had projected the application of public theory by the regulator. The regulator

here is IASB. This exposure draft tries to fill the gap of the existing regulation of IAS 16. Public

interest theory endorses the concept of protecting public interest through the activities of the

regulator, not entertaining the interest of any special group of people. Instead, the protection of

interest of common stakeholders of the entities is to be protected with this amendment.

Outline of the views presented by ED with agreement/disagreements by the comment letters

Comment Letters

Four comment letters are selected from the respondents of this exposure draft ES/2017/4. Those

comment letters have been selected from four different authorities or entities. The comment

letters used for this discussion are given below:

Grant Thornton International Limited, a London-based global consultancy firm

providing services to their clients in the domains of assurance, tax and advisory services.

The letter is dated 19th October, 2017.

RSM International Limited, a London-based consultancy firm providing services to their

clients in the domains of accounting, audit and consulting. The letter is dated 16th

October, 2017.

11 | P a g e

of some amendments. These modifications might insert:

a. Requirement of clarification is intended from the entities regarding identification of the

costs for sales of referred items of assets produced before any item falling under

Property, Plant and Equipments, which is able to operate in expected way by the

management, and

b. Assurance of disclosure and presentation requirements.

This proposal was placed before the board with the result of eleven of fourteen Board members

agreed to these modifications, while three members have disagreed.

Public Interest Theory

This exposure draft had projected the application of public theory by the regulator. The regulator

here is IASB. This exposure draft tries to fill the gap of the existing regulation of IAS 16. Public

interest theory endorses the concept of protecting public interest through the activities of the

regulator, not entertaining the interest of any special group of people. Instead, the protection of

interest of common stakeholders of the entities is to be protected with this amendment.

Outline of the views presented by ED with agreement/disagreements by the comment letters

Comment Letters

Four comment letters are selected from the respondents of this exposure draft ES/2017/4. Those

comment letters have been selected from four different authorities or entities. The comment

letters used for this discussion are given below:

Grant Thornton International Limited, a London-based global consultancy firm

providing services to their clients in the domains of assurance, tax and advisory services.

The letter is dated 19th October, 2017.

RSM International Limited, a London-based consultancy firm providing services to their

clients in the domains of accounting, audit and consulting. The letter is dated 16th

October, 2017.

11 | P a g e

Accounting and Tax Committee of Japan Foreign Trade Council Inc., a Tokyo-based

organization to raise voice for their eminent clients from different business aspects

including aspects of global accounting standards. The letter is dated 27th September,

2017.

COMITE DE PRONUNCIAMENTOS CONTABEIS, a Brasilia based accounting

standard setting organization, mainly to devote their efforts in theoretical and practical

approach towards accounting standard setting process in Brazil. The letter is dated 7th

July, 2017.

These letters will be discussed referred to the exposure draft for amendment of IAS 16.

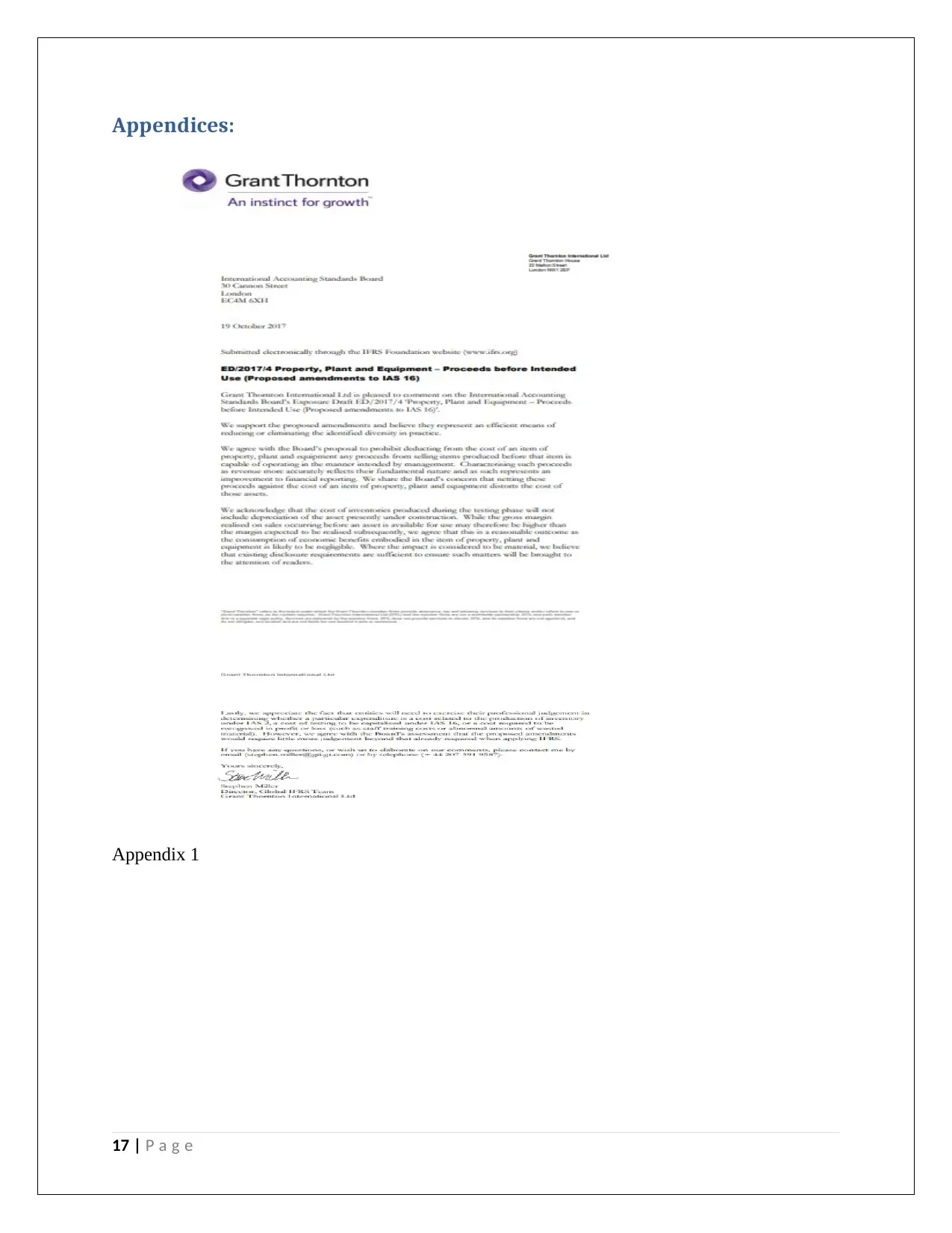

Letter of Grant Thornton International Limited (Appendix 1)

This letter was written by Stephen Miller, the Director of Global IFRS Team of Grant Thornton

International Limited. In the letter, it was mentioned that the company had agreed to the proposal

of exposure draft on the subject referred to amendment of IAS 16.

Through this letter they acknowledged the co-relation between cost of inventories, derived gross

margin and the effect of contribution by the assets to be derived for that financial information.

They have also acknowledged the disclosure of this exposure draft in the aspect of substantial

economic benefit generated for discussion. Professional acumen should be used to determine

value of inventory production under IAS 2, value of testing to be considered for capitalization

under IAS 16 and the proposed expenditure to be recognized as profit or loss due to sale of PPE

to implement this proposal placed through exposure draft. (Miller, 2017)

Letter of RSM International Limited (Appendix 2)

This letter was written by Robert Dohrer, the Global leader- Quality and Risk of RSM

International Limited. In the letter, the company agreed with the exposure draft proposal

prohibiting the deduction from the cost of PPE items during sales proceed as per discretion of the

management. They proposed to recognize the amount of sales proceeds of PPE in profit or loss

as per IFRS 15- revenue from contracts and IAS 2- inventories, which is endorsed by paragraph

21 of IAS 16 form incidental activities. At last, they extended support to this proposed transition

12 | P a g e

organization to raise voice for their eminent clients from different business aspects

including aspects of global accounting standards. The letter is dated 27th September,

2017.

COMITE DE PRONUNCIAMENTOS CONTABEIS, a Brasilia based accounting

standard setting organization, mainly to devote their efforts in theoretical and practical

approach towards accounting standard setting process in Brazil. The letter is dated 7th

July, 2017.

These letters will be discussed referred to the exposure draft for amendment of IAS 16.

Letter of Grant Thornton International Limited (Appendix 1)

This letter was written by Stephen Miller, the Director of Global IFRS Team of Grant Thornton

International Limited. In the letter, it was mentioned that the company had agreed to the proposal

of exposure draft on the subject referred to amendment of IAS 16.

Through this letter they acknowledged the co-relation between cost of inventories, derived gross

margin and the effect of contribution by the assets to be derived for that financial information.

They have also acknowledged the disclosure of this exposure draft in the aspect of substantial

economic benefit generated for discussion. Professional acumen should be used to determine

value of inventory production under IAS 2, value of testing to be considered for capitalization

under IAS 16 and the proposed expenditure to be recognized as profit or loss due to sale of PPE

to implement this proposal placed through exposure draft. (Miller, 2017)

Letter of RSM International Limited (Appendix 2)

This letter was written by Robert Dohrer, the Global leader- Quality and Risk of RSM

International Limited. In the letter, the company agreed with the exposure draft proposal

prohibiting the deduction from the cost of PPE items during sales proceed as per discretion of the

management. They proposed to recognize the amount of sales proceeds of PPE in profit or loss

as per IFRS 15- revenue from contracts and IAS 2- inventories, which is endorsed by paragraph

21 of IAS 16 form incidental activities. At last, they extended support to this proposed transition

12 | P a g e

provision of the amendment as the burden and cost of application with retrospective effect would

compensate the respective benefit. (Dohrer, 2017)

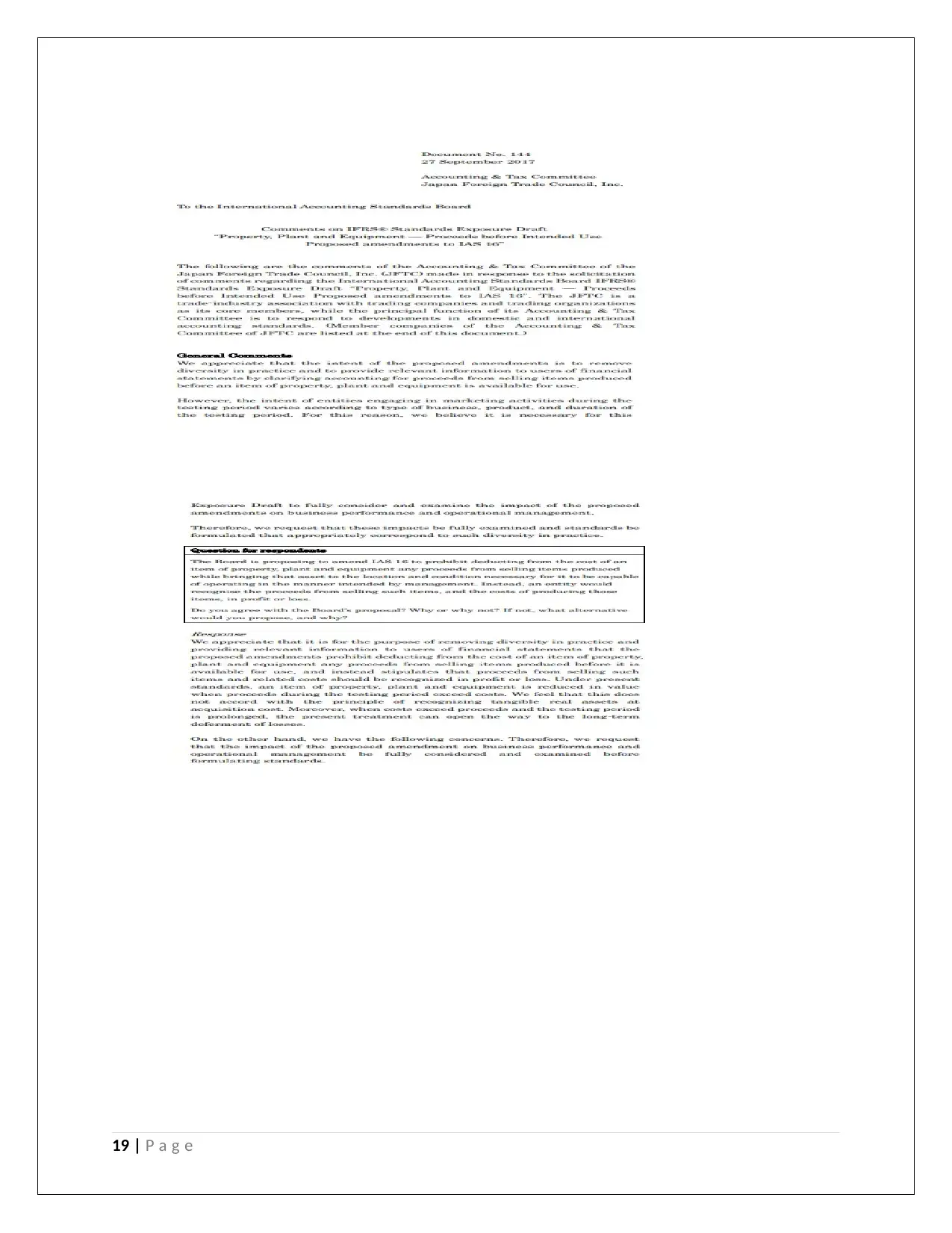

Letter of Accounting and Tax Committee of Japan Foreign Trade Council Inc. (Appendix 3)

This letter was written by Accounting and Tax Committee of Japan Foreign Trade Council Inc.

in the letter they disagreed with subsequent appeal to the International Accounting Standard

Board for considering certain impacts of this amendment proposal from the viewpoint of

different manufacturing units starting with general comments followed by response to the

question raised by IASB.

Through general comment, they have appraised the proposal of exposure draft to amend IAS 16

for PPE sales proceeds accounting treatment in profit or loss instead of adjusting the same to the

value of the assets. But they have raised concern about the impact of this amendment in case of

manufacturing units highlighting the intent of business entities engaged in production and

marketing units related to the testing period variance as per the feature of products, pattern of

business and duration of respective testing period. They have urged to the controlling authority

to examine and consider the impact of this proposed amendments on the view point of business

activities and respective operational management with the request to formulate it as per the

situation of diversity in business practice.

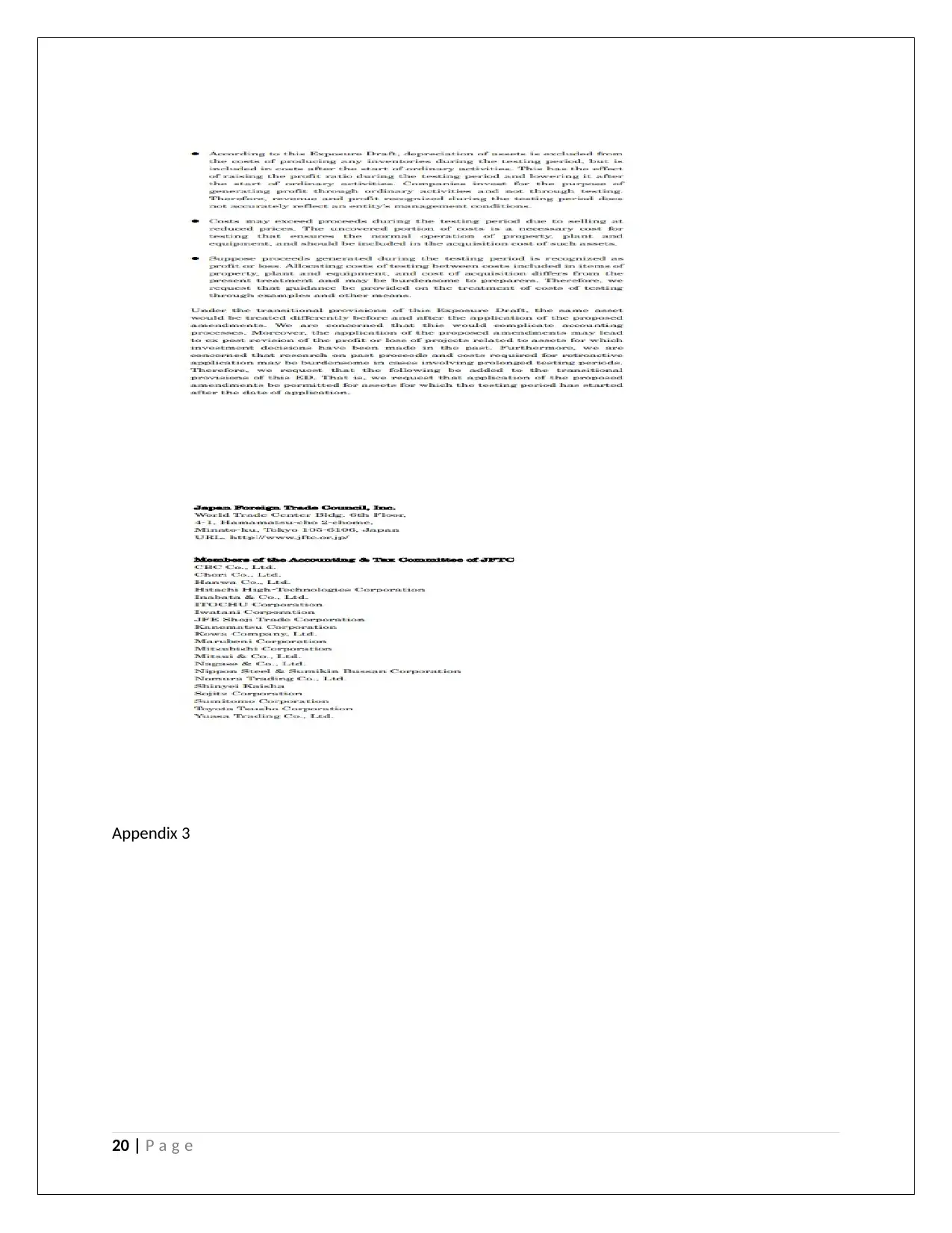

They have pointed out below mentioned questions about the application of this amendment:

The exposure draft has not clearly distinguished the role of depreciation of assets from

the production cost of inventories during testing period, but the impact of depreciation is

included in cost after the start of general activities with resultant enhancement of profit

ratio during testing period and lowering the same after the start of general activities. As

the business entities are investing in assets for general activities and not for testing

purpose to generate profit, the recognition of profit and revenue of the testing period will

not project accurately management condition of specified business entity.

With this proposal, the costs may be bigger during testing period for selling at reduced

negotiation.

13 | P a g e

compensate the respective benefit. (Dohrer, 2017)

Letter of Accounting and Tax Committee of Japan Foreign Trade Council Inc. (Appendix 3)

This letter was written by Accounting and Tax Committee of Japan Foreign Trade Council Inc.

in the letter they disagreed with subsequent appeal to the International Accounting Standard

Board for considering certain impacts of this amendment proposal from the viewpoint of

different manufacturing units starting with general comments followed by response to the

question raised by IASB.

Through general comment, they have appraised the proposal of exposure draft to amend IAS 16

for PPE sales proceeds accounting treatment in profit or loss instead of adjusting the same to the

value of the assets. But they have raised concern about the impact of this amendment in case of

manufacturing units highlighting the intent of business entities engaged in production and

marketing units related to the testing period variance as per the feature of products, pattern of

business and duration of respective testing period. They have urged to the controlling authority

to examine and consider the impact of this proposed amendments on the view point of business

activities and respective operational management with the request to formulate it as per the

situation of diversity in business practice.

They have pointed out below mentioned questions about the application of this amendment:

The exposure draft has not clearly distinguished the role of depreciation of assets from

the production cost of inventories during testing period, but the impact of depreciation is

included in cost after the start of general activities with resultant enhancement of profit

ratio during testing period and lowering the same after the start of general activities. As

the business entities are investing in assets for general activities and not for testing

purpose to generate profit, the recognition of profit and revenue of the testing period will

not project accurately management condition of specified business entity.

With this proposal, the costs may be bigger during testing period for selling at reduced

negotiation.

13 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If sales proceeds are considered as profit or loss, there should be clear directive to

differentiate the financial treatment of allocating costs of testing and cost of acquisition

of the assets. (Committee, 2017)

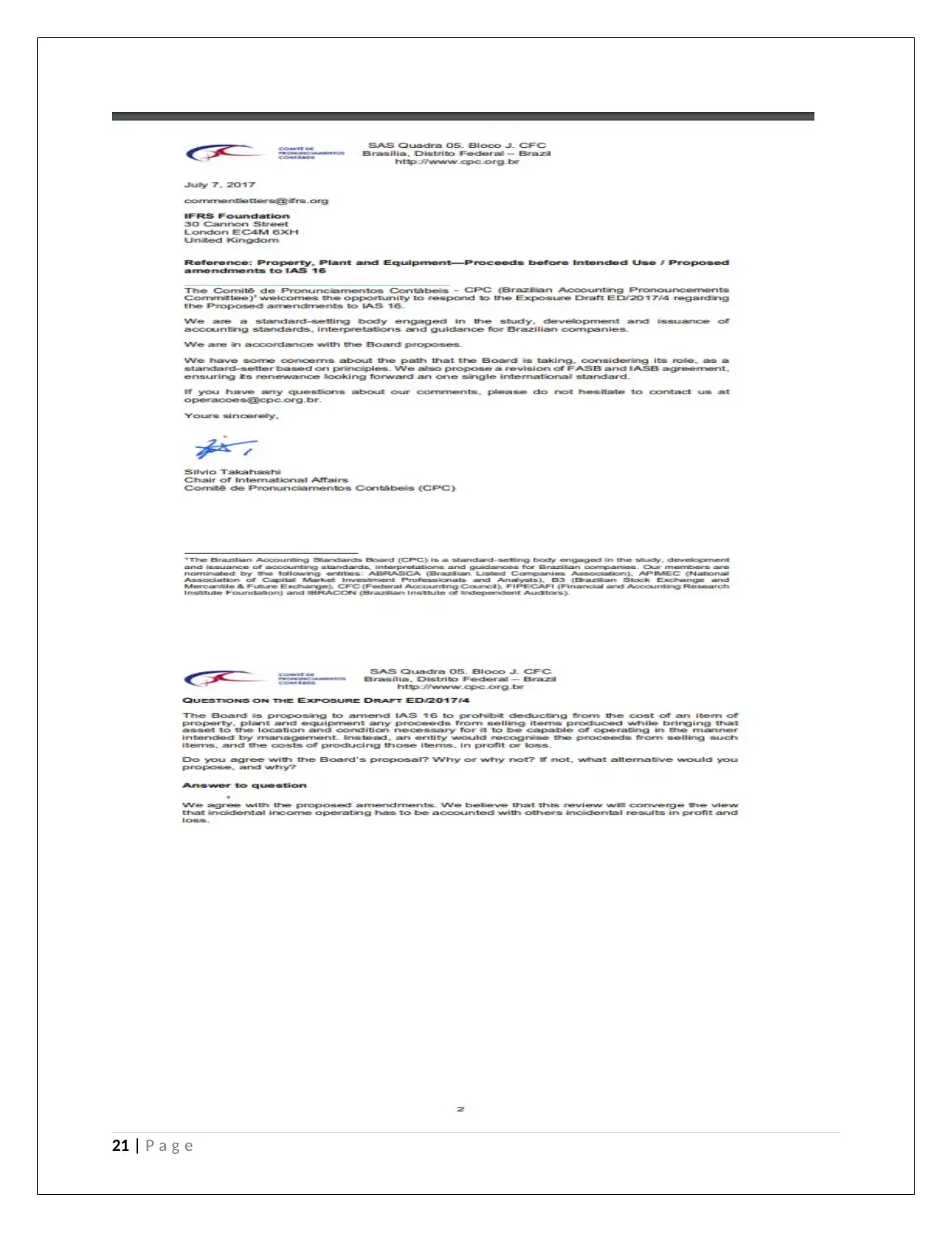

Letter from International Affairs of COMITE DE PRONUNCIAMENTOS CONTABEIS of Brasilia

(Appendix 4)

This letter was written by Silvio Takahashi, Chair of the COMITE DE PRONUNCIAMENTOS

CONTABEIS (Brazilian Accounting Standard Board) of Brasilia. In the letter they have agreed

with the proposed amendments as per the exposure draft related IAS 16. They have also reflected

their belief that this review will meet the view of operating incidental income, which should be

considered with other relevant outcomes in profit or loss.

The letter had also reiterated their concern about the route map followed by IASB regarding its

role as standard setter based on specific principles. Hence, they proposed a revision of the

agreement between FASB and IASB to ensure both will come under a single entity to control

international accounting standard setting and application. (Takahashi, 2017)

Role of the Regulation theory

There are three regulation theories- public interest theory, private interest theory and capture

theory. While public interest theory endorses the concept of secure the interest of the general

stakeholders, the private interest theory encourages to secure private interest of smll community,

and capture theory wants to influence the entire part of accounting standard or its part to favor a

certain community with political influence.

Of the four comment letters, three are from accounting related firms where as the letter from

Japan Foreign Trade Council is consortium of business entities in Japan. The three firms of

accounting, tax and audit service are endorsing the concept of this amendment, which is clear

indication of public interest theory. The letter of Japan Foreign Trade Council is representing

business entities, hence their letter had shown the indication of private interest theory to protect

the industries of Japan assembled under this organization.

14 | P a g e

differentiate the financial treatment of allocating costs of testing and cost of acquisition

of the assets. (Committee, 2017)

Letter from International Affairs of COMITE DE PRONUNCIAMENTOS CONTABEIS of Brasilia

(Appendix 4)

This letter was written by Silvio Takahashi, Chair of the COMITE DE PRONUNCIAMENTOS

CONTABEIS (Brazilian Accounting Standard Board) of Brasilia. In the letter they have agreed

with the proposed amendments as per the exposure draft related IAS 16. They have also reflected

their belief that this review will meet the view of operating incidental income, which should be

considered with other relevant outcomes in profit or loss.

The letter had also reiterated their concern about the route map followed by IASB regarding its

role as standard setter based on specific principles. Hence, they proposed a revision of the

agreement between FASB and IASB to ensure both will come under a single entity to control

international accounting standard setting and application. (Takahashi, 2017)

Role of the Regulation theory

There are three regulation theories- public interest theory, private interest theory and capture

theory. While public interest theory endorses the concept of secure the interest of the general

stakeholders, the private interest theory encourages to secure private interest of smll community,

and capture theory wants to influence the entire part of accounting standard or its part to favor a

certain community with political influence.

Of the four comment letters, three are from accounting related firms where as the letter from

Japan Foreign Trade Council is consortium of business entities in Japan. The three firms of

accounting, tax and audit service are endorsing the concept of this amendment, which is clear

indication of public interest theory. The letter of Japan Foreign Trade Council is representing

business entities, hence their letter had shown the indication of private interest theory to protect

the industries of Japan assembled under this organization.

14 | P a g e

Bibliography

ACCAGlobal. (nd). IFRS 9, Financial Instruments. Retrieved May 4, 2019, from ACCAGLOBAL website:

https://www.accaglobal.com/hk/en/student/exam-support-resources/professional-exams-

study-resources/strategic-business-reporting/technical-articles/ifrs-9.html

BDO. (2016, January 1). IAS 32 Financial Instruments: Presentation. Retrieved May 4, 2019, from BDO

Global website: https://www.bdo.global/getmedia/f82bf0ba-6e18-4952-9a33-f585e2fd0ca1/

IAS-32.pdf.aspx

BDONEWS. (2019, February). Recent Agenda Decisions of the IFRS Interpretations Committee. BDO

News , pp. 10-13.

Committee, A. a. (2017). Comments on IFRS® Standards Exposure Draft “Property, Plant and Equipment

— Proceeds before Intended Use Proposed amendments to IAS 16”. Tokyo: Japan Foregin Trade

Council Inc.

Deloitte. (1996, October). IAS 12 — Income Taxes. Retrieved May 4, 2019, from IASPLUS website:

https://www.iasplus.com/en/standards/ias/ias12

Dohrer, R. (2017). Re: Exposure Draft ED/2017/4 – Property, Plant and Equipment—Proceeds before

Intended Use (Proposed amendments to IAS 16). RSM International Limited. London: IFRS.

IAS. (2005, Decempber). IAS 8 — Accounting Policies, Changes in Accounting Estimates and Errors.

Retrieved May 4, 2019, from IAS Plus: https://www.iasplus.com/en/standards/ias/ias8

ICAEW. (2014, October). IAS 27: Separate financial statements. Retrieved May 4, 2019, from ICAEW

website: https://www.icaew.com/library/subject-gateways/accounting-standards/ifrs/ias-27

IFRS. (1998). IAS 37 Provisions, Contingent Liabilities and Contingent Assets. Retrieved May 4, 2019, from

IFRS Website: https://www.ifrs.org/issued-standards/list-of-standards/ias-37-provisions-

contingent-liabilities-and-contingent-assets/

IFRT. (2014, May 7). IAS 1 - Presentation of Financial Statements (detailed review). Retrieved May 4,

2019, from raedyratios.com website: https://www.readyratios.com/articles/ifrs/ias-1-

presentation-of-financial-statements.html

15 | P a g e

ACCAGlobal. (nd). IFRS 9, Financial Instruments. Retrieved May 4, 2019, from ACCAGLOBAL website:

https://www.accaglobal.com/hk/en/student/exam-support-resources/professional-exams-

study-resources/strategic-business-reporting/technical-articles/ifrs-9.html

BDO. (2016, January 1). IAS 32 Financial Instruments: Presentation. Retrieved May 4, 2019, from BDO

Global website: https://www.bdo.global/getmedia/f82bf0ba-6e18-4952-9a33-f585e2fd0ca1/

IAS-32.pdf.aspx

BDONEWS. (2019, February). Recent Agenda Decisions of the IFRS Interpretations Committee. BDO

News , pp. 10-13.

Committee, A. a. (2017). Comments on IFRS® Standards Exposure Draft “Property, Plant and Equipment

— Proceeds before Intended Use Proposed amendments to IAS 16”. Tokyo: Japan Foregin Trade

Council Inc.

Deloitte. (1996, October). IAS 12 — Income Taxes. Retrieved May 4, 2019, from IASPLUS website:

https://www.iasplus.com/en/standards/ias/ias12

Dohrer, R. (2017). Re: Exposure Draft ED/2017/4 – Property, Plant and Equipment—Proceeds before

Intended Use (Proposed amendments to IAS 16). RSM International Limited. London: IFRS.

IAS. (2005, Decempber). IAS 8 — Accounting Policies, Changes in Accounting Estimates and Errors.

Retrieved May 4, 2019, from IAS Plus: https://www.iasplus.com/en/standards/ias/ias8

ICAEW. (2014, October). IAS 27: Separate financial statements. Retrieved May 4, 2019, from ICAEW

website: https://www.icaew.com/library/subject-gateways/accounting-standards/ifrs/ias-27

IFRS. (1998). IAS 37 Provisions, Contingent Liabilities and Contingent Assets. Retrieved May 4, 2019, from

IFRS Website: https://www.ifrs.org/issued-standards/list-of-standards/ias-37-provisions-

contingent-liabilities-and-contingent-assets/

IFRT. (2014, May 7). IAS 1 - Presentation of Financial Statements (detailed review). Retrieved May 4,

2019, from raedyratios.com website: https://www.readyratios.com/articles/ifrs/ias-1-

presentation-of-financial-statements.html

15 | P a g e

Kalavacherla, P., & O’Donovan, B. (2018, January 31). Revenue – Are you prepared for IFRS 15? Retrieved

May 4, 2019, from KPMG website: https://home.kpmg/xx/en/home/insights/2014/05/first-

impression-revenue-2014.html

Miller, S. (2017). ED/2017/4 Property, Plant and Equipment – Proceeds before Intended Use (Proposed

amendments to IAS 16). London: Grant Thornton International Ltd.

Plus, I. (2018). Property, Plant and Equipment: Proceeds before Intended Use (Proposed Amendments to

IAS 16) [ED]. Retrieved May 4, 2019, from IASPLUS website:

https://www.iasplus.com/en-ca/projects/ifrs/exposure-drafts/property-plant-and-equipment-

proceeds-before-intended-use-proposed-amendments-to-ias-16-research

Pwc. (2017, February 14). IFRS 9, IFRS 7 - Financial instruments: Disclosure. Retrieved May 4, 2019, from

PWC website: https://inform.pwc.com/show?

action=applyInformContentTerritory&id=0903091703158809&tid=103

Standards, I. F. (2017). Property, Plant and Equipment: Proceeds before Intended Use (Amendments to

IAS 16). Retrieved May 4, 2019, from IFRS Website:

https://www.ifrs.org/projects/work-plan/property-plant-and-equipment-proceeds-before-

intended-use/

Takahashi, S. (2017). Reference: Property, Plant and Equipment—Proceeds before Intended Use /

Proposed amendments to IAS 16. Brasilia: The Comitê de Pronunciamentos Contábeis.

16 | P a g e

May 4, 2019, from KPMG website: https://home.kpmg/xx/en/home/insights/2014/05/first-

impression-revenue-2014.html

Miller, S. (2017). ED/2017/4 Property, Plant and Equipment – Proceeds before Intended Use (Proposed

amendments to IAS 16). London: Grant Thornton International Ltd.

Plus, I. (2018). Property, Plant and Equipment: Proceeds before Intended Use (Proposed Amendments to

IAS 16) [ED]. Retrieved May 4, 2019, from IASPLUS website:

https://www.iasplus.com/en-ca/projects/ifrs/exposure-drafts/property-plant-and-equipment-

proceeds-before-intended-use-proposed-amendments-to-ias-16-research

Pwc. (2017, February 14). IFRS 9, IFRS 7 - Financial instruments: Disclosure. Retrieved May 4, 2019, from

PWC website: https://inform.pwc.com/show?

action=applyInformContentTerritory&id=0903091703158809&tid=103

Standards, I. F. (2017). Property, Plant and Equipment: Proceeds before Intended Use (Amendments to

IAS 16). Retrieved May 4, 2019, from IFRS Website:

https://www.ifrs.org/projects/work-plan/property-plant-and-equipment-proceeds-before-

intended-use/

Takahashi, S. (2017). Reference: Property, Plant and Equipment—Proceeds before Intended Use /

Proposed amendments to IAS 16. Brasilia: The Comitê de Pronunciamentos Contábeis.

16 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Appendices:

Appendix 1

17 | P a g e

Appendix 1

17 | P a g e

Appendix 2

18 | P a g e

18 | P a g e

19 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix 3

20 | P a g e

20 | P a g e

21 | P a g e

Appendix 4

22 | P a g e

22 | P a g e

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.