Tesco's Data Analysis: Key Sources, Framework, and Implementation

VerifiedAdded on 2023/01/11

|19

|6871

|91

Report

AI Summary

This report provides a comprehensive analysis of Tesco's data-driven decision-making processes. It begins by identifying key data sources, including financial and non-financial data, and maps them to relevant business functions within Tesco PLC and Tesco Bank. The report highlights gaps in data integrity, such as issues with accuracy, timeliness, and completeness. It then proposes a big data analytics framework, suggesting an ERP system for financial modules to address these gaps. The implementation of this framework is outlined using the CRISP-DM methodology, detailing data understanding, business understanding, data preparation, modeling, evaluation, and deployment phases. Furthermore, the report addresses data protection and ethical considerations, emphasizing compliance with GDPR regulations. The analysis underscores Tesco's efforts to leverage data for enhanced decision-making, reduce costs, and improve consumer behavior understanding. This report is a valuable resource for students studying data analytics and business intelligence, offering insights into real-world applications of data analysis within a major retail organization.

Arden University

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Data-based decision making (DDDM) is an approach that involves the collection of information that

relies on key performance indicators or measurable indicators, the dissemination of examples and

real from these experiences and the used to create techniques and exercises for the benefit of the

business in various sectors.

Be that as it may, in order to separate the qualified inspiration from your information, it must be

accurate as applicable to your points. Collecting, separating, sorting and analyzing pieces of

information to develop knowledge-based dynamics in the business world was at the same time a

largely inclusive enterprise, which is usually different from the overall dynamic approach.

2

Data-based decision making (DDDM) is an approach that involves the collection of information that

relies on key performance indicators or measurable indicators, the dissemination of examples and

real from these experiences and the used to create techniques and exercises for the benefit of the

business in various sectors.

Be that as it may, in order to separate the qualified inspiration from your information, it must be

accurate as applicable to your points. Collecting, separating, sorting and analyzing pieces of

information to develop knowledge-based dynamics in the business world was at the same time a

largely inclusive enterprise, which is usually different from the overall dynamic approach.

2

1. What are the key sources and flows of data that are collected,

processed, stored and taken into account in the organisation’s

decision making process?

1.1. Background to the case

The organisation which is selected to be audited in this audit report is Tesco group. Tesco Group is a

group of organisations which includes retail company “Tesco PLC” and a financial institution named

Tesco Bank. Tesco PLC is a British multinational groceries and general merchandise retailer. This

company has its headquarters in England, United Kingdom and this company was formed in 1919.

The key products and services of this company include groceries, home appliances, general

merchandising and many more. The products and services of Tesco Bank includes saving and credit

of money along with products such as credit and debit cards (Ataman, Kulick and Sim, 2011).

There are two markets in which Tesco PLC operates; the first market is the retail industry in which

Tesco PLC operates. The countries to which operations of Tesco PLC are limited include United

Kingdom, United States of America, India, Spain, France, China and many more. The second market

in which Tesco operates is retail banking market. In this market, Tesco Bank operates and its

functions are limited to the region of United Kingdom only.

Instead of being operating in multiple countries, most of the operations of Tesco PLC are limited to

United Kingdom only and due to political stability of this region, there are various issues and

challenges which are being faced by Tesco(Arganda-Carreras and et. al., 2017). Tesco is a large scale

company which is impacted by every action of government. Due to BREXIT implementation,

improvement and growth ratio of Tesco has already been reduced till 2019. 2020 was the healing

year of TESCO, but due to current pandemic caused because of COVID 19, the declining of growth

continues in 2020 as well. This company is facing issues of increasing debts and reducing return on

capital employed. The revenues and profits of Tesco PLC are continuously increasing but these

profits are not compatible with the increasing number of stores of this company. The increment

trend of profits is positive but the pace of increment is decreasing.

1.2. Audit of key data sources

Financial data sources are the sourced which assist in gaining data regarding monetary

information of the company. On the other hand, non financial data sources are the sources which

helps in gaining managerial information. Tesco is a large scale company which uses annual report

and interim reports as key their key financial data sources. In addition, Tesco uses cost sheets and

inventory management report as their non financial data sources.

Table 1.1. Key financial and non-financial types of data in the case study

No Data source Data type Financial or non-financial Business units or departments

using this data

1 Annual

report

Income statement Financial Selling and Distribution

department, HR, Marketing

2 Annual

report

Balance sheet Financial Research and Development

department

3

processed, stored and taken into account in the organisation’s

decision making process?

1.1. Background to the case

The organisation which is selected to be audited in this audit report is Tesco group. Tesco Group is a

group of organisations which includes retail company “Tesco PLC” and a financial institution named

Tesco Bank. Tesco PLC is a British multinational groceries and general merchandise retailer. This

company has its headquarters in England, United Kingdom and this company was formed in 1919.

The key products and services of this company include groceries, home appliances, general

merchandising and many more. The products and services of Tesco Bank includes saving and credit

of money along with products such as credit and debit cards (Ataman, Kulick and Sim, 2011).

There are two markets in which Tesco PLC operates; the first market is the retail industry in which

Tesco PLC operates. The countries to which operations of Tesco PLC are limited include United

Kingdom, United States of America, India, Spain, France, China and many more. The second market

in which Tesco operates is retail banking market. In this market, Tesco Bank operates and its

functions are limited to the region of United Kingdom only.

Instead of being operating in multiple countries, most of the operations of Tesco PLC are limited to

United Kingdom only and due to political stability of this region, there are various issues and

challenges which are being faced by Tesco(Arganda-Carreras and et. al., 2017). Tesco is a large scale

company which is impacted by every action of government. Due to BREXIT implementation,

improvement and growth ratio of Tesco has already been reduced till 2019. 2020 was the healing

year of TESCO, but due to current pandemic caused because of COVID 19, the declining of growth

continues in 2020 as well. This company is facing issues of increasing debts and reducing return on

capital employed. The revenues and profits of Tesco PLC are continuously increasing but these

profits are not compatible with the increasing number of stores of this company. The increment

trend of profits is positive but the pace of increment is decreasing.

1.2. Audit of key data sources

Financial data sources are the sourced which assist in gaining data regarding monetary

information of the company. On the other hand, non financial data sources are the sources which

helps in gaining managerial information. Tesco is a large scale company which uses annual report

and interim reports as key their key financial data sources. In addition, Tesco uses cost sheets and

inventory management report as their non financial data sources.

Table 1.1. Key financial and non-financial types of data in the case study

No Data source Data type Financial or non-financial Business units or departments

using this data

1 Annual

report

Income statement Financial Selling and Distribution

department, HR, Marketing

2 Annual

report

Balance sheet Financial Research and Development

department

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3 Annual

report

Cash flows Financial Production department.

4 Annual

report

Statement of

changes in equity

Financial Public relations department

5 Annual

report

Statement of

comprehensive

income and loss

Financial Finance department

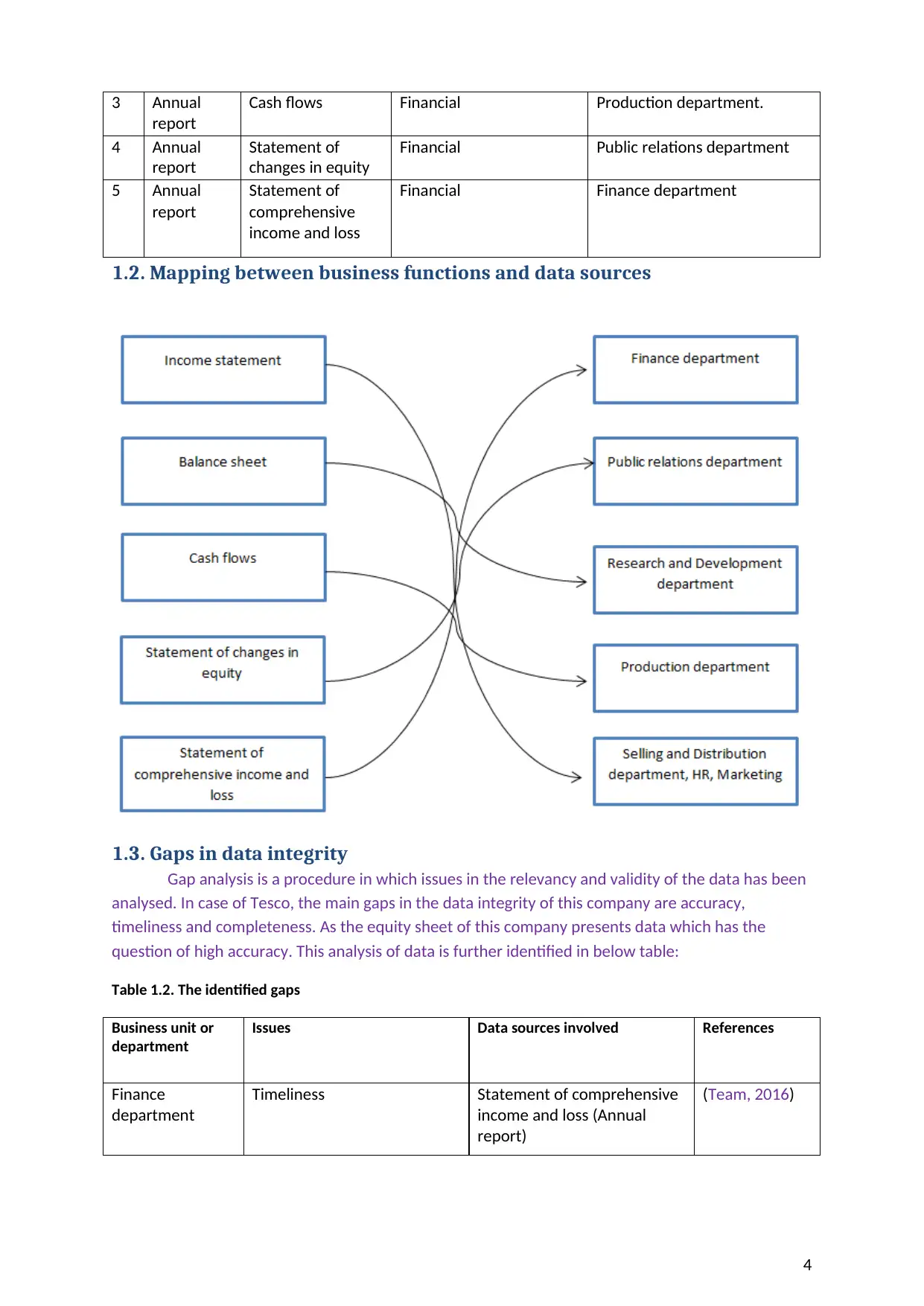

1.2. Mapping between business functions and data sources

1.3. Gaps in data integrity

Gap analysis is a procedure in which issues in the relevancy and validity of the data has been

analysed. In case of Tesco, the main gaps in the data integrity of this company are accuracy,

timeliness and completeness. As the equity sheet of this company presents data which has the

question of high accuracy. This analysis of data is further identified in below table:

Table 1.2. The identified gaps

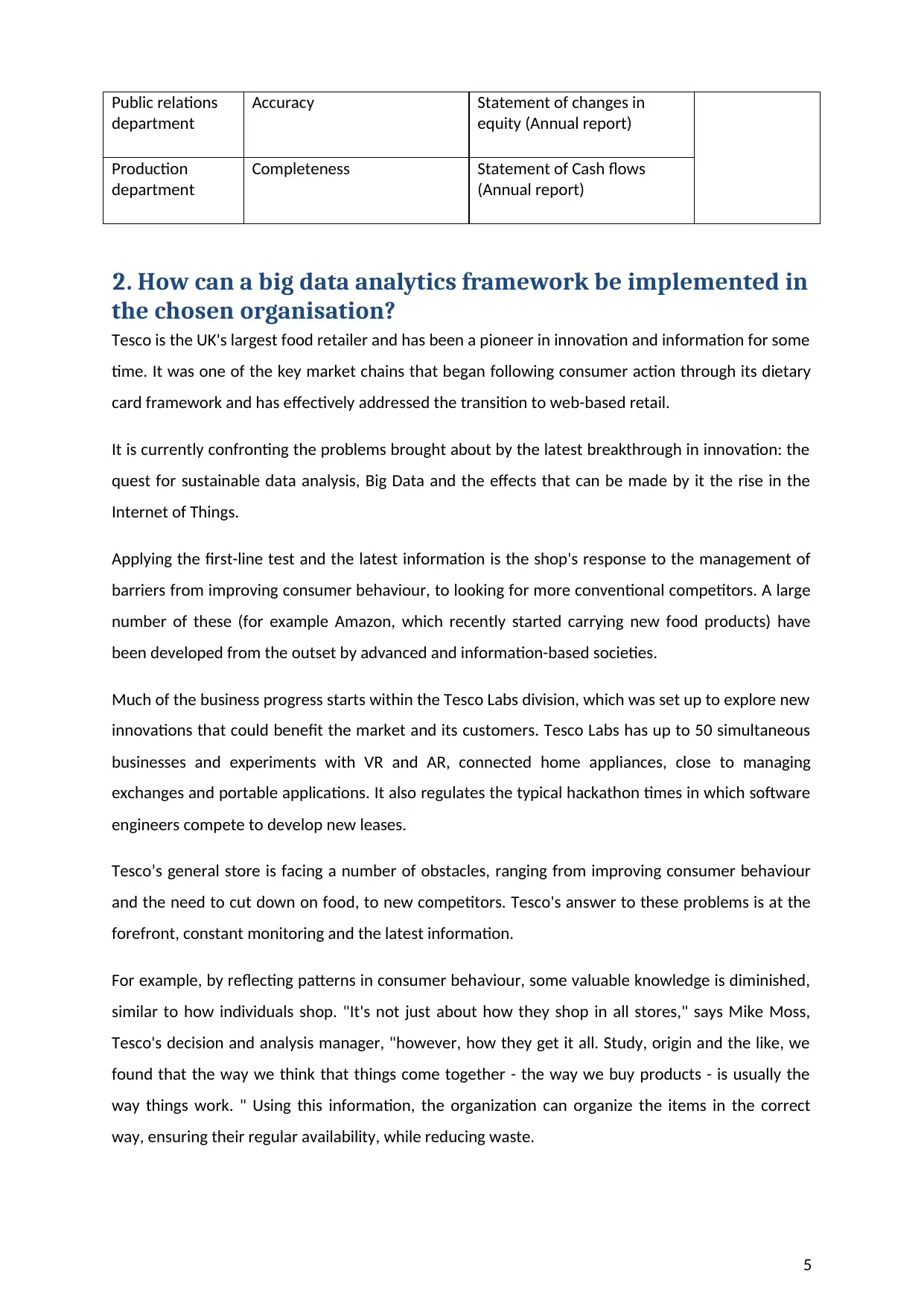

Business unit or

department

Issues Data sources involved References

Finance

department

Timeliness Statement of comprehensive

income and loss (Annual

report)

(Team, 2016)

4

report

Cash flows Financial Production department.

4 Annual

report

Statement of

changes in equity

Financial Public relations department

5 Annual

report

Statement of

comprehensive

income and loss

Financial Finance department

1.2. Mapping between business functions and data sources

1.3. Gaps in data integrity

Gap analysis is a procedure in which issues in the relevancy and validity of the data has been

analysed. In case of Tesco, the main gaps in the data integrity of this company are accuracy,

timeliness and completeness. As the equity sheet of this company presents data which has the

question of high accuracy. This analysis of data is further identified in below table:

Table 1.2. The identified gaps

Business unit or

department

Issues Data sources involved References

Finance

department

Timeliness Statement of comprehensive

income and loss (Annual

report)

(Team, 2016)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Public relations

department

Accuracy Statement of changes in

equity (Annual report)

Production

department

Completeness Statement of Cash flows

(Annual report)

2. How can a big data analytics framework be implemented in

the chosen organisation?

Tesco is the UK's largest food retailer and has been a pioneer in innovation and information for some

time. It was one of the key market chains that began following consumer action through its dietary

card framework and has effectively addressed the transition to web-based retail.

It is currently confronting the problems brought about by the latest breakthrough in innovation: the

quest for sustainable data analysis, Big Data and the effects that can be made by it the rise in the

Internet of Things.

Applying the first-line test and the latest information is the shop's response to the management of

barriers from improving consumer behaviour, to looking for more conventional competitors. A large

number of these (for example Amazon, which recently started carrying new food products) have

been developed from the outset by advanced and information-based societies.

Much of the business progress starts within the Tesco Labs division, which was set up to explore new

innovations that could benefit the market and its customers. Tesco Labs has up to 50 simultaneous

businesses and experiments with VR and AR, connected home appliances, close to managing

exchanges and portable applications. It also regulates the typical hackathon times in which software

engineers compete to develop new leases.

Tesco’s general store is facing a number of obstacles, ranging from improving consumer behaviour

and the need to cut down on food, to new competitors. Tesco's answer to these problems is at the

forefront, constant monitoring and the latest information.

For example, by reflecting patterns in consumer behaviour, some valuable knowledge is diminished,

similar to how individuals shop. "It's not just about how they shop in all stores," says Mike Moss,

Tesco's decision and analysis manager, "however, how they get it all. Study, origin and the like, we

found that the way we think that things come together - the way we buy products - is usually the

way things work. " Using this information, the organization can organize the items in the correct

way, ensuring their regular availability, while reducing waste.

5

department

Accuracy Statement of changes in

equity (Annual report)

Production

department

Completeness Statement of Cash flows

(Annual report)

2. How can a big data analytics framework be implemented in

the chosen organisation?

Tesco is the UK's largest food retailer and has been a pioneer in innovation and information for some

time. It was one of the key market chains that began following consumer action through its dietary

card framework and has effectively addressed the transition to web-based retail.

It is currently confronting the problems brought about by the latest breakthrough in innovation: the

quest for sustainable data analysis, Big Data and the effects that can be made by it the rise in the

Internet of Things.

Applying the first-line test and the latest information is the shop's response to the management of

barriers from improving consumer behaviour, to looking for more conventional competitors. A large

number of these (for example Amazon, which recently started carrying new food products) have

been developed from the outset by advanced and information-based societies.

Much of the business progress starts within the Tesco Labs division, which was set up to explore new

innovations that could benefit the market and its customers. Tesco Labs has up to 50 simultaneous

businesses and experiments with VR and AR, connected home appliances, close to managing

exchanges and portable applications. It also regulates the typical hackathon times in which software

engineers compete to develop new leases.

Tesco’s general store is facing a number of obstacles, ranging from improving consumer behaviour

and the need to cut down on food, to new competitors. Tesco's answer to these problems is at the

forefront, constant monitoring and the latest information.

For example, by reflecting patterns in consumer behaviour, some valuable knowledge is diminished,

similar to how individuals shop. "It's not just about how they shop in all stores," says Mike Moss,

Tesco's decision and analysis manager, "however, how they get it all. Study, origin and the like, we

found that the way we think that things come together - the way we buy products - is usually the

way things work. " Using this information, the organization can organize the items in the correct

way, ensuring their regular availability, while reducing waste.

5

Sensory information is also gradually used, for example, to monitor the temperature of coolers and

coolers through the source system. Each device is monitored midway and accurate calculations are

used to decide when a particular unit needs to be changed.

With 3,500 stores in the UK alone and each store that loads an average of 40,000 items, they are all

followed consistently once they contain over 100 million pieces of information. This is the place

where auditing within the database could be the most important feature: testing the innovation

where information is sent, rather than moving it in lumps for outdoor study. Tesco is moving from

information warehousing to an information lake model, based around the Hadoop structure. This

will be a concentrated, cloud-based vault for every one of its information, arranged in an approach

to make it available and usable by any arm of the organization, as and when it's required.

The business is likewise quickly getting increasingly engaged with open source advancement, and

Tesco's designers, specialists and information researchers are presently urged to utilize open source

innovation at every possible opportunity, and to offer back to OS people group.

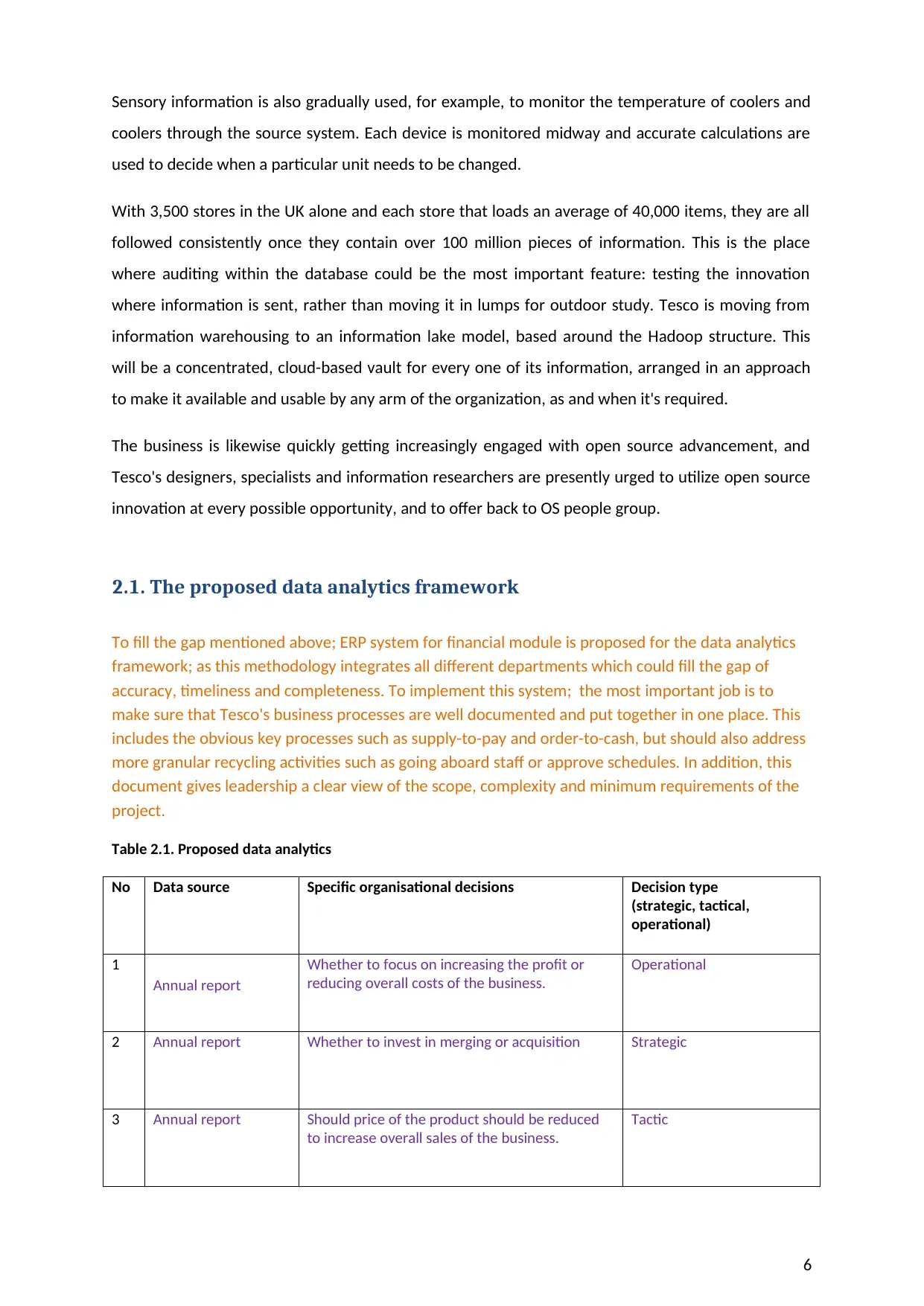

2.1. The proposed data analytics framework

To fill the gap mentioned above; ERP system for financial module is proposed for the data analytics

framework; as this methodology integrates all different departments which could fill the gap of

accuracy, timeliness and completeness. To implement this system; the most important job is to

make sure that Tesco's business processes are well documented and put together in one place. This

includes the obvious key processes such as supply-to-pay and order-to-cash, but should also address

more granular recycling activities such as going aboard staff or approve schedules. In addition, this

document gives leadership a clear view of the scope, complexity and minimum requirements of the

project.

Table 2.1. Proposed data analytics

No Data source Specific organisational decisions Decision type

(strategic, tactical,

operational)

1

Annual report

Whether to focus on increasing the profit or

reducing overall costs of the business.

Operational

2 Annual report Whether to invest in merging or acquisition Strategic

3 Annual report Should price of the product should be reduced

to increase overall sales of the business.

Tactic

6

coolers through the source system. Each device is monitored midway and accurate calculations are

used to decide when a particular unit needs to be changed.

With 3,500 stores in the UK alone and each store that loads an average of 40,000 items, they are all

followed consistently once they contain over 100 million pieces of information. This is the place

where auditing within the database could be the most important feature: testing the innovation

where information is sent, rather than moving it in lumps for outdoor study. Tesco is moving from

information warehousing to an information lake model, based around the Hadoop structure. This

will be a concentrated, cloud-based vault for every one of its information, arranged in an approach

to make it available and usable by any arm of the organization, as and when it's required.

The business is likewise quickly getting increasingly engaged with open source advancement, and

Tesco's designers, specialists and information researchers are presently urged to utilize open source

innovation at every possible opportunity, and to offer back to OS people group.

2.1. The proposed data analytics framework

To fill the gap mentioned above; ERP system for financial module is proposed for the data analytics

framework; as this methodology integrates all different departments which could fill the gap of

accuracy, timeliness and completeness. To implement this system; the most important job is to

make sure that Tesco's business processes are well documented and put together in one place. This

includes the obvious key processes such as supply-to-pay and order-to-cash, but should also address

more granular recycling activities such as going aboard staff or approve schedules. In addition, this

document gives leadership a clear view of the scope, complexity and minimum requirements of the

project.

Table 2.1. Proposed data analytics

No Data source Specific organisational decisions Decision type

(strategic, tactical,

operational)

1

Annual report

Whether to focus on increasing the profit or

reducing overall costs of the business.

Operational

2 Annual report Whether to invest in merging or acquisition Strategic

3 Annual report Should price of the product should be reduced

to increase overall sales of the business.

Tactic

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Etc.

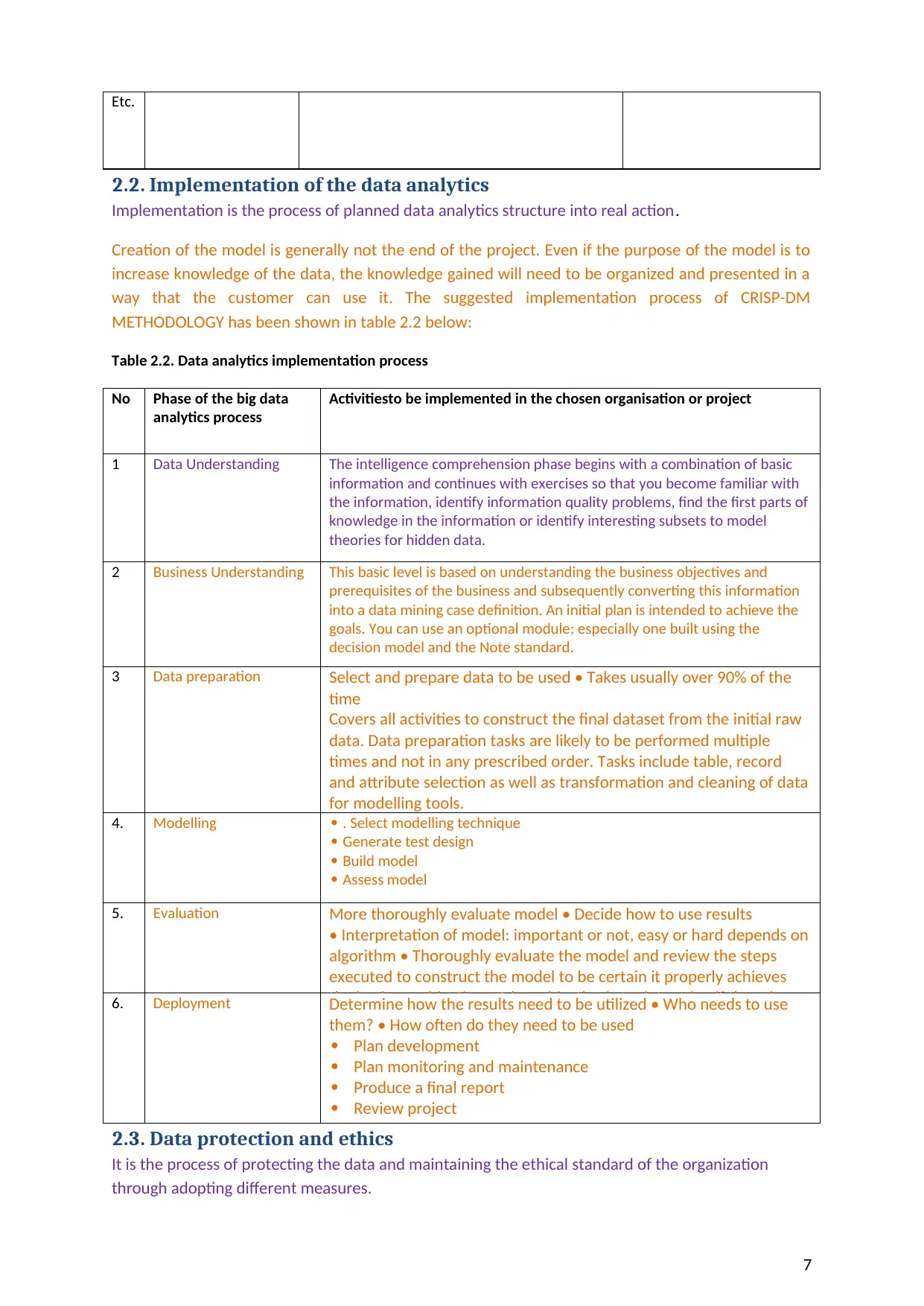

2.2. Implementation of the data analytics

Implementation is the process of planned data analytics structure into real action.

Creation of the model is generally not the end of the project. Even if the purpose of the model is to

increase knowledge of the data, the knowledge gained will need to be organized and presented in a

way that the customer can use it. The suggested implementation process of CRISP-DM

METHODOLOGY has been shown in table 2.2 below:

Table 2.2. Data analytics implementation process

No Phase of the big data

analytics process

Activitiesto be implemented in the chosen organisation or project

1 Data Understanding The intelligence comprehension phase begins with a combination of basic

information and continues with exercises so that you become familiar with

the information, identify information quality problems, find the first parts of

knowledge in the information or identify interesting subsets to model

theories for hidden data.

2 Business Understanding This basic level is based on understanding the business objectives and

prerequisites of the business and subsequently converting this information

into a data mining case definition. An initial plan is intended to achieve the

goals. You can use an optional module; especially one built using the

decision model and the Note standard.

3 Data preparation Select and prepare data to be used • Takes usually over 90% of the

time

Covers all activities to construct the final dataset from the initial raw

data. Data preparation tasks are likely to be performed multiple

times and not in any prescribed order. Tasks include table, record

and attribute selection as well as transformation and cleaning of data

for modelling tools.

4. Modelling . Select modelling technique

Generate test design

Build model

Assess model

5. Evaluation More thoroughly evaluate model • Decide how to use results

• Interpretation of model: important or not, easy or hard depends on

algorithm • Thoroughly evaluate the model and review the steps

executed to construct the model to be certain it properly achieves

the business objectives. A key objective is to determine if there is6. Deployment Determine how the results need to be utilized • Who needs to use

them? • How often do they need to be used

Plan development

Plan monitoring and maintenance

Produce a final report

Review project

2.3. Data protection and ethics

It is the process of protecting the data and maintaining the ethical standard of the organization

through adopting different measures.

7

2.2. Implementation of the data analytics

Implementation is the process of planned data analytics structure into real action.

Creation of the model is generally not the end of the project. Even if the purpose of the model is to

increase knowledge of the data, the knowledge gained will need to be organized and presented in a

way that the customer can use it. The suggested implementation process of CRISP-DM

METHODOLOGY has been shown in table 2.2 below:

Table 2.2. Data analytics implementation process

No Phase of the big data

analytics process

Activitiesto be implemented in the chosen organisation or project

1 Data Understanding The intelligence comprehension phase begins with a combination of basic

information and continues with exercises so that you become familiar with

the information, identify information quality problems, find the first parts of

knowledge in the information or identify interesting subsets to model

theories for hidden data.

2 Business Understanding This basic level is based on understanding the business objectives and

prerequisites of the business and subsequently converting this information

into a data mining case definition. An initial plan is intended to achieve the

goals. You can use an optional module; especially one built using the

decision model and the Note standard.

3 Data preparation Select and prepare data to be used • Takes usually over 90% of the

time

Covers all activities to construct the final dataset from the initial raw

data. Data preparation tasks are likely to be performed multiple

times and not in any prescribed order. Tasks include table, record

and attribute selection as well as transformation and cleaning of data

for modelling tools.

4. Modelling . Select modelling technique

Generate test design

Build model

Assess model

5. Evaluation More thoroughly evaluate model • Decide how to use results

• Interpretation of model: important or not, easy or hard depends on

algorithm • Thoroughly evaluate the model and review the steps

executed to construct the model to be certain it properly achieves

the business objectives. A key objective is to determine if there is6. Deployment Determine how the results need to be utilized • Who needs to use

them? • How often do they need to be used

Plan development

Plan monitoring and maintenance

Produce a final report

Review project

2.3. Data protection and ethics

It is the process of protecting the data and maintaining the ethical standard of the organization

through adopting different measures.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Depending on the type of information you collect, you should govern different laws. Although the

promulgation of intellectual property applies to all information, adherence to individual information

has its own laws. Basically, as of May 25, 2018, the General Data Protection Regulation (GDPR;

European Union, 2016a) applies to any EU analyst or expert in the European Economic Area (EEA)

who collects half individual information about a resident of any country, anywhere on the planet. ,

just like any scientist as a whole who collects individual information about EU residents.

Table 2.3.Data protection and ethical compliance

Data protection/ethics

requirement

Procedures to be implemented

in the chosen organisation or

project

Relevant data

protection

standard

References

1 Lawful, fair and

transparent processing

Process the personal data in

lawful manner. First to collect

genuine data and access this

data to particular user only.

IDDPS (GDPR)

2 Data subject rights Make a proper arrangement

where lodging complain with the

company must be easier for the

users or customers.

DPPs (GDPR)

3 Avoid personal data

breaches

Through adopting a high tech

systems and topology which can

protect data of each and every

employee profusely.

hexa-dimension

metric

operationalization

framework

(GDPR)

Etc.

3. Statement of a specific decision the organisation currently

needs to make, and how big data are expected to improve its

quality

Tesco is in its phase where the operations of this company are impacted due to strategic decisions

and policies of the government of the nations in which it operates. Government decisions and

policies are an external factor which cannot be controlled and in order to protect the operations, an

organisation must develop strategic and tactical plans. The major decisions which Tesco needs to

undertake includes open new stores in existing operating locations in order to fulfil their intention of

gaining higher profits and revenues. For this decision, the financial data of Tesco will be required

including variables of total number of stores, sales and profit (Bandaru, Ng and Deb, 2017).

Second decision is a strategic one which states that Tesco should increase their dividend per share so

that their return on capital employed can be improved as it will help in gaining the effective equity

position of this company. This decision will need financial data variables of dividend per share and

ratio of return on capital employed.

Third decision is to increase the number of employed in Tesco as it can help in increasing the sales

revenue of this company. For this sales value and number of employees will be required as the

financial data (Bondarenko, Bondarenko and Gonchar, 2020).

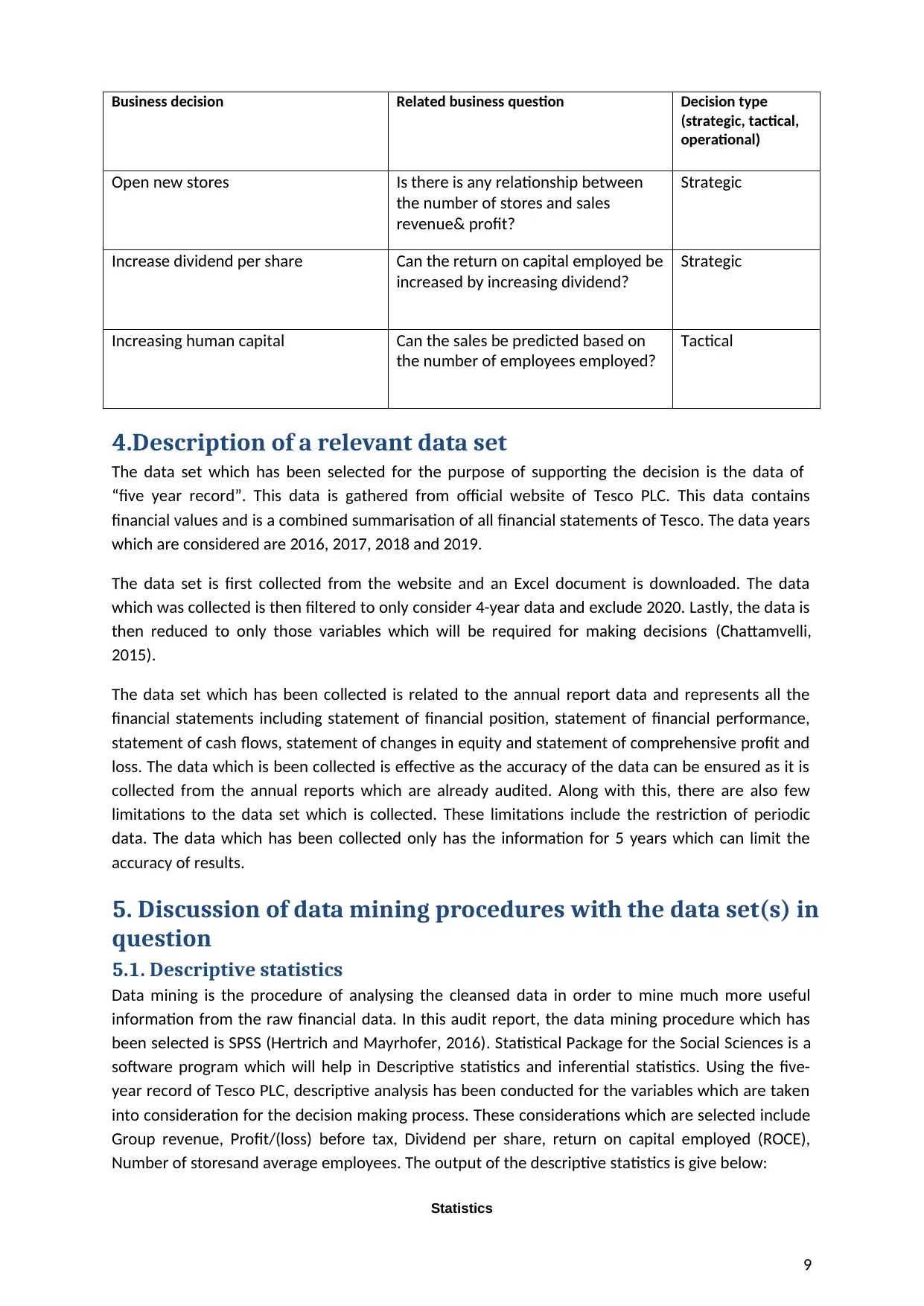

Table 3.1. Business decision

8

promulgation of intellectual property applies to all information, adherence to individual information

has its own laws. Basically, as of May 25, 2018, the General Data Protection Regulation (GDPR;

European Union, 2016a) applies to any EU analyst or expert in the European Economic Area (EEA)

who collects half individual information about a resident of any country, anywhere on the planet. ,

just like any scientist as a whole who collects individual information about EU residents.

Table 2.3.Data protection and ethical compliance

Data protection/ethics

requirement

Procedures to be implemented

in the chosen organisation or

project

Relevant data

protection

standard

References

1 Lawful, fair and

transparent processing

Process the personal data in

lawful manner. First to collect

genuine data and access this

data to particular user only.

IDDPS (GDPR)

2 Data subject rights Make a proper arrangement

where lodging complain with the

company must be easier for the

users or customers.

DPPs (GDPR)

3 Avoid personal data

breaches

Through adopting a high tech

systems and topology which can

protect data of each and every

employee profusely.

hexa-dimension

metric

operationalization

framework

(GDPR)

Etc.

3. Statement of a specific decision the organisation currently

needs to make, and how big data are expected to improve its

quality

Tesco is in its phase where the operations of this company are impacted due to strategic decisions

and policies of the government of the nations in which it operates. Government decisions and

policies are an external factor which cannot be controlled and in order to protect the operations, an

organisation must develop strategic and tactical plans. The major decisions which Tesco needs to

undertake includes open new stores in existing operating locations in order to fulfil their intention of

gaining higher profits and revenues. For this decision, the financial data of Tesco will be required

including variables of total number of stores, sales and profit (Bandaru, Ng and Deb, 2017).

Second decision is a strategic one which states that Tesco should increase their dividend per share so

that their return on capital employed can be improved as it will help in gaining the effective equity

position of this company. This decision will need financial data variables of dividend per share and

ratio of return on capital employed.

Third decision is to increase the number of employed in Tesco as it can help in increasing the sales

revenue of this company. For this sales value and number of employees will be required as the

financial data (Bondarenko, Bondarenko and Gonchar, 2020).

Table 3.1. Business decision

8

Business decision Related business question Decision type

(strategic, tactical,

operational)

Open new stores Is there is any relationship between

the number of stores and sales

revenue& profit?

Strategic

Increase dividend per share Can the return on capital employed be

increased by increasing dividend?

Strategic

Increasing human capital Can the sales be predicted based on

the number of employees employed?

Tactical

4.Description of a relevant data set

The data set which has been selected for the purpose of supporting the decision is the data of

“five year record”. This data is gathered from official website of Tesco PLC. This data contains

financial values and is a combined summarisation of all financial statements of Tesco. The data years

which are considered are 2016, 2017, 2018 and 2019.

The data set is first collected from the website and an Excel document is downloaded. The data

which was collected is then filtered to only consider 4-year data and exclude 2020. Lastly, the data is

then reduced to only those variables which will be required for making decisions (Chattamvelli,

2015).

The data set which has been collected is related to the annual report data and represents all the

financial statements including statement of financial position, statement of financial performance,

statement of cash flows, statement of changes in equity and statement of comprehensive profit and

loss. The data which is been collected is effective as the accuracy of the data can be ensured as it is

collected from the annual reports which are already audited. Along with this, there are also few

limitations to the data set which is collected. These limitations include the restriction of periodic

data. The data which has been collected only has the information for 5 years which can limit the

accuracy of results.

5. Discussion of data mining procedures with the data set(s) in

question

5.1. Descriptive statistics

Data mining is the procedure of analysing the cleansed data in order to mine much more useful

information from the raw financial data. In this audit report, the data mining procedure which has

been selected is SPSS (Hertrich and Mayrhofer, 2016). Statistical Package for the Social Sciences is a

software program which will help in Descriptive statistics and inferential statistics. Using the five-

year record of Tesco PLC, descriptive analysis has been conducted for the variables which are taken

into consideration for the decision making process. These considerations which are selected include

Group revenue, Profit/(loss) before tax, Dividend per share, return on capital employed (ROCE),

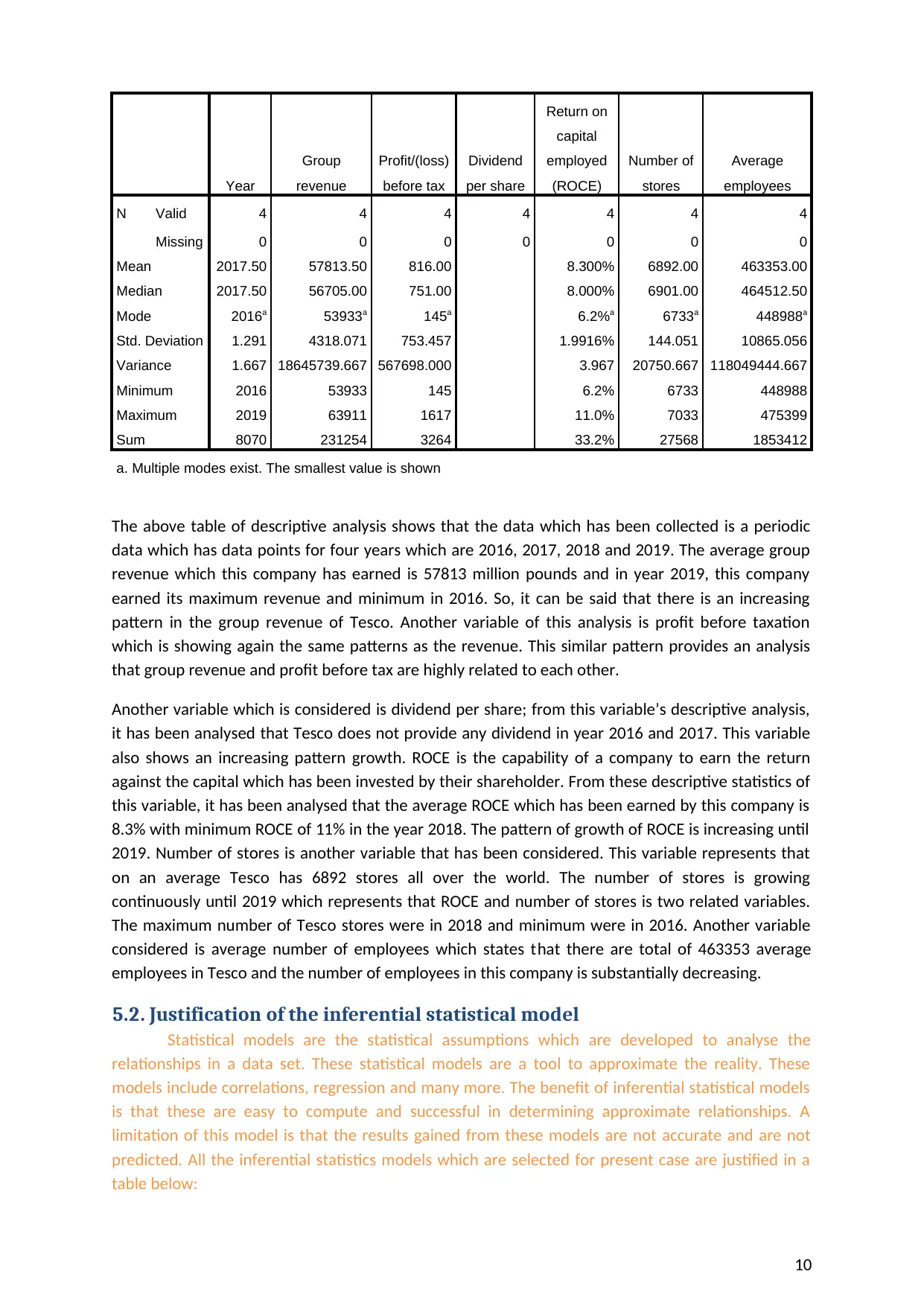

Number of storesand average employees. The output of the descriptive statistics is give below:

Statistics

9

(strategic, tactical,

operational)

Open new stores Is there is any relationship between

the number of stores and sales

revenue& profit?

Strategic

Increase dividend per share Can the return on capital employed be

increased by increasing dividend?

Strategic

Increasing human capital Can the sales be predicted based on

the number of employees employed?

Tactical

4.Description of a relevant data set

The data set which has been selected for the purpose of supporting the decision is the data of

“five year record”. This data is gathered from official website of Tesco PLC. This data contains

financial values and is a combined summarisation of all financial statements of Tesco. The data years

which are considered are 2016, 2017, 2018 and 2019.

The data set is first collected from the website and an Excel document is downloaded. The data

which was collected is then filtered to only consider 4-year data and exclude 2020. Lastly, the data is

then reduced to only those variables which will be required for making decisions (Chattamvelli,

2015).

The data set which has been collected is related to the annual report data and represents all the

financial statements including statement of financial position, statement of financial performance,

statement of cash flows, statement of changes in equity and statement of comprehensive profit and

loss. The data which is been collected is effective as the accuracy of the data can be ensured as it is

collected from the annual reports which are already audited. Along with this, there are also few

limitations to the data set which is collected. These limitations include the restriction of periodic

data. The data which has been collected only has the information for 5 years which can limit the

accuracy of results.

5. Discussion of data mining procedures with the data set(s) in

question

5.1. Descriptive statistics

Data mining is the procedure of analysing the cleansed data in order to mine much more useful

information from the raw financial data. In this audit report, the data mining procedure which has

been selected is SPSS (Hertrich and Mayrhofer, 2016). Statistical Package for the Social Sciences is a

software program which will help in Descriptive statistics and inferential statistics. Using the five-

year record of Tesco PLC, descriptive analysis has been conducted for the variables which are taken

into consideration for the decision making process. These considerations which are selected include

Group revenue, Profit/(loss) before tax, Dividend per share, return on capital employed (ROCE),

Number of storesand average employees. The output of the descriptive statistics is give below:

Statistics

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year

Group

revenue

Profit/(loss)

before tax

Dividend

per share

Return on

capital

employed

(ROCE)

Number of

stores

Average

employees

N Valid 4 4 4 4 4 4 4

Missing 0 0 0 0 0 0 0

Mean 2017.50 57813.50 816.00 8.300% 6892.00 463353.00

Median 2017.50 56705.00 751.00 8.000% 6901.00 464512.50

Mode 2016a 53933a 145a 6.2%a 6733a 448988a

Std. Deviation 1.291 4318.071 753.457 1.9916% 144.051 10865.056

Variance 1.667 18645739.667 567698.000 3.967 20750.667 118049444.667

Minimum 2016 53933 145 6.2% 6733 448988

Maximum 2019 63911 1617 11.0% 7033 475399

Sum 8070 231254 3264 33.2% 27568 1853412

a. Multiple modes exist. The smallest value is shown

The above table of descriptive analysis shows that the data which has been collected is a periodic

data which has data points for four years which are 2016, 2017, 2018 and 2019. The average group

revenue which this company has earned is 57813 million pounds and in year 2019, this company

earned its maximum revenue and minimum in 2016. So, it can be said that there is an increasing

pattern in the group revenue of Tesco. Another variable of this analysis is profit before taxation

which is showing again the same patterns as the revenue. This similar pattern provides an analysis

that group revenue and profit before tax are highly related to each other.

Another variable which is considered is dividend per share; from this variable’s descriptive analysis,

it has been analysed that Tesco does not provide any dividend in year 2016 and 2017. This variable

also shows an increasing pattern growth. ROCE is the capability of a company to earn the return

against the capital which has been invested by their shareholder. From these descriptive statistics of

this variable, it has been analysed that the average ROCE which has been earned by this company is

8.3% with minimum ROCE of 11% in the year 2018. The pattern of growth of ROCE is increasing until

2019. Number of stores is another variable that has been considered. This variable represents that

on an average Tesco has 6892 stores all over the world. The number of stores is growing

continuously until 2019 which represents that ROCE and number of stores is two related variables.

The maximum number of Tesco stores were in 2018 and minimum were in 2016. Another variable

considered is average number of employees which states that there are total of 463353 average

employees in Tesco and the number of employees in this company is substantially decreasing.

5.2. Justification of the inferential statistical model

Statistical models are the statistical assumptions which are developed to analyse the

relationships in a data set. These statistical models are a tool to approximate the reality. These

models include correlations, regression and many more. The benefit of inferential statistical models

is that these are easy to compute and successful in determining approximate relationships. A

limitation of this model is that the results gained from these models are not accurate and are not

predicted. All the inferential statistics models which are selected for present case are justified in a

table below:

10

Group

revenue

Profit/(loss)

before tax

Dividend

per share

Return on

capital

employed

(ROCE)

Number of

stores

Average

employees

N Valid 4 4 4 4 4 4 4

Missing 0 0 0 0 0 0 0

Mean 2017.50 57813.50 816.00 8.300% 6892.00 463353.00

Median 2017.50 56705.00 751.00 8.000% 6901.00 464512.50

Mode 2016a 53933a 145a 6.2%a 6733a 448988a

Std. Deviation 1.291 4318.071 753.457 1.9916% 144.051 10865.056

Variance 1.667 18645739.667 567698.000 3.967 20750.667 118049444.667

Minimum 2016 53933 145 6.2% 6733 448988

Maximum 2019 63911 1617 11.0% 7033 475399

Sum 8070 231254 3264 33.2% 27568 1853412

a. Multiple modes exist. The smallest value is shown

The above table of descriptive analysis shows that the data which has been collected is a periodic

data which has data points for four years which are 2016, 2017, 2018 and 2019. The average group

revenue which this company has earned is 57813 million pounds and in year 2019, this company

earned its maximum revenue and minimum in 2016. So, it can be said that there is an increasing

pattern in the group revenue of Tesco. Another variable of this analysis is profit before taxation

which is showing again the same patterns as the revenue. This similar pattern provides an analysis

that group revenue and profit before tax are highly related to each other.

Another variable which is considered is dividend per share; from this variable’s descriptive analysis,

it has been analysed that Tesco does not provide any dividend in year 2016 and 2017. This variable

also shows an increasing pattern growth. ROCE is the capability of a company to earn the return

against the capital which has been invested by their shareholder. From these descriptive statistics of

this variable, it has been analysed that the average ROCE which has been earned by this company is

8.3% with minimum ROCE of 11% in the year 2018. The pattern of growth of ROCE is increasing until

2019. Number of stores is another variable that has been considered. This variable represents that

on an average Tesco has 6892 stores all over the world. The number of stores is growing

continuously until 2019 which represents that ROCE and number of stores is two related variables.

The maximum number of Tesco stores were in 2018 and minimum were in 2016. Another variable

considered is average number of employees which states that there are total of 463353 average

employees in Tesco and the number of employees in this company is substantially decreasing.

5.2. Justification of the inferential statistical model

Statistical models are the statistical assumptions which are developed to analyse the

relationships in a data set. These statistical models are a tool to approximate the reality. These

models include correlations, regression and many more. The benefit of inferential statistical models

is that these are easy to compute and successful in determining approximate relationships. A

limitation of this model is that the results gained from these models are not accurate and are not

predicted. All the inferential statistics models which are selected for present case are justified in a

table below:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

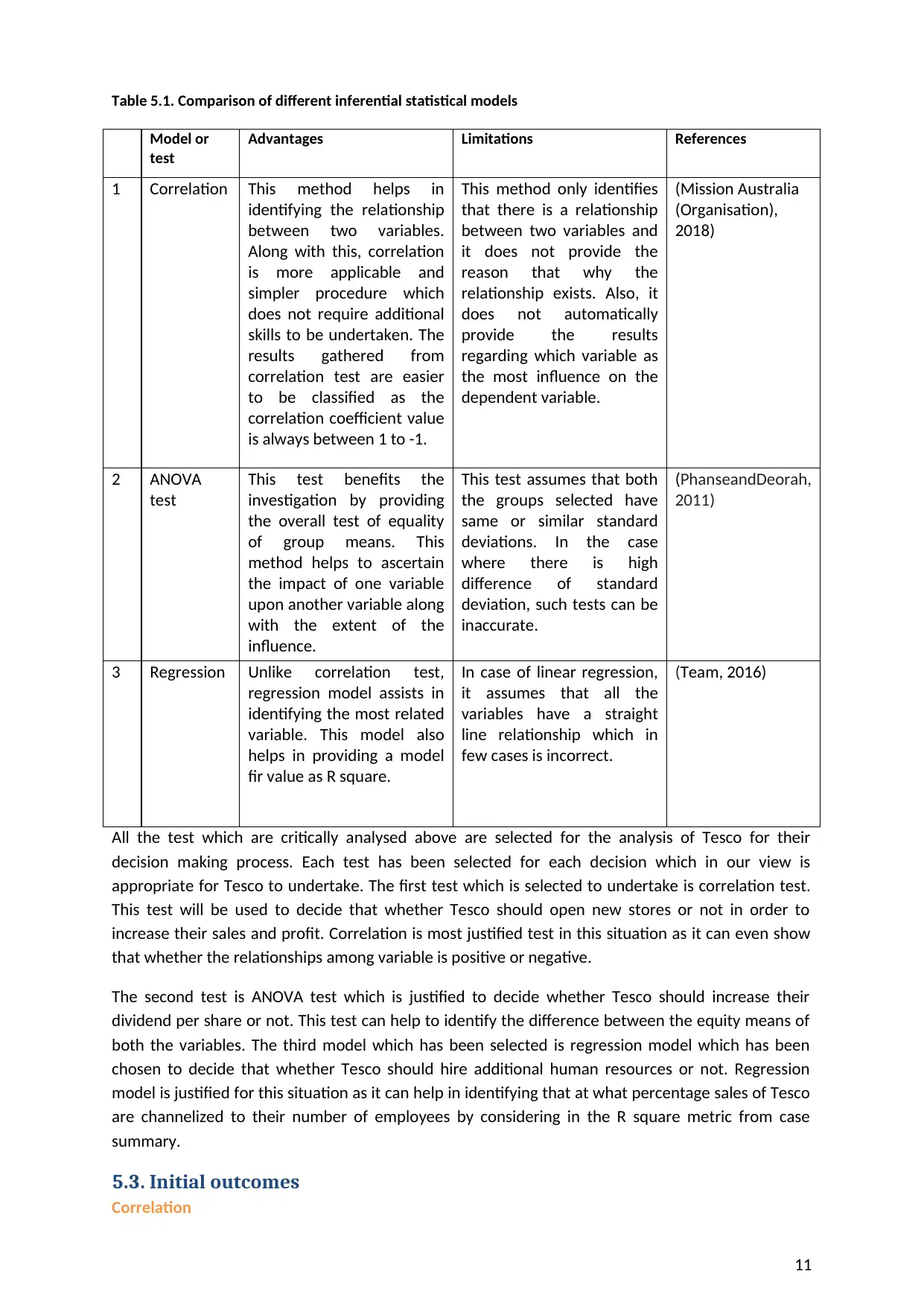

Table 5.1. Comparison of different inferential statistical models

Model or

test

Advantages Limitations References

1 Correlation This method helps in

identifying the relationship

between two variables.

Along with this, correlation

is more applicable and

simpler procedure which

does not require additional

skills to be undertaken. The

results gathered from

correlation test are easier

to be classified as the

correlation coefficient value

is always between 1 to -1.

This method only identifies

that there is a relationship

between two variables and

it does not provide the

reason that why the

relationship exists. Also, it

does not automatically

provide the results

regarding which variable as

the most influence on the

dependent variable.

(Mission Australia

(Organisation),

2018)

2 ANOVA

test

This test benefits the

investigation by providing

the overall test of equality

of group means. This

method helps to ascertain

the impact of one variable

upon another variable along

with the extent of the

influence.

This test assumes that both

the groups selected have

same or similar standard

deviations. In the case

where there is high

difference of standard

deviation, such tests can be

inaccurate.

(PhanseandDeorah,

2011)

3 Regression Unlike correlation test,

regression model assists in

identifying the most related

variable. This model also

helps in providing a model

fir value as R square.

In case of linear regression,

it assumes that all the

variables have a straight

line relationship which in

few cases is incorrect.

(Team, 2016)

All the test which are critically analysed above are selected for the analysis of Tesco for their

decision making process. Each test has been selected for each decision which in our view is

appropriate for Tesco to undertake. The first test which is selected to undertake is correlation test.

This test will be used to decide that whether Tesco should open new stores or not in order to

increase their sales and profit. Correlation is most justified test in this situation as it can even show

that whether the relationships among variable is positive or negative.

The second test is ANOVA test which is justified to decide whether Tesco should increase their

dividend per share or not. This test can help to identify the difference between the equity means of

both the variables. The third model which has been selected is regression model which has been

chosen to decide that whether Tesco should hire additional human resources or not. Regression

model is justified for this situation as it can help in identifying that at what percentage sales of Tesco

are channelized to their number of employees by considering in the R square metric from case

summary.

5.3. Initial outcomes

Correlation

11

Model or

test

Advantages Limitations References

1 Correlation This method helps in

identifying the relationship

between two variables.

Along with this, correlation

is more applicable and

simpler procedure which

does not require additional

skills to be undertaken. The

results gathered from

correlation test are easier

to be classified as the

correlation coefficient value

is always between 1 to -1.

This method only identifies

that there is a relationship

between two variables and

it does not provide the

reason that why the

relationship exists. Also, it

does not automatically

provide the results

regarding which variable as

the most influence on the

dependent variable.

(Mission Australia

(Organisation),

2018)

2 ANOVA

test

This test benefits the

investigation by providing

the overall test of equality

of group means. This

method helps to ascertain

the impact of one variable

upon another variable along

with the extent of the

influence.

This test assumes that both

the groups selected have

same or similar standard

deviations. In the case

where there is high

difference of standard

deviation, such tests can be

inaccurate.

(PhanseandDeorah,

2011)

3 Regression Unlike correlation test,

regression model assists in

identifying the most related

variable. This model also

helps in providing a model

fir value as R square.

In case of linear regression,

it assumes that all the

variables have a straight

line relationship which in

few cases is incorrect.

(Team, 2016)

All the test which are critically analysed above are selected for the analysis of Tesco for their

decision making process. Each test has been selected for each decision which in our view is

appropriate for Tesco to undertake. The first test which is selected to undertake is correlation test.

This test will be used to decide that whether Tesco should open new stores or not in order to

increase their sales and profit. Correlation is most justified test in this situation as it can even show

that whether the relationships among variable is positive or negative.

The second test is ANOVA test which is justified to decide whether Tesco should increase their

dividend per share or not. This test can help to identify the difference between the equity means of

both the variables. The third model which has been selected is regression model which has been

chosen to decide that whether Tesco should hire additional human resources or not. Regression

model is justified for this situation as it can help in identifying that at what percentage sales of Tesco

are channelized to their number of employees by considering in the R square metric from case

summary.

5.3. Initial outcomes

Correlation

11

Correlations

Group revenue

Profit/(loss)

before tax

Number of

stores

Group revenue Pearson Correlation 1 .859 .721

Sig. (2-tailed) .141 .279

N 4 4 4

Profit/(loss) before tax Pearson Correlation .859 1 .929

Sig. (2-tailed) .141 .071

N 4 4 4

Pearson Correlation .721 .929 1

Sig. (2-tailed) .279 .071

N 4 4 4

ANOVA test

Case Processing Summary

Cases

Included Excluded Total

N Percent N Percent N Percent

Return on capital employed

(ROCE) * Dividend per

share

4 100.0% 0 0.0% 4 100.0%

Report

Return on capital employed (ROCE)

Dividend per share Mean N Std. Deviation

0 7.150% 2 1.3435%

3.00 11.000% 1 .

5.77 7.900% 1 .

Total 8.300% 4 1.9916%

Regression

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .265a .070 -.394 5099.141

a. Predictors: (Constant), Average employees

12

Group revenue

Profit/(loss)

before tax

Number of

stores

Group revenue Pearson Correlation 1 .859 .721

Sig. (2-tailed) .141 .279

N 4 4 4

Profit/(loss) before tax Pearson Correlation .859 1 .929

Sig. (2-tailed) .141 .071

N 4 4 4

Pearson Correlation .721 .929 1

Sig. (2-tailed) .279 .071

N 4 4 4

ANOVA test

Case Processing Summary

Cases

Included Excluded Total

N Percent N Percent N Percent

Return on capital employed

(ROCE) * Dividend per

share

4 100.0% 0 0.0% 4 100.0%

Report

Return on capital employed (ROCE)

Dividend per share Mean N Std. Deviation

0 7.150% 2 1.3435%

3.00 11.000% 1 .

5.77 7.900% 1 .

Total 8.300% 4 1.9916%

Regression

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .265a .070 -.394 5099.141

a. Predictors: (Constant), Average employees

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.