Demand and Supply Assignment (PDF)

VerifiedAdded on 2021/05/19

|21

|1157

|473

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Demand and Supply

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Demand

Demand normally means the desire or

willingness for a good.

Apart from the desire or willingness, consumer

should be able to buy the good. Demand is

therefore an effective desire.

Demand normally means the desire or

willingness for a good.

Apart from the desire or willingness, consumer

should be able to buy the good. Demand is

therefore an effective desire.

There are thus three main characteristics of

demand in economics

1. Willingness and ability to pay.

2. Demand is always at a price.

3. Demand is always per unit of time.

demand in economics

1. Willingness and ability to pay.

2. Demand is always at a price.

3. Demand is always per unit of time.

• Individual’s Demand for a commodity:

The individual’s demand for a commodity is the

amount of a commodity which the consumer is

willing to purchase at any given price over a

specified period of time, certeris paribus.

• The market Demand for a Commodity:

The market demand for a commodity is obtained

by adding up the total quantity demanded at

various prices by all the individuals over a

specified period of time in the market.

certeris paribus (Latin phrase) means all other things being unchanged or constant

The individual’s demand for a commodity is the

amount of a commodity which the consumer is

willing to purchase at any given price over a

specified period of time, certeris paribus.

• The market Demand for a Commodity:

The market demand for a commodity is obtained

by adding up the total quantity demanded at

various prices by all the individuals over a

specified period of time in the market.

certeris paribus (Latin phrase) means all other things being unchanged or constant

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Kinds of Demand:

There are three types of demand:

• Price Demand

• Income Demand

• Cross Demand

There are three types of demand:

• Price Demand

• Income Demand

• Cross Demand

Price Demand

• It refers to various quantities of a good or

service that a consumer would be willing to

purchase at all possible prices in a given

market at a given point of time, ceteris

paribus.

• It refers to various quantities of a good or

service that a consumer would be willing to

purchase at all possible prices in a given

market at a given point of time, ceteris

paribus.

Income Demand

• It refers to various quantities of a good or

services that a consumer would be willing to

purchase at different levels of income, ceteris

paribus.

• It refers to various quantities of a good or

services that a consumer would be willing to

purchase at different levels of income, ceteris

paribus.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cross Demand

• It refers to various quantities of a good or

service that a consumer would be willing to

purchase not due to changes in the price of the

commodity under consideration, but due to

changes in the price of related commodities.

• It refers to various quantities of a good or

service that a consumer would be willing to

purchase not due to changes in the price of the

commodity under consideration, but due to

changes in the price of related commodities.

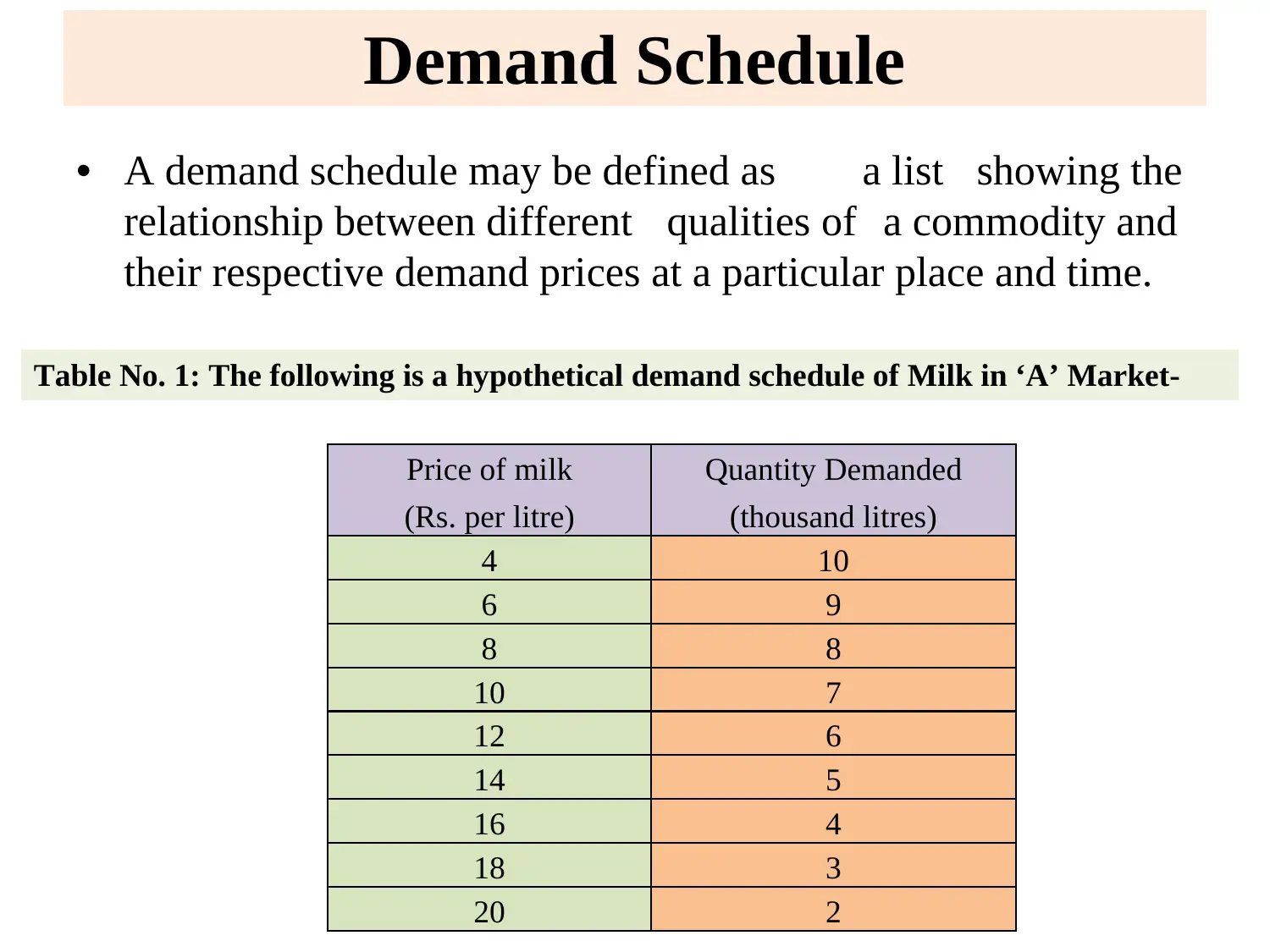

Demand Schedule

• A demand schedule may be defined as a list showing the

relationship between different qualities of a commodity and

their respective demand prices at a particular place and time.

Table No. 1: The following is a hypothetical demand schedule of Milk in ‘A’ Market-

Price of milk

(Rs. per litre)

Quantity Demanded

(thousand litres)

4 10

6 9

8 8

10 7

12 6

14 5

16 4

18 3

20 2

• A demand schedule may be defined as a list showing the

relationship between different qualities of a commodity and

their respective demand prices at a particular place and time.

Table No. 1: The following is a hypothetical demand schedule of Milk in ‘A’ Market-

Price of milk

(Rs. per litre)

Quantity Demanded

(thousand litres)

4 10

6 9

8 8

10 7

12 6

14 5

16 4

18 3

20 2

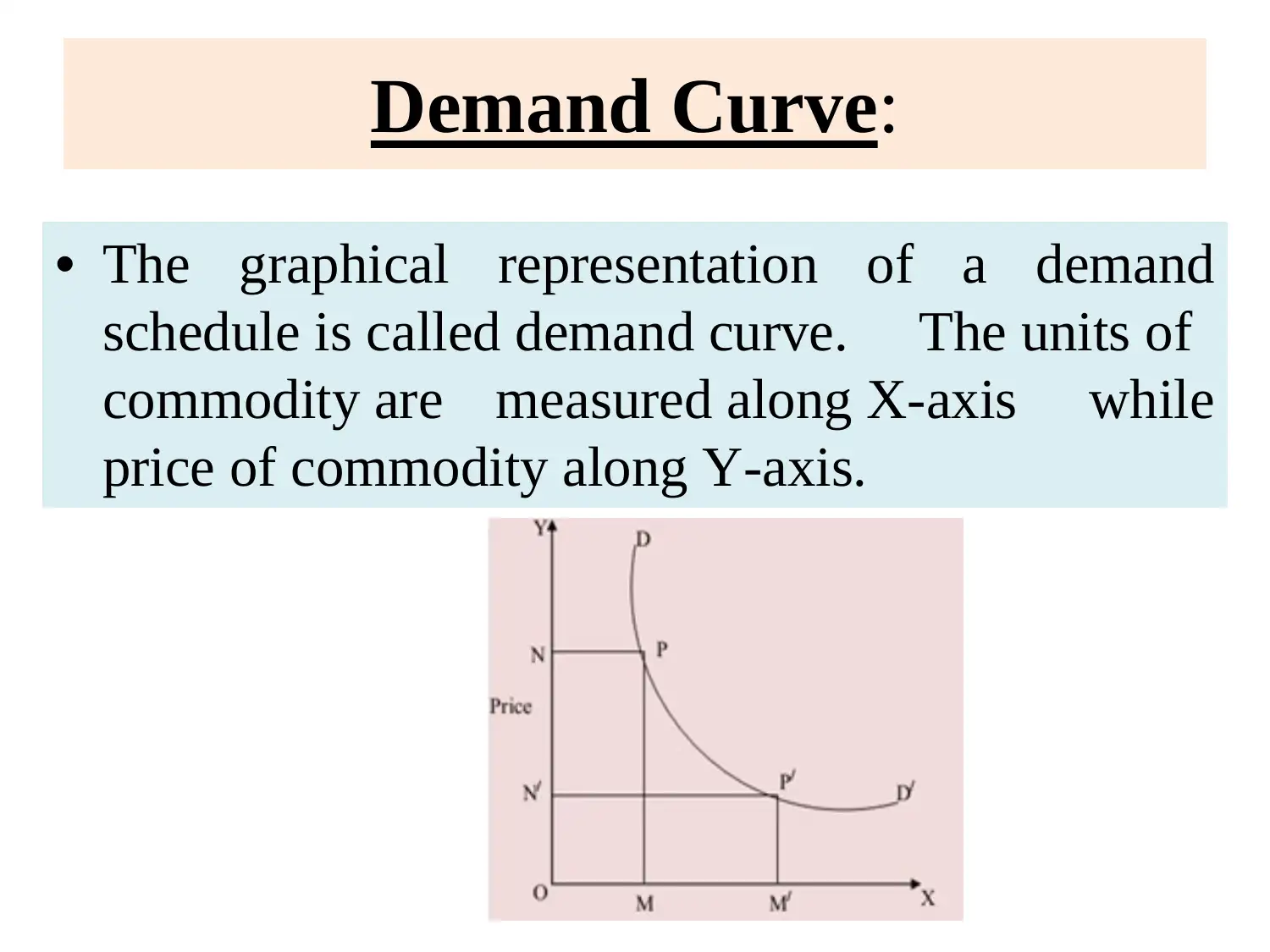

Demand Curve:

• The graphical representation of a demand

schedule is called demand curve. The units of

commodity are measured along X-axis while

price of commodity along Y-axis.

• The graphical representation of a demand

schedule is called demand curve. The units of

commodity are measured along X-axis while

price of commodity along Y-axis.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

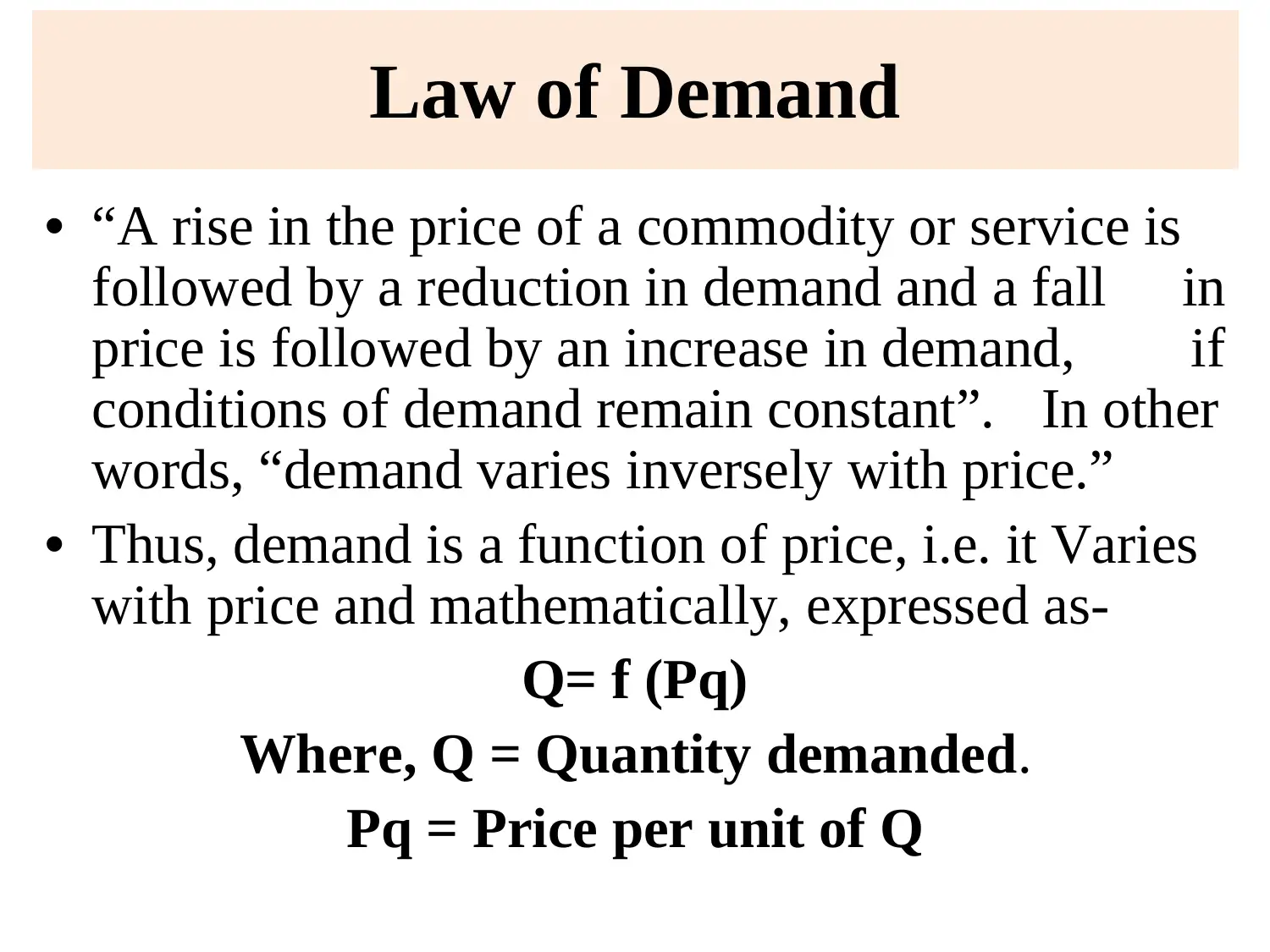

Law of Demand

• “A rise in the price of a commodity or service is

followed by a reduction in demand and a fall in

price is followed by an increase in demand, if

conditions of demand remain constant”. In other

words, “demand varies inversely with price.”

• Thus, demand is a function of price, i.e. it Varies

with price and mathematically, expressed as-

Q= f (Pq)

Where, Q = Quantity demanded.

Pq = Price per unit of Q

• “A rise in the price of a commodity or service is

followed by a reduction in demand and a fall in

price is followed by an increase in demand, if

conditions of demand remain constant”. In other

words, “demand varies inversely with price.”

• Thus, demand is a function of price, i.e. it Varies

with price and mathematically, expressed as-

Q= f (Pq)

Where, Q = Quantity demanded.

Pq = Price per unit of Q

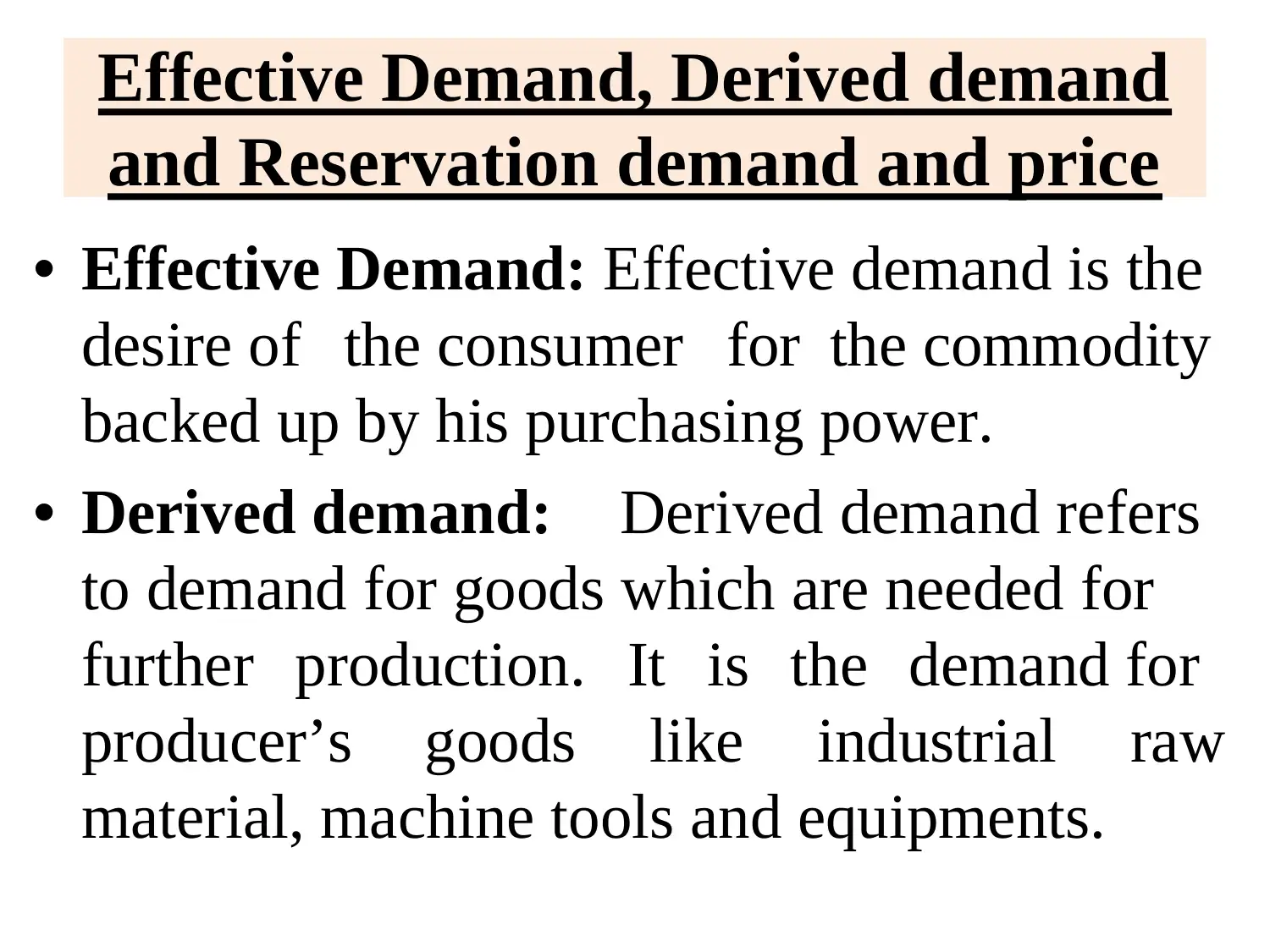

Effective Demand, Derived demand

and Reservation demand and price

• Effective Demand: Effective demand is the

desire of the consumer for the commodity

backed up by his purchasing power.

• Derived demand: Derived demand refers

to demand for goods which are needed for

further production. It is the demand for

producer’s goods like industrial raw

material, machine tools and equipments.

and Reservation demand and price

• Effective Demand: Effective demand is the

desire of the consumer for the commodity

backed up by his purchasing power.

• Derived demand: Derived demand refers

to demand for goods which are needed for

further production. It is the demand for

producer’s goods like industrial raw

material, machine tools and equipments.

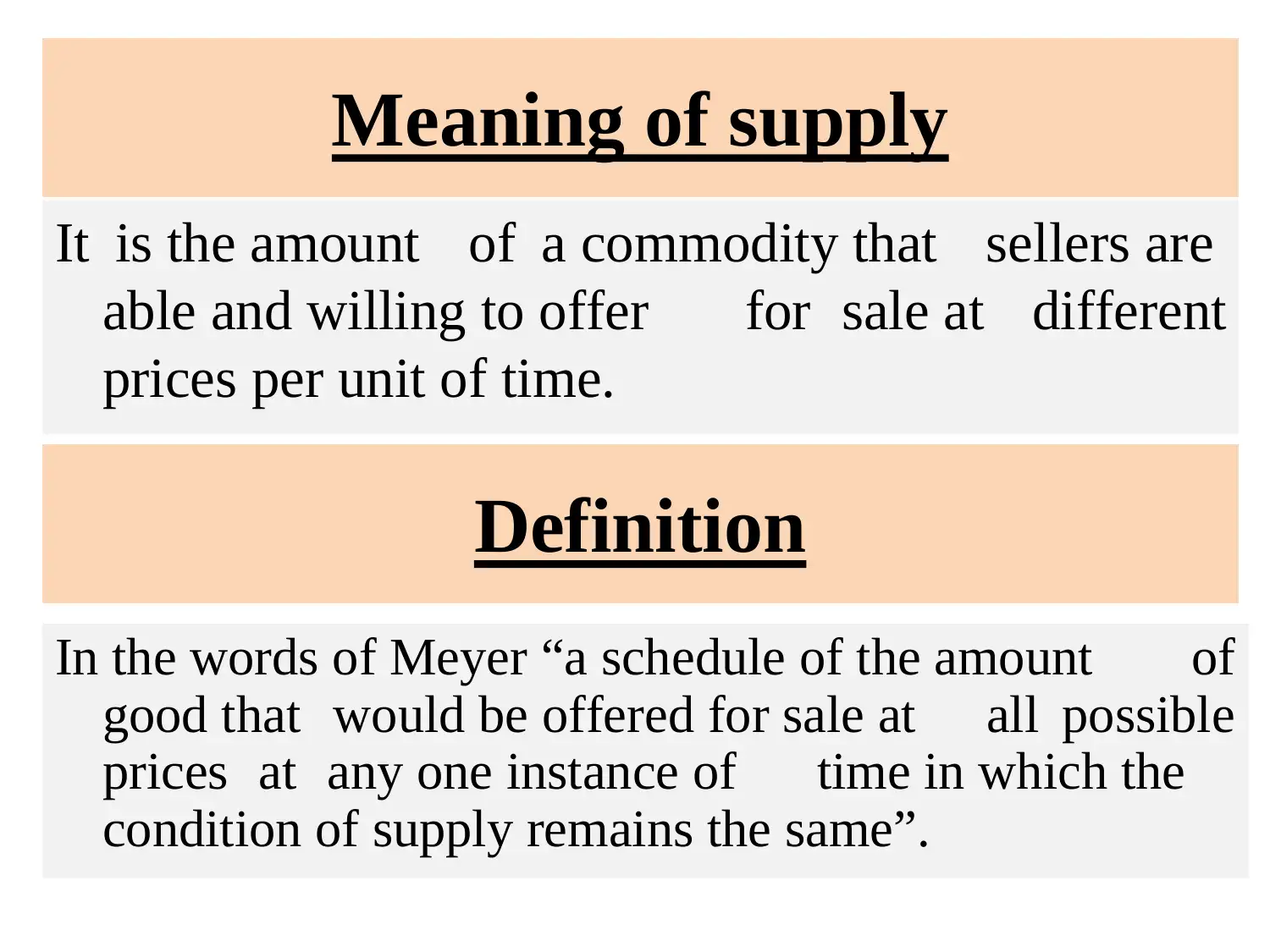

Meaning of supply

It is the amount of a commodity that sellers are

able and willing to offer for sale at different

prices per unit of time.

Definition

In the words of Meyer “a schedule of the amount of

good that would be offered for sale at all possible

prices at any one instance of time in which the

condition of supply remains the same”.

It is the amount of a commodity that sellers are

able and willing to offer for sale at different

prices per unit of time.

Definition

In the words of Meyer “a schedule of the amount of

good that would be offered for sale at all possible

prices at any one instance of time in which the

condition of supply remains the same”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

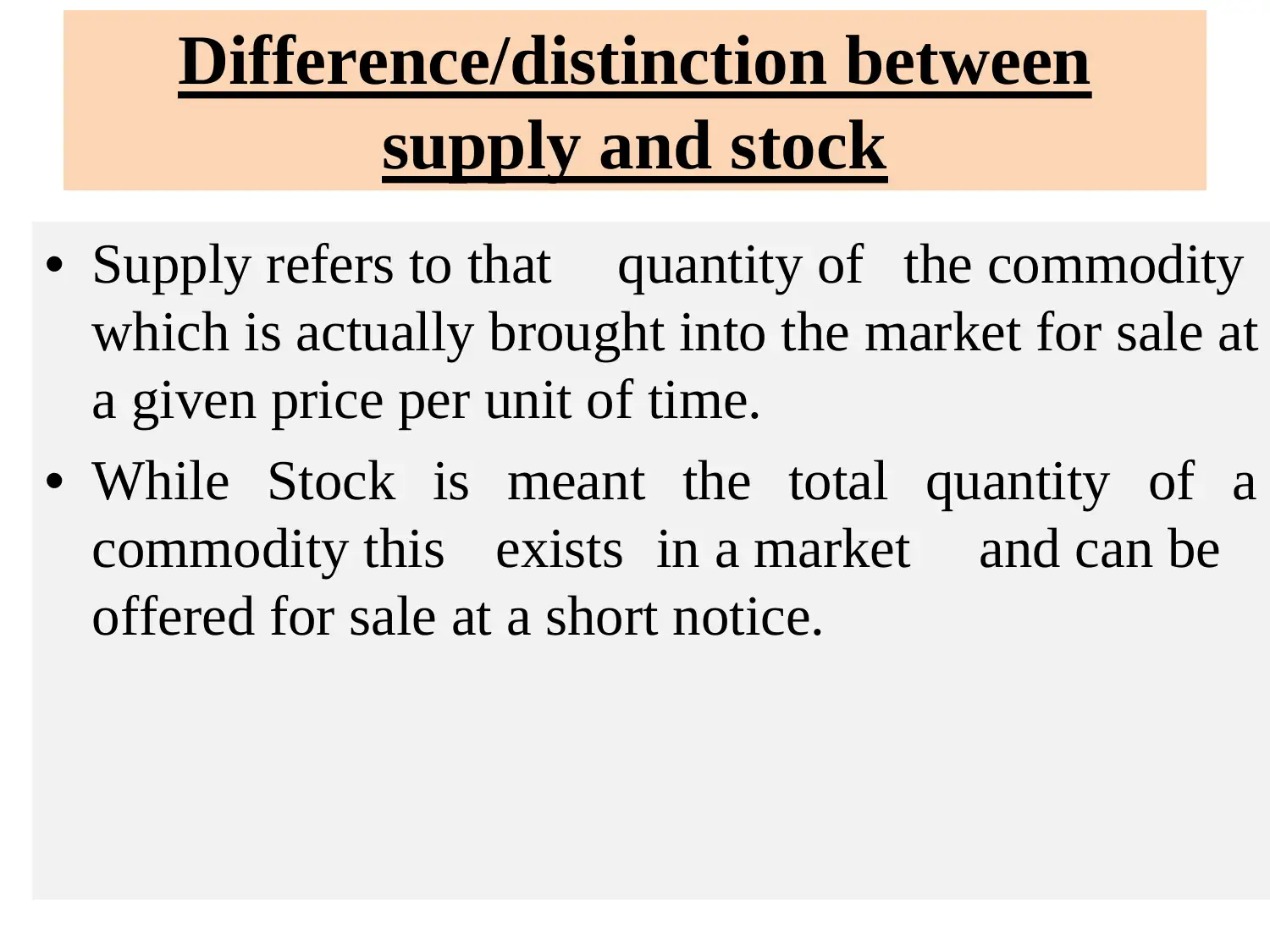

Difference/distinction between

supply and stock

• Supply refers to that quantity of the commodity

which is actually brought into the market for sale at

a given price per unit of time.

• While Stock is meant the total quantity of a

commodity this exists in a market and can be

offered for sale at a short notice.

supply and stock

• Supply refers to that quantity of the commodity

which is actually brought into the market for sale at

a given price per unit of time.

• While Stock is meant the total quantity of a

commodity this exists in a market and can be

offered for sale at a short notice.

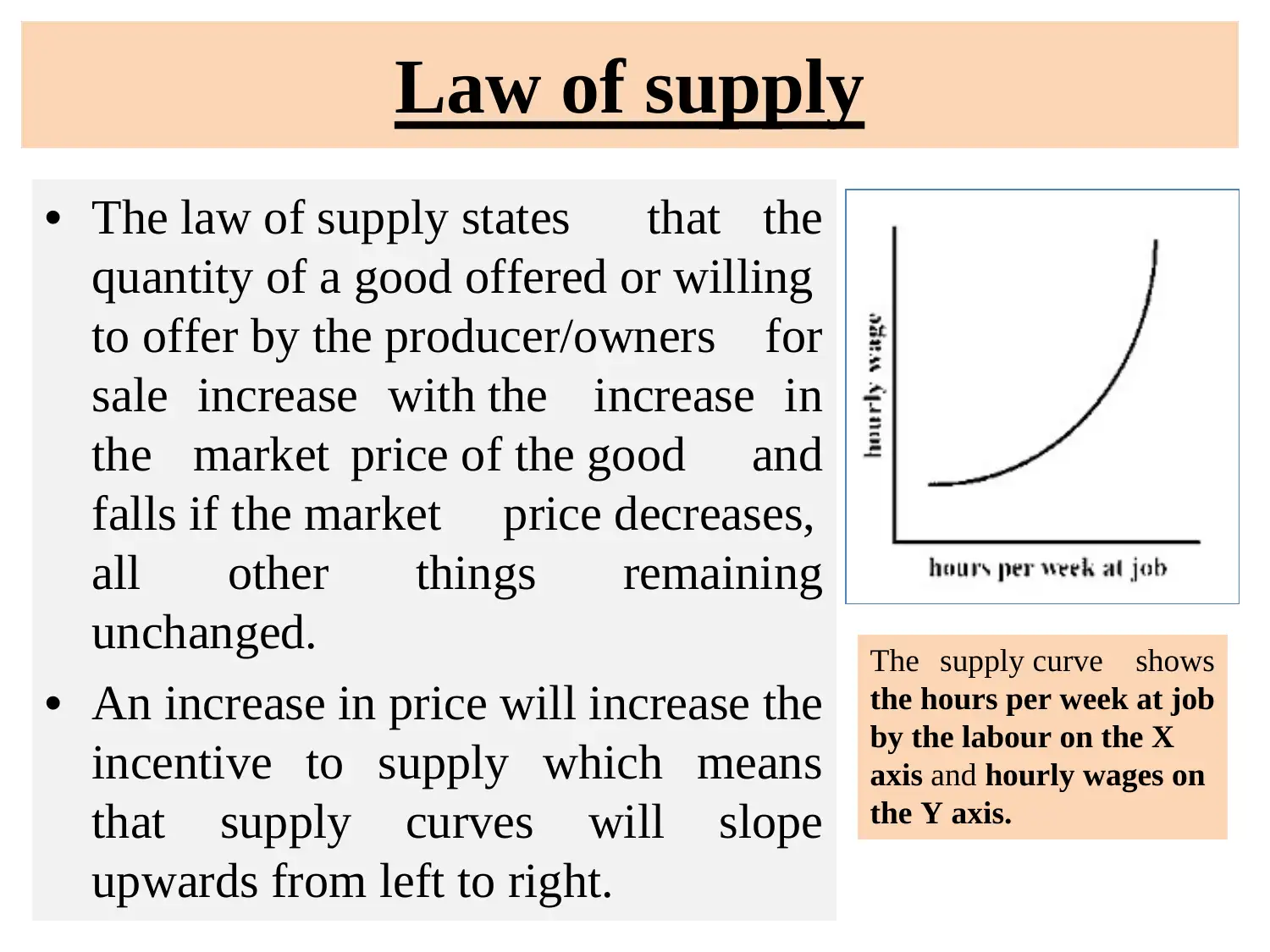

Law of supply

• The law of supply states that the

quantity of a good offered or willing

to offer by the producer/owners for

sale increase with the increase in

the market price of the good and

falls if the market price decreases,

all other things remaining

unchanged.

• An increase in price will increase the

incentive to supply which means

that supply curves will slope

upwards from left to right.

The supply curve shows

the hours per week at job

by the labour on the X

axis and hourly wages on

the Y axis.

• The law of supply states that the

quantity of a good offered or willing

to offer by the producer/owners for

sale increase with the increase in

the market price of the good and

falls if the market price decreases,

all other things remaining

unchanged.

• An increase in price will increase the

incentive to supply which means

that supply curves will slope

upwards from left to right.

The supply curve shows

the hours per week at job

by the labour on the X

axis and hourly wages on

the Y axis.

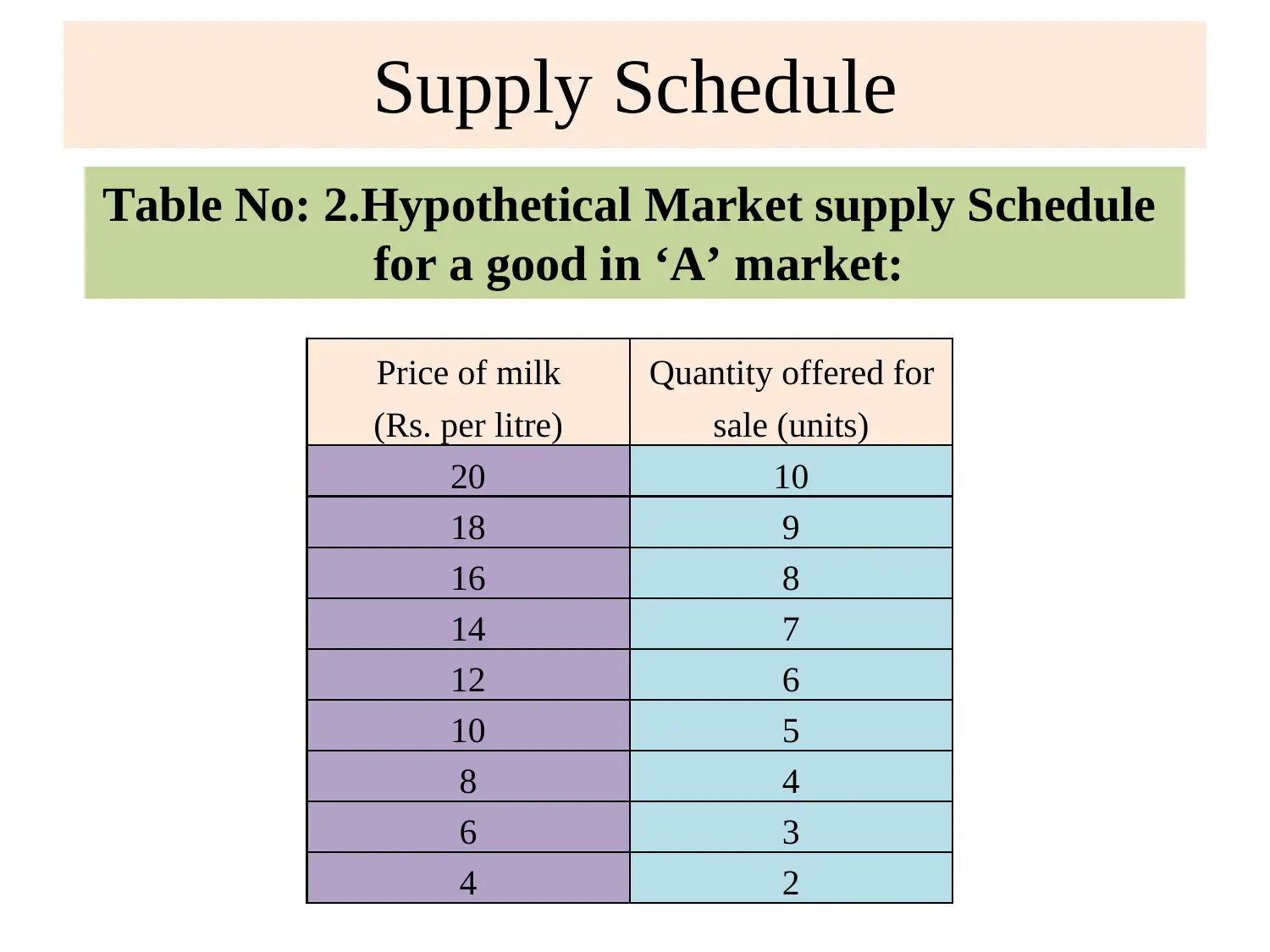

Supply Schedule

Price of milk

(Rs. per litre)

Quantity offered for

sale (units)

20 10

18 9

16 8

14 7

12 6

10 5

8 4

6 3

4 2

Table No: 2.Hypothetical Market supply Schedule

for a good in ‘A’ market:

Price of milk

(Rs. per litre)

Quantity offered for

sale (units)

20 10

18 9

16 8

14 7

12 6

10 5

8 4

6 3

4 2

Table No: 2.Hypothetical Market supply Schedule

for a good in ‘A’ market:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

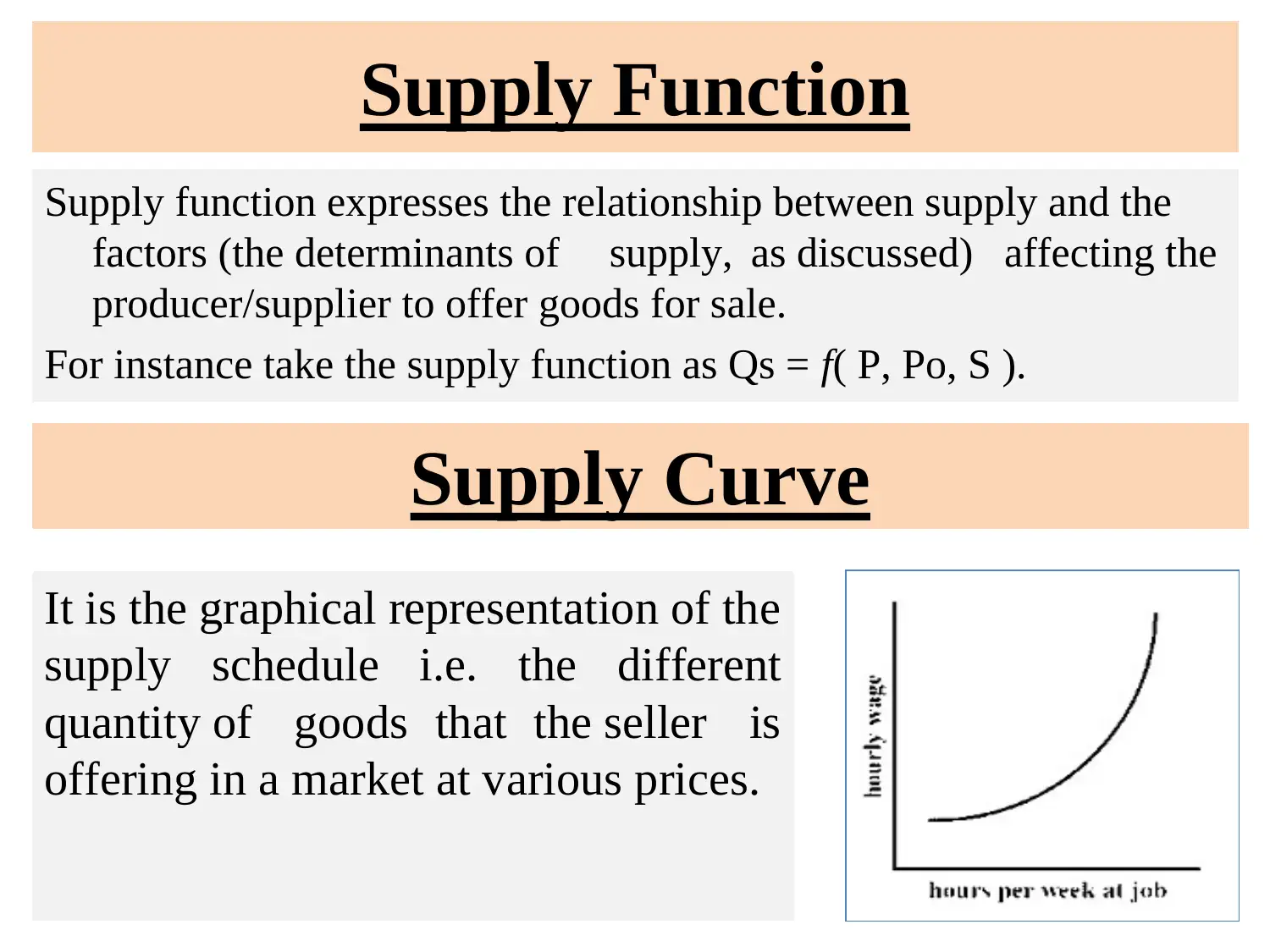

Supply Function

Supply function expresses the relationship between supply and the

factors (the determinants of supply, as discussed) affecting the

producer/supplier to offer goods for sale.

For instance take the supply function as Qs = f( P, Po, S ).

Supply Curve

It is the graphical representation of the

supply schedule i.e. the different

quantity of goods that the seller is

offering in a market at various prices.

Supply function expresses the relationship between supply and the

factors (the determinants of supply, as discussed) affecting the

producer/supplier to offer goods for sale.

For instance take the supply function as Qs = f( P, Po, S ).

Supply Curve

It is the graphical representation of the

supply schedule i.e. the different

quantity of goods that the seller is

offering in a market at various prices.

The time periods can be of different

lengths.

• Short Run: This means that the existing production is

already on hand and that the cost incurred on its

production does not influence its price.

• Intermediate Run: This refers to the time during

which goods can be produced only with the existing

production facilities. The existing capacity puts an

upper limit on the quantity that can be offered for

sale.

• Long run: The term long run refers to the time during

which production facilities themselves may be expand

or contracted.

lengths.

• Short Run: This means that the existing production is

already on hand and that the cost incurred on its

production does not influence its price.

• Intermediate Run: This refers to the time during

which goods can be produced only with the existing

production facilities. The existing capacity puts an

upper limit on the quantity that can be offered for

sale.

• Long run: The term long run refers to the time during

which production facilities themselves may be expand

or contracted.

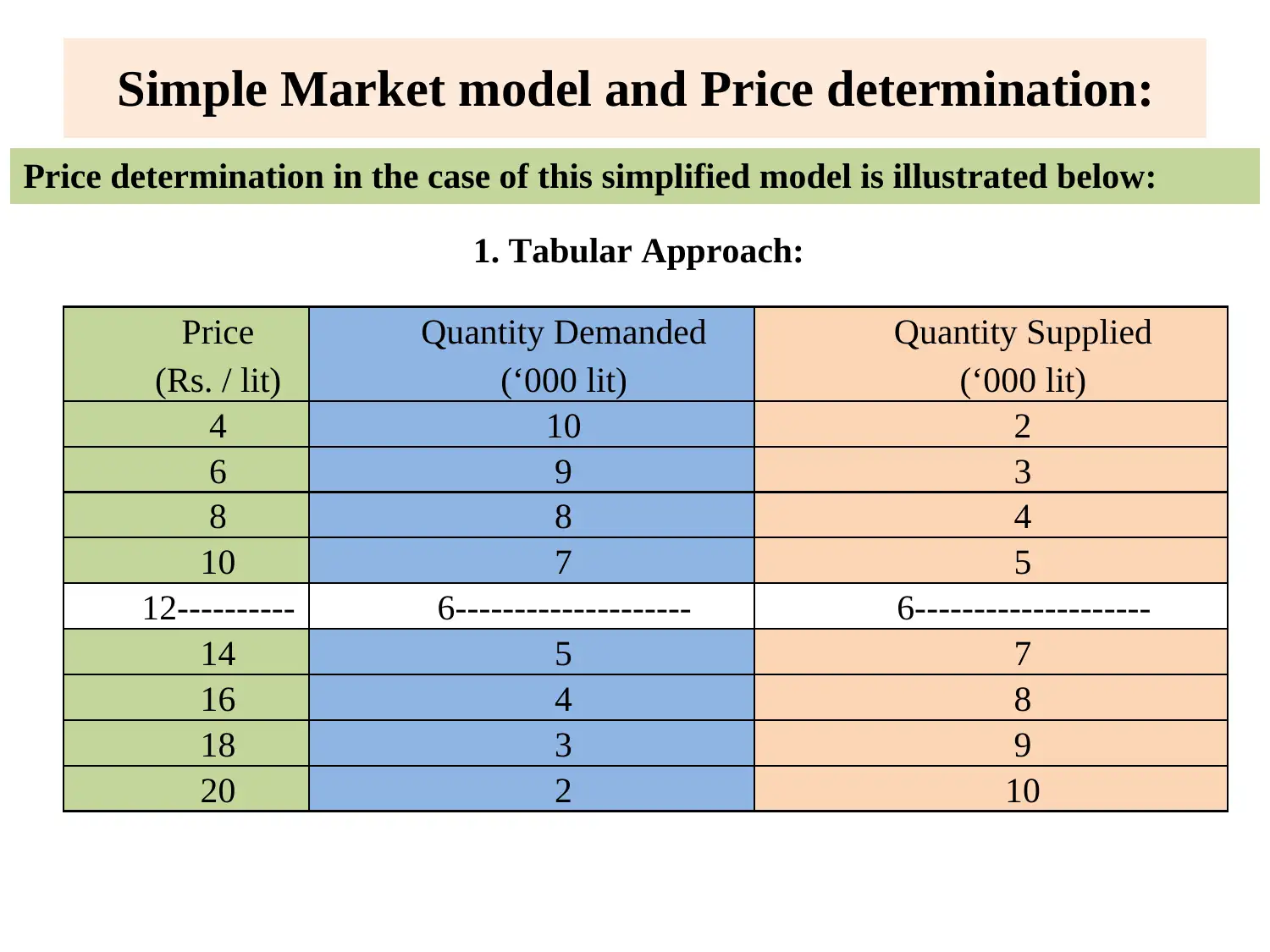

Simple Market model and Price determination:

1. Tabular Approach:

Price determination in the case of this simplified model is illustrated below:

Price

(Rs. / lit)

Quantity Demanded

(‘000 lit)

Quantity Supplied

(‘000 lit)

4 10 2

6 9 3

8 8 4

10 7 5

12---------- 6-------------------- 6--------------------

14 5 7

16 4 8

18 3 9

20 2 10

1. Tabular Approach:

Price determination in the case of this simplified model is illustrated below:

Price

(Rs. / lit)

Quantity Demanded

(‘000 lit)

Quantity Supplied

(‘000 lit)

4 10 2

6 9 3

8 8 4

10 7 5

12---------- 6-------------------- 6--------------------

14 5 7

16 4 8

18 3 9

20 2 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

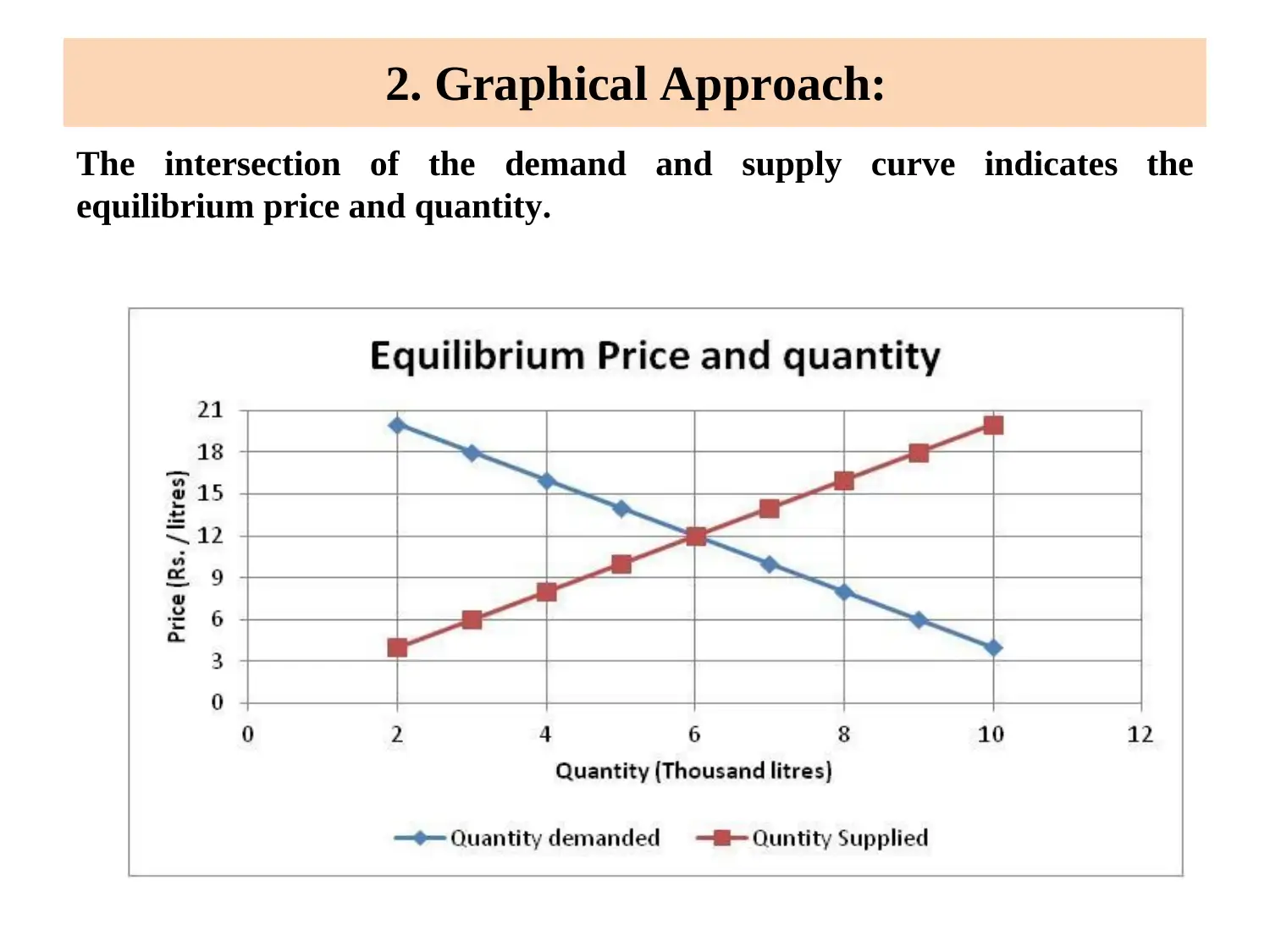

2. Graphical Approach:

The intersection of the demand and supply curve indicates the

equilibrium price and quantity.

The intersection of the demand and supply curve indicates the

equilibrium price and quantity.

Thank you

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.