Depreciation: Methods, Calculations, and Examples in Finance

VerifiedAdded on 2019/09/24

|6

|1121

|217

Homework Assignment

AI Summary

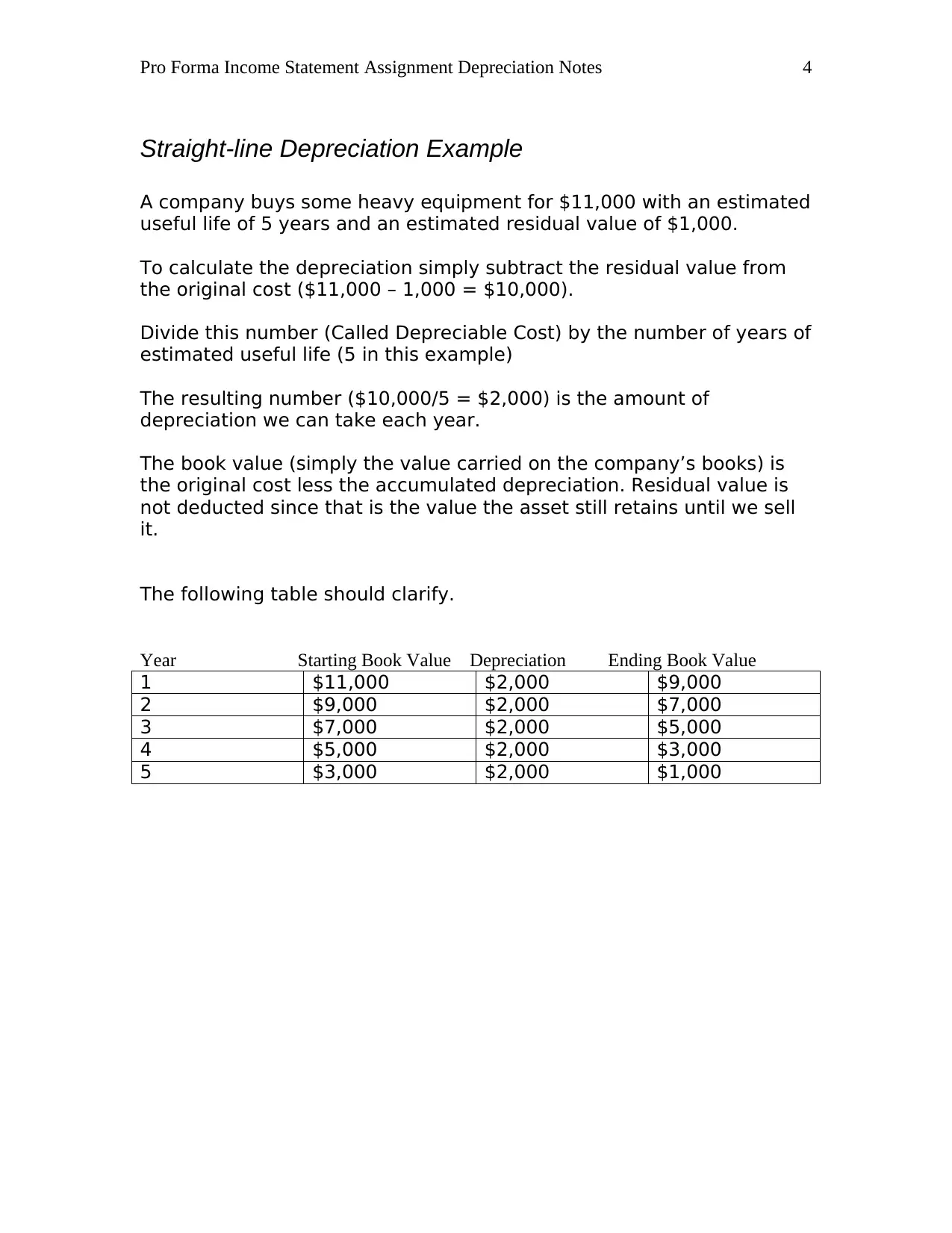

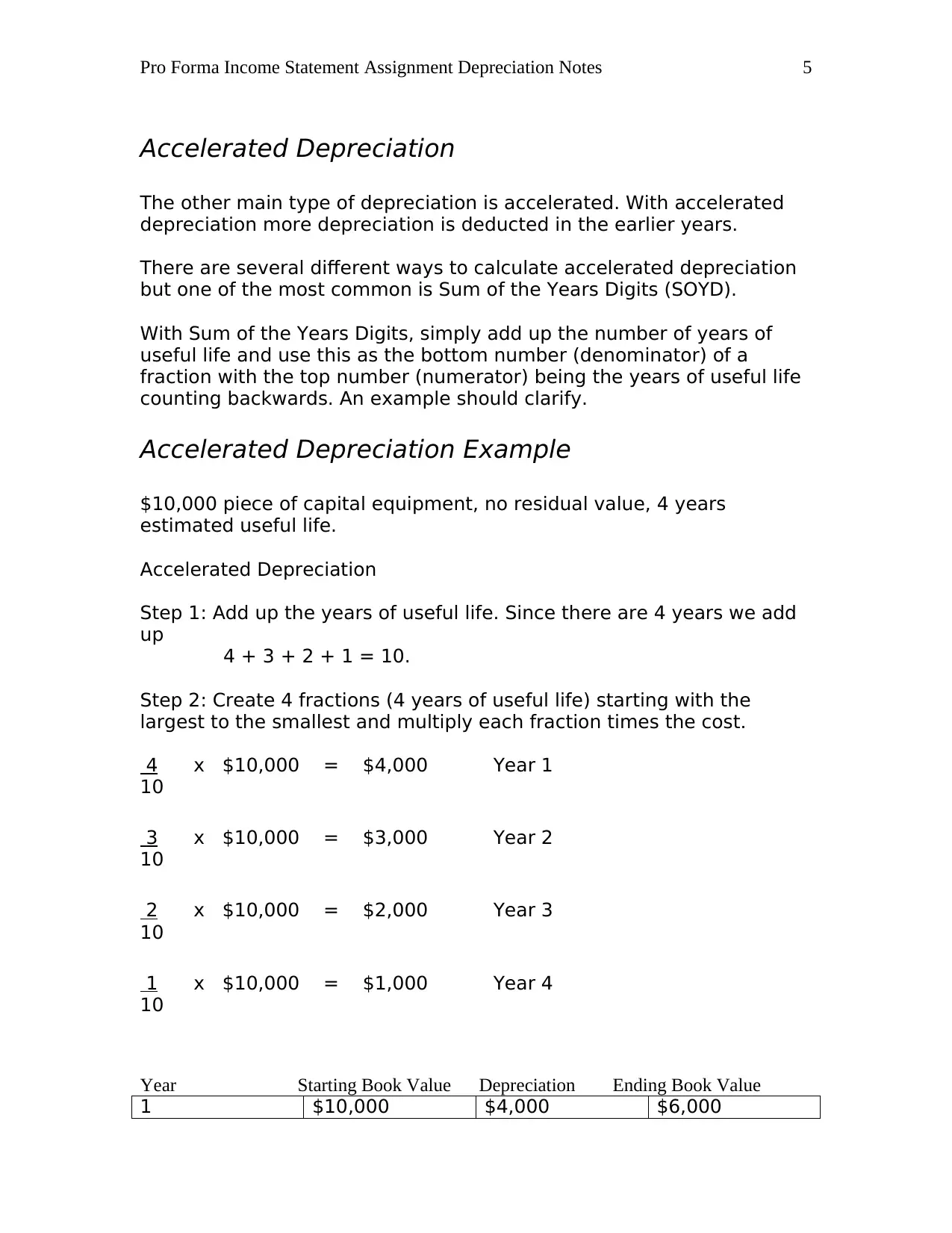

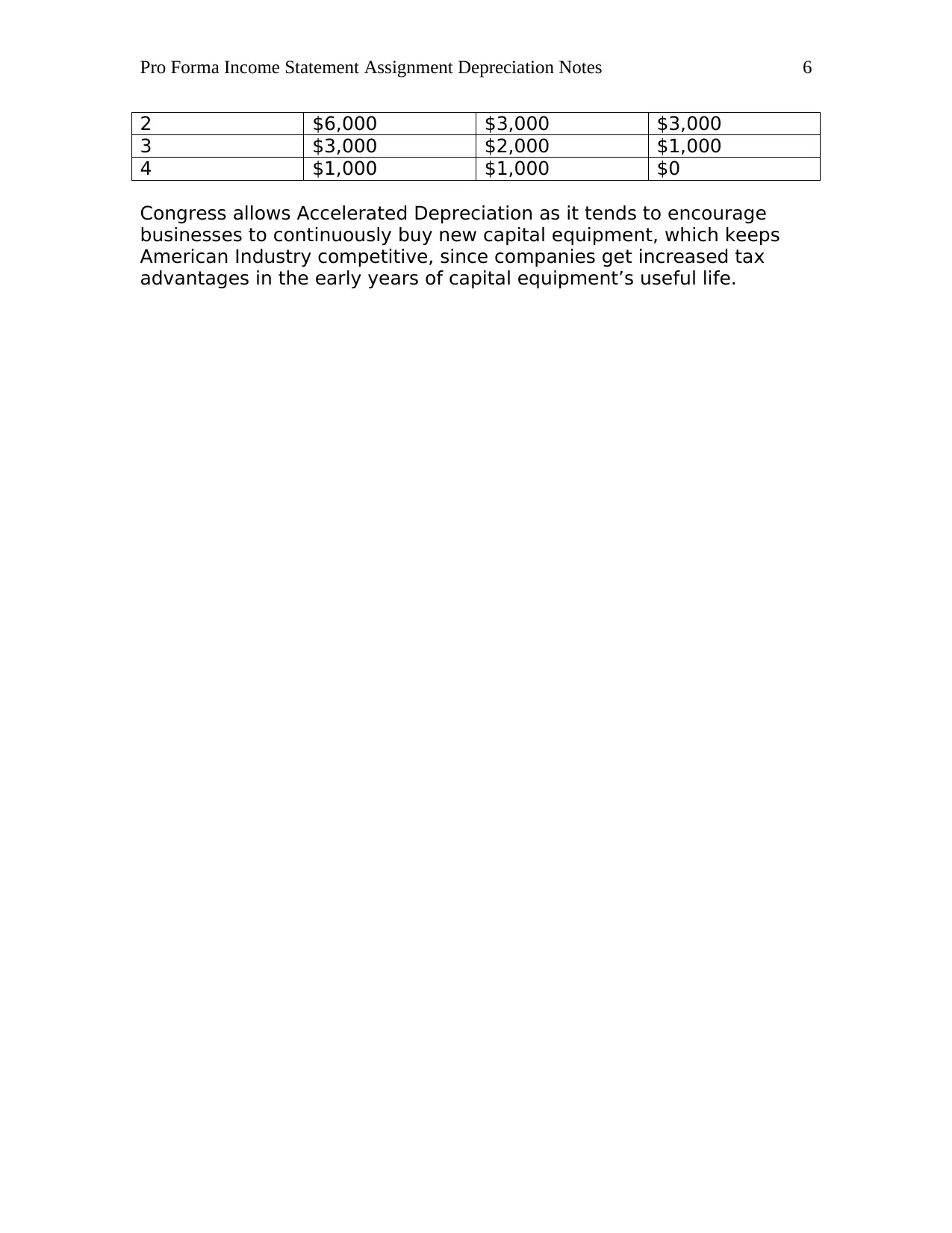

This assignment provides a comprehensive introduction to depreciation, a key concept in finance and accounting. It explains depreciation as an income tax deduction used to recover the cost of property over time, covering both tangible and intangible assets. The assignment outlines the requirements for property to be depreciable, including ownership, business use, determinable useful life, and lasting more than one year. It then delves into the two primary depreciation methods: straight-line and accelerated depreciation. The straight-line method is explained with a detailed example, illustrating how to calculate annual depreciation expense, book value, and residual value. The assignment also explores accelerated depreciation, specifically the sum of the years' digits (SOYD) method, providing a step-by-step example to demonstrate its calculation. The document emphasizes the importance of depreciation in encouraging capital investment and its impact on tax advantages for businesses. It also highlights that interpretation of IRS regulations is best left to tax professionals.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.