Economic and Financial Management: Vodafone Plc. Performance Analysis

VerifiedAdded on 2022/08/13

|13

|3026

|21

Report

AI Summary

This report presents a financial analysis of Vodafone Plc., examining its performance from 2017 to 2019. It begins with an executive summary and an introduction outlining the relationship between business and economic factors. The report then delves into the analysis of economic factors, both macro and micro, and their impact on Vodafone's operations, including the effects of Brexit and legal changes. A key component of the report is the financial ratio analysis, including Return on Capital Employed (ROCE), Net Profit Margin, Current Ratio, and Debtors Collection Period, with calculations and interpretations for each year. The report discusses the significance of accounting ratios and concludes with recommendations based on the findings. The analysis reveals a decline in ROCE in 2019 due to impairment losses, and fluctuations in net profit margins, highlighting the influence of external factors and financial strategies on Vodafone's performance. The current ratio indicates an improved short-term financial health in 2019, and the debtors collection period is also discussed, providing a comprehensive overview of Vodafone's financial position and management efficiency.

ECONOMIC AND FINANCIAL MANAGEMENT

Module code: 216MANSC/216MANEL

2/18/2020

Student’s name:

Module code: 216MANSC/216MANEL

2/18/2020

Student’s name:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The module and the assignment are aimed at guiding the decision making processes to the

various group of stakeholders. The significance of such a guide lies in the fact that the

business operations are affected by the external and internal environment factors. The result

of the same is that the financial performance fluctuates and so the demand for the shares of an

organisation in the market. The analysis of the shifts in the financial performance has been

conducted with the aid of the financial ratios which are one of the most basic tools for

financial analysis. The importance of the accounting ratios is that the ease of computation,

comparison and evaluation of the changes.

The module and the assignment are aimed at guiding the decision making processes to the

various group of stakeholders. The significance of such a guide lies in the fact that the

business operations are affected by the external and internal environment factors. The result

of the same is that the financial performance fluctuates and so the demand for the shares of an

organisation in the market. The analysis of the shifts in the financial performance has been

conducted with the aid of the financial ratios which are one of the most basic tools for

financial analysis. The importance of the accounting ratios is that the ease of computation,

comparison and evaluation of the changes.

Contents

Introduction...........................................................................................................................................3

A. Analysis of the Economic Factors and the discussion of the impacts on the business...................3

B. Financial Ratio Analysis................................................................................................................4

(i) Return on capital employed:......................................................................................................4

(ii) Net Profit Margin:..................................................................................................................5

(iii) Current Ratio:........................................................................................................................7

(iv) Debtors Collection Period:.....................................................................................................8

C. Accounting Ratios and their significance......................................................................................9

D. Recommendations.......................................................................................................................10

E. Conclusion...................................................................................................................................10

References...........................................................................................................................................12

Introduction...........................................................................................................................................3

A. Analysis of the Economic Factors and the discussion of the impacts on the business...................3

B. Financial Ratio Analysis................................................................................................................4

(i) Return on capital employed:......................................................................................................4

(ii) Net Profit Margin:..................................................................................................................5

(iii) Current Ratio:........................................................................................................................7

(iv) Debtors Collection Period:.....................................................................................................8

C. Accounting Ratios and their significance......................................................................................9

D. Recommendations.......................................................................................................................10

E. Conclusion...................................................................................................................................10

References...........................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

A business organisation engages in the production of goods and services that drive the

economic output of a nation or a region. The relationship of a business and the economy can

be stated in the fact that the collective performances of business affect the economy at large.

In conjunction to this, the economic factors such as the inflation rates, interest rates,

consumer behaviour, employment rates, banking policies affect the performances of the

businesses (Robinson et. al. 2015). This means the increment or the decrement in the cost of

production which includes the material costs, labour costs, taxation charges, and others lead

to the movements and the shifts in the supply and demand curves.

The aim of the following report is to highlight the economic factors that influence the

conducts of a business, as examined in the case of the organisation Vodafone Plc., which is a

renowned organisation of UK and globally as well.

A. Analysis of the Economic Factors and the discussion of the

impacts on the business

There are various macro and micro economic factors that influence the conduct of the

business, which are elaborated as follows.

Macro Factors: The key macro-economic factors that affect the conduct of a business are

political, economic, social, legal and the technological factors. All the above factors lead to

the increment or the decrease in the cost of production of goods or the provision of the

services. For instance, the current external environment of Vodafone is influenced by the

events like Brexit, the legal changes leading to disposal of the certain business units. As the

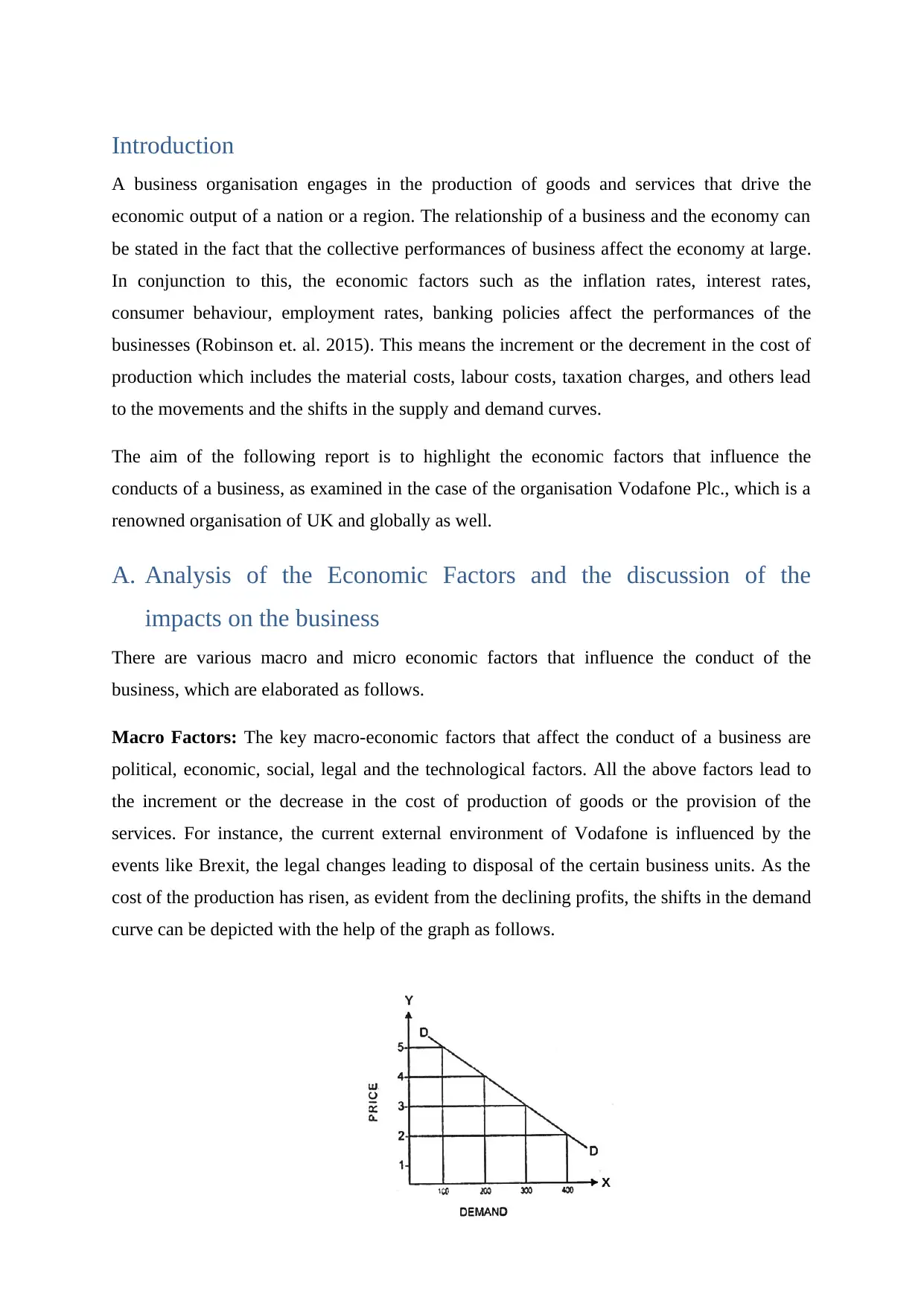

cost of the production has risen, as evident from the declining profits, the shifts in the demand

curve can be depicted with the help of the graph as follows.

A business organisation engages in the production of goods and services that drive the

economic output of a nation or a region. The relationship of a business and the economy can

be stated in the fact that the collective performances of business affect the economy at large.

In conjunction to this, the economic factors such as the inflation rates, interest rates,

consumer behaviour, employment rates, banking policies affect the performances of the

businesses (Robinson et. al. 2015). This means the increment or the decrement in the cost of

production which includes the material costs, labour costs, taxation charges, and others lead

to the movements and the shifts in the supply and demand curves.

The aim of the following report is to highlight the economic factors that influence the

conducts of a business, as examined in the case of the organisation Vodafone Plc., which is a

renowned organisation of UK and globally as well.

A. Analysis of the Economic Factors and the discussion of the

impacts on the business

There are various macro and micro economic factors that influence the conduct of the

business, which are elaborated as follows.

Macro Factors: The key macro-economic factors that affect the conduct of a business are

political, economic, social, legal and the technological factors. All the above factors lead to

the increment or the decrease in the cost of production of goods or the provision of the

services. For instance, the current external environment of Vodafone is influenced by the

events like Brexit, the legal changes leading to disposal of the certain business units. As the

cost of the production has risen, as evident from the declining profits, the shifts in the demand

curve can be depicted with the help of the graph as follows.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As depicted in the figure above, as the cost of production and the prices of a commodity rises,

the demand of the said product falls.

Micro Factors: While the macro factors deal with the external business environment, the

micro factors are the ones focussed on the internal business environment or the stakeholders

of the entity. The micro factors include the distribution channels, competitors, customers,

suppliers, and others. Thus, the change in the above factors influences the demands of the

products, the financial performances and eventually the share prices of the stock of the

company. The shifts are caused due to the changes in the population structure, the changes in

the consumer preferences, shifts in the prices of the substitute or the complementary goods

and others.

Glimpse of the financial performance for three year period

The financial performance of the company Vodafone was analysed over a period of three

years. The performance from the point of view of profitability was lowest in the year 2019

due to the disposal activities, though the assets improved in the said year. Overall it can be

stated that the external factors of the legal regulations and the resulting impact influenced the

financial performance considerably.

B. Financial Ratio Analysis

(i) Return on capital employed:

The return on capital employed ratio is used to measure the profitability of the company in

relation to the capital used. Thus, it is assessed that how well an organisation generates

profits against the capital employed in the business (Delen, Kuzey and Uyar, 2013). The ratio

is of prime interest to the potential and the existing investors, to assess the return that would

be earned on their investments. The earnings before interest and tax or the operating profit is

used for the said evaluation to analyse the efficiency of the company in relation to the

operations that is without the consideration of the interests and the taxes. The formula for the

computation of the above ratio is stated as follows.

Return on capital employed: Operating Profit/ Capital Employed

The following table highlights the return on the capital employed of Vodafone for the years

2019, 2018 and 2017.

the demand of the said product falls.

Micro Factors: While the macro factors deal with the external business environment, the

micro factors are the ones focussed on the internal business environment or the stakeholders

of the entity. The micro factors include the distribution channels, competitors, customers,

suppliers, and others. Thus, the change in the above factors influences the demands of the

products, the financial performances and eventually the share prices of the stock of the

company. The shifts are caused due to the changes in the population structure, the changes in

the consumer preferences, shifts in the prices of the substitute or the complementary goods

and others.

Glimpse of the financial performance for three year period

The financial performance of the company Vodafone was analysed over a period of three

years. The performance from the point of view of profitability was lowest in the year 2019

due to the disposal activities, though the assets improved in the said year. Overall it can be

stated that the external factors of the legal regulations and the resulting impact influenced the

financial performance considerably.

B. Financial Ratio Analysis

(i) Return on capital employed:

The return on capital employed ratio is used to measure the profitability of the company in

relation to the capital used. Thus, it is assessed that how well an organisation generates

profits against the capital employed in the business (Delen, Kuzey and Uyar, 2013). The ratio

is of prime interest to the potential and the existing investors, to assess the return that would

be earned on their investments. The earnings before interest and tax or the operating profit is

used for the said evaluation to analyse the efficiency of the company in relation to the

operations that is without the consideration of the interests and the taxes. The formula for the

computation of the above ratio is stated as follows.

Return on capital employed: Operating Profit/ Capital Employed

The following table highlights the return on the capital employed of Vodafone for the years

2019, 2018 and 2017.

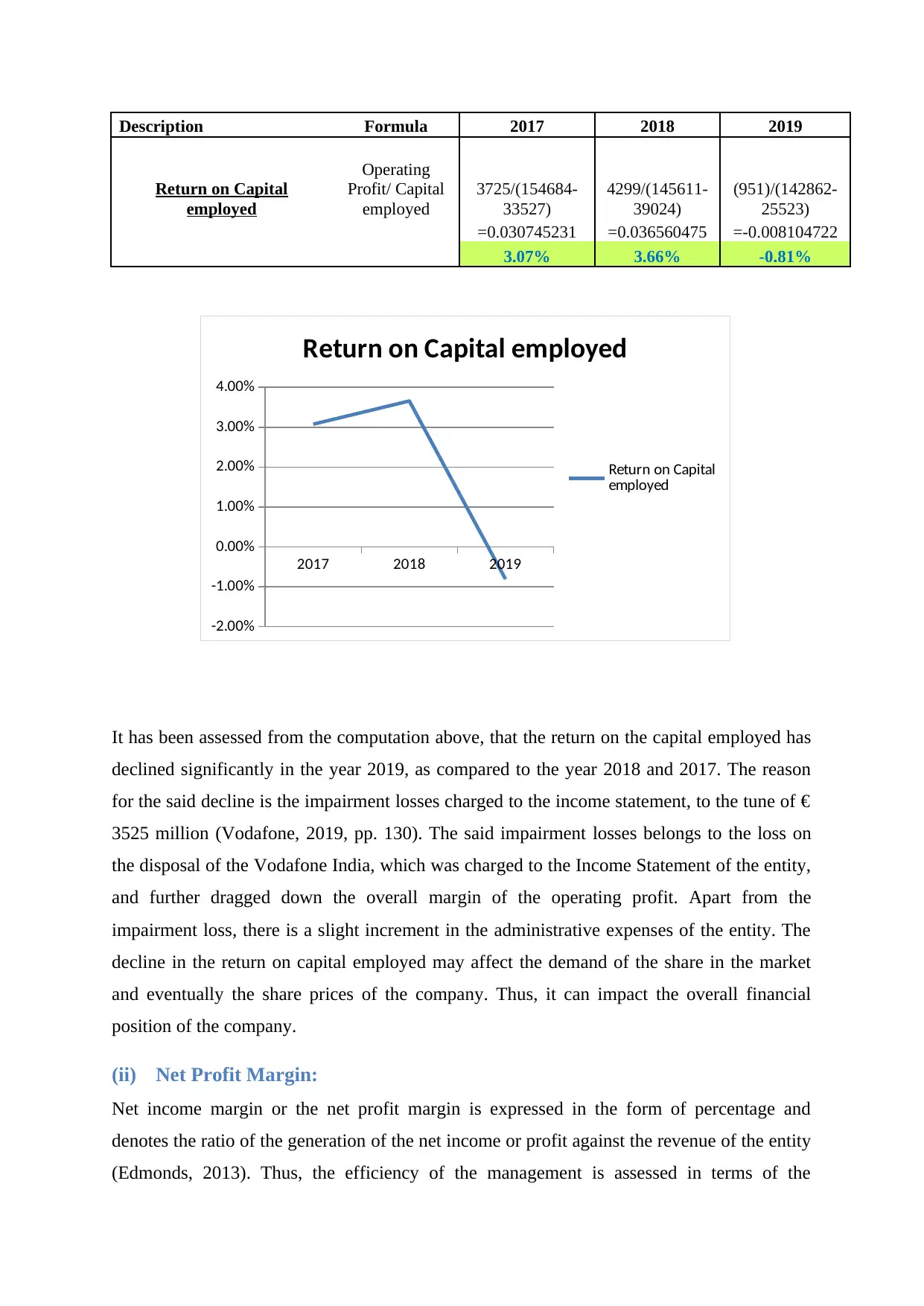

Description Formula 2017 2018 2019

Return on Capital

employed

Operating

Profit/ Capital

employed

3725/(154684-

33527)

4299/(145611-

39024)

(951)/(142862-

25523)

=0.030745231 =0.036560475 =-0.008104722

3.07% 3.66% -0.81%

It has been assessed from the computation above, that the return on the capital employed has

declined significantly in the year 2019, as compared to the year 2018 and 2017. The reason

for the said decline is the impairment losses charged to the income statement, to the tune of €

3525 million (Vodafone, 2019, pp. 130). The said impairment losses belongs to the loss on

the disposal of the Vodafone India, which was charged to the Income Statement of the entity,

and further dragged down the overall margin of the operating profit. Apart from the

impairment loss, there is a slight increment in the administrative expenses of the entity. The

decline in the return on capital employed may affect the demand of the share in the market

and eventually the share prices of the company. Thus, it can impact the overall financial

position of the company.

(ii) Net Profit Margin:

Net income margin or the net profit margin is expressed in the form of percentage and

denotes the ratio of the generation of the net income or profit against the revenue of the entity

(Edmonds, 2013). Thus, the efficiency of the management is assessed in terms of the

2017 2018 2019

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

Return on Capital employed

Return on Capital

employed

Return on Capital

employed

Operating

Profit/ Capital

employed

3725/(154684-

33527)

4299/(145611-

39024)

(951)/(142862-

25523)

=0.030745231 =0.036560475 =-0.008104722

3.07% 3.66% -0.81%

It has been assessed from the computation above, that the return on the capital employed has

declined significantly in the year 2019, as compared to the year 2018 and 2017. The reason

for the said decline is the impairment losses charged to the income statement, to the tune of €

3525 million (Vodafone, 2019, pp. 130). The said impairment losses belongs to the loss on

the disposal of the Vodafone India, which was charged to the Income Statement of the entity,

and further dragged down the overall margin of the operating profit. Apart from the

impairment loss, there is a slight increment in the administrative expenses of the entity. The

decline in the return on capital employed may affect the demand of the share in the market

and eventually the share prices of the company. Thus, it can impact the overall financial

position of the company.

(ii) Net Profit Margin:

Net income margin or the net profit margin is expressed in the form of percentage and

denotes the ratio of the generation of the net income or profit against the revenue of the entity

(Edmonds, 2013). Thus, the efficiency of the management is assessed in terms of the

2017 2018 2019

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

Return on Capital employed

Return on Capital

employed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

generation of profits for the business segment, the entity is operating in. The said ratio is of

prime interest not only for the shareholders of the entity, but the other stakeholders as well.

The analysis of the said ratio is conducted generally in relation to the performance of the

industry competitors and the yearly performance of the entity itself. The formula is expressed

as follows.

Net Profit Margin = Net profit / Sales or revenue

The following table indicates the net profit margins of the company Vodafone for the

financial years 2019, 2018, 2017.

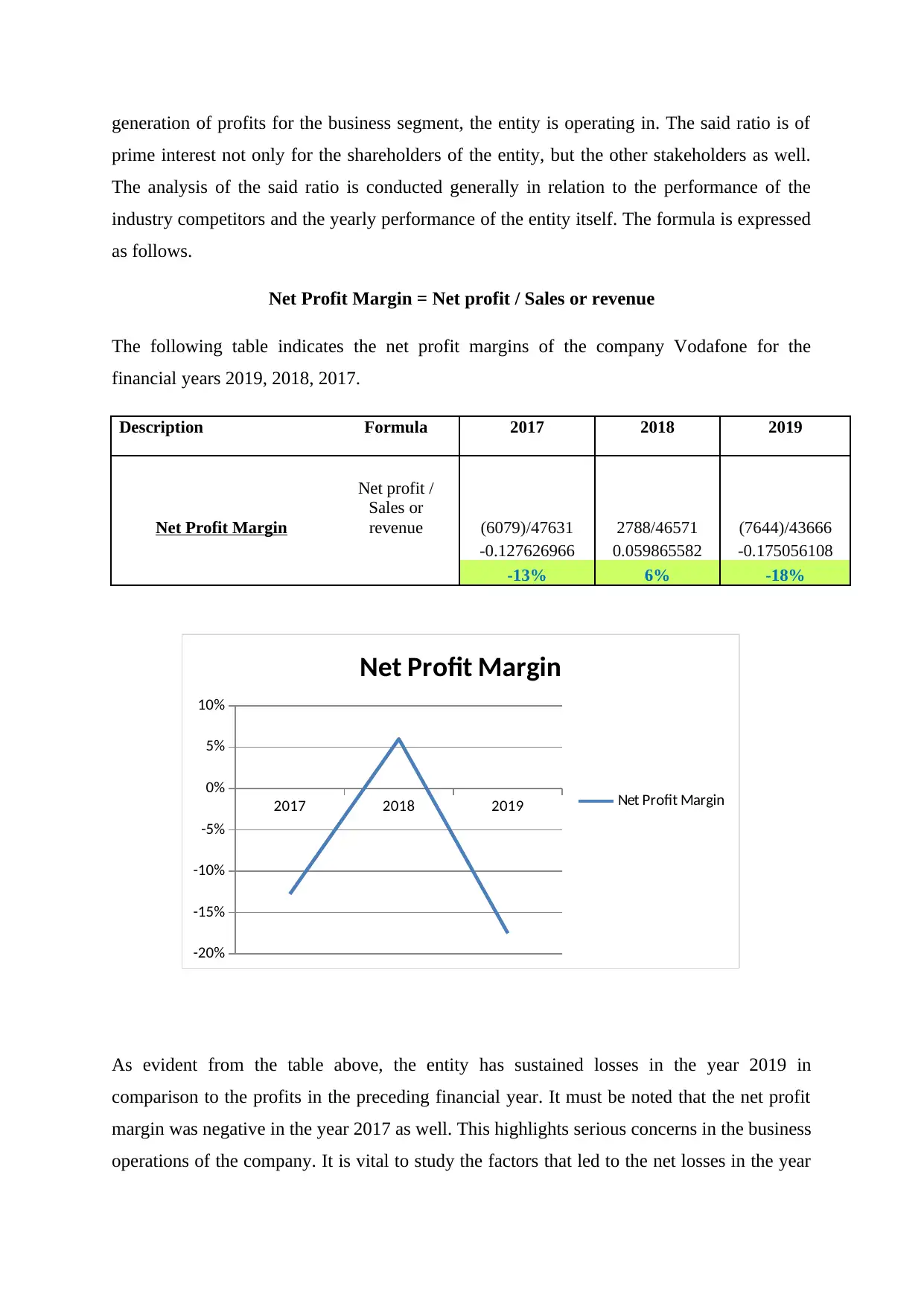

Description Formula 2017 2018 2019

Net Profit Margin

Net profit /

Sales or

revenue (6079)/47631 2788/46571 (7644)/43666

-0.127626966 0.059865582 -0.175056108

-13% 6% -18%

As evident from the table above, the entity has sustained losses in the year 2019 in

comparison to the profits in the preceding financial year. It must be noted that the net profit

margin was negative in the year 2017 as well. This highlights serious concerns in the business

operations of the company. It is vital to study the factors that led to the net losses in the year

2017 2018 2019

-20%

-15%

-10%

-5%

0%

5%

10%

Net Profit Margin

Net Profit Margin

prime interest not only for the shareholders of the entity, but the other stakeholders as well.

The analysis of the said ratio is conducted generally in relation to the performance of the

industry competitors and the yearly performance of the entity itself. The formula is expressed

as follows.

Net Profit Margin = Net profit / Sales or revenue

The following table indicates the net profit margins of the company Vodafone for the

financial years 2019, 2018, 2017.

Description Formula 2017 2018 2019

Net Profit Margin

Net profit /

Sales or

revenue (6079)/47631 2788/46571 (7644)/43666

-0.127626966 0.059865582 -0.175056108

-13% 6% -18%

As evident from the table above, the entity has sustained losses in the year 2019 in

comparison to the profits in the preceding financial year. It must be noted that the net profit

margin was negative in the year 2017 as well. This highlights serious concerns in the business

operations of the company. It is vital to study the factors that led to the net losses in the year

2017 2018 2019

-20%

-15%

-10%

-5%

0%

5%

10%

Net Profit Margin

Net Profit Margin

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2019, as described as follows. Not only the entity suffered operating losses due to the

charging of the impairment losses in the income statement but also the financing costs for the

year 2019 were much higher than the preceding financial years. The finance cost for the year

2019 amounted to € 2088 million (Vodafone, 2019, pp. 111). The increment in the financing

costs is attributed to the bonds and other liabilities (Vodafone, 2019, pp. 136). Thus, it can be

concluded that the inclusion of the bonds and other liabilities have not only led to the

increment in the risk in the capital structure, but also led to the greater charge in the income

statement, affecting the overall profitability. Hence, this is a negative sign for the entity from

the point of view of stakeholders.

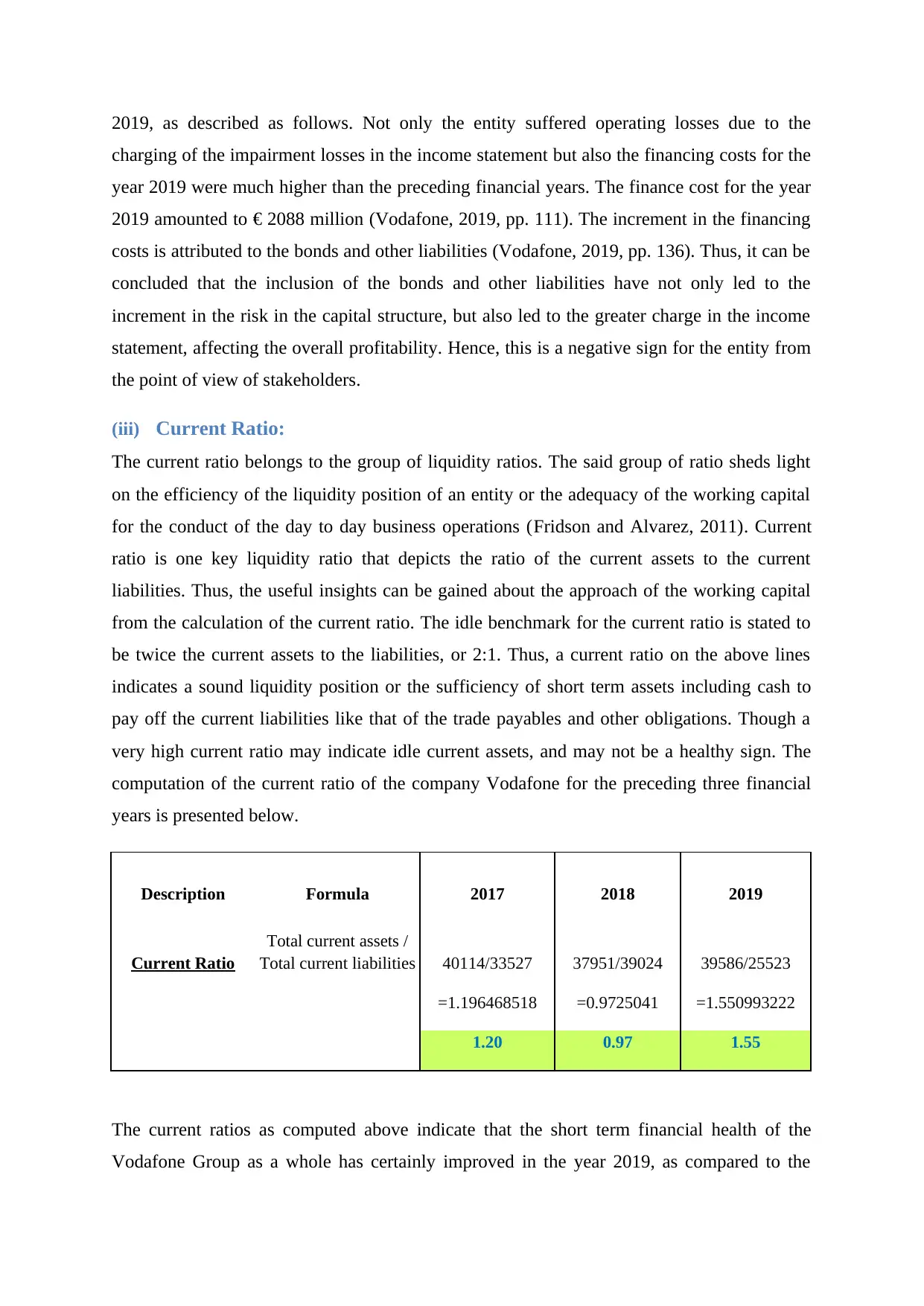

(iii) Current Ratio:

The current ratio belongs to the group of liquidity ratios. The said group of ratio sheds light

on the efficiency of the liquidity position of an entity or the adequacy of the working capital

for the conduct of the day to day business operations (Fridson and Alvarez, 2011). Current

ratio is one key liquidity ratio that depicts the ratio of the current assets to the current

liabilities. Thus, the useful insights can be gained about the approach of the working capital

from the calculation of the current ratio. The idle benchmark for the current ratio is stated to

be twice the current assets to the liabilities, or 2:1. Thus, a current ratio on the above lines

indicates a sound liquidity position or the sufficiency of short term assets including cash to

pay off the current liabilities like that of the trade payables and other obligations. Though a

very high current ratio may indicate idle current assets, and may not be a healthy sign. The

computation of the current ratio of the company Vodafone for the preceding three financial

years is presented below.

Description Formula 2017 2018 2019

Current Ratio

Total current assets /

Total current liabilities 40114/33527 37951/39024 39586/25523

=1.196468518 =0.9725041 =1.550993222

1.20 0.97 1.55

The current ratios as computed above indicate that the short term financial health of the

Vodafone Group as a whole has certainly improved in the year 2019, as compared to the

charging of the impairment losses in the income statement but also the financing costs for the

year 2019 were much higher than the preceding financial years. The finance cost for the year

2019 amounted to € 2088 million (Vodafone, 2019, pp. 111). The increment in the financing

costs is attributed to the bonds and other liabilities (Vodafone, 2019, pp. 136). Thus, it can be

concluded that the inclusion of the bonds and other liabilities have not only led to the

increment in the risk in the capital structure, but also led to the greater charge in the income

statement, affecting the overall profitability. Hence, this is a negative sign for the entity from

the point of view of stakeholders.

(iii) Current Ratio:

The current ratio belongs to the group of liquidity ratios. The said group of ratio sheds light

on the efficiency of the liquidity position of an entity or the adequacy of the working capital

for the conduct of the day to day business operations (Fridson and Alvarez, 2011). Current

ratio is one key liquidity ratio that depicts the ratio of the current assets to the current

liabilities. Thus, the useful insights can be gained about the approach of the working capital

from the calculation of the current ratio. The idle benchmark for the current ratio is stated to

be twice the current assets to the liabilities, or 2:1. Thus, a current ratio on the above lines

indicates a sound liquidity position or the sufficiency of short term assets including cash to

pay off the current liabilities like that of the trade payables and other obligations. Though a

very high current ratio may indicate idle current assets, and may not be a healthy sign. The

computation of the current ratio of the company Vodafone for the preceding three financial

years is presented below.

Description Formula 2017 2018 2019

Current Ratio

Total current assets /

Total current liabilities 40114/33527 37951/39024 39586/25523

=1.196468518 =0.9725041 =1.550993222

1.20 0.97 1.55

The current ratios as computed above indicate that the short term financial health of the

Vodafone Group as a whole has certainly improved in the year 2019, as compared to the

earlier years. The ratio of 1.55 in the year 2019 is close to the benchmark, and the same is a

positive sign. The major component that is responsible for the said increase in the current

assets is in the form of the cash and cash equivalents. The cash and cash equivalents were €

4674 million in the year 2018, the same tripled around to € 13637 million in the year 2019.

The said improvement is also attributed to the decrease in the short term borrowings of the

company from € 8513 million in the year 2018, to € 4270 million in the year 2019. However,

such an increase in the cash and cash equivalents may also be indicative of the idle funds in

the company, as the other short term assets have also increased such as that of the trade and

other receivables and other investments. Also to note, the decrease in the working capital for

the year 2018 was also due to the decrease in the cash and cash equivalents, as were needed

for the disposal of the certain units of the group, such as the one in India. Hence, it can be

seen that the company has made a conscious effort to replenish its short term assets after the

disposal business strategy. The graphical representation of the movement of the above ratio is

depicted below.

2017 2018 2019

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Current Ratio

Current Ratio

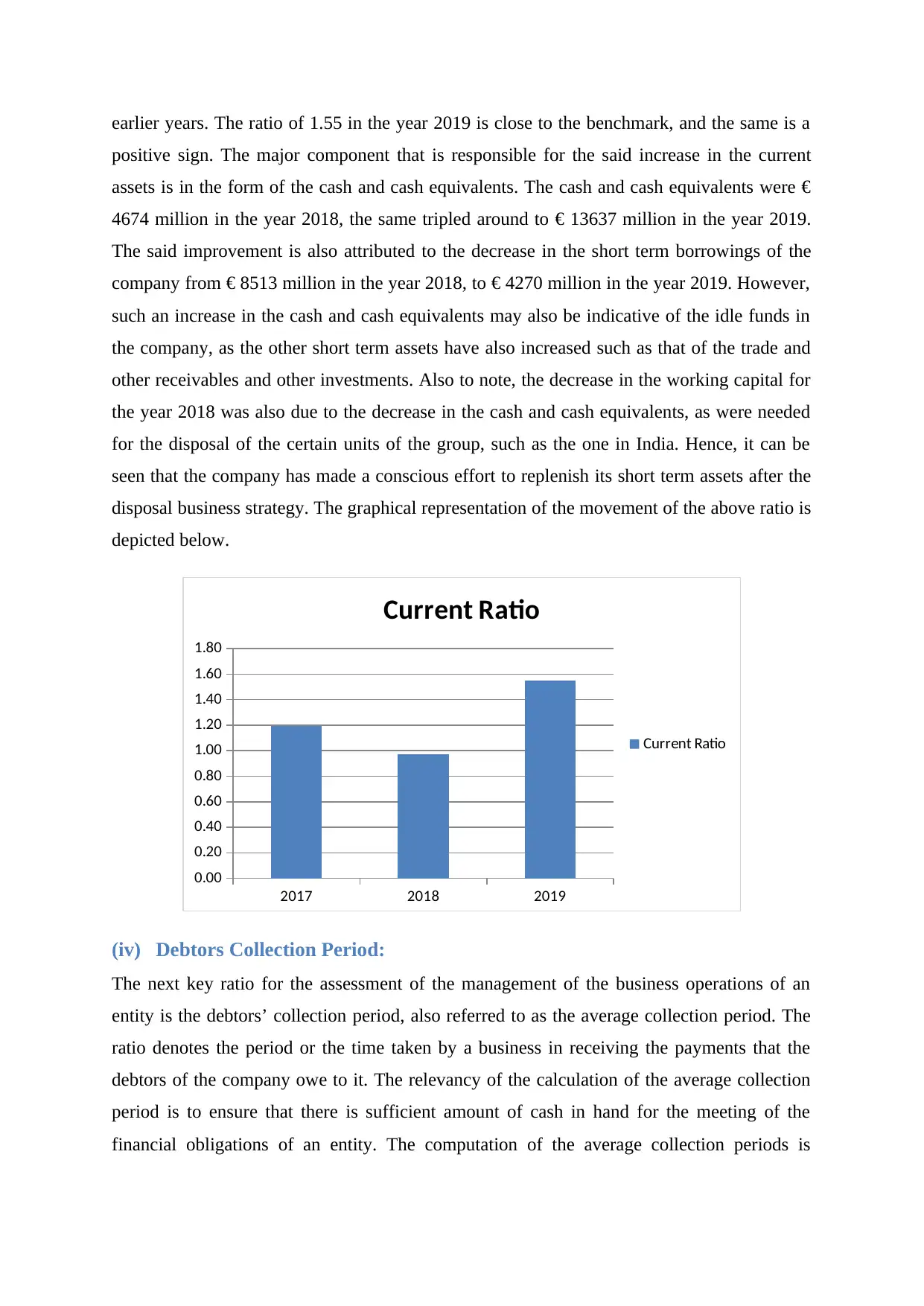

(iv) Debtors Collection Period:

The next key ratio for the assessment of the management of the business operations of an

entity is the debtors’ collection period, also referred to as the average collection period. The

ratio denotes the period or the time taken by a business in receiving the payments that the

debtors of the company owe to it. The relevancy of the calculation of the average collection

period is to ensure that there is sufficient amount of cash in hand for the meeting of the

financial obligations of an entity. The computation of the average collection periods is

positive sign. The major component that is responsible for the said increase in the current

assets is in the form of the cash and cash equivalents. The cash and cash equivalents were €

4674 million in the year 2018, the same tripled around to € 13637 million in the year 2019.

The said improvement is also attributed to the decrease in the short term borrowings of the

company from € 8513 million in the year 2018, to € 4270 million in the year 2019. However,

such an increase in the cash and cash equivalents may also be indicative of the idle funds in

the company, as the other short term assets have also increased such as that of the trade and

other receivables and other investments. Also to note, the decrease in the working capital for

the year 2018 was also due to the decrease in the cash and cash equivalents, as were needed

for the disposal of the certain units of the group, such as the one in India. Hence, it can be

seen that the company has made a conscious effort to replenish its short term assets after the

disposal business strategy. The graphical representation of the movement of the above ratio is

depicted below.

2017 2018 2019

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Current Ratio

Current Ratio

(iv) Debtors Collection Period:

The next key ratio for the assessment of the management of the business operations of an

entity is the debtors’ collection period, also referred to as the average collection period. The

ratio denotes the period or the time taken by a business in receiving the payments that the

debtors of the company owe to it. The relevancy of the calculation of the average collection

period is to ensure that there is sufficient amount of cash in hand for the meeting of the

financial obligations of an entity. The computation of the average collection periods is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

significant for the companies that rely on the debtors for the short term liquidity and the cash

flows. The formula is expressed as follows.

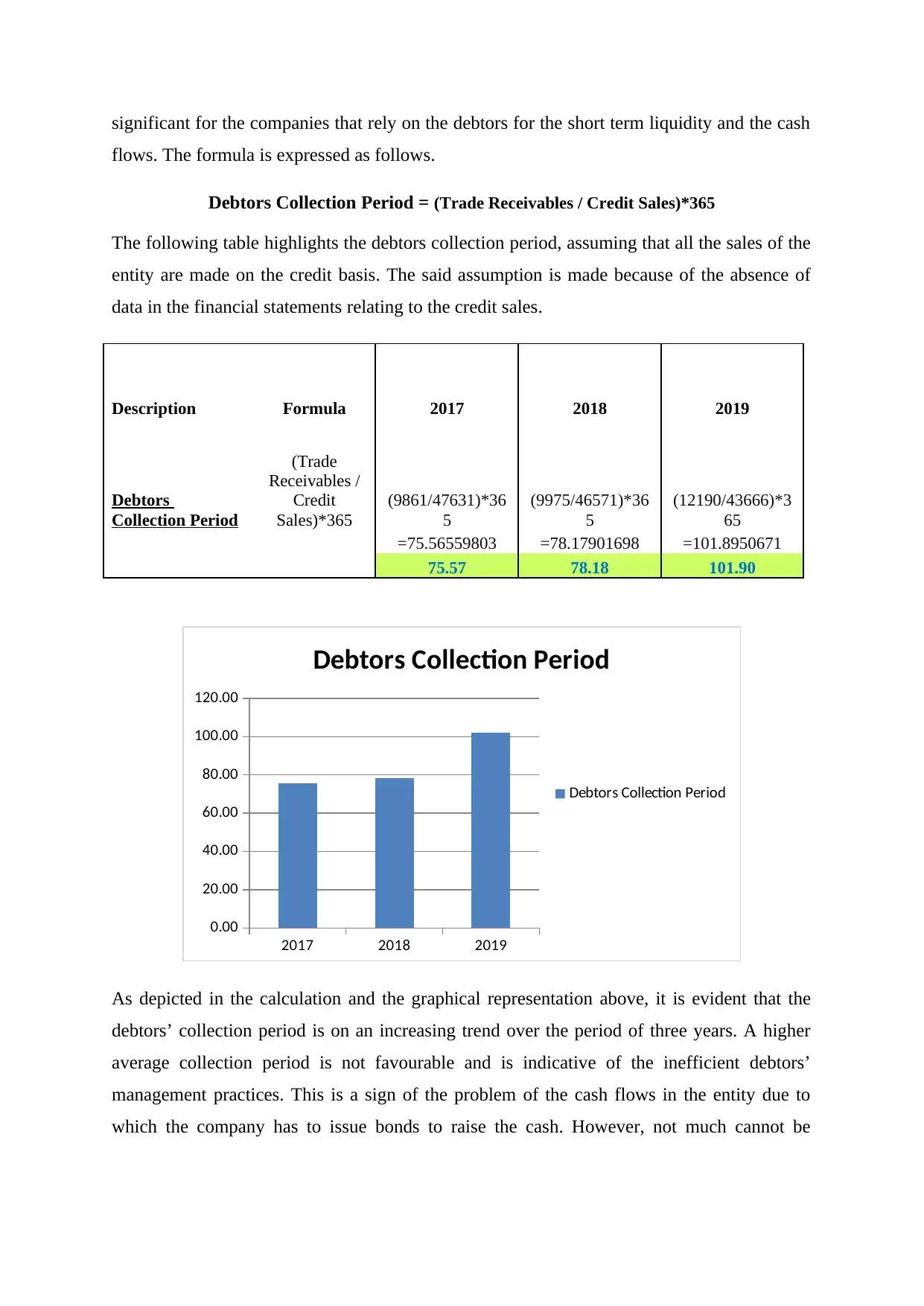

Debtors Collection Period = (Trade Receivables / Credit Sales)*365

The following table highlights the debtors collection period, assuming that all the sales of the

entity are made on the credit basis. The said assumption is made because of the absence of

data in the financial statements relating to the credit sales.

Description Formula 2017 2018 2019

Debtors

Collection Period

(Trade

Receivables /

Credit

Sales)*365

(9861/47631)*36

5

(9975/46571)*36

5

(12190/43666)*3

65

=75.56559803 =78.17901698 =101.8950671

75.57 78.18 101.90

2017 2018 2019

0.00

20.00

40.00

60.00

80.00

100.00

120.00

Debtors Collection Period

Debtors Collection Period

As depicted in the calculation and the graphical representation above, it is evident that the

debtors’ collection period is on an increasing trend over the period of three years. A higher

average collection period is not favourable and is indicative of the inefficient debtors’

management practices. This is a sign of the problem of the cash flows in the entity due to

which the company has to issue bonds to raise the cash. However, not much cannot be

flows. The formula is expressed as follows.

Debtors Collection Period = (Trade Receivables / Credit Sales)*365

The following table highlights the debtors collection period, assuming that all the sales of the

entity are made on the credit basis. The said assumption is made because of the absence of

data in the financial statements relating to the credit sales.

Description Formula 2017 2018 2019

Debtors

Collection Period

(Trade

Receivables /

Credit

Sales)*365

(9861/47631)*36

5

(9975/46571)*36

5

(12190/43666)*3

65

=75.56559803 =78.17901698 =101.8950671

75.57 78.18 101.90

2017 2018 2019

0.00

20.00

40.00

60.00

80.00

100.00

120.00

Debtors Collection Period

Debtors Collection Period

As depicted in the calculation and the graphical representation above, it is evident that the

debtors’ collection period is on an increasing trend over the period of three years. A higher

average collection period is not favourable and is indicative of the inefficient debtors’

management practices. This is a sign of the problem of the cash flows in the entity due to

which the company has to issue bonds to raise the cash. However, not much cannot be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

commented on the evaluation as conducted above, because of the absence of the exact data on

the credit sales.

C. Accounting Ratios and their significance

Thus, various accounting ratios are calculated in the previous parts to examine the various

aspects of the business. The rationale behind the calculation of the varied accounting ratios is

that the same aids in the financial analysis followed by the decision making of the different

stakeholder groups. Out of the various financial analysis tools, the ratio analysis is most

simplified and presents a trend of performance, along with the room for the comparison of the

data within industry and among different financial periods. The significance also lies in the

fact that it leads to the simplification of the large volume of financial data and aids in the

evaluation of the same (Williams and Dobelman, 2017). Various groups of ratios are

focussed on the various area of the business and highlight the financial performance of the

entity over a concerned period. The ratio analysis as conducted of the company Vodafone

highlighted the important aspects of the profitability, liquidity and the efficiency. The

comparison of the ratios over the three financial years led to the evaluation of the trends of

the performances.

D. Recommendations

The following segment is representative of the recommendations on the basis of the financial

analysis as conducted in the previous parts. The first recommendation that is extended to the

entity is to balance out the portion of the debts in the financing structure, as the servicing cost

of the same in the form of the interests is leading to the significant decline in the operating

and the overall profits of the entity. In addition, it has been suggested to balance the short

term assets of the company Vodafone. This is because there is fluctuating trends in the cash

flows of the company, and if the same would continue, the management would find it

difficult to address the short term obligations efficiently. Further, it has been suggested to the

organisations to manage the administrative expenses of the company, to reduce the pressure

on the earnings of the company, and maintain the levels of the profits.

E. Conclusion

The above report was an attempt to highlight the impact of the varied economic factors on the

financial performance of an entity. The financial analysis was conducted as aided by the

accounting ratios led to the observation that the financial performance of the entity Vodafone

the credit sales.

C. Accounting Ratios and their significance

Thus, various accounting ratios are calculated in the previous parts to examine the various

aspects of the business. The rationale behind the calculation of the varied accounting ratios is

that the same aids in the financial analysis followed by the decision making of the different

stakeholder groups. Out of the various financial analysis tools, the ratio analysis is most

simplified and presents a trend of performance, along with the room for the comparison of the

data within industry and among different financial periods. The significance also lies in the

fact that it leads to the simplification of the large volume of financial data and aids in the

evaluation of the same (Williams and Dobelman, 2017). Various groups of ratios are

focussed on the various area of the business and highlight the financial performance of the

entity over a concerned period. The ratio analysis as conducted of the company Vodafone

highlighted the important aspects of the profitability, liquidity and the efficiency. The

comparison of the ratios over the three financial years led to the evaluation of the trends of

the performances.

D. Recommendations

The following segment is representative of the recommendations on the basis of the financial

analysis as conducted in the previous parts. The first recommendation that is extended to the

entity is to balance out the portion of the debts in the financing structure, as the servicing cost

of the same in the form of the interests is leading to the significant decline in the operating

and the overall profits of the entity. In addition, it has been suggested to balance the short

term assets of the company Vodafone. This is because there is fluctuating trends in the cash

flows of the company, and if the same would continue, the management would find it

difficult to address the short term obligations efficiently. Further, it has been suggested to the

organisations to manage the administrative expenses of the company, to reduce the pressure

on the earnings of the company, and maintain the levels of the profits.

E. Conclusion

The above report was an attempt to highlight the impact of the varied economic factors on the

financial performance of an entity. The financial analysis was conducted as aided by the

accounting ratios led to the observation that the financial performance of the entity Vodafone

fluctuates considerably over the period of the three financial years, as were chosen for the

report. The varied business areas like liquidity, efficiency and profitability were examined

with the help of key ratios. In addition, the recommendations are provided based on the above

mentioned performance indicators.

References

Delen, D., Kuzey, C., and Uyar, A. (2013) Measuring firm performance using financial

ratios: A decision tree approach. Expert Systems with Applications, 40(10), pp. 3970-3983.

Edmonds, T. P. (2013) Fundamental financial accounting concepts. UK: McGraw-Hill.

Fridson, M. S., and Alvarez, F. (2011) Financial statement analysis: a practitioner's guide

Vol. 597. UK: John Wiley & Sons.

Robinson, T. R., Henry, E., Pirie, W. L., and Broihahn, M. A. (2015) International financial

statement analysis. UK: John Wiley & Sons.

Vodafone Group Plc. (2019) Vodafone Group Plc. Annual Report 2019 [online] Available

from: https://www.vodafone.com/investors/investor-information/annual-report/downloads/Vodafone-

full-annual-report-2019.pdf [Accessed on: 20 February 2020].

Williams, E. E., and Dobelman, J. A. (2017) Financial statement analysis. World Scientific

Book Chapters, pp. 109-169.

report. The varied business areas like liquidity, efficiency and profitability were examined

with the help of key ratios. In addition, the recommendations are provided based on the above

mentioned performance indicators.

References

Delen, D., Kuzey, C., and Uyar, A. (2013) Measuring firm performance using financial

ratios: A decision tree approach. Expert Systems with Applications, 40(10), pp. 3970-3983.

Edmonds, T. P. (2013) Fundamental financial accounting concepts. UK: McGraw-Hill.

Fridson, M. S., and Alvarez, F. (2011) Financial statement analysis: a practitioner's guide

Vol. 597. UK: John Wiley & Sons.

Robinson, T. R., Henry, E., Pirie, W. L., and Broihahn, M. A. (2015) International financial

statement analysis. UK: John Wiley & Sons.

Vodafone Group Plc. (2019) Vodafone Group Plc. Annual Report 2019 [online] Available

from: https://www.vodafone.com/investors/investor-information/annual-report/downloads/Vodafone-

full-annual-report-2019.pdf [Accessed on: 20 February 2020].

Williams, E. E., and Dobelman, J. A. (2017) Financial statement analysis. World Scientific

Book Chapters, pp. 109-169.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.