BUS102 Microeconomics Assignment: Production, Tax, and Market Impact

VerifiedAdded on 2023/06/12

|11

|1232

|341

Homework Assignment

AI Summary

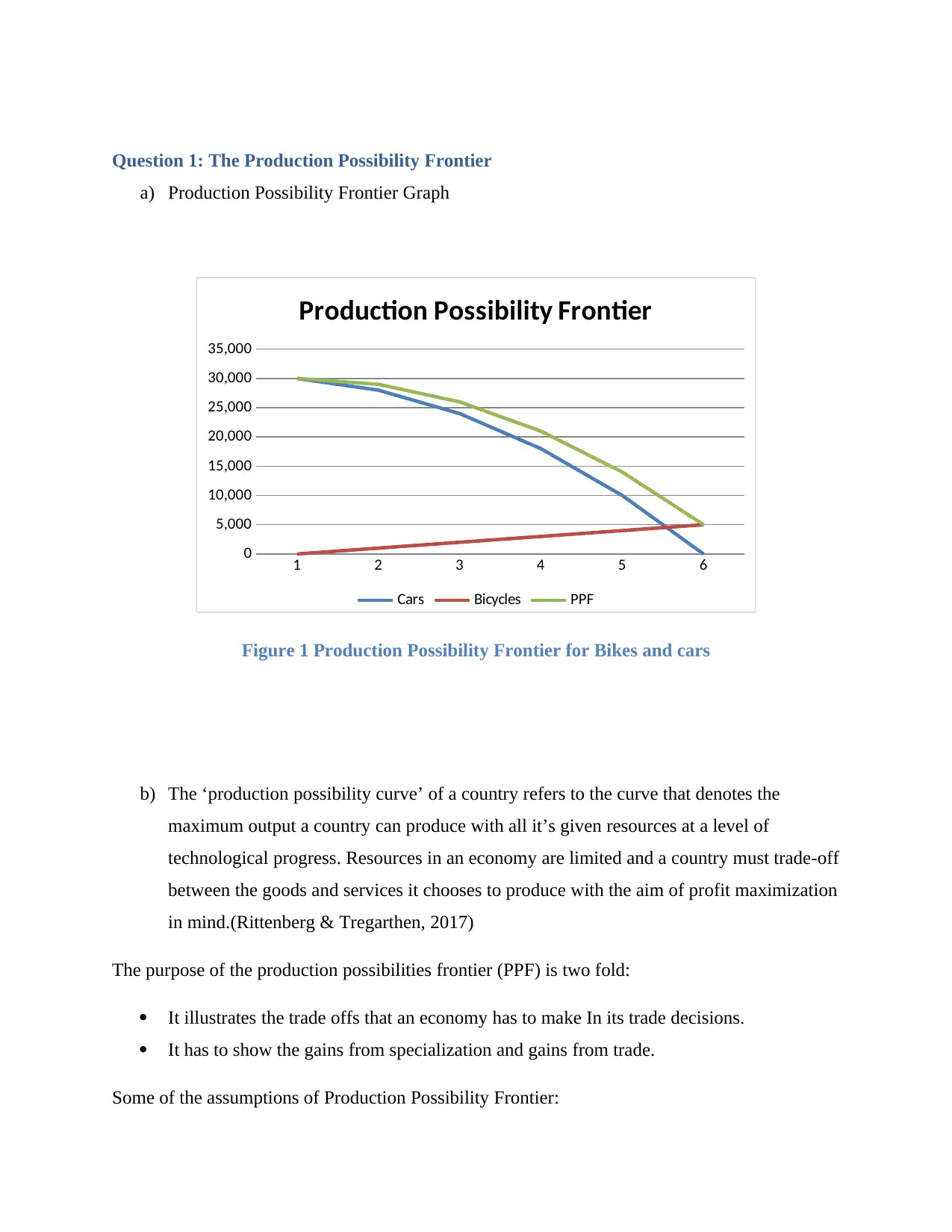

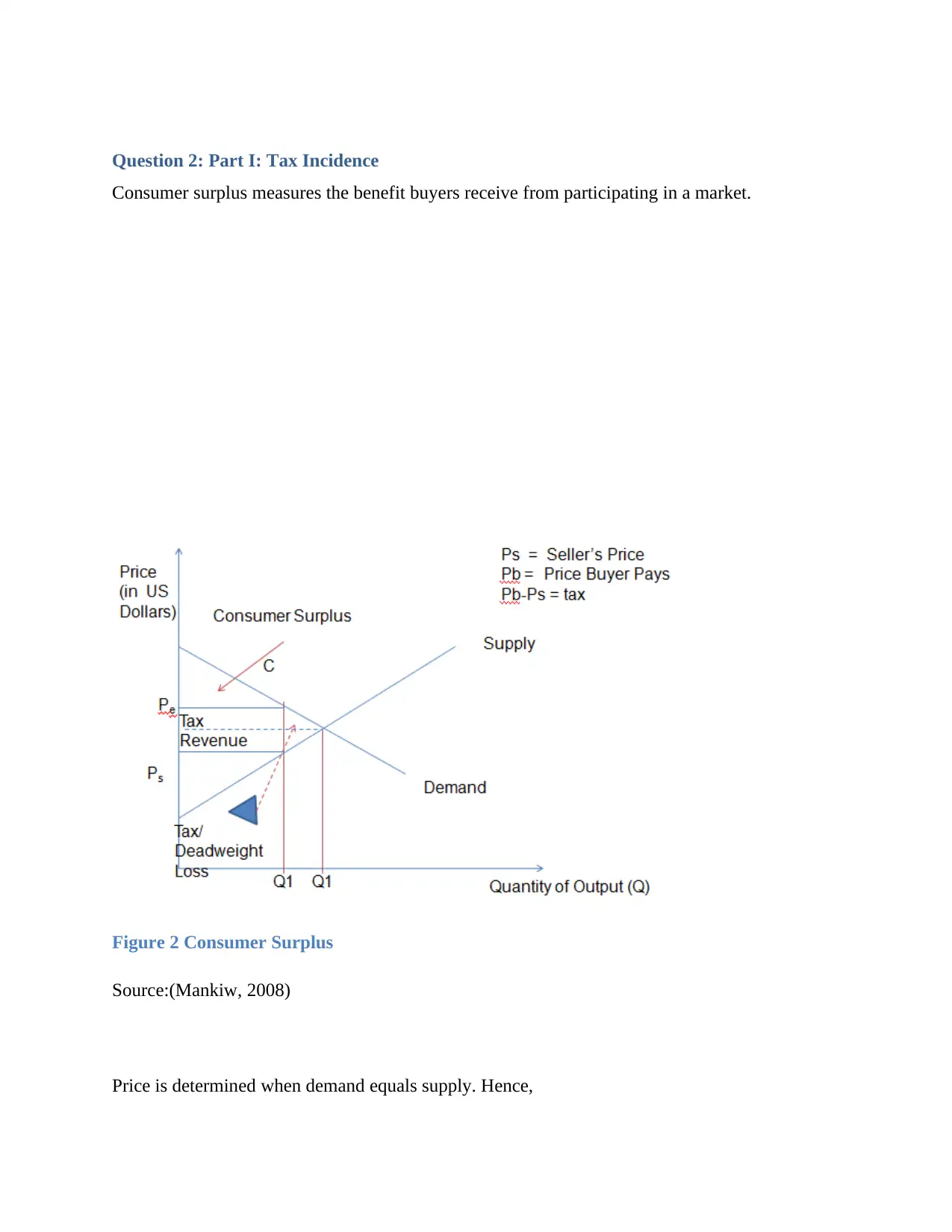

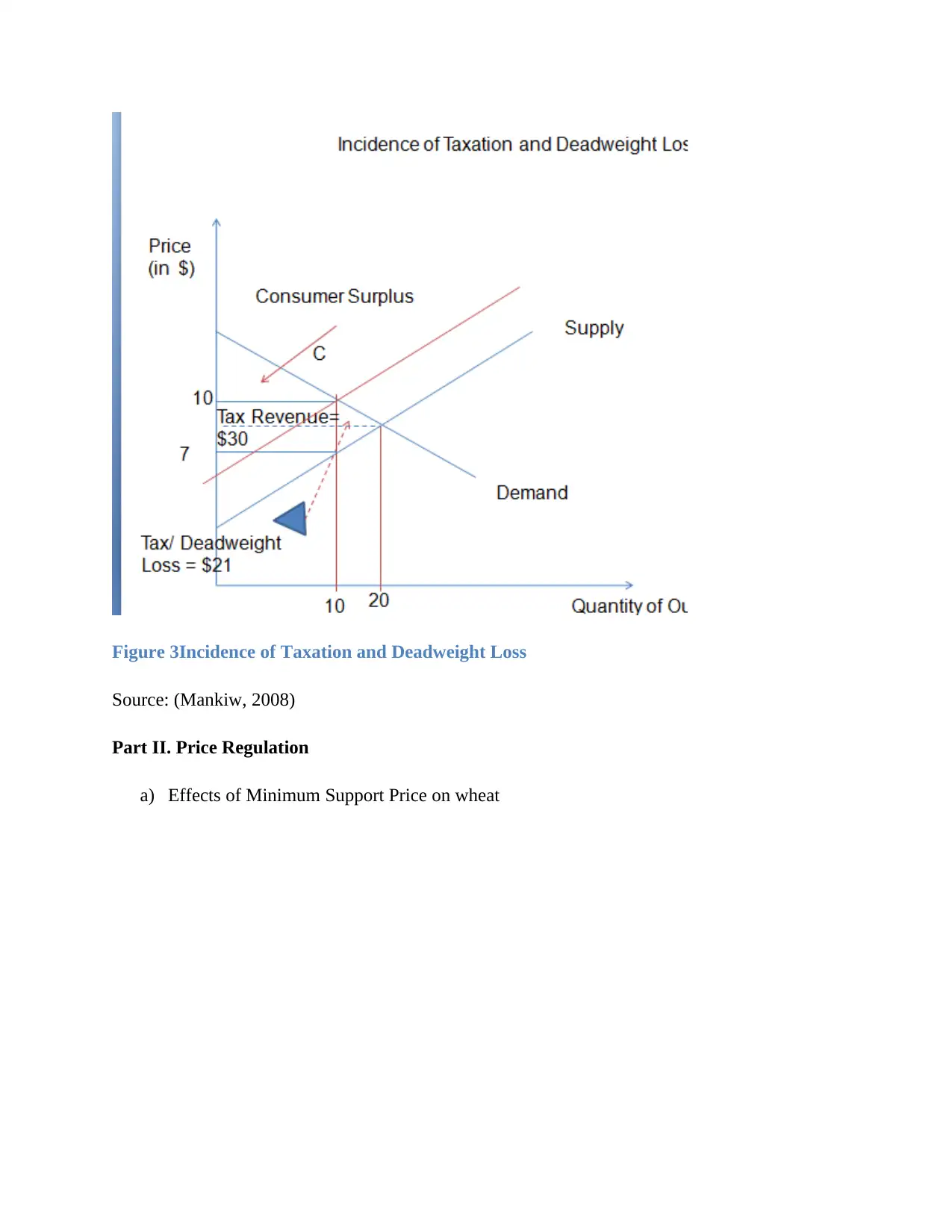

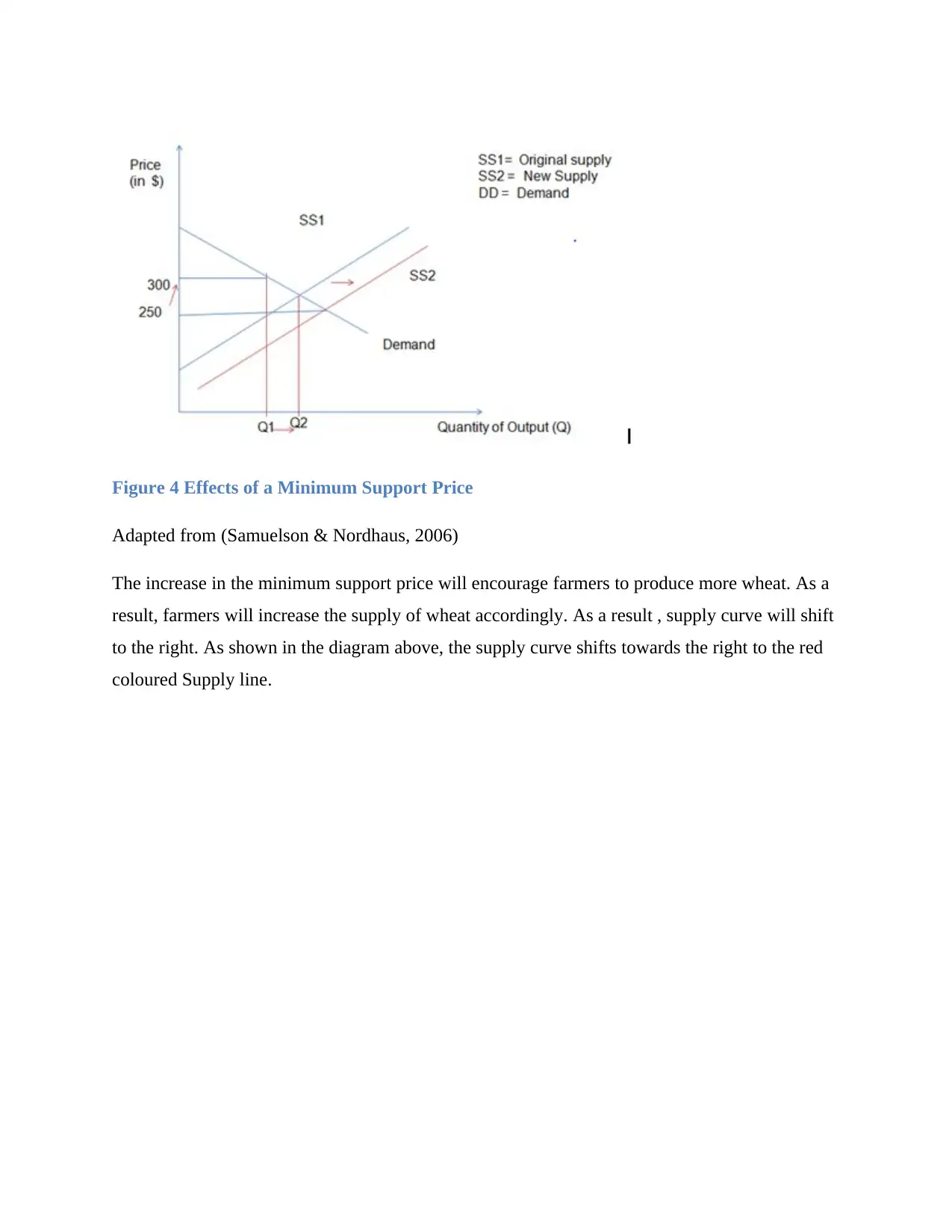

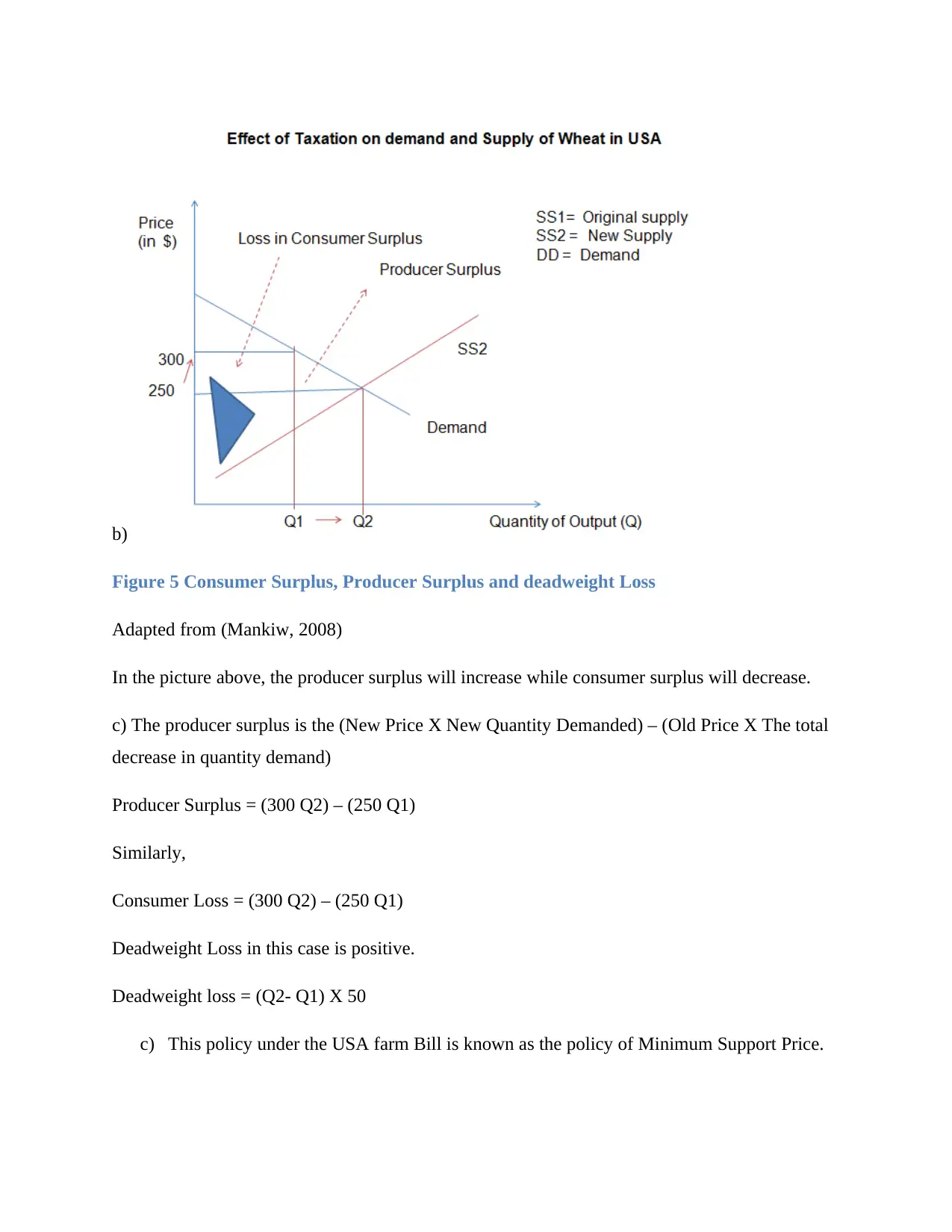

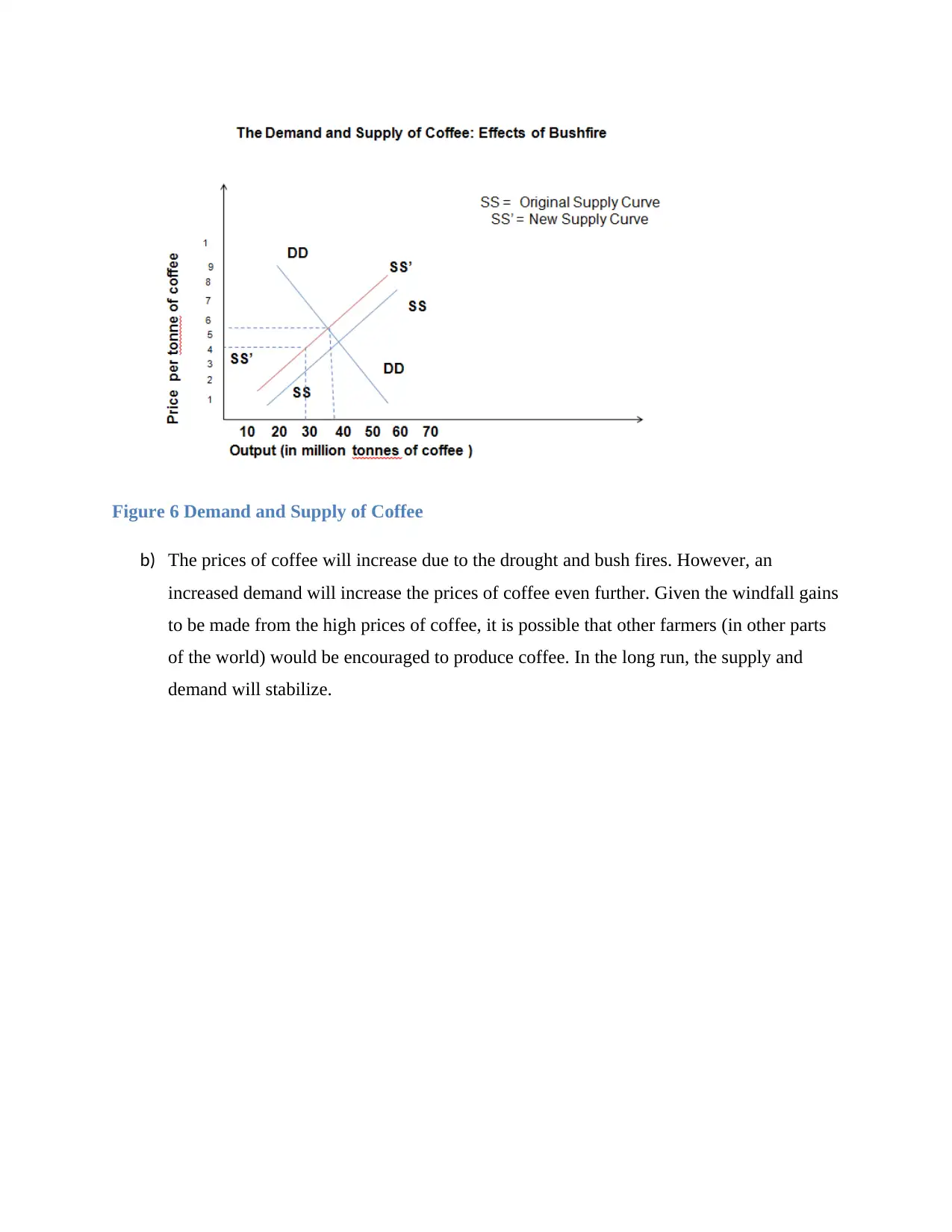

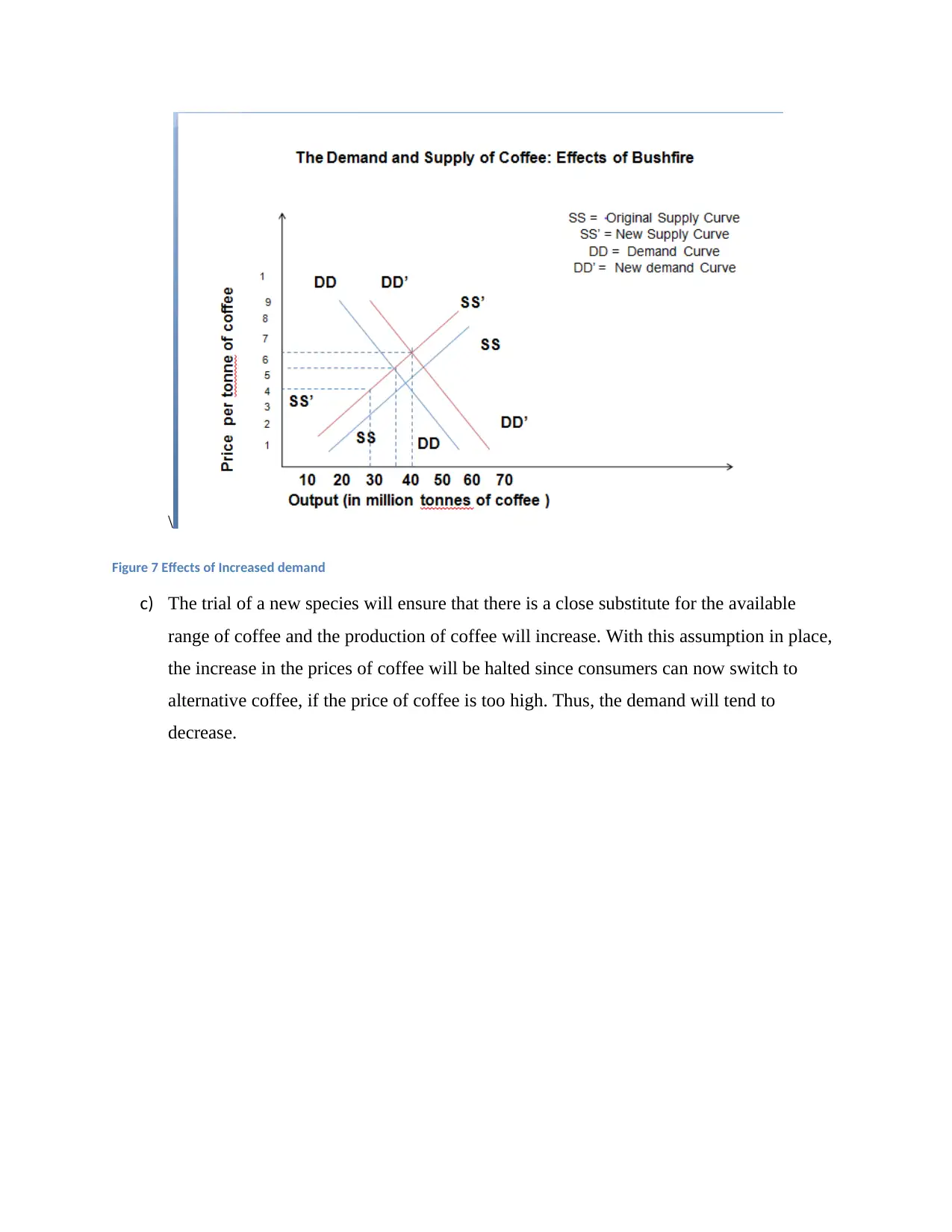

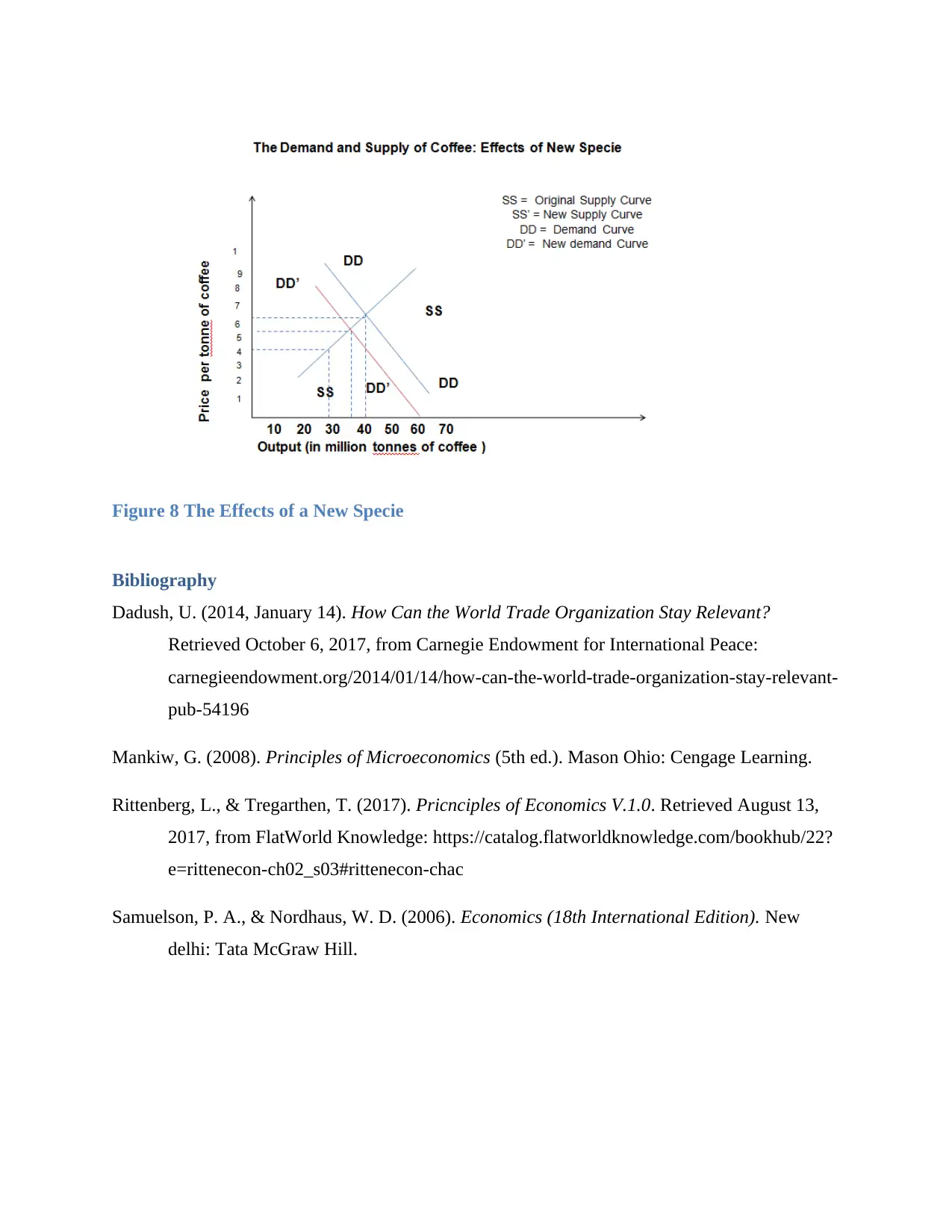

This microeconomics assignment delves into several key concepts. It begins with an analysis of the Production Possibility Frontier (PPF), illustrating trade-offs and specialization gains, followed by an examination of tax incidence, consumer surplus, and deadweight loss resulting from taxation. The assignment further investigates the effects of minimum support prices on wheat markets, assessing impacts on producer and consumer surpluses, international trade, and ethical considerations. Finally, it analyzes the impact of natural disasters, such as bush fires and droughts, on coffee supply and prices, considering both short-term and long-term effects, including potential shifts in demand and the introduction of new coffee species. This assignment showcases a comprehensive understanding of microeconomic principles and their practical applications. Desklib provides similar past papers and solved assignments for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.