Economics Assignment: Macroeconomics, Semester 2, University

VerifiedAdded on 2021/06/18

|14

|3088

|71

Homework Assignment

AI Summary

This economics assignment delves into various macroeconomic concepts. It begins by analyzing the Federal Reserve's balance sheet and the impact of open market operations. The assignment then explores the currency-deposit ratio and money supply during the Great Depression. Further, it examines nominal and real exchange rates, interest rate parity, and exchange rate interventions. The document also discusses purchasing power parity, current accounts, and the J-curve. The assignment analyzes Nash equilibrium in the context of financial institutions and the Fed, and the Channel-Corridor approach to monetary policy. Finally, it covers fixed exchange rates, unconventional monetary policies, and their effects on the economy, including aggregate demand, investment, and savings. The assignment provides a comprehensive overview of key macroeconomic principles and their practical applications.

Running head: ECONOMICS ASSIGNMENT

Economics Assignment

Name of the student

Name of the university

Author Note

Economics Assignment

Name of the student

Name of the university

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS ASSIGNMENT

Table of Contents

Answer 1:...................................................................................................................................2

Answer 2:...................................................................................................................................3

Answer 3:...................................................................................................................................4

Answer 4:...................................................................................................................................5

Answer 5:...................................................................................................................................6

Answer 6:...................................................................................................................................7

Answer 7:...................................................................................................................................7

Answer 8:...................................................................................................................................8

Answer 9:...................................................................................................................................9

References:...............................................................................................................................11

Table of Contents

Answer 1:...................................................................................................................................2

Answer 2:...................................................................................................................................3

Answer 3:...................................................................................................................................4

Answer 4:...................................................................................................................................5

Answer 5:...................................................................................................................................6

Answer 6:...................................................................................................................................7

Answer 7:...................................................................................................................................7

Answer 8:...................................................................................................................................8

Answer 9:...................................................................................................................................9

References:...............................................................................................................................11

2ECONOMICS ASSIGNMENT

RD

RS

Reserves

0

Iff

If1

If*

NBR1 NBR*

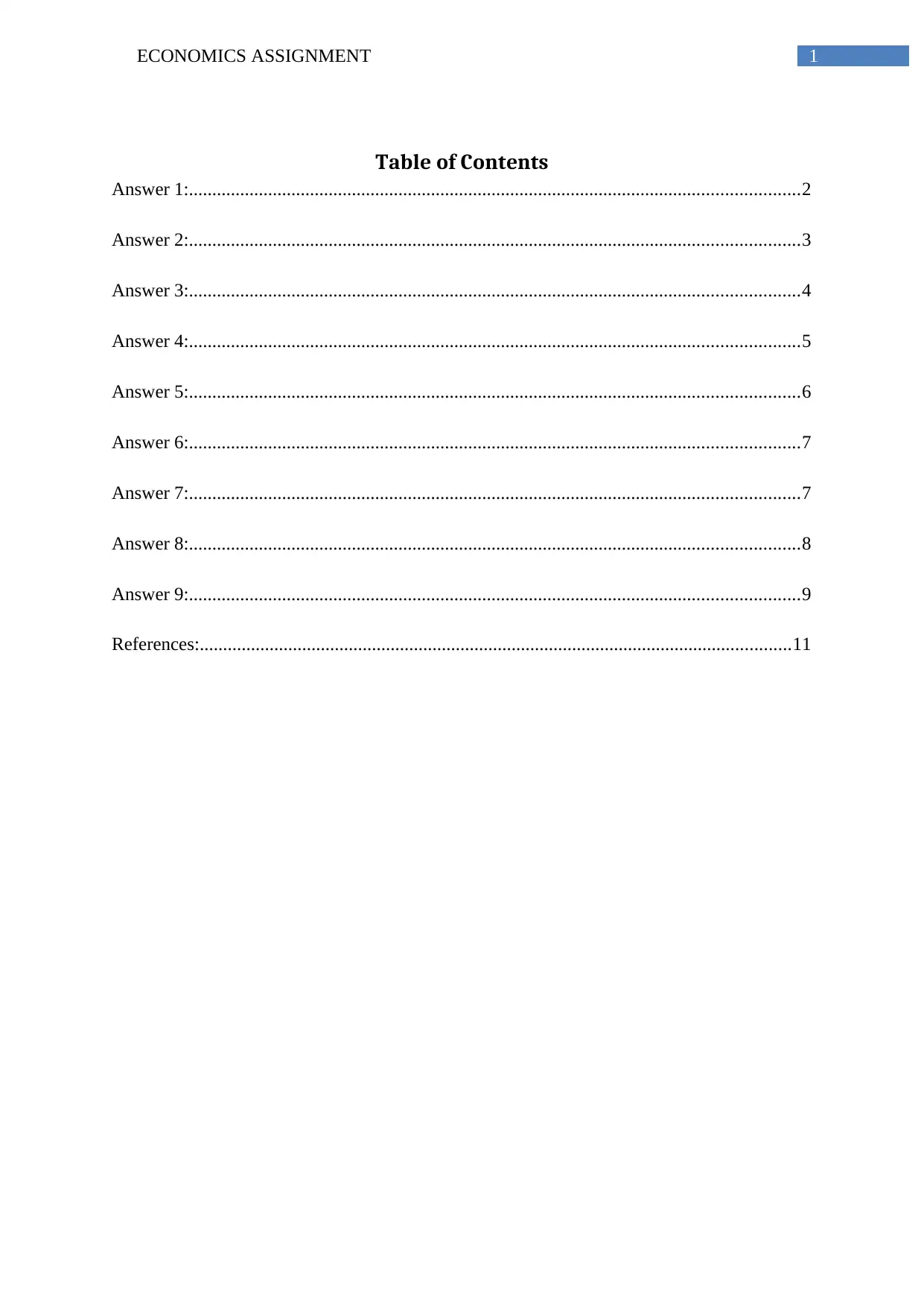

Answer 1:

The balance sheet of the Fed’s reserve system has both assets and liabilities while

asset considers securities and loans to financial institutions and liabilities include currency in

circulation and reserves. On the other side, open market sale occurs when the Federal Reserve

sells government securities to decrease reserves or currency (Ihrig, Meade & Weinbach,

2015). As it helps the government to decrease the monetary base, it is contractionary by

nature and it decreases the liability of the bank. Moreover, reverse repurchase agreement

occurs liability side of the bank. Hence, this creates bank liabilities.

Non-borrowed reserves represent the difference between total reserves and borrowed

reserves, which is the sum of credit. This credit is extended through the regular discount

window program of the Federal Reserve along with credit extended with the help of certain

liquidity facilities of the Federal Reserve (Ahelegbey, Billio & Casarin, 2016). Open market

operation helps to change the quantity of non-borrowed reserves through decreasing the

supply of reserves by selling in open market.

Figure 1: Open market sales

RD

RS

Reserves

0

Iff

If1

If*

NBR1 NBR*

Answer 1:

The balance sheet of the Fed’s reserve system has both assets and liabilities while

asset considers securities and loans to financial institutions and liabilities include currency in

circulation and reserves. On the other side, open market sale occurs when the Federal Reserve

sells government securities to decrease reserves or currency (Ihrig, Meade & Weinbach,

2015). As it helps the government to decrease the monetary base, it is contractionary by

nature and it decreases the liability of the bank. Moreover, reverse repurchase agreement

occurs liability side of the bank. Hence, this creates bank liabilities.

Non-borrowed reserves represent the difference between total reserves and borrowed

reserves, which is the sum of credit. This credit is extended through the regular discount

window program of the Federal Reserve along with credit extended with the help of certain

liquidity facilities of the Federal Reserve (Ahelegbey, Billio & Casarin, 2016). Open market

operation helps to change the quantity of non-borrowed reserves through decreasing the

supply of reserves by selling in open market.

Figure 1: Open market sales

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS ASSIGNMENT

Source: (created by author)

According to figure 1, an open market sale reduces the reserve supply, that is R1 from

R* and consequently increases the federal funds rate from If* to If1. Thus, non-borrowing

reserve decreases open market selling.

Answer 2:

Excess reserve (er) ratio is the ratio between excess reserve (ER) to demand deposits

(D), that is, er = ER/ D. Moreover, the currency-deposit ratio (c) represents the ratio between

currency (C) with demand deposits (D), that is, c= C/D.

During Great Depression, money supply decreased significantly and this in turn led

the economy into depression. Consequently, deposits in bank decreased and the amount of

currency in hand increased (Blanchard & Summers, 2017). Moreover, most of the

commercial banks kept excess reserves enable. This implied ER and C increased compare to

demand deposits. Those phenomenons had led the excess reserve ratio and currency-deposit

ratio to increase further.

Money supply has negative relation with currency holdings and the amount of excess

reserves of banks. Hence, during depression, money supply decreased as C and ER increased.

During this season, money base increased while money multiplier fell due to increase in

excess-reserve ratio (er) and currency-deposit (c) ratio (Goodhart, Bartsch & Ashworth,

2016). Monetary base (MB) is the sum total of checkable deposits (D), excess reserve (ER)

and currency (C) this value increases positive, that is, MB= C+D+ER. On the other side, the

equation of money multiplier (m) is :

m= (1+c)/ (rr+er+c).

Hence, er and c have opposite relation with money supply.

Source: (created by author)

According to figure 1, an open market sale reduces the reserve supply, that is R1 from

R* and consequently increases the federal funds rate from If* to If1. Thus, non-borrowing

reserve decreases open market selling.

Answer 2:

Excess reserve (er) ratio is the ratio between excess reserve (ER) to demand deposits

(D), that is, er = ER/ D. Moreover, the currency-deposit ratio (c) represents the ratio between

currency (C) with demand deposits (D), that is, c= C/D.

During Great Depression, money supply decreased significantly and this in turn led

the economy into depression. Consequently, deposits in bank decreased and the amount of

currency in hand increased (Blanchard & Summers, 2017). Moreover, most of the

commercial banks kept excess reserves enable. This implied ER and C increased compare to

demand deposits. Those phenomenons had led the excess reserve ratio and currency-deposit

ratio to increase further.

Money supply has negative relation with currency holdings and the amount of excess

reserves of banks. Hence, during depression, money supply decreased as C and ER increased.

During this season, money base increased while money multiplier fell due to increase in

excess-reserve ratio (er) and currency-deposit (c) ratio (Goodhart, Bartsch & Ashworth,

2016). Monetary base (MB) is the sum total of checkable deposits (D), excess reserve (ER)

and currency (C) this value increases positive, that is, MB= C+D+ER. On the other side, the

equation of money multiplier (m) is :

m= (1+c)/ (rr+er+c).

Hence, er and c have opposite relation with money supply.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS ASSIGNMENT

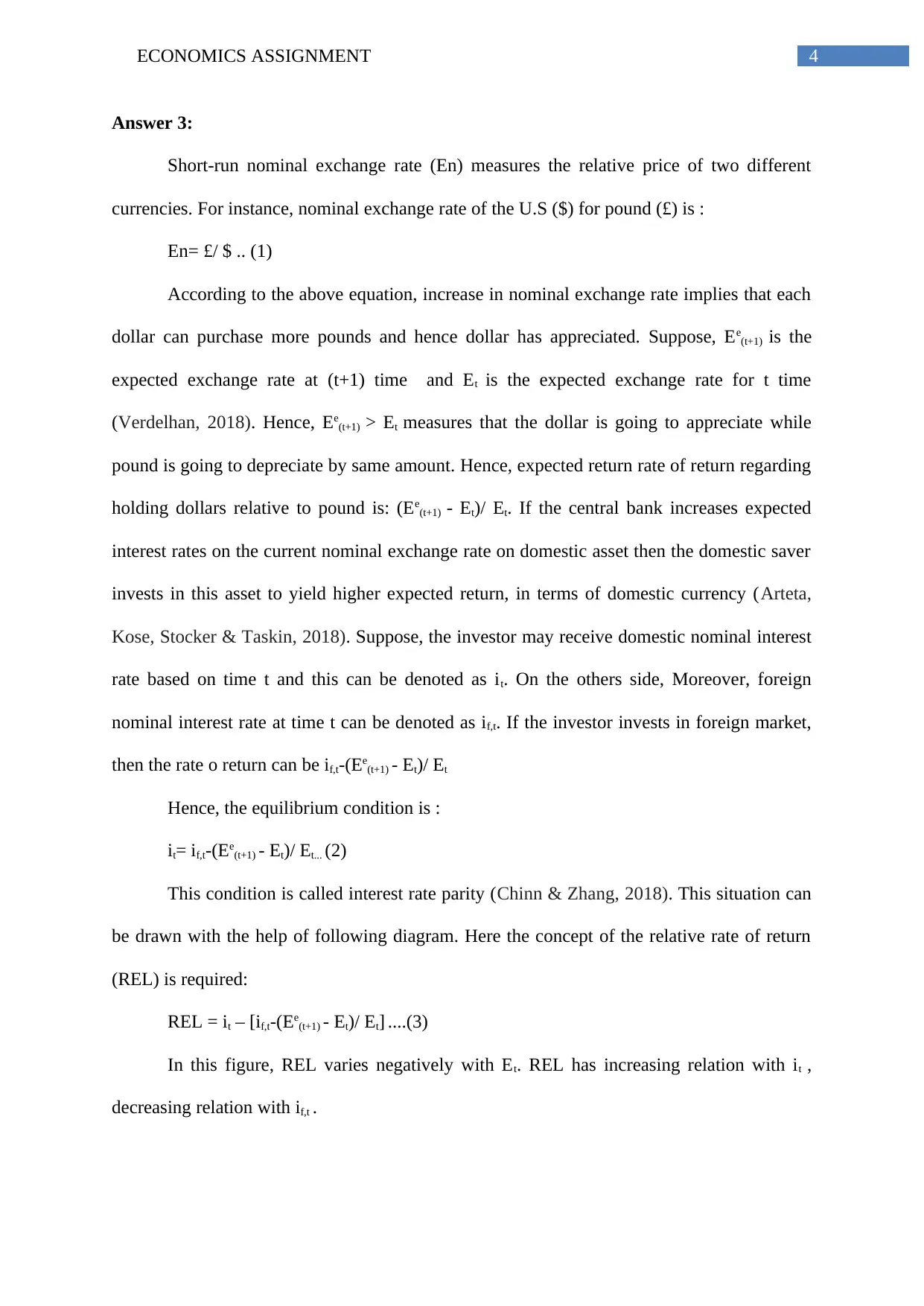

Answer 3:

Short-run nominal exchange rate (En) measures the relative price of two different

currencies. For instance, nominal exchange rate of the U.S ($) for pound (£) is :

En= £/ $ .. (1)

According to the above equation, increase in nominal exchange rate implies that each

dollar can purchase more pounds and hence dollar has appreciated. Suppose, Ee(t+1) is the

expected exchange rate at (t+1) time and Et is the expected exchange rate for t time

(Verdelhan, 2018). Hence, Ee(t+1) > Et measures that the dollar is going to appreciate while

pound is going to depreciate by same amount. Hence, expected return rate of return regarding

holding dollars relative to pound is: (Ee(t+1) - Et)/ Et. If the central bank increases expected

interest rates on the current nominal exchange rate on domestic asset then the domestic saver

invests in this asset to yield higher expected return, in terms of domestic currency (Arteta,

Kose, Stocker & Taskin, 2018). Suppose, the investor may receive domestic nominal interest

rate based on time t and this can be denoted as it. On the others side, Moreover, foreign

nominal interest rate at time t can be denoted as if,t. If the investor invests in foreign market,

then the rate o return can be if,t-(Ee(t+1) - Et)/ Et

Hence, the equilibrium condition is :

it= if,t-(Ee(t+1) - Et)/ Et... (2)

This condition is called interest rate parity (Chinn & Zhang, 2018). This situation can

be drawn with the help of following diagram. Here the concept of the relative rate of return

(REL) is required:

REL = it – [if,t-(Ee(t+1) - Et)/ Et] ....(3)

In this figure, REL varies negatively with Et. REL has increasing relation with it ,

decreasing relation with if,t .

Answer 3:

Short-run nominal exchange rate (En) measures the relative price of two different

currencies. For instance, nominal exchange rate of the U.S ($) for pound (£) is :

En= £/ $ .. (1)

According to the above equation, increase in nominal exchange rate implies that each

dollar can purchase more pounds and hence dollar has appreciated. Suppose, Ee(t+1) is the

expected exchange rate at (t+1) time and Et is the expected exchange rate for t time

(Verdelhan, 2018). Hence, Ee(t+1) > Et measures that the dollar is going to appreciate while

pound is going to depreciate by same amount. Hence, expected return rate of return regarding

holding dollars relative to pound is: (Ee(t+1) - Et)/ Et. If the central bank increases expected

interest rates on the current nominal exchange rate on domestic asset then the domestic saver

invests in this asset to yield higher expected return, in terms of domestic currency (Arteta,

Kose, Stocker & Taskin, 2018). Suppose, the investor may receive domestic nominal interest

rate based on time t and this can be denoted as it. On the others side, Moreover, foreign

nominal interest rate at time t can be denoted as if,t. If the investor invests in foreign market,

then the rate o return can be if,t-(Ee(t+1) - Et)/ Et

Hence, the equilibrium condition is :

it= if,t-(Ee(t+1) - Et)/ Et... (2)

This condition is called interest rate parity (Chinn & Zhang, 2018). This situation can

be drawn with the help of following diagram. Here the concept of the relative rate of return

(REL) is required:

REL = it – [if,t-(Ee(t+1) - Et)/ Et] ....(3)

In this figure, REL varies negatively with Et. REL has increasing relation with it ,

decreasing relation with if,t .

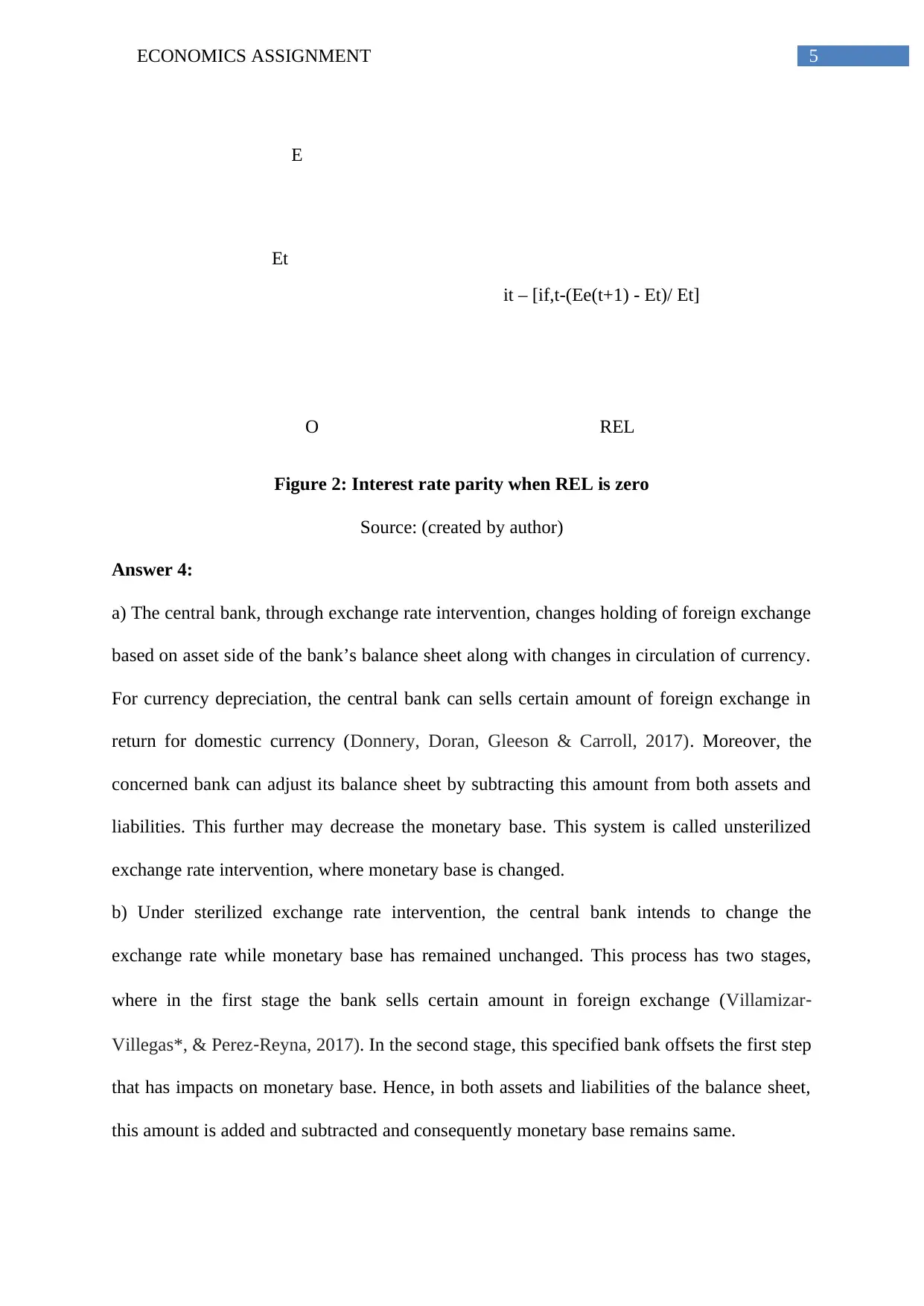

5ECONOMICS ASSIGNMENT

E

Et

O REL

it – [if,t-(Ee(t+1) - Et)/ Et]

Figure 2: Interest rate parity when REL is zero

Source: (created by author)

Answer 4:

a) The central bank, through exchange rate intervention, changes holding of foreign exchange

based on asset side of the bank’s balance sheet along with changes in circulation of currency.

For currency depreciation, the central bank can sells certain amount of foreign exchange in

return for domestic currency (Donnery, Doran, Gleeson & Carroll, 2017). Moreover, the

concerned bank can adjust its balance sheet by subtracting this amount from both assets and

liabilities. This further may decrease the monetary base. This system is called unsterilized

exchange rate intervention, where monetary base is changed.

b) Under sterilized exchange rate intervention, the central bank intends to change the

exchange rate while monetary base has remained unchanged. This process has two stages,

where in the first stage the bank sells certain amount in foreign exchange (Villamizar‐

Villegas*, & Perez‐Reyna, 2017). In the second stage, this specified bank offsets the first step

that has impacts on monetary base. Hence, in both assets and liabilities of the balance sheet,

this amount is added and subtracted and consequently monetary base remains same.

E

Et

O REL

it – [if,t-(Ee(t+1) - Et)/ Et]

Figure 2: Interest rate parity when REL is zero

Source: (created by author)

Answer 4:

a) The central bank, through exchange rate intervention, changes holding of foreign exchange

based on asset side of the bank’s balance sheet along with changes in circulation of currency.

For currency depreciation, the central bank can sells certain amount of foreign exchange in

return for domestic currency (Donnery, Doran, Gleeson & Carroll, 2017). Moreover, the

concerned bank can adjust its balance sheet by subtracting this amount from both assets and

liabilities. This further may decrease the monetary base. This system is called unsterilized

exchange rate intervention, where monetary base is changed.

b) Under sterilized exchange rate intervention, the central bank intends to change the

exchange rate while monetary base has remained unchanged. This process has two stages,

where in the first stage the bank sells certain amount in foreign exchange (Villamizar‐

Villegas*, & Perez‐Reyna, 2017). In the second stage, this specified bank offsets the first step

that has impacts on monetary base. Hence, in both assets and liabilities of the balance sheet,

this amount is added and subtracted and consequently monetary base remains same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS ASSIGNMENT

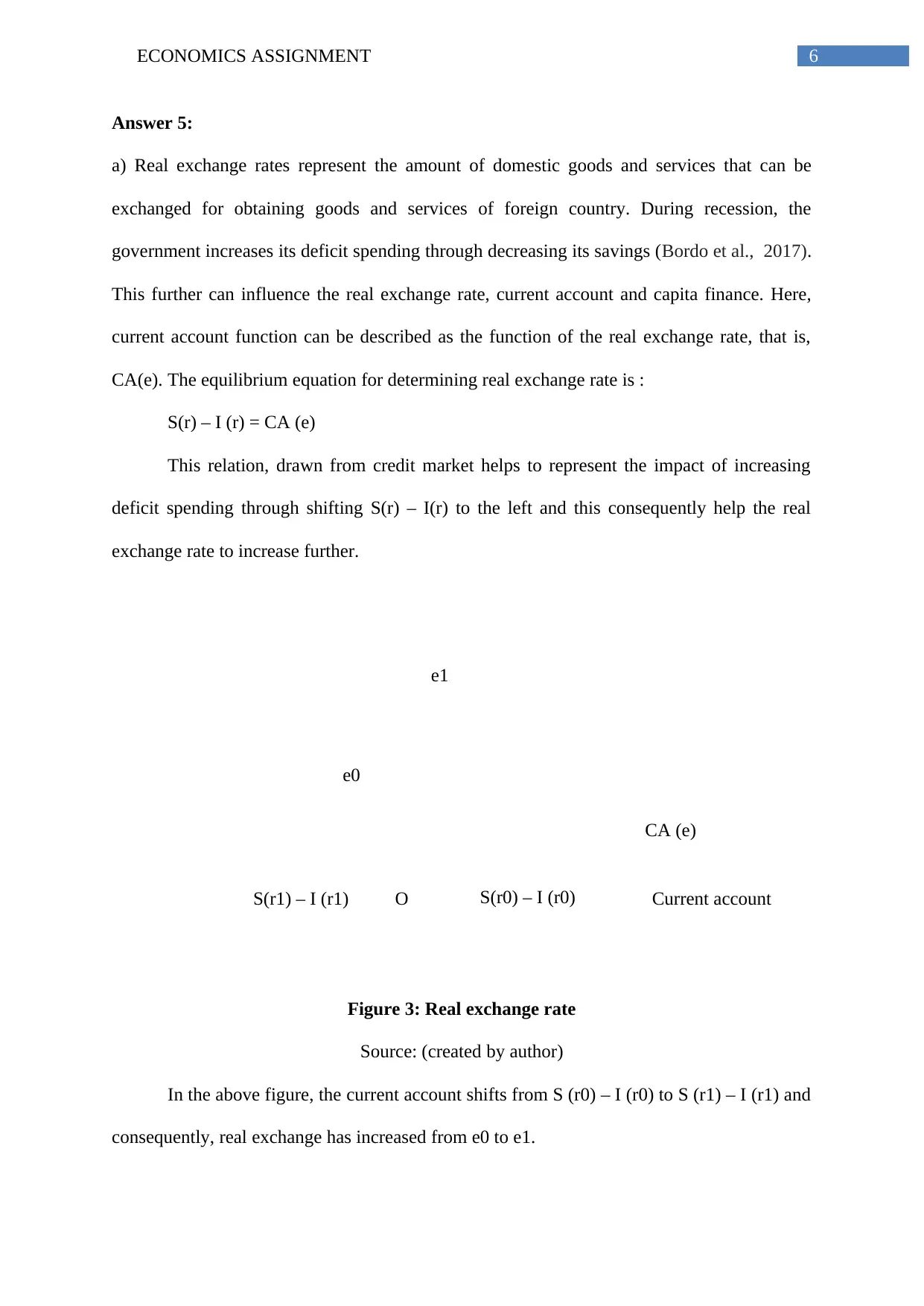

CA (e)

S(r1) – I (r1) O S(r0) – I (r0) Current account

e1

e0

Answer 5:

a) Real exchange rates represent the amount of domestic goods and services that can be

exchanged for obtaining goods and services of foreign country. During recession, the

government increases its deficit spending through decreasing its savings (Bordo et al., 2017).

This further can influence the real exchange rate, current account and capita finance. Here,

current account function can be described as the function of the real exchange rate, that is,

CA(e). The equilibrium equation for determining real exchange rate is :

S(r) – I (r) = CA (e)

This relation, drawn from credit market helps to represent the impact of increasing

deficit spending through shifting S(r) – I(r) to the left and this consequently help the real

exchange rate to increase further.

Figure 3: Real exchange rate

Source: (created by author)

In the above figure, the current account shifts from S (r0) – I (r0) to S (r1) – I (r1) and

consequently, real exchange has increased from e0 to e1.

CA (e)

S(r1) – I (r1) O S(r0) – I (r0) Current account

e1

e0

Answer 5:

a) Real exchange rates represent the amount of domestic goods and services that can be

exchanged for obtaining goods and services of foreign country. During recession, the

government increases its deficit spending through decreasing its savings (Bordo et al., 2017).

This further can influence the real exchange rate, current account and capita finance. Here,

current account function can be described as the function of the real exchange rate, that is,

CA(e). The equilibrium equation for determining real exchange rate is :

S(r) – I (r) = CA (e)

This relation, drawn from credit market helps to represent the impact of increasing

deficit spending through shifting S(r) – I(r) to the left and this consequently help the real

exchange rate to increase further.

Figure 3: Real exchange rate

Source: (created by author)

In the above figure, the current account shifts from S (r0) – I (r0) to S (r1) – I (r1) and

consequently, real exchange has increased from e0 to e1.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS ASSIGNMENT

b) Purchasing power parity (PPP) describes that the exchange rate between two nations and

the ratio of their currencies’ respective purchasing power are same in the absence of any trade

barriers (Chia, Lim & Ong, 2014). In long-run, the cost for purchasing any product with same

amount in domestic currency and with foreign currency is same without any arbitrage profit

opportunity.

c) In short-run, current account (CA) is a function of real exchange rate and this has a

negative slope (Rogoff, 2017). J-curve shows that domestic goods can be cheaper compare to

the foreign one, if exchange rate decreases and this further influence to increase exports and

decrease of import. Hence, current account can be in surplus.

Answer 6:

a) In the given game, the Nash equilibrium occurs at outcome B, when financial institutions

can take high risk while the Fed takes strategy to bail out those firms.

However, the first-best outcome is C, where fed takes strategy to no bail out and

financial institutions take their corresponding strategy to take risks (Salimans et al., 2016).

However, it is not the Nash equilibrium.

b) The financial institutions take higher risks for the Fed’s strategy to bail out. However,

during recession, those institutions may fail (Salimans et al., 2016). At this situation, the

policy announcement of the Fed regarding no longer bail out can push the economy towards

an adverse situation. Hence, it is not time consistent but not credible at time of recession.

Nash equilibrium can help the Fed to obtain its time consistent and credible policy

from where it can pick the most required strategy.

Answer 7:

a) The reserve demand (Rd) curve of the Fed depends on the excess reserve ratio and the

required reserve ratio. As the Rd shifts randomly, the Fed can conduct monetary policy by

targeting either the quantity of reserve or the federal Funds rate. Under the Channel-Corridor

b) Purchasing power parity (PPP) describes that the exchange rate between two nations and

the ratio of their currencies’ respective purchasing power are same in the absence of any trade

barriers (Chia, Lim & Ong, 2014). In long-run, the cost for purchasing any product with same

amount in domestic currency and with foreign currency is same without any arbitrage profit

opportunity.

c) In short-run, current account (CA) is a function of real exchange rate and this has a

negative slope (Rogoff, 2017). J-curve shows that domestic goods can be cheaper compare to

the foreign one, if exchange rate decreases and this further influence to increase exports and

decrease of import. Hence, current account can be in surplus.

Answer 6:

a) In the given game, the Nash equilibrium occurs at outcome B, when financial institutions

can take high risk while the Fed takes strategy to bail out those firms.

However, the first-best outcome is C, where fed takes strategy to no bail out and

financial institutions take their corresponding strategy to take risks (Salimans et al., 2016).

However, it is not the Nash equilibrium.

b) The financial institutions take higher risks for the Fed’s strategy to bail out. However,

during recession, those institutions may fail (Salimans et al., 2016). At this situation, the

policy announcement of the Fed regarding no longer bail out can push the economy towards

an adverse situation. Hence, it is not time consistent but not credible at time of recession.

Nash equilibrium can help the Fed to obtain its time consistent and credible policy

from where it can pick the most required strategy.

Answer 7:

a) The reserve demand (Rd) curve of the Fed depends on the excess reserve ratio and the

required reserve ratio. As the Rd shifts randomly, the Fed can conduct monetary policy by

targeting either the quantity of reserve or the federal Funds rate. Under the Channel-Corridor

8ECONOMICS ASSIGNMENT

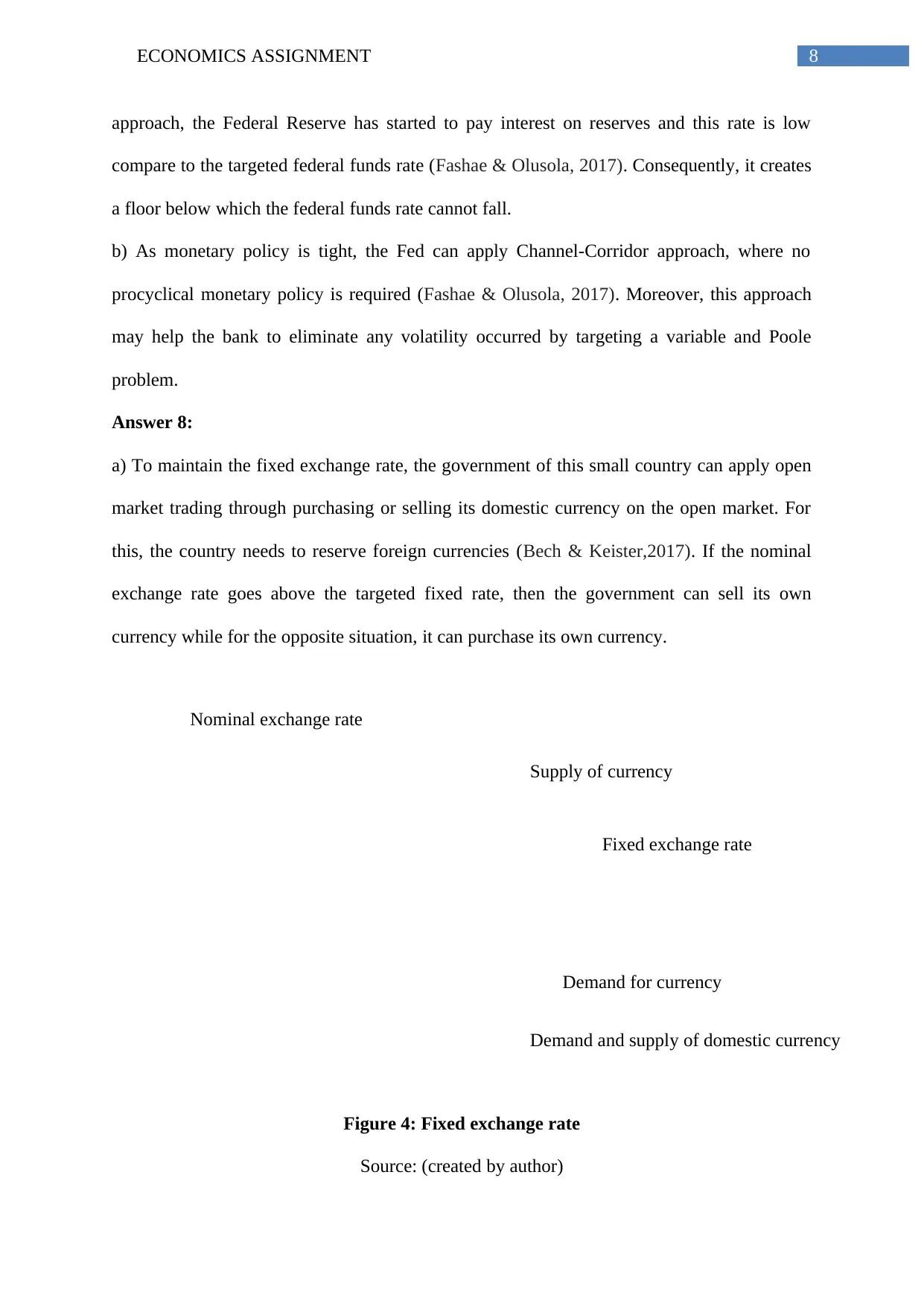

Demand and supply of domestic currency

Nominal exchange rate

Supply of currency

Demand for currency

Fixed exchange rate

approach, the Federal Reserve has started to pay interest on reserves and this rate is low

compare to the targeted federal funds rate (Fashae & Olusola, 2017). Consequently, it creates

a floor below which the federal funds rate cannot fall.

b) As monetary policy is tight, the Fed can apply Channel-Corridor approach, where no

procyclical monetary policy is required (Fashae & Olusola, 2017). Moreover, this approach

may help the bank to eliminate any volatility occurred by targeting a variable and Poole

problem.

Answer 8:

a) To maintain the fixed exchange rate, the government of this small country can apply open

market trading through purchasing or selling its domestic currency on the open market. For

this, the country needs to reserve foreign currencies (Bech & Keister,2017). If the nominal

exchange rate goes above the targeted fixed rate, then the government can sell its own

currency while for the opposite situation, it can purchase its own currency.

Figure 4: Fixed exchange rate

Source: (created by author)

Demand and supply of domestic currency

Nominal exchange rate

Supply of currency

Demand for currency

Fixed exchange rate

approach, the Federal Reserve has started to pay interest on reserves and this rate is low

compare to the targeted federal funds rate (Fashae & Olusola, 2017). Consequently, it creates

a floor below which the federal funds rate cannot fall.

b) As monetary policy is tight, the Fed can apply Channel-Corridor approach, where no

procyclical monetary policy is required (Fashae & Olusola, 2017). Moreover, this approach

may help the bank to eliminate any volatility occurred by targeting a variable and Poole

problem.

Answer 8:

a) To maintain the fixed exchange rate, the government of this small country can apply open

market trading through purchasing or selling its domestic currency on the open market. For

this, the country needs to reserve foreign currencies (Bech & Keister,2017). If the nominal

exchange rate goes above the targeted fixed rate, then the government can sell its own

currency while for the opposite situation, it can purchase its own currency.

Figure 4: Fixed exchange rate

Source: (created by author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS ASSIGNMENT

E

Ef

O REL

it – [if,t-(Ee(t+1) - Et)/ Et]

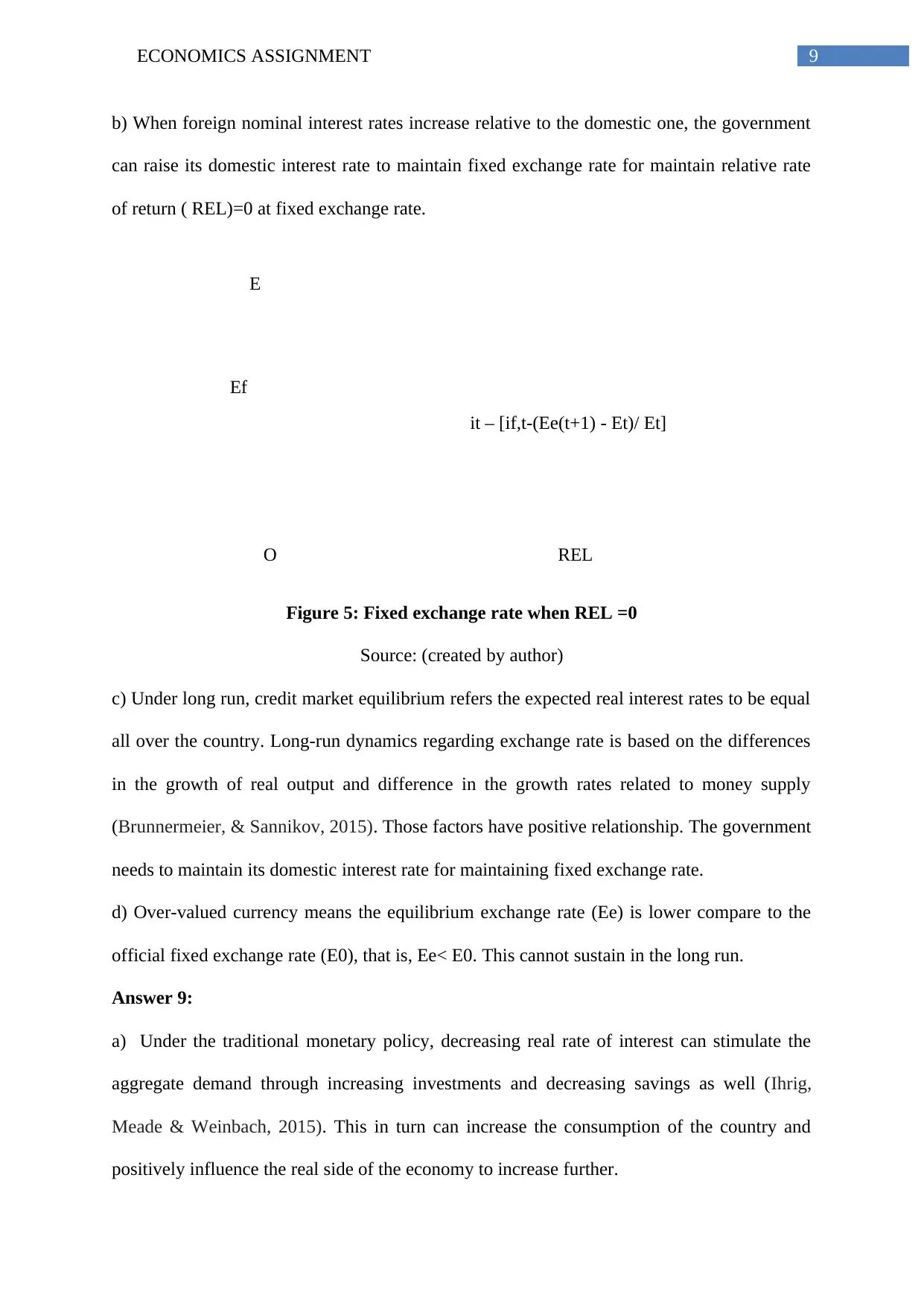

b) When foreign nominal interest rates increase relative to the domestic one, the government

can raise its domestic interest rate to maintain fixed exchange rate for maintain relative rate

of return ( REL)=0 at fixed exchange rate.

Figure 5: Fixed exchange rate when REL =0

Source: (created by author)

c) Under long run, credit market equilibrium refers the expected real interest rates to be equal

all over the country. Long-run dynamics regarding exchange rate is based on the differences

in the growth of real output and difference in the growth rates related to money supply

(Brunnermeier, & Sannikov, 2015). Those factors have positive relationship. The government

needs to maintain its domestic interest rate for maintaining fixed exchange rate.

d) Over-valued currency means the equilibrium exchange rate (Ee) is lower compare to the

official fixed exchange rate (E0), that is, Ee< E0. This cannot sustain in the long run.

Answer 9:

a) Under the traditional monetary policy, decreasing real rate of interest can stimulate the

aggregate demand through increasing investments and decreasing savings as well (Ihrig,

Meade & Weinbach, 2015). This in turn can increase the consumption of the country and

positively influence the real side of the economy to increase further.

E

Ef

O REL

it – [if,t-(Ee(t+1) - Et)/ Et]

b) When foreign nominal interest rates increase relative to the domestic one, the government

can raise its domestic interest rate to maintain fixed exchange rate for maintain relative rate

of return ( REL)=0 at fixed exchange rate.

Figure 5: Fixed exchange rate when REL =0

Source: (created by author)

c) Under long run, credit market equilibrium refers the expected real interest rates to be equal

all over the country. Long-run dynamics regarding exchange rate is based on the differences

in the growth of real output and difference in the growth rates related to money supply

(Brunnermeier, & Sannikov, 2015). Those factors have positive relationship. The government

needs to maintain its domestic interest rate for maintaining fixed exchange rate.

d) Over-valued currency means the equilibrium exchange rate (Ee) is lower compare to the

official fixed exchange rate (E0), that is, Ee< E0. This cannot sustain in the long run.

Answer 9:

a) Under the traditional monetary policy, decreasing real rate of interest can stimulate the

aggregate demand through increasing investments and decreasing savings as well (Ihrig,

Meade & Weinbach, 2015). This in turn can increase the consumption of the country and

positively influence the real side of the economy to increase further.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS ASSIGNMENT

b) Various types of unconventional monetary policies are quantitative easing, credit easing,

signaling and forward guidance (Neely, 2015). Different forms of assets, for instance,

treasury securities, federal agency debt influence the balance sheet of the Fed. However, the

overall Fed assets level has remained relatively constant due to increase in long term holding.

b) Various types of unconventional monetary policies are quantitative easing, credit easing,

signaling and forward guidance (Neely, 2015). Different forms of assets, for instance,

treasury securities, federal agency debt influence the balance sheet of the Fed. However, the

overall Fed assets level has remained relatively constant due to increase in long term holding.

11ECONOMICS ASSIGNMENT

References:

Ahelegbey, D. F., Billio, M., & Casarin, R. (2016). Bayesian graphical models for structural

vector autoregressive processes. Journal of Applied Econometrics, 31(2), 357-386.

Arteta, C., Kose, M. A., Stocker, M., & Taskin, T. (2018). Implications of negative interest

rate policies: An early assessment. Pacific Economic Review, 23(1), 8-26.

Bech, M., & Keister, T. (2017). Liquidity regulation and the implementation of monetary

policy. Journal of Monetary Economics, 92, 64-77.

Blanchard, O., & Summers, L. (2017, October). Rethinking Stabilization Policy: Back to the

Future. In Rethinking Macroeconomic Policy Conference, Peterson Institute for

International Economics, October (pp. 12-13).

Bordo, M. D., Choudhri, E. U., Fazio, G., & MacDonald, R. (2017). The real exchange rate in

the long run: Balassa-Samuelson effects reconsidered. Journal of International Money

and Finance, 75, 69-92.

Brunnermeier, M. K., & Sannikov, Y. (2015). International credit flows and pecuniary

externalities. American Economic Journal: Macroeconomics, 7(1), 297-338.

Chia, R. C. J., Lim, S. Y., & Ong, S. L. (2014). Long-run validity of purchasing power parity

and cointegration analysis for low income African countries. Economics

Bulletin, 34(3), 1438-1447.

Chinn, M. D., & Zhang, Y. (2018). Uncovered Interest Parity and Monetary Policy Near and

Far from the Zero Lower Bound. Open Economies Review, 29(1), 1-30.

Donnery, S., Doran, D., Gleeson, R., & Carroll, K. (2017). Non-standard Monetary Policy

Measures and the Balance Sheets of Eurosystem Central Banks. Quarterly Bulletin

Articles, 79-94.

References:

Ahelegbey, D. F., Billio, M., & Casarin, R. (2016). Bayesian graphical models for structural

vector autoregressive processes. Journal of Applied Econometrics, 31(2), 357-386.

Arteta, C., Kose, M. A., Stocker, M., & Taskin, T. (2018). Implications of negative interest

rate policies: An early assessment. Pacific Economic Review, 23(1), 8-26.

Bech, M., & Keister, T. (2017). Liquidity regulation and the implementation of monetary

policy. Journal of Monetary Economics, 92, 64-77.

Blanchard, O., & Summers, L. (2017, October). Rethinking Stabilization Policy: Back to the

Future. In Rethinking Macroeconomic Policy Conference, Peterson Institute for

International Economics, October (pp. 12-13).

Bordo, M. D., Choudhri, E. U., Fazio, G., & MacDonald, R. (2017). The real exchange rate in

the long run: Balassa-Samuelson effects reconsidered. Journal of International Money

and Finance, 75, 69-92.

Brunnermeier, M. K., & Sannikov, Y. (2015). International credit flows and pecuniary

externalities. American Economic Journal: Macroeconomics, 7(1), 297-338.

Chia, R. C. J., Lim, S. Y., & Ong, S. L. (2014). Long-run validity of purchasing power parity

and cointegration analysis for low income African countries. Economics

Bulletin, 34(3), 1438-1447.

Chinn, M. D., & Zhang, Y. (2018). Uncovered Interest Parity and Monetary Policy Near and

Far from the Zero Lower Bound. Open Economies Review, 29(1), 1-30.

Donnery, S., Doran, D., Gleeson, R., & Carroll, K. (2017). Non-standard Monetary Policy

Measures and the Balance Sheets of Eurosystem Central Banks. Quarterly Bulletin

Articles, 79-94.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.