Economy of Australia: Microeconomics and Macroeconomics

Added on 2023-03-23

11 Pages1589 Words48 Views

Running head: ECONOMICS

Economics

Name of the Student

Name of the University

Author Note

Economics

Name of the Student

Name of the University

Author Note

1ECONOMY OF AUSTRALIA

Table of Contents

Part a: Microeconomics..............................................................................................................2

Answer to question 1..............................................................................................................2

Answer to question 2..............................................................................................................2

Answer to question 3..............................................................................................................3

Answer to question 4..............................................................................................................4

Part b: Macroeconomics.............................................................................................................4

Answer to Question 1.............................................................................................................4

Answer to question 2..............................................................................................................5

Answer to question 3..............................................................................................................6

Answer to question 4..............................................................................................................7

Answer to question 5..............................................................................................................7

References..................................................................................................................................9

Table of Contents

Part a: Microeconomics..............................................................................................................2

Answer to question 1..............................................................................................................2

Answer to question 2..............................................................................................................2

Answer to question 3..............................................................................................................3

Answer to question 4..............................................................................................................4

Part b: Macroeconomics.............................................................................................................4

Answer to Question 1.............................................................................................................4

Answer to question 2..............................................................................................................5

Answer to question 3..............................................................................................................6

Answer to question 4..............................................................................................................7

Answer to question 5..............................................................................................................7

References..................................................................................................................................9

2ECONOMY OF AUSTRALIA

Part a: Microeconomics

Answer to question 1

Commonwealth Bank, ANZ, NAB and Westpac are the leading banks in Australia

that dominates the banking industry (Statista 2017). The way these banks control the

industry, it takes the form of an oligopoly market structure. The major attributes of banking

industry with oligopoly in Australia are barrier to entry and restriction for consumers in

switching banks. These four banks together serve above 80 percent of the lending market in

Australia.

In the period of Global Financial Crisis (GFC), unlike most of the countries Australia

handled its banking industry tactfully, which is a laudable task for that period. Policies taken

by the Reserve Bank of Australia and Australian Prudential Regulatory Authority (ARPA)

are the key factors that drove the banking sector efficiently and kept it away from being

victim of GFC. The major policies were restricting banks from merging and competition

limitation leading to reduction of venturesome policies of banks. Further, increased deposit

guarantee prevented small banks from bankruptcy. Hence, these policies enabled banks to

sustain the poor state of the financial market.

Answer to question 2

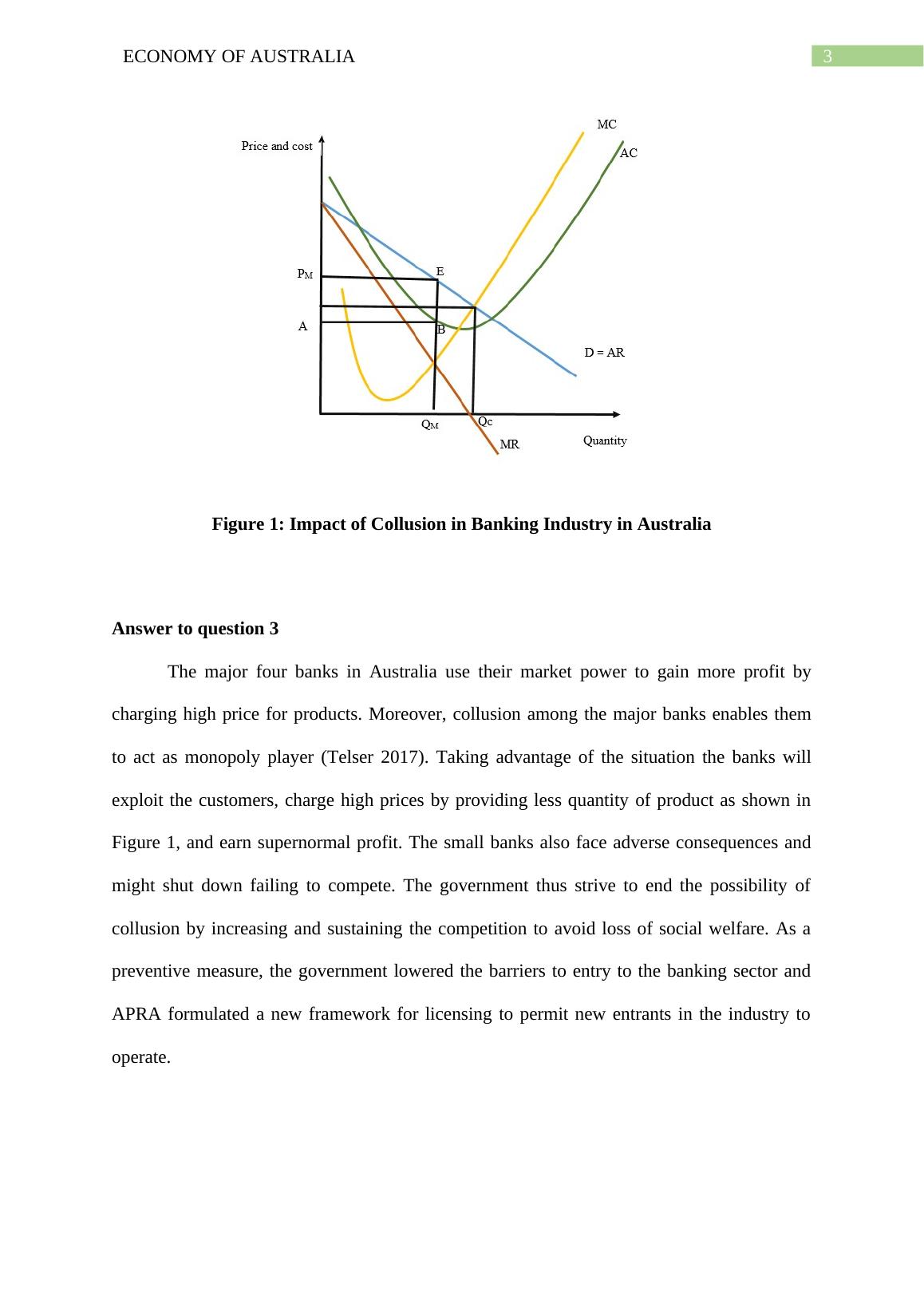

Four major banks of Australia if collude will gain monopoly power over the market.

The banks for their products will charge high prices to gain more profit. The small banks take

the price fixed by the big banks as given and price their products accordingly. Therefore, with

the full control over the market, the big banks will charge high prices for lower quantity of

products and gains super normal profit. Hence, due to collusion among big banks the price

quantity fell below competitive quantity. The equilibrium price and quantity after collusion is

at PM and QM shown in the Figure 1 given below

Part a: Microeconomics

Answer to question 1

Commonwealth Bank, ANZ, NAB and Westpac are the leading banks in Australia

that dominates the banking industry (Statista 2017). The way these banks control the

industry, it takes the form of an oligopoly market structure. The major attributes of banking

industry with oligopoly in Australia are barrier to entry and restriction for consumers in

switching banks. These four banks together serve above 80 percent of the lending market in

Australia.

In the period of Global Financial Crisis (GFC), unlike most of the countries Australia

handled its banking industry tactfully, which is a laudable task for that period. Policies taken

by the Reserve Bank of Australia and Australian Prudential Regulatory Authority (ARPA)

are the key factors that drove the banking sector efficiently and kept it away from being

victim of GFC. The major policies were restricting banks from merging and competition

limitation leading to reduction of venturesome policies of banks. Further, increased deposit

guarantee prevented small banks from bankruptcy. Hence, these policies enabled banks to

sustain the poor state of the financial market.

Answer to question 2

Four major banks of Australia if collude will gain monopoly power over the market.

The banks for their products will charge high prices to gain more profit. The small banks take

the price fixed by the big banks as given and price their products accordingly. Therefore, with

the full control over the market, the big banks will charge high prices for lower quantity of

products and gains super normal profit. Hence, due to collusion among big banks the price

quantity fell below competitive quantity. The equilibrium price and quantity after collusion is

at PM and QM shown in the Figure 1 given below

3ECONOMY OF AUSTRALIA

Figure 1: Impact of Collusion in Banking Industry in Australia

Answer to question 3

The major four banks in Australia use their market power to gain more profit by

charging high price for products. Moreover, collusion among the major banks enables them

to act as monopoly player (Telser 2017). Taking advantage of the situation the banks will

exploit the customers, charge high prices by providing less quantity of product as shown in

Figure 1, and earn supernormal profit. The small banks also face adverse consequences and

might shut down failing to compete. The government thus strive to end the possibility of

collusion by increasing and sustaining the competition to avoid loss of social welfare. As a

preventive measure, the government lowered the barriers to entry to the banking sector and

APRA formulated a new framework for licensing to permit new entrants in the industry to

operate.

Figure 1: Impact of Collusion in Banking Industry in Australia

Answer to question 3

The major four banks in Australia use their market power to gain more profit by

charging high price for products. Moreover, collusion among the major banks enables them

to act as monopoly player (Telser 2017). Taking advantage of the situation the banks will

exploit the customers, charge high prices by providing less quantity of product as shown in

Figure 1, and earn supernormal profit. The small banks also face adverse consequences and

might shut down failing to compete. The government thus strive to end the possibility of

collusion by increasing and sustaining the competition to avoid loss of social welfare. As a

preventive measure, the government lowered the barriers to entry to the banking sector and

APRA formulated a new framework for licensing to permit new entrants in the industry to

operate.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Economics: Microeconomics and Macroeconomicslg...

|11

|1491

|372

Economics: Microeconomics and Macroeconomicslg...

|12

|1714

|321

Economics: Microeconomics and Macroeconomics Study Materiallg...

|10

|1397

|415

Economics: Australian Banks and Oligopoly Marketlg...

|12

|1880

|54

Economics Assessment: Microeconomics and Macroeconomicslg...

|10

|1388

|132

Economic Principles in Finance Industrylg...

|13

|3153

|287