ECOM4000 Economics Assignment: Micro & Macro Analysis in Australia

VerifiedAdded on 2023/03/30

|11

|1491

|372

Homework Assignment

AI Summary

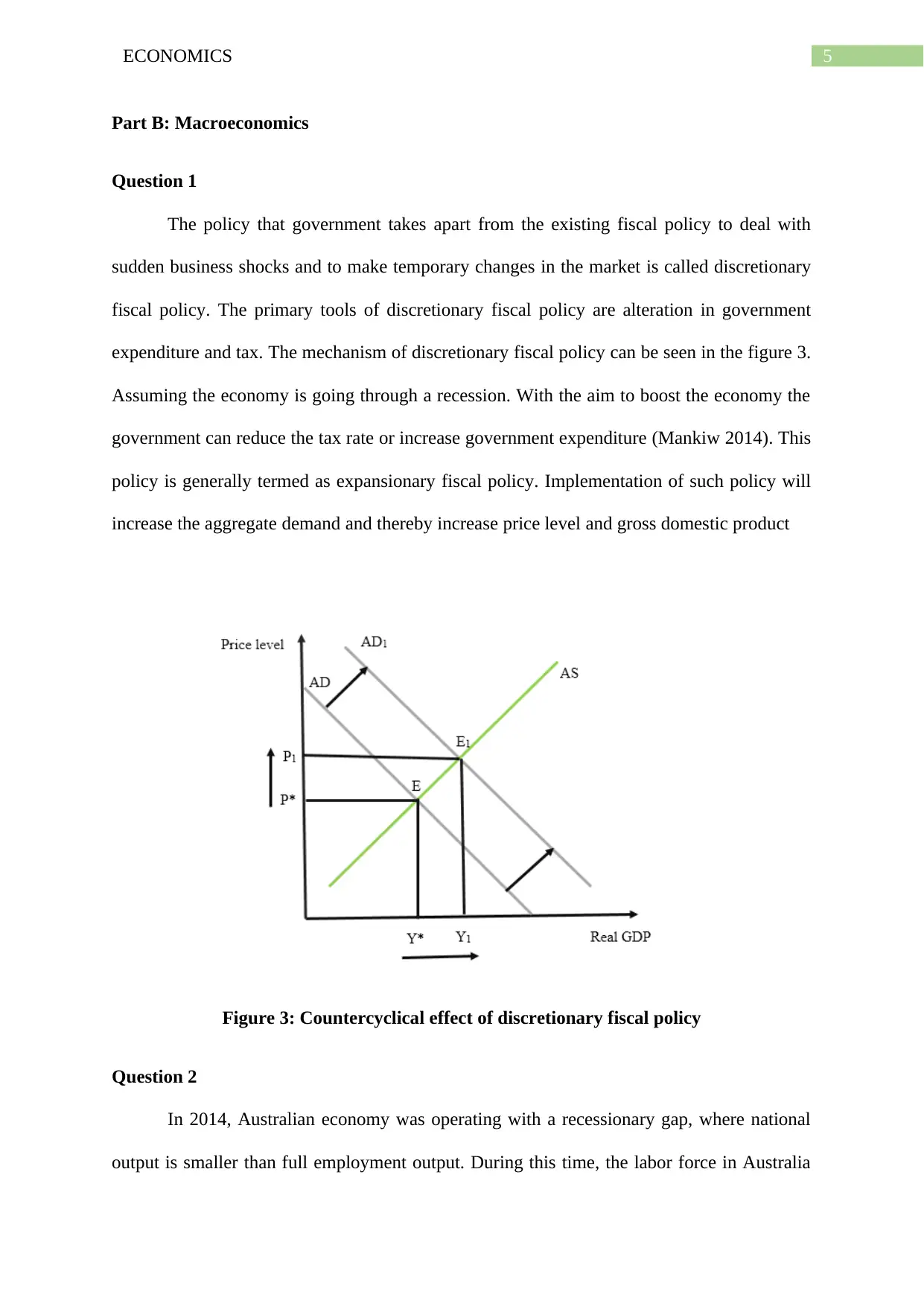

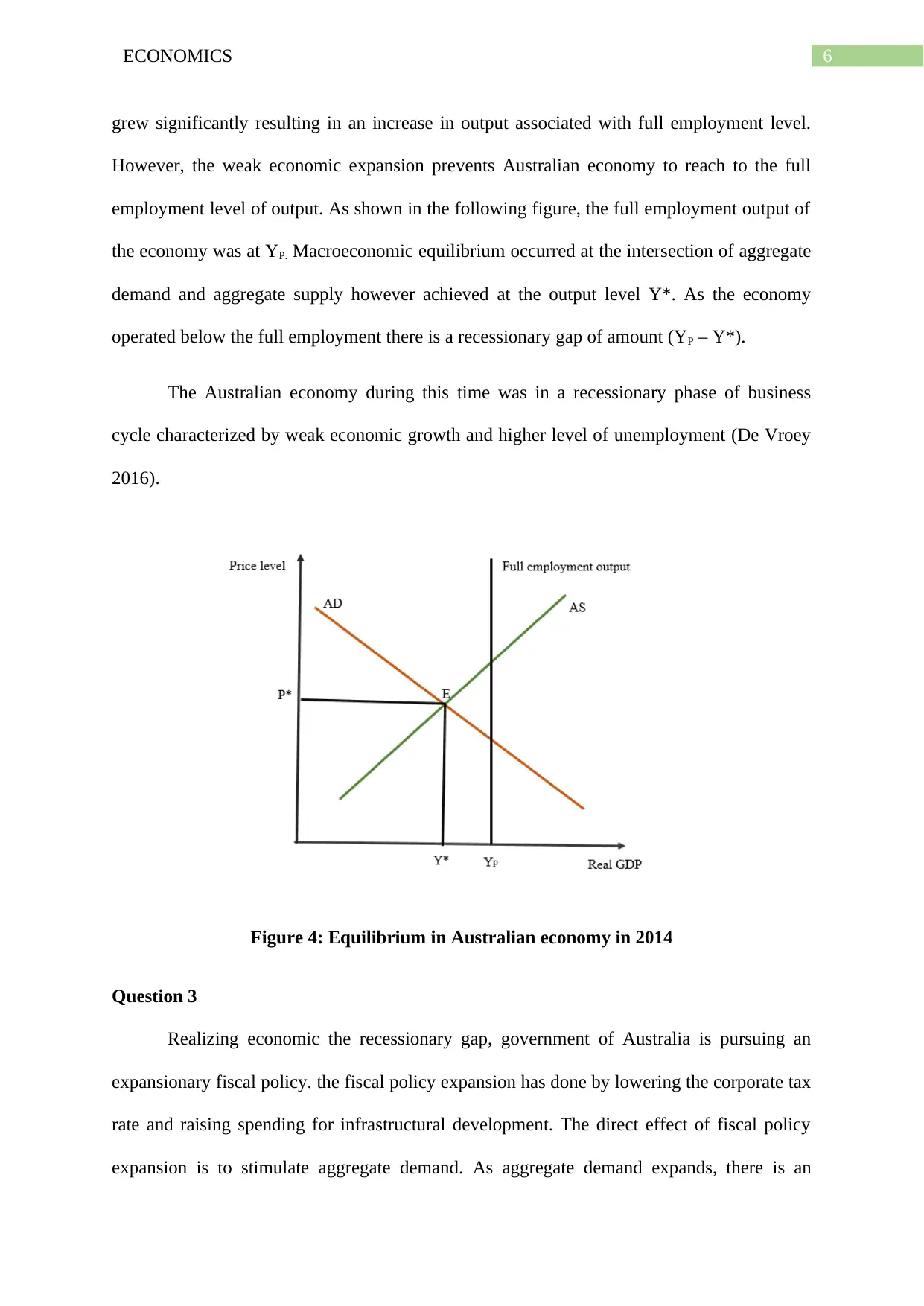

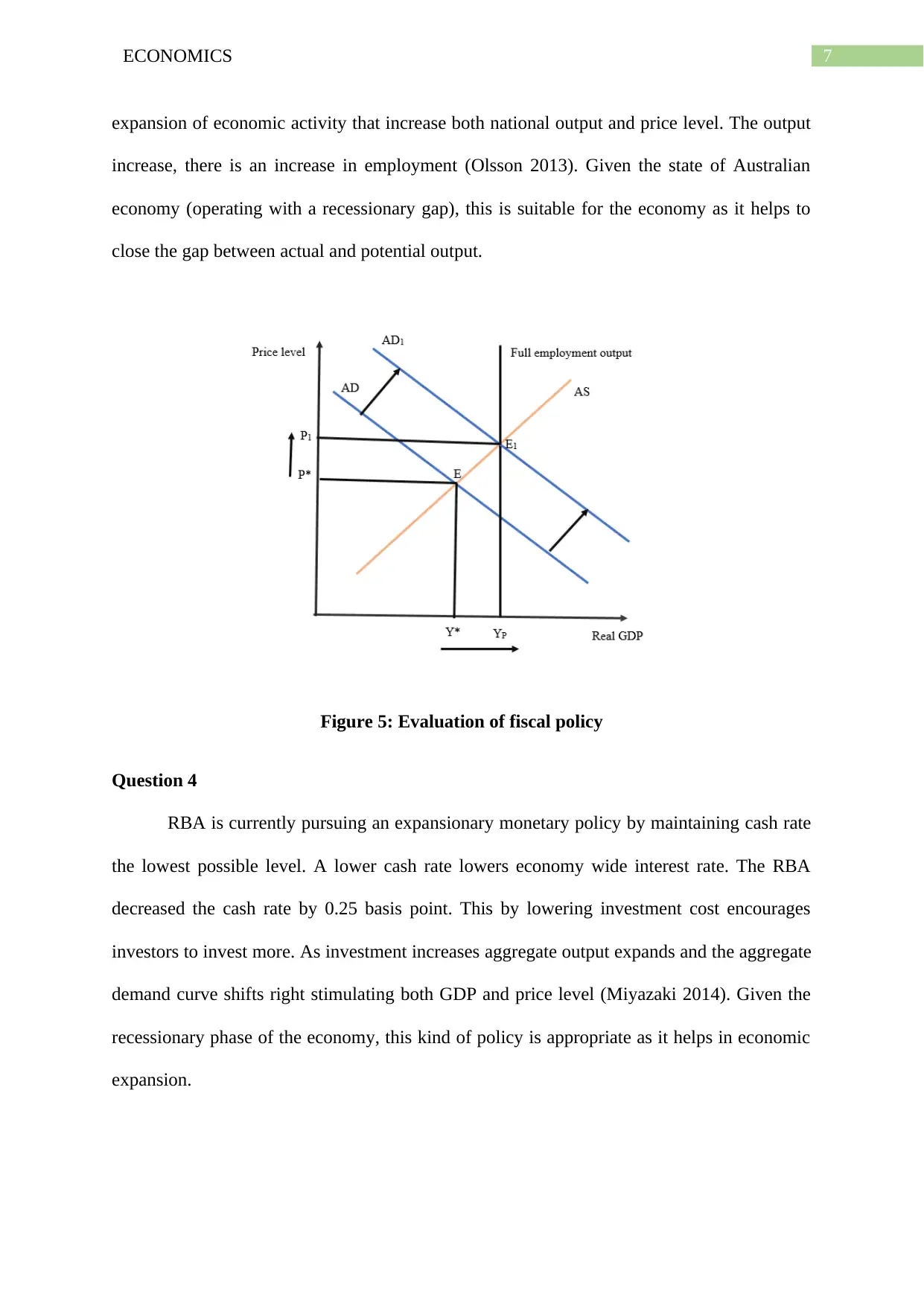

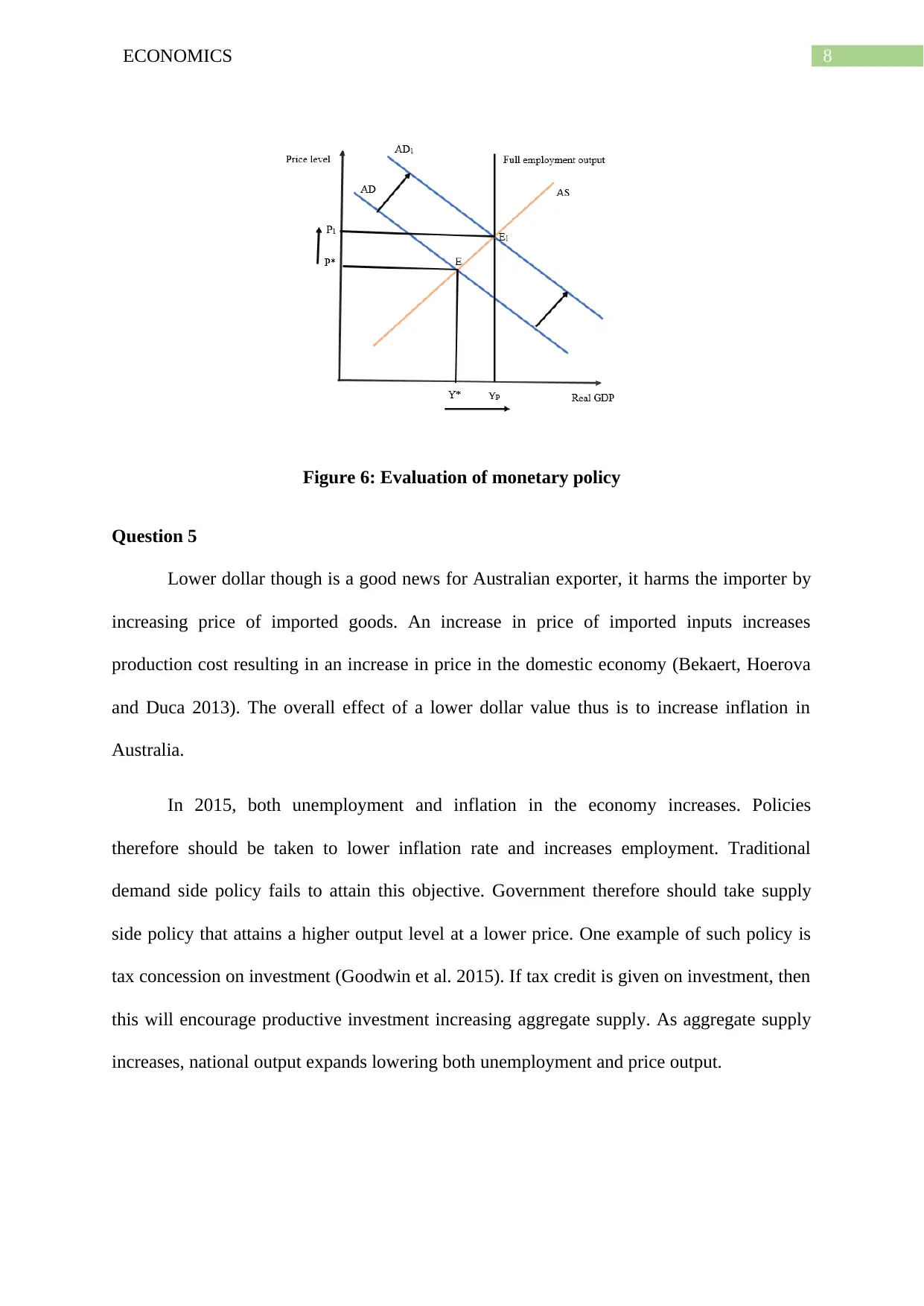

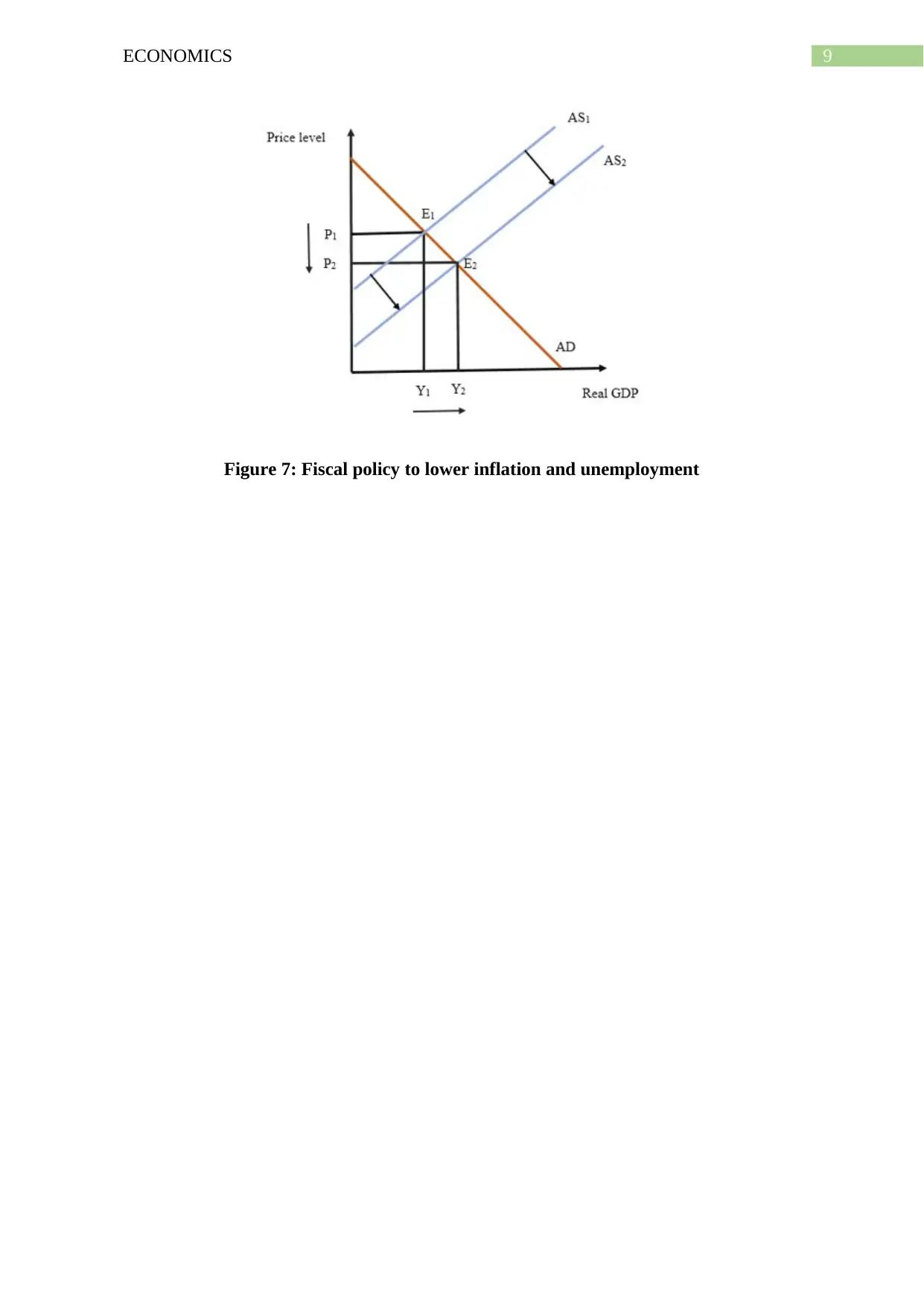

This economics assignment provides a comprehensive analysis of microeconomic and macroeconomic principles within the context of the Australian economy. The microeconomics section examines the oligopolistic structure of the Australian banking industry, focusing on the dominance of the four major banks (ANZ, Westpac, NAB, and Commonwealth Bank) and the impact of collusion. It discusses the role of APRA in promoting competition through new licensing policies and analyzes the dynamics of market entry and profit levels. The macroeconomics section explores discretionary fiscal policy, its tools (government expenditure and tax), and its application in addressing economic shocks. It evaluates Australia's economic conditions in 2014, including the recessionary gap and the impact of expansionary fiscal policies, alongside the role of the RBA's monetary policy in stimulating aggregate demand. Furthermore, it addresses the implications of a lower dollar value on inflation and unemployment, advocating for supply-side policies like tax concessions on investment to achieve higher output and lower prices. Desklib offers a wide array of solved assignments and past papers for students seeking academic support.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.