Effective Planning Tools for Managing Accounts

VerifiedAdded on 2024/05/14

|13

|1935

|498

AI Summary

Explore the important tools and techniques in management accounting including financial statement analysis, budgetary control, decision accounting, and case studies. Learn how these tools aid in decision-making and financial planning.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Effective Planning Tools for Managing Accounts

1 | P a g e

1 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Part A Important tool and techniques in management accounting..................................................3

Analysis of Financial Tools.........................................................................................................3

Budgetary Control........................................................................................................................4

Decision accounting.....................................................................................................................6

Part B...............................................................................................................................................8

Case 1...........................................................................................................................................8

References:....................................................................................................................................12

2 | P a g e

Part A Important tool and techniques in management accounting..................................................3

Analysis of Financial Tools.........................................................................................................3

Budgetary Control........................................................................................................................4

Decision accounting.....................................................................................................................6

Part B...............................................................................................................................................8

Case 1...........................................................................................................................................8

References:....................................................................................................................................12

2 | P a g e

Part A Important tool and techniques in management accounting

There are different tools and techniques available or the management accountant. The

management accountant can use one of these tools for taking decision regarding management

accounting decision. Following are some important tools that are available for the management

accountant:

Analysis of Financial Tools

It is one of the most important management accounting tool that is available in the market.

Financial statement means the statement of profit and loss, balance sheet and cash flow statement

of the company (Chiarini & Vagnoni, 2014). These financial statements are used by the

management accountant for ration analysis, comparison of the profitability of the company with

past period. The financial analysis helps the company in following analysis:

1. Profitability: It is the ability of the company to generate profit for present and future

period of the company.

2. Solvency: It determines the capability of the company to meet its current obligation

within time.

3. Liquidity: It is the ability of the company to have current assets over and above the

current liability of the company (Chiarini & Vagnoni, 2014).

4. Stability: The term stability defines the capacity of the company to remain in the business

for the determined period. It is the capacity to bear losses that can occur in the future

year.

Example of financial statement analysis

Particular 2018 ($ Million) 2017 ($ Million) 2016 ($ Million)

Revenue 5,000 4,000 3,000

Cost of Goods Sold 3,200 3,000 2,500

3 | P a g e

There are different tools and techniques available or the management accountant. The

management accountant can use one of these tools for taking decision regarding management

accounting decision. Following are some important tools that are available for the management

accountant:

Analysis of Financial Tools

It is one of the most important management accounting tool that is available in the market.

Financial statement means the statement of profit and loss, balance sheet and cash flow statement

of the company (Chiarini & Vagnoni, 2014). These financial statements are used by the

management accountant for ration analysis, comparison of the profitability of the company with

past period. The financial analysis helps the company in following analysis:

1. Profitability: It is the ability of the company to generate profit for present and future

period of the company.

2. Solvency: It determines the capability of the company to meet its current obligation

within time.

3. Liquidity: It is the ability of the company to have current assets over and above the

current liability of the company (Chiarini & Vagnoni, 2014).

4. Stability: The term stability defines the capacity of the company to remain in the business

for the determined period. It is the capacity to bear losses that can occur in the future

year.

Example of financial statement analysis

Particular 2018 ($ Million) 2017 ($ Million) 2016 ($ Million)

Revenue 5,000 4,000 3,000

Cost of Goods Sold 3,200 3,000 2,500

3 | P a g e

Gross Profit 1,800 1,000 500

Depreciation -500 -450 -400

SB&A -300 -300 -300

Interest -50 -50 -50

Earnings Before Tax 950 200 -250

Tax -225 20 0

Net Earnings 725 180 -250

Net profit margin 14.5% 4.5% -8.33%

Now from the above table it can be ascertained the net profit percentage of company is in

growing trend and it has generated highest 14.5% net profit margin in the year 2018.

Budgetary Control

This tool of management accounting will concentrate in making plans for future business period.

The main process under this tool is to evaluate the past performance of the company and

anticipate the future inflation and growth of the company. Budget is prepared only after making

that evaluation by the management accountant. The main reason for the preparation of budget is

to prepare a standard for the employees of the company that has to be followed in order to

4 | P a g e

Depreciation -500 -450 -400

SB&A -300 -300 -300

Interest -50 -50 -50

Earnings Before Tax 950 200 -250

Tax -225 20 0

Net Earnings 725 180 -250

Net profit margin 14.5% 4.5% -8.33%

Now from the above table it can be ascertained the net profit percentage of company is in

growing trend and it has generated highest 14.5% net profit margin in the year 2018.

Budgetary Control

This tool of management accounting will concentrate in making plans for future business period.

The main process under this tool is to evaluate the past performance of the company and

anticipate the future inflation and growth of the company. Budget is prepared only after making

that evaluation by the management accountant. The main reason for the preparation of budget is

to prepare a standard for the employees of the company that has to be followed in order to

4 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

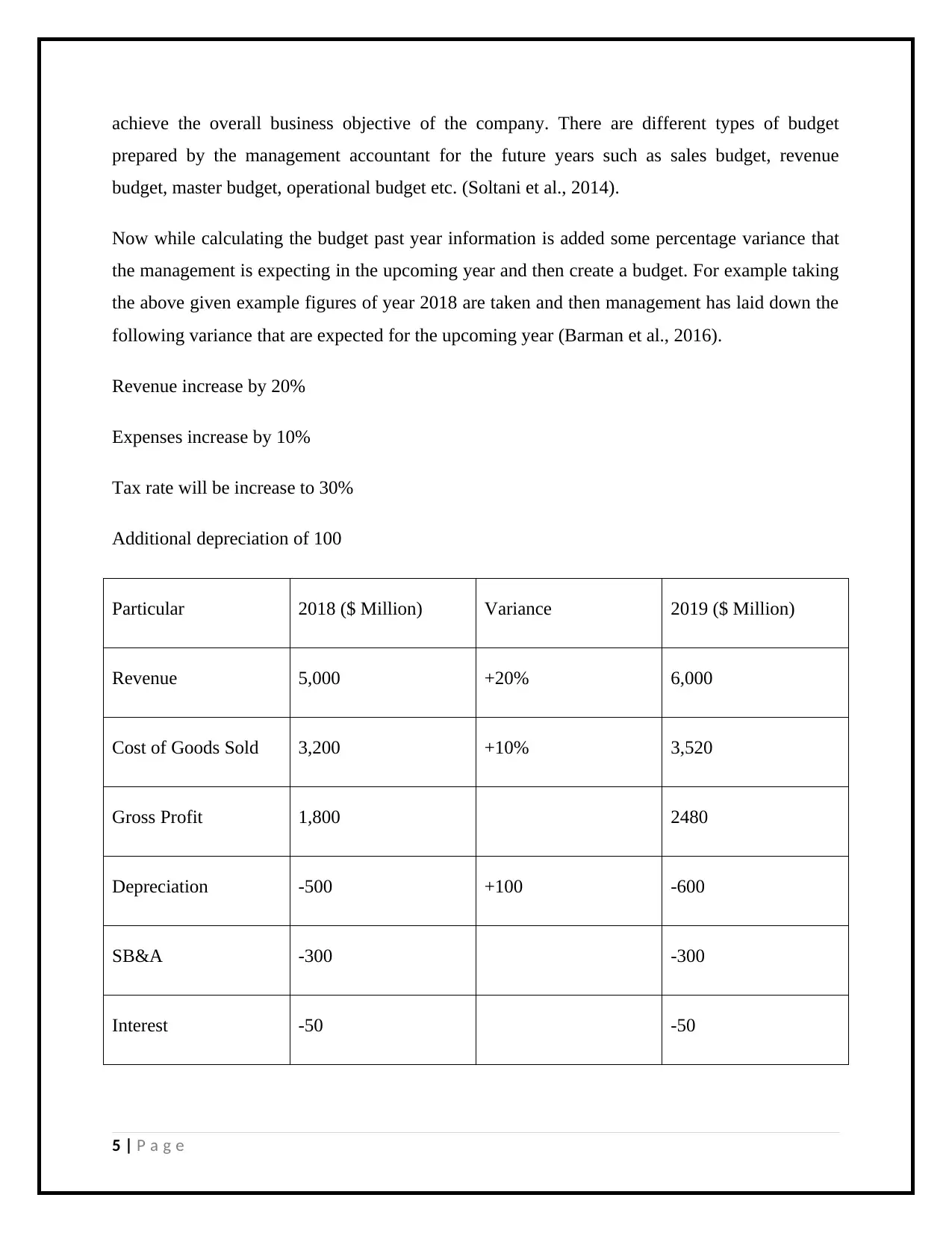

achieve the overall business objective of the company. There are different types of budget

prepared by the management accountant for the future years such as sales budget, revenue

budget, master budget, operational budget etc. (Soltani et al., 2014).

Now while calculating the budget past year information is added some percentage variance that

the management is expecting in the upcoming year and then create a budget. For example taking

the above given example figures of year 2018 are taken and then management has laid down the

following variance that are expected for the upcoming year (Barman et al., 2016).

Revenue increase by 20%

Expenses increase by 10%

Tax rate will be increase to 30%

Additional depreciation of 100

Particular 2018 ($ Million) Variance 2019 ($ Million)

Revenue 5,000 +20% 6,000

Cost of Goods Sold 3,200 +10% 3,520

Gross Profit 1,800 2480

Depreciation -500 +100 -600

SB&A -300 -300

Interest -50 -50

5 | P a g e

prepared by the management accountant for the future years such as sales budget, revenue

budget, master budget, operational budget etc. (Soltani et al., 2014).

Now while calculating the budget past year information is added some percentage variance that

the management is expecting in the upcoming year and then create a budget. For example taking

the above given example figures of year 2018 are taken and then management has laid down the

following variance that are expected for the upcoming year (Barman et al., 2016).

Revenue increase by 20%

Expenses increase by 10%

Tax rate will be increase to 30%

Additional depreciation of 100

Particular 2018 ($ Million) Variance 2019 ($ Million)

Revenue 5,000 +20% 6,000

Cost of Goods Sold 3,200 +10% 3,520

Gross Profit 1,800 2480

Depreciation -500 +100 -600

SB&A -300 -300

Interest -50 -50

5 | P a g e

Earnings Before Tax 950 1,530

Tax -225 30% of income 459

Net Earnings 725 1,071

Net profit margin 14.5% 17.85%

Decision accounting

The decision accounting is the tool that is used in the management accounting process. Decision

making tools take care of the various decisions that are used by the management of the company

is taking overall decision of the company. The decision is regarding the operation of various

activities and buy and sell of the various assets and movement of cash flow within the company.

Following are some important decision taken under the decision making process:

1. To buy or to construct any fixed assets

2. Accepting and rejection of business activities

3. To choose the best available alternatives

4. To ascertain the price of any product of the company.

5. To calculate the opportunity cost of new projects that can be accepted by the company.

6. Proper allocation of cost to various products produced with the help of selection of proper

cost driver by the company.

Examples of decision making techniques that are used by the management accountant from

selection of different options are:

Decision matrix: This technique is used to evaluate a number of options which are available in

the decision making. Each of the option available is weighted and scored individually than all the

option is compared and the best alternative is selected (Cooper et al., 2017).

6 | P a g e

Tax -225 30% of income 459

Net Earnings 725 1,071

Net profit margin 14.5% 17.85%

Decision accounting

The decision accounting is the tool that is used in the management accounting process. Decision

making tools take care of the various decisions that are used by the management of the company

is taking overall decision of the company. The decision is regarding the operation of various

activities and buy and sell of the various assets and movement of cash flow within the company.

Following are some important decision taken under the decision making process:

1. To buy or to construct any fixed assets

2. Accepting and rejection of business activities

3. To choose the best available alternatives

4. To ascertain the price of any product of the company.

5. To calculate the opportunity cost of new projects that can be accepted by the company.

6. Proper allocation of cost to various products produced with the help of selection of proper

cost driver by the company.

Examples of decision making techniques that are used by the management accountant from

selection of different options are:

Decision matrix: This technique is used to evaluate a number of options which are available in

the decision making. Each of the option available is weighted and scored individually than all the

option is compared and the best alternative is selected (Cooper et al., 2017).

6 | P a g e

Decision tree: It is the graph that states the outcome of each probability from accepting the

project and therefore can be easily analyzed by the management accountant.

Cost benefit analysis: The cost benefit analysis mainly based on the comparison on the cost

involved in accepting the project and the amount of benefit derived from the acceptance of the

project.

SWOT analysis: it includes the analysis of Strength, Weakness, Opportunity and Threats.

Different methods of Management Accounting Report

Cost report

The cost report are prepared by the management so that the cost involved in the business

operations like production, administration, marketing etc can be ascertained. The cost report of

different years can be compared by the management of the company for evaluating the change in

cost and the reason for such change in cost. The management of the company wants to reduce the

cost to minimum so that the profit can be increased.

Budget report

Budget is an estimation statement of the future expenditure and revenue on the basis of past

results. The budgets are prepared by the company to set a goal for the different departments of

the company. The budget planned should be practically achievable. The management of the

company prepares a number of budgets for every year like sales budget, cost budget, revenue

budget, and master budget. Budget includes the inflation and projects to be accepted in the future

years. The budgets are prepared on the basis of past report (Maas et al., 2016).

Execution Report

The execution report lay down the guideline for the employees of the company in which the

execution of the plan is to make. The execution report is prepared by the top level management

of the company keeping in mind the goals which want to be achieved during the given financial

7 | P a g e

project and therefore can be easily analyzed by the management accountant.

Cost benefit analysis: The cost benefit analysis mainly based on the comparison on the cost

involved in accepting the project and the amount of benefit derived from the acceptance of the

project.

SWOT analysis: it includes the analysis of Strength, Weakness, Opportunity and Threats.

Different methods of Management Accounting Report

Cost report

The cost report are prepared by the management so that the cost involved in the business

operations like production, administration, marketing etc can be ascertained. The cost report of

different years can be compared by the management of the company for evaluating the change in

cost and the reason for such change in cost. The management of the company wants to reduce the

cost to minimum so that the profit can be increased.

Budget report

Budget is an estimation statement of the future expenditure and revenue on the basis of past

results. The budgets are prepared by the company to set a goal for the different departments of

the company. The budget planned should be practically achievable. The management of the

company prepares a number of budgets for every year like sales budget, cost budget, revenue

budget, and master budget. Budget includes the inflation and projects to be accepted in the future

years. The budgets are prepared on the basis of past report (Maas et al., 2016).

Execution Report

The execution report lay down the guideline for the employees of the company in which the

execution of the plan is to make. The execution report is prepared by the top level management

of the company keeping in mind the goals which want to be achieved during the given financial

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

year. The execution report can be made by the company for different financial periods. Some of

the company prepares the execution plan for every month.

Job cost report

The job cost report is simply a project evaluation report prepared by the management of the

company. The job cost report is used by the management for decision making while making

selection of project from different projects. The job cost report compare the income derived from

a project and the expense incurred for that project. The most profitable project can be identified

by the management of the company and should concentrate on that project (Maas et al., 2016).

8 | P a g e

the company prepares the execution plan for every month.

Job cost report

The job cost report is simply a project evaluation report prepared by the management of the

company. The job cost report is used by the management for decision making while making

selection of project from different projects. The job cost report compare the income derived from

a project and the expense incurred for that project. The most profitable project can be identified

by the management of the company and should concentrate on that project (Maas et al., 2016).

8 | P a g e

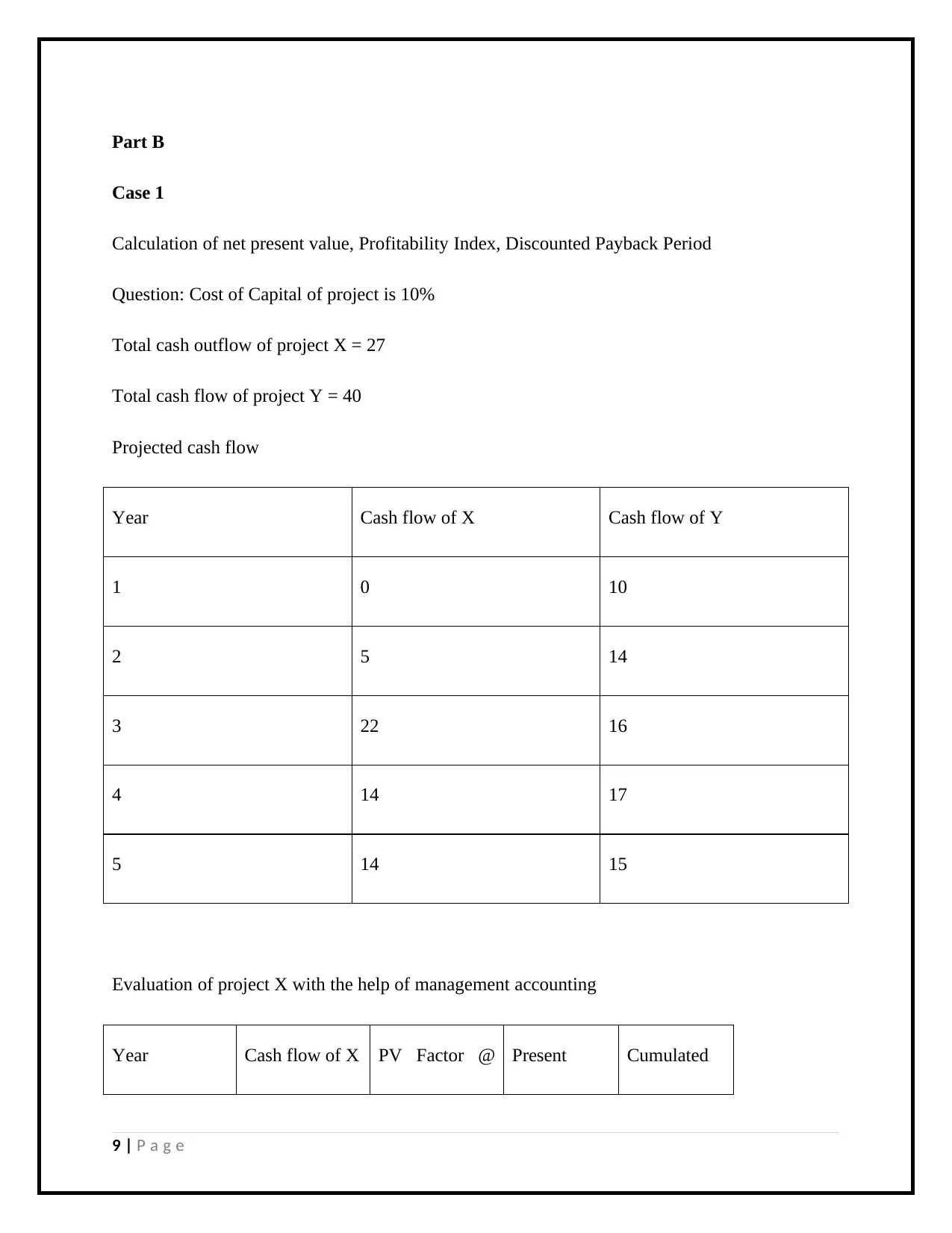

Part B

Case 1

Calculation of net present value, Profitability Index, Discounted Payback Period

Question: Cost of Capital of project is 10%

Total cash outflow of project X = 27

Total cash flow of project Y = 40

Projected cash flow

Year Cash flow of X Cash flow of Y

1 0 10

2 5 14

3 22 16

4 14 17

5 14 15

Evaluation of project X with the help of management accounting

Year Cash flow of X PV Factor @ Present Cumulated

9 | P a g e

Case 1

Calculation of net present value, Profitability Index, Discounted Payback Period

Question: Cost of Capital of project is 10%

Total cash outflow of project X = 27

Total cash flow of project Y = 40

Projected cash flow

Year Cash flow of X Cash flow of Y

1 0 10

2 5 14

3 22 16

4 14 17

5 14 15

Evaluation of project X with the help of management accounting

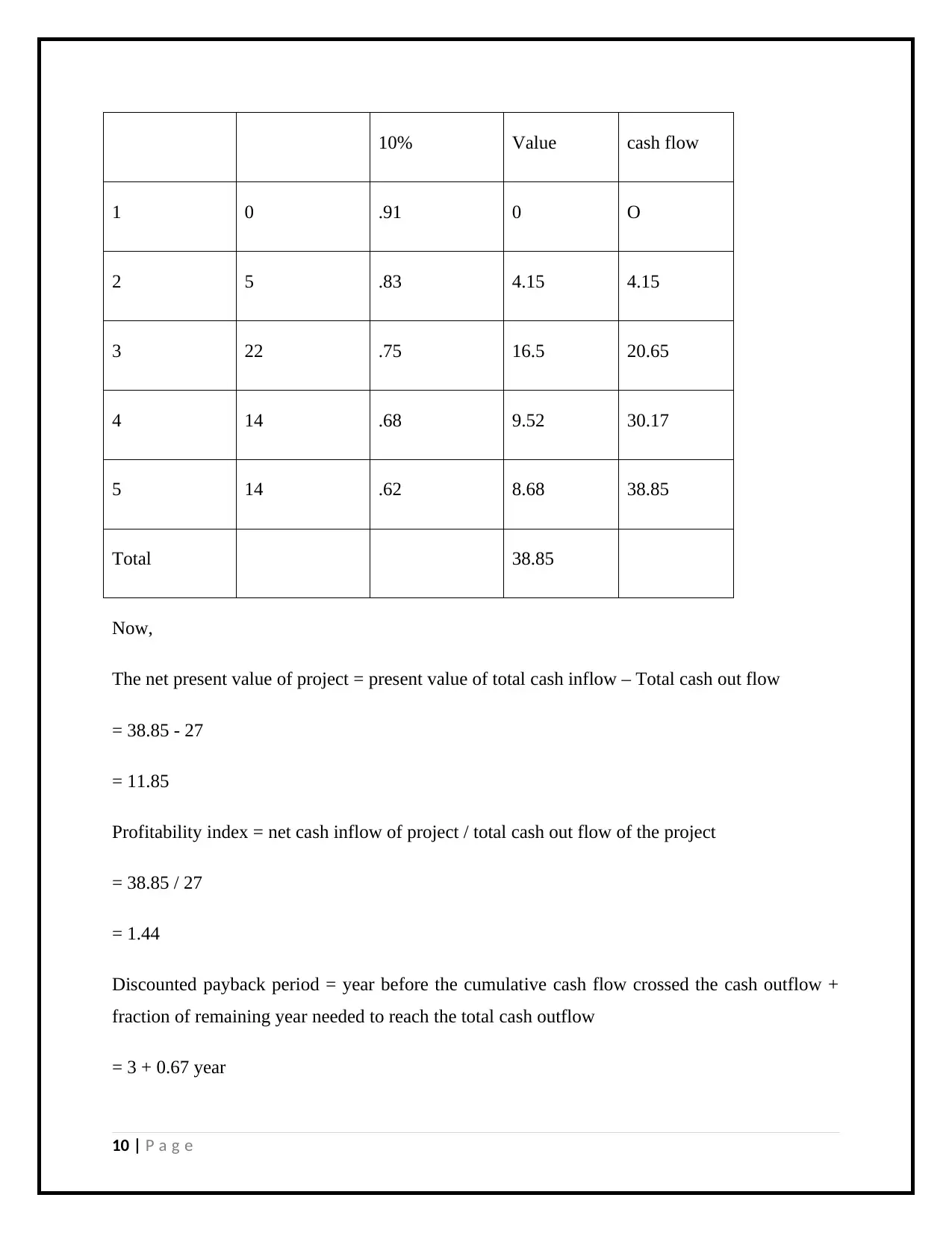

Year Cash flow of X PV Factor @ Present Cumulated

9 | P a g e

10% Value cash flow

1 0 .91 0 O

2 5 .83 4.15 4.15

3 22 .75 16.5 20.65

4 14 .68 9.52 30.17

5 14 .62 8.68 38.85

Total 38.85

Now,

The net present value of project = present value of total cash inflow – Total cash out flow

= 38.85 - 27

= 11.85

Profitability index = net cash inflow of project / total cash out flow of the project

= 38.85 / 27

= 1.44

Discounted payback period = year before the cumulative cash flow crossed the cash outflow +

fraction of remaining year needed to reach the total cash outflow

= 3 + 0.67 year

10 | P a g e

1 0 .91 0 O

2 5 .83 4.15 4.15

3 22 .75 16.5 20.65

4 14 .68 9.52 30.17

5 14 .62 8.68 38.85

Total 38.85

Now,

The net present value of project = present value of total cash inflow – Total cash out flow

= 38.85 - 27

= 11.85

Profitability index = net cash inflow of project / total cash out flow of the project

= 38.85 / 27

= 1.44

Discounted payback period = year before the cumulative cash flow crossed the cash outflow +

fraction of remaining year needed to reach the total cash outflow

= 3 + 0.67 year

10 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

= 3.67 year.

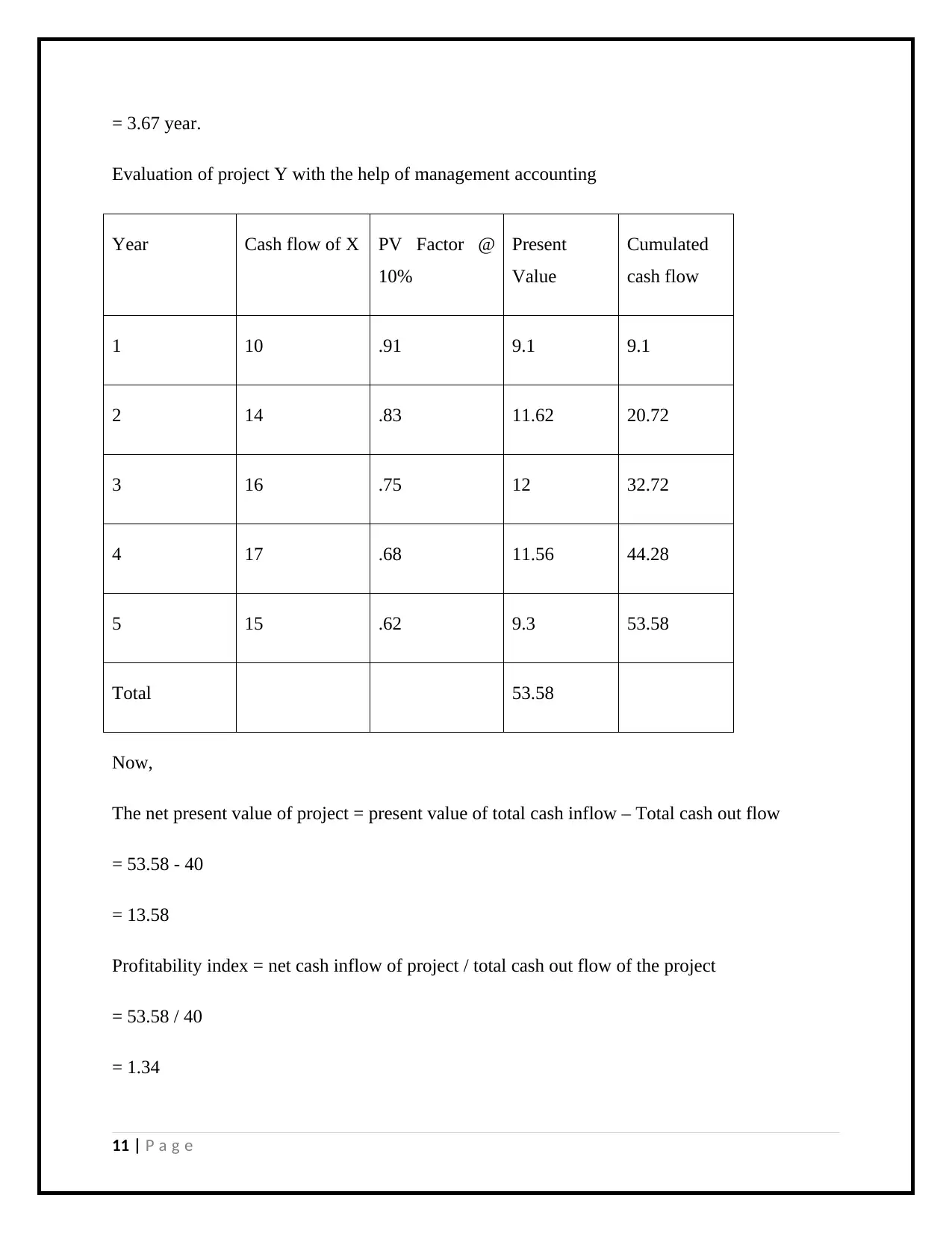

Evaluation of project Y with the help of management accounting

Year Cash flow of X PV Factor @

10%

Present

Value

Cumulated

cash flow

1 10 .91 9.1 9.1

2 14 .83 11.62 20.72

3 16 .75 12 32.72

4 17 .68 11.56 44.28

5 15 .62 9.3 53.58

Total 53.58

Now,

The net present value of project = present value of total cash inflow – Total cash out flow

= 53.58 - 40

= 13.58

Profitability index = net cash inflow of project / total cash out flow of the project

= 53.58 / 40

= 1.34

11 | P a g e

Evaluation of project Y with the help of management accounting

Year Cash flow of X PV Factor @

10%

Present

Value

Cumulated

cash flow

1 10 .91 9.1 9.1

2 14 .83 11.62 20.72

3 16 .75 12 32.72

4 17 .68 11.56 44.28

5 15 .62 9.3 53.58

Total 53.58

Now,

The net present value of project = present value of total cash inflow – Total cash out flow

= 53.58 - 40

= 13.58

Profitability index = net cash inflow of project / total cash out flow of the project

= 53.58 / 40

= 1.34

11 | P a g e

Discounted payback period = year before the cumulative cash flow crossed the cash outflow +

fraction of remaining year needed to reach the total cash outflow

= 3 + 0.63 year

= 3.63 year.

In the give case management accounting is used to determine the most profitable project which

should be accepted by the company. The company can depend upon any of the factor for

determining the profitability of the factor.

12 | P a g e

fraction of remaining year needed to reach the total cash outflow

= 3 + 0.63 year

= 3.63 year.

In the give case management accounting is used to determine the most profitable project which

should be accepted by the company. The company can depend upon any of the factor for

determining the profitability of the factor.

12 | P a g e

Bibliography

Barman, E., Hall, M. & Millo, Y., 2016. Accounting measurement tools and their impact on.

London: Econstor.

Chiarini, A. & Vagnoni, E., 2014. World-class manufacturing by Fiat. Comparison with Toyota

Production System from a Strategic Management, Management Accounting, Operations

Management and Performance Measurement dimension. International Journal of Production

Research , pp.590-606.

Cooper, D.J., Ezzamel, M. & Qu, S.Q., 2017. Popularizing a Management Accounting Idea: The

Case of the Balanced Scorecard. Wiley online library, pp.991-1025.

Maas, K., Schaltegger, S. & Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, pp.237-48.

Soltani, , Nayebzadeh, & Moeinaddin, , 2014. The Impact Examination of the Techniques of

Management Accounting. International Journal of Academic Research in Accounting, Finance

and Management Sciences, pp.382-89.

13 | P a g e

Barman, E., Hall, M. & Millo, Y., 2016. Accounting measurement tools and their impact on.

London: Econstor.

Chiarini, A. & Vagnoni, E., 2014. World-class manufacturing by Fiat. Comparison with Toyota

Production System from a Strategic Management, Management Accounting, Operations

Management and Performance Measurement dimension. International Journal of Production

Research , pp.590-606.

Cooper, D.J., Ezzamel, M. & Qu, S.Q., 2017. Popularizing a Management Accounting Idea: The

Case of the Balanced Scorecard. Wiley online library, pp.991-1025.

Maas, K., Schaltegger, S. & Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, pp.237-48.

Soltani, , Nayebzadeh, & Moeinaddin, , 2014. The Impact Examination of the Techniques of

Management Accounting. International Journal of Academic Research in Accounting, Finance

and Management Sciences, pp.382-89.

13 | P a g e

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.