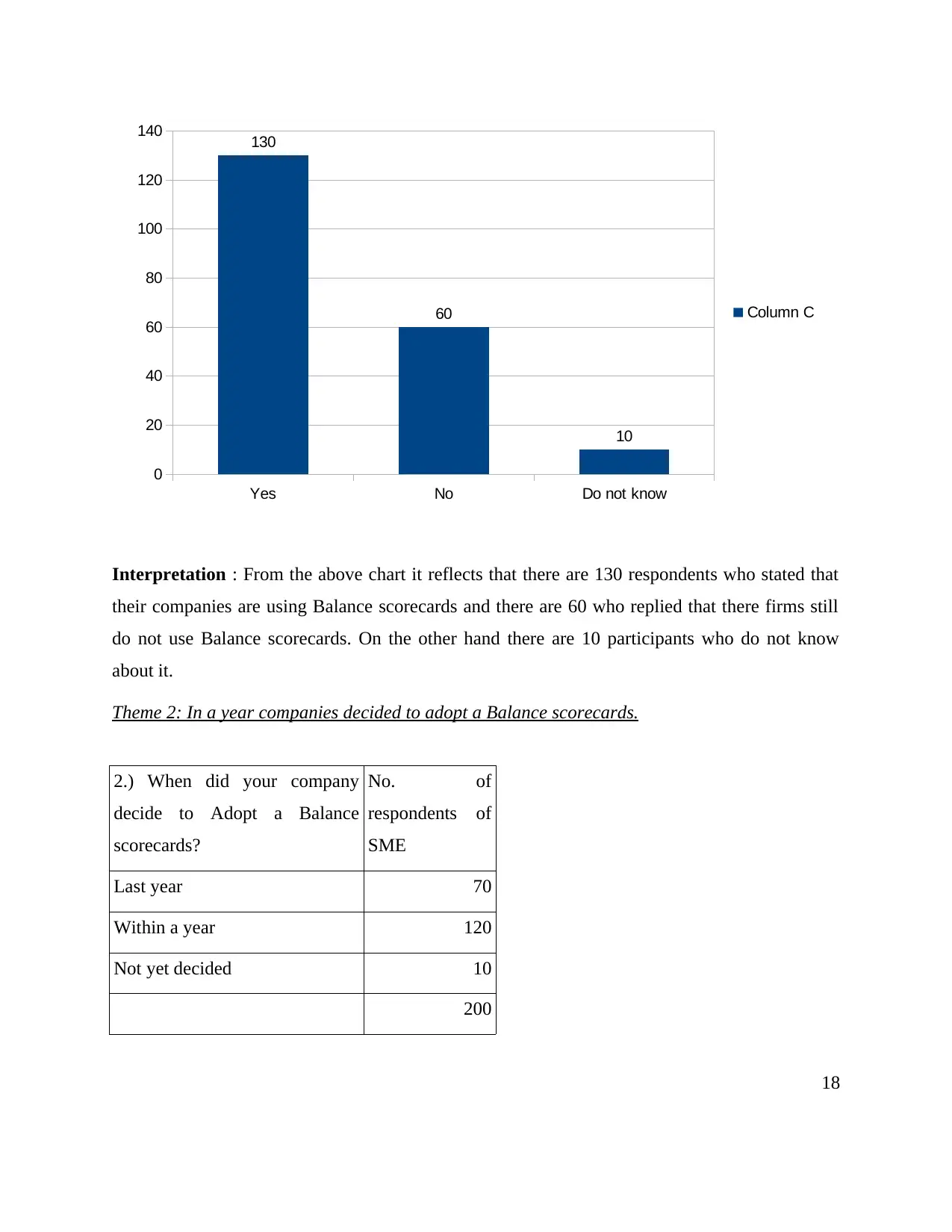

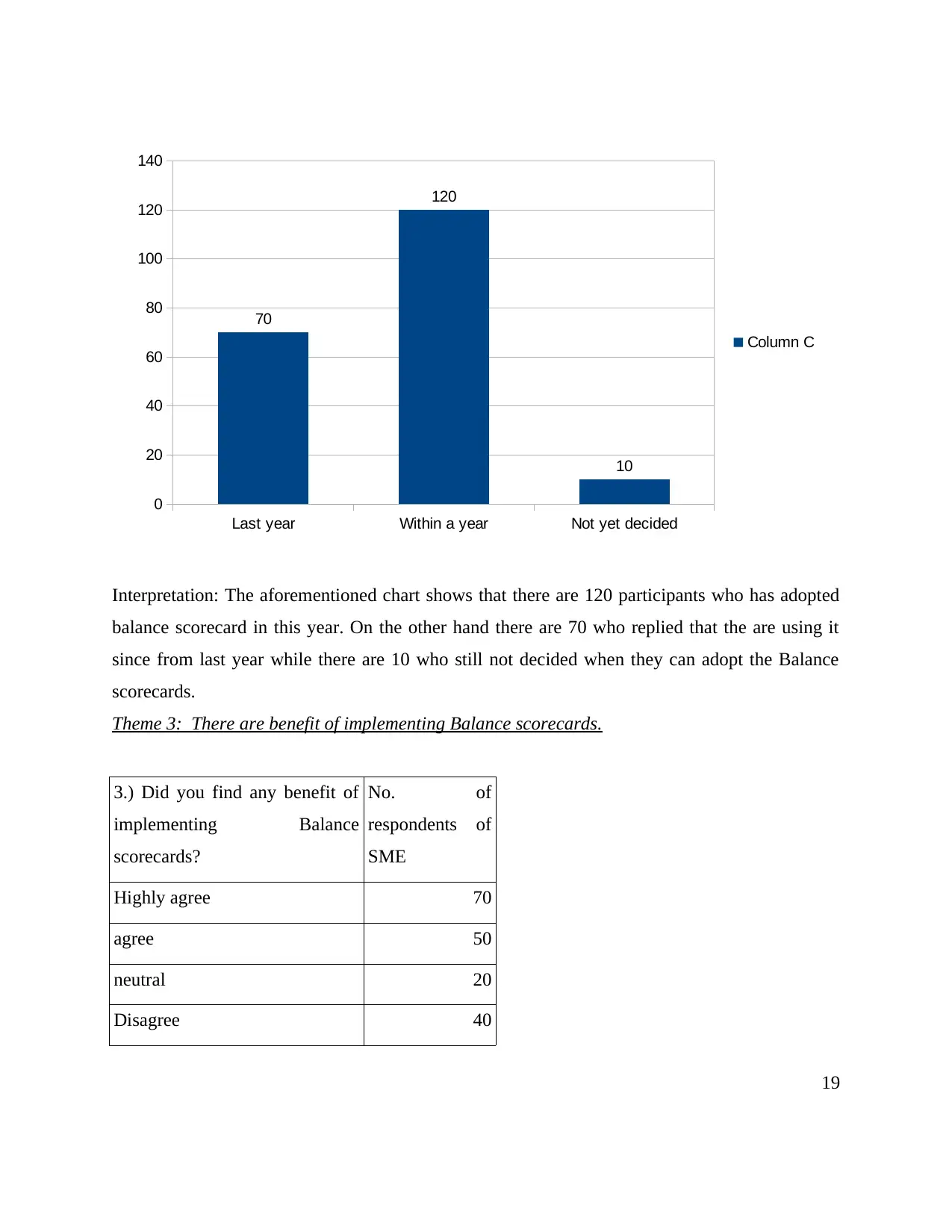

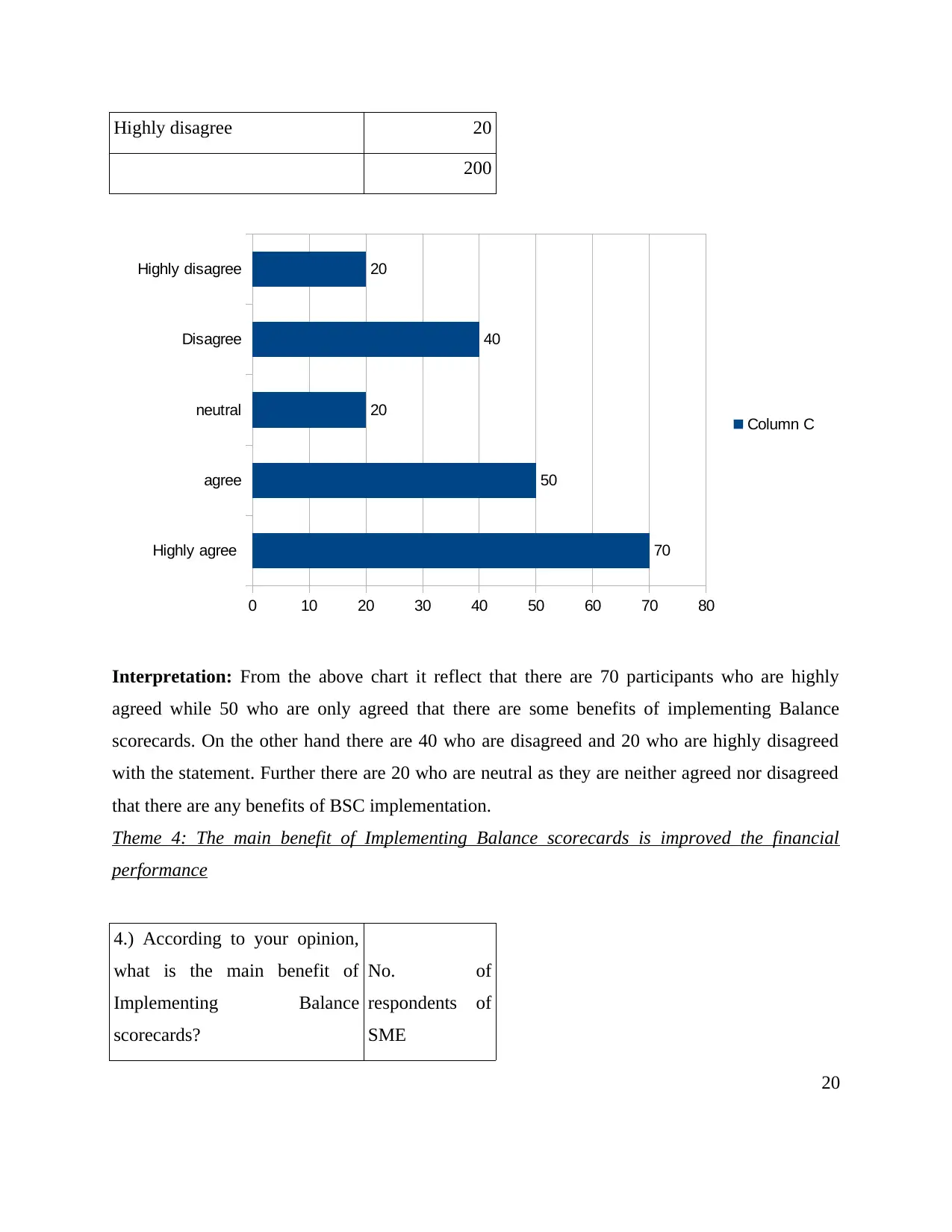

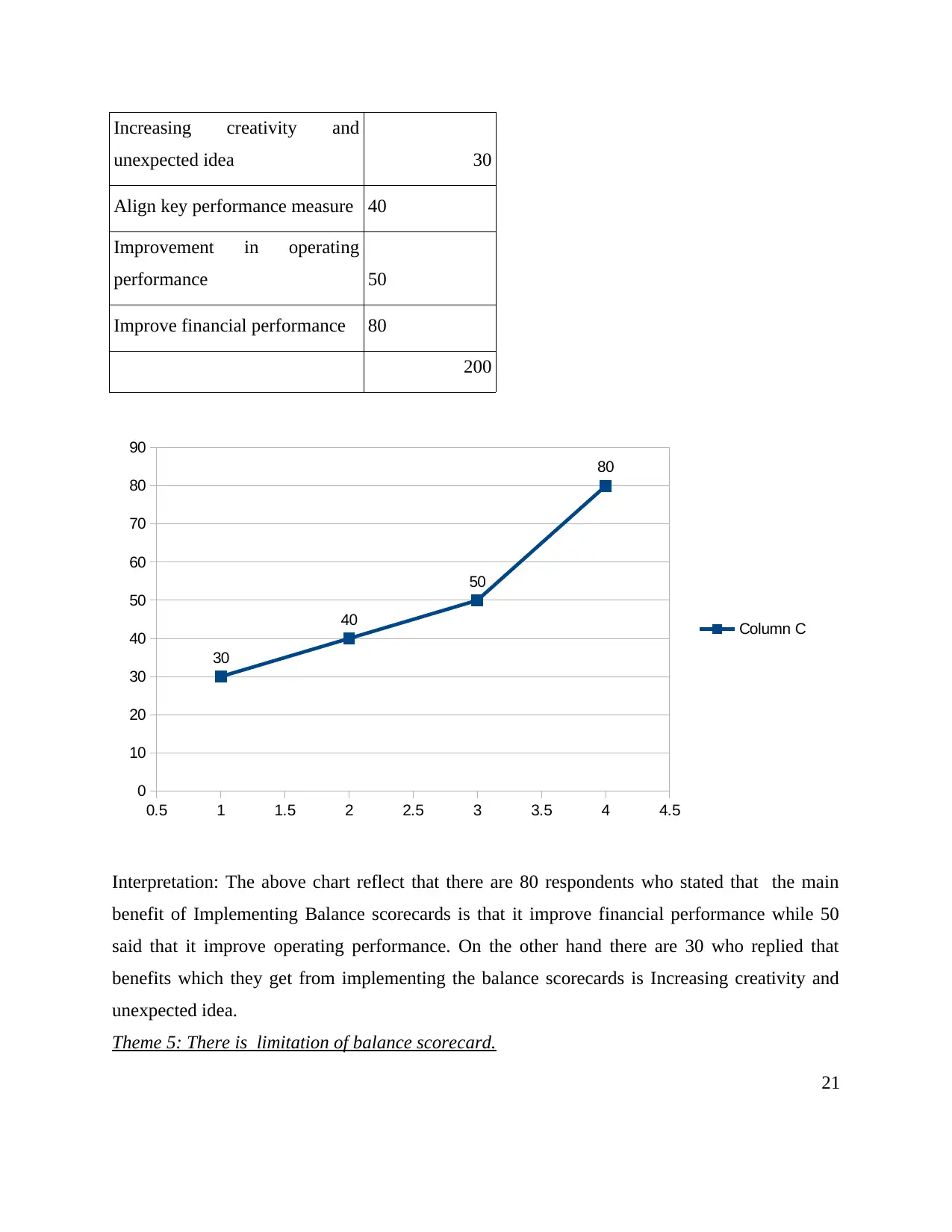

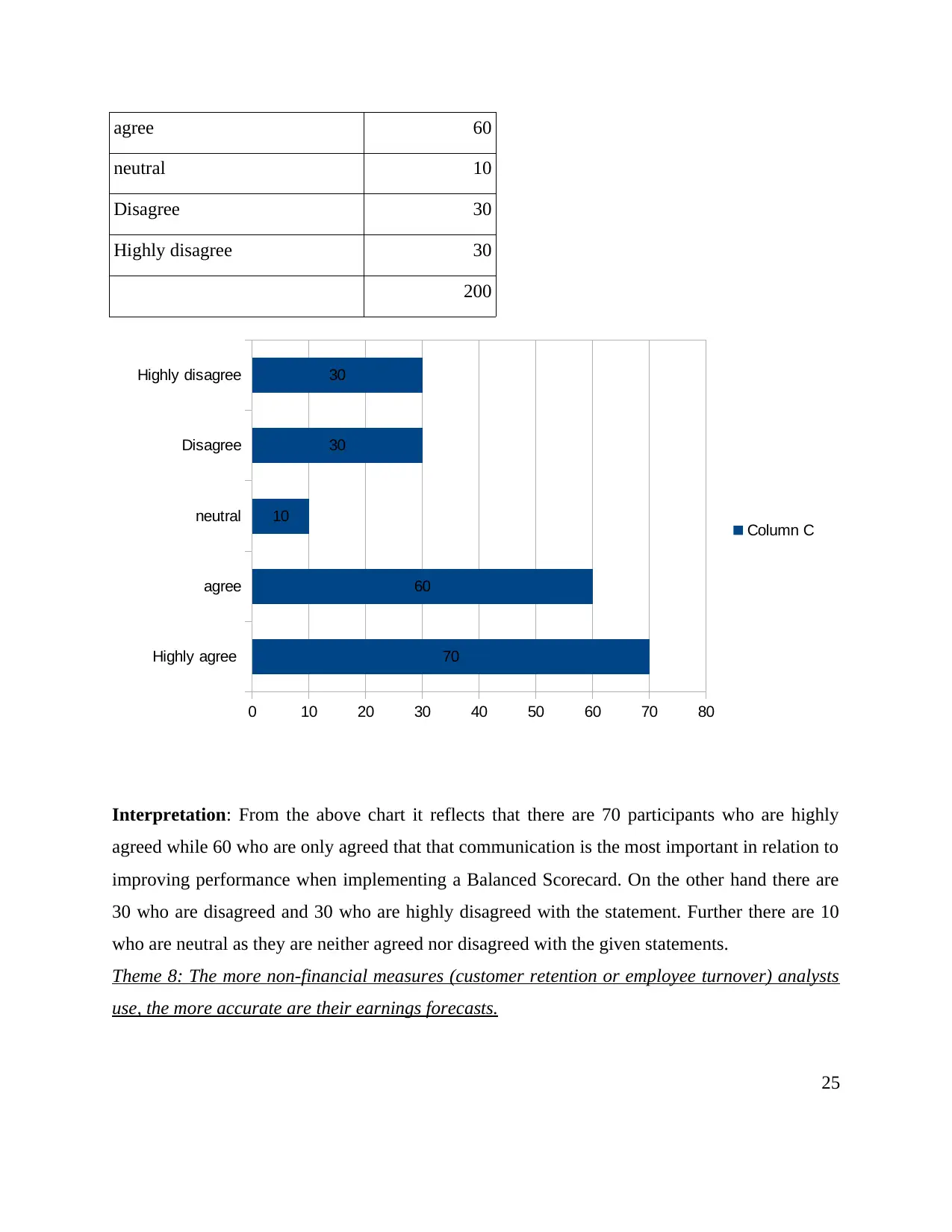

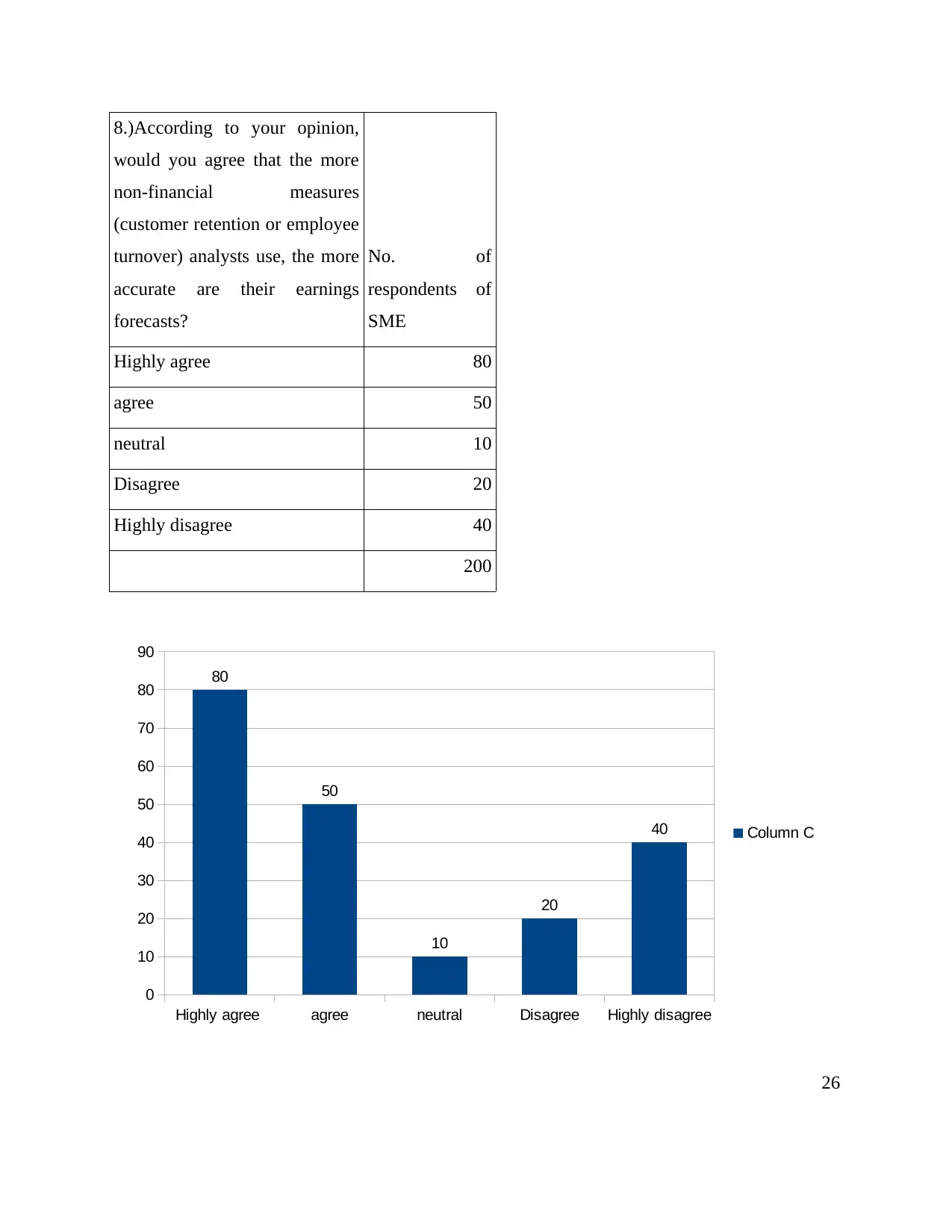

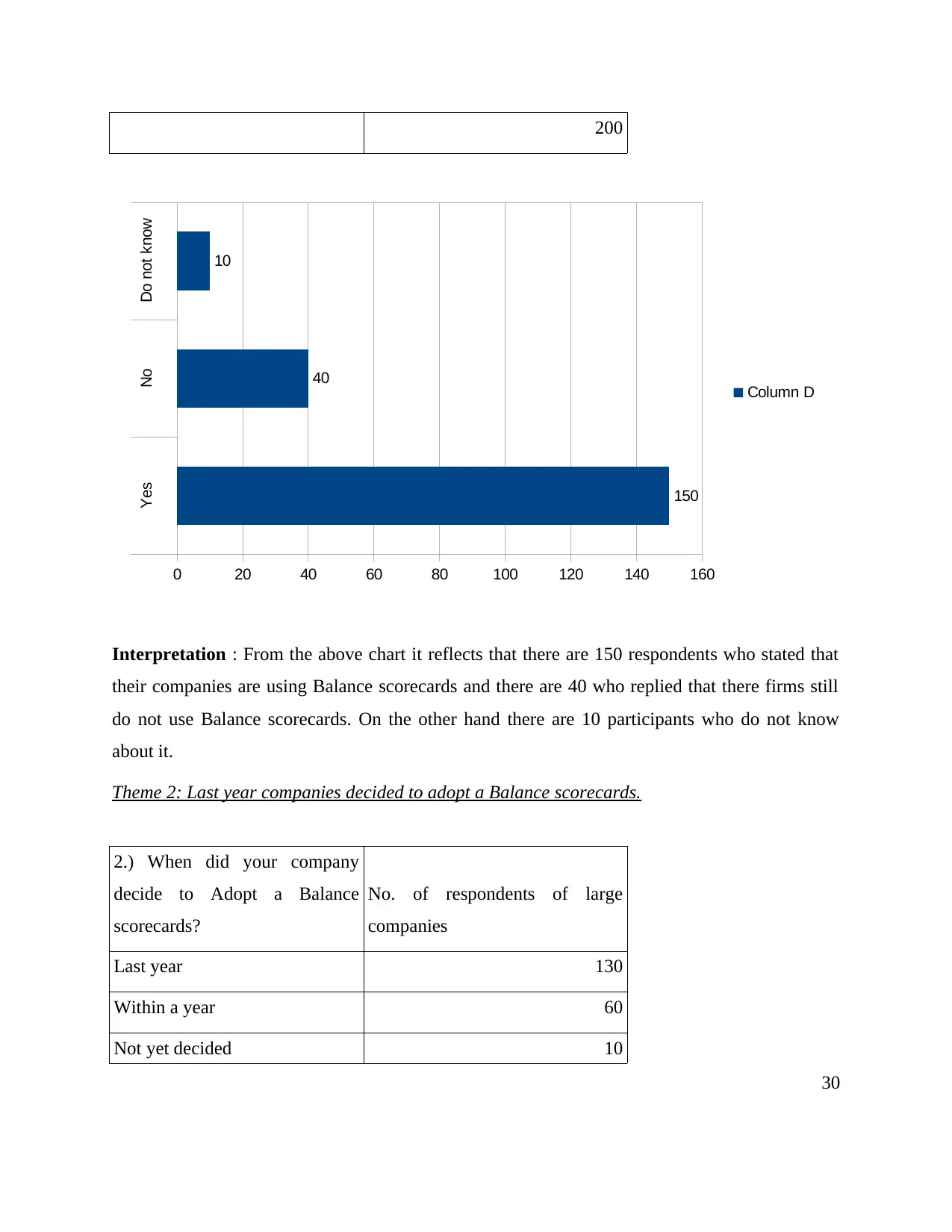

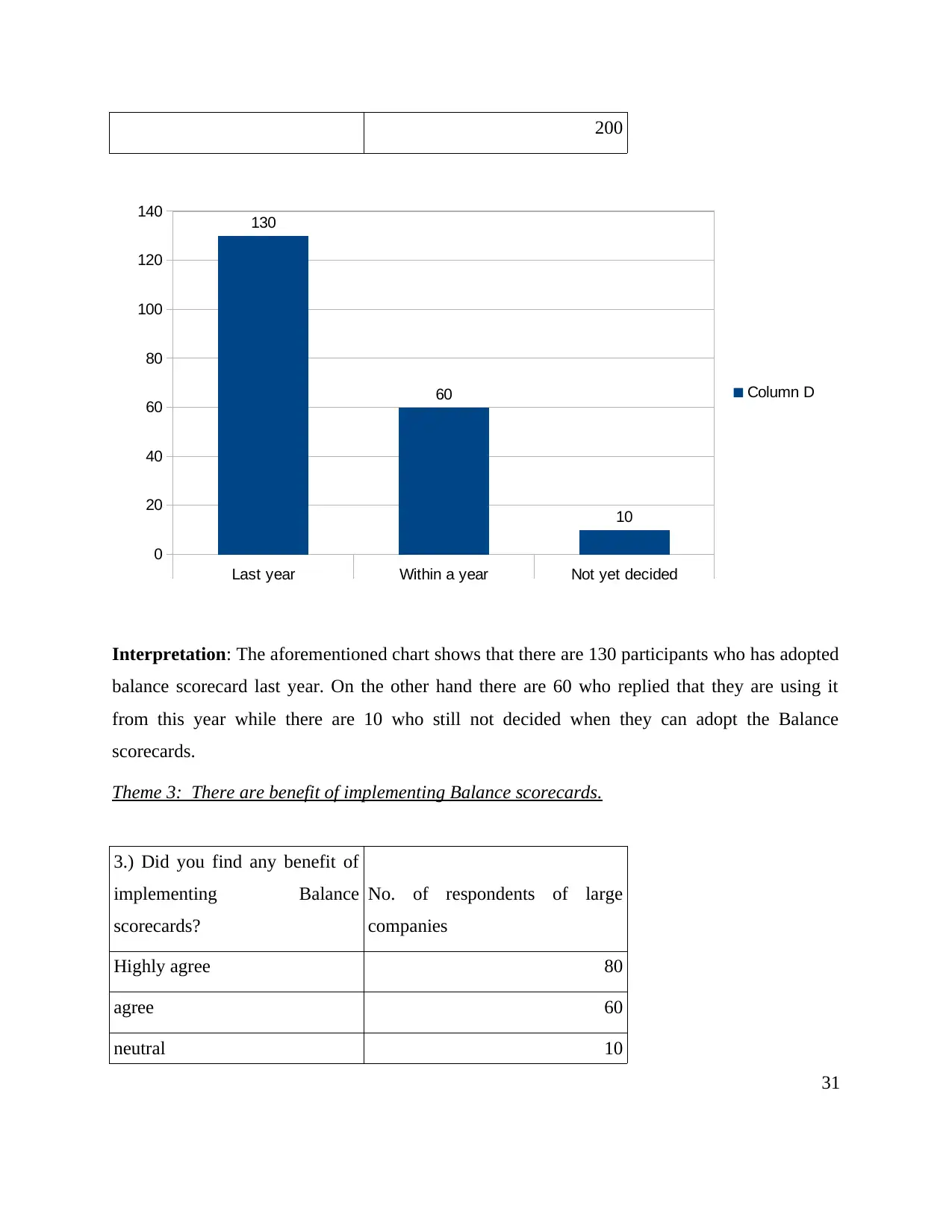

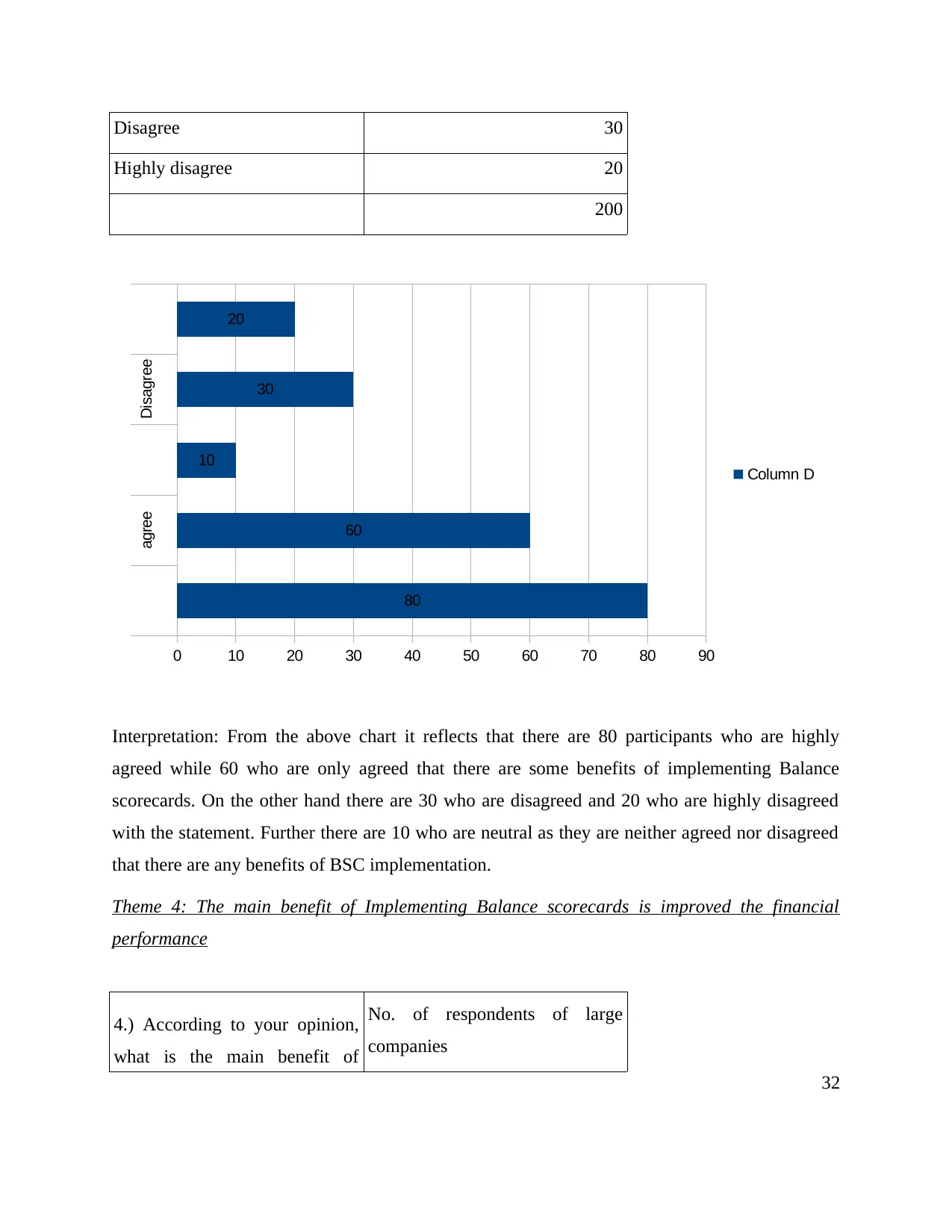

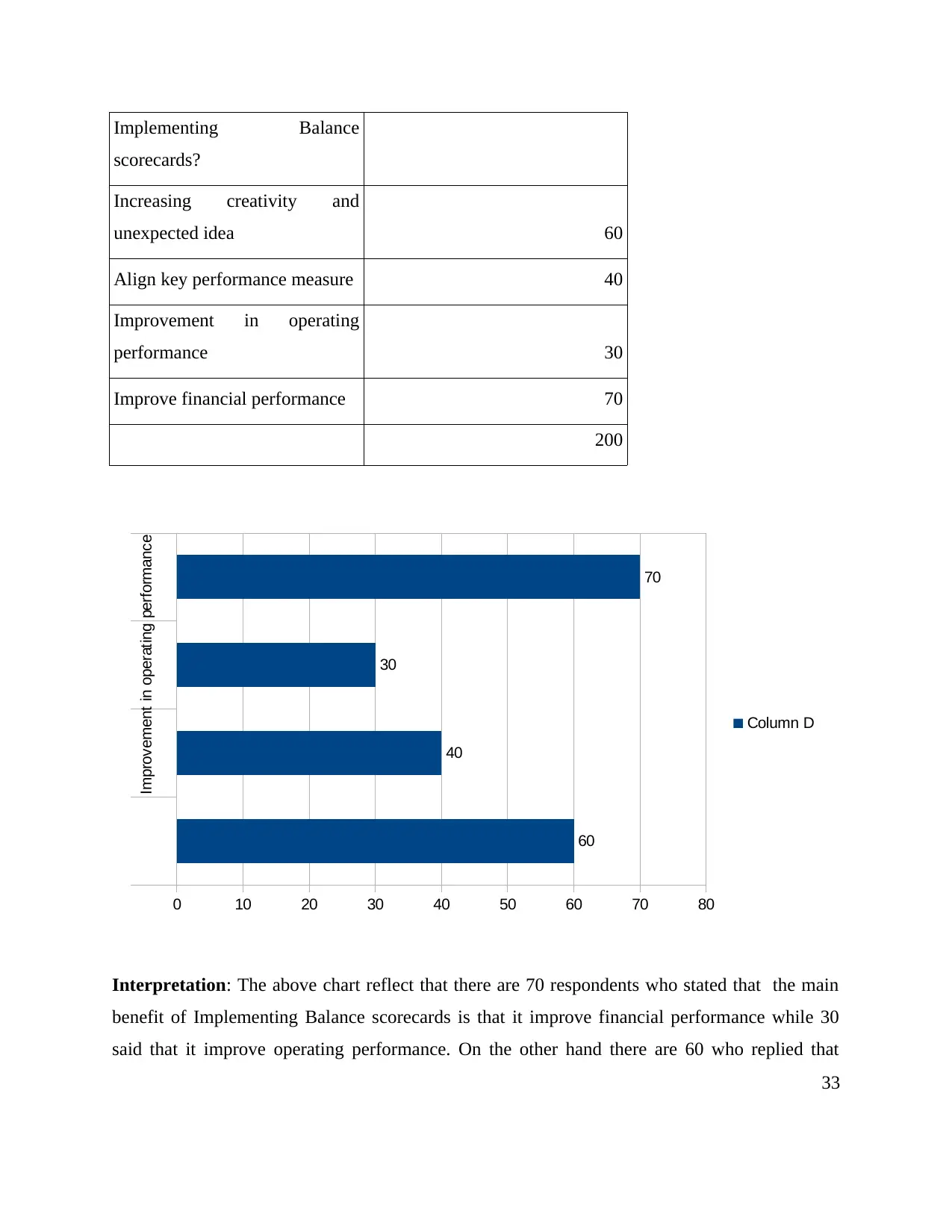

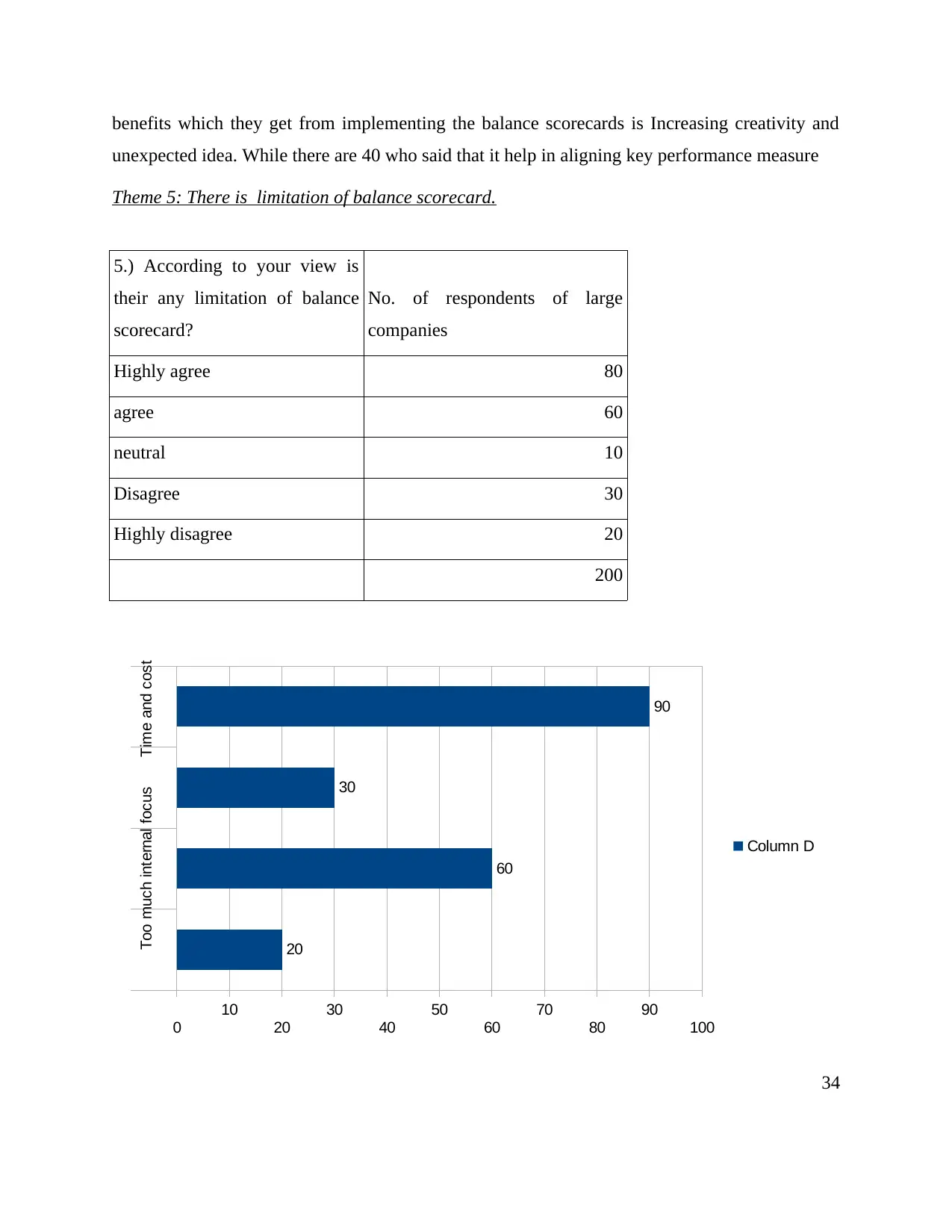

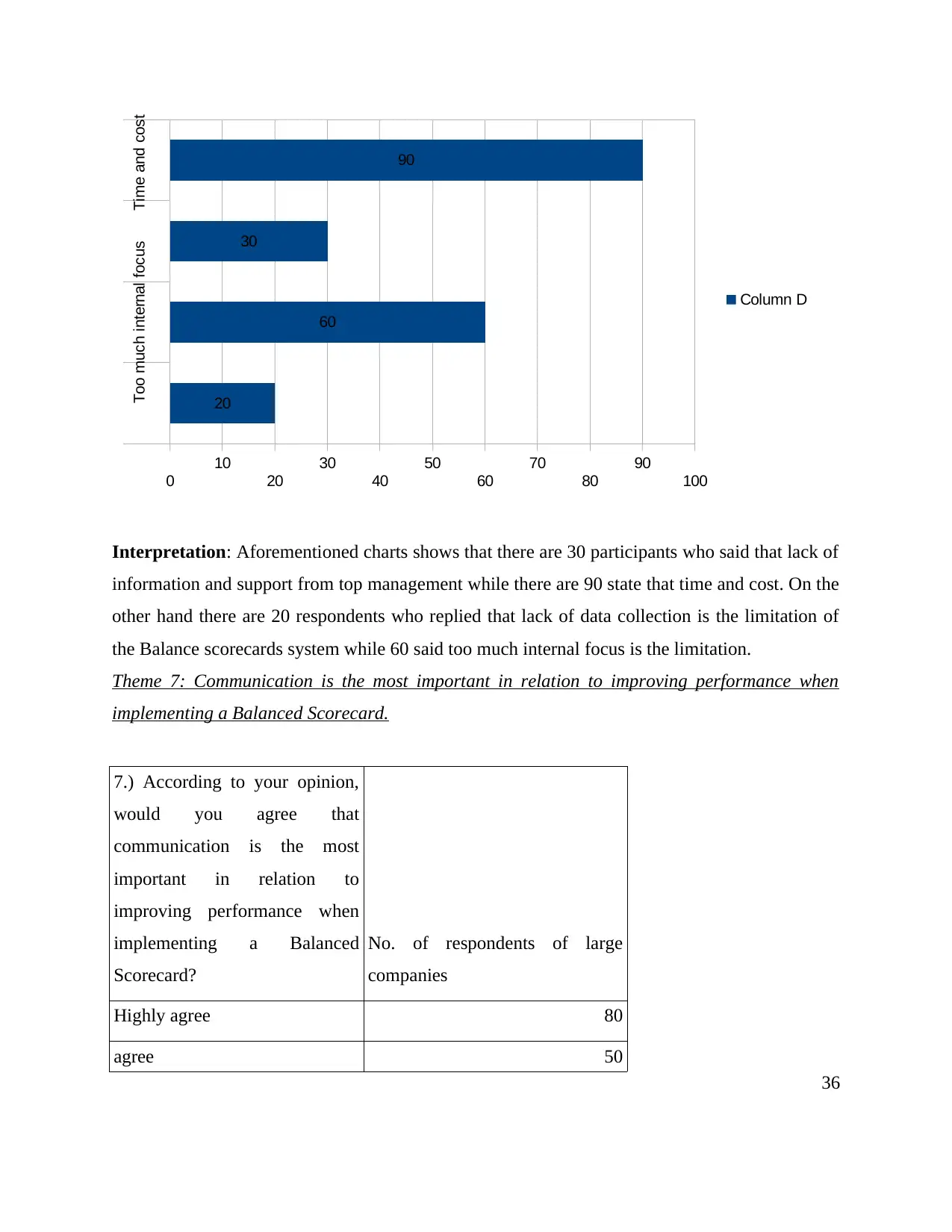

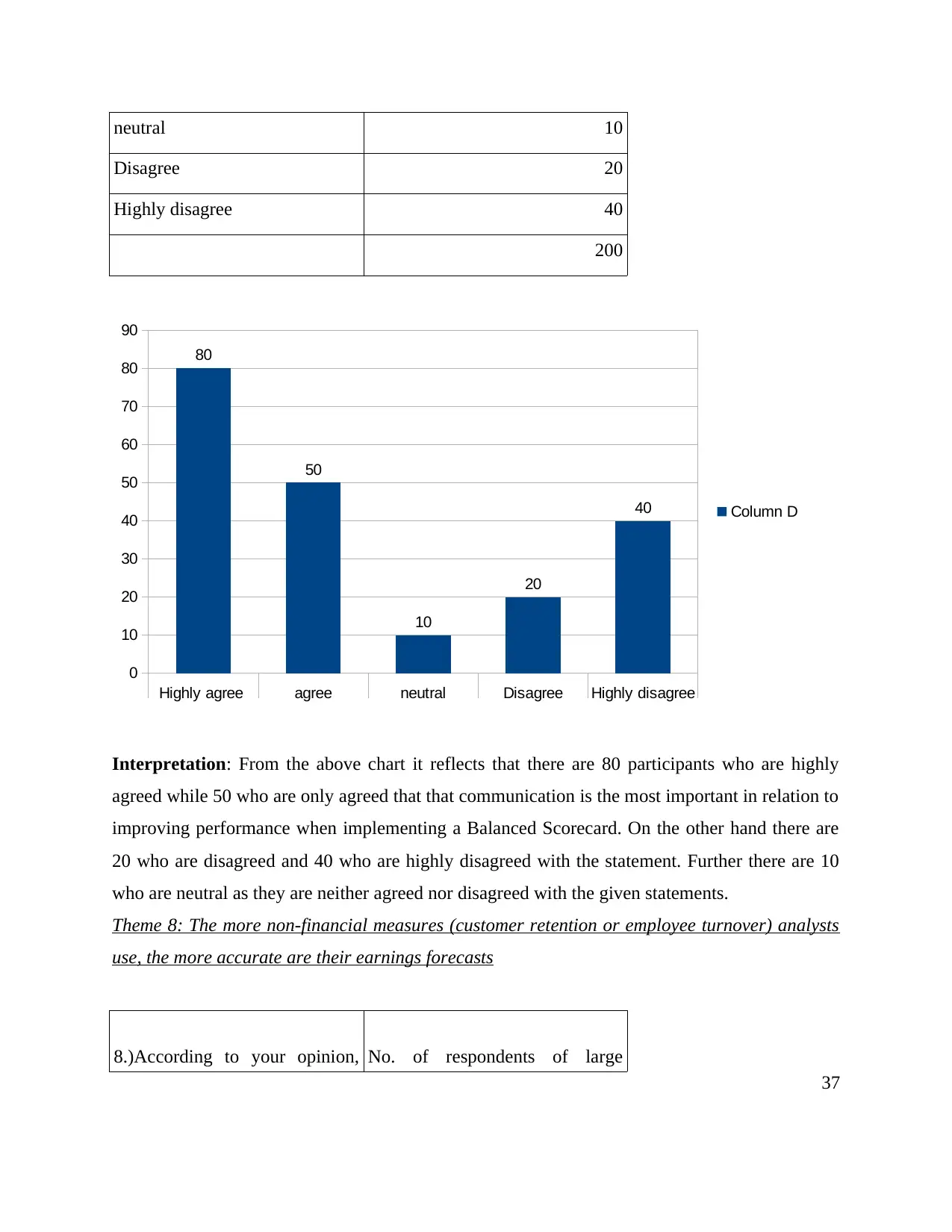

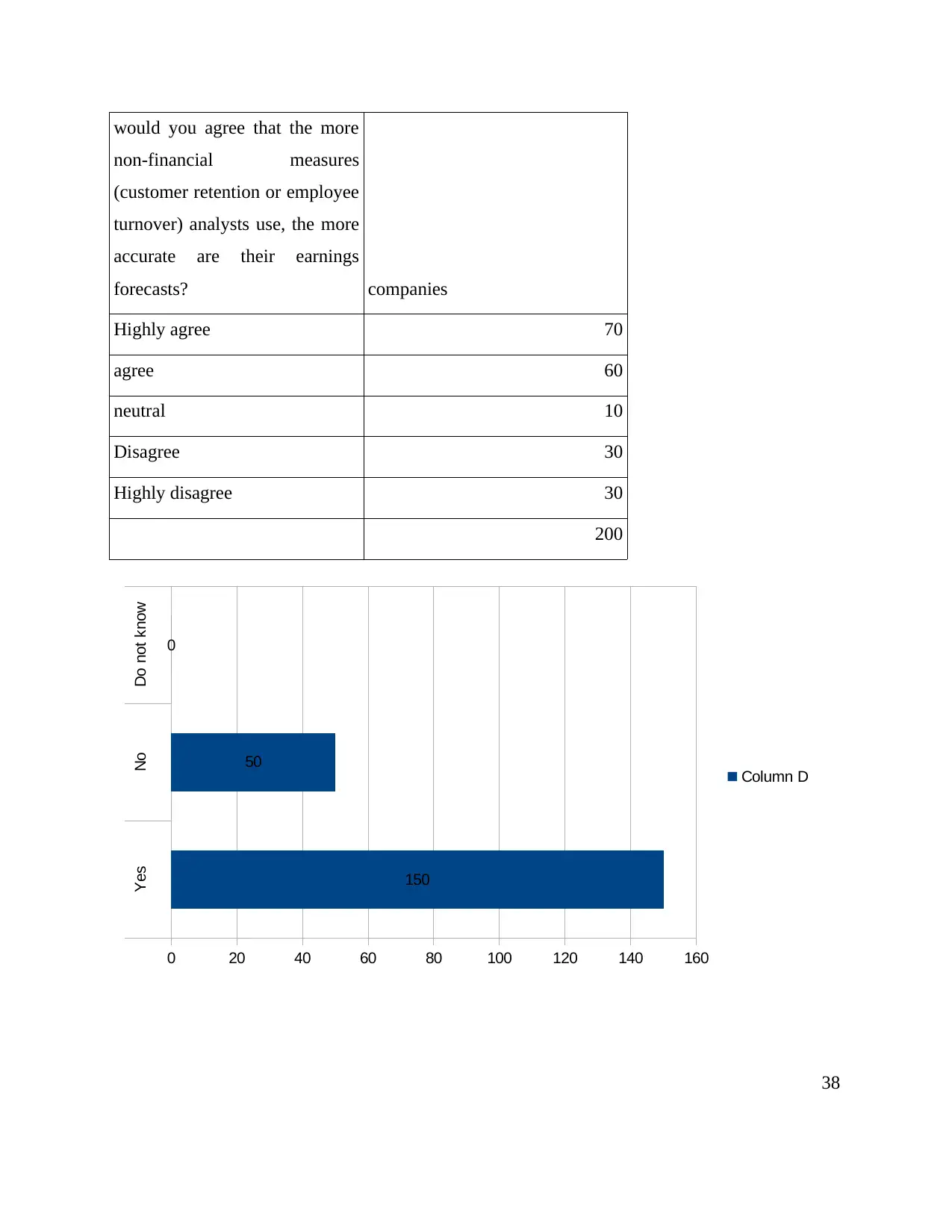

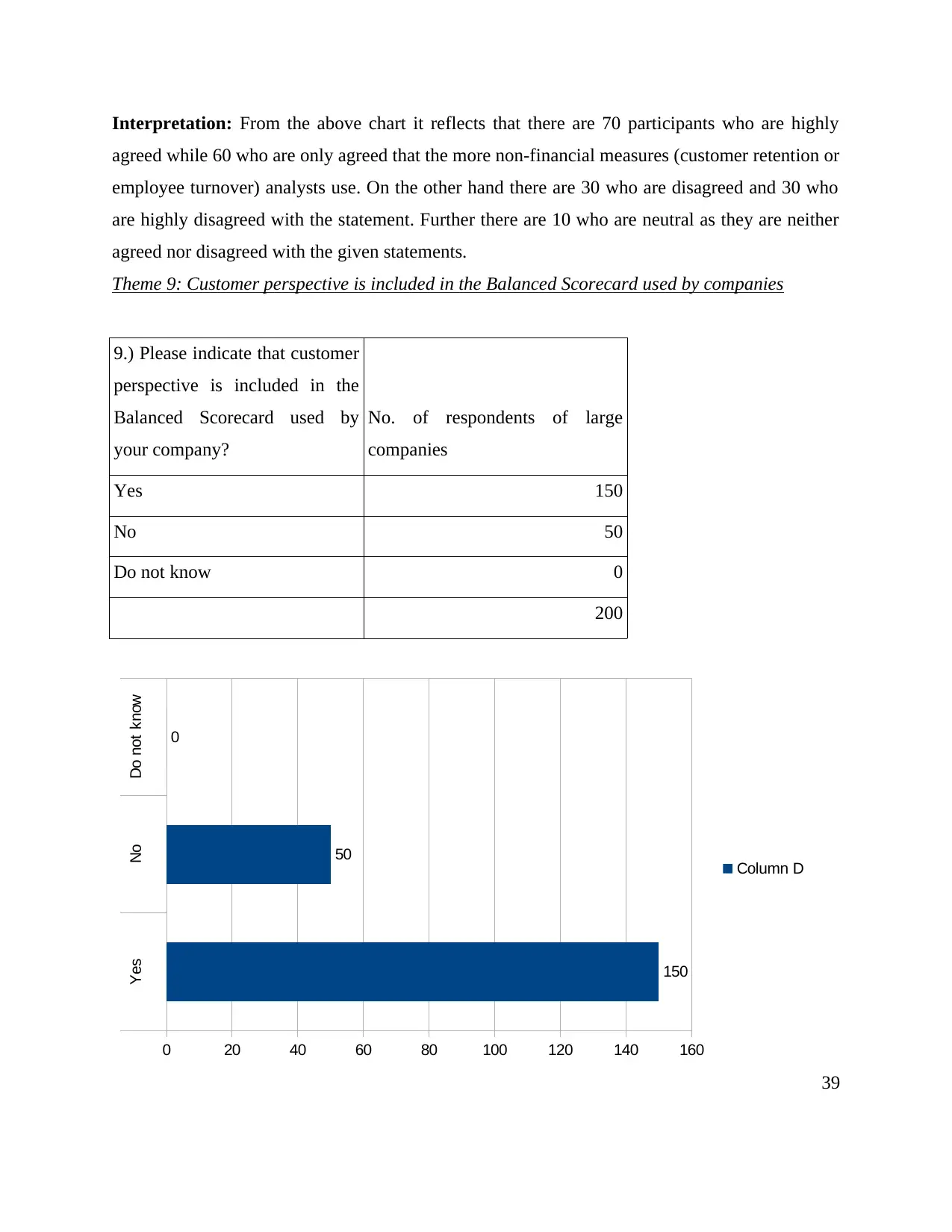

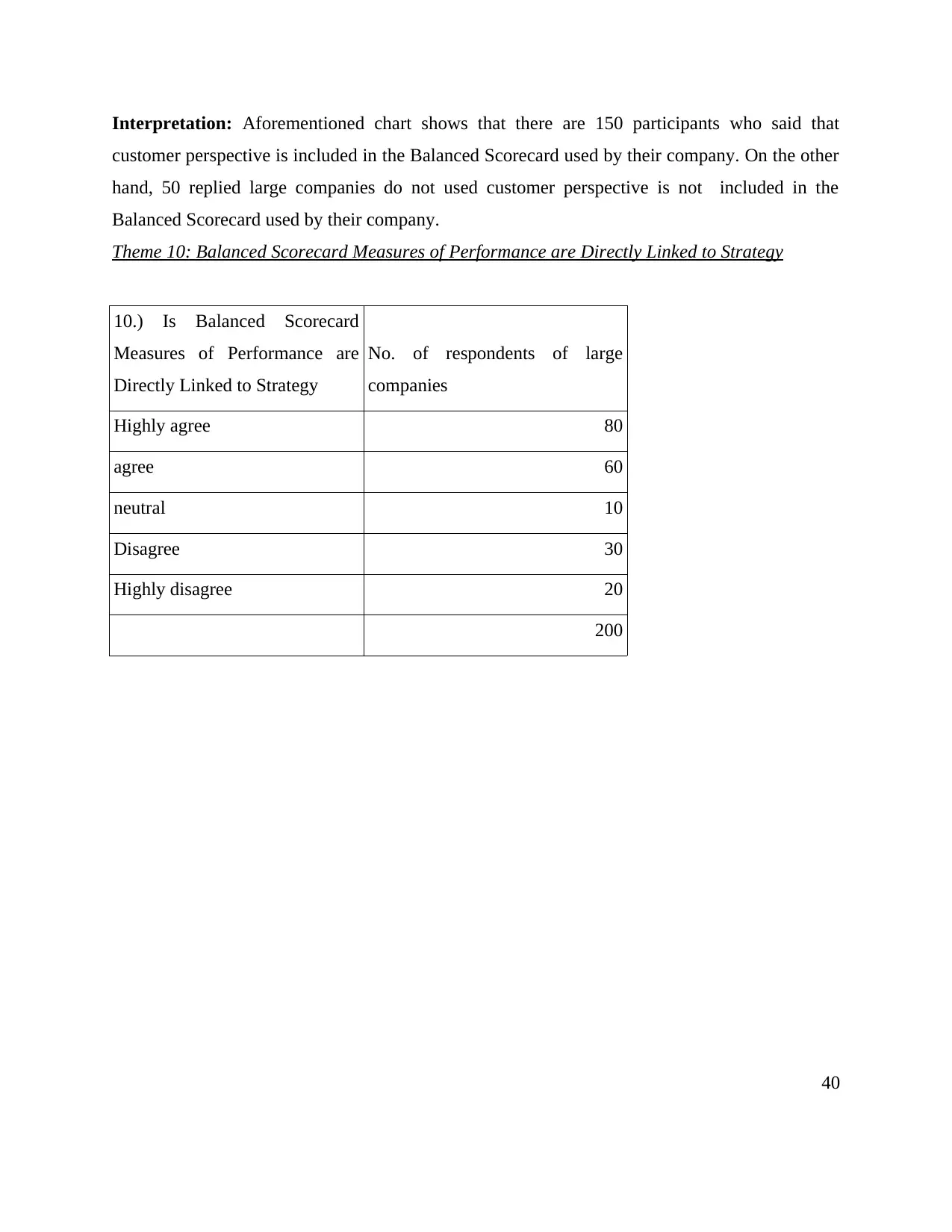

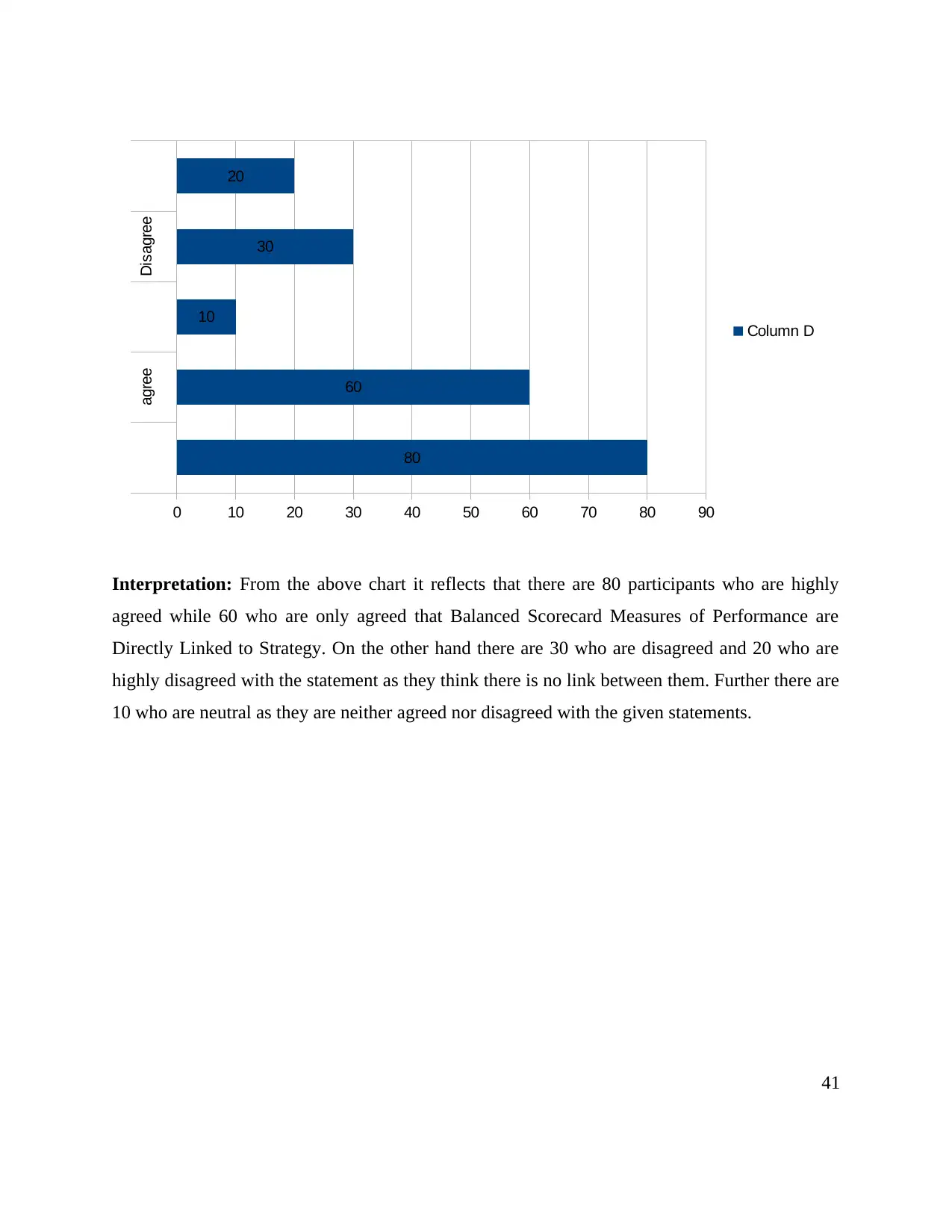

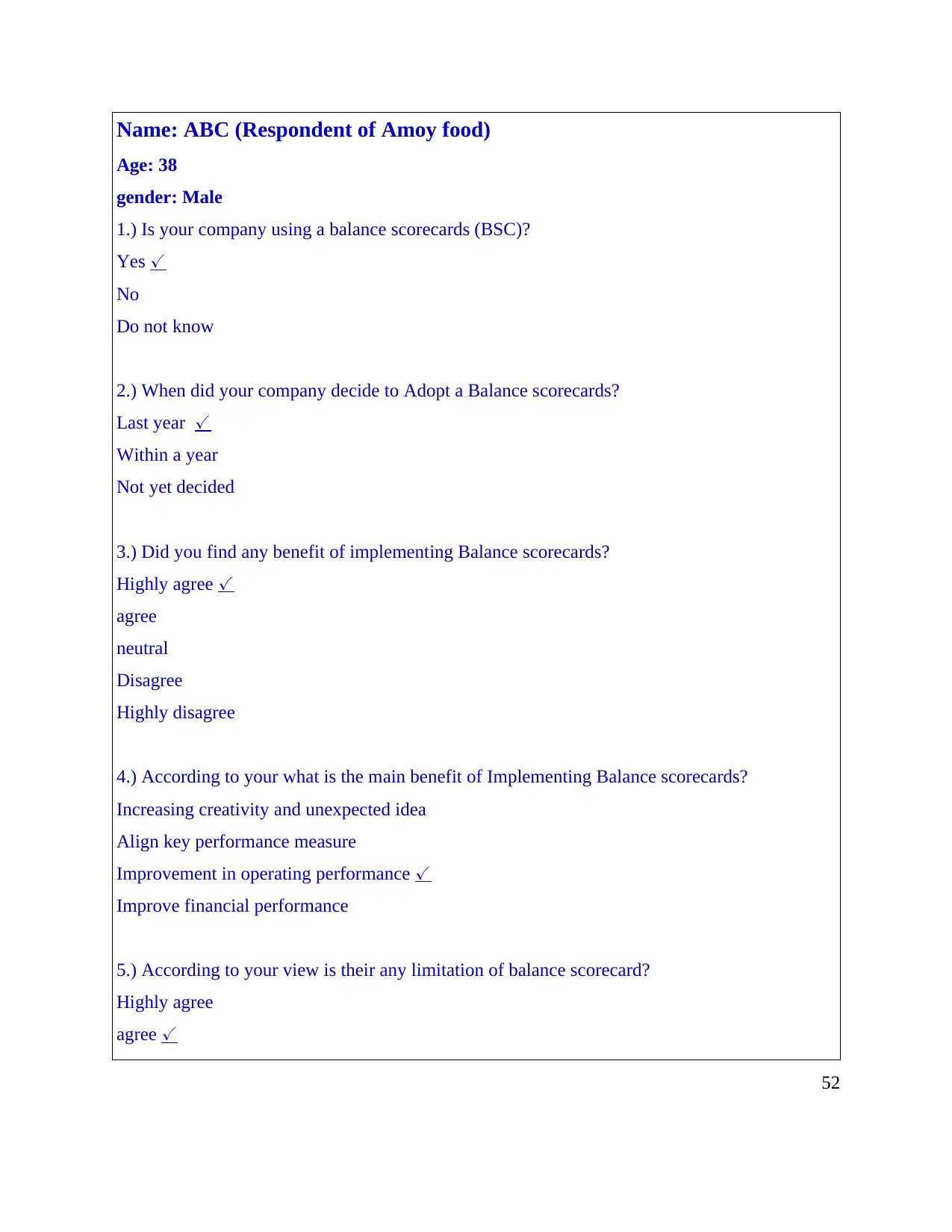

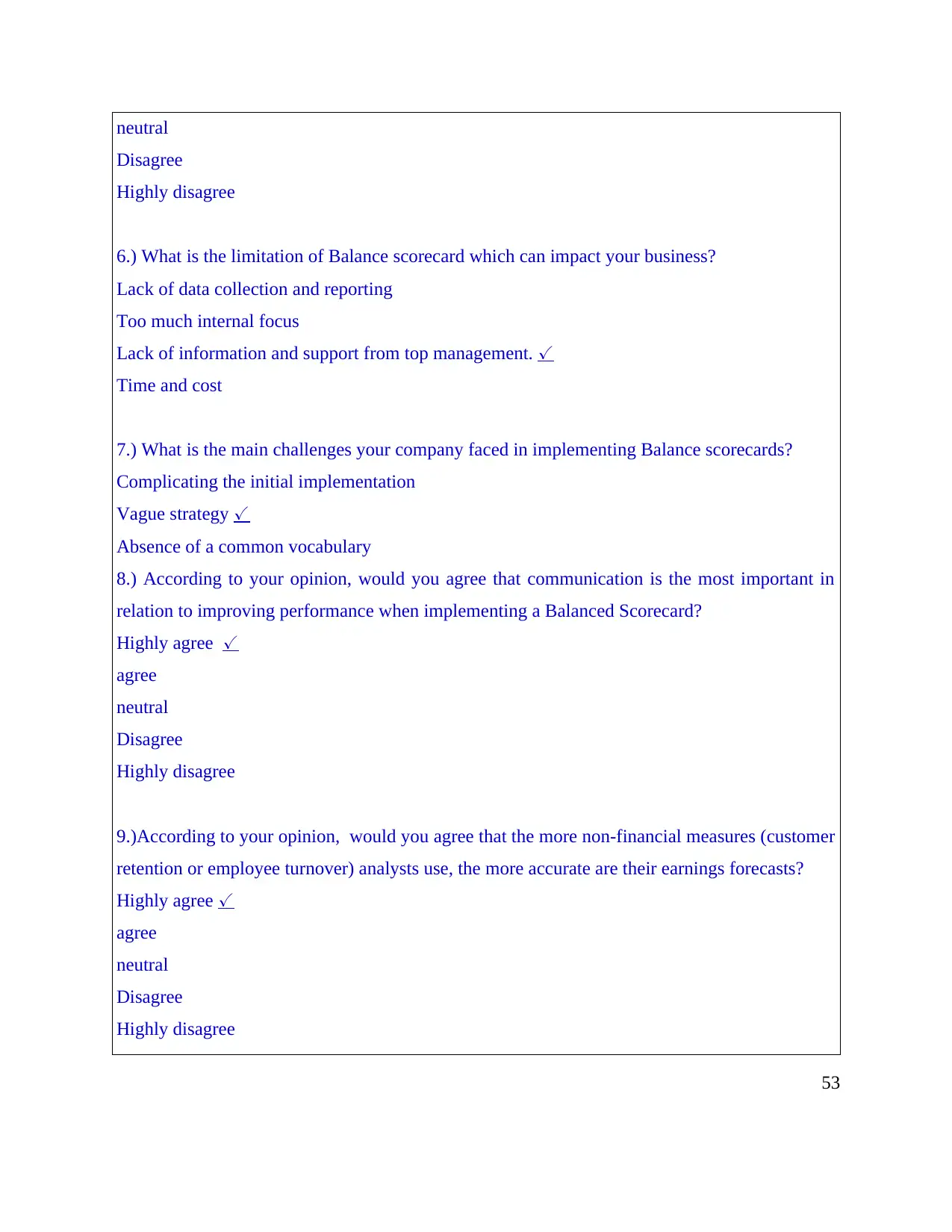

The assignment provided is a study guide on the Balanced Scorecard, a strategic management system that measures an organization's performance from four perspectives: financial, customer, internal processes, and learning and growth. The guide discusses the benefits of implementing a Balanced Scorecard, including increased creativity and unexpected ideas, alignment of key performance measures, improvement in operating performance, and improved financial performance. However, it also highlights limitations such as lack of data collection and reporting, too much internal focus, and lack of information and support from top management. The study guide concludes that effective communication is crucial for improving performance when implementing a Balanced Scorecard, and suggests that using non-financial measures can enhance the accuracy of earnings forecasts.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)