Finance Homework: Adjusting Events, Journal Entries, Tax Calculations

VerifiedAdded on 2020/01/23

|14

|3200

|86

Homework Assignment

AI Summary

This finance assignment presents solutions to several questions related to accounting standards, journal entries, and tax calculations. Question 1 analyzes adjusting and non-adjusting events according to AASB 110, and IAS 10, including scenarios involving stock loss due to fire, share valuation, sale of a business, delivery of goods, and tax fines. Question 2 provides journal entries for Ketchup Ltd, covering share application, allotment, and final call, including underwriting commission and share forfeiture. Question 3 calculates the current tax liability, considering depreciation differences between company accounts and income tax, including deferred tax assets and liabilities for plant, motor vehicles, and prepaid insurance. The assignment offers a comprehensive overview of financial accounting principles.

Finance Questions

03

03

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................2

a) .................................................................................................................................................2

b) .................................................................................................................................................3

c) .................................................................................................................................................3

d) .................................................................................................................................................4

e) .................................................................................................................................................4

QUESTION 2...................................................................................................................................4

QUESTION 3...................................................................................................................................7

b)..................................................................................................................................................9

QUESTION 4...................................................................................................................................9

QUESTION 5.................................................................................................................................12

a) ...............................................................................................................................................12

b) ...............................................................................................................................................14

REFERENCES..............................................................................................................................15

03

QUESTION 1...................................................................................................................................2

a) .................................................................................................................................................2

b) .................................................................................................................................................3

c) .................................................................................................................................................3

d) .................................................................................................................................................4

e) .................................................................................................................................................4

QUESTION 2...................................................................................................................................4

QUESTION 3...................................................................................................................................7

b)..................................................................................................................................................9

QUESTION 4...................................................................................................................................9

QUESTION 5.................................................................................................................................12

a) ...............................................................................................................................................12

b) ...............................................................................................................................................14

REFERENCES..............................................................................................................................15

03

QUESTION 1

a)

According to Accounting standards board 110 which is concerned with all kinds of

transactions or events occurred in the financial statements or business after the reporting period.

There are two kinds of events takes places in the business which needs to be identified by an

entity in order to classify all kinds of transactions such as adjusting events or non-adjusting

events takes places in an entity.

In the give case scenarios, this particular transactions belongs to adjusting events as these

transactions exists in the balance sheet at the end of reporting period at 30 June 2016.

Accounting treatment

Abnormal loss a/c Dr 1750,000

To stock lost due to fire 1750,000

(being stock damaged due to fire transferred to abnormal loss)

Insurer a/c Dr 1500,000

Loss on stock a/c Dr 2,50,000

To night club 1750,000

Bank a/c Dr 1500000

To Insurer 1500000

(being insurance claim received)

Profit entities will use AASB 110 which is concerns with considering all the events

occurring after the reporting period. This standard says that any event whether favorable or

unfavorable occurred after reporting period or before finalization of balance sheet which in the

current case fire destroy the stock on 25th August 2016. This transaction is related to non-

adjusting event as conditions lies initially in the business that this particular transactions will

occur in the future are regarded as the non-adjusting events. The reason behind taking these

transactions as non-adjusting event as this reduces the fair market value between the end of the

reporting period.

03

a)

According to Accounting standards board 110 which is concerned with all kinds of

transactions or events occurred in the financial statements or business after the reporting period.

There are two kinds of events takes places in the business which needs to be identified by an

entity in order to classify all kinds of transactions such as adjusting events or non-adjusting

events takes places in an entity.

In the give case scenarios, this particular transactions belongs to adjusting events as these

transactions exists in the balance sheet at the end of reporting period at 30 June 2016.

Accounting treatment

Abnormal loss a/c Dr 1750,000

To stock lost due to fire 1750,000

(being stock damaged due to fire transferred to abnormal loss)

Insurer a/c Dr 1500,000

Loss on stock a/c Dr 2,50,000

To night club 1750,000

Bank a/c Dr 1500000

To Insurer 1500000

(being insurance claim received)

Profit entities will use AASB 110 which is concerns with considering all the events

occurring after the reporting period. This standard says that any event whether favorable or

unfavorable occurred after reporting period or before finalization of balance sheet which in the

current case fire destroy the stock on 25th August 2016. This transaction is related to non-

adjusting event as conditions lies initially in the business that this particular transactions will

occur in the future are regarded as the non-adjusting events. The reason behind taking these

transactions as non-adjusting event as this reduces the fair market value between the end of the

reporting period.

03

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

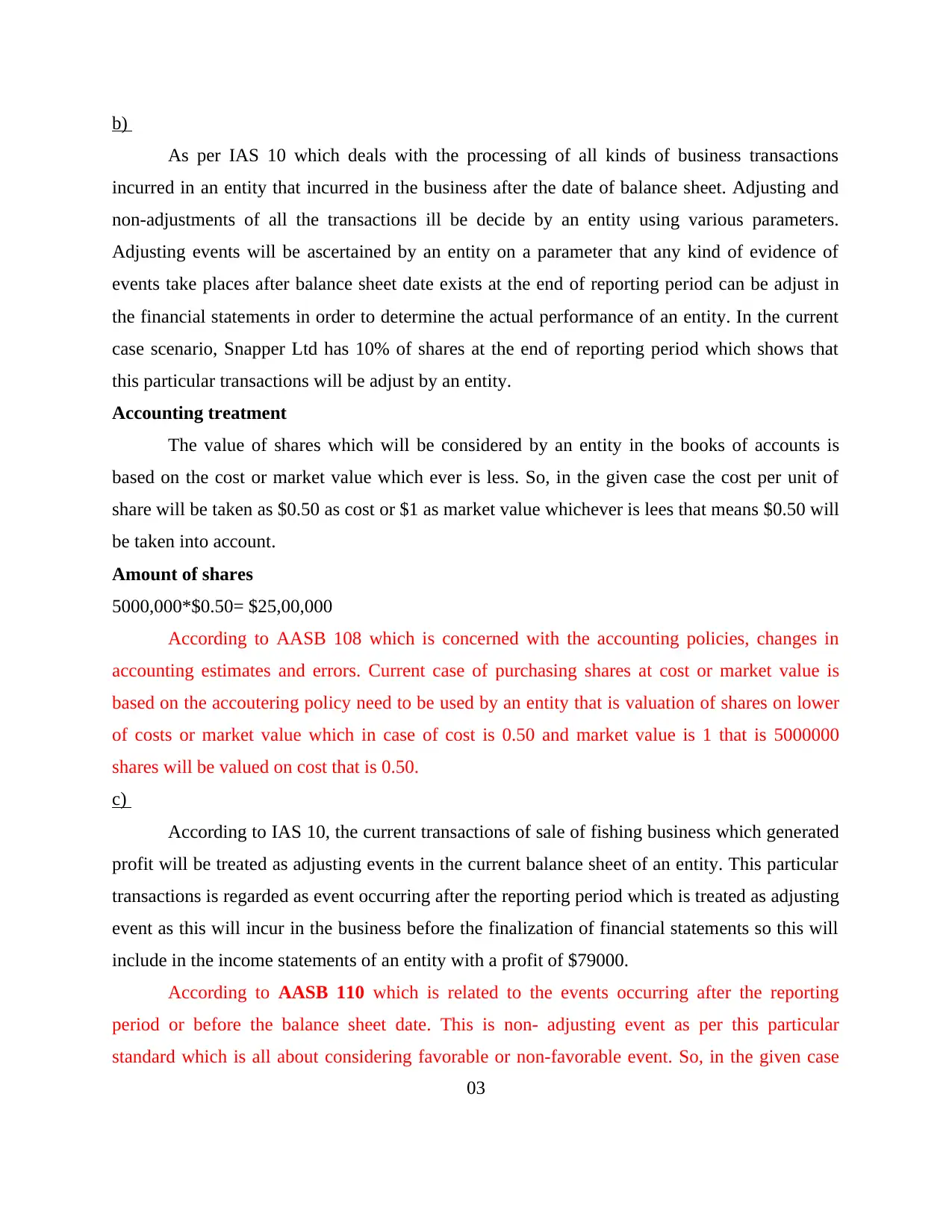

b)

As per IAS 10 which deals with the processing of all kinds of business transactions

incurred in an entity that incurred in the business after the date of balance sheet. Adjusting and

non-adjustments of all the transactions ill be decide by an entity using various parameters.

Adjusting events will be ascertained by an entity on a parameter that any kind of evidence of

events take places after balance sheet date exists at the end of reporting period can be adjust in

the financial statements in order to determine the actual performance of an entity. In the current

case scenario, Snapper Ltd has 10% of shares at the end of reporting period which shows that

this particular transactions will be adjust by an entity.

Accounting treatment

The value of shares which will be considered by an entity in the books of accounts is

based on the cost or market value which ever is less. So, in the given case the cost per unit of

share will be taken as $0.50 as cost or $1 as market value whichever is lees that means $0.50 will

be taken into account.

Amount of shares

5000,000*$0.50= $25,00,000

According to AASB 108 which is concerned with the accounting policies, changes in

accounting estimates and errors. Current case of purchasing shares at cost or market value is

based on the accoutering policy need to be used by an entity that is valuation of shares on lower

of costs or market value which in case of cost is 0.50 and market value is 1 that is 5000000

shares will be valued on cost that is 0.50.

c)

According to IAS 10, the current transactions of sale of fishing business which generated

profit will be treated as adjusting events in the current balance sheet of an entity. This particular

transactions is regarded as event occurring after the reporting period which is treated as adjusting

event as this will incur in the business before the finalization of financial statements so this will

include in the income statements of an entity with a profit of $79000.

According to AASB 110 which is related to the events occurring after the reporting

period or before the balance sheet date. This is non- adjusting event as per this particular

standard which is all about considering favorable or non-favorable event. So, in the given case

03

As per IAS 10 which deals with the processing of all kinds of business transactions

incurred in an entity that incurred in the business after the date of balance sheet. Adjusting and

non-adjustments of all the transactions ill be decide by an entity using various parameters.

Adjusting events will be ascertained by an entity on a parameter that any kind of evidence of

events take places after balance sheet date exists at the end of reporting period can be adjust in

the financial statements in order to determine the actual performance of an entity. In the current

case scenario, Snapper Ltd has 10% of shares at the end of reporting period which shows that

this particular transactions will be adjust by an entity.

Accounting treatment

The value of shares which will be considered by an entity in the books of accounts is

based on the cost or market value which ever is less. So, in the given case the cost per unit of

share will be taken as $0.50 as cost or $1 as market value whichever is lees that means $0.50 will

be taken into account.

Amount of shares

5000,000*$0.50= $25,00,000

According to AASB 108 which is concerned with the accounting policies, changes in

accounting estimates and errors. Current case of purchasing shares at cost or market value is

based on the accoutering policy need to be used by an entity that is valuation of shares on lower

of costs or market value which in case of cost is 0.50 and market value is 1 that is 5000000

shares will be valued on cost that is 0.50.

c)

According to IAS 10, the current transactions of sale of fishing business which generated

profit will be treated as adjusting events in the current balance sheet of an entity. This particular

transactions is regarded as event occurring after the reporting period which is treated as adjusting

event as this will incur in the business before the finalization of financial statements so this will

include in the income statements of an entity with a profit of $79000.

According to AASB 110 which is related to the events occurring after the reporting

period or before the balance sheet date. This is non- adjusting event as per this particular

standard which is all about considering favorable or non-favorable event. So, in the given case

03

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

scenario profit generated from the sale of transaction on 5 August are regarded as favorably

adjusting event.

d)

It is regarded as the adjusting event as this particular transactions incurred in the business

as the end of reporting period that is evident that delivery of goods will take places in June and

invoice received on August before finalization of financial statements.

Accounting treatment of the above mention transactions is that invoice of goods received

is of $85000 will be shown in trade receivables and on the other hand $100000 will be treated as

closing stock that will be recorded in the balance sheet as the closing stock incurred in the

business.

It is regarded as the adjusting transactions as this falls under AASB 101 which is

concerned with the presentation of financial statements. The invoice received to company for the

goods delivered in June is regarded as the forward contract. The value of closing stock is

estimated as 100000 as the difference arises of 15000 will be taken into consideration as it is

adjusting events takes places in an entity.

e)

It is adjusting event as the charging of fine for not filing income tax return by an

individual for the previous year 2015 by the assessing officer of Australian taxation officer is of

$55000. It is evident from the above that discrepancy found in the fine charge by the authority at

the end of reporting period that is 30 June 2016 which ascertain the overall status of events

incurred in the business that is to be consider by an entity as adjusting or non-adjusting event for

improving existing business performance of an entity. On later date that is on 12 August fine

charged revised from $55000 to $5000 will be considered by an entity in the books of accounts

in order to reduce the current amount of taxation incurred in the business.

It is related with the AASB 1054, which is concerned with the additional disclosures

made by an entity when sudden facts and figures discovered in the business. This is adjusting

event according to this particular accounting standards. In the current case scenario, wrong

determination of tax by Australian tax officer will affect the condition of an entity as this is

regarded as the material effect. This material effect will be attached at the end of the nonracial

statements as disclosures to accounts for the revision of tax amount from 55000 to 5000.

03

adjusting event.

d)

It is regarded as the adjusting event as this particular transactions incurred in the business

as the end of reporting period that is evident that delivery of goods will take places in June and

invoice received on August before finalization of financial statements.

Accounting treatment of the above mention transactions is that invoice of goods received

is of $85000 will be shown in trade receivables and on the other hand $100000 will be treated as

closing stock that will be recorded in the balance sheet as the closing stock incurred in the

business.

It is regarded as the adjusting transactions as this falls under AASB 101 which is

concerned with the presentation of financial statements. The invoice received to company for the

goods delivered in June is regarded as the forward contract. The value of closing stock is

estimated as 100000 as the difference arises of 15000 will be taken into consideration as it is

adjusting events takes places in an entity.

e)

It is adjusting event as the charging of fine for not filing income tax return by an

individual for the previous year 2015 by the assessing officer of Australian taxation officer is of

$55000. It is evident from the above that discrepancy found in the fine charge by the authority at

the end of reporting period that is 30 June 2016 which ascertain the overall status of events

incurred in the business that is to be consider by an entity as adjusting or non-adjusting event for

improving existing business performance of an entity. On later date that is on 12 August fine

charged revised from $55000 to $5000 will be considered by an entity in the books of accounts

in order to reduce the current amount of taxation incurred in the business.

It is related with the AASB 1054, which is concerned with the additional disclosures

made by an entity when sudden facts and figures discovered in the business. This is adjusting

event according to this particular accounting standards. In the current case scenario, wrong

determination of tax by Australian tax officer will affect the condition of an entity as this is

regarded as the material effect. This material effect will be attached at the end of the nonracial

statements as disclosures to accounts for the revision of tax amount from 55000 to 5000.

03

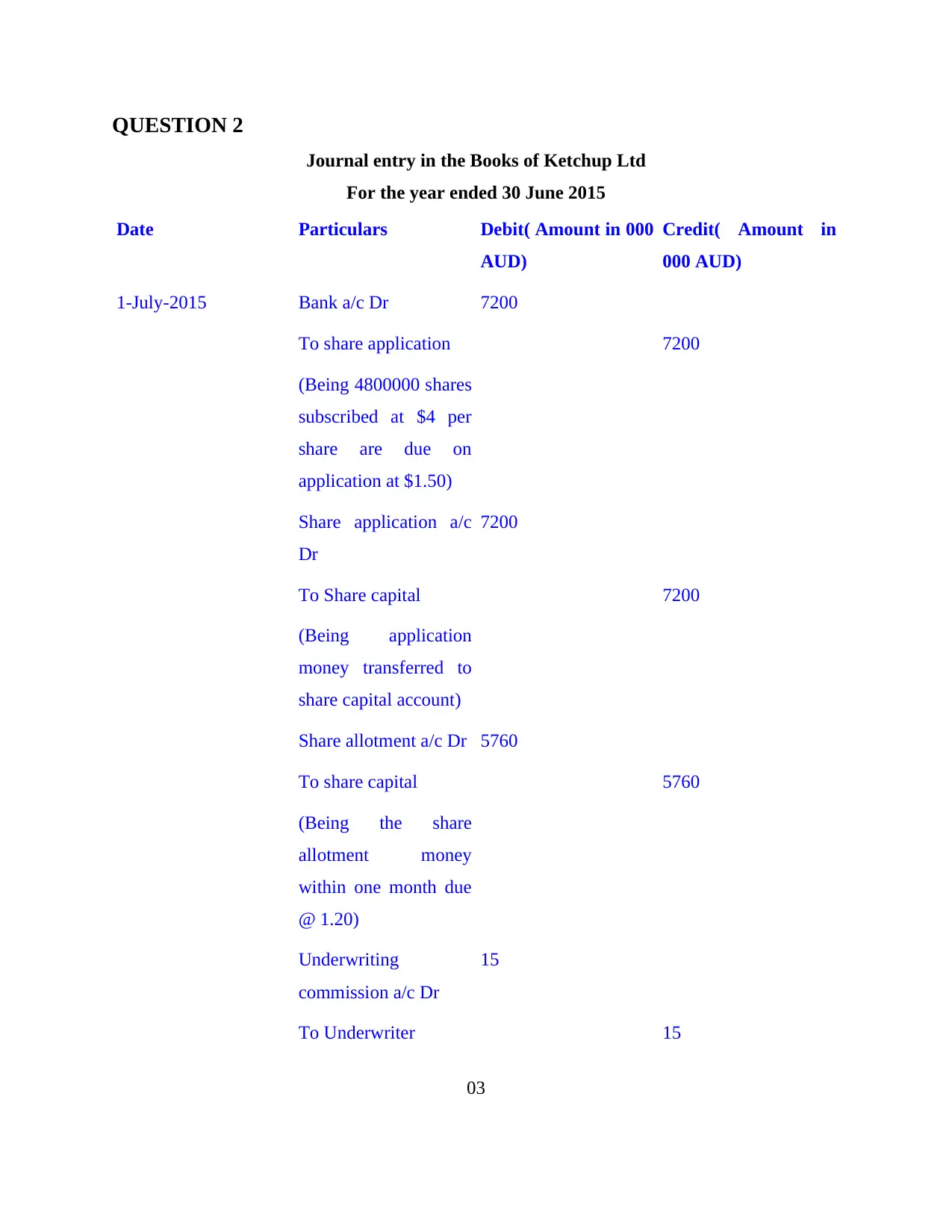

QUESTION 2

Journal entry in the Books of Ketchup Ltd

For the year ended 30 June 2015

Date Particulars Debit( Amount in 000

AUD)

Credit( Amount in

000 AUD)

1-July-2015 Bank a/c Dr 7200

To share application 7200

(Being 4800000 shares

subscribed at $4 per

share are due on

application at $1.50)

Share application a/c

Dr

7200

To Share capital 7200

(Being application

money transferred to

share capital account)

Share allotment a/c Dr 5760

To share capital 5760

(Being the share

allotment money

within one month due

@ 1.20)

Underwriting

commission a/c Dr

15

To Underwriter 15

03

Journal entry in the Books of Ketchup Ltd

For the year ended 30 June 2015

Date Particulars Debit( Amount in 000

AUD)

Credit( Amount in

000 AUD)

1-July-2015 Bank a/c Dr 7200

To share application 7200

(Being 4800000 shares

subscribed at $4 per

share are due on

application at $1.50)

Share application a/c

Dr

7200

To Share capital 7200

(Being application

money transferred to

share capital account)

Share allotment a/c Dr 5760

To share capital 5760

(Being the share

allotment money

within one month due

@ 1.20)

Underwriting

commission a/c Dr

15

To Underwriter 15

03

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

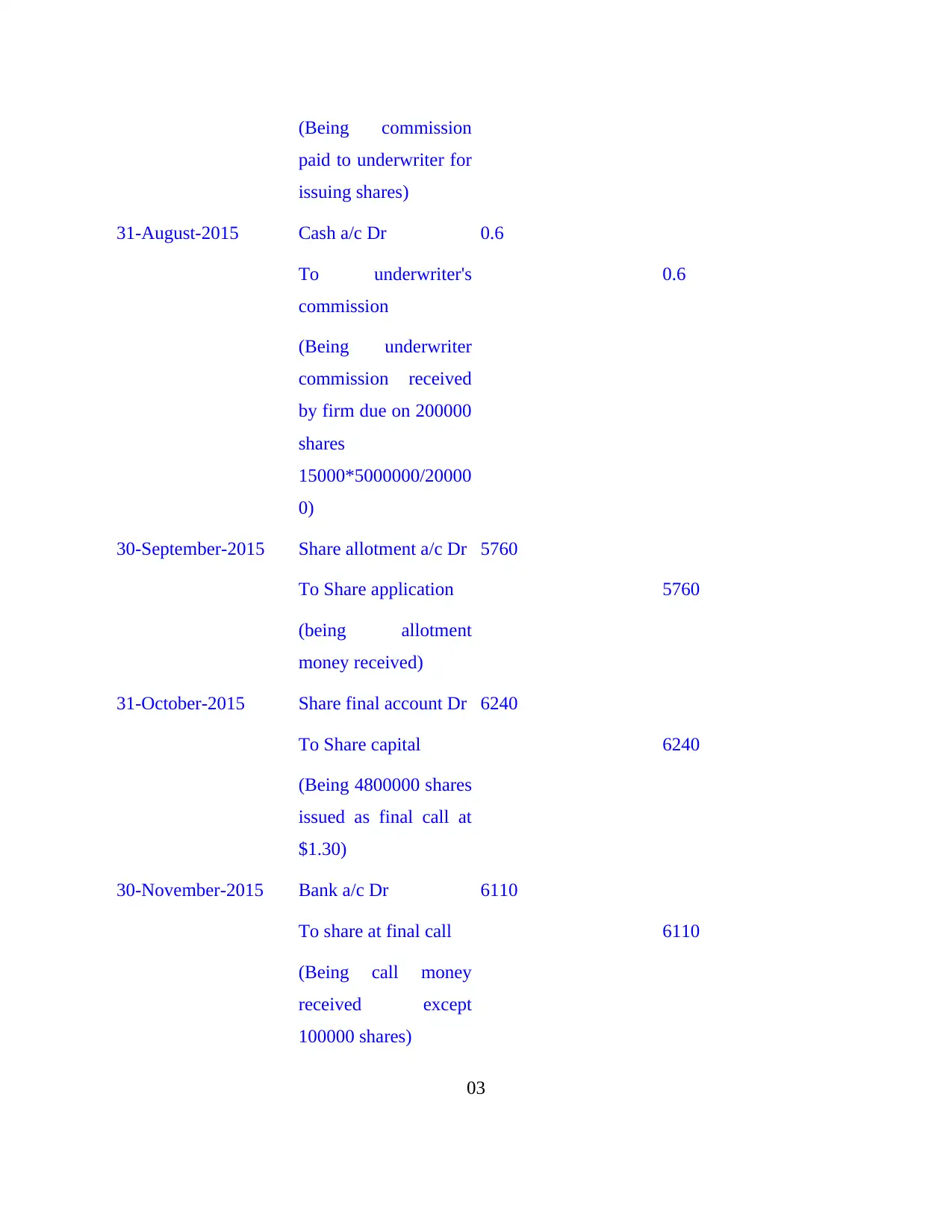

(Being commission

paid to underwriter for

issuing shares)

31-August-2015 Cash a/c Dr 0.6

To underwriter's

commission

0.6

(Being underwriter

commission received

by firm due on 200000

shares

15000*5000000/20000

0)

30-September-2015 Share allotment a/c Dr 5760

To Share application 5760

(being allotment

money received)

31-October-2015 Share final account Dr 6240

To Share capital 6240

(Being 4800000 shares

issued as final call at

$1.30)

30-November-2015 Bank a/c Dr 6110

To share at final call 6110

(Being call money

received except

100000 shares)

03

paid to underwriter for

issuing shares)

31-August-2015 Cash a/c Dr 0.6

To underwriter's

commission

0.6

(Being underwriter

commission received

by firm due on 200000

shares

15000*5000000/20000

0)

30-September-2015 Share allotment a/c Dr 5760

To Share application 5760

(being allotment

money received)

31-October-2015 Share final account Dr 6240

To Share capital 6240

(Being 4800000 shares

issued as final call at

$1.30)

30-November-2015 Bank a/c Dr 6110

To share at final call 6110

(Being call money

received except

100000 shares)

03

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

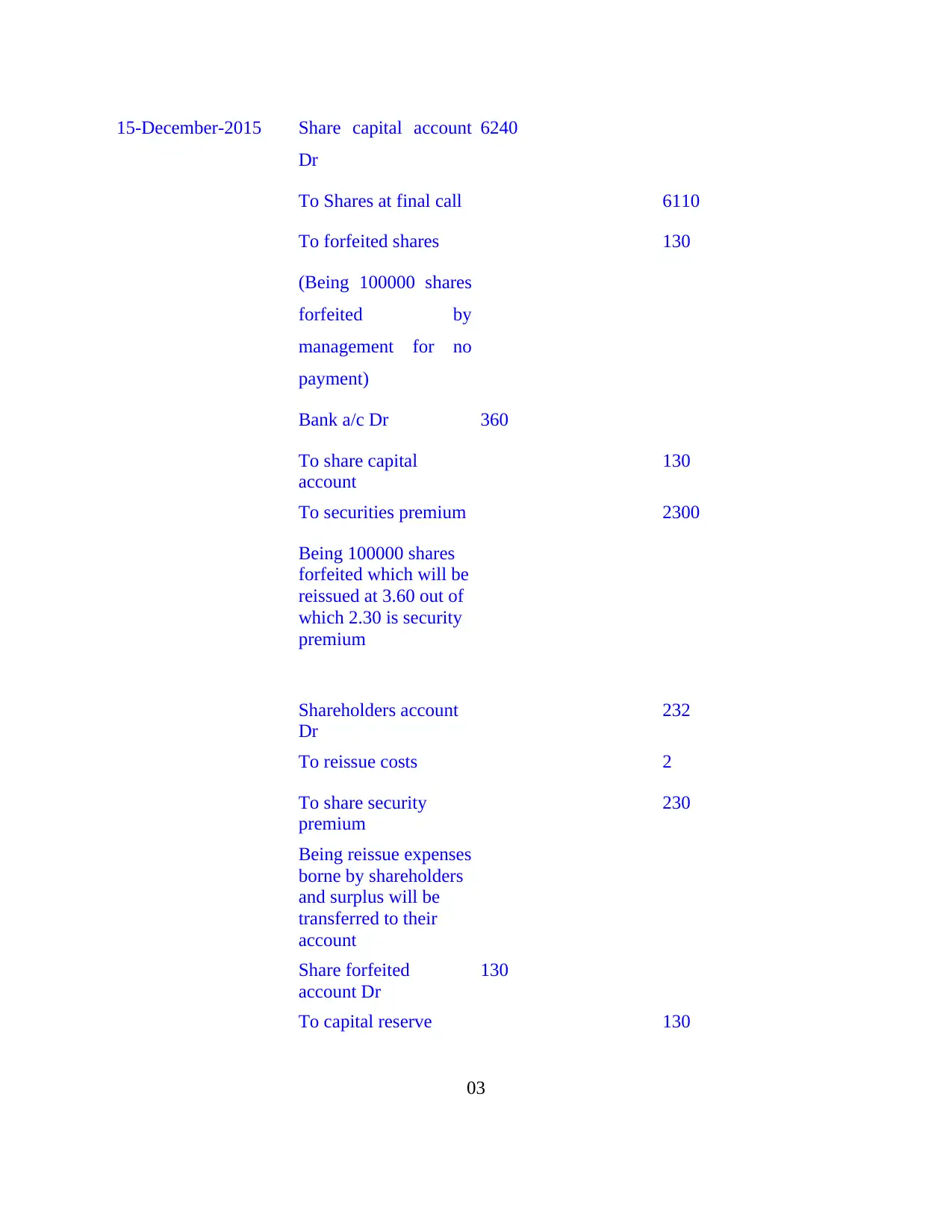

15-December-2015 Share capital account

Dr

6240

To Shares at final call 6110

To forfeited shares 130

(Being 100000 shares

forfeited by

management for no

payment)

Bank a/c Dr 360

To share capital

account

130

To securities premium 2300

Being 100000 shares

forfeited which will be

reissued at 3.60 out of

which 2.30 is security

premium

Shareholders account

Dr

232

To reissue costs 2

To share security

premium

230

Being reissue expenses

borne by shareholders

and surplus will be

transferred to their

account

Share forfeited

account Dr

130

To capital reserve 130

03

Dr

6240

To Shares at final call 6110

To forfeited shares 130

(Being 100000 shares

forfeited by

management for no

payment)

Bank a/c Dr 360

To share capital

account

130

To securities premium 2300

Being 100000 shares

forfeited which will be

reissued at 3.60 out of

which 2.30 is security

premium

Shareholders account

Dr

232

To reissue costs 2

To share security

premium

230

Being reissue expenses

borne by shareholders

and surplus will be

transferred to their

account

Share forfeited

account Dr

130

To capital reserve 130

03

Being forfeited shares

transferred to the

capital reserve account

of Ketchup Ltd

QUESTION 3

Calculation of current tax liability for the year ended 30 June 2016

Plant

Year Companies act

Depreciation

rate Income tax act

Depreciation

rate Difference

Value of Plant 15.00% Value of plant 20.00%

2015 AUD$ 315000

AUD $ 315000

* 15% =

47,250.00 AUD $ 315000

AUD$ 315000

* 20 % =

63,000.00

AUD $

15,750.00

2016 AUD$ 315000 AUD 47250 AUD $ 315000 AUD $ 63000 AUD $ 15750

Deferred

liability 4725

Motor vehicle

Year Companies act

Depreciation

rate Income tax act

Depreciation

rate Difference

Value of motor

vehicle 20.00% Value of plant 15.00%

2015 AUD $ 100000 AUD $ 20000 AUD $ 100000 AUD $ 15000 AUD $5000

2016 AUD $ 100000 AUD $ 20000 AUD $ 100000 AUD $ 15000 AUD $5000

Deferred tax

assets

5000 * 30%

1500

Prepaid insurance

03

transferred to the

capital reserve account

of Ketchup Ltd

QUESTION 3

Calculation of current tax liability for the year ended 30 June 2016

Plant

Year Companies act

Depreciation

rate Income tax act

Depreciation

rate Difference

Value of Plant 15.00% Value of plant 20.00%

2015 AUD$ 315000

AUD $ 315000

* 15% =

47,250.00 AUD $ 315000

AUD$ 315000

* 20 % =

63,000.00

AUD $

15,750.00

2016 AUD$ 315000 AUD 47250 AUD $ 315000 AUD $ 63000 AUD $ 15750

Deferred

liability 4725

Motor vehicle

Year Companies act

Depreciation

rate Income tax act

Depreciation

rate Difference

Value of motor

vehicle 20.00% Value of plant 15.00%

2015 AUD $ 100000 AUD $ 20000 AUD $ 100000 AUD $ 15000 AUD $5000

2016 AUD $ 100000 AUD $ 20000 AUD $ 100000 AUD $ 15000 AUD $5000

Deferred tax

assets

5000 * 30%

1500

Prepaid insurance

03

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

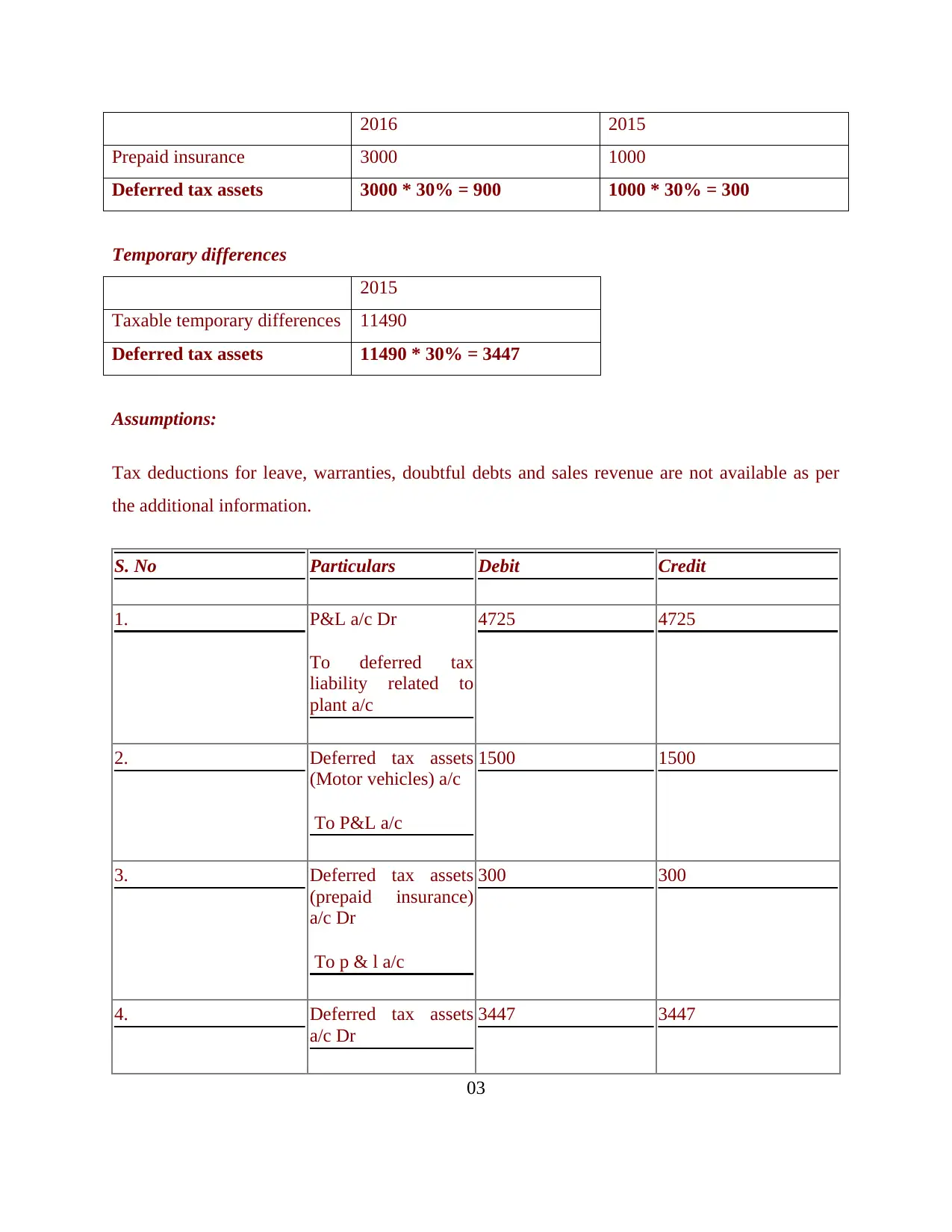

2016 2015

Prepaid insurance 3000 1000

Deferred tax assets 3000 * 30% = 900 1000 * 30% = 300

Temporary differences

2015

Taxable temporary differences 11490

Deferred tax assets 11490 * 30% = 3447

Assumptions:

Tax deductions for leave, warranties, doubtful debts and sales revenue are not available as per

the additional information.

S. No Particulars Debit Credit

1. P&L a/c Dr

To deferred tax

liability related to

plant a/c

4725 4725

2. Deferred tax assets

(Motor vehicles) a/c

To P&L a/c

1500 1500

3. Deferred tax assets

(prepaid insurance)

a/c Dr

To p & l a/c

300 300

4. Deferred tax assets

a/c Dr

3447 3447

03

Prepaid insurance 3000 1000

Deferred tax assets 3000 * 30% = 900 1000 * 30% = 300

Temporary differences

2015

Taxable temporary differences 11490

Deferred tax assets 11490 * 30% = 3447

Assumptions:

Tax deductions for leave, warranties, doubtful debts and sales revenue are not available as per

the additional information.

S. No Particulars Debit Credit

1. P&L a/c Dr

To deferred tax

liability related to

plant a/c

4725 4725

2. Deferred tax assets

(Motor vehicles) a/c

To P&L a/c

1500 1500

3. Deferred tax assets

(prepaid insurance)

a/c Dr

To p & l a/c

300 300

4. Deferred tax assets

a/c Dr

3447 3447

03

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

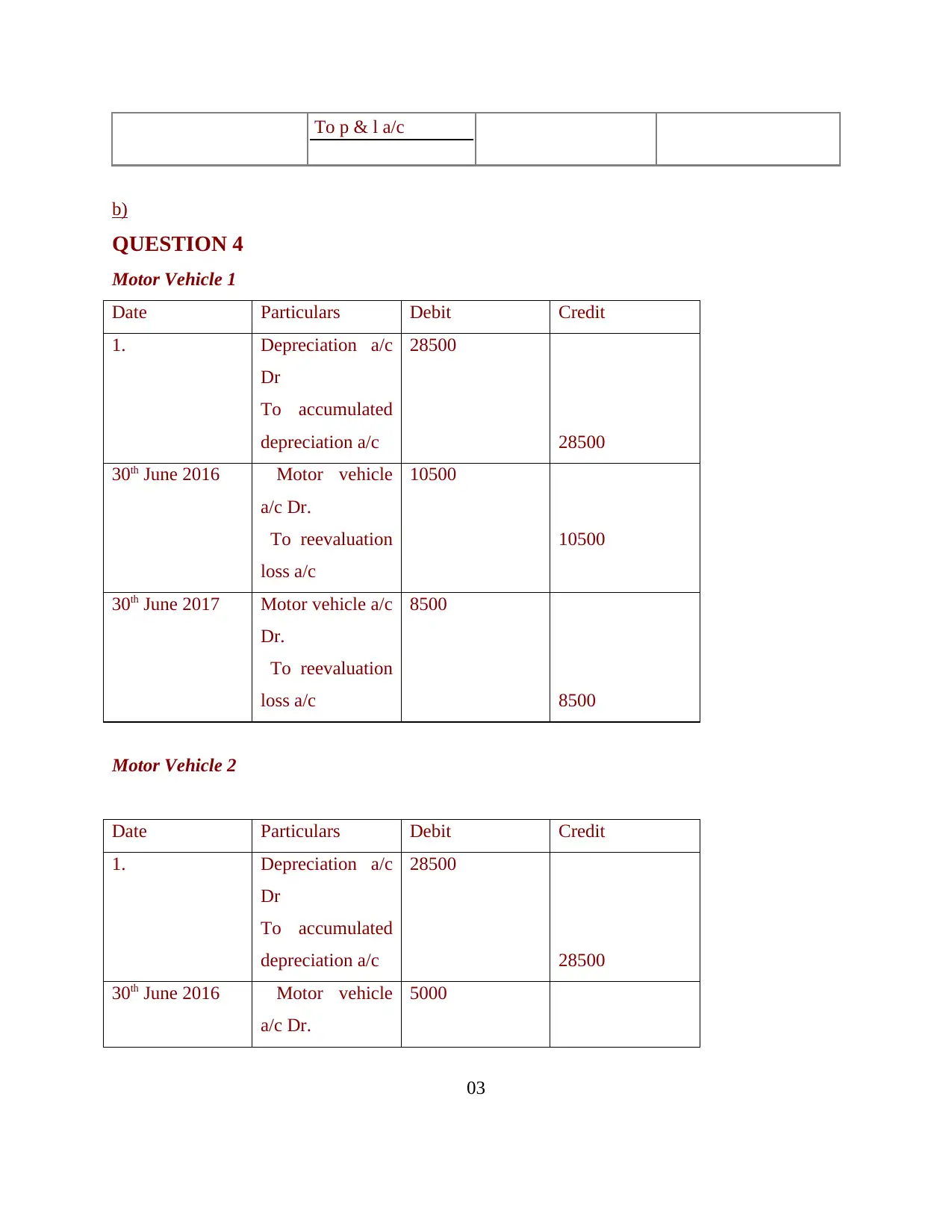

To p & l a/c

b)

QUESTION 4

Motor Vehicle 1

Date Particulars Debit Credit

1. Depreciation a/c

Dr

To accumulated

depreciation a/c

28500

28500

30th June 2016 Motor vehicle

a/c Dr.

To reevaluation

loss a/c

10500

10500

30th June 2017 Motor vehicle a/c

Dr.

To reevaluation

loss a/c

8500

8500

Motor Vehicle 2

Date Particulars Debit Credit

1. Depreciation a/c

Dr

To accumulated

depreciation a/c

28500

28500

30th June 2016 Motor vehicle

a/c Dr.

5000

03

b)

QUESTION 4

Motor Vehicle 1

Date Particulars Debit Credit

1. Depreciation a/c

Dr

To accumulated

depreciation a/c

28500

28500

30th June 2016 Motor vehicle

a/c Dr.

To reevaluation

loss a/c

10500

10500

30th June 2017 Motor vehicle a/c

Dr.

To reevaluation

loss a/c

8500

8500

Motor Vehicle 2

Date Particulars Debit Credit

1. Depreciation a/c

Dr

To accumulated

depreciation a/c

28500

28500

30th June 2016 Motor vehicle

a/c Dr.

5000

03

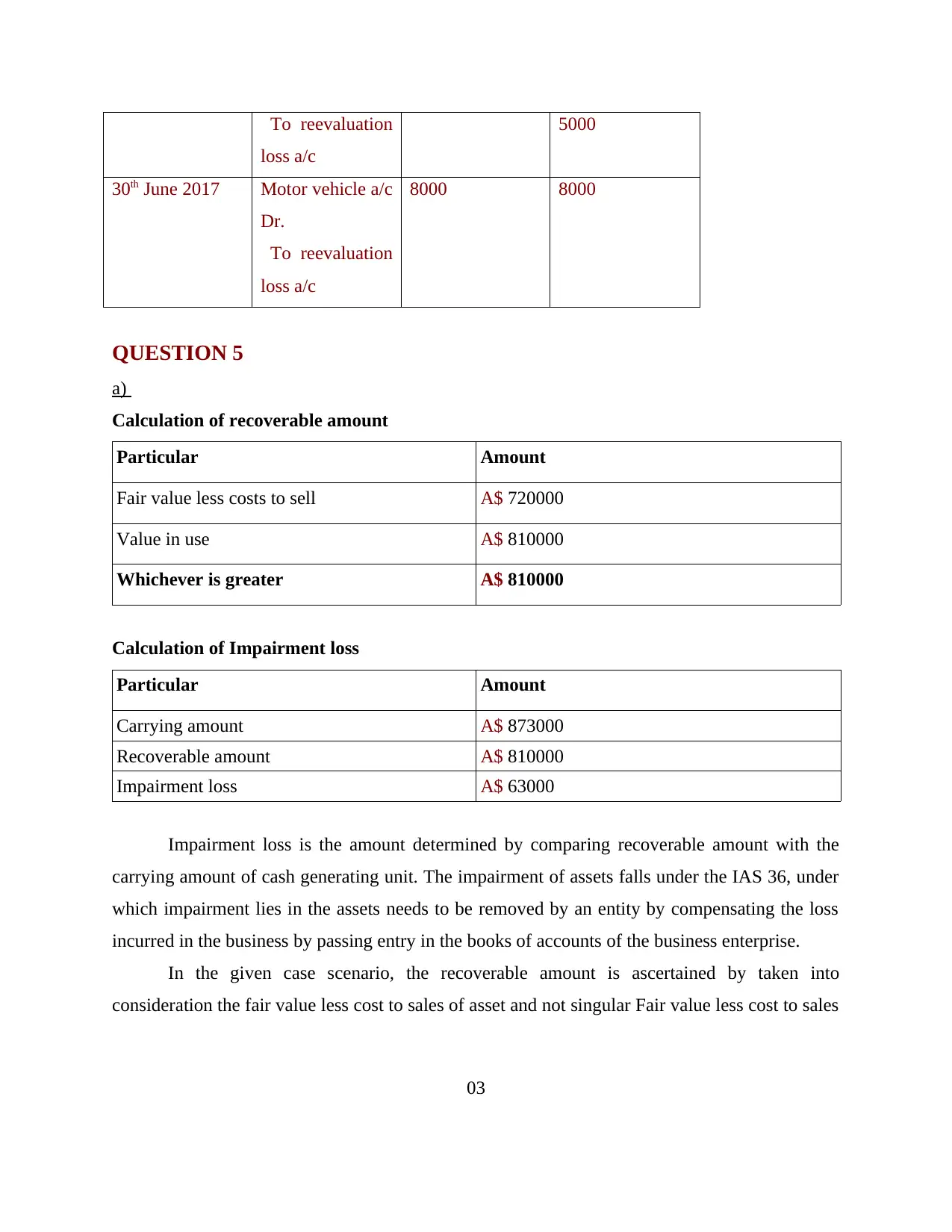

To reevaluation

loss a/c

5000

30th June 2017 Motor vehicle a/c

Dr.

To reevaluation

loss a/c

8000 8000

QUESTION 5

a)

Calculation of recoverable amount

Particular Amount

Fair value less costs to sell A$ 720000

Value in use A$ 810000

Whichever is greater A$ 810000

Calculation of Impairment loss

Particular Amount

Carrying amount A$ 873000

Recoverable amount A$ 810000

Impairment loss A$ 63000

Impairment loss is the amount determined by comparing recoverable amount with the

carrying amount of cash generating unit. The impairment of assets falls under the IAS 36, under

which impairment lies in the assets needs to be removed by an entity by compensating the loss

incurred in the business by passing entry in the books of accounts of the business enterprise.

In the given case scenario, the recoverable amount is ascertained by taken into

consideration the fair value less cost to sales of asset and not singular Fair value less cost to sales

03

loss a/c

5000

30th June 2017 Motor vehicle a/c

Dr.

To reevaluation

loss a/c

8000 8000

QUESTION 5

a)

Calculation of recoverable amount

Particular Amount

Fair value less costs to sell A$ 720000

Value in use A$ 810000

Whichever is greater A$ 810000

Calculation of Impairment loss

Particular Amount

Carrying amount A$ 873000

Recoverable amount A$ 810000

Impairment loss A$ 63000

Impairment loss is the amount determined by comparing recoverable amount with the

carrying amount of cash generating unit. The impairment of assets falls under the IAS 36, under

which impairment lies in the assets needs to be removed by an entity by compensating the loss

incurred in the business by passing entry in the books of accounts of the business enterprise.

In the given case scenario, the recoverable amount is ascertained by taken into

consideration the fair value less cost to sales of asset and not singular Fair value less cost to sales

03

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.