Executive Remuneration and Performance Measures in Mayne Pharma and CSL Limited

VerifiedAdded on 2023/06/06

|11

|1895

|196

AI Summary

This article discusses the executive remuneration and performance measures used in Mayne Pharma and CSL Limited. It covers the details of the remuneration committee and membership, allocation of executive remuneration, mix of performance measures used, financial versus non-financial measures, and a summary of findings.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGERIAL ACCOUNTING

Table of Contents

Company review:.......................................................................................................................2

Details of remuneration committee and membership:...........................................................2

Allocation of executive remuneration:...................................................................................3

Mix of performance measures used:......................................................................................4

Financial versus non-financial measures:..............................................................................6

Summary of findings:.................................................................................................................7

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Company review:.......................................................................................................................2

Details of remuneration committee and membership:...........................................................2

Allocation of executive remuneration:...................................................................................3

Mix of performance measures used:......................................................................................4

Financial versus non-financial measures:..............................................................................6

Summary of findings:.................................................................................................................7

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

2MANAGERIAL ACCOUNTING

Company review:

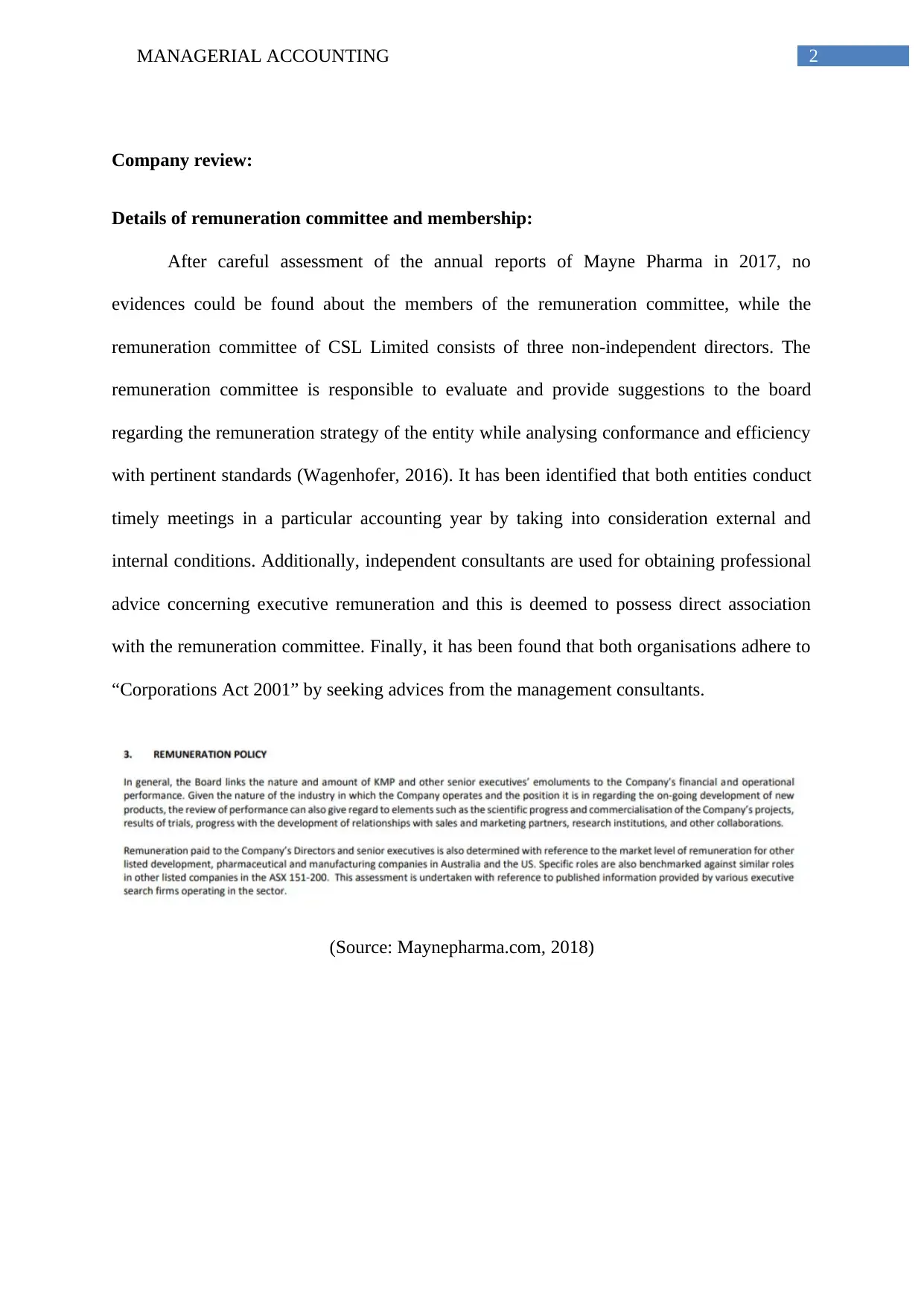

Details of remuneration committee and membership:

After careful assessment of the annual reports of Mayne Pharma in 2017, no

evidences could be found about the members of the remuneration committee, while the

remuneration committee of CSL Limited consists of three non-independent directors. The

remuneration committee is responsible to evaluate and provide suggestions to the board

regarding the remuneration strategy of the entity while analysing conformance and efficiency

with pertinent standards (Wagenhofer, 2016). It has been identified that both entities conduct

timely meetings in a particular accounting year by taking into consideration external and

internal conditions. Additionally, independent consultants are used for obtaining professional

advice concerning executive remuneration and this is deemed to possess direct association

with the remuneration committee. Finally, it has been found that both organisations adhere to

“Corporations Act 2001” by seeking advices from the management consultants.

(Source: Maynepharma.com, 2018)

Company review:

Details of remuneration committee and membership:

After careful assessment of the annual reports of Mayne Pharma in 2017, no

evidences could be found about the members of the remuneration committee, while the

remuneration committee of CSL Limited consists of three non-independent directors. The

remuneration committee is responsible to evaluate and provide suggestions to the board

regarding the remuneration strategy of the entity while analysing conformance and efficiency

with pertinent standards (Wagenhofer, 2016). It has been identified that both entities conduct

timely meetings in a particular accounting year by taking into consideration external and

internal conditions. Additionally, independent consultants are used for obtaining professional

advice concerning executive remuneration and this is deemed to possess direct association

with the remuneration committee. Finally, it has been found that both organisations adhere to

“Corporations Act 2001” by seeking advices from the management consultants.

(Source: Maynepharma.com, 2018)

3MANAGERIAL ACCOUNTING

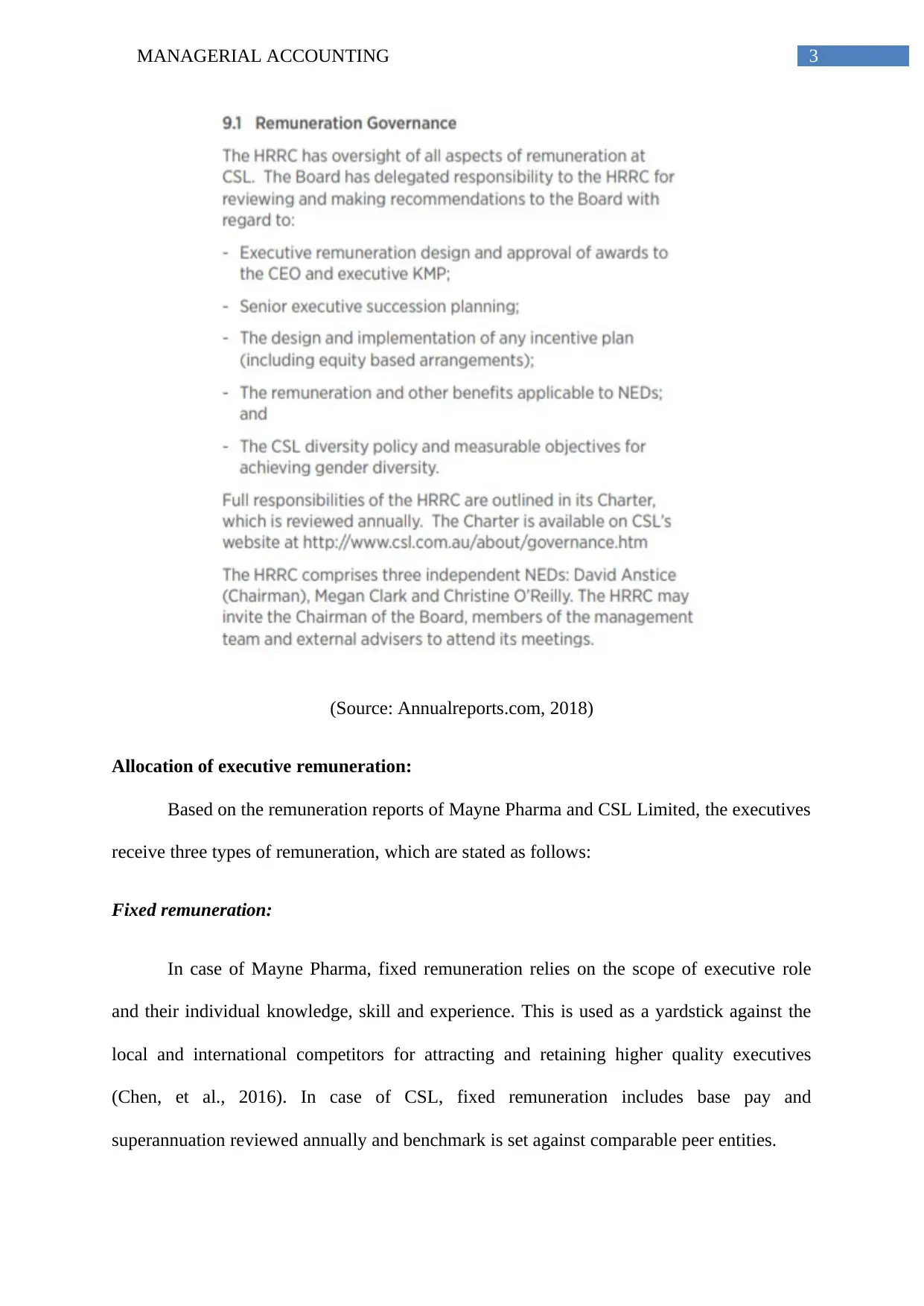

(Source: Annualreports.com, 2018)

Allocation of executive remuneration:

Based on the remuneration reports of Mayne Pharma and CSL Limited, the executives

receive three types of remuneration, which are stated as follows:

Fixed remuneration:

In case of Mayne Pharma, fixed remuneration relies on the scope of executive role

and their individual knowledge, skill and experience. This is used as a yardstick against the

local and international competitors for attracting and retaining higher quality executives

(Chen, et al., 2016). In case of CSL, fixed remuneration includes base pay and

superannuation reviewed annually and benchmark is set against comparable peer entities.

(Source: Annualreports.com, 2018)

Allocation of executive remuneration:

Based on the remuneration reports of Mayne Pharma and CSL Limited, the executives

receive three types of remuneration, which are stated as follows:

Fixed remuneration:

In case of Mayne Pharma, fixed remuneration relies on the scope of executive role

and their individual knowledge, skill and experience. This is used as a yardstick against the

local and international competitors for attracting and retaining higher quality executives

(Chen, et al., 2016). In case of CSL, fixed remuneration includes base pay and

superannuation reviewed annually and benchmark is set against comparable peer entities.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGERIAL ACCOUNTING

Short-term incentives (STI):

By using STI, it is possible for the participants to avail the opportunity of earning cash

as well as incentives related to deferred equity, in which particular outcomes could be

accomplished in the particular year (Fu, Carson and Simnett, 2015). In case of Mayne

Pharma, STIs rely on the results of the yearly corporate scorecard and individual performance

in opposition to knowledge performance indicators. In case of CSL Limited, annual STI

program is provided for aligning the executive interest with short-term operational and

financial targets for the year.

Long-term incentives (LTI):

In the words of Haque (2017), LTIs are reward systems developed for improving the

employee performance in long-term. This is done by giving rewards to the employees and

this does not have any direct association with the stock price of the organisation. For both

organisations, these systems are developed for aligning the executive as well as employee

performance with the shareholders’ interest. The market benchmarks, individual

performance, main skills and success potential help in setting the award amounts

(Wagenhofer, 2016).

Mix of performance measures used:

Various performance users could be used for analysing the financial health of the two

organisations in contrast to executive pay.

Financial measures:

In case of Mayne Pharma, the earnings per share of the organisation have increased

from 4.77 cents in 2016 to 6.18 cents in 2017, while the same has been $2.689 in 2016

compared to $2.937 in 2017. The main reason that earnings per share of both the

Short-term incentives (STI):

By using STI, it is possible for the participants to avail the opportunity of earning cash

as well as incentives related to deferred equity, in which particular outcomes could be

accomplished in the particular year (Fu, Carson and Simnett, 2015). In case of Mayne

Pharma, STIs rely on the results of the yearly corporate scorecard and individual performance

in opposition to knowledge performance indicators. In case of CSL Limited, annual STI

program is provided for aligning the executive interest with short-term operational and

financial targets for the year.

Long-term incentives (LTI):

In the words of Haque (2017), LTIs are reward systems developed for improving the

employee performance in long-term. This is done by giving rewards to the employees and

this does not have any direct association with the stock price of the organisation. For both

organisations, these systems are developed for aligning the executive as well as employee

performance with the shareholders’ interest. The market benchmarks, individual

performance, main skills and success potential help in setting the award amounts

(Wagenhofer, 2016).

Mix of performance measures used:

Various performance users could be used for analysing the financial health of the two

organisations in contrast to executive pay.

Financial measures:

In case of Mayne Pharma, the earnings per share of the organisation have increased

from 4.77 cents in 2016 to 6.18 cents in 2017, while the same has been $2.689 in 2016

compared to $2.937 in 2017. The main reason that earnings per share of both the

5MANAGERIAL ACCOUNTING

organisations have increased over the year is the considerable rise in net income. This has

helped in maximising the wealth of the shareholders and accordingly, executive remuneration

has increased for both the organisations. However, for CSL Limited, the return on investment

has fallen from 26.8% in 2016 to 24.5% in 2017. On the other hand, for Mayne Pharma, the

return on capital invested has increased from 30% in 2016 to 32.60% in 2017 due to the fact

that the amount is utilised for generating adequate amounts from its unused asset base.

Therefore, in terms of performance measures, Mayne Pharma has conducted better

shareholder payout, since it has maximised both its earnings per share and return on invested

capital over the year.

Non-financial measure:

The non-financial measure used for assessing the performance of Mayne Pharma is

the balanced scorecard approach. However, this approach is not used by CSL Limited.

Hence, this method is applied for Mayne Pharma only, which is elucidated briefly as follows:

Financial perspective:

Mayne Pharma has the goal of minimising its business expenditures. This is

accomplished by enhancing productivity along with optimising business processes. For

accomplishing the same, the organisation has formulated a five-year plan and the process of

implementation is conducted in distinct steps. In addition, it is viewed to be involved in

higher return activities so that the total profit could be increased. Finally, the risks would be

reduced by shift over from net income to portfolio widening of fees associated with products

(Ireland, 2016). As a result, it would enable to provide protection to the organisation (Kent,

Kercher and Routledge, 2018).

Customer perspective:

organisations have increased over the year is the considerable rise in net income. This has

helped in maximising the wealth of the shareholders and accordingly, executive remuneration

has increased for both the organisations. However, for CSL Limited, the return on investment

has fallen from 26.8% in 2016 to 24.5% in 2017. On the other hand, for Mayne Pharma, the

return on capital invested has increased from 30% in 2016 to 32.60% in 2017 due to the fact

that the amount is utilised for generating adequate amounts from its unused asset base.

Therefore, in terms of performance measures, Mayne Pharma has conducted better

shareholder payout, since it has maximised both its earnings per share and return on invested

capital over the year.

Non-financial measure:

The non-financial measure used for assessing the performance of Mayne Pharma is

the balanced scorecard approach. However, this approach is not used by CSL Limited.

Hence, this method is applied for Mayne Pharma only, which is elucidated briefly as follows:

Financial perspective:

Mayne Pharma has the goal of minimising its business expenditures. This is

accomplished by enhancing productivity along with optimising business processes. For

accomplishing the same, the organisation has formulated a five-year plan and the process of

implementation is conducted in distinct steps. In addition, it is viewed to be involved in

higher return activities so that the total profit could be increased. Finally, the risks would be

reduced by shift over from net income to portfolio widening of fees associated with products

(Ireland, 2016). As a result, it would enable to provide protection to the organisation (Kent,

Kercher and Routledge, 2018).

Customer perspective:

6MANAGERIAL ACCOUNTING

Mayne Pharma has developed a long-term plan for ensuring that adequate customers

are generated to arrive at positive financial performance. Moreover, it has set apart adequate

amount of funds in relation to research and development for obtaining considerable

knowledge regarding fulfilling the user needs in a better fashion (Safari, Cooper and

Dellaportas, 2016).

Internal processes perspective:

After the customer requirements are identified, Mayne Pharma is engaged in cross-

selling products due to the presence of proactive staffs. This is possible because of effective

interpersonal relationships maintained on the part of the staffs with the customers (Skovoroda

and Bruce, 2017).

Learning and growth perspective:

Balanced scorecard is utilised for providing excess motivation to the staffs so that

positive work outcomes could be assured. Moreover, the resources are allocated to the areas

having no potential of providing maximum gains.

Financial versus non-financial measures:

In terms of financial performance, the earnings per share and share price of Mayne

Pharma have been taken into consideration.

Mayne Pharma has developed a long-term plan for ensuring that adequate customers

are generated to arrive at positive financial performance. Moreover, it has set apart adequate

amount of funds in relation to research and development for obtaining considerable

knowledge regarding fulfilling the user needs in a better fashion (Safari, Cooper and

Dellaportas, 2016).

Internal processes perspective:

After the customer requirements are identified, Mayne Pharma is engaged in cross-

selling products due to the presence of proactive staffs. This is possible because of effective

interpersonal relationships maintained on the part of the staffs with the customers (Skovoroda

and Bruce, 2017).

Learning and growth perspective:

Balanced scorecard is utilised for providing excess motivation to the staffs so that

positive work outcomes could be assured. Moreover, the resources are allocated to the areas

having no potential of providing maximum gains.

Financial versus non-financial measures:

In terms of financial performance, the earnings per share and share price of Mayne

Pharma have been taken into consideration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

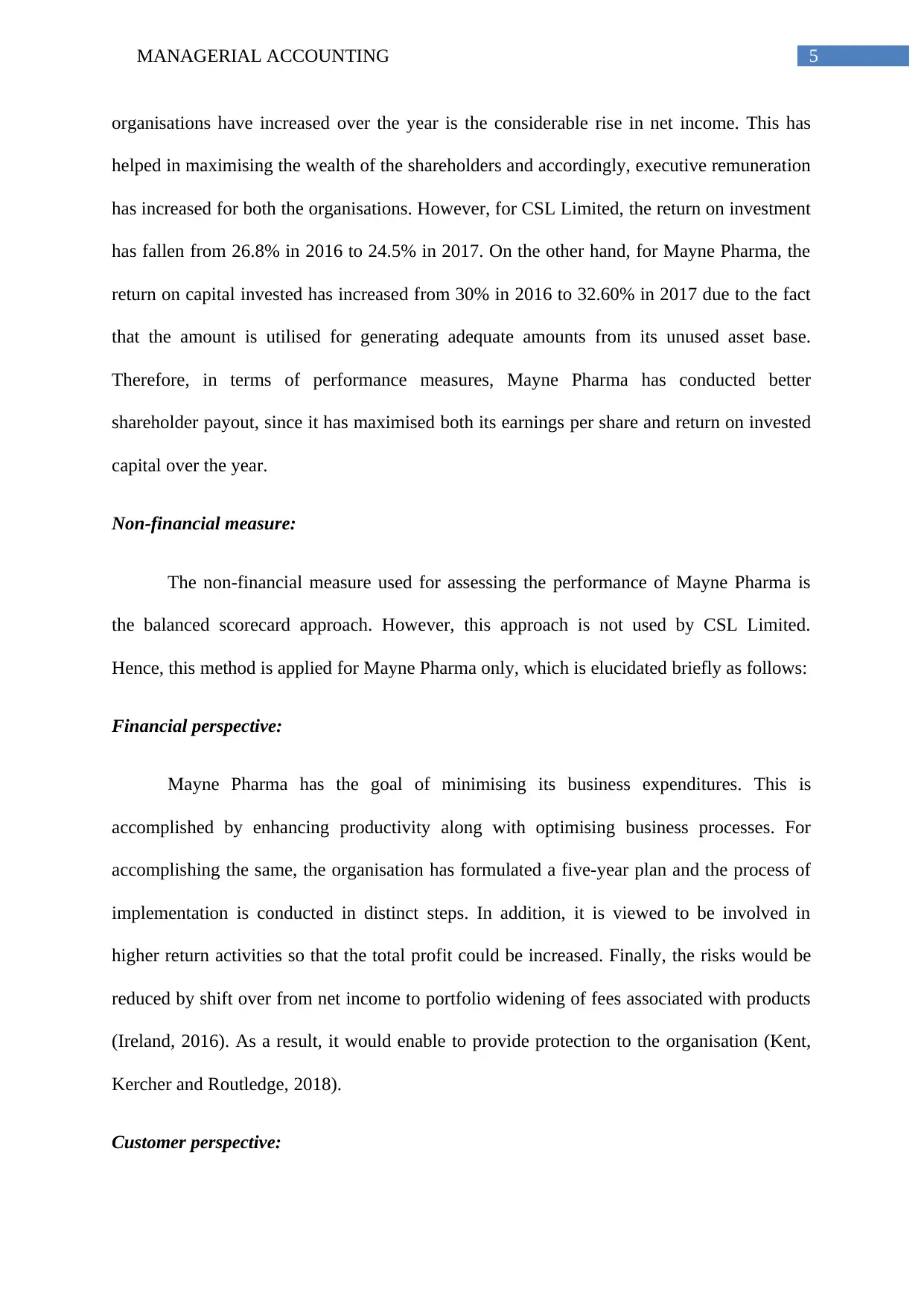

According to the above figure, it is clearly inherent that the share price of the

organisation has been on the increasing scale and the current share price stands at $1.22.

However, fluctuations could be observed in the share price of the organisation from

September 2017 to September 2018. Despite such fluctuations, the organisation has managed

to increase its payments to the employees. After analysing the staff performance, Mayne

Pharma has provided certain benefits in the form of short-term incentives and long-term

incentives to its executive and non-executive members. This is because the resources are

motivated through incentives as well as allowances according to their contribution and

performance for accomplishing the goals and productivity developed within the organisation.

Summary of findings:

Based on the above discussion, it could be found that that Mayne Pharma and CSL

Limited conduct timely meetings in a particular accounting year by taking into consideration

external and internal conditions. Additionally, independent consultants are used for obtaining

professional advice concerning executive remuneration and this is deemed to possess direct

association with the remuneration committee. Finally, it has been found that both

organisations adhere to “Corporations Act 2001” by seeking advices from the management

consultants. In terms of performance measures, Mayne Pharma has conducted better

shareholder payout, since it has maximised both its earnings per share and return on invested

capital over the year.

Mayne Pharma has the goal of minimising its business expenditures. This is

accomplished by enhancing productivity along with optimising business processes. For

accomplishing the same, the organisation has formulated a five-year plan and the process of

implementation is conducted in distinct steps. In addition, it is viewed to be involved in

higher return activities so that the total profit could be increased.

According to the above figure, it is clearly inherent that the share price of the

organisation has been on the increasing scale and the current share price stands at $1.22.

However, fluctuations could be observed in the share price of the organisation from

September 2017 to September 2018. Despite such fluctuations, the organisation has managed

to increase its payments to the employees. After analysing the staff performance, Mayne

Pharma has provided certain benefits in the form of short-term incentives and long-term

incentives to its executive and non-executive members. This is because the resources are

motivated through incentives as well as allowances according to their contribution and

performance for accomplishing the goals and productivity developed within the organisation.

Summary of findings:

Based on the above discussion, it could be found that that Mayne Pharma and CSL

Limited conduct timely meetings in a particular accounting year by taking into consideration

external and internal conditions. Additionally, independent consultants are used for obtaining

professional advice concerning executive remuneration and this is deemed to possess direct

association with the remuneration committee. Finally, it has been found that both

organisations adhere to “Corporations Act 2001” by seeking advices from the management

consultants. In terms of performance measures, Mayne Pharma has conducted better

shareholder payout, since it has maximised both its earnings per share and return on invested

capital over the year.

Mayne Pharma has the goal of minimising its business expenditures. This is

accomplished by enhancing productivity along with optimising business processes. For

accomplishing the same, the organisation has formulated a five-year plan and the process of

implementation is conducted in distinct steps. In addition, it is viewed to be involved in

higher return activities so that the total profit could be increased.

8MANAGERIAL ACCOUNTING

Conclusion:

Based on the above discussion, it could be stated that both Mayne Pharma and ASL

Limited have developed remuneration committees for reviewing and recommending the

executive compensation of the board committees. Accordingly, executive remuneration has

been carried out by using fixed remuneration, short-term incentives and long-term incentives.

However, in terms of financial performance in share market, Mayne Pharma is enjoying

competitive advantage over CSL Limited and thus, it has increased its executive

remuneration accordingly.

Conclusion:

Based on the above discussion, it could be stated that both Mayne Pharma and ASL

Limited have developed remuneration committees for reviewing and recommending the

executive compensation of the board committees. Accordingly, executive remuneration has

been carried out by using fixed remuneration, short-term incentives and long-term incentives.

However, in terms of financial performance in share market, Mayne Pharma is enjoying

competitive advantage over CSL Limited and thus, it has increased its executive

remuneration accordingly.

9MANAGERIAL ACCOUNTING

References:

Annualreports.com., 2018. [online] Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_CSL_2017.pdf

[Accessed 10 Sep. 2018].

Chen, L.H., Chung, H.H., Peters, G.F. and Wynn, J.P., 2016. Does Incentive-Based

Compensation for Chief Internal Auditors Impact Objectivity? An External Audit Risk

Perspective. Auditing: A Journal of Practice & Theory, 36(2), pp.21-43.

Fu, Y., Carson, E. and Simnett, R., 2015. Transparency report disclosure by Australian audit

firms and opportunities for research. Managerial Auditing Journal, 30(8/9), pp.870-910.

Haque, F., 2017. The effects of board characteristics and sustainable compensation policy on

carbon performance of UK firms. The British Accounting Review, 49(3), pp.347-364.

Ireland, I.N., 2016. Annual Report and Accounts for the Year Ended 31 March 2016. Invest

NI.

Kent, P., Kercher, K. and Routledge, J., 2018. Remuneration committees, shareholder dissent

on CEO pay and the CEO pay–performance link. Accounting & Finance, 58(2), pp.445-475.

Maynepharma.com., 2018. [online] Available at:

https://www.maynepharma.com/media/1964/2017-annual-report.pdf [Accessed 10 Sep.

2018].

Safari, M., Cooper, B.J. and Dellaportas, S., 2016. The influence of remuneration structures

on financial reporting quality: evidence from Australia. Australian Accounting Review, 26(1),

pp.66-75.

References:

Annualreports.com., 2018. [online] Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_CSL_2017.pdf

[Accessed 10 Sep. 2018].

Chen, L.H., Chung, H.H., Peters, G.F. and Wynn, J.P., 2016. Does Incentive-Based

Compensation for Chief Internal Auditors Impact Objectivity? An External Audit Risk

Perspective. Auditing: A Journal of Practice & Theory, 36(2), pp.21-43.

Fu, Y., Carson, E. and Simnett, R., 2015. Transparency report disclosure by Australian audit

firms and opportunities for research. Managerial Auditing Journal, 30(8/9), pp.870-910.

Haque, F., 2017. The effects of board characteristics and sustainable compensation policy on

carbon performance of UK firms. The British Accounting Review, 49(3), pp.347-364.

Ireland, I.N., 2016. Annual Report and Accounts for the Year Ended 31 March 2016. Invest

NI.

Kent, P., Kercher, K. and Routledge, J., 2018. Remuneration committees, shareholder dissent

on CEO pay and the CEO pay–performance link. Accounting & Finance, 58(2), pp.445-475.

Maynepharma.com., 2018. [online] Available at:

https://www.maynepharma.com/media/1964/2017-annual-report.pdf [Accessed 10 Sep.

2018].

Safari, M., Cooper, B.J. and Dellaportas, S., 2016. The influence of remuneration structures

on financial reporting quality: evidence from Australia. Australian Accounting Review, 26(1),

pp.66-75.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGERIAL ACCOUNTING

Skovoroda, R. and Bruce, A., 2017. Shifting the goalposts? Analysing changes to

performance peer groups used to determine the remuneration of FTSE 100 CEOs. British

Journal of Management, 28(2), pp.265-279.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management

accounting. Management Accounting Research, 31, pp.112-117.

Skovoroda, R. and Bruce, A., 2017. Shifting the goalposts? Analysing changes to

performance peer groups used to determine the remuneration of FTSE 100 CEOs. British

Journal of Management, 28(2), pp.265-279.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management

accounting. Management Accounting Research, 31, pp.112-117.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.