Factors Impacting Auditor Independence in Auditing Profession

VerifiedAdded on 2020/03/16

|82

|14591

|169

Report

AI Summary

This report, authored by Ehsanul Quayoum from Angila Ruskin University, investigates the factors affecting auditor independence within the auditing profession. The study begins with an introduction that establishes the importance of auditor independence, the problem statement, and the aim of the study, which is to identify factors influencing external auditor independence. The literature review explores auditor independence, relevant theories like social identity, audit quality, and agency theories, and empirical studies. The research methodology section details the research philosophy, approach, design, strategy, sampling techniques, data collection, and analysis methods. The analysis and findings chapter presents the results, followed by a conclusion and recommendations section that summarizes the research, links findings to objectives, and suggests improvements. The report also includes a survey questionnaire and a comprehensive reference list. The study's significance lies in its contribution to understanding factors that influence the auditor's ability to provide unbiased financial reports. It investigates various factors such as competitive levels, the size of audit fees, and audit agency capabilities, and concludes with recommendations for enhancing audit processes and ensuring auditor independence.

Running head: AUDITOR’S INDEPENDENCE

Factors Affecting Auditor Independence

Name of Student: Ehsanul Quayoum

Student ID:1642610

Name of University: Angila Ruskin University

Author Note

Factors Affecting Auditor Independence

Name of Student: Ehsanul Quayoum

Student ID:1642610

Name of University: Angila Ruskin University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITOR’S INDEPENDENCE

Acknowledgement

I would also like to take this opportunity to thank my professor without whose, constant support

and guidance, the research would not have been possible.

Firstly, I would like to thank God the Almighty in giving me the strength and courage without

which I could not have completed the entire study. Secondly, I would like to thank my family

and relatives who gave me constant support mentally and physically so that I can complete the

study on time. Lastly, I would like to give thanks to my peers and the friends who have helped

me in providing the appropriate information throughout the project and helped me in doing the

in-depth analysis of the research. Without their proper guidance, it is impossible for me to

complete the project.

Thanks and Regards,

Yours Sincerely,

AUDITOR’S INDEPENDENCE

Acknowledgement

I would also like to take this opportunity to thank my professor without whose, constant support

and guidance, the research would not have been possible.

Firstly, I would like to thank God the Almighty in giving me the strength and courage without

which I could not have completed the entire study. Secondly, I would like to thank my family

and relatives who gave me constant support mentally and physically so that I can complete the

study on time. Lastly, I would like to give thanks to my peers and the friends who have helped

me in providing the appropriate information throughout the project and helped me in doing the

in-depth analysis of the research. Without their proper guidance, it is impossible for me to

complete the project.

Thanks and Regards,

Yours Sincerely,

2

AUDITOR’S INDEPENDENCE

Abstract

The main aim of this research process was to study the factors that will help in creating an

impact on the independence of the auditors within the profession of auditing. It is considered to

be one of the main factors in this profession, as it has helped in diagnosing the objective factors

and the personal ones that can affect the independent factors of the auditors. The literature

review has helped in analyzing the various literature and theories that are present with the

auditing profession. The identification of the factors has helped in gaining better insights

regarding the factors that help in influencing the factors of independence.

The researcher has collected the data from the respondents in a true and honest manner that has

helped in carrying out the research process in a better manner and the manipulation that was not

done helped the researcher in carrying out the research in a professional manner. the analysis and

the findings have been done according to the statistical manner with the help of graphs and charts

so that it can result in presenting the figures in an efficient manner. Lastly, the researcher was

able to provide better recommendations regarding the factors so that it can help the auditors in

understanding the important factors, which will help them in doing the business in a better way.

AUDITOR’S INDEPENDENCE

Abstract

The main aim of this research process was to study the factors that will help in creating an

impact on the independence of the auditors within the profession of auditing. It is considered to

be one of the main factors in this profession, as it has helped in diagnosing the objective factors

and the personal ones that can affect the independent factors of the auditors. The literature

review has helped in analyzing the various literature and theories that are present with the

auditing profession. The identification of the factors has helped in gaining better insights

regarding the factors that help in influencing the factors of independence.

The researcher has collected the data from the respondents in a true and honest manner that has

helped in carrying out the research process in a better manner and the manipulation that was not

done helped the researcher in carrying out the research in a professional manner. the analysis and

the findings have been done according to the statistical manner with the help of graphs and charts

so that it can result in presenting the figures in an efficient manner. Lastly, the researcher was

able to provide better recommendations regarding the factors so that it can help the auditors in

understanding the important factors, which will help them in doing the business in a better way.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITOR’S INDEPENDENCE

Table of Contents

Chapter 1: Introduction:...................................................................................................................6

1.1 Introduction:..........................................................................................................................6

1.2 Problem Statement:................................................................................................................7

1.3 Aim of Study:........................................................................................................................8

1.4: Research Objectives.............................................................................................................8

1.5 Research Questions................................................................................................................8

1.6: Research Hypothesis.............................................................................................................9

1.7 Significance of the Study:......................................................................................................9

1.8 Structure of Dissertation:.....................................................................................................10

Chapter 2: Literature Review.........................................................................................................11

2.1 Conceptual Framework:.......................................................................................................11

2.1.1 Auditor’s Independence: General Overview................................................................12

2.1.2 Terms and Definitions:.................................................................................................13

2.2 Factors Affecting Auditor’s Independence:.........................................................................14

2.2.1 Personality:...................................................................................................................14

2.2.2 Rules and Regulations:.................................................................................................15

2.2.3 Familiarity:...................................................................................................................15

2.3 Social Identity Theory:........................................................................................................16

2.4 Audit Quality Theory:..........................................................................................................17

AUDITOR’S INDEPENDENCE

Table of Contents

Chapter 1: Introduction:...................................................................................................................6

1.1 Introduction:..........................................................................................................................6

1.2 Problem Statement:................................................................................................................7

1.3 Aim of Study:........................................................................................................................8

1.4: Research Objectives.............................................................................................................8

1.5 Research Questions................................................................................................................8

1.6: Research Hypothesis.............................................................................................................9

1.7 Significance of the Study:......................................................................................................9

1.8 Structure of Dissertation:.....................................................................................................10

Chapter 2: Literature Review.........................................................................................................11

2.1 Conceptual Framework:.......................................................................................................11

2.1.1 Auditor’s Independence: General Overview................................................................12

2.1.2 Terms and Definitions:.................................................................................................13

2.2 Factors Affecting Auditor’s Independence:.........................................................................14

2.2.1 Personality:...................................................................................................................14

2.2.2 Rules and Regulations:.................................................................................................15

2.2.3 Familiarity:...................................................................................................................15

2.3 Social Identity Theory:........................................................................................................16

2.4 Audit Quality Theory:..........................................................................................................17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITOR’S INDEPENDENCE

2.5 Agency Theory:...................................................................................................................17

2.6 Auditing Pillars: Competence and Independence................................................................19

2.7 Testing Auditor’s Competence and Independence:.............................................................19

2.8 Empirical Studies on factors affecting Auditor’s Independence:........................................21

Factors affecting independence of external auditors.....................................................................23

Objective factors........................................................................................................................23

Size of audit firm...................................................................................................................23

Provision of non-audit services.............................................................................................24

Tenure with the client............................................................................................................24

Competition level in the audit service market.......................................................................25

Chapter 3: Research Methodology................................................................................................26

3.0: Introduction........................................................................................................................26

3.1: Research Outline.................................................................................................................26

3.2: Research Philosophy...........................................................................................................27

3.2.1: Justification of positivism philosophy.........................................................................28

3.3: Research Approach.............................................................................................................28

3.3.1: Justification for deductive approach............................................................................29

3.4: Research Design.................................................................................................................30

3.4.1: Justification for descriptive design..............................................................................30

3.5: Research strategy................................................................................................................31

AUDITOR’S INDEPENDENCE

2.5 Agency Theory:...................................................................................................................17

2.6 Auditing Pillars: Competence and Independence................................................................19

2.7 Testing Auditor’s Competence and Independence:.............................................................19

2.8 Empirical Studies on factors affecting Auditor’s Independence:........................................21

Factors affecting independence of external auditors.....................................................................23

Objective factors........................................................................................................................23

Size of audit firm...................................................................................................................23

Provision of non-audit services.............................................................................................24

Tenure with the client............................................................................................................24

Competition level in the audit service market.......................................................................25

Chapter 3: Research Methodology................................................................................................26

3.0: Introduction........................................................................................................................26

3.1: Research Outline.................................................................................................................26

3.2: Research Philosophy...........................................................................................................27

3.2.1: Justification of positivism philosophy.........................................................................28

3.3: Research Approach.............................................................................................................28

3.3.1: Justification for deductive approach............................................................................29

3.4: Research Design.................................................................................................................30

3.4.1: Justification for descriptive design..............................................................................30

3.5: Research strategy................................................................................................................31

5

AUDITOR’S INDEPENDENCE

3.5.1: Justification for the survey strategy.............................................................................31

3.6: Sampling technique and sampling size...............................................................................32

3.6.1: Justifying the selection of probability sampling technique.........................................33

3.7: Data collection technique...................................................................................................33

3.7.1: Justifying the primary data collection technique.........................................................34

3.8: Data analysis technique......................................................................................................34

3.8.1: Justification for SPSS..................................................................................................34

3.9: Ethical Considerations........................................................................................................35

3.10: Summary...........................................................................................................................35

Chapter 4: Analysis and Findings..................................................................................................36

Chapter 5: Conclusion and Recommendations..............................................................................69

5.1: Conclusion..........................................................................................................................69

5.2: Linking with objectives......................................................................................................69

5.3: Recommendations..............................................................................................................70

5.4: Scope of the research..........................................................................................................71

Reference List................................................................................................................................72

Appendix........................................................................................................................................79

Survey Questionnaire.................................................................................................................79

AUDITOR’S INDEPENDENCE

3.5.1: Justification for the survey strategy.............................................................................31

3.6: Sampling technique and sampling size...............................................................................32

3.6.1: Justifying the selection of probability sampling technique.........................................33

3.7: Data collection technique...................................................................................................33

3.7.1: Justifying the primary data collection technique.........................................................34

3.8: Data analysis technique......................................................................................................34

3.8.1: Justification for SPSS..................................................................................................34

3.9: Ethical Considerations........................................................................................................35

3.10: Summary...........................................................................................................................35

Chapter 4: Analysis and Findings..................................................................................................36

Chapter 5: Conclusion and Recommendations..............................................................................69

5.1: Conclusion..........................................................................................................................69

5.2: Linking with objectives......................................................................................................69

5.3: Recommendations..............................................................................................................70

5.4: Scope of the research..........................................................................................................71

Reference List................................................................................................................................72

Appendix........................................................................................................................................79

Survey Questionnaire.................................................................................................................79

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITOR’S INDEPENDENCE

Chapter 1: Introduction:

1.1 Introduction:

The independence and neutrality of the auditor is the most significant principles that is

being recognized by the consecutive global conferences held during the previous year’s Supreme

Audit Institutions of the representatives of the nations on global basis. It has been one of the key

concerns for both the shareholders and became the relevance of this principle is predictable in

securing a main concern over the money of the public in efficient manner for managing of the

economy (Alzeban and Gwilliam 2014).

The independence of the external auditor is stated to be one of the most significant issues

received by the audit with substantial attention since the initiation of the concerto of the audit

profession is viewed as a fundamental player in suggesting the corporate management and

organizations in performing their roles and responsibilities in proper manner. It is important for

the auditor on executing their functions with apt responsibility and professional mode, the

significance of the autonomy of the external auditor cannot be exaggerated. It has been one of

the important factors in understanding the factors having the capability in influencing the

exercise of audit through jeopardizing the independence factor of external auditor (Tepalagul and

Lin 2015).

In this perspective, the aim of this paper is in studying the factors impacting the

independence of the external auditor in the profession of auditing, and the liberty of the external

auditor has got with bigger interest by the researchers in the auditing field. The reason for the

same is that independent auditors as the prime basis for the eminence of the process of audit and

then the investors’ confidence in the non-financial and financial information, this area have been

AUDITOR’S INDEPENDENCE

Chapter 1: Introduction:

1.1 Introduction:

The independence and neutrality of the auditor is the most significant principles that is

being recognized by the consecutive global conferences held during the previous year’s Supreme

Audit Institutions of the representatives of the nations on global basis. It has been one of the key

concerns for both the shareholders and became the relevance of this principle is predictable in

securing a main concern over the money of the public in efficient manner for managing of the

economy (Alzeban and Gwilliam 2014).

The independence of the external auditor is stated to be one of the most significant issues

received by the audit with substantial attention since the initiation of the concerto of the audit

profession is viewed as a fundamental player in suggesting the corporate management and

organizations in performing their roles and responsibilities in proper manner. It is important for

the auditor on executing their functions with apt responsibility and professional mode, the

significance of the autonomy of the external auditor cannot be exaggerated. It has been one of

the important factors in understanding the factors having the capability in influencing the

exercise of audit through jeopardizing the independence factor of external auditor (Tepalagul and

Lin 2015).

In this perspective, the aim of this paper is in studying the factors impacting the

independence of the external auditor in the profession of auditing, and the liberty of the external

auditor has got with bigger interest by the researchers in the auditing field. The reason for the

same is that independent auditors as the prime basis for the eminence of the process of audit and

then the investors’ confidence in the non-financial and financial information, this area have been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITOR’S INDEPENDENCE

tried by many of the articles undertaking the relationship between the external auditor’s

independence and audit process quality (Abbot et al. 2016). There exists difference in the views

among all the revelries interested within the audit concept about the auditor’s independence and

the audit quality indicating the crystallization of the thought of the auditor’s independence and

the significant factors influencing it in the profession of audit (Dhaliwal et al. 2015).

The researcher would be following both the historical method in keeping track of the

prior studies that have to make the study relevant, inductive approach along with descriptive

approach in determining the influence of the factors on the factor of independence of external

auditors. This would be increasing the efficacy and competence level of the process of audit

through the extrapolation of the studies and the research in describing the impact of external

auditor’s independence on the profession of audit (He et al. 2017).

1.2 Problem Statement:

Audit is fundamentally entrusted with the task of exposure in the statements financially

and this realism is what the users of the information of accounting expect. However, the auditors

might not ensure this reality and this reality might fall short of the expectation of the users. This

deficit within the effectiveness of audit is being broadly branded as the expectation gap of audit.

On most occasions the users of financial statement deem an auditor report to be the clean

statement for health (Cannon and Bedard 2016). Thus most of the expectations of the users

towards the auditor is actually more than what it should be. The expectation within the gap

occurs when there are dissimilarities between the expectations of the public from the auditor and

the actual offerings of the auditor (Knechel and Salterio 2016).

This generally put the auditor’s reporting and investigative independence in peril that

might defeat the principle of the audit of public and corrode the independence. It is therefore not

AUDITOR’S INDEPENDENCE

tried by many of the articles undertaking the relationship between the external auditor’s

independence and audit process quality (Abbot et al. 2016). There exists difference in the views

among all the revelries interested within the audit concept about the auditor’s independence and

the audit quality indicating the crystallization of the thought of the auditor’s independence and

the significant factors influencing it in the profession of audit (Dhaliwal et al. 2015).

The researcher would be following both the historical method in keeping track of the

prior studies that have to make the study relevant, inductive approach along with descriptive

approach in determining the influence of the factors on the factor of independence of external

auditors. This would be increasing the efficacy and competence level of the process of audit

through the extrapolation of the studies and the research in describing the impact of external

auditor’s independence on the profession of audit (He et al. 2017).

1.2 Problem Statement:

Audit is fundamentally entrusted with the task of exposure in the statements financially

and this realism is what the users of the information of accounting expect. However, the auditors

might not ensure this reality and this reality might fall short of the expectation of the users. This

deficit within the effectiveness of audit is being broadly branded as the expectation gap of audit.

On most occasions the users of financial statement deem an auditor report to be the clean

statement for health (Cannon and Bedard 2016). Thus most of the expectations of the users

towards the auditor is actually more than what it should be. The expectation within the gap

occurs when there are dissimilarities between the expectations of the public from the auditor and

the actual offerings of the auditor (Knechel and Salterio 2016).

This generally put the auditor’s reporting and investigative independence in peril that

might defeat the principle of the audit of public and corrode the independence. It is therefore not

8

AUDITOR’S INDEPENDENCE

much clear if the factor of independence of the auditor has any considerable impact on the

accountability of the private industry. Auditor’s independence is primary to the confidence of the

public in the factor of financial reporting along with the profession. This study focuses on

providing added understanding of the factors influencing the independence of the auditor

(DeFond and Zhang 2014).

1.3 Aim of Study:

The primary aim of this study is in identifying the factors that affects the independence of

the external auditor. The sub-aims are:

a. To identify the factors that is being classified into the intent factors and other personal

affecting the varying degrees on the factor of independence of the external auditor

b. To evade the negative effects of the factors on the independence

1.4: Research Objectives

a. To identify the competitive level among the auditors regarding the independent factors

b. To identify the factors that lead to independence of the auditors

1.5 Research Questions

The problem of this particular study is in answering the following questions, including:

a. What are the aspects influencing the independence of the external auditor in the profession of

auditing?

b. What is the precedence of the factors that affects the independence of the external auditor in

the profession of auditing?

AUDITOR’S INDEPENDENCE

much clear if the factor of independence of the auditor has any considerable impact on the

accountability of the private industry. Auditor’s independence is primary to the confidence of the

public in the factor of financial reporting along with the profession. This study focuses on

providing added understanding of the factors influencing the independence of the auditor

(DeFond and Zhang 2014).

1.3 Aim of Study:

The primary aim of this study is in identifying the factors that affects the independence of

the external auditor. The sub-aims are:

a. To identify the factors that is being classified into the intent factors and other personal

affecting the varying degrees on the factor of independence of the external auditor

b. To evade the negative effects of the factors on the independence

1.4: Research Objectives

a. To identify the competitive level among the auditors regarding the independent factors

b. To identify the factors that lead to independence of the auditors

1.5 Research Questions

The problem of this particular study is in answering the following questions, including:

a. What are the aspects influencing the independence of the external auditor in the profession of

auditing?

b. What is the precedence of the factors that affects the independence of the external auditor in

the profession of auditing?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITOR’S INDEPENDENCE

c. What is the consequence of the size of the fee of audit on the auditor’s independence factor?

d. How does the audit agency capability influence the independence of the auditor?

1.6: Research Hypothesis

The research will be based on the following hypothesis:

H0- The other services that are provided by the auditors will not help in gaining a competitive

advantage

H1- The other services that are provided by the auditors will help in gaining a competitive

advantage

1.7 Significance of the Study:

The key importance or significance of the study lies in the fact that it would be shedding

light to proclaim the factors that impact on the independence and impartiality the external auditor

in the profession of auditor. The present study recognized by the several factors influencing the

auditor’s independence among the organizations in depicting the most consistent financial

statements. Auditors have been facing several challenges in their endeavor of ensuring ethical

and accurate depiction of the financial reports of the organization for which they work. The fact

that auditor is generally been employed or tapered by the corporations for which they are

auditing signifying they have been at the mercy of the employers and the way they illustrate

information is critical. This present study would shed light on the aspects and the ways they can

be functional in making the process of auditing appropriate. The upshot of the study would

importantly advance the knowledge frontier adding to the existing academic literature on the

independence of auditor.

AUDITOR’S INDEPENDENCE

c. What is the consequence of the size of the fee of audit on the auditor’s independence factor?

d. How does the audit agency capability influence the independence of the auditor?

1.6: Research Hypothesis

The research will be based on the following hypothesis:

H0- The other services that are provided by the auditors will not help in gaining a competitive

advantage

H1- The other services that are provided by the auditors will help in gaining a competitive

advantage

1.7 Significance of the Study:

The key importance or significance of the study lies in the fact that it would be shedding

light to proclaim the factors that impact on the independence and impartiality the external auditor

in the profession of auditor. The present study recognized by the several factors influencing the

auditor’s independence among the organizations in depicting the most consistent financial

statements. Auditors have been facing several challenges in their endeavor of ensuring ethical

and accurate depiction of the financial reports of the organization for which they work. The fact

that auditor is generally been employed or tapered by the corporations for which they are

auditing signifying they have been at the mercy of the employers and the way they illustrate

information is critical. This present study would shed light on the aspects and the ways they can

be functional in making the process of auditing appropriate. The upshot of the study would

importantly advance the knowledge frontier adding to the existing academic literature on the

independence of auditor.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITOR’S INDEPENDENCE

1.8 Structure of Dissertation:

This dissertation would be consisting of 5 segments or chapters that would be taken into

consideration by the researcher. The 1st chapter introduced the topic to the reader along with the

research questions, its objectives and significance of the same. The second chapter dealt with the

literature review on the subject, focusing on what the previous researches had to say or discussed

on the matter. The third chapter is about research methodology taking in the sorts of research

types and the ways data would be collected or gathered from various sources for analysis. The 4th

chapter is about the analysis part where the researcher would be evaluating the data gathered

from various sources. The last chapter is the conclusion and recommendation part where the

researcher would provide a full summary of the research along with suggestions on the things

that could be done to better the situation. The limitations of the study and the scope for future

research would be taken into account to for this research study.

AUDITOR’S INDEPENDENCE

1.8 Structure of Dissertation:

This dissertation would be consisting of 5 segments or chapters that would be taken into

consideration by the researcher. The 1st chapter introduced the topic to the reader along with the

research questions, its objectives and significance of the same. The second chapter dealt with the

literature review on the subject, focusing on what the previous researches had to say or discussed

on the matter. The third chapter is about research methodology taking in the sorts of research

types and the ways data would be collected or gathered from various sources for analysis. The 4th

chapter is about the analysis part where the researcher would be evaluating the data gathered

from various sources. The last chapter is the conclusion and recommendation part where the

researcher would provide a full summary of the research along with suggestions on the things

that could be done to better the situation. The limitations of the study and the scope for future

research would be taken into account to for this research study.

11

AUDITOR’S INDEPENDENCE

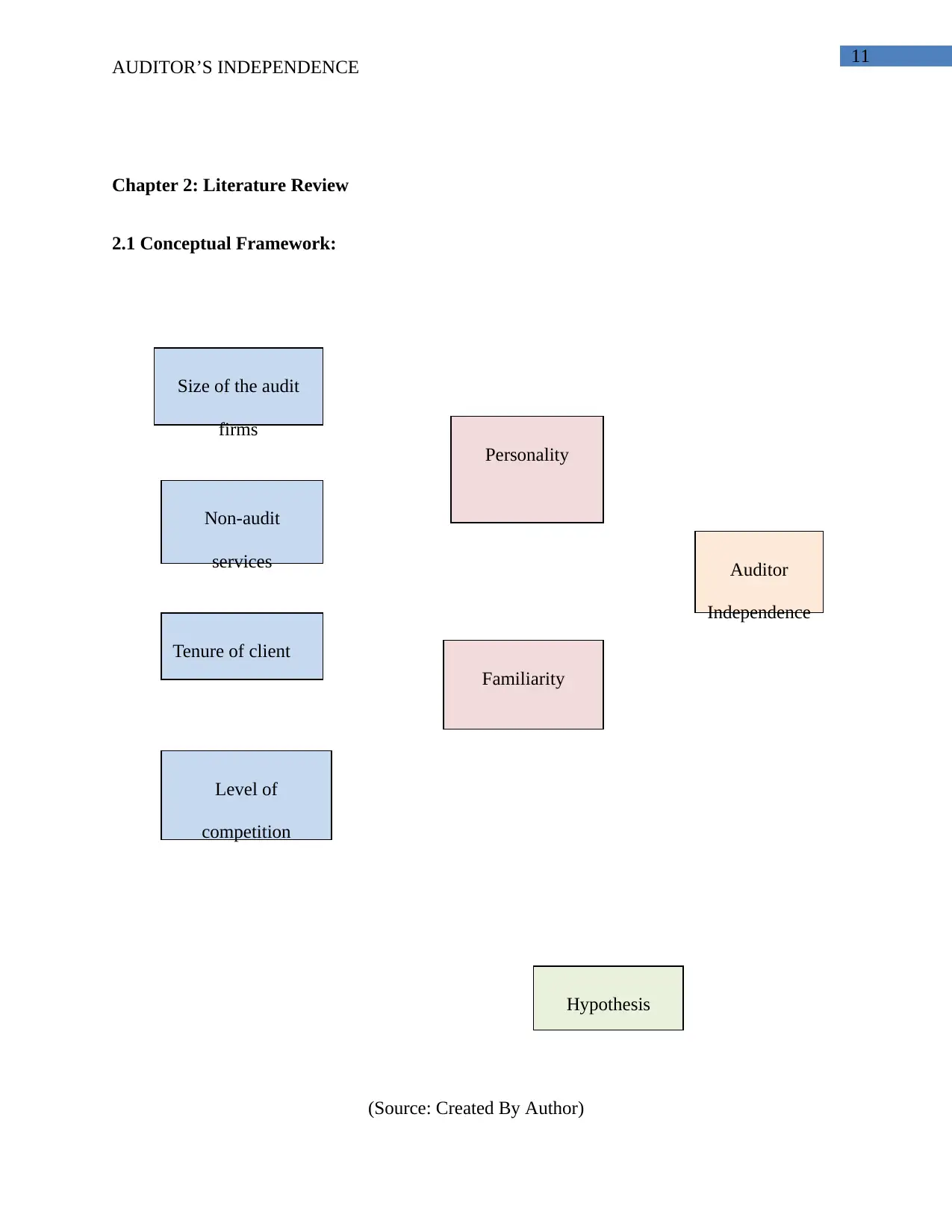

Chapter 2: Literature Review

2.1 Conceptual Framework:

(Source: Created By Author)

Size of the audit

firms

Non-audit

services

Tenure of client

Level of

competition

Personality

Familiarity

Auditor

Independence

Hypothesis

AUDITOR’S INDEPENDENCE

Chapter 2: Literature Review

2.1 Conceptual Framework:

(Source: Created By Author)

Size of the audit

firms

Non-audit

services

Tenure of client

Level of

competition

Personality

Familiarity

Auditor

Independence

Hypothesis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 82

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.