Difference Between Security Market Line

VerifiedAdded on 2021/06/15

|15

|3567

|32

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FIN201 Assignment, Trimester 1 2018

Investment management

‘

Investment management

‘

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Introduction................................................................................................................................4

Difference between Security Market Line (SML) and Capital Market Line (CML).................4

Importance of minimum variance portfolio...............................................................................8

Relevancy of CAPM in comparison to other equations...........................................................11

Conclusion................................................................................................................................13

References................................................................................................................................14

Introduction................................................................................................................................4

Difference between Security Market Line (SML) and Capital Market Line (CML).................4

Importance of minimum variance portfolio...............................................................................8

Relevancy of CAPM in comparison to other equations...........................................................11

Conclusion................................................................................................................................13

References................................................................................................................................14

LIST OF FIGURES

Figure 1: Capital market line graph...........................................................................................4

Figure 2: Security market line....................................................................................................6

Figure 3: Frontier of Minimum variance portfolio....................................................................8

Figure 4: Capital asset pricing model.......................................................................................10

Figure 1: Capital market line graph...........................................................................................4

Figure 2: Security market line....................................................................................................6

Figure 3: Frontier of Minimum variance portfolio....................................................................8

Figure 4: Capital asset pricing model.......................................................................................10

INTRODUCTION

The present study is based on evaluation advance concepts of investment portfolio

management in order to gain an understanding for making better investment decisions. In the

first part, the study will cover the difference between Security Market Line and Capital

Market Line by considering proper graph and its interpretation. Further, discussion of

minimum variance portfolio and its significance will be done by making use of relevant

examples. In the last part of the study; relevancy of CAPM model will be discussed in

comparison to another model available for computation of return on investment.

DIFFERENCE BETWEEN SECURITY MARKET LINE (SML)

AND CAPITAL MARKET LINE (CML)

The capital market line arises from the integration of free of risk asset and the market

portfolio. Every point together with the CML has premium profiles of risk-return to the

portfolio on the effective edge (Asness, Frazzini and Pedersen, 2012). Derivation of CML is

held by drawing a tangent line from the point of intercept upon the efficient frontier till when

the expected return is equivalent to the free of risk rate of return (Hodnett and Hsieh, 2012).

A line is put in use in the pricing approach of a capital asset to demonstrate the return rates

for the efficient portfolio based on the free of risk rate of return and the risk level, i.e.,

standards deviation for a specified portfolio (Lee and Su, 2014).

The CML is stated to be top-notch to the efficient frontier, as it considers the addition of risk-

free asset within the portfolio (Brown, 2012). The CAPM which stands for capital asset

pricing model illustrates that essentially the market portfolio is the efficient frontier.

Formula: E(Ri) = RF + SDc×{E(RM)-RF}/SDm

In which the SDC refers to a portfolio standard deviation C return, while the SDM is

regarded as a market-return standard deviation.

The present study is based on evaluation advance concepts of investment portfolio

management in order to gain an understanding for making better investment decisions. In the

first part, the study will cover the difference between Security Market Line and Capital

Market Line by considering proper graph and its interpretation. Further, discussion of

minimum variance portfolio and its significance will be done by making use of relevant

examples. In the last part of the study; relevancy of CAPM model will be discussed in

comparison to another model available for computation of return on investment.

DIFFERENCE BETWEEN SECURITY MARKET LINE (SML)

AND CAPITAL MARKET LINE (CML)

The capital market line arises from the integration of free of risk asset and the market

portfolio. Every point together with the CML has premium profiles of risk-return to the

portfolio on the effective edge (Asness, Frazzini and Pedersen, 2012). Derivation of CML is

held by drawing a tangent line from the point of intercept upon the efficient frontier till when

the expected return is equivalent to the free of risk rate of return (Hodnett and Hsieh, 2012).

A line is put in use in the pricing approach of a capital asset to demonstrate the return rates

for the efficient portfolio based on the free of risk rate of return and the risk level, i.e.,

standards deviation for a specified portfolio (Lee and Su, 2014).

The CML is stated to be top-notch to the efficient frontier, as it considers the addition of risk-

free asset within the portfolio (Brown, 2012). The CAPM which stands for capital asset

pricing model illustrates that essentially the market portfolio is the efficient frontier.

Formula: E(Ri) = RF + SDc×{E(RM)-RF}/SDm

In which the SDC refers to a portfolio standard deviation C return, while the SDM is

regarded as a market-return standard deviation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

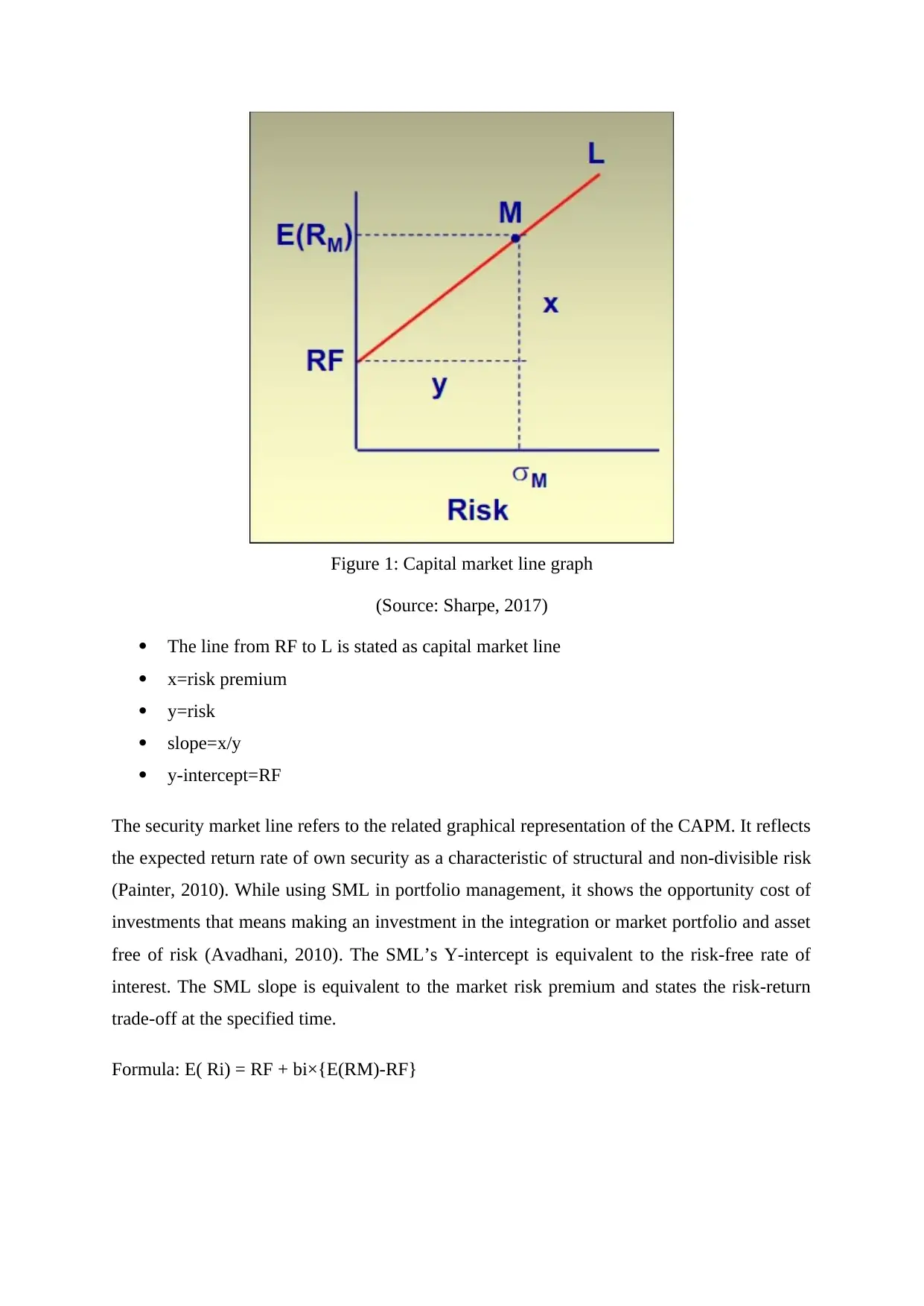

Figure 1: Capital market line graph

(Source: Sharpe, 2017)

The line from RF to L is stated as capital market line

x=risk premium

y=risk

slope=x/y

y-intercept=RF

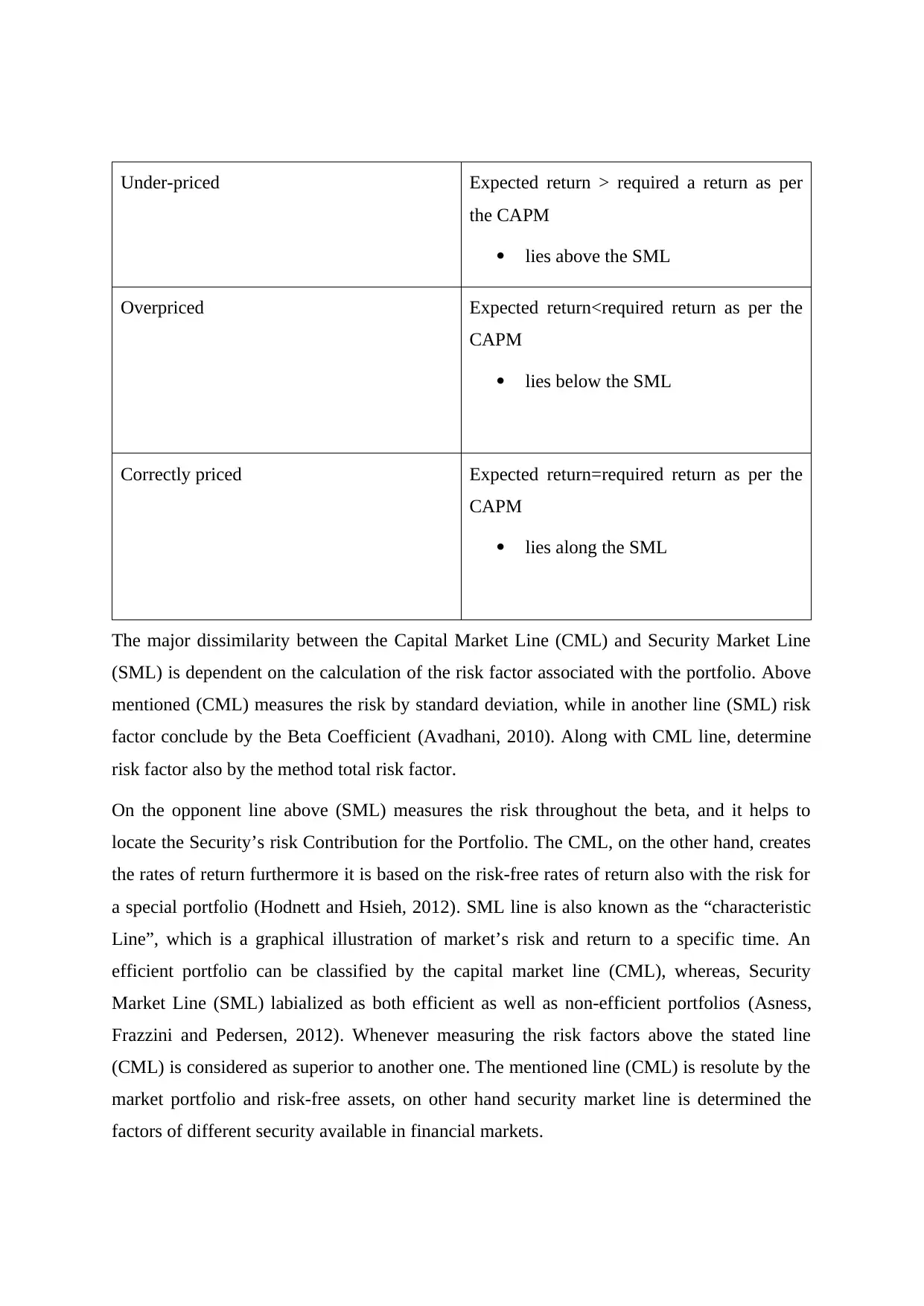

The security market line refers to the related graphical representation of the CAPM. It reflects

the expected return rate of own security as a characteristic of structural and non-divisible risk

(Painter, 2010). While using SML in portfolio management, it shows the opportunity cost of

investments that means making an investment in the integration or market portfolio and asset

free of risk (Avadhani, 2010). The SML’s Y-intercept is equivalent to the risk-free rate of

interest. The SML slope is equivalent to the market risk premium and states the risk-return

trade-off at the specified time.

Formula: E( Ri) = RF + bi×{E(RM)-RF}

(Source: Sharpe, 2017)

The line from RF to L is stated as capital market line

x=risk premium

y=risk

slope=x/y

y-intercept=RF

The security market line refers to the related graphical representation of the CAPM. It reflects

the expected return rate of own security as a characteristic of structural and non-divisible risk

(Painter, 2010). While using SML in portfolio management, it shows the opportunity cost of

investments that means making an investment in the integration or market portfolio and asset

free of risk (Avadhani, 2010). The SML’s Y-intercept is equivalent to the risk-free rate of

interest. The SML slope is equivalent to the market risk premium and states the risk-return

trade-off at the specified time.

Formula: E( Ri) = RF + bi×{E(RM)-RF}

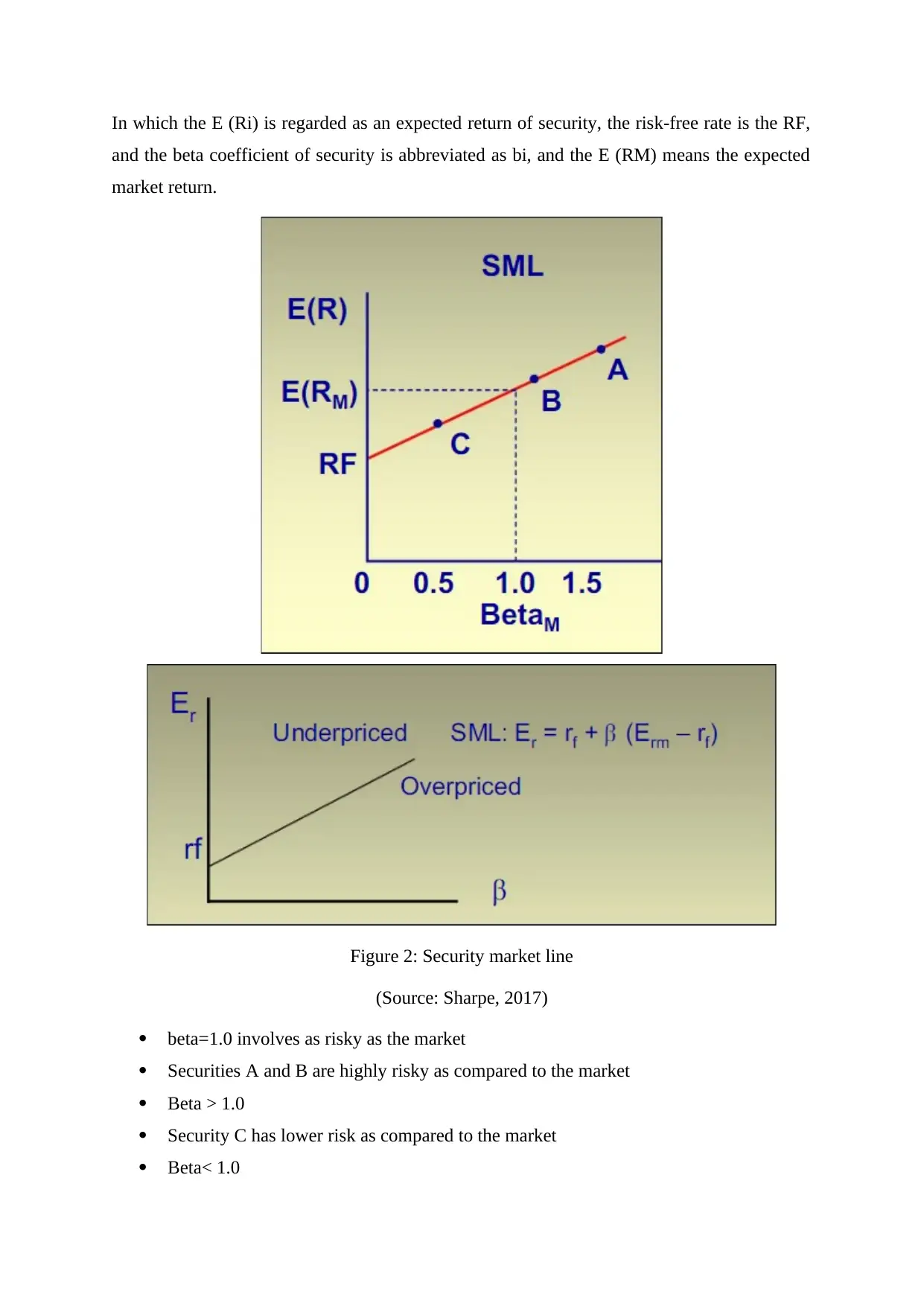

In which the E (Ri) is regarded as an expected return of security, the risk-free rate is the RF,

and the beta coefficient of security is abbreviated as bi, and the E (RM) means the expected

market return.

Figure 2: Security market line

(Source: Sharpe, 2017)

beta=1.0 involves as risky as the market

Securities A and B are highly risky as compared to the market

Beta > 1.0

Security C has lower risk as compared to the market

Beta< 1.0

and the beta coefficient of security is abbreviated as bi, and the E (RM) means the expected

market return.

Figure 2: Security market line

(Source: Sharpe, 2017)

beta=1.0 involves as risky as the market

Securities A and B are highly risky as compared to the market

Beta > 1.0

Security C has lower risk as compared to the market

Beta< 1.0

Under-priced Expected return > required a return as per

the CAPM

lies above the SML

Overpriced Expected return<required return as per the

CAPM

lies below the SML

Correctly priced Expected return=required return as per the

CAPM

lies along the SML

The major dissimilarity between the Capital Market Line (CML) and Security Market Line

(SML) is dependent on the calculation of the risk factor associated with the portfolio. Above

mentioned (CML) measures the risk by standard deviation, while in another line (SML) risk

factor conclude by the Beta Coefficient (Avadhani, 2010). Along with CML line, determine

risk factor also by the method total risk factor.

On the opponent line above (SML) measures the risk throughout the beta, and it helps to

locate the Security’s risk Contribution for the Portfolio. The CML, on the other hand, creates

the rates of return furthermore it is based on the risk-free rates of return also with the risk for

a special portfolio (Hodnett and Hsieh, 2012). SML line is also known as the “characteristic

Line”, which is a graphical illustration of market’s risk and return to a specific time. An

efficient portfolio can be classified by the capital market line (CML), whereas, Security

Market Line (SML) labialized as both efficient as well as non-efficient portfolios (Asness,

Frazzini and Pedersen, 2012). Whenever measuring the risk factors above the stated line

(CML) is considered as superior to another one. The mentioned line (CML) is resolute by the

market portfolio and risk-free assets, on other hand security market line is determined the

factors of different security available in financial markets.

the CAPM

lies above the SML

Overpriced Expected return<required return as per the

CAPM

lies below the SML

Correctly priced Expected return=required return as per the

CAPM

lies along the SML

The major dissimilarity between the Capital Market Line (CML) and Security Market Line

(SML) is dependent on the calculation of the risk factor associated with the portfolio. Above

mentioned (CML) measures the risk by standard deviation, while in another line (SML) risk

factor conclude by the Beta Coefficient (Avadhani, 2010). Along with CML line, determine

risk factor also by the method total risk factor.

On the opponent line above (SML) measures the risk throughout the beta, and it helps to

locate the Security’s risk Contribution for the Portfolio. The CML, on the other hand, creates

the rates of return furthermore it is based on the risk-free rates of return also with the risk for

a special portfolio (Hodnett and Hsieh, 2012). SML line is also known as the “characteristic

Line”, which is a graphical illustration of market’s risk and return to a specific time. An

efficient portfolio can be classified by the capital market line (CML), whereas, Security

Market Line (SML) labialized as both efficient as well as non-efficient portfolios (Asness,

Frazzini and Pedersen, 2012). Whenever measuring the risk factors above the stated line

(CML) is considered as superior to another one. The mentioned line (CML) is resolute by the

market portfolio and risk-free assets, on other hand security market line is determined the

factors of different security available in financial markets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Capital market line illustrates defined effective portfolio, and both effective and non-

effective portfolio is defined by the graph. When the returns are computed, the CML

portfolios expected return is demonstrated on the Y-axis (Antoniou, Doukas and

Subrahmanyam, 2015). On the contrary to this, for SML, the securities return is presented

with the

Y-axis, whereas for CML, The portfolio standard deviation is presented on the X-axis and for

SML, the Beta of security is represented on the X-axis.

Statement showing key differences among CML and SML

Capital market line Security market line

CML can be termed as graphical

representation of CAPM which shows

connection between total risk and proposed

return from the efficient portfolio.

SML can be termed as graphical

representation of CAPM which shows

connection between systematic risk and

return expected from individual stock asset.

In this, measurement of risk is done through

standard deviation which is also known as

total risk factor.

In this, measurement of risk is done through

beta as it assist in determining risk

contribution of security to the portfolio.

This graph defines merely efficient

portfolio.

This graph defines merely efficient as well

as non-efficient portfolio.

The market portfolio and assets which are free of risks are identified by CML whereas SML

identifies the security variables (Bierman and Smidt, 2012).

IMPORTANCE OF MINIMUM VARIANCE PORTFOLIO

The minimum variance portfolio can be defined as the risk-based approach used for the

construction of the portfolio. This concept indicates while forming portfolio instead of

considering the risk and return simultaneously; only risk is to be used in constructing

effective portfolio is defined by the graph. When the returns are computed, the CML

portfolios expected return is demonstrated on the Y-axis (Antoniou, Doukas and

Subrahmanyam, 2015). On the contrary to this, for SML, the securities return is presented

with the

Y-axis, whereas for CML, The portfolio standard deviation is presented on the X-axis and for

SML, the Beta of security is represented on the X-axis.

Statement showing key differences among CML and SML

Capital market line Security market line

CML can be termed as graphical

representation of CAPM which shows

connection between total risk and proposed

return from the efficient portfolio.

SML can be termed as graphical

representation of CAPM which shows

connection between systematic risk and

return expected from individual stock asset.

In this, measurement of risk is done through

standard deviation which is also known as

total risk factor.

In this, measurement of risk is done through

beta as it assist in determining risk

contribution of security to the portfolio.

This graph defines merely efficient

portfolio.

This graph defines merely efficient as well

as non-efficient portfolio.

The market portfolio and assets which are free of risks are identified by CML whereas SML

identifies the security variables (Bierman and Smidt, 2012).

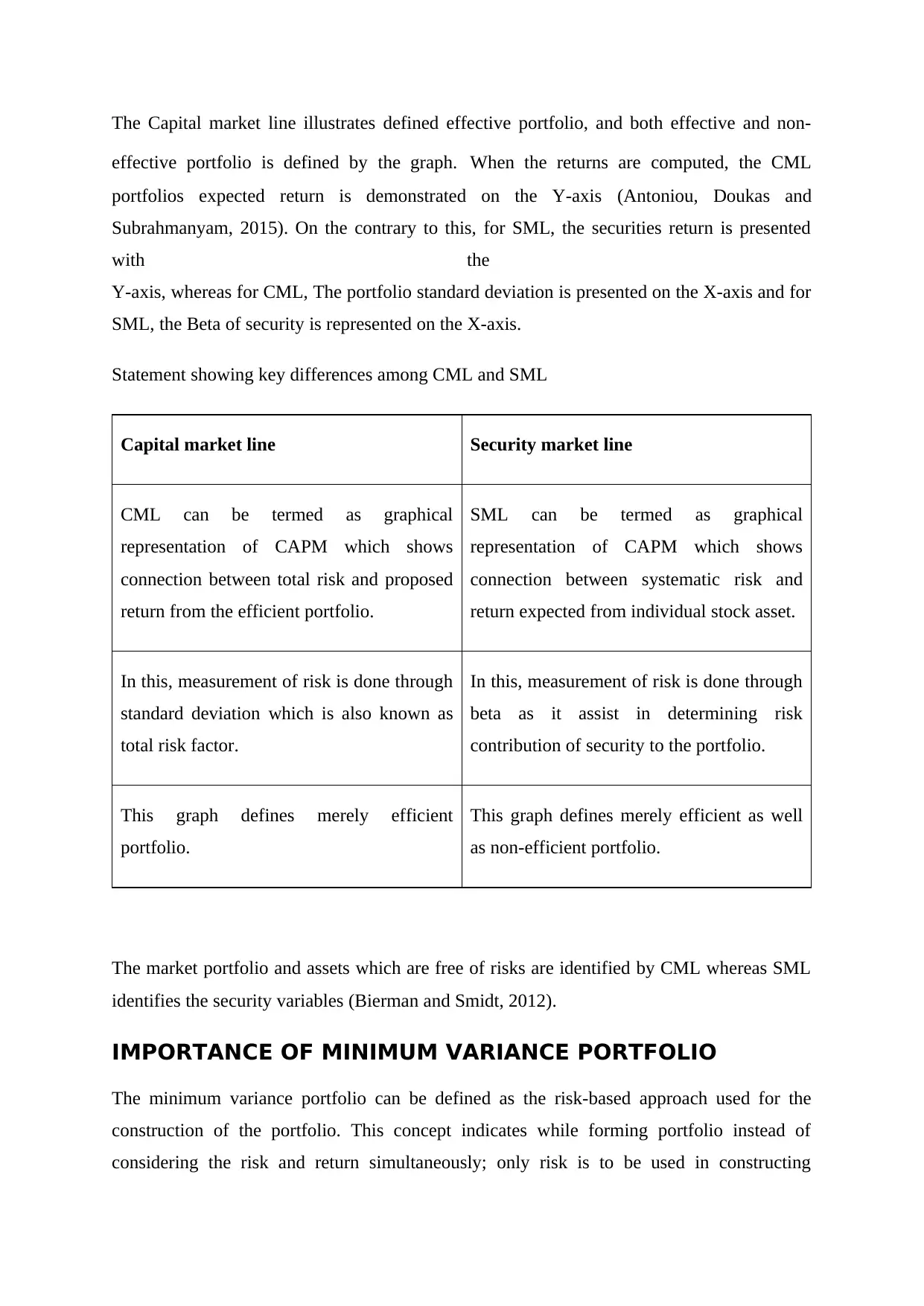

IMPORTANCE OF MINIMUM VARIANCE PORTFOLIO

The minimum variance portfolio can be defined as the risk-based approach used for the

construction of the portfolio. This concept indicates while forming portfolio instead of

considering the risk and return simultaneously; only risk is to be used in constructing

portfolio (Bodnar, Parolya and Schmid, 2018). This approach is viable for investors as the

determination of future returns is not an easy task and estimations made are not accurate in all

cases. Consideration of this aspect leads to forming a more robust portfolio that is less

subjected to estimation of risk. Computation of weights can be done by using following

formula for forming minimum variance portfolio for two assets:

Variance = (w(1)^2 xo(1)^2) + (w(2)^2 xo(2)^2) + (2 x (w(1)o(1)w(2)o(2)q(1,2))

In this formula

w (1) = the weight of the first asset in the portfolio

w (2) = the weight of the second asset in the portfolio

o (1) = the standard deviation of the first asset in the portfolio

o (2) = the standard deviation of the second asset in the portfolio

Cov (1,2) = the covariance of the portfolio for two assets, this can be sampled to

q(1,2)o(1)o(2), where q(1,2) is the correlation between the two assets selected for the

portfolio

Figure 3: Frontier of Minimum variance portfolio

determination of future returns is not an easy task and estimations made are not accurate in all

cases. Consideration of this aspect leads to forming a more robust portfolio that is less

subjected to estimation of risk. Computation of weights can be done by using following

formula for forming minimum variance portfolio for two assets:

Variance = (w(1)^2 xo(1)^2) + (w(2)^2 xo(2)^2) + (2 x (w(1)o(1)w(2)o(2)q(1,2))

In this formula

w (1) = the weight of the first asset in the portfolio

w (2) = the weight of the second asset in the portfolio

o (1) = the standard deviation of the first asset in the portfolio

o (2) = the standard deviation of the second asset in the portfolio

Cov (1,2) = the covariance of the portfolio for two assets, this can be sampled to

q(1,2)o(1)o(2), where q(1,2) is the correlation between the two assets selected for the

portfolio

Figure 3: Frontier of Minimum variance portfolio

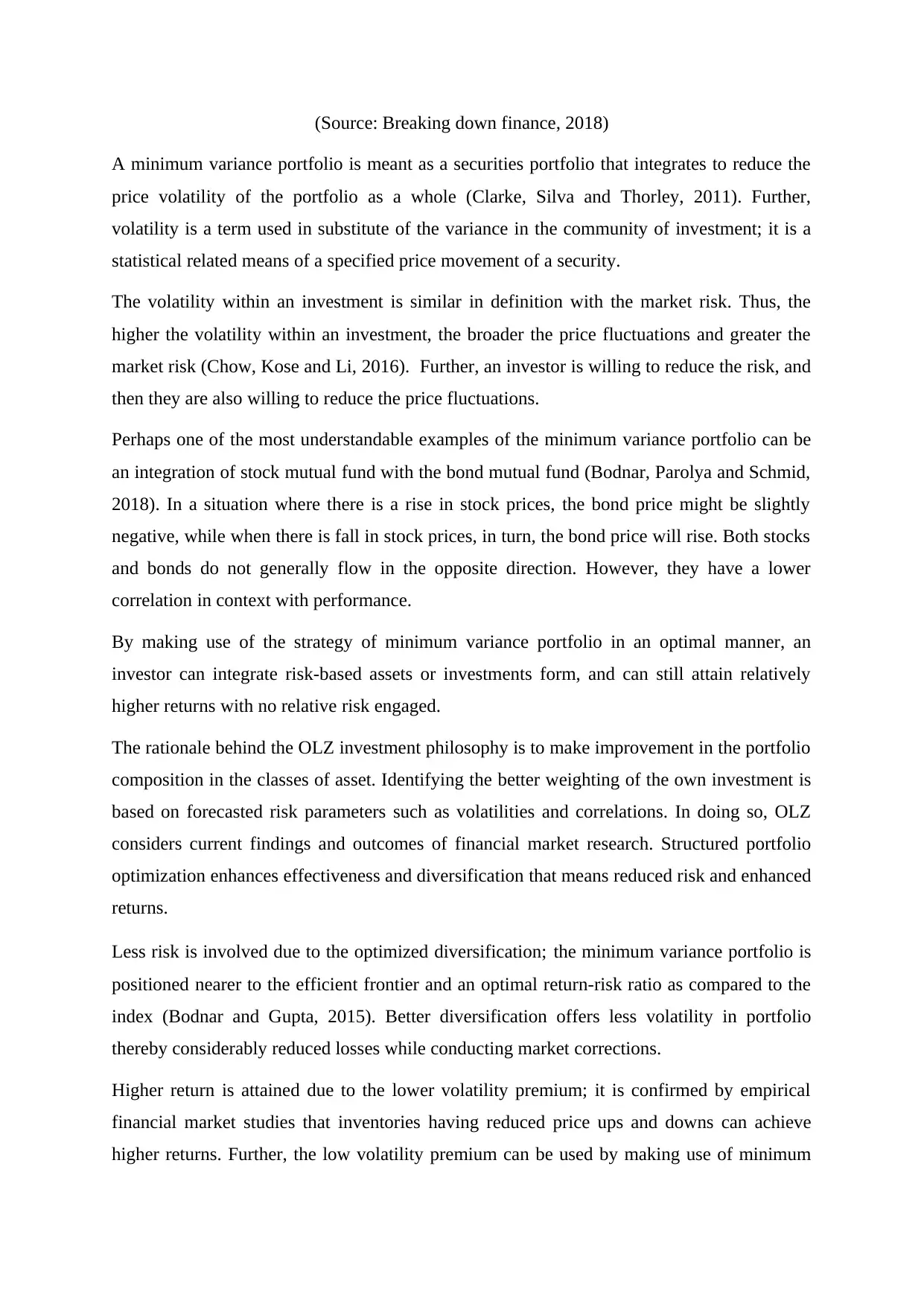

(Source: Breaking down finance, 2018)

A minimum variance portfolio is meant as a securities portfolio that integrates to reduce the

price volatility of the portfolio as a whole (Clarke, Silva and Thorley, 2011). Further,

volatility is a term used in substitute of the variance in the community of investment; it is a

statistical related means of a specified price movement of a security.

The volatility within an investment is similar in definition with the market risk. Thus, the

higher the volatility within an investment, the broader the price fluctuations and greater the

market risk (Chow, Kose and Li, 2016). Further, an investor is willing to reduce the risk, and

then they are also willing to reduce the price fluctuations.

Perhaps one of the most understandable examples of the minimum variance portfolio can be

an integration of stock mutual fund with the bond mutual fund (Bodnar, Parolya and Schmid,

2018). In a situation where there is a rise in stock prices, the bond price might be slightly

negative, while when there is fall in stock prices, in turn, the bond price will rise. Both stocks

and bonds do not generally flow in the opposite direction. However, they have a lower

correlation in context with performance.

By making use of the strategy of minimum variance portfolio in an optimal manner, an

investor can integrate risk-based assets or investments form, and can still attain relatively

higher returns with no relative risk engaged.

The rationale behind the OLZ investment philosophy is to make improvement in the portfolio

composition in the classes of asset. Identifying the better weighting of the own investment is

based on forecasted risk parameters such as volatilities and correlations. In doing so, OLZ

considers current findings and outcomes of financial market research. Structured portfolio

optimization enhances effectiveness and diversification that means reduced risk and enhanced

returns.

Less risk is involved due to the optimized diversification; the minimum variance portfolio is

positioned nearer to the efficient frontier and an optimal return-risk ratio as compared to the

index (Bodnar and Gupta, 2015). Better diversification offers less volatility in portfolio

thereby considerably reduced losses while conducting market corrections.

Higher return is attained due to the lower volatility premium; it is confirmed by empirical

financial market studies that inventories having reduced price ups and downs can achieve

higher returns. Further, the low volatility premium can be used by making use of minimum

A minimum variance portfolio is meant as a securities portfolio that integrates to reduce the

price volatility of the portfolio as a whole (Clarke, Silva and Thorley, 2011). Further,

volatility is a term used in substitute of the variance in the community of investment; it is a

statistical related means of a specified price movement of a security.

The volatility within an investment is similar in definition with the market risk. Thus, the

higher the volatility within an investment, the broader the price fluctuations and greater the

market risk (Chow, Kose and Li, 2016). Further, an investor is willing to reduce the risk, and

then they are also willing to reduce the price fluctuations.

Perhaps one of the most understandable examples of the minimum variance portfolio can be

an integration of stock mutual fund with the bond mutual fund (Bodnar, Parolya and Schmid,

2018). In a situation where there is a rise in stock prices, the bond price might be slightly

negative, while when there is fall in stock prices, in turn, the bond price will rise. Both stocks

and bonds do not generally flow in the opposite direction. However, they have a lower

correlation in context with performance.

By making use of the strategy of minimum variance portfolio in an optimal manner, an

investor can integrate risk-based assets or investments form, and can still attain relatively

higher returns with no relative risk engaged.

The rationale behind the OLZ investment philosophy is to make improvement in the portfolio

composition in the classes of asset. Identifying the better weighting of the own investment is

based on forecasted risk parameters such as volatilities and correlations. In doing so, OLZ

considers current findings and outcomes of financial market research. Structured portfolio

optimization enhances effectiveness and diversification that means reduced risk and enhanced

returns.

Less risk is involved due to the optimized diversification; the minimum variance portfolio is

positioned nearer to the efficient frontier and an optimal return-risk ratio as compared to the

index (Bodnar and Gupta, 2015). Better diversification offers less volatility in portfolio

thereby considerably reduced losses while conducting market corrections.

Higher return is attained due to the lower volatility premium; it is confirmed by empirical

financial market studies that inventories having reduced price ups and downs can achieve

higher returns. Further, the low volatility premium can be used by making use of minimum

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

variance portfolio in an optimal manner, due to the correlation among own investments are

also considered.

RELEVANCY OF CAPM IN COMPARISON TO OTHER

EQUATIONS

RRR which stands for required rate of return is an element in a lot of metrics implemented in

company finance and valuation of equity. The RRR depicts the requirement of profit in

commencing a project or investment (Fonseca, 2017). Further, RRR could be implemented in

order to aid investors in making a decision if or if not they shall proceed in purchasing

security. On the other hand, company executive and the finance expertise compute the RRR

for investments inclusive of the purchase of possible merger & acquisitions and production-

related equipment’s.

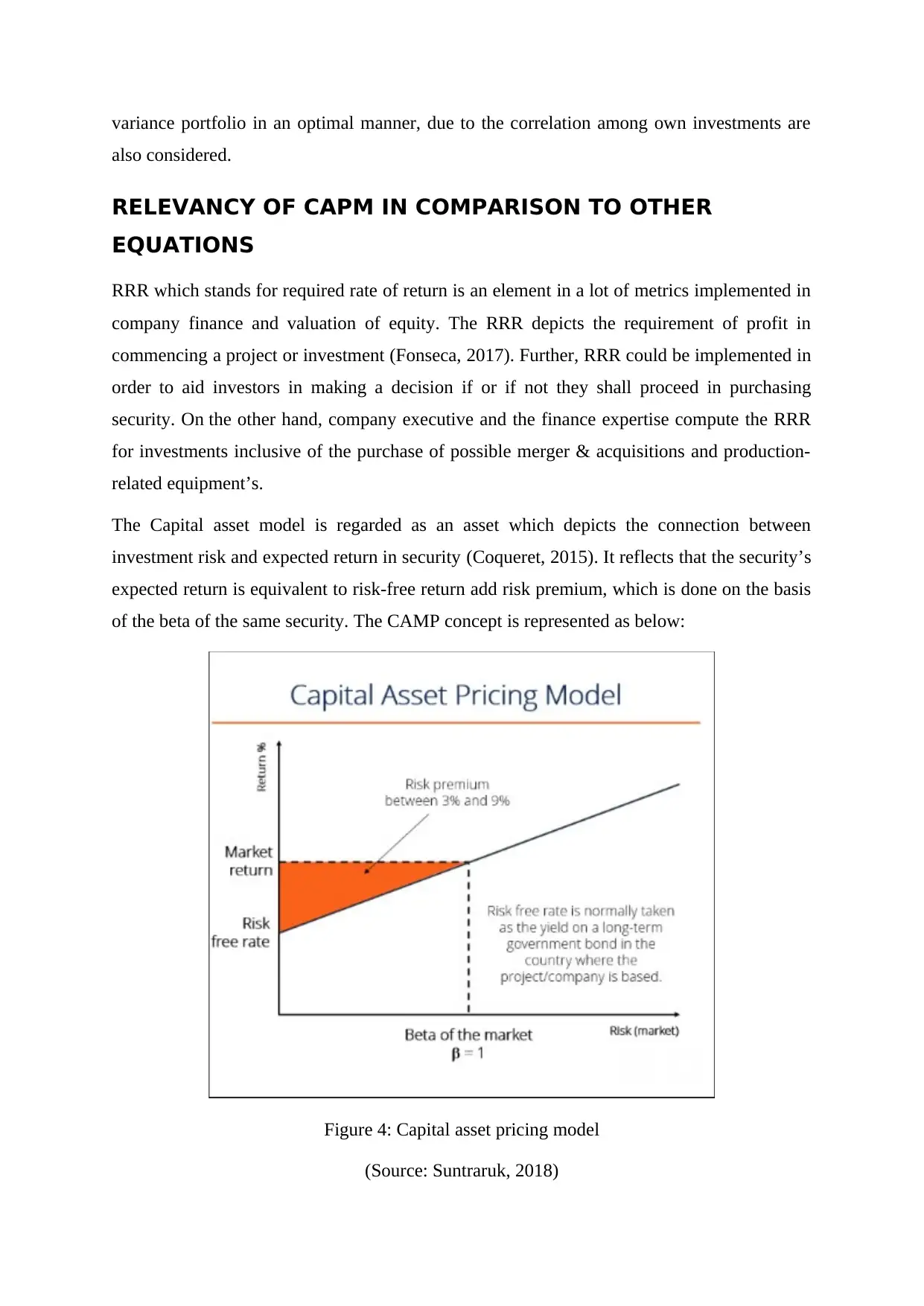

The Capital asset model is regarded as an asset which depicts the connection between

investment risk and expected return in security (Coqueret, 2015). It reflects that the security’s

expected return is equivalent to risk-free return add risk premium, which is done on the basis

of the beta of the same security. The CAMP concept is represented as below:

Figure 4: Capital asset pricing model

(Source: Suntraruk, 2018)

also considered.

RELEVANCY OF CAPM IN COMPARISON TO OTHER

EQUATIONS

RRR which stands for required rate of return is an element in a lot of metrics implemented in

company finance and valuation of equity. The RRR depicts the requirement of profit in

commencing a project or investment (Fonseca, 2017). Further, RRR could be implemented in

order to aid investors in making a decision if or if not they shall proceed in purchasing

security. On the other hand, company executive and the finance expertise compute the RRR

for investments inclusive of the purchase of possible merger & acquisitions and production-

related equipment’s.

The Capital asset model is regarded as an asset which depicts the connection between

investment risk and expected return in security (Coqueret, 2015). It reflects that the security’s

expected return is equivalent to risk-free return add risk premium, which is done on the basis

of the beta of the same security. The CAMP concept is represented as below:

Figure 4: Capital asset pricing model

(Source: Suntraruk, 2018)

The formula of CAPM is broadly used in the financial sector by several occupations like an

accountant, investment bankers and financial analysts (Fernandez, 2015). It is considered as

an important aspect of the weighted average cost of capital as CAPM helps in calculating the

equity costs.

The formula of CAPM has continued in viable over 40 years of investment analysis due to its

various benefits in comparison to other methods (Coqueret, 2015). One of the major reason,

due to which CAPM is viable that it solely focused on systematic risk while computing rate

of return (Zabarankin, Pavlikov and Uryasev, 2014). This factor indicates the realism that

diversified portfolios fundamentally disregarded all the unsystematic risk stanching from

characteristics of individual asset investment (Fonseca, 2017). This presumption is valid

because; diversification of systematic risk cannot be done, and it is integral to the entire stock

market or to the particular market segment.

WACC is also used immensely in the financial model; it can be implemented to look out for

the NPV and future cash inflows and outflows of the made investment. Additionally, it

computes the entity’s value and ultimately reaches computing equity value (Zabarankin,

Pavlikov and Uryasev, 2014).

CAPM comes with various benefits; it is a calculation which is simple to use that can be

easily tested to gain a variety of potential results for providing confidence with the RRR.

CAPM considers systematic risk, which is apart from other methods, like dividend discount

model. It is also known as market risk and is considered as a significant factor, as it is

unexpected and generally it is not possible to entirely mitigate it as it is not completely

expected. The theory that investors retain a diversified portfolio, same as the market portfolio

makes reduction the unsystematic risk (Suntraruk, 2018). While business lookout for

opportunities, is the mix of business and financial aspects vary from the existing business,

then the other calculations of required return such as the WACC cannot be implemented, but

CAPM can be used (Coqueret, 2015).

CAPM model assists investors to determine the price they should pay for the particular

security by determining its fair price. For example, one stock is comparatively riskier than

other stock; the price of the stock will also fluctuate as per the risk. Same aspects are applied

to the rate of return provided by stock; higher the rate indicates higher market price and vice

versa (Zabarankin, Pavlikov and Uryasev, 2014). Therefore; this model is generally used for

the purpose of determining fair price of investment to be made by the investor. In situation;

accountant, investment bankers and financial analysts (Fernandez, 2015). It is considered as

an important aspect of the weighted average cost of capital as CAPM helps in calculating the

equity costs.

The formula of CAPM has continued in viable over 40 years of investment analysis due to its

various benefits in comparison to other methods (Coqueret, 2015). One of the major reason,

due to which CAPM is viable that it solely focused on systematic risk while computing rate

of return (Zabarankin, Pavlikov and Uryasev, 2014). This factor indicates the realism that

diversified portfolios fundamentally disregarded all the unsystematic risk stanching from

characteristics of individual asset investment (Fonseca, 2017). This presumption is valid

because; diversification of systematic risk cannot be done, and it is integral to the entire stock

market or to the particular market segment.

WACC is also used immensely in the financial model; it can be implemented to look out for

the NPV and future cash inflows and outflows of the made investment. Additionally, it

computes the entity’s value and ultimately reaches computing equity value (Zabarankin,

Pavlikov and Uryasev, 2014).

CAPM comes with various benefits; it is a calculation which is simple to use that can be

easily tested to gain a variety of potential results for providing confidence with the RRR.

CAPM considers systematic risk, which is apart from other methods, like dividend discount

model. It is also known as market risk and is considered as a significant factor, as it is

unexpected and generally it is not possible to entirely mitigate it as it is not completely

expected. The theory that investors retain a diversified portfolio, same as the market portfolio

makes reduction the unsystematic risk (Suntraruk, 2018). While business lookout for

opportunities, is the mix of business and financial aspects vary from the existing business,

then the other calculations of required return such as the WACC cannot be implemented, but

CAPM can be used (Coqueret, 2015).

CAPM model assists investors to determine the price they should pay for the particular

security by determining its fair price. For example, one stock is comparatively riskier than

other stock; the price of the stock will also fluctuate as per the risk. Same aspects are applied

to the rate of return provided by stock; higher the rate indicates higher market price and vice

versa (Zabarankin, Pavlikov and Uryasev, 2014). Therefore; this model is generally used for

the purpose of determining fair price of investment to be made by the investor. In situation;

where investor determines the return on risk assets, they can apply time value of money to

compute the present value of investment in order to make a viable choice. By extending this

analysis, an investor can compare their fair to market value and can plan for bargain

strategies as per the concerned case of overstatement or understatement.

It can be said that no model is ideal, but every model has its own traits that make them

applicable and beneficial. CAPM has been criticized for its unreasonable estimations, offers

highly useful results as compared to DDM or WACC, in most of the events (Dhrymes, 2017).

The calculation of CAPM is easy, and while using it in conjunction with other investment

mosaic aspects, it can offer supreme yield data, supporting or reducing a possible investment.

CONCLUSION

In accordance with the present study; conclusion can be drawn that it is important for

investors to understand each and every factor of tools and components of investment in order

to have a better understanding of the market. Study concludes that the primary dissimilarity

between the Capital Market Line and Security Market Line is reliant on on the calculation of

the risk factor associated with the portfolio. Further; the market portfolio and security assets

which are free of risks are identified by CML whereas SML identifies the security variables.

The present study shows that by using of suitable tools like CAPM and minimum variance

portfolio investor can make suitable choice to get desire return within their risk appetite.

compute the present value of investment in order to make a viable choice. By extending this

analysis, an investor can compare their fair to market value and can plan for bargain

strategies as per the concerned case of overstatement or understatement.

It can be said that no model is ideal, but every model has its own traits that make them

applicable and beneficial. CAPM has been criticized for its unreasonable estimations, offers

highly useful results as compared to DDM or WACC, in most of the events (Dhrymes, 2017).

The calculation of CAPM is easy, and while using it in conjunction with other investment

mosaic aspects, it can offer supreme yield data, supporting or reducing a possible investment.

CONCLUSION

In accordance with the present study; conclusion can be drawn that it is important for

investors to understand each and every factor of tools and components of investment in order

to have a better understanding of the market. Study concludes that the primary dissimilarity

between the Capital Market Line and Security Market Line is reliant on on the calculation of

the risk factor associated with the portfolio. Further; the market portfolio and security assets

which are free of risks are identified by CML whereas SML identifies the security variables.

The present study shows that by using of suitable tools like CAPM and minimum variance

portfolio investor can make suitable choice to get desire return within their risk appetite.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Hodnett, K. and Hsieh, H.H., 2012. Capital market theories: Market efficiency versus

investor prospects. The International Business & Economics Research Journal

(Online), 11(8), p.849.

Brown, R., 2012. Analysis of investments & management of portfolios.

Painter, M.J., 2010. The portfolio diversification impact of a farmland real estate investment

trust. The International Business & Economics Research Journal, 9(5), p.115.

Avadhani, V.A., 2010. Investment management. Himalaya Publishing House.

Asness, C.S., Frazzini, A. and Pedersen, L.H., 2012. Leverage aversion and risk

parity. Financial Analysts Journal, 68(1), pp.47-59.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Antoniou, C., Doukas, J.A. and Subrahmanyam, A., 2015. Investor sentiment, beta, and the

cost of equity capital. Management Science, 62(2), pp.347-367.

Sharpe, W., 2017. Capital Market Theory, Efficiency, and Imperfections. Quantitative

Financial Analytics: The Path to Investment Profits, p.445.

Fonseca, R.J., 2017, September. Capital Asset Pricing Model—A Structured Robust

Approach. In International Conference on Optimization and Decision Science (pp. 385-392).

Springer, Cham.

Suntraruk, P., 2018. A simple test pf the CAPM Model under Bull and Bear market

conditions. AU Journal of Management, 6(1), pp.62-70.

Fernandez, P., 2015. CAPM: an absurd model. Business Valuation Review, 34(1), pp.4-23.

Zabarankin, M., Pavlikov, K. and Uryasev, S., 2014. Capital asset pricing model (CAPM)

with drawdown measure. European Journal of Operational Research, 234(2), pp.508-517.

Dhrymes, P.J., 2017. Portfolio Theory: Origins, Markowitz and CAPM Based Selection. In

Portfolio Construction, Measurement, and Efficiency (pp. 39-48). Springer, Cham.

Hodnett, K. and Hsieh, H.H., 2012. Capital market theories: Market efficiency versus

investor prospects. The International Business & Economics Research Journal

(Online), 11(8), p.849.

Brown, R., 2012. Analysis of investments & management of portfolios.

Painter, M.J., 2010. The portfolio diversification impact of a farmland real estate investment

trust. The International Business & Economics Research Journal, 9(5), p.115.

Avadhani, V.A., 2010. Investment management. Himalaya Publishing House.

Asness, C.S., Frazzini, A. and Pedersen, L.H., 2012. Leverage aversion and risk

parity. Financial Analysts Journal, 68(1), pp.47-59.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Antoniou, C., Doukas, J.A. and Subrahmanyam, A., 2015. Investor sentiment, beta, and the

cost of equity capital. Management Science, 62(2), pp.347-367.

Sharpe, W., 2017. Capital Market Theory, Efficiency, and Imperfections. Quantitative

Financial Analytics: The Path to Investment Profits, p.445.

Fonseca, R.J., 2017, September. Capital Asset Pricing Model—A Structured Robust

Approach. In International Conference on Optimization and Decision Science (pp. 385-392).

Springer, Cham.

Suntraruk, P., 2018. A simple test pf the CAPM Model under Bull and Bear market

conditions. AU Journal of Management, 6(1), pp.62-70.

Fernandez, P., 2015. CAPM: an absurd model. Business Valuation Review, 34(1), pp.4-23.

Zabarankin, M., Pavlikov, K. and Uryasev, S., 2014. Capital asset pricing model (CAPM)

with drawdown measure. European Journal of Operational Research, 234(2), pp.508-517.

Dhrymes, P.J., 2017. Portfolio Theory: Origins, Markowitz and CAPM Based Selection. In

Portfolio Construction, Measurement, and Efficiency (pp. 39-48). Springer, Cham.

Bodnar, T. and Gupta, A.K., 2015. Robustness of the inference procedures for the global

minimum variance portfolio weights in a skew-normal model. The European Journal of

Finance, 21(13-14), pp.1176-1194.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-

390.

Clarke, R., De Silva, H. and Thorley, S., 2011. Minimum-variance portfolio composition.

Journal of Portfolio Management, 37(2), p.31.

Chow, T.M., Kose, E. and Li, F., 2016. The impact of constraints on minimum-variance

portfolios. Financial Analysts Journal, 72(2), pp.52-70.

Coqueret, G., 2015. Diversified minimum-variance portfolios. Annals of Finance, 11(2),

pp.221-241.

Lee, M.C. and Su, L.E., 2014. Capital Market Line Based on Efficient Frontier of Portfolio

with Borrowing and Lending Rate. Universal Journal of Accounting and Finance, 2(4),

pp.69-76.

Breaking down finance, 2018. Minimum variance portfolio. Available through <

http://breakingdownfinance.com/finance-topics/modern-portfolio-theory/minimum-variance-

portfolio/>. [Accessed on 22nd May 2018].

minimum variance portfolio weights in a skew-normal model. The European Journal of

Finance, 21(13-14), pp.1176-1194.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-

390.

Clarke, R., De Silva, H. and Thorley, S., 2011. Minimum-variance portfolio composition.

Journal of Portfolio Management, 37(2), p.31.

Chow, T.M., Kose, E. and Li, F., 2016. The impact of constraints on minimum-variance

portfolios. Financial Analysts Journal, 72(2), pp.52-70.

Coqueret, G., 2015. Diversified minimum-variance portfolios. Annals of Finance, 11(2),

pp.221-241.

Lee, M.C. and Su, L.E., 2014. Capital Market Line Based on Efficient Frontier of Portfolio

with Borrowing and Lending Rate. Universal Journal of Accounting and Finance, 2(4),

pp.69-76.

Breaking down finance, 2018. Minimum variance portfolio. Available through <

http://breakingdownfinance.com/finance-topics/modern-portfolio-theory/minimum-variance-

portfolio/>. [Accessed on 22nd May 2018].

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.