FIN3322: Bank Management - Analyzing Bank Performance Report 2016

VerifiedAdded on 2021/10/09

|66

|15517

|73

Report

AI Summary

This report provides a comprehensive analysis of the financial performance of Hatton National Bank (HNB) and Commercial Bank of Ceylon PLC, two leading commercial banks in Sri Lanka. The analysis includes a comparative study of their products, achievements, and financial ratios, covering profitability, activity, leverage, and market ratios. The report delves into common-size financial statements, interpretation of ratios, and Due Pont analysis for both banks. Furthermore, it examines the CAMELS framework, assessing capital adequacy, asset quality, management quality, earnings, liquidity, and sensitivity. The risk management frameworks, including credit, market, liquidity, operational, reputational, and legal risks, are also evaluated. The report also includes a detailed examination of capital adequacy and liquidity management, along with non-performing loans management. The report is based on the FIN3322 Bank Management course at the University of Sri Jayewardenepura.

FIN3322: Bank Management

Group Assignment 2016

Analyzing Bank Performance

By

Department of Finance

2016

Group Assignment 2016

Analyzing Bank Performance

By

Department of Finance

2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FIN3322: Bank Management

Group Assignment 2016

Analyzing Bank Performance -Hatton

National Bank & Commercial Bank

By

Department of Finance

This Report submitted to the Department of Finance,

Faculty of Management Studies and Commerce, University of Sri Jayewardenepura, as a

partial fulfillment of the requirement of FIN:3322 Bank Management course

2016

Group Assignment 2016

Analyzing Bank Performance -Hatton

National Bank & Commercial Bank

By

Department of Finance

This Report submitted to the Department of Finance,

Faculty of Management Studies and Commerce, University of Sri Jayewardenepura, as a

partial fulfillment of the requirement of FIN:3322 Bank Management course

2016

Declaration

We certify that this project report does not incorporate without acknowledgement, any material

previously submitted for a course or a degree in any university, and to the best of our knowledge

and belief it does not contain any material previously published or written by another person,

except where reference is made in the text.

No. CPM Number MC Number Name of the Member Signature

01 10473 70155 M.L.N. Premarathne

02 11966 73973 W.K.A. Wanniarachchi

03 12002 73388 C.A Halambaarachchi

04 12079 73264 K.P.M Kumari De Silva

05 12089 73551 G.C. Lakshika

06 12096 73649 P.I. Nilmini

07 12225 73248 D.S.Dahanayake

08 12361 73775 R.A.V. Ransinghe

09 12386 73818 K.V.D.Sakunika

10 12521 73393 K.W.C. Harshima

We certify that this project report does not incorporate without acknowledgement, any material

previously submitted for a course or a degree in any university, and to the best of our knowledge

and belief it does not contain any material previously published or written by another person,

except where reference is made in the text.

No. CPM Number MC Number Name of the Member Signature

01 10473 70155 M.L.N. Premarathne

02 11966 73973 W.K.A. Wanniarachchi

03 12002 73388 C.A Halambaarachchi

04 12079 73264 K.P.M Kumari De Silva

05 12089 73551 G.C. Lakshika

06 12096 73649 P.I. Nilmini

07 12225 73248 D.S.Dahanayake

08 12361 73775 R.A.V. Ransinghe

09 12386 73818 K.V.D.Sakunika

10 12521 73393 K.W.C. Harshima

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Acknowledgment

First and foremost, we would like to thank our Bank Management lecturer Mr. Wickrama

Narayana and our tutorial coordinator Ms. Gayani Kaushalya for the guidance and the

understanding provided towards achieving this assignment as a successful one.

Then we take this opportunity to convey our sincere gratitude to our beloved parents for

being with us.

Last but not least, we should acknowledge our group members who work together to get

this assignment as a successful one.

i

First and foremost, we would like to thank our Bank Management lecturer Mr. Wickrama

Narayana and our tutorial coordinator Ms. Gayani Kaushalya for the guidance and the

understanding provided towards achieving this assignment as a successful one.

Then we take this opportunity to convey our sincere gratitude to our beloved parents for

being with us.

Last but not least, we should acknowledge our group members who work together to get

this assignment as a successful one.

i

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Commercial Bank of Ceylon PLC.........................................................................................................1

Products.............................................................................................................................................1

Achievements....................................................................................................................................2

Hatton National Bank PLC....................................................................................................................3

Produts...............................................................................................................................................3

Achievements....................................................................................................................................4

Ratio Analysis.......................................................................................................................................5

Ratio calculation of Hatton National Bank........................................................................................5

Ratio calculation of Commercial Bank..............................................................................................9

Common size Financial Statements.................................................................................................12

Interpretation of Ratios....................................................................................................................18

Interpretation of Common Size Statements.....................................................................................22

Due Pont Analysis...............................................................................................................................25

Commercial Bank............................................................................................................................25

Hatton National Bank......................................................................................................................26

CAMELS Framework..........................................................................................................................28

Capital Adequacy............................................................................................................................29

Asset Quality...................................................................................................................................29

Management Quality.......................................................................................................................31

Smart Schools’ initiative..................................................................................................................32

Earnings...........................................................................................................................................33

Liquidity..........................................................................................................................................34

Sensitivity Analysis.........................................................................................................................34

Risk Management Framework.............................................................................................................35

Credit Risk.......................................................................................................................................39

Market risk......................................................................................................................................44

Liquidity risk...................................................................................................................................45

Operational Risk..............................................................................................................................48

Reputational risk..............................................................................................................................50

Legal and Documentation Risk........................................................................................................50

Capital Adequacy Ratio.......................................................................................................................52

Liquidity Management........................................................................................................................54

Non-Performing Loans Management...................................................................................................56

ii

Commercial Bank of Ceylon PLC.........................................................................................................1

Products.............................................................................................................................................1

Achievements....................................................................................................................................2

Hatton National Bank PLC....................................................................................................................3

Produts...............................................................................................................................................3

Achievements....................................................................................................................................4

Ratio Analysis.......................................................................................................................................5

Ratio calculation of Hatton National Bank........................................................................................5

Ratio calculation of Commercial Bank..............................................................................................9

Common size Financial Statements.................................................................................................12

Interpretation of Ratios....................................................................................................................18

Interpretation of Common Size Statements.....................................................................................22

Due Pont Analysis...............................................................................................................................25

Commercial Bank............................................................................................................................25

Hatton National Bank......................................................................................................................26

CAMELS Framework..........................................................................................................................28

Capital Adequacy............................................................................................................................29

Asset Quality...................................................................................................................................29

Management Quality.......................................................................................................................31

Smart Schools’ initiative..................................................................................................................32

Earnings...........................................................................................................................................33

Liquidity..........................................................................................................................................34

Sensitivity Analysis.........................................................................................................................34

Risk Management Framework.............................................................................................................35

Credit Risk.......................................................................................................................................39

Market risk......................................................................................................................................44

Liquidity risk...................................................................................................................................45

Operational Risk..............................................................................................................................48

Reputational risk..............................................................................................................................50

Legal and Documentation Risk........................................................................................................50

Capital Adequacy Ratio.......................................................................................................................52

Liquidity Management........................................................................................................................54

Non-Performing Loans Management...................................................................................................56

ii

Table of Figures

Figure 1 Commercial Bank Logo 1

Figure 2 HNB Logo 3

Figure 3 Duepont Analysis for Commercial Bank 25

Figure 4 Duepont ANalysis for Commercial Bank 26

Figure 5 Sectoral Distribution of Loans -Commercial Bank 30

Figure 6 - Sectoral Distribution of Loans as a percentage 30

Figure 7 Risk Government Strucute for HNB 37

Figure 8 HNB's Risk Profile 38

Figure 9 Commercial Bank Financial Risk Management Framework 39

Figure 10 Non-performing Advances 40

Figure 11 Credit Risk Management Cycle 41

Figure 12 Loan Portfolio 44

Figure 13 HNB Liquidity Gap Analysis 46

Figure 14 Liquidity Ratios 47

Figure 15 Exposure to Liquidity Risk 47

Figure 16 Liquidity Ratios 48

Figure 17 Liquidity Reserves 48

Figure 18 Key Risk Indicators 50

Figure 19 NPA Ratio 57

iii

Figure 1 Commercial Bank Logo 1

Figure 2 HNB Logo 3

Figure 3 Duepont Analysis for Commercial Bank 25

Figure 4 Duepont ANalysis for Commercial Bank 26

Figure 5 Sectoral Distribution of Loans -Commercial Bank 30

Figure 6 - Sectoral Distribution of Loans as a percentage 30

Figure 7 Risk Government Strucute for HNB 37

Figure 8 HNB's Risk Profile 38

Figure 9 Commercial Bank Financial Risk Management Framework 39

Figure 10 Non-performing Advances 40

Figure 11 Credit Risk Management Cycle 41

Figure 12 Loan Portfolio 44

Figure 13 HNB Liquidity Gap Analysis 46

Figure 14 Liquidity Ratios 47

Figure 15 Exposure to Liquidity Risk 47

Figure 16 Liquidity Ratios 48

Figure 17 Liquidity Reserves 48

Figure 18 Key Risk Indicators 50

Figure 19 NPA Ratio 57

iii

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Executive Summary

Our report concentrates on analyzing the financial performance of two most private leading

commercial banks in Sri Lanka, namely commercial Bank of Ceylon PLC and Hatton

National Bank PLC.

Instead of comparing two time periods of the same commercial bank, in our report we have

comparatively analyzed the same time duration of two different award winning commercial

banks in Sri Lanka. Our analysis on commercial bank and HNB bank has covered the areas

of,

Financial position statement ratios and numbers

Comprehensive income statement ratios and numbers

Due Pont analysis for each bank

CAMELS Framework

Risk management framework of each bank

Capital adequacy calculation

Liquidity management

iv

Our report concentrates on analyzing the financial performance of two most private leading

commercial banks in Sri Lanka, namely commercial Bank of Ceylon PLC and Hatton

National Bank PLC.

Instead of comparing two time periods of the same commercial bank, in our report we have

comparatively analyzed the same time duration of two different award winning commercial

banks in Sri Lanka. Our analysis on commercial bank and HNB bank has covered the areas

of,

Financial position statement ratios and numbers

Comprehensive income statement ratios and numbers

Due Pont analysis for each bank

CAMELS Framework

Risk management framework of each bank

Capital adequacy calculation

Liquidity management

iv

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Commercial Bank of Ceylon PLC.

Commercial Bank of Ceylon PLC is an award winning Commercial Bank in Sri Lanka with

205 branches and an ATM network of 625 ATMs. It established under the vision of,

"To be the most technologically advanced, innovative and customer friendly financial

services organization in Sri Lanka, poised for further expansion in South Asia".

The birth of the bank occurred in 1920s, during the pre-independence era and currently

expanded its operations to Bangladesh as well. The bank has won several awards including

‘The Strongest Bank in Sri Lanka in 2016’award by the Asian Banker and “The Most

Respected Bank in Sri Lanka – 2016” by LMD rankings. With the commitment of the bank

current Chairman Mr. K. G. D. D. Dheerasinghe and his team, the bank is moving forward

being a successful Commercial Bank in Sri Lanka.

Products

Savings

o Regular Savings Account

o Super Saver Account

o RFC Savings Account

o Power Savings Account

o Udara Senior Citizens Account

o Arunalu Children’s Savings Account

o Isuru Minor’s Savings Account

o DotCom Youth Savings Account

Deposits and Investments

o Millionaire Account

o Money Market Accounts

o Treasury Bonds

o Treasury Bills

o Fixed Deposits

o Call Deposits

o RFC Fixed Deposits

Current Accounts

o Current Accounts

o Achiever Current Accounts

Loans

o Home Loans

o Foreign Currency Home Loans

o Personal Loans

Figure 1 Commercial Bank Logo

Commercial Bank of Ceylon PLC is an award winning Commercial Bank in Sri Lanka with

205 branches and an ATM network of 625 ATMs. It established under the vision of,

"To be the most technologically advanced, innovative and customer friendly financial

services organization in Sri Lanka, poised for further expansion in South Asia".

The birth of the bank occurred in 1920s, during the pre-independence era and currently

expanded its operations to Bangladesh as well. The bank has won several awards including

‘The Strongest Bank in Sri Lanka in 2016’award by the Asian Banker and “The Most

Respected Bank in Sri Lanka – 2016” by LMD rankings. With the commitment of the bank

current Chairman Mr. K. G. D. D. Dheerasinghe and his team, the bank is moving forward

being a successful Commercial Bank in Sri Lanka.

Products

Savings

o Regular Savings Account

o Super Saver Account

o RFC Savings Account

o Power Savings Account

o Udara Senior Citizens Account

o Arunalu Children’s Savings Account

o Isuru Minor’s Savings Account

o DotCom Youth Savings Account

Deposits and Investments

o Millionaire Account

o Money Market Accounts

o Treasury Bonds

o Treasury Bills

o Fixed Deposits

o Call Deposits

o RFC Fixed Deposits

Current Accounts

o Current Accounts

o Achiever Current Accounts

Loans

o Home Loans

o Foreign Currency Home Loans

o Personal Loans

Figure 1 Commercial Bank Logo

o Education Loans

o Professionals’ Loans

o Pensioners’ Loans

o Gold Loans

Cards

o Platinum Credit Cards

o Credit Cards

o Debit Cards

Services

o Online Banking

o Mobile Banking

Islamic Banking

Elite Banking

Achievements

Declared Best Private Sector Bank in Sri Lanka and best for CSR, Brand Excellence and

Sustainability in the Banking industry

The Commercial Bank of Ceylon won four top awards including Best Private Sector Bank in

Sri Lanka at the 2016 South Asian Partnership Summit & Business Awards presented by

World HRD Congress and endorsed by the Asian Confederation of Businesses.

Ranked amongst ‘500 Strongest Banks’ in Asia Pacific region by The Asian Banker

The Commercial Bank of Ceylon PLC has been adjudged ‘The Strongest Bank in Sri Lanka

in 2016’ following a detailed and transparent scorecard compiled and analyzed by The Asian

Banker, a leading provider of strategic intelligence on the financial services industry.

Wins Sector Award for Banking, leads all listed companies in total assets; placed second

overall on PAT

The Commercial Bank of Ceylon has topped the LMD 100 ranking of Sri Lanka’s leading

listed companies in terms of Assets, taken second place overall on Profit After Tax (PAT)

and fifth place overall on Turnover in the magazine’s just published rankings for 2014-15.

The Bank also won the Sector Award for Banking at the ceremony.

The Commercial Bank of Ceylon PLC has become the only Sri Lankan bank to be ranked

among the Top 1000 Banks of the World for the sixth year running, setting yet another

benchmark for consistency.

This prestigious ranking is published annually by ‘The Banker’ magazine of the UK, and the

2016 list is based on the Bank’s key performance indicators for FY 2015.

2

o Professionals’ Loans

o Pensioners’ Loans

o Gold Loans

Cards

o Platinum Credit Cards

o Credit Cards

o Debit Cards

Services

o Online Banking

o Mobile Banking

Islamic Banking

Elite Banking

Achievements

Declared Best Private Sector Bank in Sri Lanka and best for CSR, Brand Excellence and

Sustainability in the Banking industry

The Commercial Bank of Ceylon won four top awards including Best Private Sector Bank in

Sri Lanka at the 2016 South Asian Partnership Summit & Business Awards presented by

World HRD Congress and endorsed by the Asian Confederation of Businesses.

Ranked amongst ‘500 Strongest Banks’ in Asia Pacific region by The Asian Banker

The Commercial Bank of Ceylon PLC has been adjudged ‘The Strongest Bank in Sri Lanka

in 2016’ following a detailed and transparent scorecard compiled and analyzed by The Asian

Banker, a leading provider of strategic intelligence on the financial services industry.

Wins Sector Award for Banking, leads all listed companies in total assets; placed second

overall on PAT

The Commercial Bank of Ceylon has topped the LMD 100 ranking of Sri Lanka’s leading

listed companies in terms of Assets, taken second place overall on Profit After Tax (PAT)

and fifth place overall on Turnover in the magazine’s just published rankings for 2014-15.

The Bank also won the Sector Award for Banking at the ceremony.

The Commercial Bank of Ceylon PLC has become the only Sri Lankan bank to be ranked

among the Top 1000 Banks of the World for the sixth year running, setting yet another

benchmark for consistency.

This prestigious ranking is published annually by ‘The Banker’ magazine of the UK, and the

2016 list is based on the Bank’s key performance indicators for FY 2015.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Hatton National Bank PLC.

Hatton National Bank PLC is also an award winning private commercial bank in Sri Lanka

currently operating with 249 branches island wide. It has been internationally recognized as

the “Best Retail Bank in Sri Lanka” by Asian Banker Magazine many times as well as “The

Bank of the Year” in both 2012 and 2013 by The Banker Magazine of UK. It operates under

the vision of,

“To be the acknowledged leader and chosen partner in providing financial solutions through

inspired people.”

Its 1st branches were opened at Pussellawa, Gampola and Maskeliya and the Recently opened

HNB bank in Jaffna became the 1st green building of Northern Region.

HNB was able to achieve an international credit rating by becoming the first Sri Lankan bank

to obtain an international credit rating while maintaining a national long-term rating by Fitch

Ratings (Lanka) Ltd as AA-.

Produts

Savings

o General Savings

Regular Savings

Capital Savings

HNV Adhishtana

o Minor Savings

Singithi Kirikatiyo

Singithi Lama

Singithi Surakum

Diri Daru

o Youth Savings

HNB Teen

HNB Yauwanabhimana

HNB You

o Senior Citizens

Senior Citizens Scheme

Sathkara for Gov. Servants

o Term Deposits

Fixed Deposits

Call Deposits

o Foreign Currency Savings

3

Figure 2 HNB Logo

Hatton National Bank PLC is also an award winning private commercial bank in Sri Lanka

currently operating with 249 branches island wide. It has been internationally recognized as

the “Best Retail Bank in Sri Lanka” by Asian Banker Magazine many times as well as “The

Bank of the Year” in both 2012 and 2013 by The Banker Magazine of UK. It operates under

the vision of,

“To be the acknowledged leader and chosen partner in providing financial solutions through

inspired people.”

Its 1st branches were opened at Pussellawa, Gampola and Maskeliya and the Recently opened

HNB bank in Jaffna became the 1st green building of Northern Region.

HNB was able to achieve an international credit rating by becoming the first Sri Lankan bank

to obtain an international credit rating while maintaining a national long-term rating by Fitch

Ratings (Lanka) Ltd as AA-.

Produts

Savings

o General Savings

Regular Savings

Capital Savings

HNV Adhishtana

o Minor Savings

Singithi Kirikatiyo

Singithi Lama

Singithi Surakum

Diri Daru

o Youth Savings

HNB Teen

HNB Yauwanabhimana

HNB You

o Senior Citizens

Senior Citizens Scheme

Sathkara for Gov. Servants

o Term Deposits

Fixed Deposits

Call Deposits

o Foreign Currency Savings

3

Figure 2 HNB Logo

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Loans

o Vehicle Loans

o Personal Loans

o Shanthi Home Loans

o Educational Loans

o Sathkara for Gov. Servants

o Debt Consolidation Loans

Cards

o International Debit Cards

o HNB Credit Cards

o HNB Travel Cards

o HNB Affinity Cards

Remittance

Current Accounts

o Privilege Current Account

o Shareline Current Account

o Current Account

Promotions

o General Promotions

o Card Promotions

o Shanthi Loyalty Card Discounts

Leasings

Achievements

'The Best Retail Bank' for the 8th time by the 'Asian Banker'

HNB was once again recognized as 'The Best Retail Bank', in Sri Lanka at the 'Asia at the

'Asian Banker' International Excellence in Retail Financial Services 2016 Awards ceremony

held in Hong Kong recently. This is the 8th time that HNB has been bestowed with the 'Best

Retail Bank Award' by the 'Asian Banker'.

The 'Best Retail Bank in Sri Lanka'

HNB was once again recognized as the 'Best Retail Bank in Sri Lanka' for the seventh time

by the prestigious ‘The Asian Banker’ at the Asian Banker Excellence in Retail Financial

Services Awards ceremony held recently in Singapore.

The International Excellence in Retail Financial Services programme is the most rigorous,

prestigious and transparent awards programme for retail banking in Asia Pacific, Central

Asia, the Middle East and Africa. The programme evaluates over 250 banks in 42 countries

in a thorough evaluation process.

HNB MOMO wins international award for Marketing Campaign of the Year

4

o Vehicle Loans

o Personal Loans

o Shanthi Home Loans

o Educational Loans

o Sathkara for Gov. Servants

o Debt Consolidation Loans

Cards

o International Debit Cards

o HNB Credit Cards

o HNB Travel Cards

o HNB Affinity Cards

Remittance

Current Accounts

o Privilege Current Account

o Shareline Current Account

o Current Account

Promotions

o General Promotions

o Card Promotions

o Shanthi Loyalty Card Discounts

Leasings

Achievements

'The Best Retail Bank' for the 8th time by the 'Asian Banker'

HNB was once again recognized as 'The Best Retail Bank', in Sri Lanka at the 'Asia at the

'Asian Banker' International Excellence in Retail Financial Services 2016 Awards ceremony

held in Hong Kong recently. This is the 8th time that HNB has been bestowed with the 'Best

Retail Bank Award' by the 'Asian Banker'.

The 'Best Retail Bank in Sri Lanka'

HNB was once again recognized as the 'Best Retail Bank in Sri Lanka' for the seventh time

by the prestigious ‘The Asian Banker’ at the Asian Banker Excellence in Retail Financial

Services Awards ceremony held recently in Singapore.

The International Excellence in Retail Financial Services programme is the most rigorous,

prestigious and transparent awards programme for retail banking in Asia Pacific, Central

Asia, the Middle East and Africa. The programme evaluates over 250 banks in 42 countries

in a thorough evaluation process.

HNB MOMO wins international award for Marketing Campaign of the Year

4

HNB won the 'Marketing Campaign of The Year' category award for the marketing and

communications campaign developed for HNB MOMO the mobile POS solution introduced

by the bank for the first time in Sri Lanka in 2013.

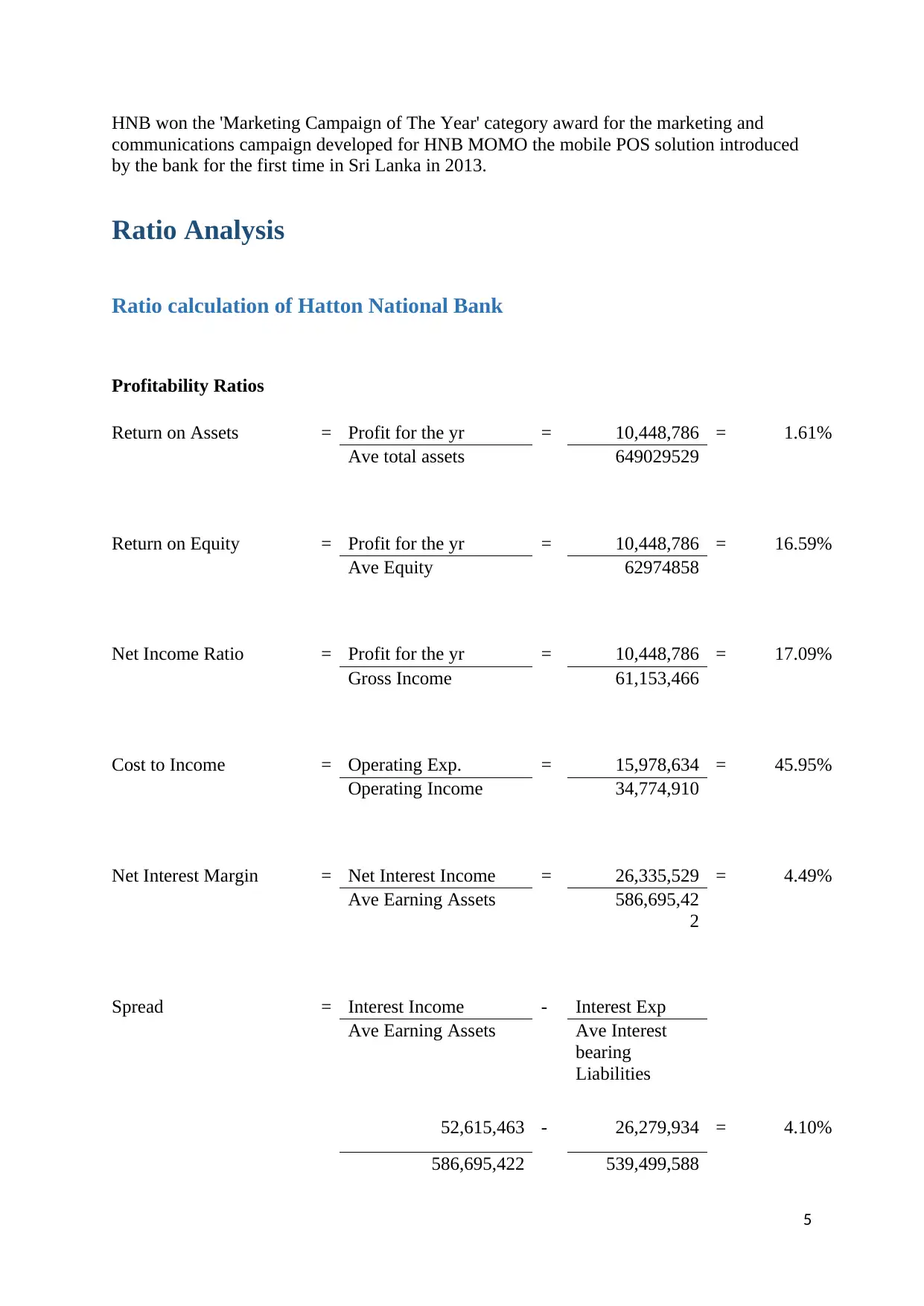

Ratio Analysis

Ratio calculation of Hatton National Bank

Profitability Ratios

Return on Assets = Profit for the yr = 10,448,786 = 1.61%

Ave total assets 649029529

Return on Equity = Profit for the yr = 10,448,786 = 16.59%

Ave Equity 62974858

Net Income Ratio = Profit for the yr = 10,448,786 = 17.09%

Gross Income 61,153,466

Cost to Income = Operating Exp. = 15,978,634 = 45.95%

Operating Income 34,774,910

Net Interest Margin = Net Interest Income = 26,335,529 = 4.49%

Ave Earning Assets 586,695,42

2

Spread = Interest Income - Interest Exp

Ave Earning Assets Ave Interest

bearing

Liabilities

52,615,463 - 26,279,934 = 4.10%

586,695,422 539,499,588

5

communications campaign developed for HNB MOMO the mobile POS solution introduced

by the bank for the first time in Sri Lanka in 2013.

Ratio Analysis

Ratio calculation of Hatton National Bank

Profitability Ratios

Return on Assets = Profit for the yr = 10,448,786 = 1.61%

Ave total assets 649029529

Return on Equity = Profit for the yr = 10,448,786 = 16.59%

Ave Equity 62974858

Net Income Ratio = Profit for the yr = 10,448,786 = 17.09%

Gross Income 61,153,466

Cost to Income = Operating Exp. = 15,978,634 = 45.95%

Operating Income 34,774,910

Net Interest Margin = Net Interest Income = 26,335,529 = 4.49%

Ave Earning Assets 586,695,42

2

Spread = Interest Income - Interest Exp

Ave Earning Assets Ave Interest

bearing

Liabilities

52,615,463 - 26,279,934 = 4.10%

586,695,422 539,499,588

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 66

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.