Financial Accounting: Statements, Depreciation, and Cash Flows

VerifiedAdded on 2022/12/30

|9

|764

|98

Homework Assignment

AI Summary

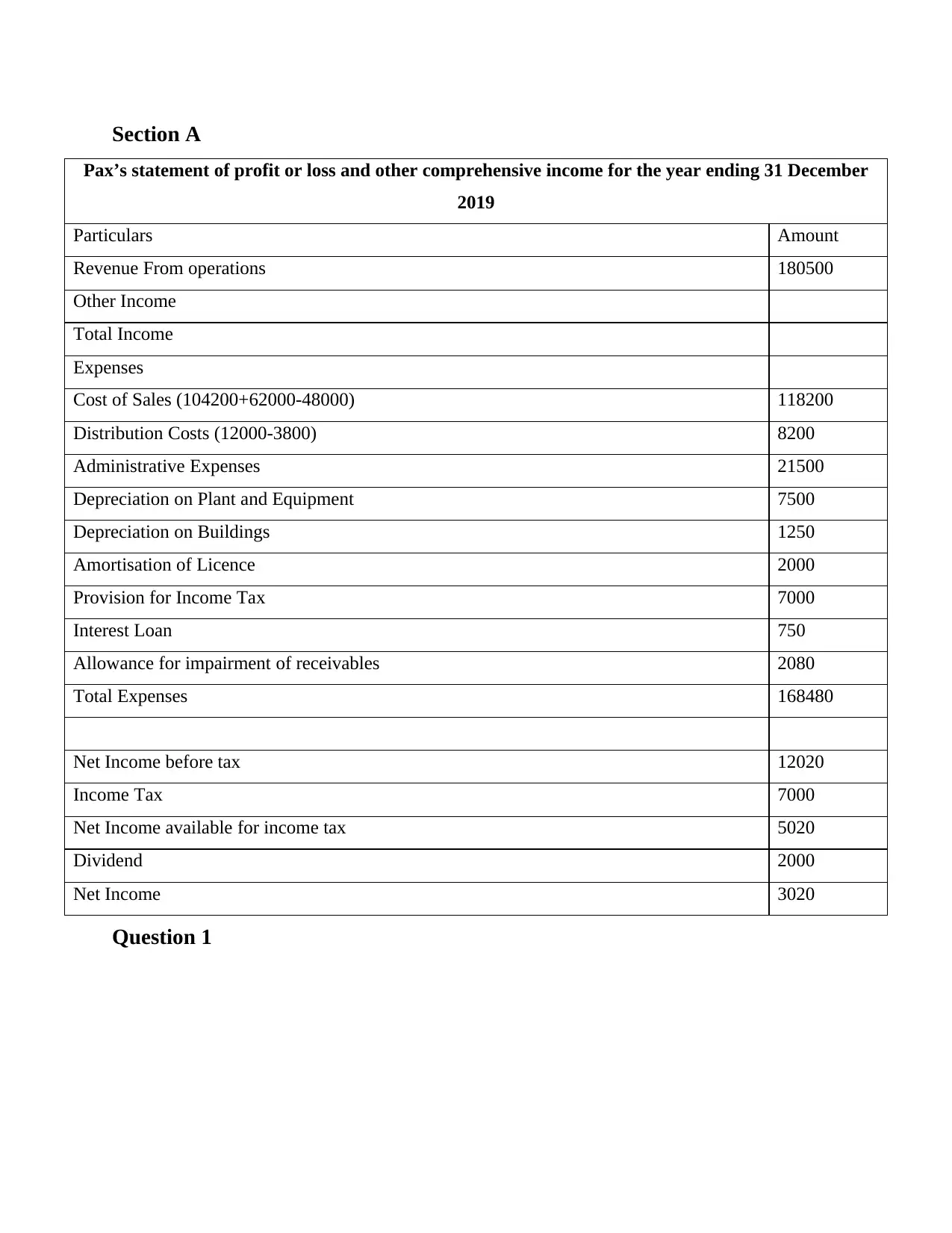

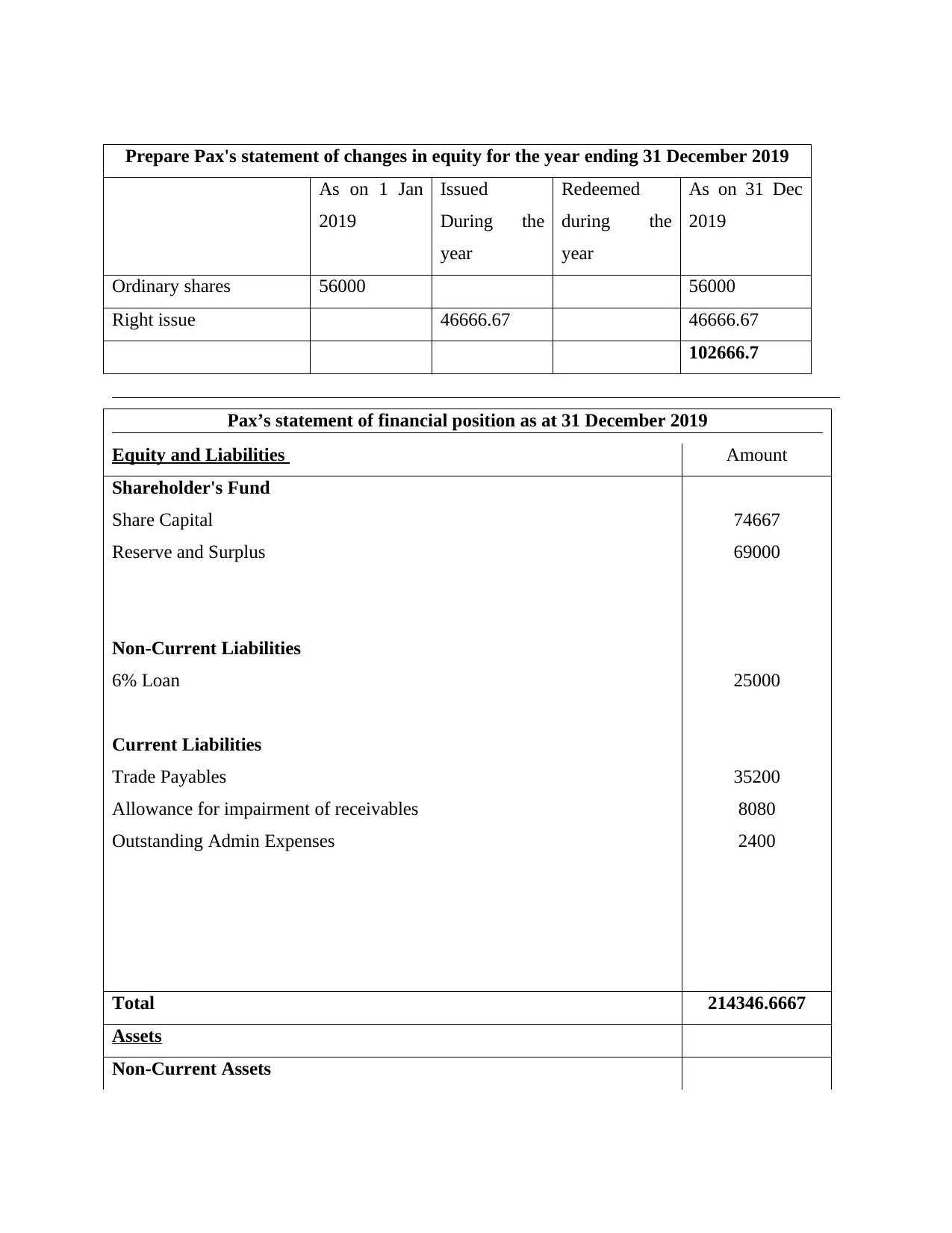

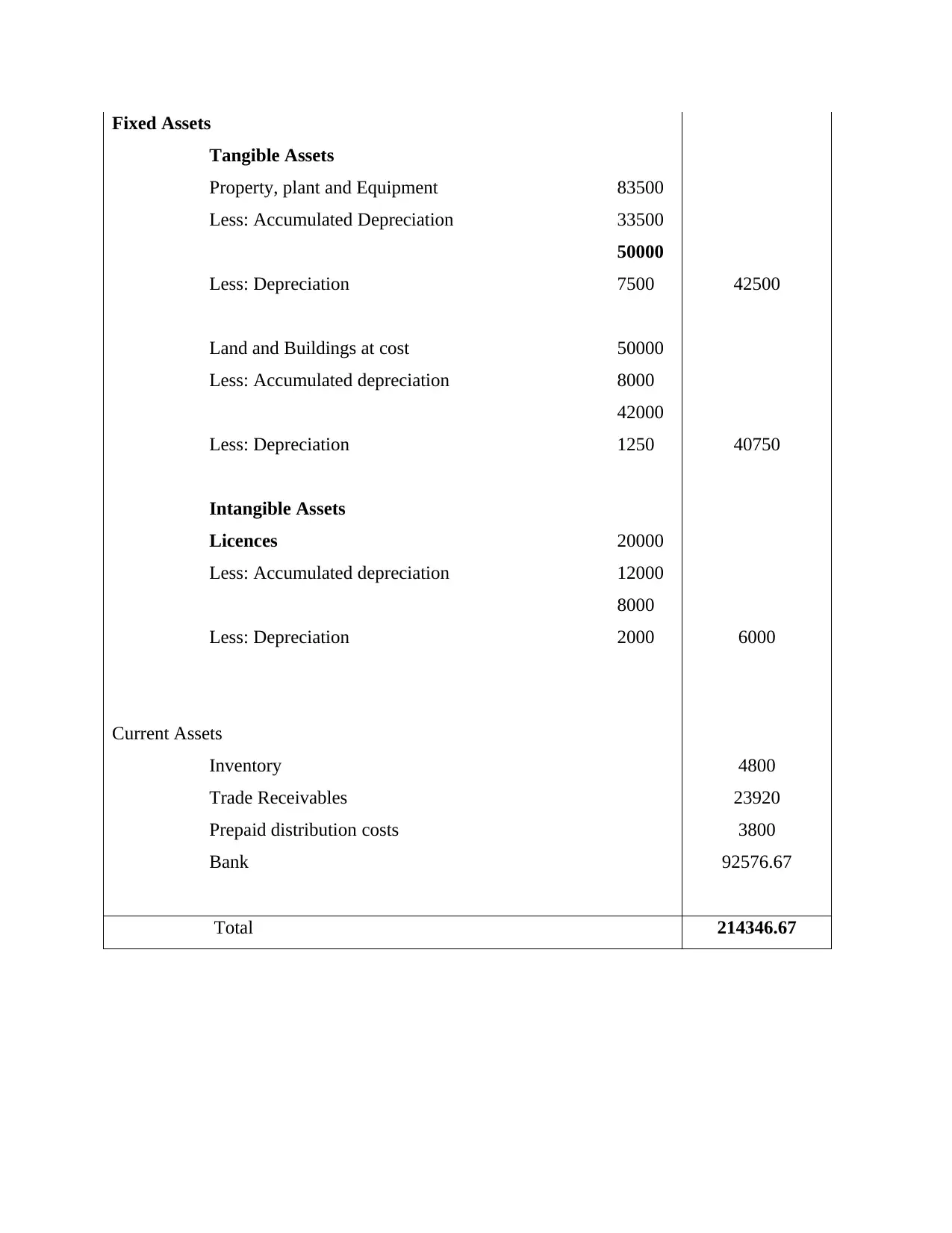

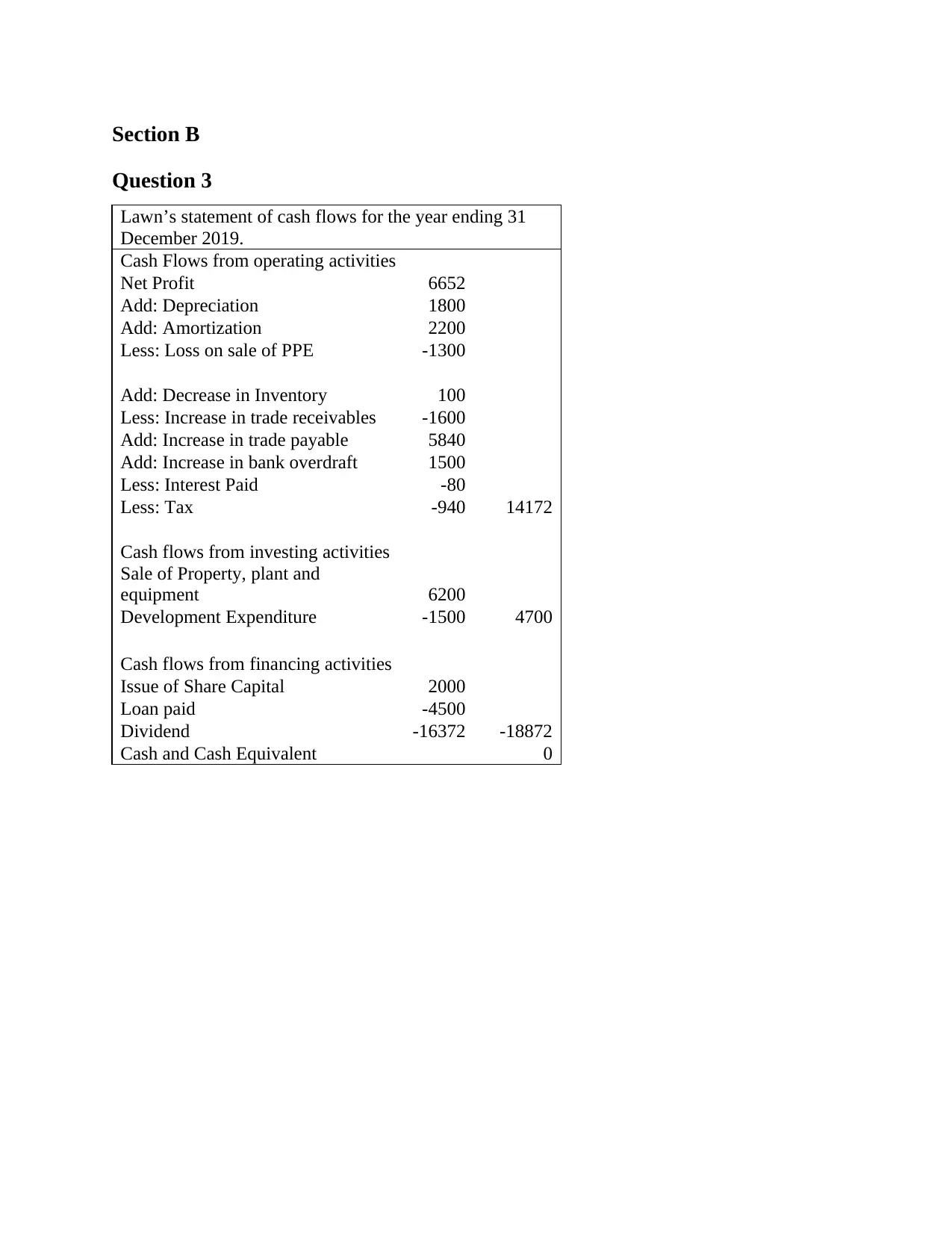

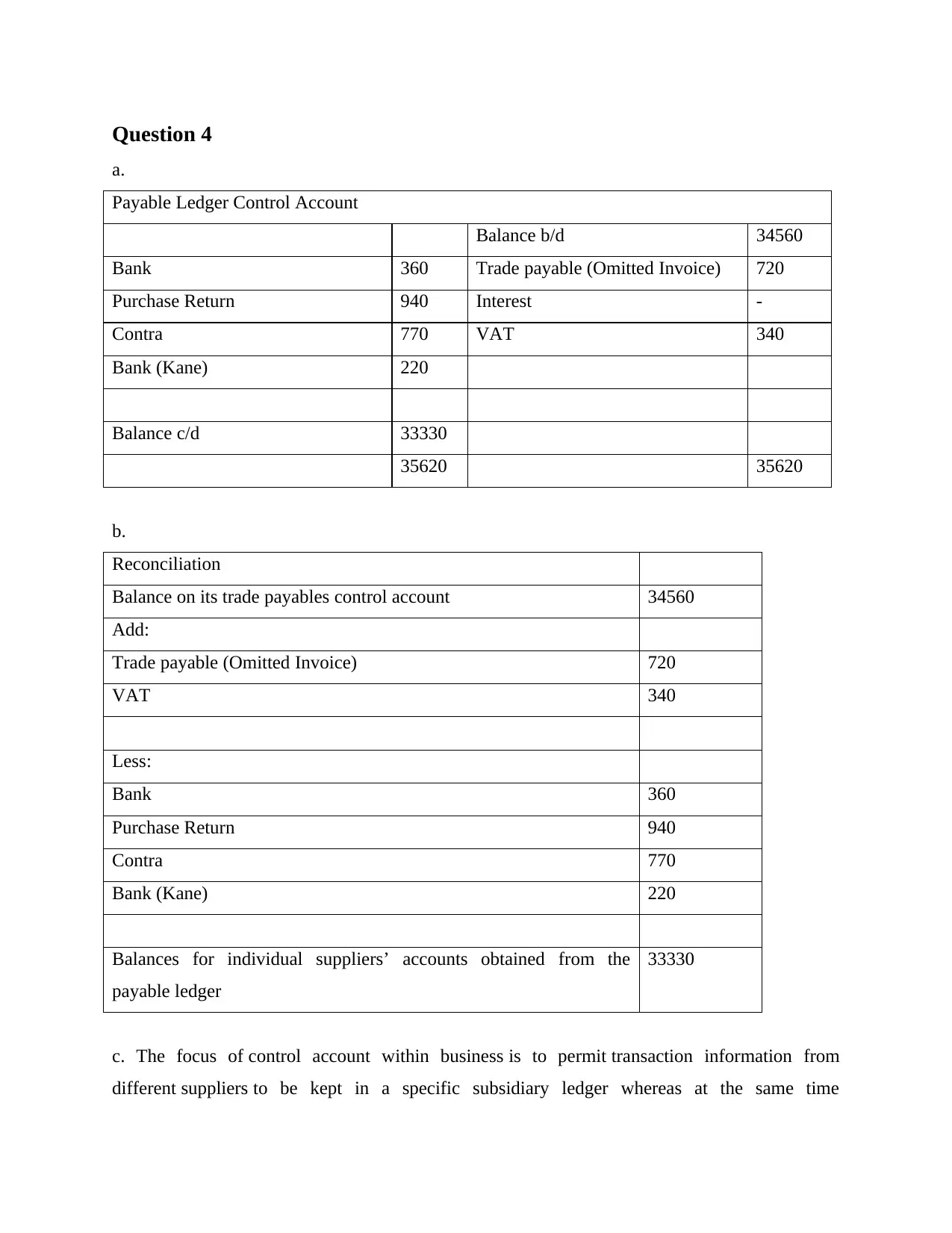

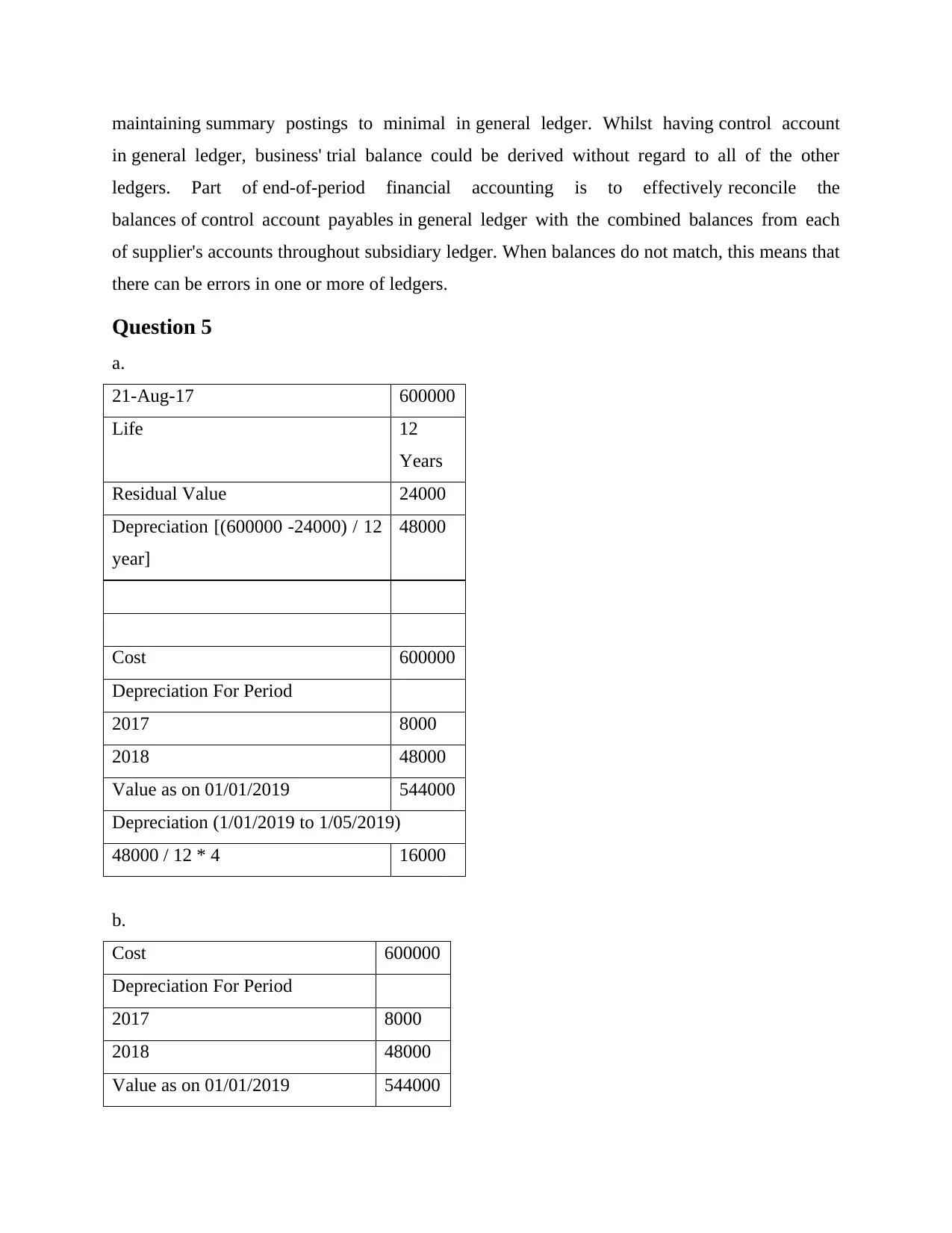

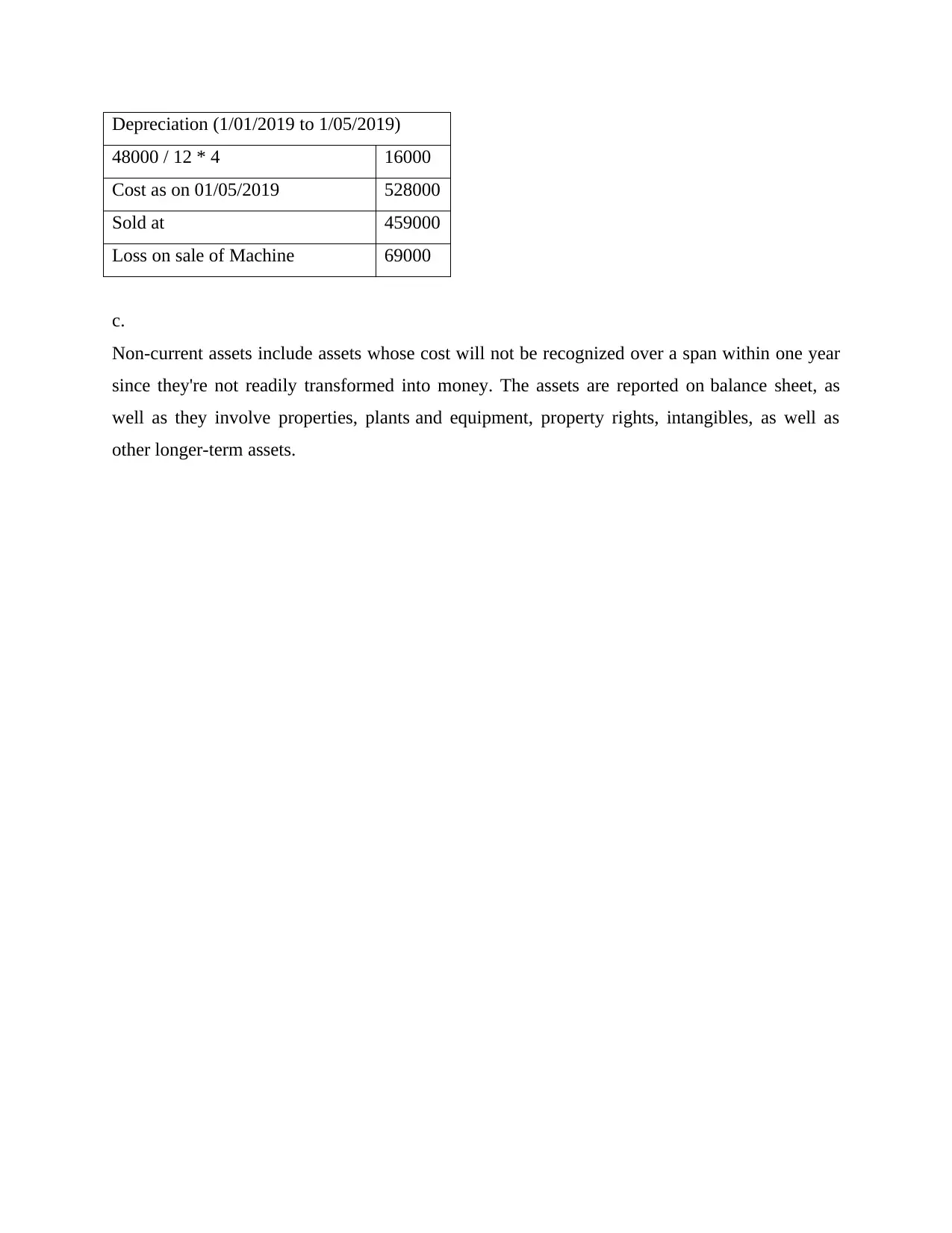

This financial accounting assignment provides a comprehensive solution to various accounting problems. The assignment includes the preparation of Pax's statement of profit or loss and other comprehensive income, statement of changes in equity, and statement of financial position. It also features Lawn's statement of cash flows. The solution includes the completion of a payable ledger control account and reconciliation, along with detailed calculations for depreciation using the straight-line method. The assignment covers key financial accounting concepts, including financial statement preparation, cash flow analysis, depreciation methods, and control account reconciliation, providing a complete and detailed guide for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.